Finance: Corporate Governance Models & Investment Decision Techniques

VerifiedAdded on 2023/06/18

|17

|4353

|459

Report

AI Summary

This finance report provides a comprehensive overview of key finance concepts and their practical applications. It begins by discussing the "Comply or Explain" model of corporate governance, highlighting its benefits and limitations, and explains the characteristics of financial statement filing for UK Plcs, emphasizing the importance of qualitative characteristics and adherence to IFRS standards. The report then delves into investment appraisal techniques, calculating the payback period and accounting rate of return (ARR) for two investment proposals, critically evaluating the payback technique, and explaining the advantages and disadvantages of the internal rate of return (IRR). Furthermore, it explores the concept of contribution and its importance to cost-volume-profit (CVP) analysis, describes CVP usage in 'dropping a product or service' and 'special contract' decisions, and outlines the limitations of the CVP technique. Finally, the report addresses financial planning, including preparing an opening statement, monthly cash flow forecast, and additional expenses businesses should consider when seeking financial assistance. This report is designed to provide a thorough understanding of these finance topics.

Introduction to Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

a) Discussing “Comply or Explain” model of corporate governance.........................................3

b) Explaining characteristics of approach that is used for filing financial statements................4

QUESTION 2...................................................................................................................................5

a) Calculating Payback period....................................................................................................5

b) Calculating Accounting rate of return for both proposals......................................................7

c) Critically evaluating Payback technique.................................................................................8

d) Explaining characteristics of investment decision techniques with advantages &

disadvantages of IRR..................................................................................................................9

QUESTION 3.................................................................................................................................10

a) explaining the concept of contribution and its importance to CVP technique....................10

b) Explaining CVP usage in dropping a product or service special contract decision..........11

c) Describing CVP & its related limitation in context of both economies model and other

interpretation.............................................................................................................................11

QUESTION 4.................................................................................................................................12

a)................................................................................................................................................12

b)...............................................................................................................................................13

c) Explaining additional expenses business should take into account as result of needing

financial assistance...................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

a) Discussing “Comply or Explain” model of corporate governance.........................................3

b) Explaining characteristics of approach that is used for filing financial statements................4

QUESTION 2...................................................................................................................................5

a) Calculating Payback period....................................................................................................5

b) Calculating Accounting rate of return for both proposals......................................................7

c) Critically evaluating Payback technique.................................................................................8

d) Explaining characteristics of investment decision techniques with advantages &

disadvantages of IRR..................................................................................................................9

QUESTION 3.................................................................................................................................10

a) explaining the concept of contribution and its importance to CVP technique....................10

b) Explaining CVP usage in dropping a product or service special contract decision..........11

c) Describing CVP & its related limitation in context of both economies model and other

interpretation.............................................................................................................................11

QUESTION 4.................................................................................................................................12

a)................................................................................................................................................12

b)...............................................................................................................................................13

c) Explaining additional expenses business should take into account as result of needing

financial assistance...................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Finance is a system which requires transfer of funds between borrowers and lenders or

investors. It depicts managing money and identifying sources from where it can be acquired at

least cost. The present report will discuss the “Comply or Explain” model of corporate

governance and will explain the characteristics of approach used to file final accounts to major

authorities. Further, report will calculate the payback period and ARR of two investment

proposals of Edinburgh & Newcastle.

It will also highlight advantages and disadvantages of IRR. In addition to this, study will

outline concept of contribution and its importance and will describe nature of 'dropping a product

or service’ and ‘special contract’ decisions. Study will also shed light on limitations of CVP

technique. Lastly, report will prepare opening statement, monthly cash flow forecast.

QUESTION 1

a) Discussing “Comply or Explain” model of corporate governance

Comply or Explain is a mechanism which is generally used in UK as a prominent part of

corporate governance. It means that all the corporate bodies should comply with rules and

regulations laid down by Corporate governance or should explain the reasons why they are not

complying with it (Ho, 2017). Main reason behind this approach is to let the market or industry

decide that whether a set standard of rules and regulations are fit & appropriate for companies or

not. This principle provides full flexibility to companies to make a decision of either complying

with Code or not and state reason for not complying. It is beneficial because it asks for

transparency in company transactions and business, and in case of breach of any principles,

sufficient explanations can be given (Comply or Explain (UK) – Definition, 2021). Company

can benefit from Code at the times of introducing new initiatives and changes by preventing box-

ticking.

The principle also shows recognition and justification, that is, there are several other

alternatives for achieving good governance outside code. There are many companies in UK

having good governance without any intervention of government body. However, on critical

note, sometimes investors state that explanations given by company at the times of non-

compliance with code are not adequate and businesses fail to explain the good governance

Finance is a system which requires transfer of funds between borrowers and lenders or

investors. It depicts managing money and identifying sources from where it can be acquired at

least cost. The present report will discuss the “Comply or Explain” model of corporate

governance and will explain the characteristics of approach used to file final accounts to major

authorities. Further, report will calculate the payback period and ARR of two investment

proposals of Edinburgh & Newcastle.

It will also highlight advantages and disadvantages of IRR. In addition to this, study will

outline concept of contribution and its importance and will describe nature of 'dropping a product

or service’ and ‘special contract’ decisions. Study will also shed light on limitations of CVP

technique. Lastly, report will prepare opening statement, monthly cash flow forecast.

QUESTION 1

a) Discussing “Comply or Explain” model of corporate governance

Comply or Explain is a mechanism which is generally used in UK as a prominent part of

corporate governance. It means that all the corporate bodies should comply with rules and

regulations laid down by Corporate governance or should explain the reasons why they are not

complying with it (Ho, 2017). Main reason behind this approach is to let the market or industry

decide that whether a set standard of rules and regulations are fit & appropriate for companies or

not. This principle provides full flexibility to companies to make a decision of either complying

with Code or not and state reason for not complying. It is beneficial because it asks for

transparency in company transactions and business, and in case of breach of any principles,

sufficient explanations can be given (Comply or Explain (UK) – Definition, 2021). Company

can benefit from Code at the times of introducing new initiatives and changes by preventing box-

ticking.

The principle also shows recognition and justification, that is, there are several other

alternatives for achieving good governance outside code. There are many companies in UK

having good governance without any intervention of government body. However, on critical

note, sometimes investors state that explanations given by company at the times of non-

compliance with code are not adequate and businesses fail to explain the good governance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

alternatives (Roberts and et.al., 2020). In addition to this, organizations not complying with the

Code have bad reputation and impression in market.

Mutual trust with investors and shareholders must be build by company which is possible

when companies maintain good governance. A solid foundation is build by having trust and

commitment with investor which is done by complying with laws laid by government.

b) Explaining characteristics of approach that is used for filing financial statements

There are various characteristics that need to be applied by organization in order to filing

financial statement by Plc’s operating in UK. Companies listed in UK require to pay attention

two financial reporting framework so that preparation of financial statement according to

legislation, regulations, etc can be exerted. There are qualitative characteristic which are require

to be used by formulating financial statement that includes understand ability, relevance,

reliability,comparability, timeliness, etc that allow to accomplish objective of filing can become

possible (Xiuli, 201). International accounting standard requires the firm to largely concentrate

on highlighting crucial characteristics that can make particular statement reliable and materialist

in turn greater accuracy & fairness in functional practices of business can be maintained.

To accomplish the objective of providing all relevant, reliable, etc to give full

disclosure by considering all past, present and future events so that assistance to stakeholders in

taking strategic decision can become possible. There are various approaches which need to be

specified for having ability to file the financial statement within house and London Stock

Exchange. It involves the qualitative features that are required to be maintained in respect to

avoid any legal obligation on company. It is essential for the firm to largely concentrating on

giving different aspects like full disclosing, reliability, simplicity, relevancy,comparability,

understand ability,completeness, accuracy, promptness, reliability, analytical, qualities,

qualities, etc so that significant information while creating financial reports can be provided.

There are various requirements that are need to attained by companies for being eligible for

trading on stock exchange (Subair and et.al., 2020). Investors usually make their decision of

trading by paying attention on gathering information from financial statements of the company.

For this purpose, firms are obligated to utilize qualitative characteristics in turn eligibility to

trade on stock exchange can be derived. As per the UK GAAP,IFRS standard, etc prevailing in

UK require its company to highlight these characteristics in its financial statement so that

greater sustainability and efficiency of processing can be derived. The main approach for

Code have bad reputation and impression in market.

Mutual trust with investors and shareholders must be build by company which is possible

when companies maintain good governance. A solid foundation is build by having trust and

commitment with investor which is done by complying with laws laid by government.

b) Explaining characteristics of approach that is used for filing financial statements

There are various characteristics that need to be applied by organization in order to filing

financial statement by Plc’s operating in UK. Companies listed in UK require to pay attention

two financial reporting framework so that preparation of financial statement according to

legislation, regulations, etc can be exerted. There are qualitative characteristic which are require

to be used by formulating financial statement that includes understand ability, relevance,

reliability,comparability, timeliness, etc that allow to accomplish objective of filing can become

possible (Xiuli, 201). International accounting standard requires the firm to largely concentrate

on highlighting crucial characteristics that can make particular statement reliable and materialist

in turn greater accuracy & fairness in functional practices of business can be maintained.

To accomplish the objective of providing all relevant, reliable, etc to give full

disclosure by considering all past, present and future events so that assistance to stakeholders in

taking strategic decision can become possible. There are various approaches which need to be

specified for having ability to file the financial statement within house and London Stock

Exchange. It involves the qualitative features that are required to be maintained in respect to

avoid any legal obligation on company. It is essential for the firm to largely concentrating on

giving different aspects like full disclosing, reliability, simplicity, relevancy,comparability,

understand ability,completeness, accuracy, promptness, reliability, analytical, qualities,

qualities, etc so that significant information while creating financial reports can be provided.

There are various requirements that are need to attained by companies for being eligible for

trading on stock exchange (Subair and et.al., 2020). Investors usually make their decision of

trading by paying attention on gathering information from financial statements of the company.

For this purpose, firms are obligated to utilize qualitative characteristics in turn eligibility to

trade on stock exchange can be derived. As per the UK GAAP,IFRS standard, etc prevailing in

UK require its company to highlight these characteristics in its financial statement so that

greater sustainability and efficiency of processing can be derived. The main approach for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

utilization of these characteristics is to safe guard interest of financial statement users so that

higher trustworthiness can be provided. For this purpose, companies in UK adopts IFRS

standards in order to consolidated financial statement in turn ability to function smoothly

and effectively can be obtained. To coordinate with corporate governance, all scale of

organization pay attention on developing such mentioned approaches in turn highers

sustainability and growth can be derived. On the basis of this, it can be interpreted that

approaches using qualitative characteristics, IFRS, accounting , etc concept can help in meeting

criteria for smooth functioning.

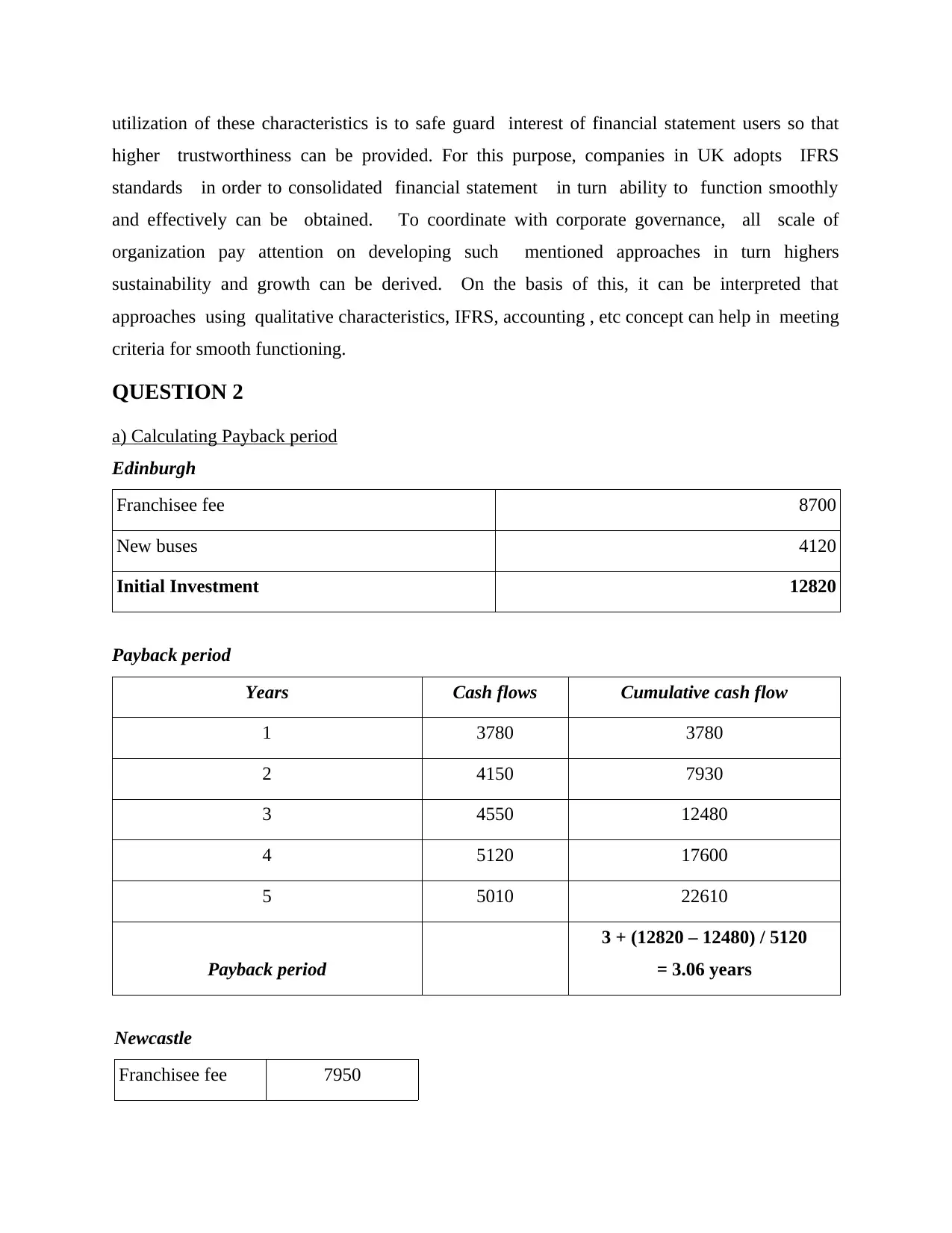

QUESTION 2

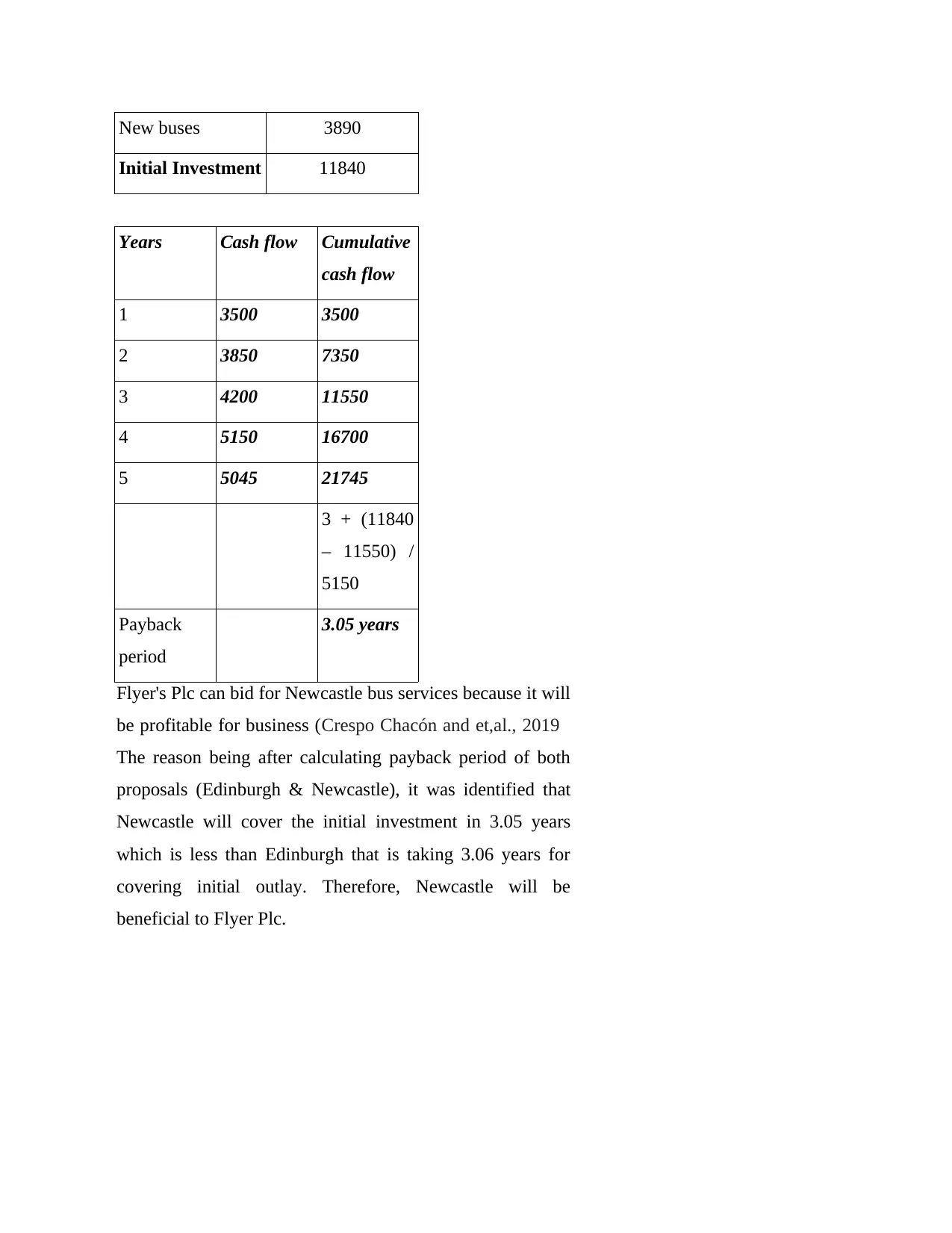

a) Calculating Payback period

Edinburgh

Franchisee fee 8700

New buses 4120

Initial Investment 12820

Payback period

Years Cash flows Cumulative cash flow

1 3780 3780

2 4150 7930

3 4550 12480

4 5120 17600

5 5010 22610

Payback period

3 + (12820 – 12480) / 5120

= 3.06 years

Newcastle

Franchisee fee 7950

higher trustworthiness can be provided. For this purpose, companies in UK adopts IFRS

standards in order to consolidated financial statement in turn ability to function smoothly

and effectively can be obtained. To coordinate with corporate governance, all scale of

organization pay attention on developing such mentioned approaches in turn highers

sustainability and growth can be derived. On the basis of this, it can be interpreted that

approaches using qualitative characteristics, IFRS, accounting , etc concept can help in meeting

criteria for smooth functioning.

QUESTION 2

a) Calculating Payback period

Edinburgh

Franchisee fee 8700

New buses 4120

Initial Investment 12820

Payback period

Years Cash flows Cumulative cash flow

1 3780 3780

2 4150 7930

3 4550 12480

4 5120 17600

5 5010 22610

Payback period

3 + (12820 – 12480) / 5120

= 3.06 years

Newcastle

Franchisee fee 7950

New buses 3890

Initial Investment 11840

Years Cash flow Cumulative

cash flow

1 3500 3500

2 3850 7350

3 4200 11550

4 5150 16700

5 5045 21745

3 + (11840

– 11550) /

5150

Payback

period

3.05 years

Flyer's Plc can bid for Newcastle bus services because it will

be profitable for business (Crespo Chacón and et,al., 2019

The reason being after calculating payback period of both

proposals (Edinburgh & Newcastle), it was identified that

Newcastle will cover the initial investment in 3.05 years

which is less than Edinburgh that is taking 3.06 years for

covering initial outlay. Therefore, Newcastle will be

beneficial to Flyer Plc.

Initial Investment 11840

Years Cash flow Cumulative

cash flow

1 3500 3500

2 3850 7350

3 4200 11550

4 5150 16700

5 5045 21745

3 + (11840

– 11550) /

5150

Payback

period

3.05 years

Flyer's Plc can bid for Newcastle bus services because it will

be profitable for business (Crespo Chacón and et,al., 2019

The reason being after calculating payback period of both

proposals (Edinburgh & Newcastle), it was identified that

Newcastle will cover the initial investment in 3.05 years

which is less than Edinburgh that is taking 3.06 years for

covering initial outlay. Therefore, Newcastle will be

beneficial to Flyer Plc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

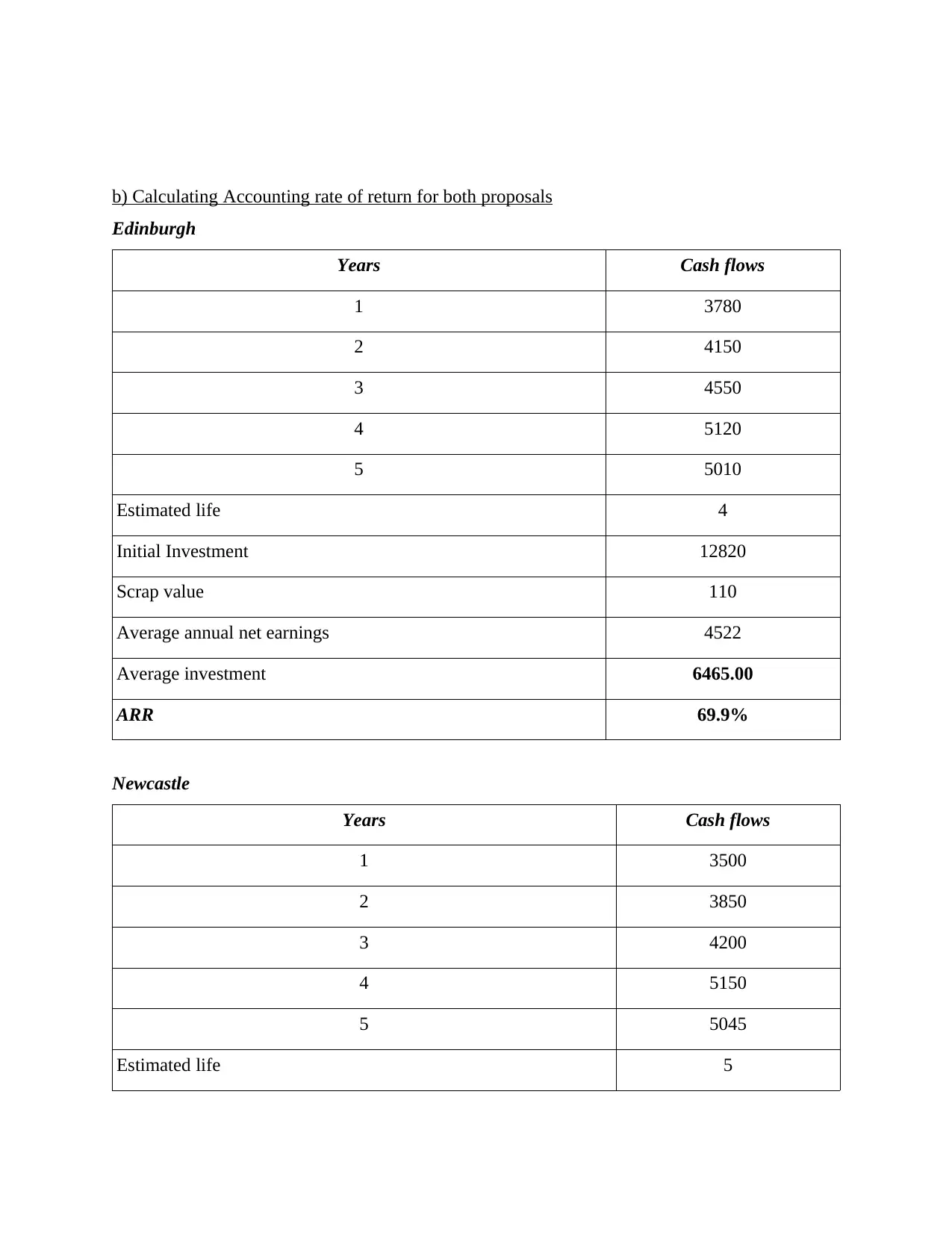

b) Calculating Accounting rate of return for both proposals

Edinburgh

Years Cash flows

1 3780

2 4150

3 4550

4 5120

5 5010

Estimated life 4

Initial Investment 12820

Scrap value 110

Average annual net earnings 4522

Average investment 6465.00

ARR 69.9%

Newcastle

Years Cash flows

1 3500

2 3850

3 4200

4 5150

5 5045

Estimated life 5

Edinburgh

Years Cash flows

1 3780

2 4150

3 4550

4 5120

5 5010

Estimated life 4

Initial Investment 12820

Scrap value 110

Average annual net earnings 4522

Average investment 6465.00

ARR 69.9%

Newcastle

Years Cash flows

1 3500

2 3850

3 4200

4 5150

5 5045

Estimated life 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

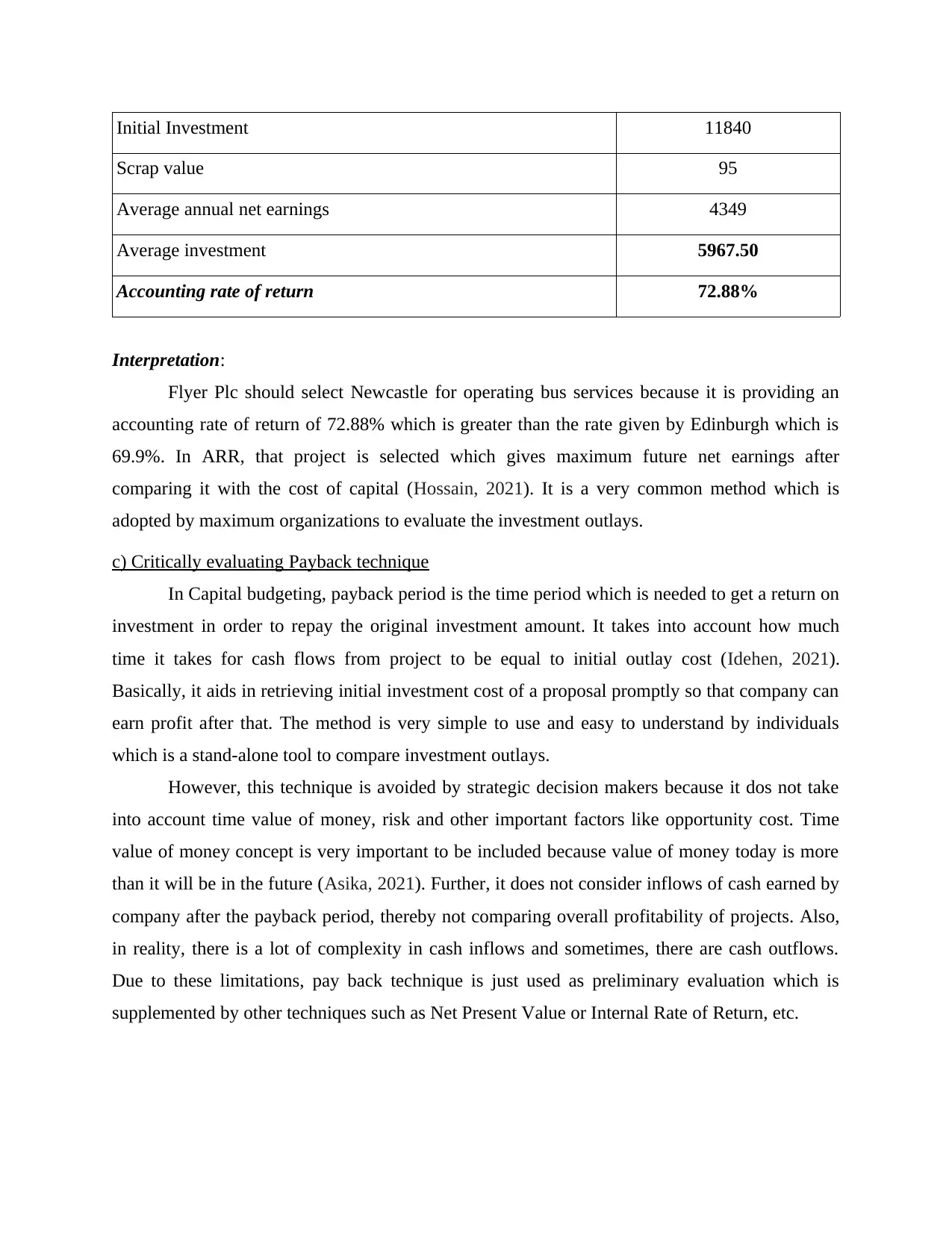

Initial Investment 11840

Scrap value 95

Average annual net earnings 4349

Average investment 5967.50

Accounting rate of return 72.88%

Interpretation:

Flyer Plc should select Newcastle for operating bus services because it is providing an

accounting rate of return of 72.88% which is greater than the rate given by Edinburgh which is

69.9%. In ARR, that project is selected which gives maximum future net earnings after

comparing it with the cost of capital (Hossain, 2021). It is a very common method which is

adopted by maximum organizations to evaluate the investment outlays.

c) Critically evaluating Payback technique

In Capital budgeting, payback period is the time period which is needed to get a return on

investment in order to repay the original investment amount. It takes into account how much

time it takes for cash flows from project to be equal to initial outlay cost (Idehen, 2021).

Basically, it aids in retrieving initial investment cost of a proposal promptly so that company can

earn profit after that. The method is very simple to use and easy to understand by individuals

which is a stand-alone tool to compare investment outlays.

However, this technique is avoided by strategic decision makers because it dos not take

into account time value of money, risk and other important factors like opportunity cost. Time

value of money concept is very important to be included because value of money today is more

than it will be in the future (Asika, 2021). Further, it does not consider inflows of cash earned by

company after the payback period, thereby not comparing overall profitability of projects. Also,

in reality, there is a lot of complexity in cash inflows and sometimes, there are cash outflows.

Due to these limitations, pay back technique is just used as preliminary evaluation which is

supplemented by other techniques such as Net Present Value or Internal Rate of Return, etc.

Scrap value 95

Average annual net earnings 4349

Average investment 5967.50

Accounting rate of return 72.88%

Interpretation:

Flyer Plc should select Newcastle for operating bus services because it is providing an

accounting rate of return of 72.88% which is greater than the rate given by Edinburgh which is

69.9%. In ARR, that project is selected which gives maximum future net earnings after

comparing it with the cost of capital (Hossain, 2021). It is a very common method which is

adopted by maximum organizations to evaluate the investment outlays.

c) Critically evaluating Payback technique

In Capital budgeting, payback period is the time period which is needed to get a return on

investment in order to repay the original investment amount. It takes into account how much

time it takes for cash flows from project to be equal to initial outlay cost (Idehen, 2021).

Basically, it aids in retrieving initial investment cost of a proposal promptly so that company can

earn profit after that. The method is very simple to use and easy to understand by individuals

which is a stand-alone tool to compare investment outlays.

However, this technique is avoided by strategic decision makers because it dos not take

into account time value of money, risk and other important factors like opportunity cost. Time

value of money concept is very important to be included because value of money today is more

than it will be in the future (Asika, 2021). Further, it does not consider inflows of cash earned by

company after the payback period, thereby not comparing overall profitability of projects. Also,

in reality, there is a lot of complexity in cash inflows and sometimes, there are cash outflows.

Due to these limitations, pay back technique is just used as preliminary evaluation which is

supplemented by other techniques such as Net Present Value or Internal Rate of Return, etc.

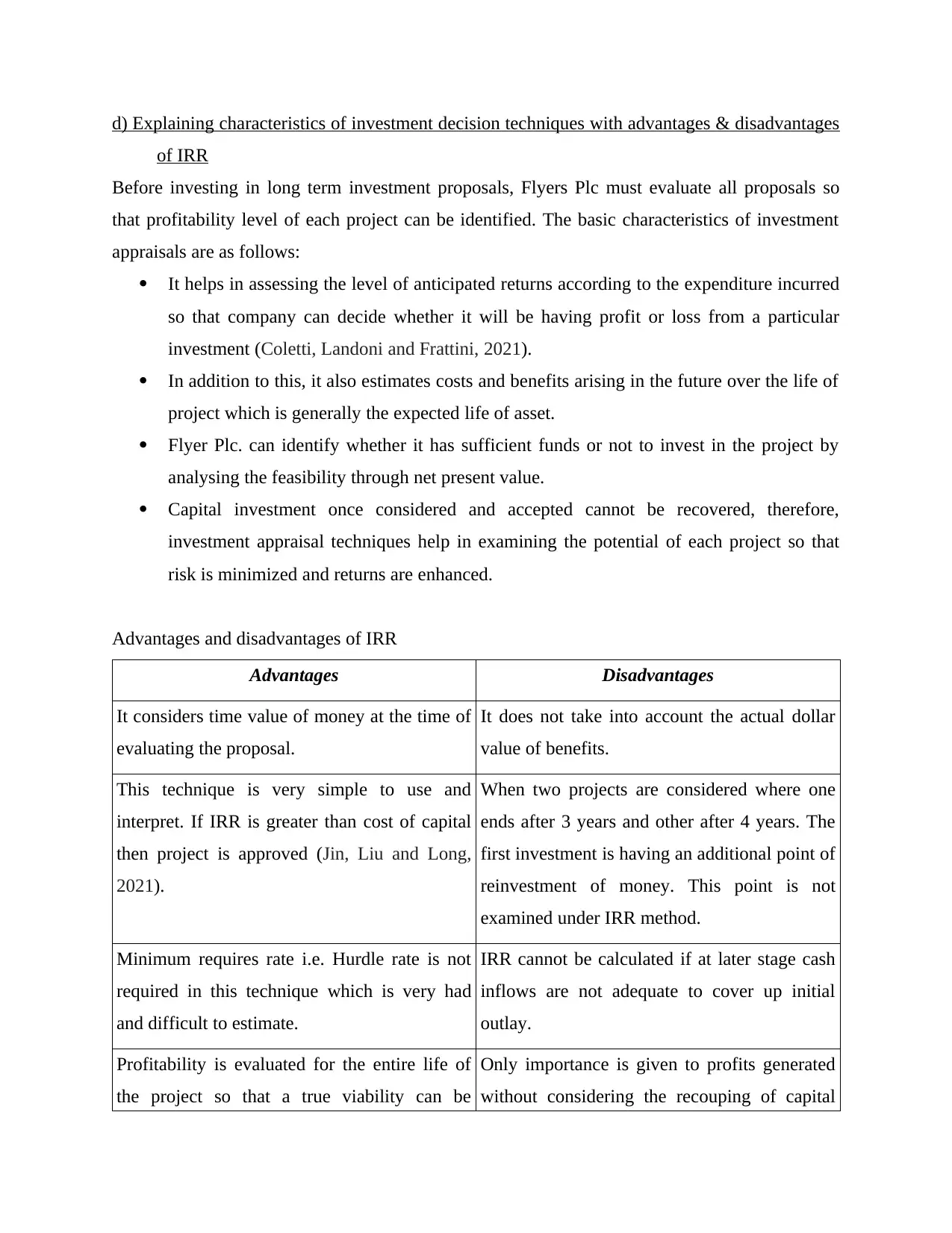

d) Explaining characteristics of investment decision techniques with advantages & disadvantages

of IRR

Before investing in long term investment proposals, Flyers Plc must evaluate all proposals so

that profitability level of each project can be identified. The basic characteristics of investment

appraisals are as follows:

It helps in assessing the level of anticipated returns according to the expenditure incurred

so that company can decide whether it will be having profit or loss from a particular

investment (Coletti, Landoni and Frattini, 2021).

In addition to this, it also estimates costs and benefits arising in the future over the life of

project which is generally the expected life of asset.

Flyer Plc. can identify whether it has sufficient funds or not to invest in the project by

analysing the feasibility through net present value.

Capital investment once considered and accepted cannot be recovered, therefore,

investment appraisal techniques help in examining the potential of each project so that

risk is minimized and returns are enhanced.

Advantages and disadvantages of IRR

Advantages Disadvantages

It considers time value of money at the time of

evaluating the proposal.

It does not take into account the actual dollar

value of benefits.

This technique is very simple to use and

interpret. If IRR is greater than cost of capital

then project is approved (Jin, Liu and Long,

2021).

When two projects are considered where one

ends after 3 years and other after 4 years. The

first investment is having an additional point of

reinvestment of money. This point is not

examined under IRR method.

Minimum requires rate i.e. Hurdle rate is not

required in this technique which is very had

and difficult to estimate.

IRR cannot be calculated if at later stage cash

inflows are not adequate to cover up initial

outlay.

Profitability is evaluated for the entire life of

the project so that a true viability can be

Only importance is given to profits generated

without considering the recouping of capital

of IRR

Before investing in long term investment proposals, Flyers Plc must evaluate all proposals so

that profitability level of each project can be identified. The basic characteristics of investment

appraisals are as follows:

It helps in assessing the level of anticipated returns according to the expenditure incurred

so that company can decide whether it will be having profit or loss from a particular

investment (Coletti, Landoni and Frattini, 2021).

In addition to this, it also estimates costs and benefits arising in the future over the life of

project which is generally the expected life of asset.

Flyer Plc. can identify whether it has sufficient funds or not to invest in the project by

analysing the feasibility through net present value.

Capital investment once considered and accepted cannot be recovered, therefore,

investment appraisal techniques help in examining the potential of each project so that

risk is minimized and returns are enhanced.

Advantages and disadvantages of IRR

Advantages Disadvantages

It considers time value of money at the time of

evaluating the proposal.

It does not take into account the actual dollar

value of benefits.

This technique is very simple to use and

interpret. If IRR is greater than cost of capital

then project is approved (Jin, Liu and Long,

2021).

When two projects are considered where one

ends after 3 years and other after 4 years. The

first investment is having an additional point of

reinvestment of money. This point is not

examined under IRR method.

Minimum requires rate i.e. Hurdle rate is not

required in this technique which is very had

and difficult to estimate.

IRR cannot be calculated if at later stage cash

inflows are not adequate to cover up initial

outlay.

Profitability is evaluated for the entire life of

the project so that a true viability can be

Only importance is given to profits generated

without considering the recouping of capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

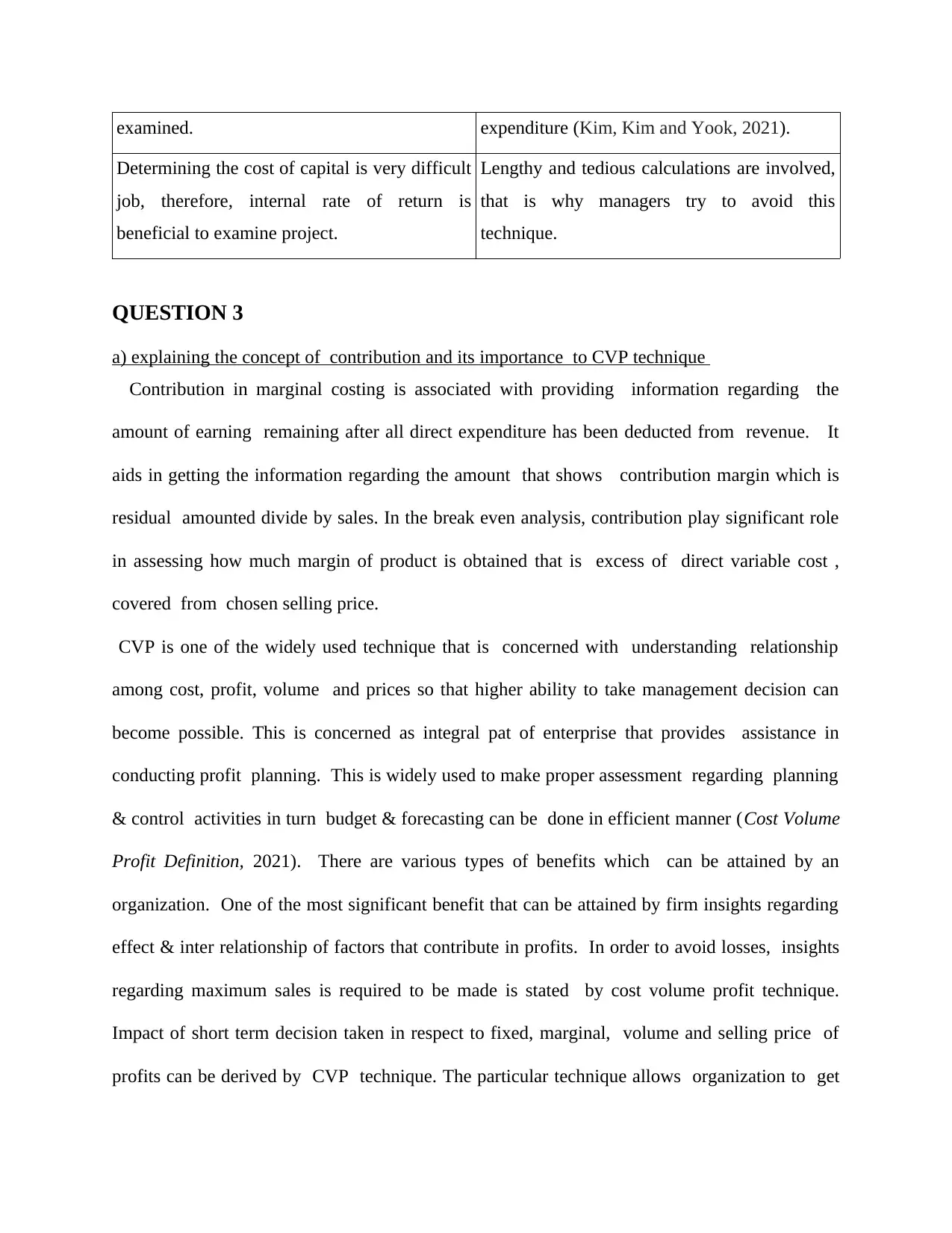

examined. expenditure (Kim, Kim and Yook, 2021).

Determining the cost of capital is very difficult

job, therefore, internal rate of return is

beneficial to examine project.

Lengthy and tedious calculations are involved,

that is why managers try to avoid this

technique.

QUESTION 3

a) explaining the concept of contribution and its importance to CVP technique

Contribution in marginal costing is associated with providing information regarding the

amount of earning remaining after all direct expenditure has been deducted from revenue. It

aids in getting the information regarding the amount that shows contribution margin which is

residual amounted divide by sales. In the break even analysis, contribution play significant role

in assessing how much margin of product is obtained that is excess of direct variable cost ,

covered from chosen selling price.

CVP is one of the widely used technique that is concerned with understanding relationship

among cost, profit, volume and prices so that higher ability to take management decision can

become possible. This is concerned as integral pat of enterprise that provides assistance in

conducting profit planning. This is widely used to make proper assessment regarding planning

& control activities in turn budget & forecasting can be done in efficient manner (Cost Volume

Profit Definition, 2021). There are various types of benefits which can be attained by an

organization. One of the most significant benefit that can be attained by firm insights regarding

effect & inter relationship of factors that contribute in profits. In order to avoid losses, insights

regarding maximum sales is required to be made is stated by cost volume profit technique.

Impact of short term decision taken in respect to fixed, marginal, volume and selling price of

profits can be derived by CVP technique. The particular technique allows organization to get

Determining the cost of capital is very difficult

job, therefore, internal rate of return is

beneficial to examine project.

Lengthy and tedious calculations are involved,

that is why managers try to avoid this

technique.

QUESTION 3

a) explaining the concept of contribution and its importance to CVP technique

Contribution in marginal costing is associated with providing information regarding the

amount of earning remaining after all direct expenditure has been deducted from revenue. It

aids in getting the information regarding the amount that shows contribution margin which is

residual amounted divide by sales. In the break even analysis, contribution play significant role

in assessing how much margin of product is obtained that is excess of direct variable cost ,

covered from chosen selling price.

CVP is one of the widely used technique that is concerned with understanding relationship

among cost, profit, volume and prices so that higher ability to take management decision can

become possible. This is concerned as integral pat of enterprise that provides assistance in

conducting profit planning. This is widely used to make proper assessment regarding planning

& control activities in turn budget & forecasting can be done in efficient manner (Cost Volume

Profit Definition, 2021). There are various types of benefits which can be attained by an

organization. One of the most significant benefit that can be attained by firm insights regarding

effect & inter relationship of factors that contribute in profits. In order to avoid losses, insights

regarding maximum sales is required to be made is stated by cost volume profit technique.

Impact of short term decision taken in respect to fixed, marginal, volume and selling price of

profits can be derived by CVP technique. The particular technique allows organization to get

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

deeper knowledge regarding the components like level of activity, unit selling price, variable &

total fixed cost and sales mix so that appropriate decision can be formulated.

b) Explaining CVP usage in dropping a product or service special contract decision

There are several decision which can be taken by organization through considering different

aspects so that higher reliability & sustainability can be derived. In addition to this, CVP

analysis helps determining the outcome that can play role of adding value to organization. The

main role play in taking decision regarding the price policies so that higher profitability can be

attained. For achieving higher profitability & sustainability there are various kinds of decision

that are taken so that ability to accomplish objective can become possible. Dropping profit and

service decision require to pay attention the factors like profits, cost, etc so that better

comparison can be made. These requires firm to pay attention on such technique that can be

useful in ascertaining impacting factor in deeper manner. CVP is one of the significant

technique that shares in assessing such all the factor that is highly useful in assessing that

product is useful in attaining those objectives or not.

CVP as well concentrate on getting the data regarding break even point, fixed cost, etc. The

special contract is required to make assessment that it should be accepted or rejected. CVP

technique aids in evaluating aspects like qualitative factors, role of fixed cost, capacity require

to fulfill order, etc. Takings decision by considering such factor can allow firm to analyse that

it should be accepted or rejected in order to have smooth functioning.

c) Describing CVP & its related limitation in context of both economies model and other

interpretation

Each model has certain limitation which need to be specified while taking decision so

that overall criteria required for smooth function can be derived. According to economic model

and other interpretation it can be identified that there are various limitations which need to be

total fixed cost and sales mix so that appropriate decision can be formulated.

b) Explaining CVP usage in dropping a product or service special contract decision

There are several decision which can be taken by organization through considering different

aspects so that higher reliability & sustainability can be derived. In addition to this, CVP

analysis helps determining the outcome that can play role of adding value to organization. The

main role play in taking decision regarding the price policies so that higher profitability can be

attained. For achieving higher profitability & sustainability there are various kinds of decision

that are taken so that ability to accomplish objective can become possible. Dropping profit and

service decision require to pay attention the factors like profits, cost, etc so that better

comparison can be made. These requires firm to pay attention on such technique that can be

useful in ascertaining impacting factor in deeper manner. CVP is one of the significant

technique that shares in assessing such all the factor that is highly useful in assessing that

product is useful in attaining those objectives or not.

CVP as well concentrate on getting the data regarding break even point, fixed cost, etc. The

special contract is required to make assessment that it should be accepted or rejected. CVP

technique aids in evaluating aspects like qualitative factors, role of fixed cost, capacity require

to fulfill order, etc. Takings decision by considering such factor can allow firm to analyse that

it should be accepted or rejected in order to have smooth functioning.

c) Describing CVP & its related limitation in context of both economies model and other

interpretation

Each model has certain limitation which need to be specified while taking decision so

that overall criteria required for smooth function can be derived. According to economic model

and other interpretation it can be identified that there are various limitations which need to be

highlighted so that possible of wrong business practice can be avoided (Cost Volume Profit

Analysis: Definition, Objectives, Assumptions, Limitations, 2020). There are assumptions like

constant selling price, sales mix,inventories do not change, etc that are not possible in realistic

world.

The limitation comprises identifying difference in fixed & variable cost which tend to

provide inaccurate results. Relationship between variable cost & volume of cost output is not

always effective. CVP technique is not suitable for the company providing multi products as

well selling price is not constant. This keeps on changing due to various external factor and

ignore influence of these factor on variable & fixed kind of cost. Major limitation that need to

be specified for achieving deeper knowledge of its drawback in turn respective course of action

can be applied. There is presence of inventory which is assumed to be kept constant that leads

this particular technique towards failure. It is not effective for longer run that interrupt in

having crucial information so that overall objective of business can be accomplished. On the

basis of this, it can be identified that these limitation results in getting efficiency & accuracy

of business operation in turn greater emphasis on this should be provided.

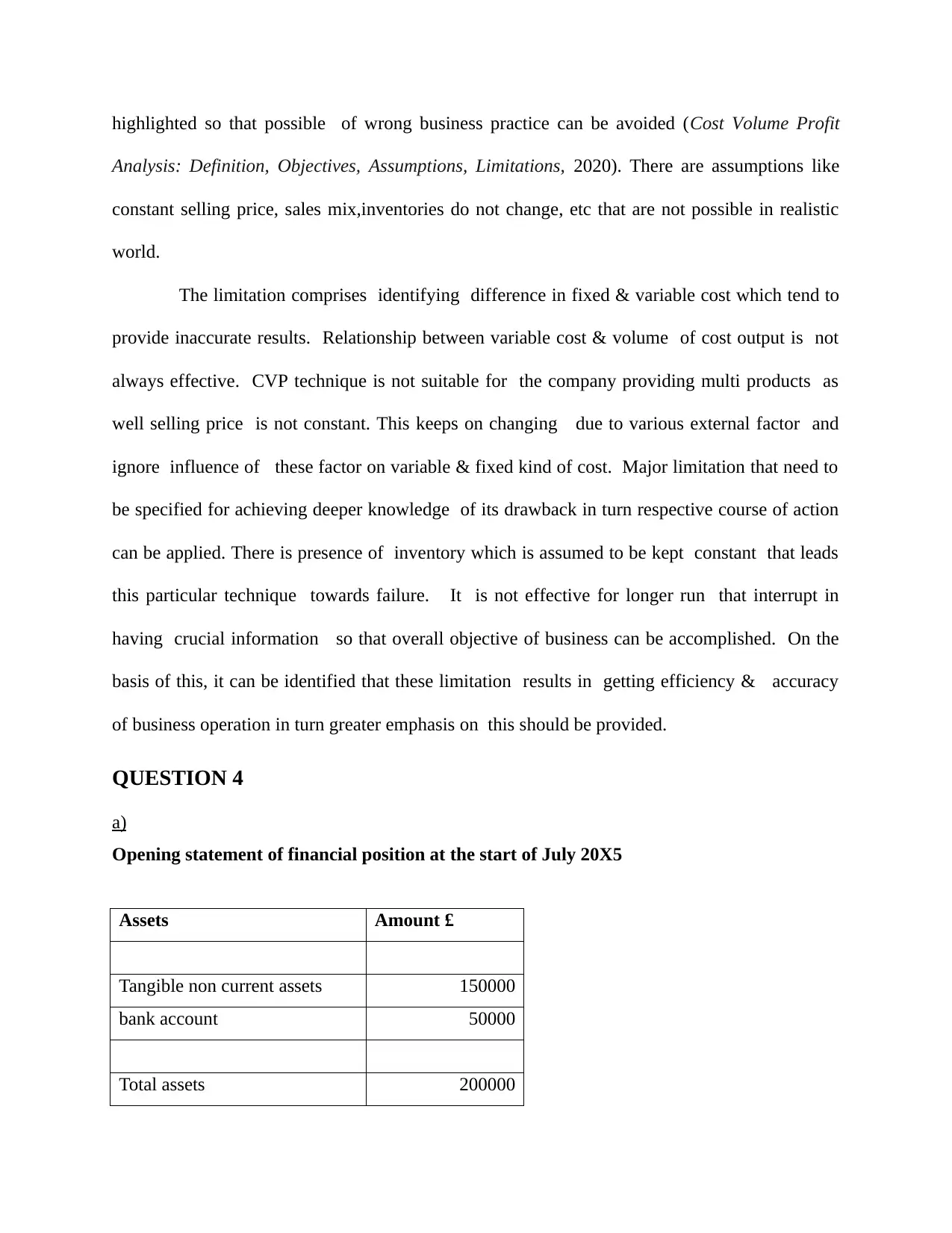

QUESTION 4

a)

Opening statement of financial position at the start of July 20X5

Assets Amount £

Tangible non current assets 150000

bank account 50000

Total assets 200000

Analysis: Definition, Objectives, Assumptions, Limitations, 2020). There are assumptions like

constant selling price, sales mix,inventories do not change, etc that are not possible in realistic

world.

The limitation comprises identifying difference in fixed & variable cost which tend to

provide inaccurate results. Relationship between variable cost & volume of cost output is not

always effective. CVP technique is not suitable for the company providing multi products as

well selling price is not constant. This keeps on changing due to various external factor and

ignore influence of these factor on variable & fixed kind of cost. Major limitation that need to

be specified for achieving deeper knowledge of its drawback in turn respective course of action

can be applied. There is presence of inventory which is assumed to be kept constant that leads

this particular technique towards failure. It is not effective for longer run that interrupt in

having crucial information so that overall objective of business can be accomplished. On the

basis of this, it can be identified that these limitation results in getting efficiency & accuracy

of business operation in turn greater emphasis on this should be provided.

QUESTION 4

a)

Opening statement of financial position at the start of July 20X5

Assets Amount £

Tangible non current assets 150000

bank account 50000

Total assets 200000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.