Corporate Accounting: Merger, Acquisition, and Valuation Report

VerifiedAdded on 2023/04/17

|15

|4664

|384

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting, focusing on mergers and acquisitions (M&A) within the context of Vodafone Group plc and BT Group. The introduction establishes the importance of corporate accounting and outlines the report's objectives, including examining the merits of cash versus equity funding in M&A deals. The main body delves into the reasons behind companies choosing M&A, such as strategic business goals and economic development, and discusses the advantages of both cash and equity funding. The report then presents an overview of Vodafone Group plc, highlighting its financial performance and strategic decisions, and provides a detailed financial analysis of BT Group, including key financial indicators like revenue, EBITDA, and ROCE. The capital structure and Weighted Average Cost of Capital (WACC) are examined, followed by a valuation of the target company using the discounted free cash flow method. The report concludes with recommendations based on the analysis, summarizing the key findings and offering insights into the potential acquisition of BT Group by Vodafone. Finally, the report provides a summary of the analysis and a list of references.

Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

Main Body.......................................................................................................................................3

(a): Reason behind companies choose merger and acquisition..............................................3

(b): Overview of the company taken as acquisition target.....................................................5

(c): Capital structure and WACC...........................................................................................7

(d): Valuation of the target company by using discounted free cash flow method................9

(e): Recommendation...........................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

2

INTRODUCTION...........................................................................................................................3

Main Body.......................................................................................................................................3

(a): Reason behind companies choose merger and acquisition..............................................3

(b): Overview of the company taken as acquisition target.....................................................5

(c): Capital structure and WACC...........................................................................................7

(d): Valuation of the target company by using discounted free cash flow method................9

(e): Recommendation...........................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

2

INTRODUCTION

Corporate accounting is an essential branch of finance that deal with accounting information

for companies, formulation of their final reports and cash flow statement for specific activities

such as absorption and amalgamation. The primary purpose of corporate accounting is to

maintain proper balance among financial systems of a company. “Vodafone group plc” is a

public listed company which has been taken into account for the corporate restructuring. This

project report aimed at providing specific information about relative merits of cash or equity

funding relation in merger and acquisition (Zadek, Evans and Pruzan, 2013). Apart from this,

justification regarding chosen company by the help of using key financial data is covered

effectively. Along with that calculation of weighted cost of capital and valuation of target

companies by using discounted cash flow method has being discussed properly in this report.

Further this report summary all the analysis by providing reliable recommendation has been

mentioned clearly.

Main Body

(a): Reason behind companies choose merger and acquisition

Corporate restructuring is an essential action which has been taken by companies to

significantly change their structure in order to increase future growth and profitability. The

primary reason behind most of the companies used restructuring is to overcome all their financial

issues or losses from couple of period (Koh, Durand, Dai and Chang, 2015). It seems to be

necessity to analyse financial adjustments to their assets and debts obligations. Basically, it will

be taken into account to reduce cost of manufacturing in an accounting period of time. As a

business proprietor, company can always look for their future growth and earn maximum money

by serving wide range of customer base. Thus, it is essential for an organisation to identify

valuable ways to grow their business operations and do this at a drastic pace (Bhasin, 2013).

It has been seen that M&A is done because of strategic business reasons, but the primary

reasons for any business combination are economic development as a core. Gaining a

competitive benefits or wide market share is another crucial motive behind going of M&A

(Phillips and Zhdanov, 2013). Most of the time company used to decide for merger in order to

earn a better distribution of network for marketing their business products. Merger and

acquisition is one of the valuable options that can help companies without having waited for long

3

Corporate accounting is an essential branch of finance that deal with accounting information

for companies, formulation of their final reports and cash flow statement for specific activities

such as absorption and amalgamation. The primary purpose of corporate accounting is to

maintain proper balance among financial systems of a company. “Vodafone group plc” is a

public listed company which has been taken into account for the corporate restructuring. This

project report aimed at providing specific information about relative merits of cash or equity

funding relation in merger and acquisition (Zadek, Evans and Pruzan, 2013). Apart from this,

justification regarding chosen company by the help of using key financial data is covered

effectively. Along with that calculation of weighted cost of capital and valuation of target

companies by using discounted cash flow method has being discussed properly in this report.

Further this report summary all the analysis by providing reliable recommendation has been

mentioned clearly.

Main Body

(a): Reason behind companies choose merger and acquisition

Corporate restructuring is an essential action which has been taken by companies to

significantly change their structure in order to increase future growth and profitability. The

primary reason behind most of the companies used restructuring is to overcome all their financial

issues or losses from couple of period (Koh, Durand, Dai and Chang, 2015). It seems to be

necessity to analyse financial adjustments to their assets and debts obligations. Basically, it will

be taken into account to reduce cost of manufacturing in an accounting period of time. As a

business proprietor, company can always look for their future growth and earn maximum money

by serving wide range of customer base. Thus, it is essential for an organisation to identify

valuable ways to grow their business operations and do this at a drastic pace (Bhasin, 2013).

It has been seen that M&A is done because of strategic business reasons, but the primary

reasons for any business combination are economic development as a core. Gaining a

competitive benefits or wide market share is another crucial motive behind going of M&A

(Phillips and Zhdanov, 2013). Most of the time company used to decide for merger in order to

earn a better distribution of network for marketing their business products. Merger and

acquisition is one of the valuable options that can help companies without having waited for long

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

years regarding their marketing and sales planning to pay-off. In case, company wants to grow

faster, this can be right option for them that would deliver instant outcomes. The basic motive of

organisation in merger and acquisition is to secure a valuable opportunity that could either attain

the aims and objectives of growth. It would also deliver right areas of expansion which will

include to product and services line in the market that is presently not serving by firm. The basic

motivation regarding this recreation is that the resulting combination of items, key people and

current pipeline would allow overall business to operate their business in new market and tends

to provide sufficient amount of option to existing target market. Operating business by using

merger and acquisition doesn’t always free from challenge, but it also results in plenty of new

problems. It consists of regulating a company with total presence in multiple locations as well as

has more complex goods and service portfolio.

There are some other issues that are related to cost reduction objective which can be

associated with the revenue growth opportunities. Keeping all specific challenges in mind,

company go for mergers that diversify their overall business operations in more than one nation.

It can acquire another company which is seemingly unrelated to control implication on specific

performance to increase profitability (Hui, Klasa and Yeung, 2012). There are various essential

reasons to be taken into consideration for going with merger and acquisition. Some of them are

discussed below:

Synergies: By proper combination of business activities, performance would increase and

cost will reduce because of synergies among two legal entities. An organisation will always

attempt to merge with other company that is having complementary strength as well as

weaknesses (Dutordoir, Roosenboom and Vasconcelos, 2014).

Diversification: In most of the cases, companies use merger and acquisition techniques for

diversify their business. It seeks to provide proper shape their aim that is often merges with those

companies which is having deeper market penetration.

Growth: It used to give opportunity to acquire company to nurture market share instead of

having really on doing their work by themselves (Mueller, 2013). Most of the time companies

used to buy a competitive business in accordance to a price. Growth can lead to increase their

market presence and increase future sustainability of the company.

Eliminate competition: Plenty of merger and acquisition deals tend to allow owner to

reduce upcoming competition and try to earn maximum market share from their overall

4

faster, this can be right option for them that would deliver instant outcomes. The basic motive of

organisation in merger and acquisition is to secure a valuable opportunity that could either attain

the aims and objectives of growth. It would also deliver right areas of expansion which will

include to product and services line in the market that is presently not serving by firm. The basic

motivation regarding this recreation is that the resulting combination of items, key people and

current pipeline would allow overall business to operate their business in new market and tends

to provide sufficient amount of option to existing target market. Operating business by using

merger and acquisition doesn’t always free from challenge, but it also results in plenty of new

problems. It consists of regulating a company with total presence in multiple locations as well as

has more complex goods and service portfolio.

There are some other issues that are related to cost reduction objective which can be

associated with the revenue growth opportunities. Keeping all specific challenges in mind,

company go for mergers that diversify their overall business operations in more than one nation.

It can acquire another company which is seemingly unrelated to control implication on specific

performance to increase profitability (Hui, Klasa and Yeung, 2012). There are various essential

reasons to be taken into consideration for going with merger and acquisition. Some of them are

discussed below:

Synergies: By proper combination of business activities, performance would increase and

cost will reduce because of synergies among two legal entities. An organisation will always

attempt to merge with other company that is having complementary strength as well as

weaknesses (Dutordoir, Roosenboom and Vasconcelos, 2014).

Diversification: In most of the cases, companies use merger and acquisition techniques for

diversify their business. It seeks to provide proper shape their aim that is often merges with those

companies which is having deeper market penetration.

Growth: It used to give opportunity to acquire company to nurture market share instead of

having really on doing their work by themselves (Mueller, 2013). Most of the time companies

used to buy a competitive business in accordance to a price. Growth can lead to increase their

market presence and increase future sustainability of the company.

Eliminate competition: Plenty of merger and acquisition deals tend to allow owner to

reduce upcoming competition and try to earn maximum market share from their overall

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

productive market. It is more uncommon for acquiring company’s shareholders that can sells to

their shares and force the cost lower in relation to the companies paying too much for their

estimated company (Whish and Bailey, 2015).

Merits of cash and equity funding

Financial restructuring is an essential reorganizing financial structure that comprises of

equity and debt capital. It can be done because either compulsion as well as part of accounting

strategy of the company.

Merits of cash: It would create transparency is cash management. It is considered as

automated process such as smart safes and provides faster access to the business to manage their

cash. This visibility tends to facilities in effective decision making and allows businesses to be

more effectively manage their operations in proper manner (Edwards, 2013).

Merits of equity funding: In every business organisation, equity financing that does not

take capital out of their business. It will help in long term planning for the investors that does not

expect to retain a quick return on their overall investment. It carries no repayment obligation as

well as provides extra working funds that can be useful to grow a business effectively for long

period of time.

(b): Overview of the company taken as acquisition target

“Vodafone group plc” is a leading British multinational telecom conglomerate which is

situated in London. It owns and deals in almost 25 nations as well as have partner network in 47

countries. It is basically listed on London Stock Exchange (LSE) as well as constituents of FTSE

100 index (Financial performance. 2018). It would have a great market capitalisation with total

£46.571 billion in 2018. The primary reason for the selection of this company is to analyse the

past case situation which is related with the merger of their Indian mobile business with idea

network. It is one of the successful mergers that set a platform for the company to increase their

profitability and market share in front of other companies. It is one of the faster networks in

telecom sector that would connect maximum people with their valuable connection. The

“Vodafone group” is planning to acquire BT group which is also a telecom company operating in

London. It is having large customer base with total of wide customers and largest operator of 4G

services in many parts of the nation. The entire strategy of BT group is essential part of

Vodafone group which is outlined in group planning analysis.

5

their shares and force the cost lower in relation to the companies paying too much for their

estimated company (Whish and Bailey, 2015).

Merits of cash and equity funding

Financial restructuring is an essential reorganizing financial structure that comprises of

equity and debt capital. It can be done because either compulsion as well as part of accounting

strategy of the company.

Merits of cash: It would create transparency is cash management. It is considered as

automated process such as smart safes and provides faster access to the business to manage their

cash. This visibility tends to facilities in effective decision making and allows businesses to be

more effectively manage their operations in proper manner (Edwards, 2013).

Merits of equity funding: In every business organisation, equity financing that does not

take capital out of their business. It will help in long term planning for the investors that does not

expect to retain a quick return on their overall investment. It carries no repayment obligation as

well as provides extra working funds that can be useful to grow a business effectively for long

period of time.

(b): Overview of the company taken as acquisition target

“Vodafone group plc” is a leading British multinational telecom conglomerate which is

situated in London. It owns and deals in almost 25 nations as well as have partner network in 47

countries. It is basically listed on London Stock Exchange (LSE) as well as constituents of FTSE

100 index (Financial performance. 2018). It would have a great market capitalisation with total

£46.571 billion in 2018. The primary reason for the selection of this company is to analyse the

past case situation which is related with the merger of their Indian mobile business with idea

network. It is one of the successful mergers that set a platform for the company to increase their

profitability and market share in front of other companies. It is one of the faster networks in

telecom sector that would connect maximum people with their valuable connection. The

“Vodafone group” is planning to acquire BT group which is also a telecom company operating in

London. It is having large customer base with total of wide customers and largest operator of 4G

services in many parts of the nation. The entire strategy of BT group is essential part of

Vodafone group which is outlined in group planning analysis.

5

There are certain key financial performance indicators those are related with BT revenue

and EBITDA. Revenue for the year was amounted to € 23.74 billion with total operating income

of € 3.381 billion in 2018. The most valuable objective assessment of financial position of a firm

is the return they are generating on their asset and the quantity as well as quality of outcome they

are getting in an accounting period (Mueller, Carter and Ross-Smith, 2011).

BT turnover and revenue after tax have increased in respect to last year, but they are still

minimum than those in 2018. A decline of 6.7% has been recorded over the last two year time. It

would indicate that business has very minimum variable costs that are line with heavy fixed cost

investment basically made through telecommunication sectors (Annual report BT group. 2018).

In the past few year, operating profit is also declined. This would indicates that business is

having some pricing pressures as well as spending more on their promotion this is reason behind

decline of profit by 0.5%. They have attained financial guidance which was set out at the initial

stage of the year for adjusted EBITDA. It gets increased for normalised free cash flow. BT

telecom has its key measure of group revenue trend underlying with total earning which reduce

their transit of 1.0% in 2017. The overall performance of the company has been affected in our

enterprise businesses. Specifically in international services where earning has come down

because of ongoing demand market situation and low IP exchange volumes (Higdon, 2011).

The BT Telecom is aware of their problems and has aimed on reducing their net debts

which has come down from 9838 to 8932 from last year. The net cash cost of a particular items

was amounted as €828m this constitute of payment associated with the settlement of warranty

claims in respect to the BT acquisition of €225 m in 2017 (Morningstar, 2018). The ROCE of

BT telecom is showing positive growth of return as compare to last year with 21.80% return in

2018. The company is also able to generate a valuable amount of net margin with total of 8.57%.

In relation to the liquidity position is also not so effective as its current liabilities has exceeded

the asset because of which the value comes down to below 1. It means that BT telecom is having

issues regarding meeting their short-term obligations (Brealey, Myers, Allen and Mohanty,

2012). The debt to equity ratio is showing that BT Company is not being able to generate

valuable amount of cash to fulfil their debt obligation. In 2018, only 1.18 debts to equity has

been calculation which is low for the company. It means that company is not utilising their

increase profit in their business.

6

and EBITDA. Revenue for the year was amounted to € 23.74 billion with total operating income

of € 3.381 billion in 2018. The most valuable objective assessment of financial position of a firm

is the return they are generating on their asset and the quantity as well as quality of outcome they

are getting in an accounting period (Mueller, Carter and Ross-Smith, 2011).

BT turnover and revenue after tax have increased in respect to last year, but they are still

minimum than those in 2018. A decline of 6.7% has been recorded over the last two year time. It

would indicate that business has very minimum variable costs that are line with heavy fixed cost

investment basically made through telecommunication sectors (Annual report BT group. 2018).

In the past few year, operating profit is also declined. This would indicates that business is

having some pricing pressures as well as spending more on their promotion this is reason behind

decline of profit by 0.5%. They have attained financial guidance which was set out at the initial

stage of the year for adjusted EBITDA. It gets increased for normalised free cash flow. BT

telecom has its key measure of group revenue trend underlying with total earning which reduce

their transit of 1.0% in 2017. The overall performance of the company has been affected in our

enterprise businesses. Specifically in international services where earning has come down

because of ongoing demand market situation and low IP exchange volumes (Higdon, 2011).

The BT Telecom is aware of their problems and has aimed on reducing their net debts

which has come down from 9838 to 8932 from last year. The net cash cost of a particular items

was amounted as €828m this constitute of payment associated with the settlement of warranty

claims in respect to the BT acquisition of €225 m in 2017 (Morningstar, 2018). The ROCE of

BT telecom is showing positive growth of return as compare to last year with 21.80% return in

2018. The company is also able to generate a valuable amount of net margin with total of 8.57%.

In relation to the liquidity position is also not so effective as its current liabilities has exceeded

the asset because of which the value comes down to below 1. It means that BT telecom is having

issues regarding meeting their short-term obligations (Brealey, Myers, Allen and Mohanty,

2012). The debt to equity ratio is showing that BT Company is not being able to generate

valuable amount of cash to fulfil their debt obligation. In 2018, only 1.18 debts to equity has

been calculation which is low for the company. It means that company is not utilising their

increase profit in their business.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

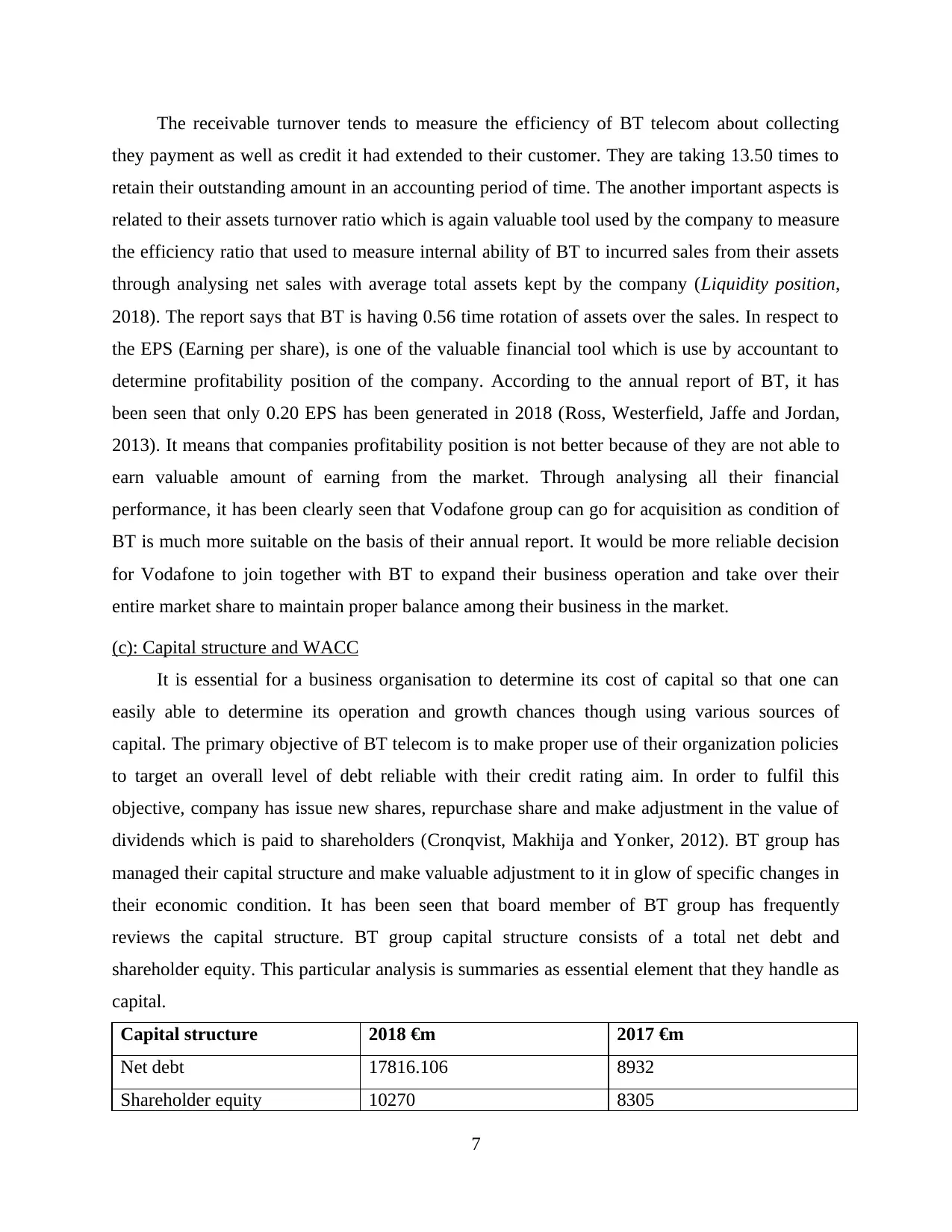

The receivable turnover tends to measure the efficiency of BT telecom about collecting

they payment as well as credit it had extended to their customer. They are taking 13.50 times to

retain their outstanding amount in an accounting period of time. The another important aspects is

related to their assets turnover ratio which is again valuable tool used by the company to measure

the efficiency ratio that used to measure internal ability of BT to incurred sales from their assets

through analysing net sales with average total assets kept by the company (Liquidity position,

2018). The report says that BT is having 0.56 time rotation of assets over the sales. In respect to

the EPS (Earning per share), is one of the valuable financial tool which is use by accountant to

determine profitability position of the company. According to the annual report of BT, it has

been seen that only 0.20 EPS has been generated in 2018 (Ross, Westerfield, Jaffe and Jordan,

2013). It means that companies profitability position is not better because of they are not able to

earn valuable amount of earning from the market. Through analysing all their financial

performance, it has been clearly seen that Vodafone group can go for acquisition as condition of

BT is much more suitable on the basis of their annual report. It would be more reliable decision

for Vodafone to join together with BT to expand their business operation and take over their

entire market share to maintain proper balance among their business in the market.

(c): Capital structure and WACC

It is essential for a business organisation to determine its cost of capital so that one can

easily able to determine its operation and growth chances though using various sources of

capital. The primary objective of BT telecom is to make proper use of their organization policies

to target an overall level of debt reliable with their credit rating aim. In order to fulfil this

objective, company has issue new shares, repurchase share and make adjustment in the value of

dividends which is paid to shareholders (Cronqvist, Makhija and Yonker, 2012). BT group has

managed their capital structure and make valuable adjustment to it in glow of specific changes in

their economic condition. It has been seen that board member of BT group has frequently

reviews the capital structure. BT group capital structure consists of a total net debt and

shareholder equity. This particular analysis is summaries as essential element that they handle as

capital.

Capital structure 2018 €m 2017 €m

Net debt 17816.106 8932

Shareholder equity 10270 8305

7

they payment as well as credit it had extended to their customer. They are taking 13.50 times to

retain their outstanding amount in an accounting period of time. The another important aspects is

related to their assets turnover ratio which is again valuable tool used by the company to measure

the efficiency ratio that used to measure internal ability of BT to incurred sales from their assets

through analysing net sales with average total assets kept by the company (Liquidity position,

2018). The report says that BT is having 0.56 time rotation of assets over the sales. In respect to

the EPS (Earning per share), is one of the valuable financial tool which is use by accountant to

determine profitability position of the company. According to the annual report of BT, it has

been seen that only 0.20 EPS has been generated in 2018 (Ross, Westerfield, Jaffe and Jordan,

2013). It means that companies profitability position is not better because of they are not able to

earn valuable amount of earning from the market. Through analysing all their financial

performance, it has been clearly seen that Vodafone group can go for acquisition as condition of

BT is much more suitable on the basis of their annual report. It would be more reliable decision

for Vodafone to join together with BT to expand their business operation and take over their

entire market share to maintain proper balance among their business in the market.

(c): Capital structure and WACC

It is essential for a business organisation to determine its cost of capital so that one can

easily able to determine its operation and growth chances though using various sources of

capital. The primary objective of BT telecom is to make proper use of their organization policies

to target an overall level of debt reliable with their credit rating aim. In order to fulfil this

objective, company has issue new shares, repurchase share and make adjustment in the value of

dividends which is paid to shareholders (Cronqvist, Makhija and Yonker, 2012). BT group has

managed their capital structure and make valuable adjustment to it in glow of specific changes in

their economic condition. It has been seen that board member of BT group has frequently

reviews the capital structure. BT group capital structure consists of a total net debt and

shareholder equity. This particular analysis is summaries as essential element that they handle as

capital.

Capital structure 2018 €m 2017 €m

Net debt 17816.106 8932

Shareholder equity 10270 8305

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

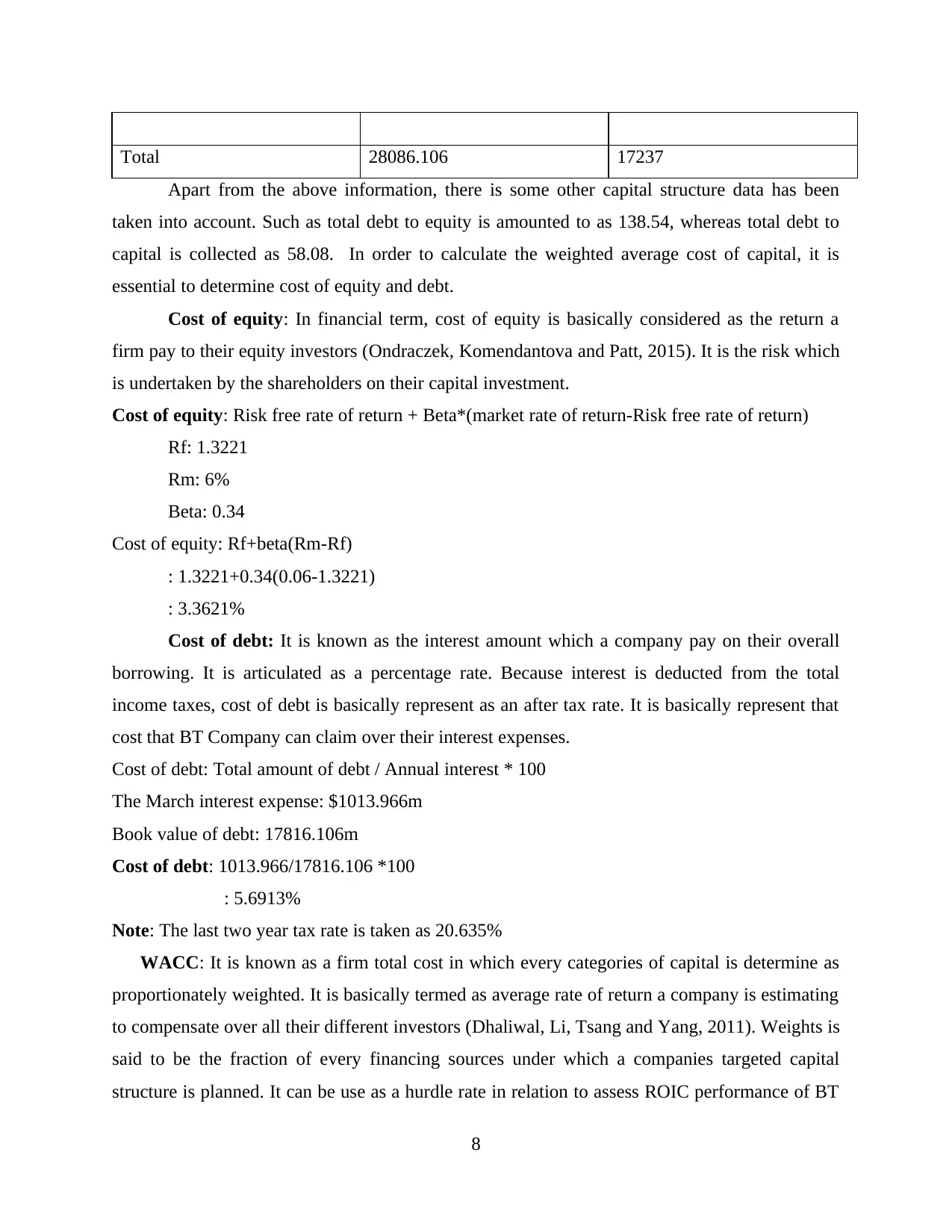

Total 28086.106 17237

Apart from the above information, there is some other capital structure data has been

taken into account. Such as total debt to equity is amounted to as 138.54, whereas total debt to

capital is collected as 58.08. In order to calculate the weighted average cost of capital, it is

essential to determine cost of equity and debt.

Cost of equity: In financial term, cost of equity is basically considered as the return a

firm pay to their equity investors (Ondraczek, Komendantova and Patt, 2015). It is the risk which

is undertaken by the shareholders on their capital investment.

Cost of equity: Risk free rate of return + Beta*(market rate of return-Risk free rate of return)

Rf: 1.3221

Rm: 6%

Beta: 0.34

Cost of equity: Rf+beta(Rm-Rf)

: 1.3221+0.34(0.06-1.3221)

: 3.3621%

Cost of debt: It is known as the interest amount which a company pay on their overall

borrowing. It is articulated as a percentage rate. Because interest is deducted from the total

income taxes, cost of debt is basically represent as an after tax rate. It is basically represent that

cost that BT Company can claim over their interest expenses.

Cost of debt: Total amount of debt / Annual interest * 100

The March interest expense: $1013.966m

Book value of debt: 17816.106m

Cost of debt: 1013.966/17816.106 *100

: 5.6913%

Note: The last two year tax rate is taken as 20.635%

WACC: It is known as a firm total cost in which every categories of capital is determine as

proportionately weighted. It is basically termed as average rate of return a company is estimating

to compensate over all their different investors (Dhaliwal, Li, Tsang and Yang, 2011). Weights is

said to be the fraction of every financing sources under which a companies targeted capital

structure is planned. It can be use as a hurdle rate in relation to assess ROIC performance of BT

8

Apart from the above information, there is some other capital structure data has been

taken into account. Such as total debt to equity is amounted to as 138.54, whereas total debt to

capital is collected as 58.08. In order to calculate the weighted average cost of capital, it is

essential to determine cost of equity and debt.

Cost of equity: In financial term, cost of equity is basically considered as the return a

firm pay to their equity investors (Ondraczek, Komendantova and Patt, 2015). It is the risk which

is undertaken by the shareholders on their capital investment.

Cost of equity: Risk free rate of return + Beta*(market rate of return-Risk free rate of return)

Rf: 1.3221

Rm: 6%

Beta: 0.34

Cost of equity: Rf+beta(Rm-Rf)

: 1.3221+0.34(0.06-1.3221)

: 3.3621%

Cost of debt: It is known as the interest amount which a company pay on their overall

borrowing. It is articulated as a percentage rate. Because interest is deducted from the total

income taxes, cost of debt is basically represent as an after tax rate. It is basically represent that

cost that BT Company can claim over their interest expenses.

Cost of debt: Total amount of debt / Annual interest * 100

The March interest expense: $1013.966m

Book value of debt: 17816.106m

Cost of debt: 1013.966/17816.106 *100

: 5.6913%

Note: The last two year tax rate is taken as 20.635%

WACC: It is known as a firm total cost in which every categories of capital is determine as

proportionately weighted. It is basically termed as average rate of return a company is estimating

to compensate over all their different investors (Dhaliwal, Li, Tsang and Yang, 2011). Weights is

said to be the fraction of every financing sources under which a companies targeted capital

structure is planned. It can be use as a hurdle rate in relation to assess ROIC performance of BT

8

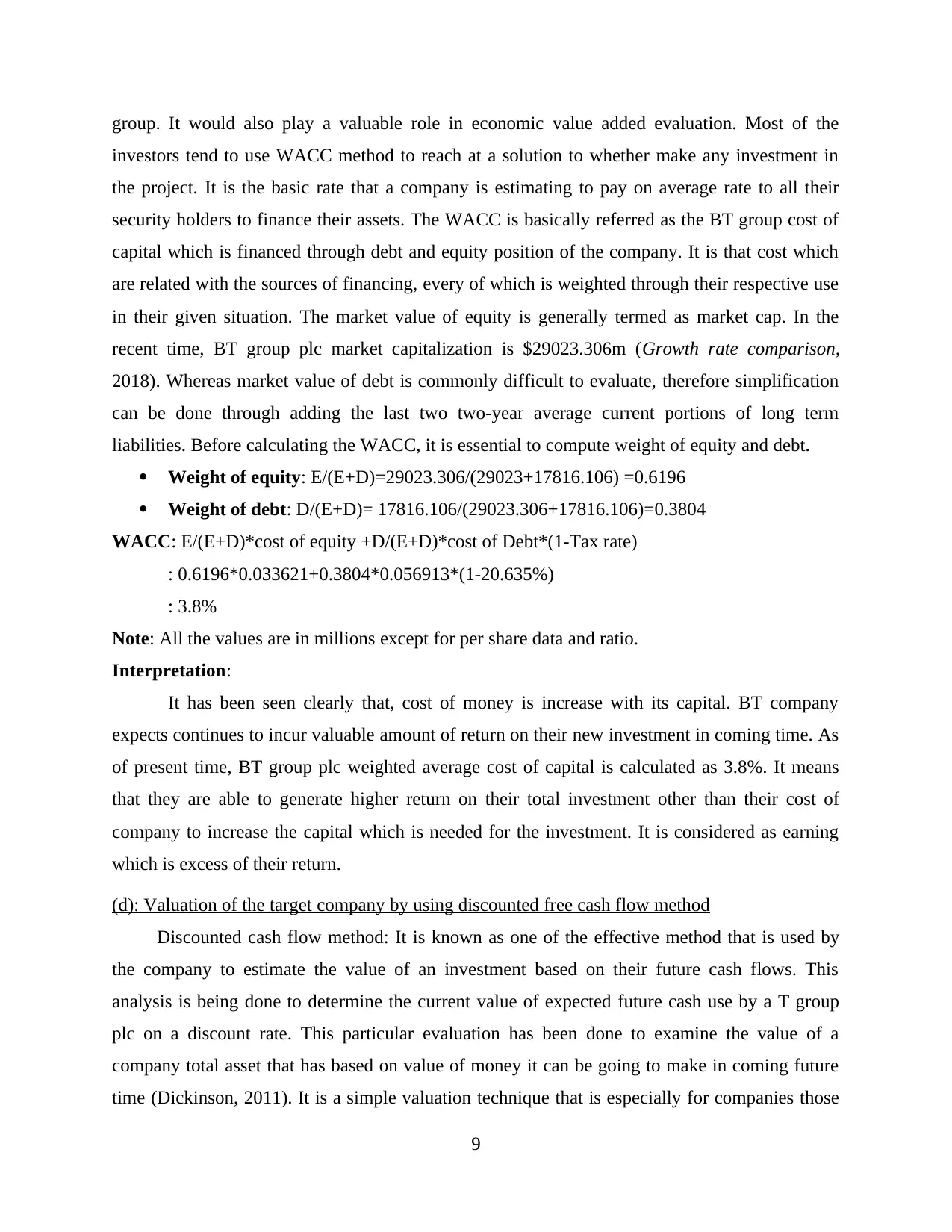

group. It would also play a valuable role in economic value added evaluation. Most of the

investors tend to use WACC method to reach at a solution to whether make any investment in

the project. It is the basic rate that a company is estimating to pay on average rate to all their

security holders to finance their assets. The WACC is basically referred as the BT group cost of

capital which is financed through debt and equity position of the company. It is that cost which

are related with the sources of financing, every of which is weighted through their respective use

in their given situation. The market value of equity is generally termed as market cap. In the

recent time, BT group plc market capitalization is $29023.306m (Growth rate comparison,

2018). Whereas market value of debt is commonly difficult to evaluate, therefore simplification

can be done through adding the last two two-year average current portions of long term

liabilities. Before calculating the WACC, it is essential to compute weight of equity and debt.

Weight of equity: E/(E+D)=29023.306/(29023+17816.106) =0.6196

Weight of debt: D/(E+D)= 17816.106/(29023.306+17816.106)=0.3804

WACC: E/(E+D)*cost of equity +D/(E+D)*cost of Debt*(1-Tax rate)

: 0.6196*0.033621+0.3804*0.056913*(1-20.635%)

: 3.8%

Note: All the values are in millions except for per share data and ratio.

Interpretation:

It has been seen clearly that, cost of money is increase with its capital. BT company

expects continues to incur valuable amount of return on their new investment in coming time. As

of present time, BT group plc weighted average cost of capital is calculated as 3.8%. It means

that they are able to generate higher return on their total investment other than their cost of

company to increase the capital which is needed for the investment. It is considered as earning

which is excess of their return.

(d): Valuation of the target company by using discounted free cash flow method

Discounted cash flow method: It is known as one of the effective method that is used by

the company to estimate the value of an investment based on their future cash flows. This

analysis is being done to determine the current value of expected future cash use by a T group

plc on a discount rate. This particular evaluation has been done to examine the value of a

company total asset that has based on value of money it can be going to make in coming future

time (Dickinson, 2011). It is a simple valuation technique that is especially for companies those

9

investors tend to use WACC method to reach at a solution to whether make any investment in

the project. It is the basic rate that a company is estimating to pay on average rate to all their

security holders to finance their assets. The WACC is basically referred as the BT group cost of

capital which is financed through debt and equity position of the company. It is that cost which

are related with the sources of financing, every of which is weighted through their respective use

in their given situation. The market value of equity is generally termed as market cap. In the

recent time, BT group plc market capitalization is $29023.306m (Growth rate comparison,

2018). Whereas market value of debt is commonly difficult to evaluate, therefore simplification

can be done through adding the last two two-year average current portions of long term

liabilities. Before calculating the WACC, it is essential to compute weight of equity and debt.

Weight of equity: E/(E+D)=29023.306/(29023+17816.106) =0.6196

Weight of debt: D/(E+D)= 17816.106/(29023.306+17816.106)=0.3804

WACC: E/(E+D)*cost of equity +D/(E+D)*cost of Debt*(1-Tax rate)

: 0.6196*0.033621+0.3804*0.056913*(1-20.635%)

: 3.8%

Note: All the values are in millions except for per share data and ratio.

Interpretation:

It has been seen clearly that, cost of money is increase with its capital. BT company

expects continues to incur valuable amount of return on their new investment in coming time. As

of present time, BT group plc weighted average cost of capital is calculated as 3.8%. It means

that they are able to generate higher return on their total investment other than their cost of

company to increase the capital which is needed for the investment. It is considered as earning

which is excess of their return.

(d): Valuation of the target company by using discounted free cash flow method

Discounted cash flow method: It is known as one of the effective method that is used by

the company to estimate the value of an investment based on their future cash flows. This

analysis is being done to determine the current value of expected future cash use by a T group

plc on a discount rate. This particular evaluation has been done to examine the value of a

company total asset that has based on value of money it can be going to make in coming future

time (Dickinson, 2011). It is a simple valuation technique that is especially for companies those

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

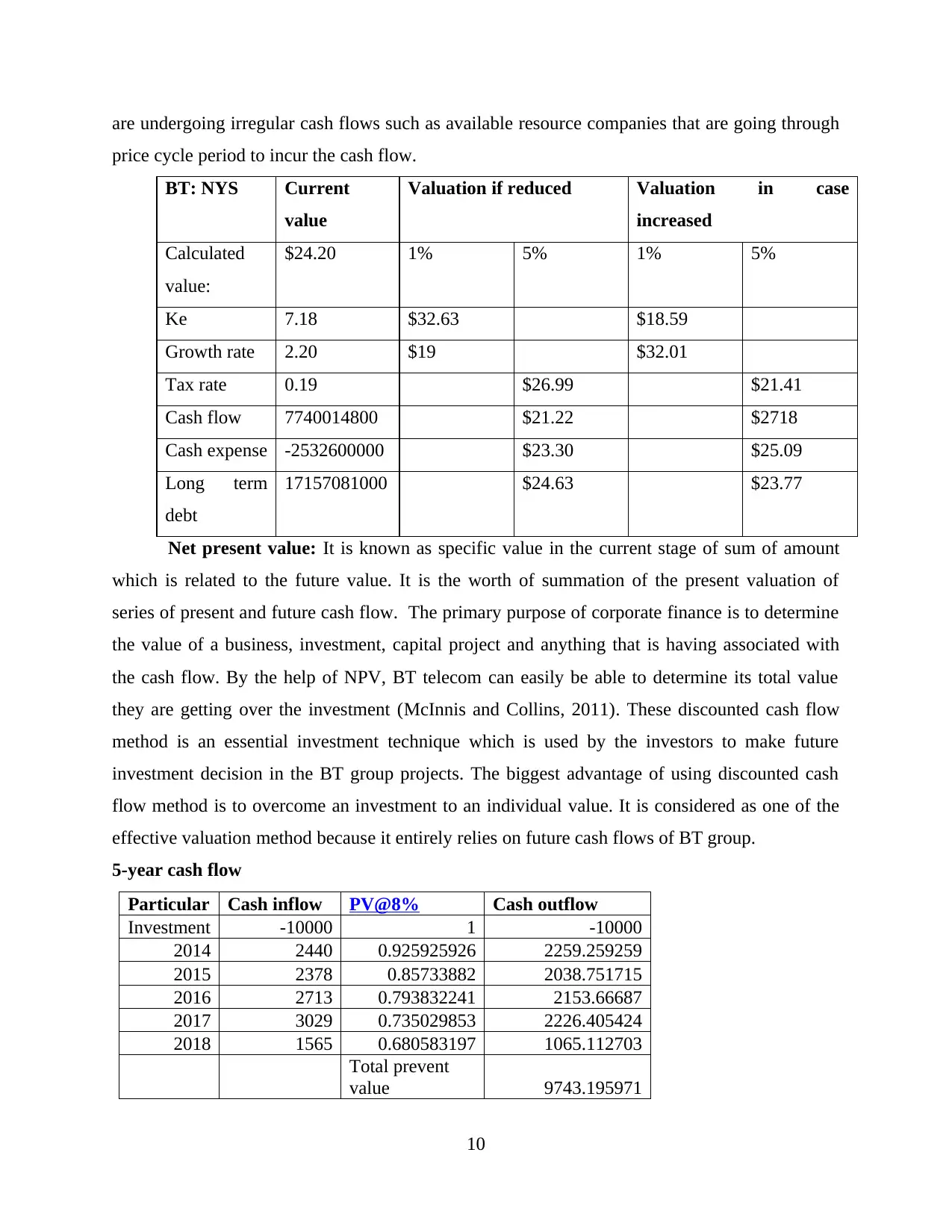

are undergoing irregular cash flows such as available resource companies that are going through

price cycle period to incur the cash flow.

BT: NYS Current

value

Valuation if reduced Valuation in case

increased

Calculated

value:

$24.20 1% 5% 1% 5%

Ke 7.18 $32.63 $18.59

Growth rate 2.20 $19 $32.01

Tax rate 0.19 $26.99 $21.41

Cash flow 7740014800 $21.22 $2718

Cash expense -2532600000 $23.30 $25.09

Long term

debt

17157081000 $24.63 $23.77

Net present value: It is known as specific value in the current stage of sum of amount

which is related to the future value. It is the worth of summation of the present valuation of

series of present and future cash flow. The primary purpose of corporate finance is to determine

the value of a business, investment, capital project and anything that is having associated with

the cash flow. By the help of NPV, BT telecom can easily be able to determine its total value

they are getting over the investment (McInnis and Collins, 2011). These discounted cash flow

method is an essential investment technique which is used by the investors to make future

investment decision in the BT group projects. The biggest advantage of using discounted cash

flow method is to overcome an investment to an individual value. It is considered as one of the

effective valuation method because it entirely relies on future cash flows of BT group.

5-year cash flow

Particular Cash inflow PV@8% Cash outflow

Investment -10000 1 -10000

2014 2440 0.925925926 2259.259259

2015 2378 0.85733882 2038.751715

2016 2713 0.793832241 2153.66687

2017 3029 0.735029853 2226.405424

2018 1565 0.680583197 1065.112703

Total prevent

value 9743.195971

10

price cycle period to incur the cash flow.

BT: NYS Current

value

Valuation if reduced Valuation in case

increased

Calculated

value:

$24.20 1% 5% 1% 5%

Ke 7.18 $32.63 $18.59

Growth rate 2.20 $19 $32.01

Tax rate 0.19 $26.99 $21.41

Cash flow 7740014800 $21.22 $2718

Cash expense -2532600000 $23.30 $25.09

Long term

debt

17157081000 $24.63 $23.77

Net present value: It is known as specific value in the current stage of sum of amount

which is related to the future value. It is the worth of summation of the present valuation of

series of present and future cash flow. The primary purpose of corporate finance is to determine

the value of a business, investment, capital project and anything that is having associated with

the cash flow. By the help of NPV, BT telecom can easily be able to determine its total value

they are getting over the investment (McInnis and Collins, 2011). These discounted cash flow

method is an essential investment technique which is used by the investors to make future

investment decision in the BT group projects. The biggest advantage of using discounted cash

flow method is to overcome an investment to an individual value. It is considered as one of the

effective valuation method because it entirely relies on future cash flows of BT group.

5-year cash flow

Particular Cash inflow PV@8% Cash outflow

Investment -10000 1 -10000

2014 2440 0.925925926 2259.259259

2015 2378 0.85733882 2038.751715

2016 2713 0.793832241 2153.66687

2017 3029 0.735029853 2226.405424

2018 1565 0.680583197 1065.112703

Total prevent

value 9743.195971

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net present

value 256.804029

From the above calculation, it has been seen that BT book value is 10000 as initial

investment during the year. At the same time, the discounted cash flow statement is calculated

with taking a present value of 8%. It has been clearly analyse that the net present value

calculated from the respective cash flows till 2018 is positive 256 billion. It means that the value

of revenue which is cash inflow is maximum than the cash outflow. In case the earning is greater

than cost, the investor used to make a valuable profit in coming period of time.

BT group book value and market capitalization:

According to the current price of BT group plc is $15.18, whereas its book value of per

share for the quarter of 2018 was analyse as 7.20. The value of prices for one share of stock is set

through buyer and sellers in the overall market. Share prices would be used to determine a

company’s total market value which is represented by market capitalization. Investors is

basically buy a stock which mean that they feel undervalued and sell those stock in case they feel

it overvalued. Market cap is said to be measurement of business has been valued that has been

based on share prices as well as number of share remain outstanding. It is commonly represents

as the market point of view of BT group plc stock value (Singh, 2015).

BT company has 1.5 million of total share which remain outstanding at a price of $25,

there market cap is 37.5 million. It is one of the basic characteristic that assists an investor to

analyse the total return and risk they are getting from their total share (Market Cap, 2018). BT

group pvt ltd is planning to analyse the market over the next coming few years as technology and

customer require changes. In case of broadband market share within BT group the total retail

share of net asset is around 22% in 2018, whereas retail share of installed base is examine as

45% in the same period. The net book value of BT group share of assets tends to controlled

through their join operation and recorded within infrastructure. The five year chances in prices

for BT telecom group has been presented below:

Year BT.A S&P 500

2014 16.8 18.6

2015 17.2 19

2016 12.7 20.3

2017 17.2 22.9

2018 10.5 17.2

11

value 256.804029

From the above calculation, it has been seen that BT book value is 10000 as initial

investment during the year. At the same time, the discounted cash flow statement is calculated

with taking a present value of 8%. It has been clearly analyse that the net present value

calculated from the respective cash flows till 2018 is positive 256 billion. It means that the value

of revenue which is cash inflow is maximum than the cash outflow. In case the earning is greater

than cost, the investor used to make a valuable profit in coming period of time.

BT group book value and market capitalization:

According to the current price of BT group plc is $15.18, whereas its book value of per

share for the quarter of 2018 was analyse as 7.20. The value of prices for one share of stock is set

through buyer and sellers in the overall market. Share prices would be used to determine a

company’s total market value which is represented by market capitalization. Investors is

basically buy a stock which mean that they feel undervalued and sell those stock in case they feel

it overvalued. Market cap is said to be measurement of business has been valued that has been

based on share prices as well as number of share remain outstanding. It is commonly represents

as the market point of view of BT group plc stock value (Singh, 2015).

BT company has 1.5 million of total share which remain outstanding at a price of $25,

there market cap is 37.5 million. It is one of the basic characteristic that assists an investor to

analyse the total return and risk they are getting from their total share (Market Cap, 2018). BT

group pvt ltd is planning to analyse the market over the next coming few years as technology and

customer require changes. In case of broadband market share within BT group the total retail

share of net asset is around 22% in 2018, whereas retail share of installed base is examine as

45% in the same period. The net book value of BT group share of assets tends to controlled

through their join operation and recorded within infrastructure. The five year chances in prices

for BT telecom group has been presented below:

Year BT.A S&P 500

2014 16.8 18.6

2015 17.2 19

2016 12.7 20.3

2017 17.2 22.9

2018 10.5 17.2

11

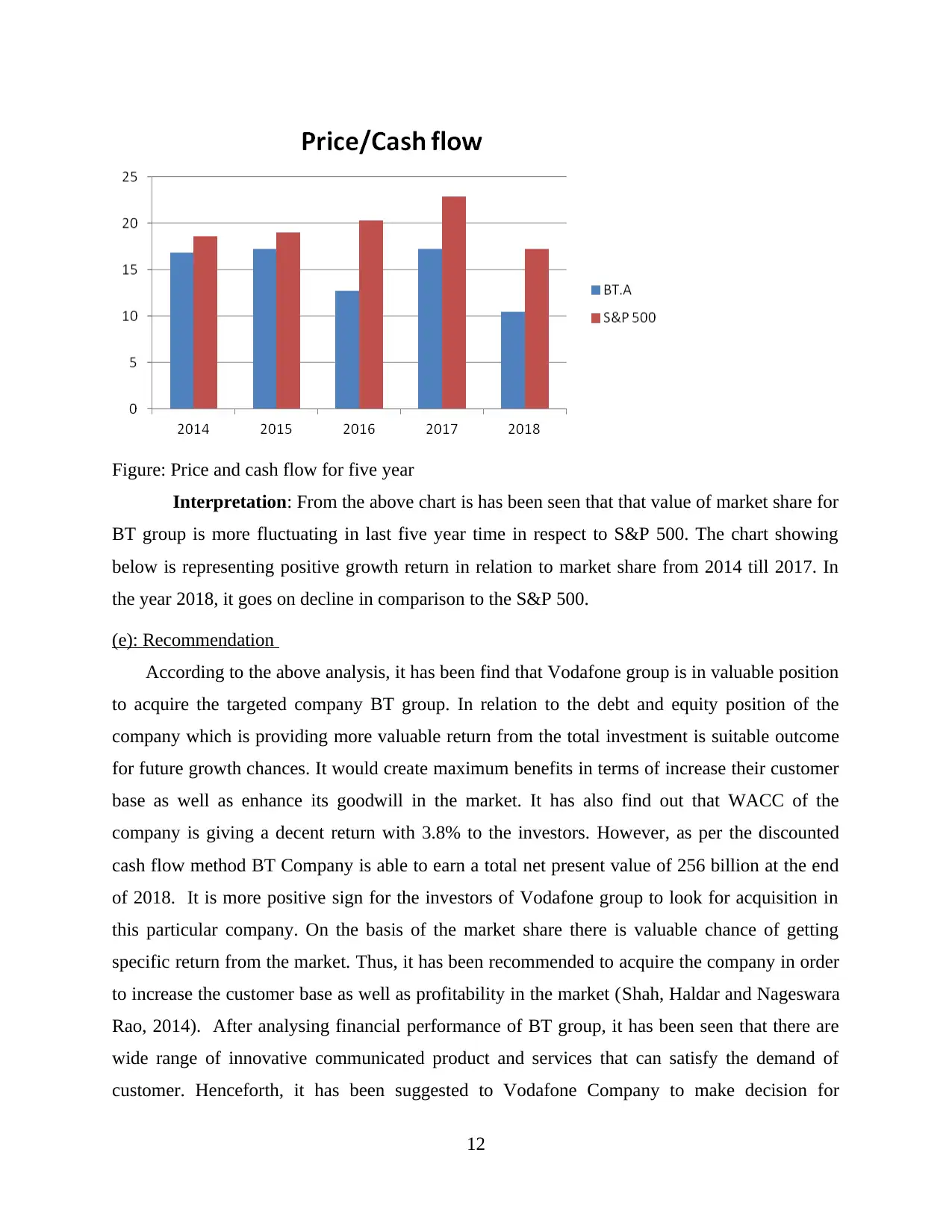

Figure: Price and cash flow for five year

Interpretation: From the above chart is has been seen that that value of market share for

BT group is more fluctuating in last five year time in respect to S&P 500. The chart showing

below is representing positive growth return in relation to market share from 2014 till 2017. In

the year 2018, it goes on decline in comparison to the S&P 500.

(e): Recommendation

According to the above analysis, it has been find that Vodafone group is in valuable position

to acquire the targeted company BT group. In relation to the debt and equity position of the

company which is providing more valuable return from the total investment is suitable outcome

for future growth chances. It would create maximum benefits in terms of increase their customer

base as well as enhance its goodwill in the market. It has also find out that WACC of the

company is giving a decent return with 3.8% to the investors. However, as per the discounted

cash flow method BT Company is able to earn a total net present value of 256 billion at the end

of 2018. It is more positive sign for the investors of Vodafone group to look for acquisition in

this particular company. On the basis of the market share there is valuable chance of getting

specific return from the market. Thus, it has been recommended to acquire the company in order

to increase the customer base as well as profitability in the market (Shah, Haldar and Nageswara

Rao, 2014). After analysing financial performance of BT group, it has been seen that there are

wide range of innovative communicated product and services that can satisfy the demand of

customer. Henceforth, it has been suggested to Vodafone Company to make decision for

12

Interpretation: From the above chart is has been seen that that value of market share for

BT group is more fluctuating in last five year time in respect to S&P 500. The chart showing

below is representing positive growth return in relation to market share from 2014 till 2017. In

the year 2018, it goes on decline in comparison to the S&P 500.

(e): Recommendation

According to the above analysis, it has been find that Vodafone group is in valuable position

to acquire the targeted company BT group. In relation to the debt and equity position of the

company which is providing more valuable return from the total investment is suitable outcome

for future growth chances. It would create maximum benefits in terms of increase their customer

base as well as enhance its goodwill in the market. It has also find out that WACC of the

company is giving a decent return with 3.8% to the investors. However, as per the discounted

cash flow method BT Company is able to earn a total net present value of 256 billion at the end

of 2018. It is more positive sign for the investors of Vodafone group to look for acquisition in

this particular company. On the basis of the market share there is valuable chance of getting

specific return from the market. Thus, it has been recommended to acquire the company in order

to increase the customer base as well as profitability in the market (Shah, Haldar and Nageswara

Rao, 2014). After analysing financial performance of BT group, it has been seen that there are

wide range of innovative communicated product and services that can satisfy the demand of

customer. Henceforth, it has been suggested to Vodafone Company to make decision for

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.