Comprehensive Solution for Corporate Accounting and Reporting Problems

VerifiedAdded on 2020/05/28

|7

|699

|92

Homework Assignment

AI Summary

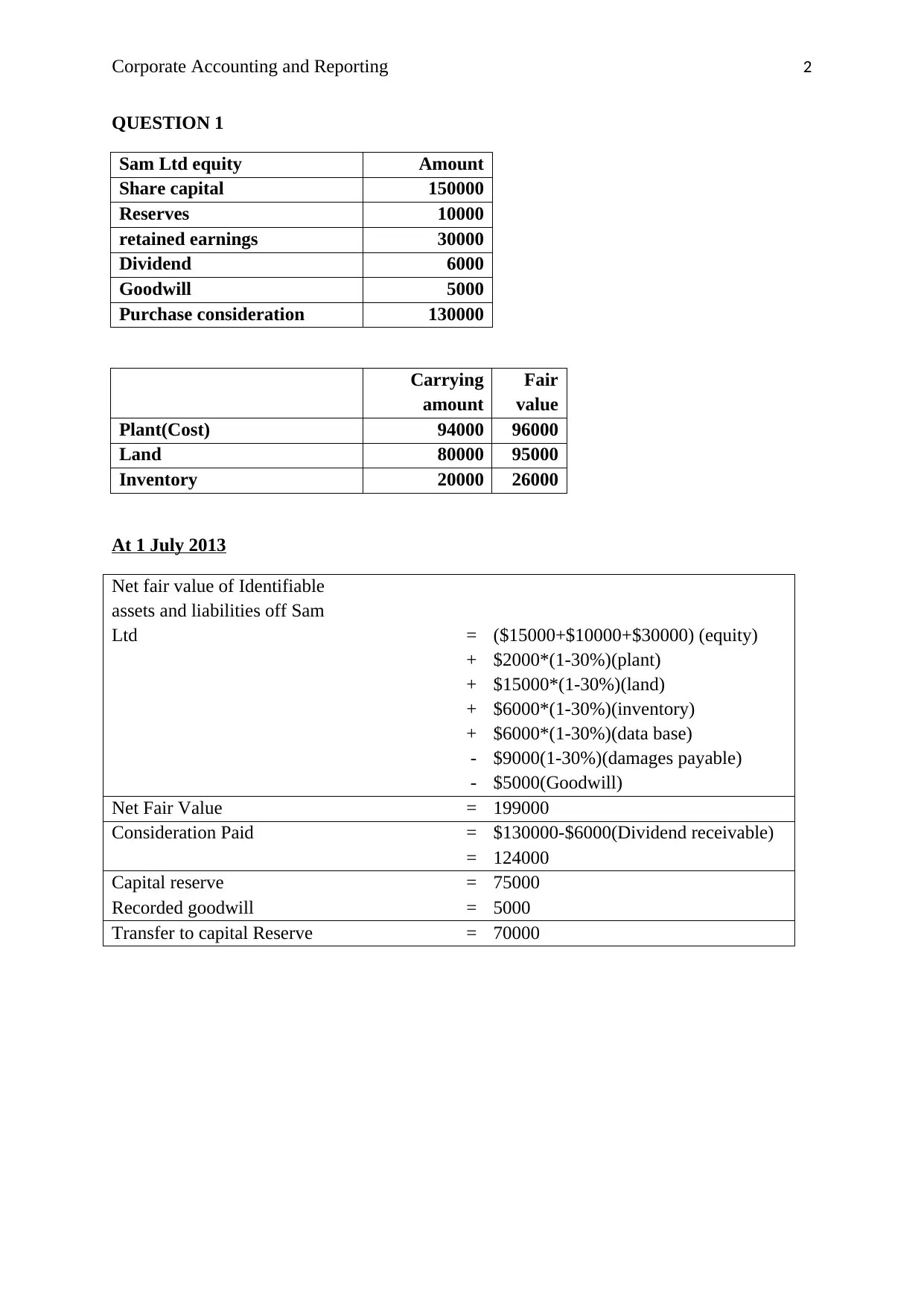

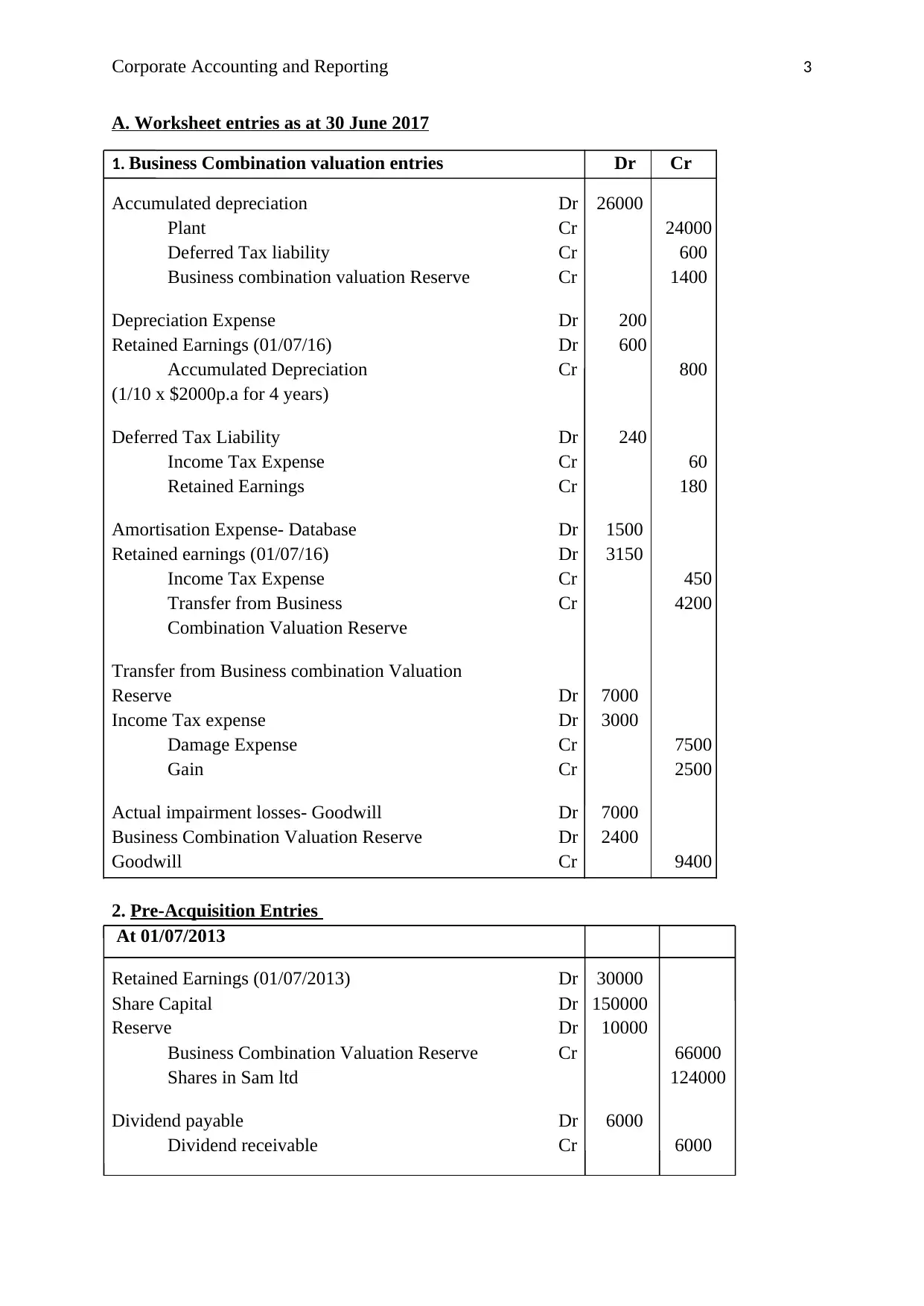

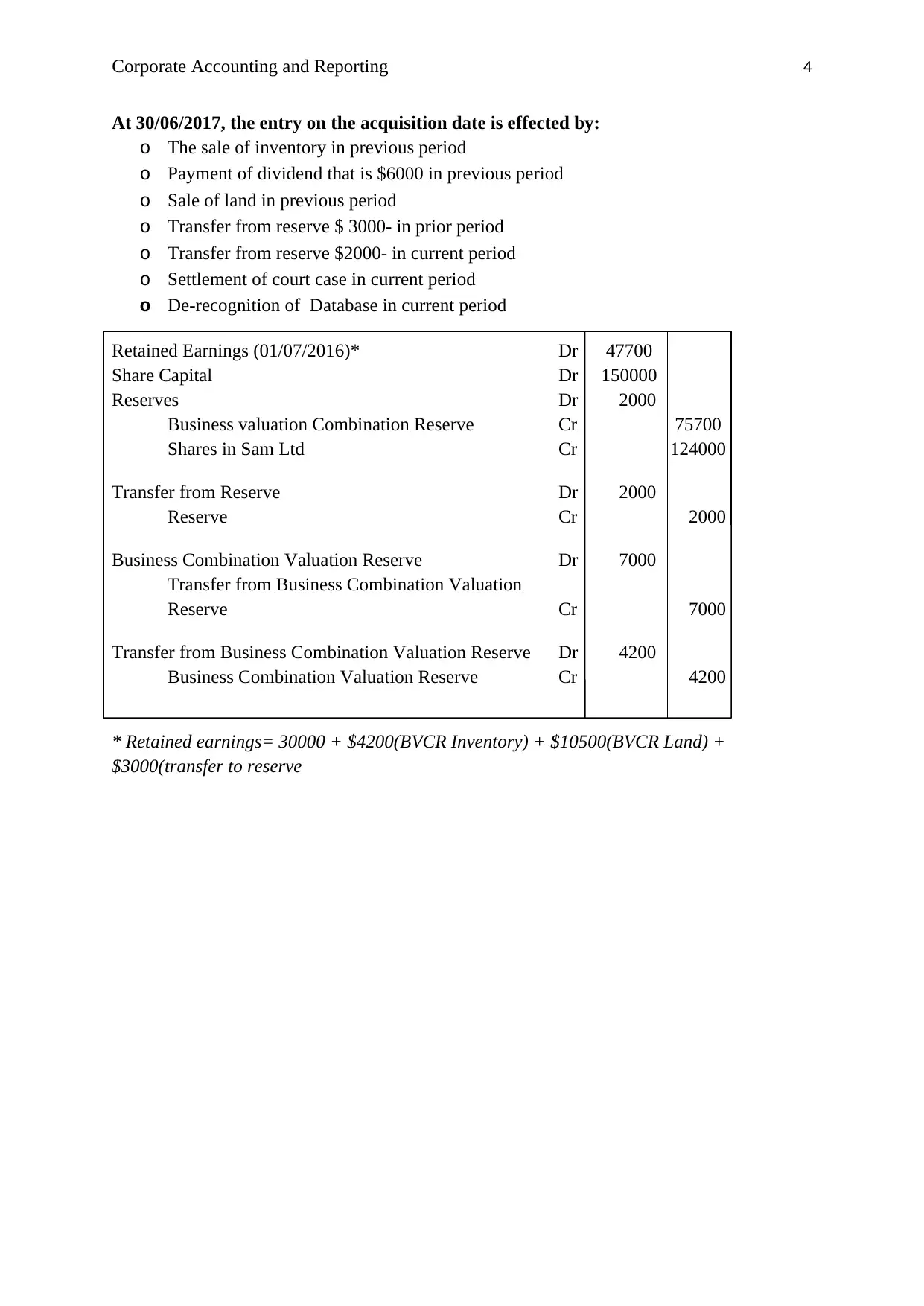

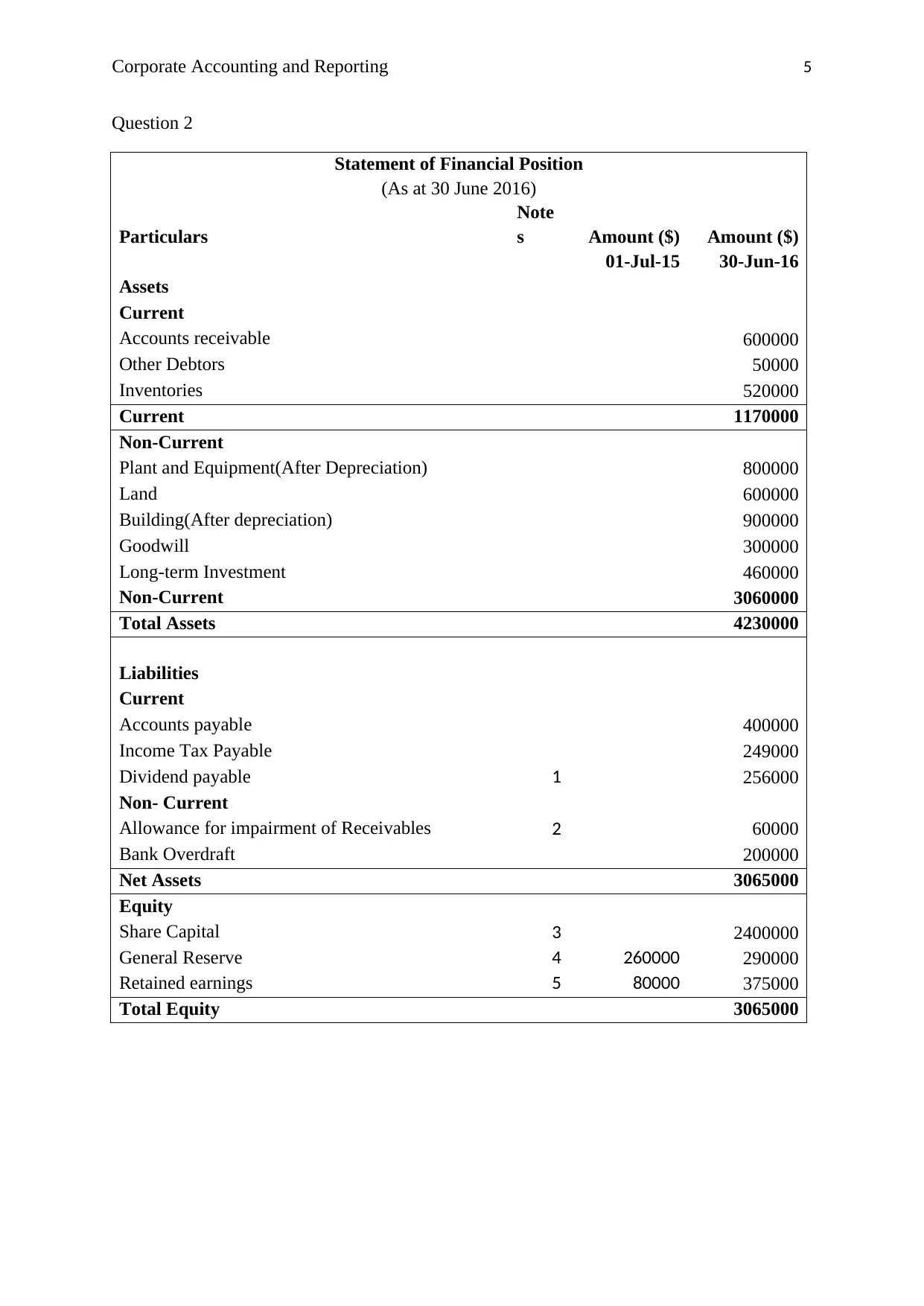

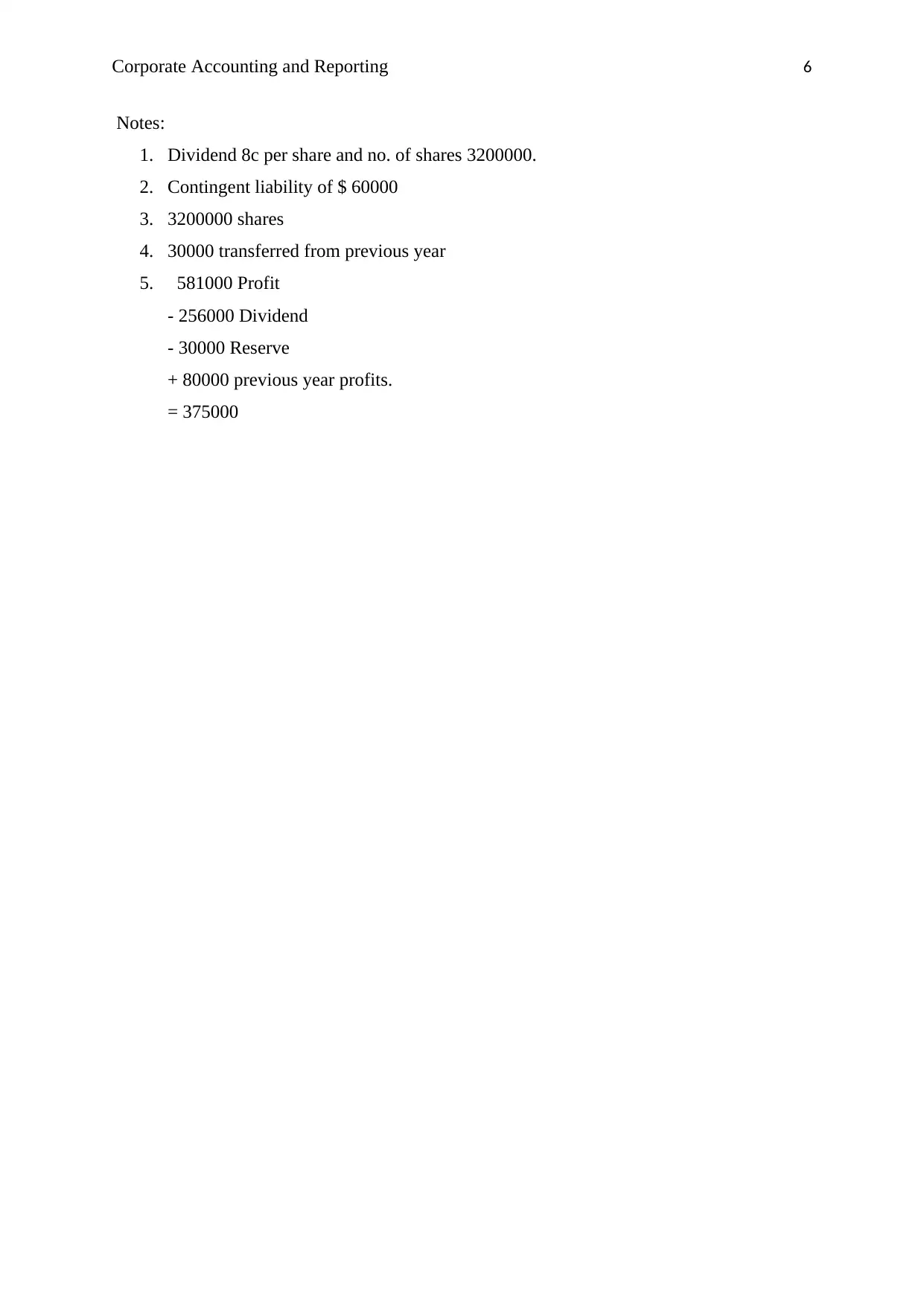

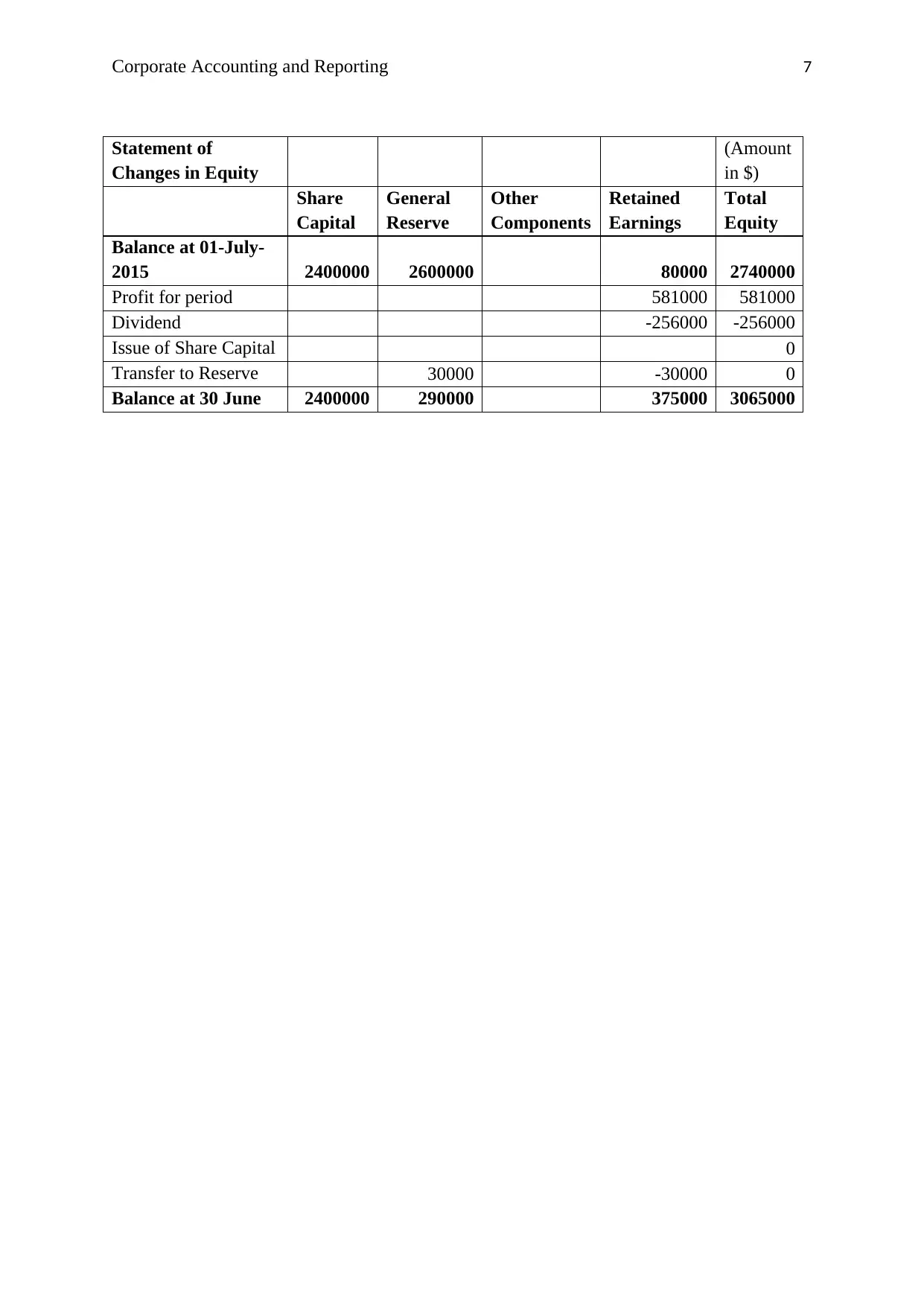

This document presents a comprehensive solution to a corporate accounting and reporting assignment. The solution addresses two key questions. The first question involves a business combination scenario, requiring the calculation of net fair value, consideration paid, and the preparation of worksheet entries. It also includes pre-acquisition entries, and adjustments for depreciation, deferred tax, and goodwill impairment. The second question focuses on the preparation of a Statement of Financial Position and a Statement of Changes in Equity, with detailed notes and calculations. The solution demonstrates the application of accounting principles to analyze financial data and prepare accurate financial statements.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.