ACCT20074 Term 2: Corporate Social Responsibility Report Analysis

VerifiedAdded on 2022/09/29

|15

|3312

|22

Report

AI Summary

This report provides a comprehensive analysis of corporate social responsibility (CSR) and sustainability reporting. It begins with an executive summary and an introduction that highlights the increasing importance of CSR in the business environment. The report explores the significance of CSR, sustainable reporting, and the ethical theories (Utilitarianism and Deontology) underpinning these concepts. It then focuses on Spark New Zealand Limited as a case study, examining its CSR activities and reporting practices in light of the Global Reporting Initiative (GRI) guidelines. The analysis includes a detailed scoring index based on GRI standards to evaluate the extent and quality of Spark New Zealand Limited's sustainability reporting. The report concludes by summarizing the key findings and implications of the analysis, offering insights into the company's approach to social responsibility and its adherence to established reporting frameworks. The report aims to provide a holistic view of CSR and its practical application in a real-world business context.

CONTEMPORARY ACCOUNTING THEORY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The organisations engage in wide range of the corporate social responsibility

practices, through the partner agencies or on their own in light of the regulatory compliance

or to improve the image. It is imperative to note that as per the industry and region of

operation of an enterprise, various guidelines have been issued for the amount and manner of

the corporate social responsibility activities. The ethical theories also support the sustainable

reporting principles. The report engages in the theoretical research of the various facets of

corporate social responsibility and sustainable reporting in the modern businesses. The report

further engages in the application of the theoretical knowledge to the practical scenario in

terms of the evaluation of the CSR activities and reporting of the Spark New Zealand

Limited, in light of the GRI principles.

The organisations engage in wide range of the corporate social responsibility

practices, through the partner agencies or on their own in light of the regulatory compliance

or to improve the image. It is imperative to note that as per the industry and region of

operation of an enterprise, various guidelines have been issued for the amount and manner of

the corporate social responsibility activities. The ethical theories also support the sustainable

reporting principles. The report engages in the theoretical research of the various facets of

corporate social responsibility and sustainable reporting in the modern businesses. The report

further engages in the application of the theoretical knowledge to the practical scenario in

terms of the evaluation of the CSR activities and reporting of the Spark New Zealand

Limited, in light of the GRI principles.

Contents

Introduction................................................................................................................................3

Significance of corporate social responsibility..........................................................................3

Sustainable Reporting representing the holistic view of the corporate social responsibility.....4

Theories representing the essence of sustainable reporting.......................................................5

Overview of the company..........................................................................................................6

Sustainability reporting (disclosure) scoring index according to the Global Reporting

Initiative (GRI) guidelines.........................................................................................................7

Extent and Quality of Sustainable Reporting of the company Spark New Zealand Limited....8

Conclusion................................................................................................................................12

References................................................................................................................................13

Introduction................................................................................................................................3

Significance of corporate social responsibility..........................................................................3

Sustainable Reporting representing the holistic view of the corporate social responsibility.....4

Theories representing the essence of sustainable reporting.......................................................5

Overview of the company..........................................................................................................6

Sustainability reporting (disclosure) scoring index according to the Global Reporting

Initiative (GRI) guidelines.........................................................................................................7

Extent and Quality of Sustainable Reporting of the company Spark New Zealand Limited....8

Conclusion................................................................................................................................12

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

With the increased complexities in the business environment and the corporate

scandals and collapses coming into light, there has been placed an enhanced responsibility on

the entities to be considerate of the welfares of the stakeholder groups and not just

concentrate on the revenue earning objectives. The term corporate social responsibility

denotes the accountability of the company towards the society and various associated

members in the light of the environmental, economic and social responsibilities (Schwartz,

2011).

The following assignment is aimed at examining the various aspect of the corporate

social responsibility in light of the case study of the company Spark New Zealand Limited

(SPK, formerly Telecom Corporation of New Zealand Limited). The concept of the

sustainability reporting and corporate social responsibility would be studied in detail with the

aid of the literature and the theories. Further, the report would involve the application of the

insights gained from the literature to the financial statements of the said company to conclude

on the extent and quality of the social responsibility fulfilment by the company.

Significance of Corporate Social Responsibility (CSR)

Bowen (1953), had stated the meaning of the corporate social responsibility in the

book “Social Responsibilities of the Businessman”, as the framework of the obligations

required to be adhered to by the enterprises, which included the designing of the policies and

undertaking decisions that extend the goals and values of the society of the wellbeing of

various members of society (Moon, 2014). As per the work of Chaffee (2017), the evolution

of the social responsibility principles can be traced back to the earlier Roman laws and

English laws as well that regarded the corporations as an tool for societal development.

Gradually over the years, the concept of the corporate social responsibility has been widened

considerably to include aligning the aspirations of the stakeholders with the corporate

objectives (Tricker, 2015). Some of the societal concerns that have formed the part of the

corporate social responsibility principles are that of rapid population growth, pollution, and

issue of the resource depletion, which are a matter of concern for almost every nation. The

growing significance of the corporate social responsibility can be traced in the fact that

numerous international and national organisations have been formed to address the various

societal concerns (Zientara, 2017). Some of the organisations are the “UN Global Compact,”

With the increased complexities in the business environment and the corporate

scandals and collapses coming into light, there has been placed an enhanced responsibility on

the entities to be considerate of the welfares of the stakeholder groups and not just

concentrate on the revenue earning objectives. The term corporate social responsibility

denotes the accountability of the company towards the society and various associated

members in the light of the environmental, economic and social responsibilities (Schwartz,

2011).

The following assignment is aimed at examining the various aspect of the corporate

social responsibility in light of the case study of the company Spark New Zealand Limited

(SPK, formerly Telecom Corporation of New Zealand Limited). The concept of the

sustainability reporting and corporate social responsibility would be studied in detail with the

aid of the literature and the theories. Further, the report would involve the application of the

insights gained from the literature to the financial statements of the said company to conclude

on the extent and quality of the social responsibility fulfilment by the company.

Significance of Corporate Social Responsibility (CSR)

Bowen (1953), had stated the meaning of the corporate social responsibility in the

book “Social Responsibilities of the Businessman”, as the framework of the obligations

required to be adhered to by the enterprises, which included the designing of the policies and

undertaking decisions that extend the goals and values of the society of the wellbeing of

various members of society (Moon, 2014). As per the work of Chaffee (2017), the evolution

of the social responsibility principles can be traced back to the earlier Roman laws and

English laws as well that regarded the corporations as an tool for societal development.

Gradually over the years, the concept of the corporate social responsibility has been widened

considerably to include aligning the aspirations of the stakeholders with the corporate

objectives (Tricker, 2015). Some of the societal concerns that have formed the part of the

corporate social responsibility principles are that of rapid population growth, pollution, and

issue of the resource depletion, which are a matter of concern for almost every nation. The

growing significance of the corporate social responsibility can be traced in the fact that

numerous international and national organisations have been formed to address the various

societal concerns (Zientara, 2017). Some of the organisations are the “UN Global Compact,”

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the “Global Reporting Initiative”, and the “World Business Council for Sustainable

Development”, the “Organization for Economic cooperation and development”, the

“International Organization for Standardization” and others. The principles and guidelines of

these organisations facilitate and guide the entities towards the best approaches for the

entities in being transparent, fair and accountable while carrying out the revenue earning

objectives. Hence, it can be stated that the principles of the CSR have evolved extensively.

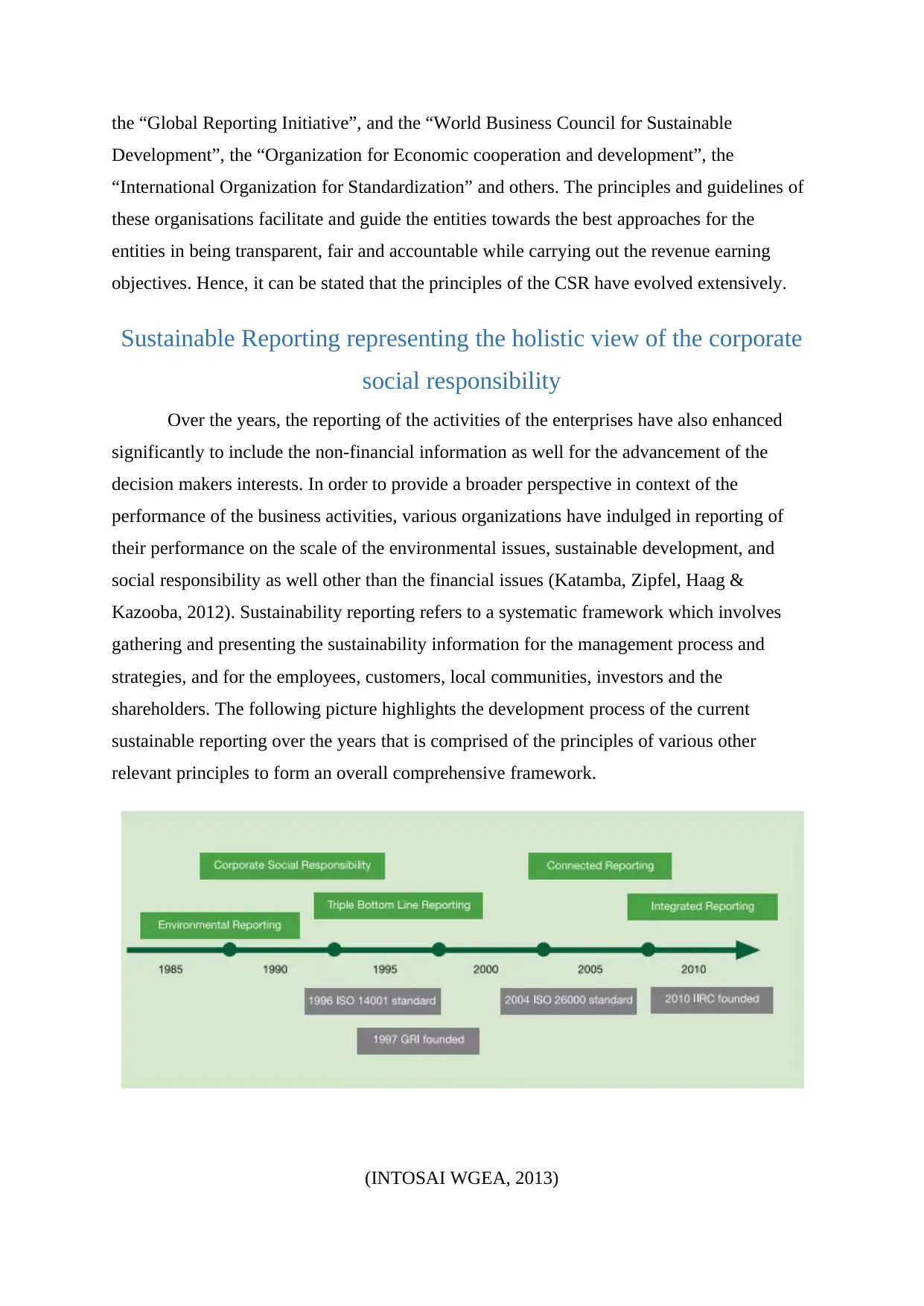

Sustainable Reporting representing the holistic view of the corporate

social responsibility

Over the years, the reporting of the activities of the enterprises have also enhanced

significantly to include the non-financial information as well for the advancement of the

decision makers interests. In order to provide a broader perspective in context of the

performance of the business activities, various organizations have indulged in reporting of

their performance on the scale of the environmental issues, sustainable development, and

social responsibility as well other than the financial issues (Katamba, Zipfel, Haag &

Kazooba, 2012). Sustainability reporting refers to a systematic framework which involves

gathering and presenting the sustainability information for the management process and

strategies, and for the employees, customers, local communities, investors and the

shareholders. The following picture highlights the development process of the current

sustainable reporting over the years that is comprised of the principles of various other

relevant principles to form an overall comprehensive framework.

(INTOSAI WGEA, 2013)

Development”, the “Organization for Economic cooperation and development”, the

“International Organization for Standardization” and others. The principles and guidelines of

these organisations facilitate and guide the entities towards the best approaches for the

entities in being transparent, fair and accountable while carrying out the revenue earning

objectives. Hence, it can be stated that the principles of the CSR have evolved extensively.

Sustainable Reporting representing the holistic view of the corporate

social responsibility

Over the years, the reporting of the activities of the enterprises have also enhanced

significantly to include the non-financial information as well for the advancement of the

decision makers interests. In order to provide a broader perspective in context of the

performance of the business activities, various organizations have indulged in reporting of

their performance on the scale of the environmental issues, sustainable development, and

social responsibility as well other than the financial issues (Katamba, Zipfel, Haag &

Kazooba, 2012). Sustainability reporting refers to a systematic framework which involves

gathering and presenting the sustainability information for the management process and

strategies, and for the employees, customers, local communities, investors and the

shareholders. The following picture highlights the development process of the current

sustainable reporting over the years that is comprised of the principles of various other

relevant principles to form an overall comprehensive framework.

(INTOSAI WGEA, 2013)

From the picture depicted above, it is evident that what started with the concentration

on the environmental reporting only, gradually involved the need and the principles of the

triple bottom line where three pillars were the people, planet and profit (INTOSAI WGEA,

2013). The 1990s further witnesses the development of a voluntary sustainability reporting

framework under Global Reporting Initiative (GRI). Further, the individual countries also

developed their respective principles for the improvement of the annual reports and accounts.

Eventually, the sustainable reporting principles also included the disclosure of the issues

related to organizational governance, fair employment practices, consideration of the human

rights and the labor practices, consumer issues, community involvement apart from the

environmental concerns such as the climate change, carbon contribution and others.

Today, various organizations are not only providing the said information in an attempt

to improve their reputations in light of the consideration of the societal issues, while others

report as part of the mandatory frameworks. Some of the aspects that form the content of the

sustainable reporting are listed as follows. The sustainable reporting principles demand the

reporting of the financial as well as the non-financial information of the energy use, water

usage, waste generation and various aspects of the procurements. Hence, it can be stated that

the sustainable reporting has become a significant tool in the presentation of the holistic view

of corporate social responsibility, which now includes a number of aspects and

responsibilities to be disclosed.

Theories representing the essence of sustainable reporting

The following segment of the report sheds light on the principles of two of the many

available theories that lead to the explanation of the gist or the rationale of the sustainable

reporting. Numerous philosophers have developed various ethical theories to provide the

guiding principles that facilitate an efficient conduct from the individuals as well as the

business organisations. These theories are aimed at overall social wellbeing in the decision

making (Scalet, 2018). While some theories stress on the performance of the duties, some are

focussed towards the outcomes of the decisions, to regard an act as ethical or unethical.

One of the most popular and chief ethical theories is of the ethical theory of

utilitarianism. The said theory of ethics is based on the belief that the mass interests must be

considered at the time of decision-making and the same should lead to the general happiness

or utility and not be concentrated only to the fulfilment of the individual interests only

(Hollander, 2016). On application of the above principles to the nature of the sustainable

on the environmental reporting only, gradually involved the need and the principles of the

triple bottom line where three pillars were the people, planet and profit (INTOSAI WGEA,

2013). The 1990s further witnesses the development of a voluntary sustainability reporting

framework under Global Reporting Initiative (GRI). Further, the individual countries also

developed their respective principles for the improvement of the annual reports and accounts.

Eventually, the sustainable reporting principles also included the disclosure of the issues

related to organizational governance, fair employment practices, consideration of the human

rights and the labor practices, consumer issues, community involvement apart from the

environmental concerns such as the climate change, carbon contribution and others.

Today, various organizations are not only providing the said information in an attempt

to improve their reputations in light of the consideration of the societal issues, while others

report as part of the mandatory frameworks. Some of the aspects that form the content of the

sustainable reporting are listed as follows. The sustainable reporting principles demand the

reporting of the financial as well as the non-financial information of the energy use, water

usage, waste generation and various aspects of the procurements. Hence, it can be stated that

the sustainable reporting has become a significant tool in the presentation of the holistic view

of corporate social responsibility, which now includes a number of aspects and

responsibilities to be disclosed.

Theories representing the essence of sustainable reporting

The following segment of the report sheds light on the principles of two of the many

available theories that lead to the explanation of the gist or the rationale of the sustainable

reporting. Numerous philosophers have developed various ethical theories to provide the

guiding principles that facilitate an efficient conduct from the individuals as well as the

business organisations. These theories are aimed at overall social wellbeing in the decision

making (Scalet, 2018). While some theories stress on the performance of the duties, some are

focussed towards the outcomes of the decisions, to regard an act as ethical or unethical.

One of the most popular and chief ethical theories is of the ethical theory of

utilitarianism. The said theory of ethics is based on the belief that the mass interests must be

considered at the time of decision-making and the same should lead to the general happiness

or utility and not be concentrated only to the fulfilment of the individual interests only

(Hollander, 2016). On application of the above principles to the nature of the sustainable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reporting, it can be stated that principles of sustainable reporting are aimed at providing

information to the interests of the every stakeholder group of the entity and not just the

shareholders (Barry, 2016). The information presented therein aids the investors and

regulators as well for the various decisions.

Yet another popular ethical theory whose father is regarded as Immanuel Kant is that

of Deontology also known as the Kantian analysis. The principles of the theory state that

legitimacy of the actions must be judged in the light of the moral principles, and the

consequences are not of much importance under said scenario. The theory is based on the

belief that if the ethical and moral guidelines are sufficiently considered at the time of making

decisions and the performance of the acts, there will be an spontaneous refinement in the

consequences as well (Vadastreanu, Maier & Maier, 2015). Thus, the theory calls for the

management of the companies to not be deviated from individual emotions, conflicts of the

interests and personal inclinations at the time of making business decisions for the

stakeholders group as a whole. In business scenario, the moral duties of the businesses calls

for the provision of the safe products to consumers, provision of the transparent information

to shareholders and investors, safeguarding the environment by engaging into sustainable

business practices, and providing safe working conditions to the employees (Chandler, 2019).

In context of the duties, various corporate frameworks have further prescribed mandatory

duties to act and present information in best interests of the stakeholders. Hence, as the

management of the organisations engage into various sustainable reporting practices and also

report the same in the financial reports, they are complying with their legally prescribed

duties and best practice guidelines. Consequently, the said compliances would lead to the

overall social well-being.

Hence, the above discussions elaborate the gist of the sustainable reporting to be the

conduct of the business in a way to be considerate of the interests of the various stakeholders

and providing information in a transparent and accountable manner.

Overview of the company

The company chosen for the analysis of the various aspects of the sustainability

reporting is the Spark New Zealand Limited. The stated organisation is based out of New

Zealand and is the supplier of telecommunications and digital services. The three chief

segments of operation for the entity are Spark Home, Mobile & Business; Spark Connect and

the Spark Digital. The segment named Spark Home, Mobile & Business is engaged in the

information to the interests of the every stakeholder group of the entity and not just the

shareholders (Barry, 2016). The information presented therein aids the investors and

regulators as well for the various decisions.

Yet another popular ethical theory whose father is regarded as Immanuel Kant is that

of Deontology also known as the Kantian analysis. The principles of the theory state that

legitimacy of the actions must be judged in the light of the moral principles, and the

consequences are not of much importance under said scenario. The theory is based on the

belief that if the ethical and moral guidelines are sufficiently considered at the time of making

decisions and the performance of the acts, there will be an spontaneous refinement in the

consequences as well (Vadastreanu, Maier & Maier, 2015). Thus, the theory calls for the

management of the companies to not be deviated from individual emotions, conflicts of the

interests and personal inclinations at the time of making business decisions for the

stakeholders group as a whole. In business scenario, the moral duties of the businesses calls

for the provision of the safe products to consumers, provision of the transparent information

to shareholders and investors, safeguarding the environment by engaging into sustainable

business practices, and providing safe working conditions to the employees (Chandler, 2019).

In context of the duties, various corporate frameworks have further prescribed mandatory

duties to act and present information in best interests of the stakeholders. Hence, as the

management of the organisations engage into various sustainable reporting practices and also

report the same in the financial reports, they are complying with their legally prescribed

duties and best practice guidelines. Consequently, the said compliances would lead to the

overall social well-being.

Hence, the above discussions elaborate the gist of the sustainable reporting to be the

conduct of the business in a way to be considerate of the interests of the various stakeholders

and providing information in a transparent and accountable manner.

Overview of the company

The company chosen for the analysis of the various aspects of the sustainability

reporting is the Spark New Zealand Limited. The stated organisation is based out of New

Zealand and is the supplier of telecommunications and digital services. The three chief

segments of operation for the entity are Spark Home, Mobile & Business; Spark Connect and

the Spark Digital. The segment named Spark Home, Mobile & Business is engaged in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

provision of the fixed line, Internet and Mobile services. The said provision is done to the

home consumers as well as the small medium business market. The second segment namely

the Spark Digital segment is engaged in the integration of the information technology (IT)

and telecommunications services and thus provides various information and communications

technology (ICT) solutions to the clients. The third and last segment Spark Connect provides

services of the network and IT operations.

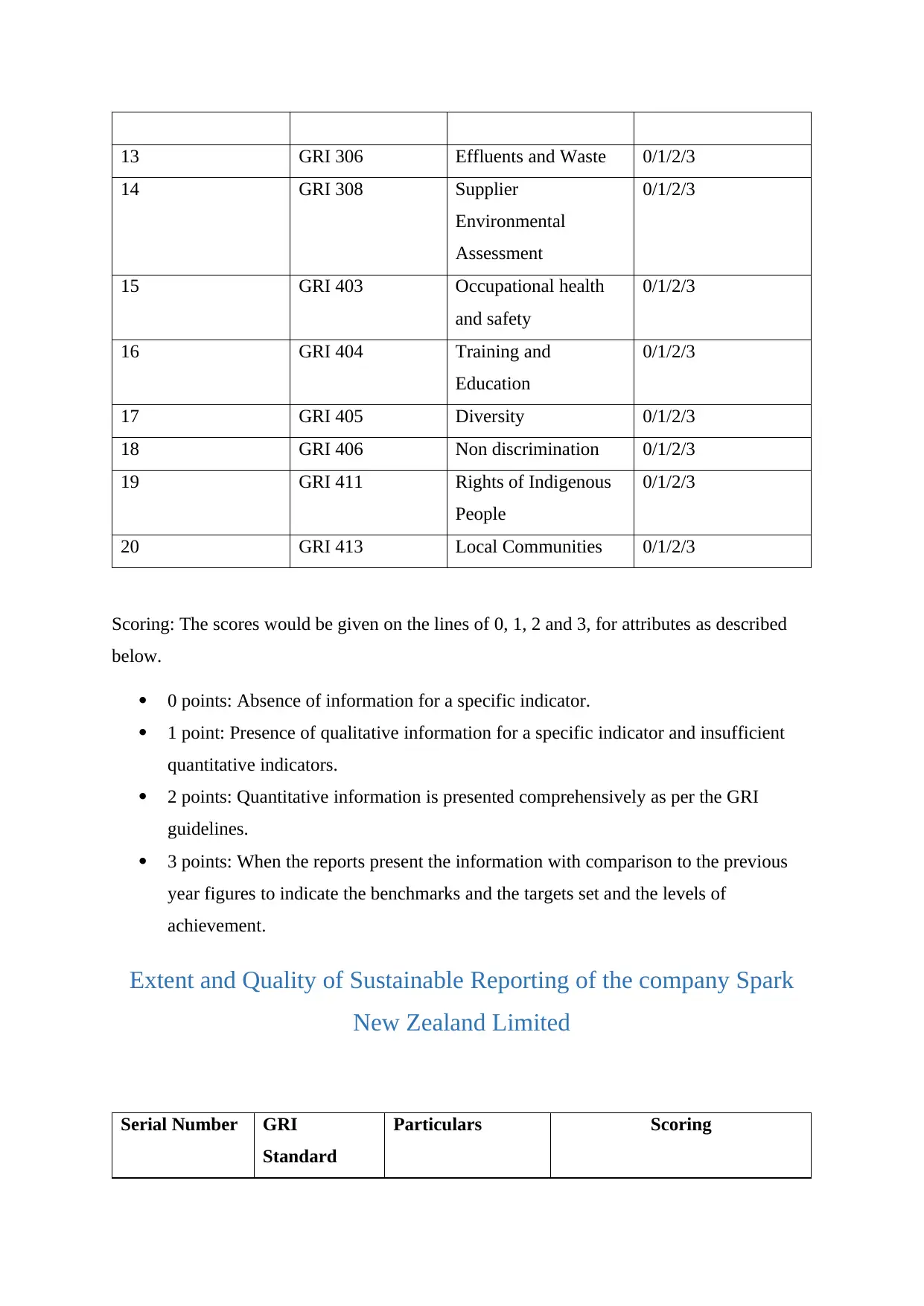

Sustainability reporting (disclosure) scoring index according to the

Global Reporting Initiative (GRI) guidelines

It is imperative to note that the numerous companies around the world take the aid of

the GRI guidelines for the development of their sustainability reports (Davys and Searcy,

2010). A sustainability reporting (disclosure) scoring index can be prepared according to the

Global Reporting Initiative (GRI) guidelines. The said benchmark would include the various

principles of the sustainable reporting and the content of the financial reports would be

examined against the same to judge the vitality of the same. There are numerous reporting

standards prescribed below under various categories to adjudge the performance of the

entities (GRI, 2019).

Serial Number GRI Standard Particulars Scoring

1 GRI 102 General Disclosures 0/1/2/3

2 GRI 103 Management

Approach

0/1/2/3

3 GRI 201 Economic

Performance

0/1/2/3

4 GRI 202 Market Presence 0/1/2/3

5 GRI 203 Indirect Economic

Impacts

0/1/2/3

6 GRI 204 Procurement Practices 0/1/2/3

7 GRI 205 Anti-Corruption 0/1/2/3

8 GRI 301 Materials 0/1/2/3

9 GRI 302 Energy 0/1/2/3

10 GRI 303 Water 0/1/2/3

11 GRI 304 Biodiversity 0/1/2/3

12 GRI 305 Emissions 0/1/2/3

home consumers as well as the small medium business market. The second segment namely

the Spark Digital segment is engaged in the integration of the information technology (IT)

and telecommunications services and thus provides various information and communications

technology (ICT) solutions to the clients. The third and last segment Spark Connect provides

services of the network and IT operations.

Sustainability reporting (disclosure) scoring index according to the

Global Reporting Initiative (GRI) guidelines

It is imperative to note that the numerous companies around the world take the aid of

the GRI guidelines for the development of their sustainability reports (Davys and Searcy,

2010). A sustainability reporting (disclosure) scoring index can be prepared according to the

Global Reporting Initiative (GRI) guidelines. The said benchmark would include the various

principles of the sustainable reporting and the content of the financial reports would be

examined against the same to judge the vitality of the same. There are numerous reporting

standards prescribed below under various categories to adjudge the performance of the

entities (GRI, 2019).

Serial Number GRI Standard Particulars Scoring

1 GRI 102 General Disclosures 0/1/2/3

2 GRI 103 Management

Approach

0/1/2/3

3 GRI 201 Economic

Performance

0/1/2/3

4 GRI 202 Market Presence 0/1/2/3

5 GRI 203 Indirect Economic

Impacts

0/1/2/3

6 GRI 204 Procurement Practices 0/1/2/3

7 GRI 205 Anti-Corruption 0/1/2/3

8 GRI 301 Materials 0/1/2/3

9 GRI 302 Energy 0/1/2/3

10 GRI 303 Water 0/1/2/3

11 GRI 304 Biodiversity 0/1/2/3

12 GRI 305 Emissions 0/1/2/3

13 GRI 306 Effluents and Waste 0/1/2/3

14 GRI 308 Supplier

Environmental

Assessment

0/1/2/3

15 GRI 403 Occupational health

and safety

0/1/2/3

16 GRI 404 Training and

Education

0/1/2/3

17 GRI 405 Diversity 0/1/2/3

18 GRI 406 Non discrimination 0/1/2/3

19 GRI 411 Rights of Indigenous

People

0/1/2/3

20 GRI 413 Local Communities 0/1/2/3

Scoring: The scores would be given on the lines of 0, 1, 2 and 3, for attributes as described

below.

0 points: Absence of information for a specific indicator.

1 point: Presence of qualitative information for a specific indicator and insufficient

quantitative indicators.

2 points: Quantitative information is presented comprehensively as per the GRI

guidelines.

3 points: When the reports present the information with comparison to the previous

year figures to indicate the benchmarks and the targets set and the levels of

achievement.

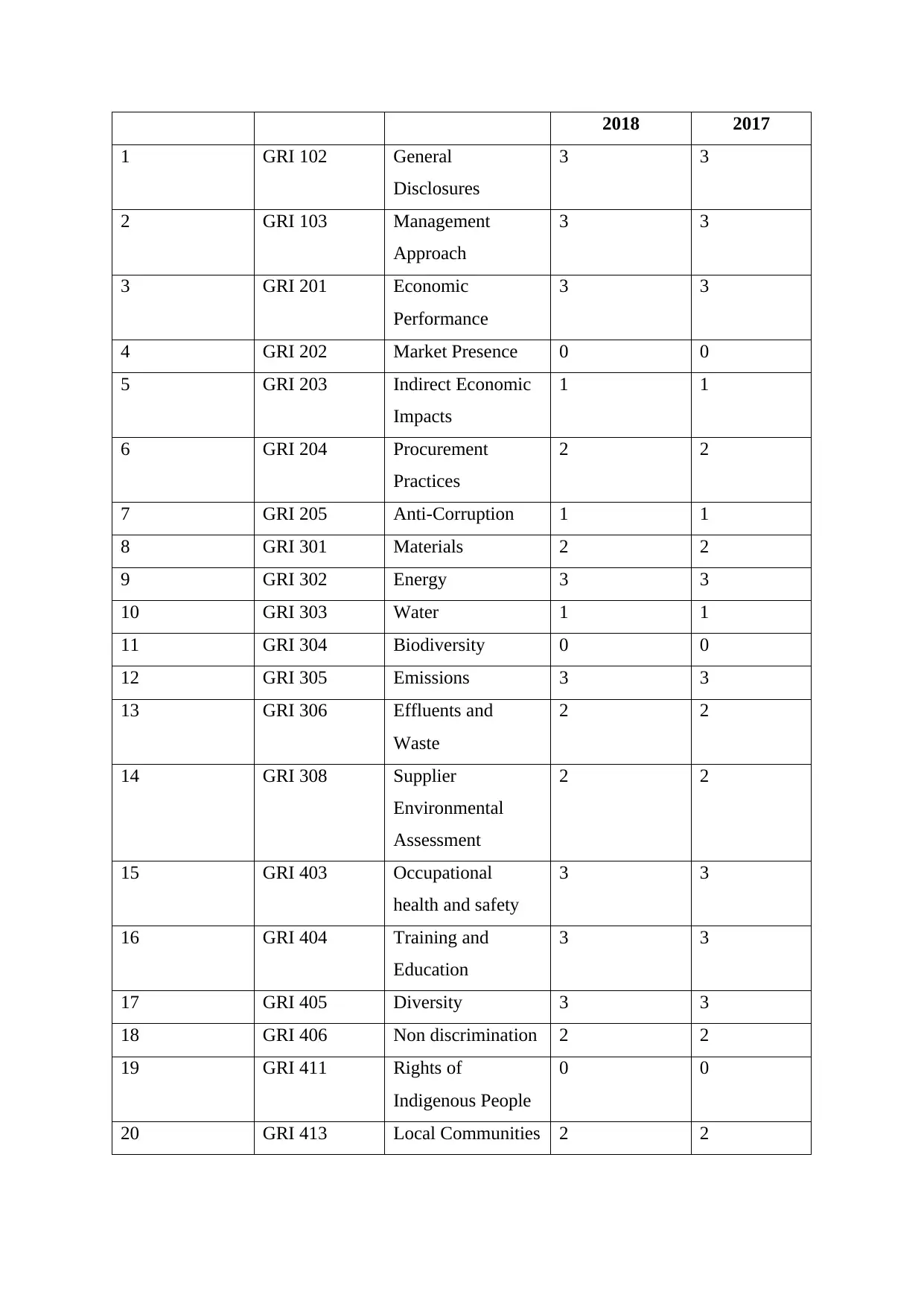

Extent and Quality of Sustainable Reporting of the company Spark

New Zealand Limited

Serial Number GRI

Standard

Particulars Scoring

14 GRI 308 Supplier

Environmental

Assessment

0/1/2/3

15 GRI 403 Occupational health

and safety

0/1/2/3

16 GRI 404 Training and

Education

0/1/2/3

17 GRI 405 Diversity 0/1/2/3

18 GRI 406 Non discrimination 0/1/2/3

19 GRI 411 Rights of Indigenous

People

0/1/2/3

20 GRI 413 Local Communities 0/1/2/3

Scoring: The scores would be given on the lines of 0, 1, 2 and 3, for attributes as described

below.

0 points: Absence of information for a specific indicator.

1 point: Presence of qualitative information for a specific indicator and insufficient

quantitative indicators.

2 points: Quantitative information is presented comprehensively as per the GRI

guidelines.

3 points: When the reports present the information with comparison to the previous

year figures to indicate the benchmarks and the targets set and the levels of

achievement.

Extent and Quality of Sustainable Reporting of the company Spark

New Zealand Limited

Serial Number GRI

Standard

Particulars Scoring

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2018 2017

1 GRI 102 General

Disclosures

3 3

2 GRI 103 Management

Approach

3 3

3 GRI 201 Economic

Performance

3 3

4 GRI 202 Market Presence 0 0

5 GRI 203 Indirect Economic

Impacts

1 1

6 GRI 204 Procurement

Practices

2 2

7 GRI 205 Anti-Corruption 1 1

8 GRI 301 Materials 2 2

9 GRI 302 Energy 3 3

10 GRI 303 Water 1 1

11 GRI 304 Biodiversity 0 0

12 GRI 305 Emissions 3 3

13 GRI 306 Effluents and

Waste

2 2

14 GRI 308 Supplier

Environmental

Assessment

2 2

15 GRI 403 Occupational

health and safety

3 3

16 GRI 404 Training and

Education

3 3

17 GRI 405 Diversity 3 3

18 GRI 406 Non discrimination 2 2

19 GRI 411 Rights of

Indigenous People

0 0

20 GRI 413 Local Communities 2 2

1 GRI 102 General

Disclosures

3 3

2 GRI 103 Management

Approach

3 3

3 GRI 201 Economic

Performance

3 3

4 GRI 202 Market Presence 0 0

5 GRI 203 Indirect Economic

Impacts

1 1

6 GRI 204 Procurement

Practices

2 2

7 GRI 205 Anti-Corruption 1 1

8 GRI 301 Materials 2 2

9 GRI 302 Energy 3 3

10 GRI 303 Water 1 1

11 GRI 304 Biodiversity 0 0

12 GRI 305 Emissions 3 3

13 GRI 306 Effluents and

Waste

2 2

14 GRI 308 Supplier

Environmental

Assessment

2 2

15 GRI 403 Occupational

health and safety

3 3

16 GRI 404 Training and

Education

3 3

17 GRI 405 Diversity 3 3

18 GRI 406 Non discrimination 2 2

19 GRI 411 Rights of

Indigenous People

0 0

20 GRI 413 Local Communities 2 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

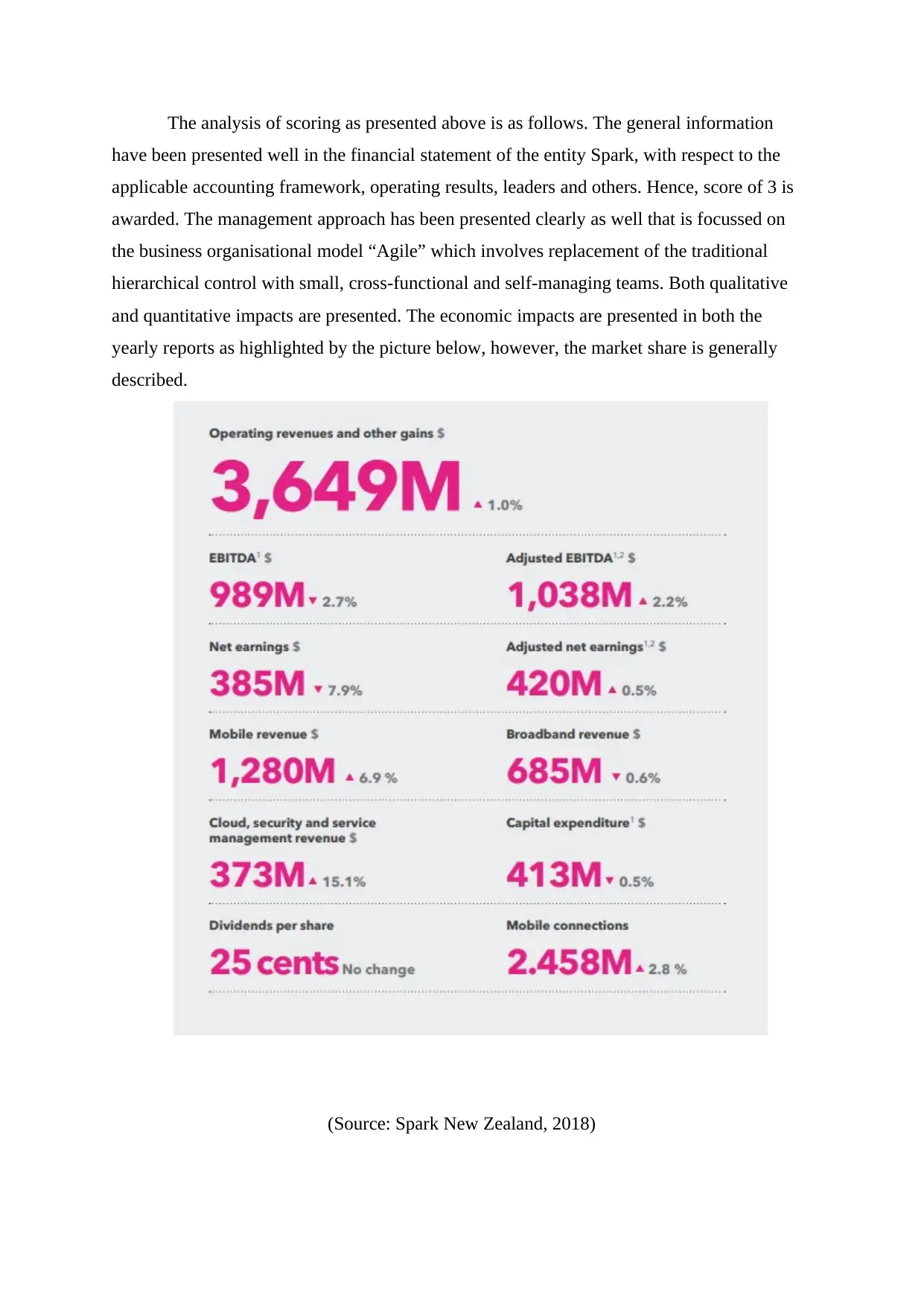

The analysis of scoring as presented above is as follows. The general information

have been presented well in the financial statement of the entity Spark, with respect to the

applicable accounting framework, operating results, leaders and others. Hence, score of 3 is

awarded. The management approach has been presented clearly as well that is focussed on

the business organisational model “Agile” which involves replacement of the traditional

hierarchical control with small, cross-functional and self-managing teams. Both qualitative

and quantitative impacts are presented. The economic impacts are presented in both the

yearly reports as highlighted by the picture below, however, the market share is generally

described.

(Source: Spark New Zealand, 2018)

have been presented well in the financial statement of the entity Spark, with respect to the

applicable accounting framework, operating results, leaders and others. Hence, score of 3 is

awarded. The management approach has been presented clearly as well that is focussed on

the business organisational model “Agile” which involves replacement of the traditional

hierarchical control with small, cross-functional and self-managing teams. Both qualitative

and quantitative impacts are presented. The economic impacts are presented in both the

yearly reports as highlighted by the picture below, however, the market share is generally

described.

(Source: Spark New Zealand, 2018)

The indirect economic impact has been presented qualitatively in the form of growth

in cloud, security and service management, launching of nationwide low-power Internet of

Things (IoT) network and others. In terms of material and energy information,

comprehensive information have been provided. For the suppliers, code of conduct has been

envisaged. As described in the score sheet above, the company has additionally provided a

range of information for the various aspects of the employment in the company. The aspects

like the diversity, inclusion, director’s remuneration, the extent of the target achieved and

upcoming targets are stated in the financial reports of both the years. Some of the aspects that

have been completely missed in the reports in the environment sections is that of the

biodiversity and in the employees section is that of the rights of the indigenous people. Other

than this, on evaluation it has been found that the reports of the company have been

comprehensively prepared highlighting the various aspects of the business functioning as

required by the sustainable reporting standards.

in cloud, security and service management, launching of nationwide low-power Internet of

Things (IoT) network and others. In terms of material and energy information,

comprehensive information have been provided. For the suppliers, code of conduct has been

envisaged. As described in the score sheet above, the company has additionally provided a

range of information for the various aspects of the employment in the company. The aspects

like the diversity, inclusion, director’s remuneration, the extent of the target achieved and

upcoming targets are stated in the financial reports of both the years. Some of the aspects that

have been completely missed in the reports in the environment sections is that of the

biodiversity and in the employees section is that of the rights of the indigenous people. Other

than this, on evaluation it has been found that the reports of the company have been

comprehensively prepared highlighting the various aspects of the business functioning as

required by the sustainable reporting standards.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.