Corporate Takeover and Consolidation Accounting Report, HA2032

VerifiedAdded on 2022/12/27

|11

|3228

|48

Report

AI Summary

This report examines corporate and financial reporting, focusing on the acquisition process and its associated accounting treatments. It analyzes the case of JKY Ltd acquiring FAB Ltd, detailing strategies for reporting information in consolidated financial statements. The report explores intra-group transactions, providing examples and accounting treatments, as well as the reporting of non-controlling interests and related disclosures in annual reports. It covers consolidation and equity accounting methods, adhering to AASB standards, and includes illustrative examples to clarify journal entries and balance sheet presentations. The report also addresses the elimination of unrealized profits from intra-group transactions and the importance of proper disclosures regarding non-controlling interests in consolidated financial statements, as per AASB 127.

Running head: CORPORATE AND FINANCIAL REPORTING

Corporate and Financial Reporting

Name of the Student:

Name of the University:

Author’s Note

Corporate and Financial Reporting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE AND FINANCIAL REPORTING

Executive Summary

The main purpose of the assessment is to discuss the acquisition process and the

accounting treatment which is associated with the same. The assessment considers the

case of JKY ltd which is going to acquire FAB ltd and therefore requires an appropriate

strategy for reporting the information in the consolidated financial statement. The

assessment would also be providing information regarding intra-group transactions and

how the same are to be treated in the books of accounts. The assessment further

emphasises on providing appropriate disclosures relating to minority interest and other

treatments which are undertaken in the annual report of the business.

CORPORATE AND FINANCIAL REPORTING

Executive Summary

The main purpose of the assessment is to discuss the acquisition process and the

accounting treatment which is associated with the same. The assessment considers the

case of JKY ltd which is going to acquire FAB ltd and therefore requires an appropriate

strategy for reporting the information in the consolidated financial statement. The

assessment would also be providing information regarding intra-group transactions and

how the same are to be treated in the books of accounts. The assessment further

emphasises on providing appropriate disclosures relating to minority interest and other

treatments which are undertaken in the annual report of the business.

2

CORPORATE AND FINANCIAL REPORTING

Table of Contents

Introduction........................................................................................................................3

Answer to Part A................................................................................................................3

Answer to Part B................................................................................................................5

Answer to Part C................................................................................................................7

Conclusion.........................................................................................................................8

Reference..........................................................................................................................9

CORPORATE AND FINANCIAL REPORTING

Table of Contents

Introduction........................................................................................................................3

Answer to Part A................................................................................................................3

Answer to Part B................................................................................................................5

Answer to Part C................................................................................................................7

Conclusion.........................................................................................................................8

Reference..........................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE AND FINANCIAL REPORTING

Introduction

In a business environment where immense competition lies, merger and

acquisition are a quite common aspect. The merger and acquisition are undertaken by

businesses for the purpose of strengthening their businesses and facing competition.

The assessment which is discussed below also deals with the case of acquisition of

FAB Ltd by JKY ltd. The reasons for acquisition are not relevant to the study but the

methods which is used by the management of JKY ltd for the purpose of acquisition and

reporting for the same is the main basis of the first part of the study (Shah, Liang and

Akbar 2013). The second part of the paper would be dealing with intra-group

transactions and the accounting treatments for the same. The study would be citing

examples of intra-group transaction so that a clearer meaning can be derived from the

same. The final part deals with the reporting of non-controlling interests and how the

same are shown in the consolidated financial statements of the business.

Answer to Part A

The acquisition strategy which is followed by a business also provides a

guideline which business needs to follow for reporting of financial information of the

business. The business of FAB ltd which is considered was acquired by JKY ltd and for

this purpose the strategy which was applied would be discussed. The two strategies

which are used by the business for conducting acquisition of a business are

consolidation accounting and equity accounting (Müller 2014). The decision regarding

which strategy is to be applied by the business for reporting consolidation transactions

depends on the senior management of the business. The two methods which are

available to the management of JKY ltd are discussed below in details:

Consolidation method of accounting:

This method is considered to be an essential method in consolidated accounting

where the assets and liabilities are accumulated for both the parent company and

subsidiary company and shown in the balance sheet of the company. The method

analyses the involvement of the parent company in the business of subsidiary and on

the basis of the same accounting transactions are recorded in the financial reports. The

income and expenses which is associated with the subsidiary company is also to be

listed in the income statement. According to “Paragraph B86 of AASB 10”, the

consolidated financial statement includes all the expenses, income, assets and liabilities

of the business for appropriate presentation of the financial results of the business

(Aasb.gov.au. 2019). The process of consolidation also comes across transactions

which has taken place between subsidiary and parent company which needs to be

eliminated or set off. The set off process is followed for avoiding a circumstance of

double counting in the accounting records and it is therefore suggested that elimination

of intercompany transactions is the best approach which can be followed by a business.

The provisions of AASB 10 includes a para B88, which sets out the measuring

criteria for the different elements which are represented in the financial statements and

also explains how the sane needs to be shown in the consolidated financial statements

of the business (Aasb.gov.au. 2019). The criteria require the management of JKY ltd to

CORPORATE AND FINANCIAL REPORTING

Introduction

In a business environment where immense competition lies, merger and

acquisition are a quite common aspect. The merger and acquisition are undertaken by

businesses for the purpose of strengthening their businesses and facing competition.

The assessment which is discussed below also deals with the case of acquisition of

FAB Ltd by JKY ltd. The reasons for acquisition are not relevant to the study but the

methods which is used by the management of JKY ltd for the purpose of acquisition and

reporting for the same is the main basis of the first part of the study (Shah, Liang and

Akbar 2013). The second part of the paper would be dealing with intra-group

transactions and the accounting treatments for the same. The study would be citing

examples of intra-group transaction so that a clearer meaning can be derived from the

same. The final part deals with the reporting of non-controlling interests and how the

same are shown in the consolidated financial statements of the business.

Answer to Part A

The acquisition strategy which is followed by a business also provides a

guideline which business needs to follow for reporting of financial information of the

business. The business of FAB ltd which is considered was acquired by JKY ltd and for

this purpose the strategy which was applied would be discussed. The two strategies

which are used by the business for conducting acquisition of a business are

consolidation accounting and equity accounting (Müller 2014). The decision regarding

which strategy is to be applied by the business for reporting consolidation transactions

depends on the senior management of the business. The two methods which are

available to the management of JKY ltd are discussed below in details:

Consolidation method of accounting:

This method is considered to be an essential method in consolidated accounting

where the assets and liabilities are accumulated for both the parent company and

subsidiary company and shown in the balance sheet of the company. The method

analyses the involvement of the parent company in the business of subsidiary and on

the basis of the same accounting transactions are recorded in the financial reports. The

income and expenses which is associated with the subsidiary company is also to be

listed in the income statement. According to “Paragraph B86 of AASB 10”, the

consolidated financial statement includes all the expenses, income, assets and liabilities

of the business for appropriate presentation of the financial results of the business

(Aasb.gov.au. 2019). The process of consolidation also comes across transactions

which has taken place between subsidiary and parent company which needs to be

eliminated or set off. The set off process is followed for avoiding a circumstance of

double counting in the accounting records and it is therefore suggested that elimination

of intercompany transactions is the best approach which can be followed by a business.

The provisions of AASB 10 includes a para B88, which sets out the measuring

criteria for the different elements which are represented in the financial statements and

also explains how the sane needs to be shown in the consolidated financial statements

of the business (Aasb.gov.au. 2019). The criteria require the management of JKY ltd to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

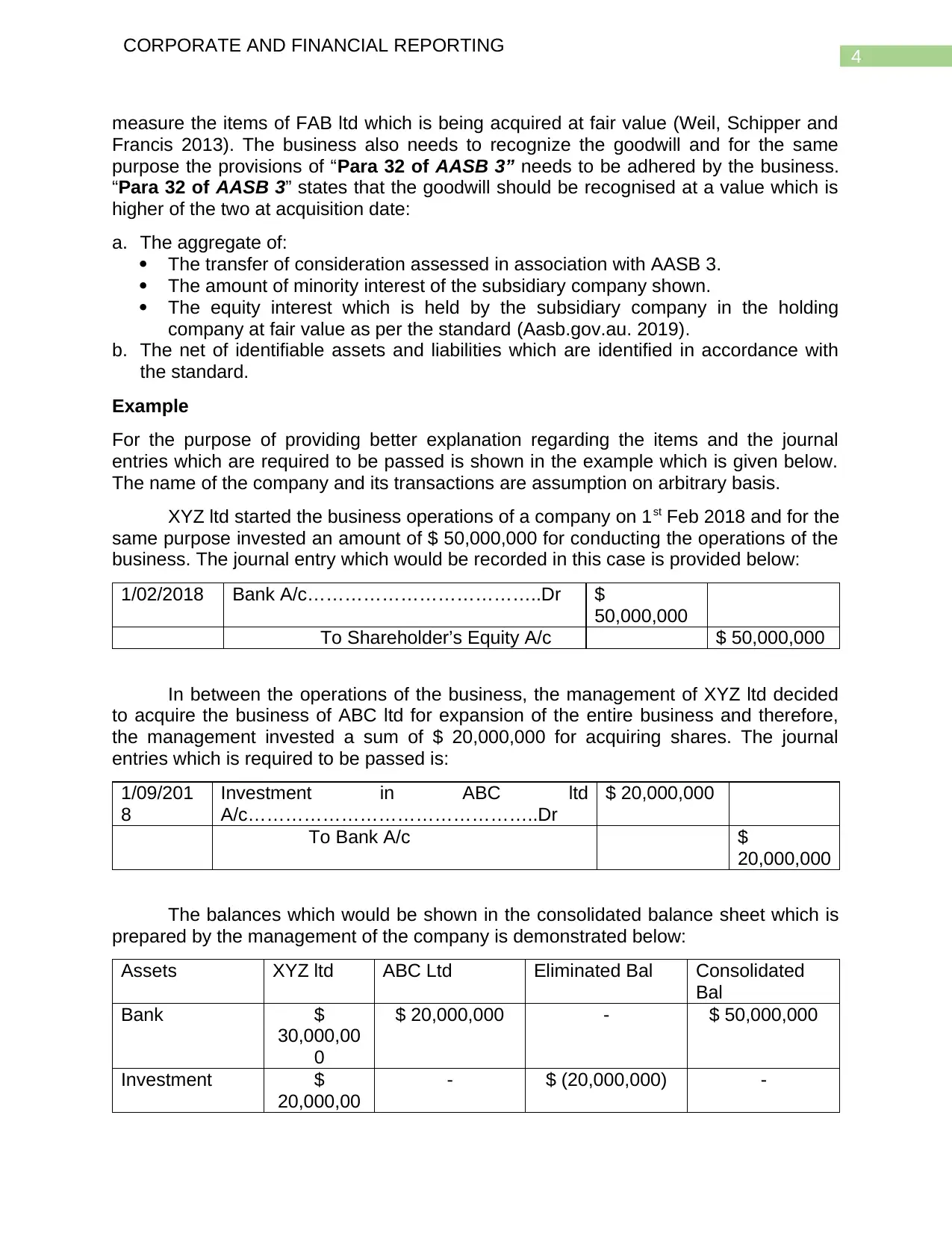

CORPORATE AND FINANCIAL REPORTING

measure the items of FAB ltd which is being acquired at fair value (Weil, Schipper and

Francis 2013). The business also needs to recognize the goodwill and for the same

purpose the provisions of “Para 32 of AASB 3” needs to be adhered by the business.

“Para 32 of AASB 3” states that the goodwill should be recognised at a value which is

higher of the two at acquisition date:

a. The aggregate of:

The transfer of consideration assessed in association with AASB 3.

The amount of minority interest of the subsidiary company shown.

The equity interest which is held by the subsidiary company in the holding

company at fair value as per the standard (Aasb.gov.au. 2019).

b. The net of identifiable assets and liabilities which are identified in accordance with

the standard.

Example

For the purpose of providing better explanation regarding the items and the journal

entries which are required to be passed is shown in the example which is given below.

The name of the company and its transactions are assumption on arbitrary basis.

XYZ ltd started the business operations of a company on 1st Feb 2018 and for the

same purpose invested an amount of $ 50,000,000 for conducting the operations of the

business. The journal entry which would be recorded in this case is provided below:

1/02/2018 Bank A/c………………………………..Dr $

50,000,000

To Shareholder’s Equity A/c $ 50,000,000

In between the operations of the business, the management of XYZ ltd decided

to acquire the business of ABC ltd for expansion of the entire business and therefore,

the management invested a sum of $ 20,000,000 for acquiring shares. The journal

entries which is required to be passed is:

1/09/201

8

Investment in ABC ltd

A/c………………………………………..Dr

$ 20,000,000

To Bank A/c $

20,000,000

The balances which would be shown in the consolidated balance sheet which is

prepared by the management of the company is demonstrated below:

Assets XYZ ltd ABC Ltd Eliminated Bal Consolidated

Bal

Bank $

30,000,00

0

$ 20,000,000 - $ 50,000,000

Investment $

20,000,00

- $ (20,000,000) -

CORPORATE AND FINANCIAL REPORTING

measure the items of FAB ltd which is being acquired at fair value (Weil, Schipper and

Francis 2013). The business also needs to recognize the goodwill and for the same

purpose the provisions of “Para 32 of AASB 3” needs to be adhered by the business.

“Para 32 of AASB 3” states that the goodwill should be recognised at a value which is

higher of the two at acquisition date:

a. The aggregate of:

The transfer of consideration assessed in association with AASB 3.

The amount of minority interest of the subsidiary company shown.

The equity interest which is held by the subsidiary company in the holding

company at fair value as per the standard (Aasb.gov.au. 2019).

b. The net of identifiable assets and liabilities which are identified in accordance with

the standard.

Example

For the purpose of providing better explanation regarding the items and the journal

entries which are required to be passed is shown in the example which is given below.

The name of the company and its transactions are assumption on arbitrary basis.

XYZ ltd started the business operations of a company on 1st Feb 2018 and for the

same purpose invested an amount of $ 50,000,000 for conducting the operations of the

business. The journal entry which would be recorded in this case is provided below:

1/02/2018 Bank A/c………………………………..Dr $

50,000,000

To Shareholder’s Equity A/c $ 50,000,000

In between the operations of the business, the management of XYZ ltd decided

to acquire the business of ABC ltd for expansion of the entire business and therefore,

the management invested a sum of $ 20,000,000 for acquiring shares. The journal

entries which is required to be passed is:

1/09/201

8

Investment in ABC ltd

A/c………………………………………..Dr

$ 20,000,000

To Bank A/c $

20,000,000

The balances which would be shown in the consolidated balance sheet which is

prepared by the management of the company is demonstrated below:

Assets XYZ ltd ABC Ltd Eliminated Bal Consolidated

Bal

Bank $

30,000,00

0

$ 20,000,000 - $ 50,000,000

Investment $

20,000,00

- $ (20,000,000) -

5

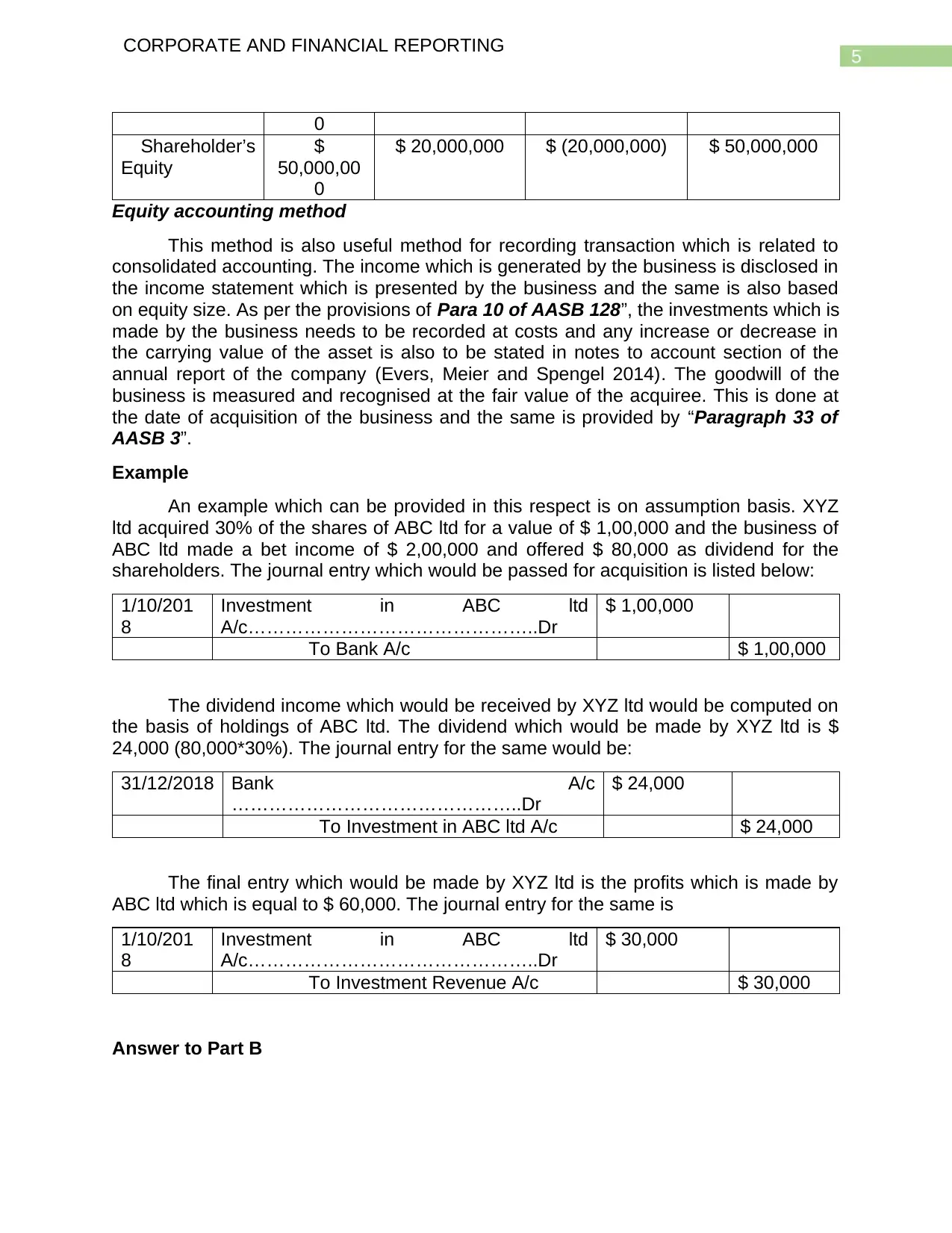

CORPORATE AND FINANCIAL REPORTING

0

Shareholder’s

Equity

$

50,000,00

0

$ 20,000,000 $ (20,000,000) $ 50,000,000

Equity accounting method

This method is also useful method for recording transaction which is related to

consolidated accounting. The income which is generated by the business is disclosed in

the income statement which is presented by the business and the same is also based

on equity size. As per the provisions of Para 10 of AASB 128”, the investments which is

made by the business needs to be recorded at costs and any increase or decrease in

the carrying value of the asset is also to be stated in notes to account section of the

annual report of the company (Evers, Meier and Spengel 2014). The goodwill of the

business is measured and recognised at the fair value of the acquiree. This is done at

the date of acquisition of the business and the same is provided by “Paragraph 33 of

AASB 3”.

Example

An example which can be provided in this respect is on assumption basis. XYZ

ltd acquired 30% of the shares of ABC ltd for a value of $ 1,00,000 and the business of

ABC ltd made a bet income of $ 2,00,000 and offered $ 80,000 as dividend for the

shareholders. The journal entry which would be passed for acquisition is listed below:

1/10/201

8

Investment in ABC ltd

A/c………………………………………..Dr

$ 1,00,000

To Bank A/c $ 1,00,000

The dividend income which would be received by XYZ ltd would be computed on

the basis of holdings of ABC ltd. The dividend which would be made by XYZ ltd is $

24,000 (80,000*30%). The journal entry for the same would be:

31/12/2018 Bank A/c

………………………………………..Dr

$ 24,000

To Investment in ABC ltd A/c $ 24,000

The final entry which would be made by XYZ ltd is the profits which is made by

ABC ltd which is equal to $ 60,000. The journal entry for the same is

1/10/201

8

Investment in ABC ltd

A/c………………………………………..Dr

$ 30,000

To Investment Revenue A/c $ 30,000

Answer to Part B

CORPORATE AND FINANCIAL REPORTING

0

Shareholder’s

Equity

$

50,000,00

0

$ 20,000,000 $ (20,000,000) $ 50,000,000

Equity accounting method

This method is also useful method for recording transaction which is related to

consolidated accounting. The income which is generated by the business is disclosed in

the income statement which is presented by the business and the same is also based

on equity size. As per the provisions of Para 10 of AASB 128”, the investments which is

made by the business needs to be recorded at costs and any increase or decrease in

the carrying value of the asset is also to be stated in notes to account section of the

annual report of the company (Evers, Meier and Spengel 2014). The goodwill of the

business is measured and recognised at the fair value of the acquiree. This is done at

the date of acquisition of the business and the same is provided by “Paragraph 33 of

AASB 3”.

Example

An example which can be provided in this respect is on assumption basis. XYZ

ltd acquired 30% of the shares of ABC ltd for a value of $ 1,00,000 and the business of

ABC ltd made a bet income of $ 2,00,000 and offered $ 80,000 as dividend for the

shareholders. The journal entry which would be passed for acquisition is listed below:

1/10/201

8

Investment in ABC ltd

A/c………………………………………..Dr

$ 1,00,000

To Bank A/c $ 1,00,000

The dividend income which would be received by XYZ ltd would be computed on

the basis of holdings of ABC ltd. The dividend which would be made by XYZ ltd is $

24,000 (80,000*30%). The journal entry for the same would be:

31/12/2018 Bank A/c

………………………………………..Dr

$ 24,000

To Investment in ABC ltd A/c $ 24,000

The final entry which would be made by XYZ ltd is the profits which is made by

ABC ltd which is equal to $ 60,000. The journal entry for the same is

1/10/201

8

Investment in ABC ltd

A/c………………………………………..Dr

$ 30,000

To Investment Revenue A/c $ 30,000

Answer to Part B

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE AND FINANCIAL REPORTING

In a large business, there are different subsidiaries operating which are also

engaged in their own operations. It is common for a subsidiary company to transact with

its parent company and this is known as intra group transactions. The preparation of the

financial statement of a business considers all these aspects and on the basis of the

same consolidation is carried forward. The provisions which are stated in “Para 29 of

AASB 127” requires the intra-group transactions, expenses and income to be

eliminated completely so that the double counting effect on the annual reports is not

present (Aasb.gov.au. 2019). Some of the common intra-group transactions which can

be listed are provided below:

Fee payment made to a member of the group

Dividend payments to members of the group

Intra-group inventory sale

Intra-group non-current asset sale

Intra-group loans

The management of the company needs to eliminate the transactions which are

provided above or any other intra-group transactions and for the same reverse journal

entry can be passed for eliminating the transaction.

The case which is provided shows that the management of JKY ltd has purchased

inventory from one if the subsidiary of the business. In terms of reporting, the subsidiary

business cannot recognise the revenue for the inventory sold unless the same is sold to

the final consumers (Barth 2015). In the meantime, the subsidiary business needs to

hold the revenue which is made from the inventory sold to JKY ltd and the same would

be treated as unrealised profits. “Para 25 of AASB 127” states that unrealised profits

made in an intra-group transaction needs to be recognised as assets under the head

non-current asset and is also required to be eliminated from inventory balance

(Aasb.gov.au. 2019).

The case shows that the subsidiary business sold inventory to JKY ltd and the sales

naturally must include a mark-up which is assumed to be 25%. The revenue for the

subsidiary business can only be realised when the inventory is sold to external party.

Therefore, it is imperative for the management to eliminate the unrealised profit from the

financial statements so that double counting of inventory does not take place. An

assumption can be made regarding the amount which is purchased by JKY ltd which is

shown to be $ 25,000. Therefore, if the mark-up is 25% on sales that the actual profit

which is made by the subsidiary is $ 5,000 ($ 25,000*25/ 125). If the amount of profit of

$ 5,000 is shown in the consolidated statement than the same would be overstating the

profits and affect the accuracy of the financial statement.

Consolidated Profit Account......................................Dr $5,000

To Consolidated Inventory Account $ 5,000

The above discussion shows the importance of eradicating the unrealised profits

from the consolidated financial statement which is prepared by the business. The profits

which is earned by the non-controlling interest of the business is to be reported. The

first approach is to recognise the non-controlling interest on the basis of proportionate

CORPORATE AND FINANCIAL REPORTING

In a large business, there are different subsidiaries operating which are also

engaged in their own operations. It is common for a subsidiary company to transact with

its parent company and this is known as intra group transactions. The preparation of the

financial statement of a business considers all these aspects and on the basis of the

same consolidation is carried forward. The provisions which are stated in “Para 29 of

AASB 127” requires the intra-group transactions, expenses and income to be

eliminated completely so that the double counting effect on the annual reports is not

present (Aasb.gov.au. 2019). Some of the common intra-group transactions which can

be listed are provided below:

Fee payment made to a member of the group

Dividend payments to members of the group

Intra-group inventory sale

Intra-group non-current asset sale

Intra-group loans

The management of the company needs to eliminate the transactions which are

provided above or any other intra-group transactions and for the same reverse journal

entry can be passed for eliminating the transaction.

The case which is provided shows that the management of JKY ltd has purchased

inventory from one if the subsidiary of the business. In terms of reporting, the subsidiary

business cannot recognise the revenue for the inventory sold unless the same is sold to

the final consumers (Barth 2015). In the meantime, the subsidiary business needs to

hold the revenue which is made from the inventory sold to JKY ltd and the same would

be treated as unrealised profits. “Para 25 of AASB 127” states that unrealised profits

made in an intra-group transaction needs to be recognised as assets under the head

non-current asset and is also required to be eliminated from inventory balance

(Aasb.gov.au. 2019).

The case shows that the subsidiary business sold inventory to JKY ltd and the sales

naturally must include a mark-up which is assumed to be 25%. The revenue for the

subsidiary business can only be realised when the inventory is sold to external party.

Therefore, it is imperative for the management to eliminate the unrealised profit from the

financial statements so that double counting of inventory does not take place. An

assumption can be made regarding the amount which is purchased by JKY ltd which is

shown to be $ 25,000. Therefore, if the mark-up is 25% on sales that the actual profit

which is made by the subsidiary is $ 5,000 ($ 25,000*25/ 125). If the amount of profit of

$ 5,000 is shown in the consolidated statement than the same would be overstating the

profits and affect the accuracy of the financial statement.

Consolidated Profit Account......................................Dr $5,000

To Consolidated Inventory Account $ 5,000

The above discussion shows the importance of eradicating the unrealised profits

from the consolidated financial statement which is prepared by the business. The profits

which is earned by the non-controlling interest of the business is to be reported. The

first approach is to recognise the non-controlling interest on the basis of proportionate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE AND FINANCIAL REPORTING

share of unrealised profits. Another approach involves not assigning any profits to the

non-controlling interest and the figure of non-controlling interest only depicts the share

capital value, reserves which are of subsidiary company.

Answer to Part C

Effects of Non-controlling Interest disclosures

As per the provisions which is provided by “Para 27 of AASB 127” that separate

consolidated financial statement are required to be prepared by a business and the

same needs to show appropriate disclosures regarding the non-controlling interest of a

business (Fox et al. 2013). Non-controlling interest refers to the equity capital and

reserves which belongs to the subsidiary company and the same are represented in the

annual reports of the parent company. At the end of any reporting period, the parent

company formulates the consolidated statement and for the same purpose

reconciliation of minority interest need to be done by the business and the same is

stated in “Para 106 (a) of AASB 101”.

The minority interest basically represents the claims in the business of parent

company. If the minority interest proportion changes than there is a change in the

subsidiary interest over the undertakings of the parent company (Horton, Serafeim and

Serafeim 2013). In a consolidation, the accounting process must consider the non-

controlling interest and the purchase consideration which is paid by the parent company

for acquiring the subsidiary business.

Changes required for Making Accurate Presentation

In order to ensure that the financial information is accurately presented, changes

are required to be made in accounting standard AASB 101. The management of a

company should look to prepare a consolidated financial statement which includes

financial information of subsidiaries as well as the parent company. The elimination of

intra transactions need to be done along with offset of any investment between the

subsidiary and parent company so that financial information can be presented

effectively at their carrying values.

The reporting for intragroup transaction should also consider the impact of

temporary difference from the elimination of profits and the same should be in

compliance with AASB 112. Moreover, the losses which is due to impairment of assets

which are realised needs to be recognised with the intra-group losses. The

management needs to combine the assets, liabilities and cash balances of the

subsidiary business and show the same in a combined manner (Costa and Agostini

2016). The accounting policies which are followed by the parent company needs to be

uniform and consistent. In addition to this, the same should also include disclosures and

explanation regarding the adjustments which are made in the financial statements. As

explained earlier, any unrealised profits which is made by the business needs to be

eradicated for faithful representation of information.

Effects of the required changes on the disclosure requirements

CORPORATE AND FINANCIAL REPORTING

share of unrealised profits. Another approach involves not assigning any profits to the

non-controlling interest and the figure of non-controlling interest only depicts the share

capital value, reserves which are of subsidiary company.

Answer to Part C

Effects of Non-controlling Interest disclosures

As per the provisions which is provided by “Para 27 of AASB 127” that separate

consolidated financial statement are required to be prepared by a business and the

same needs to show appropriate disclosures regarding the non-controlling interest of a

business (Fox et al. 2013). Non-controlling interest refers to the equity capital and

reserves which belongs to the subsidiary company and the same are represented in the

annual reports of the parent company. At the end of any reporting period, the parent

company formulates the consolidated statement and for the same purpose

reconciliation of minority interest need to be done by the business and the same is

stated in “Para 106 (a) of AASB 101”.

The minority interest basically represents the claims in the business of parent

company. If the minority interest proportion changes than there is a change in the

subsidiary interest over the undertakings of the parent company (Horton, Serafeim and

Serafeim 2013). In a consolidation, the accounting process must consider the non-

controlling interest and the purchase consideration which is paid by the parent company

for acquiring the subsidiary business.

Changes required for Making Accurate Presentation

In order to ensure that the financial information is accurately presented, changes

are required to be made in accounting standard AASB 101. The management of a

company should look to prepare a consolidated financial statement which includes

financial information of subsidiaries as well as the parent company. The elimination of

intra transactions need to be done along with offset of any investment between the

subsidiary and parent company so that financial information can be presented

effectively at their carrying values.

The reporting for intragroup transaction should also consider the impact of

temporary difference from the elimination of profits and the same should be in

compliance with AASB 112. Moreover, the losses which is due to impairment of assets

which are realised needs to be recognised with the intra-group losses. The

management needs to combine the assets, liabilities and cash balances of the

subsidiary business and show the same in a combined manner (Costa and Agostini

2016). The accounting policies which are followed by the parent company needs to be

uniform and consistent. In addition to this, the same should also include disclosures and

explanation regarding the adjustments which are made in the financial statements. As

explained earlier, any unrealised profits which is made by the business needs to be

eradicated for faithful representation of information.

Effects of the required changes on the disclosure requirements

8

CORPORATE AND FINANCIAL REPORTING

The provision of “Para 10 of AASB 127”, that if a business makes any

investments in joint ventures or subsidiaries that the same needs to be accounted for at

either costs or as per the guidelines provided by AASB 9. Therefore, some flexibility has

been provided in the preparation of the consolidated financial statement (Aasb.gov.au.

2019). The disclosure which are provided in case of consolidation is also appropriate

and the same are provided in such a manner that proper explanation is provided for

each and every treatment. Important treatments like repayment of loans, advances and

dividends in cash to parent need to be explained along with adjustments which are

made by the business (Flower 2018).

In case the parent company owns less than 50% of the voting rights in subsidiary

than disclosures are required to be made by the business in regards to the nature of

relationship which is maintained by the business. Hence, it can be stated that there is a

impact on the reporting framework as well for the percentage of holdings in terms of

portion of minority interest which needs to be stated.

Conclusion

The above discussion shows the treatments and disclosure requirements which

are to be considered while preparing consolidated financial statements. The discussion

shows the case of JKY ltd which is looking forward to acquire the business of FAB ltd

but is considering which strategy should be adopted. The discussion contrasts between

equity method and consolidated method of accounting and shows appropriate examples

relating to the same. The discussion also shows impacts of intragroup transactions on

overall reporting process and the steps which can be taken by the management of the

company for providing appropriate disclosures. The discussion also deals with minority

interest treatments and the disclosures which is to be provided in regards to the same.

CORPORATE AND FINANCIAL REPORTING

The provision of “Para 10 of AASB 127”, that if a business makes any

investments in joint ventures or subsidiaries that the same needs to be accounted for at

either costs or as per the guidelines provided by AASB 9. Therefore, some flexibility has

been provided in the preparation of the consolidated financial statement (Aasb.gov.au.

2019). The disclosure which are provided in case of consolidation is also appropriate

and the same are provided in such a manner that proper explanation is provided for

each and every treatment. Important treatments like repayment of loans, advances and

dividends in cash to parent need to be explained along with adjustments which are

made by the business (Flower 2018).

In case the parent company owns less than 50% of the voting rights in subsidiary

than disclosures are required to be made by the business in regards to the nature of

relationship which is maintained by the business. Hence, it can be stated that there is a

impact on the reporting framework as well for the percentage of holdings in terms of

portion of minority interest which needs to be stated.

Conclusion

The above discussion shows the treatments and disclosure requirements which

are to be considered while preparing consolidated financial statements. The discussion

shows the case of JKY ltd which is looking forward to acquire the business of FAB ltd

but is considering which strategy should be adopted. The discussion contrasts between

equity method and consolidated method of accounting and shows appropriate examples

relating to the same. The discussion also shows impacts of intragroup transactions on

overall reporting process and the steps which can be taken by the management of the

company for providing appropriate disclosures. The discussion also deals with minority

interest treatments and the disclosures which is to be provided in regards to the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE AND FINANCIAL REPORTING

Reference

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 3 May

2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 3 May

2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-

15.pdf [Accessed 3 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 3

May 2019].

Barth, M.E., 2015. Commentary on prospects for global financial reporting. Accounting

Perspectives, 14(3), pp.154-167.

Costa, E. and Agostini, M., 2016. Mandatory disclosure about environmental and

employee matters in the reports of Italian-listed corporate groups. Social and

Environmental Accountability Journal, 36(1), pp.10-33.

Evers, M., Meier, I. and Spengel, C., 2014. Transparency in financial reporting: Is

country-by-country reporting suitable to combat international profit shifting?. ZEW-

Centre for European Economic Research Discussion Paper, (14-015).

Flower, J., 2018. Global financial reporting. Macmillan International Higher Education.

Fox, A., Hannah, G., Helliar, C. and Veneziani, M., 2013. The costs and benefits of

IFRS implementation in the UK and Italy. Journal of Applied Accounting

Research, 14(1), pp.86-101.

Horton, J., Serafeim, G. and Serafeim, I., 2013. Does mandatory IFRS adoption

improve the information environment?. Contemporary accounting research, 30(1),

pp.388-423.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated financial

reporting. Procedia-Social and Behavioral Sciences, 109, pp.976-982.

CORPORATE AND FINANCIAL REPORTING

Reference

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 3 May

2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 3 May

2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-

15.pdf [Accessed 3 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 3

May 2019].

Barth, M.E., 2015. Commentary on prospects for global financial reporting. Accounting

Perspectives, 14(3), pp.154-167.

Costa, E. and Agostini, M., 2016. Mandatory disclosure about environmental and

employee matters in the reports of Italian-listed corporate groups. Social and

Environmental Accountability Journal, 36(1), pp.10-33.

Evers, M., Meier, I. and Spengel, C., 2014. Transparency in financial reporting: Is

country-by-country reporting suitable to combat international profit shifting?. ZEW-

Centre for European Economic Research Discussion Paper, (14-015).

Flower, J., 2018. Global financial reporting. Macmillan International Higher Education.

Fox, A., Hannah, G., Helliar, C. and Veneziani, M., 2013. The costs and benefits of

IFRS implementation in the UK and Italy. Journal of Applied Accounting

Research, 14(1), pp.86-101.

Horton, J., Serafeim, G. and Serafeim, I., 2013. Does mandatory IFRS adoption

improve the information environment?. Contemporary accounting research, 30(1),

pp.388-423.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated financial

reporting. Procedia-Social and Behavioral Sciences, 109, pp.976-982.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE AND FINANCIAL REPORTING

Shah, S.Z.A., Liang, S. and Akbar, S., 2013. International Financial Reporting

Standards and the value relevance of R&D expenditures: Pre and post IFRS

analysis. International Review of Financial Analysis, 30, pp.158-169.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

CORPORATE AND FINANCIAL REPORTING

Shah, S.Z.A., Liang, S. and Akbar, S., 2013. International Financial Reporting

Standards and the value relevance of R&D expenditures: Pre and post IFRS

analysis. International Review of Financial Analysis, 30, pp.158-169.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.