Corporate and Financial Accounting: Consolidation Accounting Report

VerifiedAdded on 2022/10/19

|11

|3339

|150

Report

AI Summary

This report critically examines the accounting factors involved in a corporate takeover scenario, specifically the acquisition of FAB Ltd by JKY Ltd. It delves into the differences between consolidation accounting and equity accounting, highlighting their impact on decision-making. The report emphasizes the importance of considering intra-group transactions and their treatment in financial reporting. Furthermore, it addresses the disclosure requirements for non-controlling interests, providing a comprehensive understanding of the key aspects of accounting for corporate takeovers. The report uses AASB standards and provides examples to illustrate the concepts. The report is structured into three parts, covering consolidation versus equity methods, intra-group transactions, and non-controlling interest disclosure, respectively, to offer a detailed overview of the crucial considerations in financial accounting for corporate takeovers.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and Financial Accounting

Name of the Student

Name of the University

Author’s Note

Corporate and Financial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary

This report involves in the critical discussion on the required accounting factors that

need to be taken into consideration in the takeover of FAB Ltd by JKY Ltd. The outcome

of the report shows that the management of JKY Ltd needs to consider the differences

between the methods of consolidation accounting and equity accounting at the time of

making the decisions. It is also needed to consider the intra-group transaction’s effects.

Executive Summary

This report involves in the critical discussion on the required accounting factors that

need to be taken into consideration in the takeover of FAB Ltd by JKY Ltd. The outcome

of the report shows that the management of JKY Ltd needs to consider the differences

between the methods of consolidation accounting and equity accounting at the time of

making the decisions. It is also needed to consider the intra-group transaction’s effects.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction........................................................................................................................3

Part A Response................................................................................................................3

Part B Response................................................................................................................5

Part C Response...............................................................................................................6

Conclusion.........................................................................................................................8

References.........................................................................................................................9

Table of Contents

Introduction........................................................................................................................3

Part A Response................................................................................................................3

Part B Response................................................................................................................5

Part C Response...............................................................................................................6

Conclusion.........................................................................................................................8

References.........................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE AND FINANCIAL ACCOUNTING

Introduction

The main objective of this report is to discuss about certain crucial aspects

regarding the acquisition of FAB Ltd by JKY Ltd while both of these companies operate

in the same industry. There are three parts in the report. First part outlines the key

differences in methodology between Consolidation Accounting and Equity Accounting.

Second part discusses the key principles on how intra-group transactions need to be

treated in the presence of proper examples. The third part is about the disclosure of

non-controlling interests.

Part A Response

As per the given scenario, the management of JKY Ltd is going through a

dilemma regarding the adoption of the appropriate strategy for taking over the business

of FAB Ltd due to the presence of two major method of acquisition; they are

Consolidation Method and Equity Method. The nature of reporting of the balance sheet

as well as income statement in the partnership is considered as the key determinant of

the selection of either of the two above-mentioned strategies. There are some

differences between the methodologies of these two methods.

Consolidation Method – The major requirement of this method is that the proportion of

involvement of the partners in the partnership business needs to be considered as the

base for recording the assets and liabilities in the balance sheet. It is needed to record

all the acquisition related incomes and expenses in the income statement and balance

sheet; and it is needed to calculate the values of the assets and liabilities. According to

the AASB 10, Paragraph B86, the main elements of the consolidated income

statements and balance sheet are the income, expenses, equity, assets and liabilities of

the parent company as well as the subsidiary firms (aasb.gov.au 2019). According to

the requirement of this consolidation method, it is needed to ensure the full elimination

of the carrying value of the investments in the parent and subsidiary company while the

proportion of the subsidiary’s equity capital held by the parent firm also needs to be

eliminated. It requires the elimination adjustments entries for the removal of

intercompany transactions for the removal of the chances of double counting of values

in the consolidation process (Young 2013).

It is noteworthy to discuss about the aspect that there are certain specific

requirements that need to be adhered to for the financial measurement of different

financial statements’ items at the date of acquisition; and the companies are needed to

use the fair value measurement base for this valuation purpose; the total process needs

to be followed in accordance with the accounting standards of AASB 10. AASB 10,

Paragraph 32 mentions the goodwill recognition procedure at the time of the goodwill

recognition by the acquirer at the acquisition date (aasb.gov.au 2019). The acquirer is

needed to consider the higher of these below two conditions:

a. The aggregate of the following:

Introduction

The main objective of this report is to discuss about certain crucial aspects

regarding the acquisition of FAB Ltd by JKY Ltd while both of these companies operate

in the same industry. There are three parts in the report. First part outlines the key

differences in methodology between Consolidation Accounting and Equity Accounting.

Second part discusses the key principles on how intra-group transactions need to be

treated in the presence of proper examples. The third part is about the disclosure of

non-controlling interests.

Part A Response

As per the given scenario, the management of JKY Ltd is going through a

dilemma regarding the adoption of the appropriate strategy for taking over the business

of FAB Ltd due to the presence of two major method of acquisition; they are

Consolidation Method and Equity Method. The nature of reporting of the balance sheet

as well as income statement in the partnership is considered as the key determinant of

the selection of either of the two above-mentioned strategies. There are some

differences between the methodologies of these two methods.

Consolidation Method – The major requirement of this method is that the proportion of

involvement of the partners in the partnership business needs to be considered as the

base for recording the assets and liabilities in the balance sheet. It is needed to record

all the acquisition related incomes and expenses in the income statement and balance

sheet; and it is needed to calculate the values of the assets and liabilities. According to

the AASB 10, Paragraph B86, the main elements of the consolidated income

statements and balance sheet are the income, expenses, equity, assets and liabilities of

the parent company as well as the subsidiary firms (aasb.gov.au 2019). According to

the requirement of this consolidation method, it is needed to ensure the full elimination

of the carrying value of the investments in the parent and subsidiary company while the

proportion of the subsidiary’s equity capital held by the parent firm also needs to be

eliminated. It requires the elimination adjustments entries for the removal of

intercompany transactions for the removal of the chances of double counting of values

in the consolidation process (Young 2013).

It is noteworthy to discuss about the aspect that there are certain specific

requirements that need to be adhered to for the financial measurement of different

financial statements’ items at the date of acquisition; and the companies are needed to

use the fair value measurement base for this valuation purpose; the total process needs

to be followed in accordance with the accounting standards of AASB 10. AASB 10,

Paragraph 32 mentions the goodwill recognition procedure at the time of the goodwill

recognition by the acquirer at the acquisition date (aasb.gov.au 2019). The acquirer is

needed to consider the higher of these below two conditions:

a. The aggregate of the following:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE AND FINANCIAL ACCOUNTING

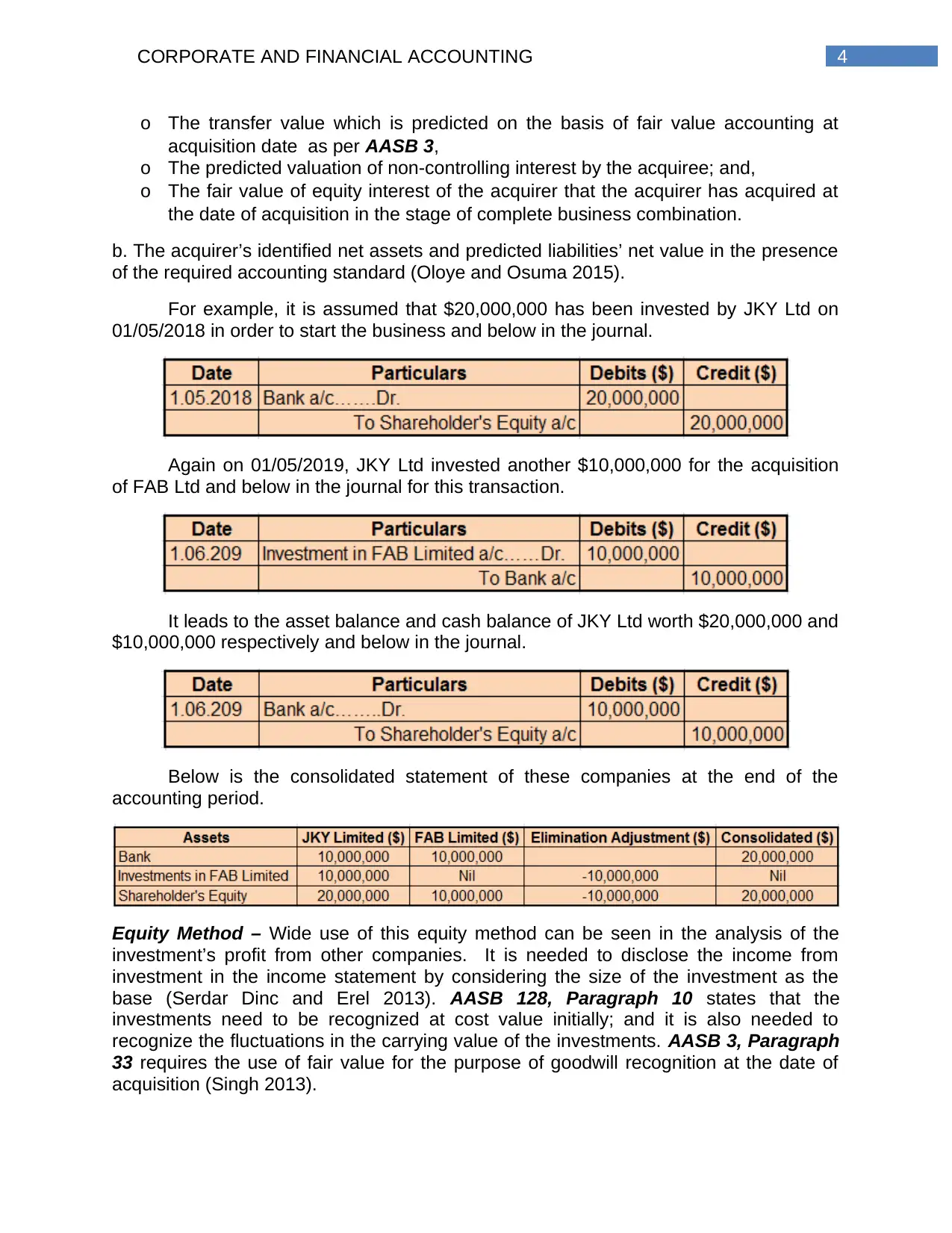

o The transfer value which is predicted on the basis of fair value accounting at

acquisition date as per AASB 3,

o The predicted valuation of non-controlling interest by the acquiree; and,

o The fair value of equity interest of the acquirer that the acquirer has acquired at

the date of acquisition in the stage of complete business combination.

b. The acquirer’s identified net assets and predicted liabilities’ net value in the presence

of the required accounting standard (Oloye and Osuma 2015).

For example, it is assumed that $20,000,000 has been invested by JKY Ltd on

01/05/2018 in order to start the business and below in the journal.

Again on 01/05/2019, JKY Ltd invested another $10,000,000 for the acquisition

of FAB Ltd and below in the journal for this transaction.

It leads to the asset balance and cash balance of JKY Ltd worth $20,000,000 and

$10,000,000 respectively and below in the journal.

Below is the consolidated statement of these companies at the end of the

accounting period.

Equity Method – Wide use of this equity method can be seen in the analysis of the

investment’s profit from other companies. It is needed to disclose the income from

investment in the income statement by considering the size of the investment as the

base (Serdar Dinc and Erel 2013). AASB 128, Paragraph 10 states that the

investments need to be recognized at cost value initially; and it is also needed to

recognize the fluctuations in the carrying value of the investments. AASB 3, Paragraph

33 requires the use of fair value for the purpose of goodwill recognition at the date of

acquisition (Singh 2013).

o The transfer value which is predicted on the basis of fair value accounting at

acquisition date as per AASB 3,

o The predicted valuation of non-controlling interest by the acquiree; and,

o The fair value of equity interest of the acquirer that the acquirer has acquired at

the date of acquisition in the stage of complete business combination.

b. The acquirer’s identified net assets and predicted liabilities’ net value in the presence

of the required accounting standard (Oloye and Osuma 2015).

For example, it is assumed that $20,000,000 has been invested by JKY Ltd on

01/05/2018 in order to start the business and below in the journal.

Again on 01/05/2019, JKY Ltd invested another $10,000,000 for the acquisition

of FAB Ltd and below in the journal for this transaction.

It leads to the asset balance and cash balance of JKY Ltd worth $20,000,000 and

$10,000,000 respectively and below in the journal.

Below is the consolidated statement of these companies at the end of the

accounting period.

Equity Method – Wide use of this equity method can be seen in the analysis of the

investment’s profit from other companies. It is needed to disclose the income from

investment in the income statement by considering the size of the investment as the

base (Serdar Dinc and Erel 2013). AASB 128, Paragraph 10 states that the

investments need to be recognized at cost value initially; and it is also needed to

recognize the fluctuations in the carrying value of the investments. AASB 3, Paragraph

33 requires the use of fair value for the purpose of goodwill recognition at the date of

acquisition (Singh 2013).

5CORPORATE AND FINANCIAL ACCOUNTING

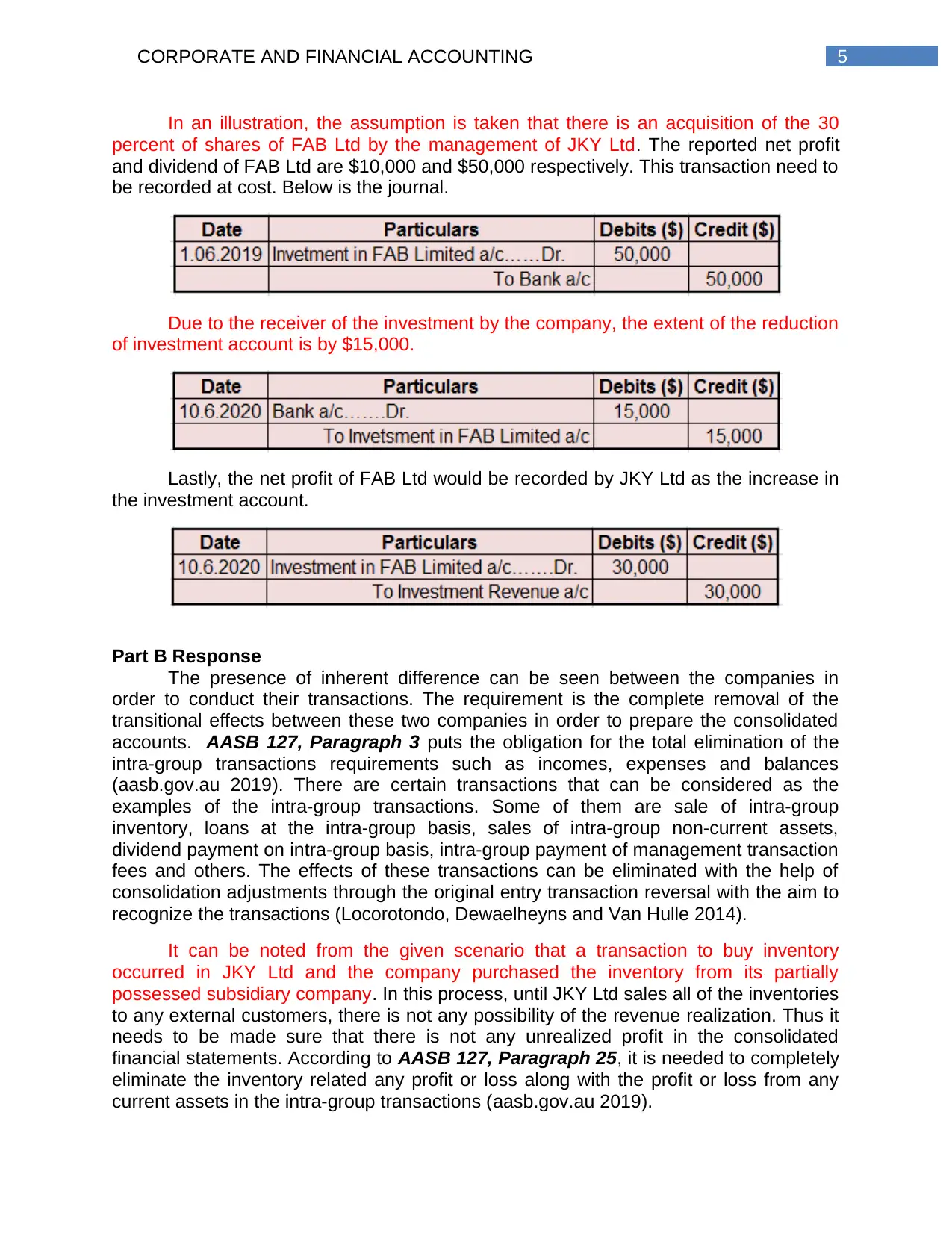

In an illustration, the assumption is taken that there is an acquisition of the 30

percent of shares of FAB Ltd by the management of JKY Ltd. The reported net profit

and dividend of FAB Ltd are $10,000 and $50,000 respectively. This transaction need to

be recorded at cost. Below is the journal.

Due to the receiver of the investment by the company, the extent of the reduction

of investment account is by $15,000.

Lastly, the net profit of FAB Ltd would be recorded by JKY Ltd as the increase in

the investment account.

Part B Response

The presence of inherent difference can be seen between the companies in

order to conduct their transactions. The requirement is the complete removal of the

transitional effects between these two companies in order to prepare the consolidated

accounts. AASB 127, Paragraph 3 puts the obligation for the total elimination of the

intra-group transactions requirements such as incomes, expenses and balances

(aasb.gov.au 2019). There are certain transactions that can be considered as the

examples of the intra-group transactions. Some of them are sale of intra-group

inventory, loans at the intra-group basis, sales of intra-group non-current assets,

dividend payment on intra-group basis, intra-group payment of management transaction

fees and others. The effects of these transactions can be eliminated with the help of

consolidation adjustments through the original entry transaction reversal with the aim to

recognize the transactions (Locorotondo, Dewaelheyns and Van Hulle 2014).

It can be noted from the given scenario that a transaction to buy inventory

occurred in JKY Ltd and the company purchased the inventory from its partially

possessed subsidiary company. In this process, until JKY Ltd sales all of the inventories

to any external customers, there is not any possibility of the revenue realization. Thus it

needs to be made sure that there is not any unrealized profit in the consolidated

financial statements. According to AASB 127, Paragraph 25, it is needed to completely

eliminate the inventory related any profit or loss along with the profit or loss from any

current assets in the intra-group transactions (aasb.gov.au 2019).

In an illustration, the assumption is taken that there is an acquisition of the 30

percent of shares of FAB Ltd by the management of JKY Ltd. The reported net profit

and dividend of FAB Ltd are $10,000 and $50,000 respectively. This transaction need to

be recorded at cost. Below is the journal.

Due to the receiver of the investment by the company, the extent of the reduction

of investment account is by $15,000.

Lastly, the net profit of FAB Ltd would be recorded by JKY Ltd as the increase in

the investment account.

Part B Response

The presence of inherent difference can be seen between the companies in

order to conduct their transactions. The requirement is the complete removal of the

transitional effects between these two companies in order to prepare the consolidated

accounts. AASB 127, Paragraph 3 puts the obligation for the total elimination of the

intra-group transactions requirements such as incomes, expenses and balances

(aasb.gov.au 2019). There are certain transactions that can be considered as the

examples of the intra-group transactions. Some of them are sale of intra-group

inventory, loans at the intra-group basis, sales of intra-group non-current assets,

dividend payment on intra-group basis, intra-group payment of management transaction

fees and others. The effects of these transactions can be eliminated with the help of

consolidation adjustments through the original entry transaction reversal with the aim to

recognize the transactions (Locorotondo, Dewaelheyns and Van Hulle 2014).

It can be noted from the given scenario that a transaction to buy inventory

occurred in JKY Ltd and the company purchased the inventory from its partially

possessed subsidiary company. In this process, until JKY Ltd sales all of the inventories

to any external customers, there is not any possibility of the revenue realization. Thus it

needs to be made sure that there is not any unrealized profit in the consolidated

financial statements. According to AASB 127, Paragraph 25, it is needed to completely

eliminate the inventory related any profit or loss along with the profit or loss from any

current assets in the intra-group transactions (aasb.gov.au 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE AND FINANCIAL ACCOUNTING

It can be seen from the given case study that JKY Ltd has sold inventory from

one subsidiary company which is partly owned and a mark-up is included in the sale

which makes the sales accurate in terms of group transactions when JKY Ltd tries to

sell the same inventory to any external customer. It is needed to consider the profit as

the unrealized profit until JKY Ltd become able in selling the inventory to external

customers which leads to the increase in the profit of the group. Thus, it is required to

fully eliminate the unrealized profit (Viñals et al. 2013).

For example, it is assumed that JKY Ltd has bought inventory worth $12,500

from one of its subsidiaries and the profit margin of the subsidiary is 20%. It leads to the

profit of $2,500 ($12,500 × 20%) that creates the overstatement of profit by this same

amount. Below is the required journal.

Consolidated Profit a/c……….Dr.

To Consolidated Inventory a/c

$2,500

$2500

The group is required to eliminate the unrealized profit that occurred from the

sale of the inventory to one of the subsidiaries in the presence of non-controlling

interest. It leads to profit uncertainty which is reported by the group for the non-

controlling interest. As per the fist method, the unrecognized profit needs to be assigned

to the non-controlling interest by using the unrecognized profit percentage as the base.

As per the second method, no profit needs to be assigned to the non-controlling interest

by the group (Ferran and Ho 2014).

In an illustration, the assumption has been taken that both the 80 percent and 70

percent interest of A Limited and B Limited respectively are acquired by JKY Ltd. A

Limited was involved in selling goods to B Limited for $10,000 whose actual cost was

$70,000. B Limited sold 50% of the purchased goods from A Limited. The unrealized

profit associated with this transaction needs to be eliminated by JKY Ltd. It is required

for A Limited to transfer $50,000 worth of profit to B Limited. The cost of the company is

$35,000. In this total process, the responsibility of JKY Ltd is to disregard the profit

worth $15,000 from the inventory related transaction. For this reason, $3000 that is

$15,000 × 20/100 is the percentage of the non-controlling interest (Vernimmen et al.

2014).

Part C Response

Effects of NCI Disclosure – At the time of the preparation and presentation of the

financial statements, the major responsibility on the management of the parent

company is to ensure the fact that the financial information of the non-controlling

interests are presented separately from that of the parent company’s financial

statements (aasb.gov.au 2019). Non-controlling is a portion of the equity of the

subsidiary which does not have any attribution towards the parent company. The

standard of AASB 127 have provided major assistance to improve the accounting and

reporting of the non-controlling interests. The main requirement in this situation is to

show and merge the changes in the financial information of both the parent company

and the subsidiary companies and this needs to be done through adhering with the

standards of AASB 101 (aasb.gov.au 2019). In this way, the values of the non-

It can be seen from the given case study that JKY Ltd has sold inventory from

one subsidiary company which is partly owned and a mark-up is included in the sale

which makes the sales accurate in terms of group transactions when JKY Ltd tries to

sell the same inventory to any external customer. It is needed to consider the profit as

the unrealized profit until JKY Ltd become able in selling the inventory to external

customers which leads to the increase in the profit of the group. Thus, it is required to

fully eliminate the unrealized profit (Viñals et al. 2013).

For example, it is assumed that JKY Ltd has bought inventory worth $12,500

from one of its subsidiaries and the profit margin of the subsidiary is 20%. It leads to the

profit of $2,500 ($12,500 × 20%) that creates the overstatement of profit by this same

amount. Below is the required journal.

Consolidated Profit a/c……….Dr.

To Consolidated Inventory a/c

$2,500

$2500

The group is required to eliminate the unrealized profit that occurred from the

sale of the inventory to one of the subsidiaries in the presence of non-controlling

interest. It leads to profit uncertainty which is reported by the group for the non-

controlling interest. As per the fist method, the unrecognized profit needs to be assigned

to the non-controlling interest by using the unrecognized profit percentage as the base.

As per the second method, no profit needs to be assigned to the non-controlling interest

by the group (Ferran and Ho 2014).

In an illustration, the assumption has been taken that both the 80 percent and 70

percent interest of A Limited and B Limited respectively are acquired by JKY Ltd. A

Limited was involved in selling goods to B Limited for $10,000 whose actual cost was

$70,000. B Limited sold 50% of the purchased goods from A Limited. The unrealized

profit associated with this transaction needs to be eliminated by JKY Ltd. It is required

for A Limited to transfer $50,000 worth of profit to B Limited. The cost of the company is

$35,000. In this total process, the responsibility of JKY Ltd is to disregard the profit

worth $15,000 from the inventory related transaction. For this reason, $3000 that is

$15,000 × 20/100 is the percentage of the non-controlling interest (Vernimmen et al.

2014).

Part C Response

Effects of NCI Disclosure – At the time of the preparation and presentation of the

financial statements, the major responsibility on the management of the parent

company is to ensure the fact that the financial information of the non-controlling

interests are presented separately from that of the parent company’s financial

statements (aasb.gov.au 2019). Non-controlling is a portion of the equity of the

subsidiary which does not have any attribution towards the parent company. The

standard of AASB 127 have provided major assistance to improve the accounting and

reporting of the non-controlling interests. The main requirement in this situation is to

show and merge the changes in the financial information of both the parent company

and the subsidiary companies and this needs to be done through adhering with the

standards of AASB 101 (aasb.gov.au 2019). In this way, the values of the non-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

controlling interest can be properly identified and the shareholders can get major clarity

on the claims regarding net assets in the consolidation process (Flower 2018).

Equity transactions can be considered as the dissimilarity of the interest of the

ownership in the parent company and this aspect does not take place in the absence of

the control of parent company on the subsidiaries. For this reason, there is a

requirement of conducting the needed adjustments in both the controlling as well as

non-controlling related carrying value when it is clear that there are changes in the

equity held by the non-controlling interest. After that, it is needed to directly recognize

the adjustments related to fair value and non-controlling interest in the presence of the

fact that they have major attribution towards the firm’s shareholders (Flower 2018).

Changes that is required – There are some key changes in the accounting standard of

AASB 101 for the appropriate representation of the consolidated financial statements of

the companies (aasb.gov.au 2019). It states that it is not needed to prepare the

separate financial statements at the reporting date. It needs to be mentioned that there

are certain financial adjustments that assist the users in demonstrating the main

transaction related impacts in the financial reporting dates of the parent company and

its subsidiary companies; and thus, these adjustments must be there.

There is a major requirement for the realization of the losses of impairment

associated with the identifiable assets. At the same time, it is also required to eliminate

the transactions that have connection with the intra-group balances, incomes and

expenses. According to AASB 112, it is required to consider the application of

provisional differences from the elimination of profit or loss through the help of the

appropriate adjustments in the parent company’s financial statements (aasb.gov.au

2019). In addition, it is required to maintain the uniformity in the application of the

accounting rules, regulation and policies in the consolidated financial statements

(Dunbar and Laing 2017).

The requirements of the companies is to ensure major attribution in the parent

company’s and its subsidiary companies’ total comprehensive income; and even in the

presence of any kind of negative impact of these certain accounting transactions of the

non-controlling interest, this major attribution needs to be continued. In this process, the

managements of the firms must correctly calculate the share of profit or loss in the

presence of outstanding cumulative preference share in one subsidiary company of the

parent company. It is needed for the companies to calculate this after considering the

required adjustments in those share related dividends (Dunbar and Laing 2017).

Implications of these Changes – One of the major requirements of the accountants of

both the parent company and the sub diary companies is to select the cost value of the

investments at the time of their recognition and measurement in the financial statements

and the accountants are required to consider the rules and regulations of the standards

of AASB 127 (aasb.gov.au 2019). This leads to the correct development of the financial

statements of the firms. At the same time, this aspect needs to be made sure that there

is the disclosure of the correct accounting policies and bases of measurement in the

presence of adequate materiality in the financial information as a result of inappropriate

disclosure. For this reason, the managements of the companies should develop the

controlling interest can be properly identified and the shareholders can get major clarity

on the claims regarding net assets in the consolidation process (Flower 2018).

Equity transactions can be considered as the dissimilarity of the interest of the

ownership in the parent company and this aspect does not take place in the absence of

the control of parent company on the subsidiaries. For this reason, there is a

requirement of conducting the needed adjustments in both the controlling as well as

non-controlling related carrying value when it is clear that there are changes in the

equity held by the non-controlling interest. After that, it is needed to directly recognize

the adjustments related to fair value and non-controlling interest in the presence of the

fact that they have major attribution towards the firm’s shareholders (Flower 2018).

Changes that is required – There are some key changes in the accounting standard of

AASB 101 for the appropriate representation of the consolidated financial statements of

the companies (aasb.gov.au 2019). It states that it is not needed to prepare the

separate financial statements at the reporting date. It needs to be mentioned that there

are certain financial adjustments that assist the users in demonstrating the main

transaction related impacts in the financial reporting dates of the parent company and

its subsidiary companies; and thus, these adjustments must be there.

There is a major requirement for the realization of the losses of impairment

associated with the identifiable assets. At the same time, it is also required to eliminate

the transactions that have connection with the intra-group balances, incomes and

expenses. According to AASB 112, it is required to consider the application of

provisional differences from the elimination of profit or loss through the help of the

appropriate adjustments in the parent company’s financial statements (aasb.gov.au

2019). In addition, it is required to maintain the uniformity in the application of the

accounting rules, regulation and policies in the consolidated financial statements

(Dunbar and Laing 2017).

The requirements of the companies is to ensure major attribution in the parent

company’s and its subsidiary companies’ total comprehensive income; and even in the

presence of any kind of negative impact of these certain accounting transactions of the

non-controlling interest, this major attribution needs to be continued. In this process, the

managements of the firms must correctly calculate the share of profit or loss in the

presence of outstanding cumulative preference share in one subsidiary company of the

parent company. It is needed for the companies to calculate this after considering the

required adjustments in those share related dividends (Dunbar and Laing 2017).

Implications of these Changes – One of the major requirements of the accountants of

both the parent company and the sub diary companies is to select the cost value of the

investments at the time of their recognition and measurement in the financial statements

and the accountants are required to consider the rules and regulations of the standards

of AASB 127 (aasb.gov.au 2019). This leads to the correct development of the financial

statements of the firms. At the same time, this aspect needs to be made sure that there

is the disclosure of the correct accounting policies and bases of measurement in the

presence of adequate materiality in the financial information as a result of inappropriate

disclosure. For this reason, the managements of the companies should develop the

8CORPORATE AND FINANCIAL ACCOUNTING

consolidated financial statements through effective disclosure of nature of any

uncertainty occurred from the requirements of regulations.

In addition, while preparing the parent company’s consolidated financial

statements, it is required for the parent company to ensure the aspects that the financial

statements of the subsidiary company are presented at the accounting period’s end.

This particular aspect ensures that all essential financial disclosures of the subsidiary

companies are there when the date of accounting year ending of the parent company

and the subsidiary companies are different. There are many instances when the parent

company does not have more than 50% voting right in one of its subsidiaries. In the

presence of this aspect, it is required for the parent company to make appropriate

disclosure of the nature of relationship between the parent company and the subsidiary.

Hence, it needs to be mentioned that all these aspects together influence the process to

prepare as well as present the financial statements of the parent companies (Carey,

Knechel and Tanewski 2013).

Conclusion

It can be seen from the above discussion that there are certain key differences

between the methodologies of the consolidation method of accounting and equity

method of accounting; and it is needed for the management of JKY Ltd to consider

these differences while adopting the strategy to take over FAB Ltd. The above

discussion also indicates towards the essential aspect that it is needed for the parent

companies to take into consideration the variations between different intra-group

transactions in case of the consolidated financial statements. According to the above

discussion, separate disclosure is needed to be made by the parent company on the

financial information of the non-controlling interests due to the fact that it has certain

major effects on the consolidated financial statements.

consolidated financial statements through effective disclosure of nature of any

uncertainty occurred from the requirements of regulations.

In addition, while preparing the parent company’s consolidated financial

statements, it is required for the parent company to ensure the aspects that the financial

statements of the subsidiary company are presented at the accounting period’s end.

This particular aspect ensures that all essential financial disclosures of the subsidiary

companies are there when the date of accounting year ending of the parent company

and the subsidiary companies are different. There are many instances when the parent

company does not have more than 50% voting right in one of its subsidiaries. In the

presence of this aspect, it is required for the parent company to make appropriate

disclosure of the nature of relationship between the parent company and the subsidiary.

Hence, it needs to be mentioned that all these aspects together influence the process to

prepare as well as present the financial statements of the parent companies (Carey,

Knechel and Tanewski 2013).

Conclusion

It can be seen from the above discussion that there are certain key differences

between the methodologies of the consolidation method of accounting and equity

method of accounting; and it is needed for the management of JKY Ltd to consider

these differences while adopting the strategy to take over FAB Ltd. The above

discussion also indicates towards the essential aspect that it is needed for the parent

companies to take into consideration the variations between different intra-group

transactions in case of the consolidated financial statements. According to the above

discussion, separate disclosure is needed to be made by the parent company on the

financial information of the non-controlling interests due to the fact that it has certain

major effects on the consolidated financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE AND FINANCIAL ACCOUNTING

References

Aasb.gov.au., 2019. Business Combinations. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 26 May

2019].

Aasb.gov.au., 2019. Consolidated Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 26

May 2019].

Aasb.gov.au., 2019. Investments in Associates and Joint Ventures. [online] Available

at: https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed

26 May 2019].

Aasb.gov.au., 2019. Presentation of Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 26

May 2019].

Aasb.gov.au., 2019. Separate Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-

15.pdf [Accessed 26 May 2019].

Carey, P., Knechel, W.R. and Tanewski, G., 2013. Costs and benefits of mandatory

auditing of for‐profit private and not‐for‐profit companies in Australia. Australian

accounting review, 23(1), pp.43-53.

Dunbar, K. and Laing, G.K., 2017. Deconstructing the Accounting Standard AASB 13

Fair Value: Exit vs Entry Price for Assets. Journal of New Business Ideas &

Trends, 15(2).

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University

Press.

Flower, J., 2018. Global financial reporting. Macmillan International Higher Education.

Locorotondo, R., Dewaelheyns, N. and Van Hulle, C., 2014. Cash holdings and

business group membership. Journal of Business Research, 67(3), pp.316-323.

Oloye, M.I. and Osuma, G., 2015. Impacts of Mergers and Acquisition on the

Performance of Nigerian Banks (A Case Study of Selected Banks). Pyrex Journal of

Business and Finance Management Research, 1(4), pp.23-40.

Serdar Dinc, I. and Erel, I., 2013. Economic nationalism in mergers and

acquisitions. The Journal of Finance, 68(6), pp.2471-2514.

Singh, K.B., 2013. The Impact of Merger and Acquistitions on Corporate Financial

Performance In India. Indian Journal of Research in Management, Business and Social

Sciences, 1(2), pp.13-16.

References

Aasb.gov.au., 2019. Business Combinations. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 26 May

2019].

Aasb.gov.au., 2019. Consolidated Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 26

May 2019].

Aasb.gov.au., 2019. Investments in Associates and Joint Ventures. [online] Available

at: https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed

26 May 2019].

Aasb.gov.au., 2019. Presentation of Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 26

May 2019].

Aasb.gov.au., 2019. Separate Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-

15.pdf [Accessed 26 May 2019].

Carey, P., Knechel, W.R. and Tanewski, G., 2013. Costs and benefits of mandatory

auditing of for‐profit private and not‐for‐profit companies in Australia. Australian

accounting review, 23(1), pp.43-53.

Dunbar, K. and Laing, G.K., 2017. Deconstructing the Accounting Standard AASB 13

Fair Value: Exit vs Entry Price for Assets. Journal of New Business Ideas &

Trends, 15(2).

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University

Press.

Flower, J., 2018. Global financial reporting. Macmillan International Higher Education.

Locorotondo, R., Dewaelheyns, N. and Van Hulle, C., 2014. Cash holdings and

business group membership. Journal of Business Research, 67(3), pp.316-323.

Oloye, M.I. and Osuma, G., 2015. Impacts of Mergers and Acquisition on the

Performance of Nigerian Banks (A Case Study of Selected Banks). Pyrex Journal of

Business and Finance Management Research, 1(4), pp.23-40.

Serdar Dinc, I. and Erel, I., 2013. Economic nationalism in mergers and

acquisitions. The Journal of Finance, 68(6), pp.2471-2514.

Singh, K.B., 2013. The Impact of Merger and Acquistitions on Corporate Financial

Performance In India. Indian Journal of Research in Management, Business and Social

Sciences, 1(2), pp.13-16.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE AND FINANCIAL ACCOUNTING

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate

finance: theory and practice. John Wiley & Sons.

Viñals, J., Pazarbasioglu, C., Surti, J., Narain, A., Erbenova, M.M. and Chow, M.J.T.,

2013. Creating a safer financial system: will the Volcker, Vickers, and Liikanen

Structural measures help? (No. 13-14). International Monetary Fund.

Young, G.R., 2013. Mergers and Aquisitions: Planning and Action. Routledge.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate

finance: theory and practice. John Wiley & Sons.

Viñals, J., Pazarbasioglu, C., Surti, J., Narain, A., Erbenova, M.M. and Chow, M.J.T.,

2013. Creating a safer financial system: will the Volcker, Vickers, and Liikanen

Structural measures help? (No. 13-14). International Monetary Fund.

Young, G.R., 2013. Mergers and Aquisitions: Planning and Action. Routledge.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.