HA2032 Corporate Takeover Decision Making & Consolidation Accounting

VerifiedAdded on 2023/04/03

|9

|2984

|256

Report

AI Summary

This report assesses the importance of financial reporting for organizations, using JKY Ltd. as a case study for purchase acquisition methods. It highlights the necessity of fair and accurate financial reporting and the role of Non-Controlling Interest (NCI), while emphasizing compliance with financial regulations. The analysis covers equity and consolidation accounting theories, intra-group transactions within JKY Ltd., and NCI disclosures as per AASB 101. The report advocates for the consolidation method of accounting for JKY Ltd., emphasizing its benefits in financial reporting and goodwill enhancement. It also examines the impact of intra-group transactions on financial statements, the significance of reconciliation processes, and the calculation of non-controlling interests. Ultimately, the report underscores the need for transparent financial statements that reflect true asset values and inform investor decisions, while adhering to statutory compliance.

Name of the Student

Name of the University

Author Note

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The report suggests the reporting of finance should be made essential criteria for all

the organizations. The suggestion can be put down to JKY Ltd for the method of the

purchase acquisition, which will help the company to provide analysis on the report.

Besides this, it is very important to note that the organization must portray very fair

and true value in its reporting of finance. NCI is considered to be the very vital tool of

the organization but it does not hold any voting rights in and for the organization. The

compliance has been made by the body of statures of the department of finance and

which is why it is relevant for the organization to create a lucid report on the grounds

of the assessment of finance.

The report suggests the reporting of finance should be made essential criteria for all

the organizations. The suggestion can be put down to JKY Ltd for the method of the

purchase acquisition, which will help the company to provide analysis on the report.

Besides this, it is very important to note that the organization must portray very fair

and true value in its reporting of finance. NCI is considered to be the very vital tool of

the organization but it does not hold any voting rights in and for the organization. The

compliance has been made by the body of statures of the department of finance and

which is why it is relevant for the organization to create a lucid report on the grounds

of the assessment of finance.

Table of Contents

Executive Summary......................................................................................................1

Introduction...................................................................................................................3

Part A response............................................................................................................3

Part B response............................................................................................................5

Part C response............................................................................................................6

Conclusion....................................................................................................................8

Reference:....................................................................................................................8

Executive Summary......................................................................................................1

Introduction...................................................................................................................3

Part A response............................................................................................................3

Part B response............................................................................................................5

Part C response............................................................................................................6

Conclusion....................................................................................................................8

Reference:....................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

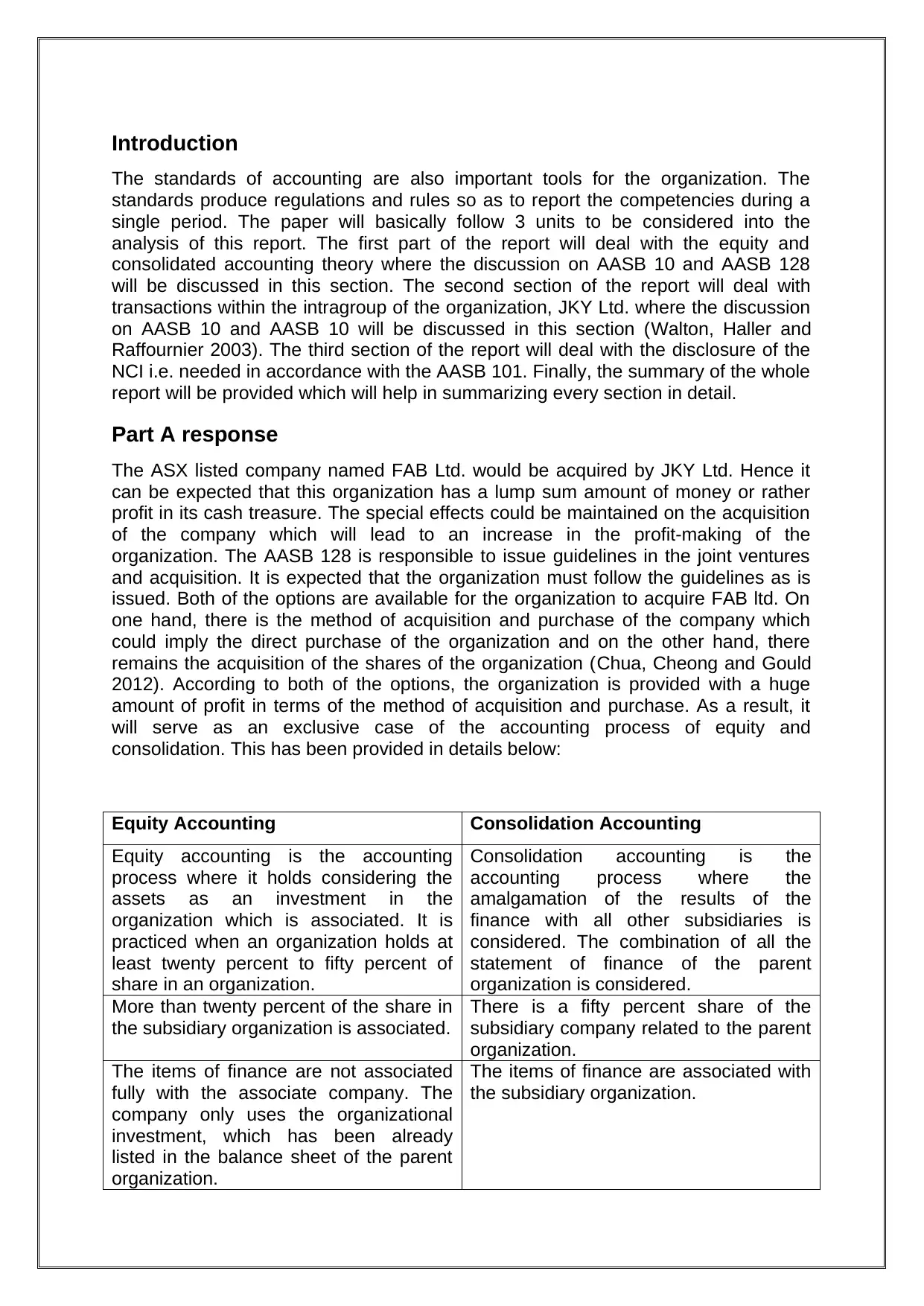

Introduction

The standards of accounting are also important tools for the organization. The

standards produce regulations and rules so as to report the competencies during a

single period. The paper will basically follow 3 units to be considered into the

analysis of this report. The first part of the report will deal with the equity and

consolidated accounting theory where the discussion on AASB 10 and AASB 128

will be discussed in this section. The second section of the report will deal with

transactions within the intragroup of the organization, JKY Ltd. where the discussion

on AASB 10 and AASB 10 will be discussed in this section (Walton, Haller and

Raffournier 2003). The third section of the report will deal with the disclosure of the

NCI i.e. needed in accordance with the AASB 101. Finally, the summary of the whole

report will be provided which will help in summarizing every section in detail.

Part A response

The ASX listed company named FAB Ltd. would be acquired by JKY Ltd. Hence it

can be expected that this organization has a lump sum amount of money or rather

profit in its cash treasure. The special effects could be maintained on the acquisition

of the company which will lead to an increase in the profit-making of the

organization. The AASB 128 is responsible to issue guidelines in the joint ventures

and acquisition. It is expected that the organization must follow the guidelines as is

issued. Both of the options are available for the organization to acquire FAB ltd. On

one hand, there is the method of acquisition and purchase of the company which

could imply the direct purchase of the organization and on the other hand, there

remains the acquisition of the shares of the organization (Chua, Cheong and Gould

2012). According to both of the options, the organization is provided with a huge

amount of profit in terms of the method of acquisition and purchase. As a result, it

will serve as an exclusive case of the accounting process of equity and

consolidation. This has been provided in details below:

Equity Accounting Consolidation Accounting

Equity accounting is the accounting

process where it holds considering the

assets as an investment in the

organization which is associated. It is

practiced when an organization holds at

least twenty percent to fifty percent of

share in an organization.

Consolidation accounting is the

accounting process where the

amalgamation of the results of the

finance with all other subsidiaries is

considered. The combination of all the

statement of finance of the parent

organization is considered.

More than twenty percent of the share in

the subsidiary organization is associated.

There is a fifty percent share of the

subsidiary company related to the parent

organization.

The items of finance are not associated

fully with the associate company. The

company only uses the organizational

investment, which has been already

listed in the balance sheet of the parent

organization.

The items of finance are associated with

the subsidiary organization.

The standards of accounting are also important tools for the organization. The

standards produce regulations and rules so as to report the competencies during a

single period. The paper will basically follow 3 units to be considered into the

analysis of this report. The first part of the report will deal with the equity and

consolidated accounting theory where the discussion on AASB 10 and AASB 128

will be discussed in this section. The second section of the report will deal with

transactions within the intragroup of the organization, JKY Ltd. where the discussion

on AASB 10 and AASB 10 will be discussed in this section (Walton, Haller and

Raffournier 2003). The third section of the report will deal with the disclosure of the

NCI i.e. needed in accordance with the AASB 101. Finally, the summary of the whole

report will be provided which will help in summarizing every section in detail.

Part A response

The ASX listed company named FAB Ltd. would be acquired by JKY Ltd. Hence it

can be expected that this organization has a lump sum amount of money or rather

profit in its cash treasure. The special effects could be maintained on the acquisition

of the company which will lead to an increase in the profit-making of the

organization. The AASB 128 is responsible to issue guidelines in the joint ventures

and acquisition. It is expected that the organization must follow the guidelines as is

issued. Both of the options are available for the organization to acquire FAB ltd. On

one hand, there is the method of acquisition and purchase of the company which

could imply the direct purchase of the organization and on the other hand, there

remains the acquisition of the shares of the organization (Chua, Cheong and Gould

2012). According to both of the options, the organization is provided with a huge

amount of profit in terms of the method of acquisition and purchase. As a result, it

will serve as an exclusive case of the accounting process of equity and

consolidation. This has been provided in details below:

Equity Accounting Consolidation Accounting

Equity accounting is the accounting

process where it holds considering the

assets as an investment in the

organization which is associated. It is

practiced when an organization holds at

least twenty percent to fifty percent of

share in an organization.

Consolidation accounting is the

accounting process where the

amalgamation of the results of the

finance with all other subsidiaries is

considered. The combination of all the

statement of finance of the parent

organization is considered.

More than twenty percent of the share in

the subsidiary organization is associated.

There is a fifty percent share of the

subsidiary company related to the parent

organization.

The items of finance are not associated

fully with the associate company. The

company only uses the organizational

investment, which has been already

listed in the balance sheet of the parent

organization.

The items of finance are associated with

the subsidiary organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The process is based on full equity that

does not allow on the basis of the full

acquisition instead of the part of the

investment of the parent organization in

the associated organization.

There is a total consolidation in the

method of acquisition.

Table 1: Equity accounting and Consolidation accounting

It will be proper and the best method if JTY Ltd. chooses the consolidation method of

accounting which the method of acquisition and purchase. Thus, it will help the

company to highlight the different aspects of the reporting of finance. It would also

assist in the consolidation of the company determining the statement of finance of

the subsidiary organization. It can be noted that there are relevant opportunities in

the increment of the goodwill and trust of the organization, which would help in

gaining the profit while attaining the trust from the people inside as well as outside

the organization (Alfredson et al., 2005). The best practice of the organization is to

achieve the benefits of the methods of acquisitions, due to the fact that the statement

of finance of the subsidiary organization is linked with the parent organization. The

best practice could be performed by reposting the common financial transaction of

the company. There would be a benefit for JTY Ltd. to avail the benefits of the

method of post-acquisition and acquisition. Hence, it can be said that the method of

purchase acquisition tends to be successful for the organization.

According to the consolidated method of accounting, there is a total disclosure of the

statement of finance of the parent organization on the basis of the subsidiary

organization.

Particulars JTY Ltd. FAB Ltd.

Assets 307000 147000

Liabilities -262000 -125000

Total Liabilities and

Equities

-307000 -147000

Table 2: Consolidated Balance Sheet

It is totally evident that the total terms under the balance sheet are listed on the

same balance sheet, which propounds the huge impact on the process of practice.

This will help the organization in managing the statement of finance for two of the

organizations. The huge effect of the practice will assist in finding the fair and true

value of reporting of the statement of finance of the mutual post acquisition of the

organization.

does not allow on the basis of the full

acquisition instead of the part of the

investment of the parent organization in

the associated organization.

There is a total consolidation in the

method of acquisition.

Table 1: Equity accounting and Consolidation accounting

It will be proper and the best method if JTY Ltd. chooses the consolidation method of

accounting which the method of acquisition and purchase. Thus, it will help the

company to highlight the different aspects of the reporting of finance. It would also

assist in the consolidation of the company determining the statement of finance of

the subsidiary organization. It can be noted that there are relevant opportunities in

the increment of the goodwill and trust of the organization, which would help in

gaining the profit while attaining the trust from the people inside as well as outside

the organization (Alfredson et al., 2005). The best practice of the organization is to

achieve the benefits of the methods of acquisitions, due to the fact that the statement

of finance of the subsidiary organization is linked with the parent organization. The

best practice could be performed by reposting the common financial transaction of

the company. There would be a benefit for JTY Ltd. to avail the benefits of the

method of post-acquisition and acquisition. Hence, it can be said that the method of

purchase acquisition tends to be successful for the organization.

According to the consolidated method of accounting, there is a total disclosure of the

statement of finance of the parent organization on the basis of the subsidiary

organization.

Particulars JTY Ltd. FAB Ltd.

Assets 307000 147000

Liabilities -262000 -125000

Total Liabilities and

Equities

-307000 -147000

Table 2: Consolidated Balance Sheet

It is totally evident that the total terms under the balance sheet are listed on the

same balance sheet, which propounds the huge impact on the process of practice.

This will help the organization in managing the statement of finance for two of the

organizations. The huge effect of the practice will assist in finding the fair and true

value of reporting of the statement of finance of the mutual post acquisition of the

organization.

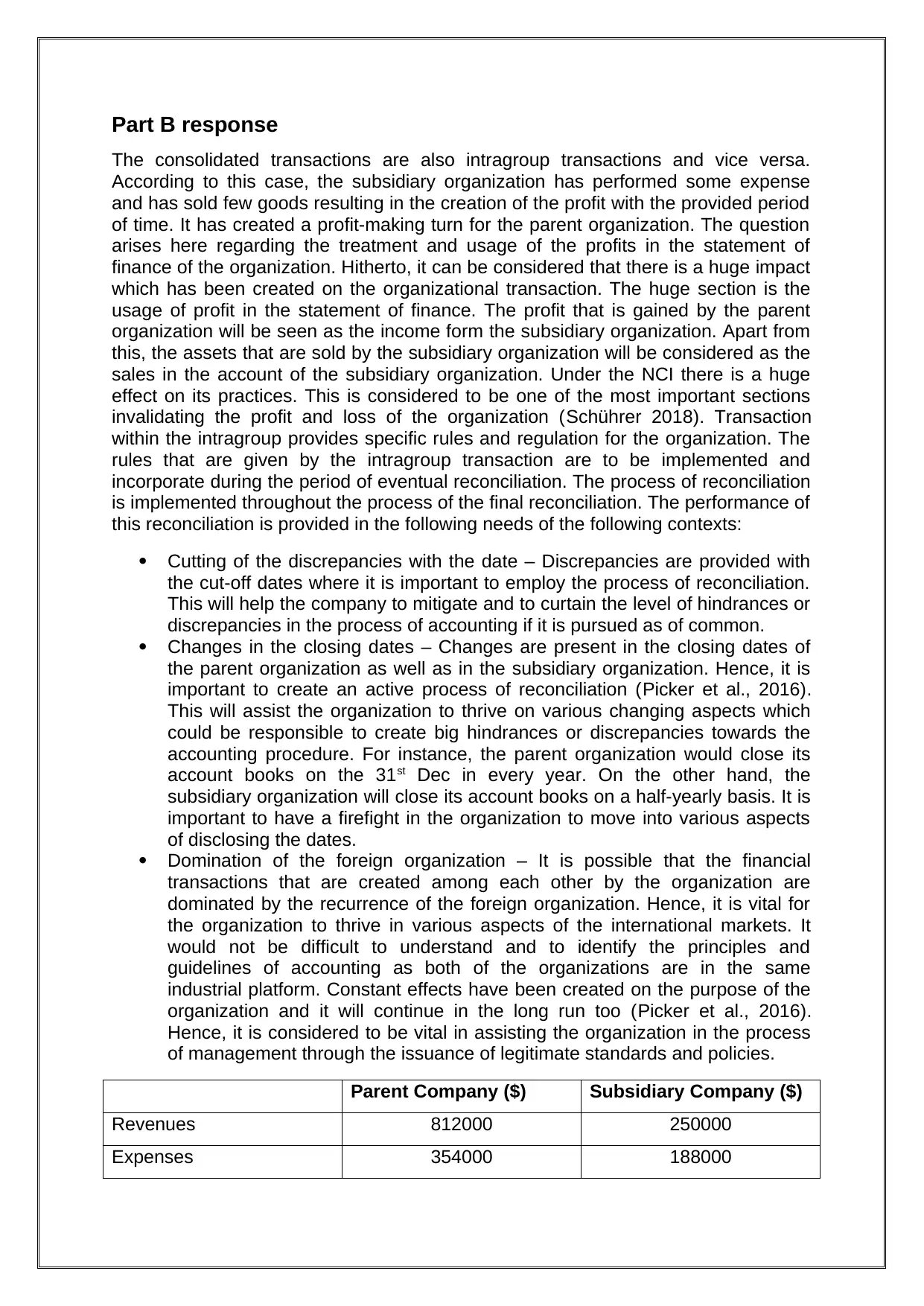

Part B response

The consolidated transactions are also intragroup transactions and vice versa.

According to this case, the subsidiary organization has performed some expense

and has sold few goods resulting in the creation of the profit with the provided period

of time. It has created a profit-making turn for the parent organization. The question

arises here regarding the treatment and usage of the profits in the statement of

finance of the organization. Hitherto, it can be considered that there is a huge impact

which has been created on the organizational transaction. The huge section is the

usage of profit in the statement of finance. The profit that is gained by the parent

organization will be seen as the income form the subsidiary organization. Apart from

this, the assets that are sold by the subsidiary organization will be considered as the

sales in the account of the subsidiary organization. Under the NCI there is a huge

effect on its practices. This is considered to be one of the most important sections

invalidating the profit and loss of the organization (Schührer 2018). Transaction

within the intragroup provides specific rules and regulation for the organization. The

rules that are given by the intragroup transaction are to be implemented and

incorporate during the period of eventual reconciliation. The process of reconciliation

is implemented throughout the process of the final reconciliation. The performance of

this reconciliation is provided in the following needs of the following contexts:

Cutting of the discrepancies with the date – Discrepancies are provided with

the cut-off dates where it is important to employ the process of reconciliation.

This will help the company to mitigate and to curtain the level of hindrances or

discrepancies in the process of accounting if it is pursued as of common.

Changes in the closing dates – Changes are present in the closing dates of

the parent organization as well as in the subsidiary organization. Hence, it is

important to create an active process of reconciliation (Picker et al., 2016).

This will assist the organization to thrive on various changing aspects which

could be responsible to create big hindrances or discrepancies towards the

accounting procedure. For instance, the parent organization would close its

account books on the 31st Dec in every year. On the other hand, the

subsidiary organization will close its account books on a half-yearly basis. It is

important to have a firefight in the organization to move into various aspects

of disclosing the dates.

Domination of the foreign organization – It is possible that the financial

transactions that are created among each other by the organization are

dominated by the recurrence of the foreign organization. Hence, it is vital for

the organization to thrive in various aspects of the international markets. It

would not be difficult to understand and to identify the principles and

guidelines of accounting as both of the organizations are in the same

industrial platform. Constant effects have been created on the purpose of the

organization and it will continue in the long run too (Picker et al., 2016).

Hence, it is considered to be vital in assisting the organization in the process

of management through the issuance of legitimate standards and policies.

Parent Company ($) Subsidiary Company ($)

Revenues 812000 250000

Expenses 354000 188000

The consolidated transactions are also intragroup transactions and vice versa.

According to this case, the subsidiary organization has performed some expense

and has sold few goods resulting in the creation of the profit with the provided period

of time. It has created a profit-making turn for the parent organization. The question

arises here regarding the treatment and usage of the profits in the statement of

finance of the organization. Hitherto, it can be considered that there is a huge impact

which has been created on the organizational transaction. The huge section is the

usage of profit in the statement of finance. The profit that is gained by the parent

organization will be seen as the income form the subsidiary organization. Apart from

this, the assets that are sold by the subsidiary organization will be considered as the

sales in the account of the subsidiary organization. Under the NCI there is a huge

effect on its practices. This is considered to be one of the most important sections

invalidating the profit and loss of the organization (Schührer 2018). Transaction

within the intragroup provides specific rules and regulation for the organization. The

rules that are given by the intragroup transaction are to be implemented and

incorporate during the period of eventual reconciliation. The process of reconciliation

is implemented throughout the process of the final reconciliation. The performance of

this reconciliation is provided in the following needs of the following contexts:

Cutting of the discrepancies with the date – Discrepancies are provided with

the cut-off dates where it is important to employ the process of reconciliation.

This will help the company to mitigate and to curtain the level of hindrances or

discrepancies in the process of accounting if it is pursued as of common.

Changes in the closing dates – Changes are present in the closing dates of

the parent organization as well as in the subsidiary organization. Hence, it is

important to create an active process of reconciliation (Picker et al., 2016).

This will assist the organization to thrive on various changing aspects which

could be responsible to create big hindrances or discrepancies towards the

accounting procedure. For instance, the parent organization would close its

account books on the 31st Dec in every year. On the other hand, the

subsidiary organization will close its account books on a half-yearly basis. It is

important to have a firefight in the organization to move into various aspects

of disclosing the dates.

Domination of the foreign organization – It is possible that the financial

transactions that are created among each other by the organization are

dominated by the recurrence of the foreign organization. Hence, it is vital for

the organization to thrive in various aspects of the international markets. It

would not be difficult to understand and to identify the principles and

guidelines of accounting as both of the organizations are in the same

industrial platform. Constant effects have been created on the purpose of the

organization and it will continue in the long run too (Picker et al., 2016).

Hence, it is considered to be vital in assisting the organization in the process

of management through the issuance of legitimate standards and policies.

Parent Company ($) Subsidiary Company ($)

Revenues 812000 250000

Expenses 354000 188000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

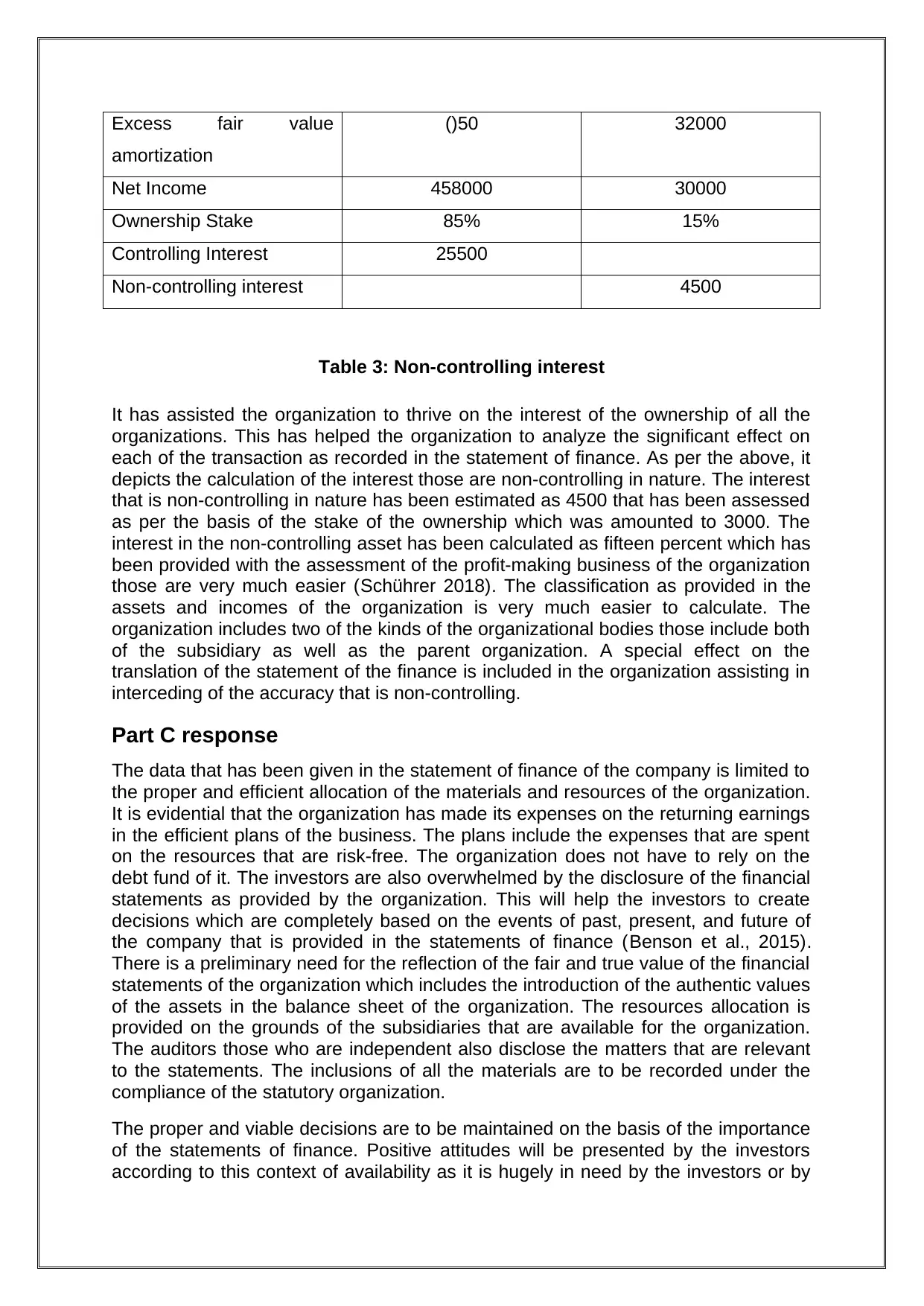

Excess fair value

amortization

()50 32000

Net Income 458000 30000

Ownership Stake 85% 15%

Controlling Interest 25500

Non-controlling interest 4500

Table 3: Non-controlling interest

It has assisted the organization to thrive on the interest of the ownership of all the

organizations. This has helped the organization to analyze the significant effect on

each of the transaction as recorded in the statement of finance. As per the above, it

depicts the calculation of the interest those are non-controlling in nature. The interest

that is non-controlling in nature has been estimated as 4500 that has been assessed

as per the basis of the stake of the ownership which was amounted to 3000. The

interest in the non-controlling asset has been calculated as fifteen percent which has

been provided with the assessment of the profit-making business of the organization

those are very much easier (Schührer 2018). The classification as provided in the

assets and incomes of the organization is very much easier to calculate. The

organization includes two of the kinds of the organizational bodies those include both

of the subsidiary as well as the parent organization. A special effect on the

translation of the statement of the finance is included in the organization assisting in

interceding of the accuracy that is non-controlling.

Part C response

The data that has been given in the statement of finance of the company is limited to

the proper and efficient allocation of the materials and resources of the organization.

It is evidential that the organization has made its expenses on the returning earnings

in the efficient plans of the business. The plans include the expenses that are spent

on the resources that are risk-free. The organization does not have to rely on the

debt fund of it. The investors are also overwhelmed by the disclosure of the financial

statements as provided by the organization. This will help the investors to create

decisions which are completely based on the events of past, present, and future of

the company that is provided in the statements of finance (Benson et al., 2015).

There is a preliminary need for the reflection of the fair and true value of the financial

statements of the organization which includes the introduction of the authentic values

of the assets in the balance sheet of the organization. The resources allocation is

provided on the grounds of the subsidiaries that are available for the organization.

The auditors those who are independent also disclose the matters that are relevant

to the statements. The inclusions of all the materials are to be recorded under the

compliance of the statutory organization.

The proper and viable decisions are to be maintained on the basis of the importance

of the statements of finance. Positive attitudes will be presented by the investors

according to this context of availability as it is hugely in need by the investors or by

amortization

()50 32000

Net Income 458000 30000

Ownership Stake 85% 15%

Controlling Interest 25500

Non-controlling interest 4500

Table 3: Non-controlling interest

It has assisted the organization to thrive on the interest of the ownership of all the

organizations. This has helped the organization to analyze the significant effect on

each of the transaction as recorded in the statement of finance. As per the above, it

depicts the calculation of the interest those are non-controlling in nature. The interest

that is non-controlling in nature has been estimated as 4500 that has been assessed

as per the basis of the stake of the ownership which was amounted to 3000. The

interest in the non-controlling asset has been calculated as fifteen percent which has

been provided with the assessment of the profit-making business of the organization

those are very much easier (Schührer 2018). The classification as provided in the

assets and incomes of the organization is very much easier to calculate. The

organization includes two of the kinds of the organizational bodies those include both

of the subsidiary as well as the parent organization. A special effect on the

translation of the statement of the finance is included in the organization assisting in

interceding of the accuracy that is non-controlling.

Part C response

The data that has been given in the statement of finance of the company is limited to

the proper and efficient allocation of the materials and resources of the organization.

It is evidential that the organization has made its expenses on the returning earnings

in the efficient plans of the business. The plans include the expenses that are spent

on the resources that are risk-free. The organization does not have to rely on the

debt fund of it. The investors are also overwhelmed by the disclosure of the financial

statements as provided by the organization. This will help the investors to create

decisions which are completely based on the events of past, present, and future of

the company that is provided in the statements of finance (Benson et al., 2015).

There is a preliminary need for the reflection of the fair and true value of the financial

statements of the organization which includes the introduction of the authentic values

of the assets in the balance sheet of the organization. The resources allocation is

provided on the grounds of the subsidiaries that are available for the organization.

The auditors those who are independent also disclose the matters that are relevant

to the statements. The inclusions of all the materials are to be recorded under the

compliance of the statutory organization.

The proper and viable decisions are to be maintained on the basis of the importance

of the statements of finance. Positive attitudes will be presented by the investors

according to this context of availability as it is hugely in need by the investors or by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the stakeholder due to the fact that their vital decisions are to be made after the

company discloses its financial statement (Benson et al., 2015). The data like the

risk of taxation is to be presented by the organization in its report of finance which

would help the stock market to identify, understand and to make legitimate decisions

on the terms of investments and expenditures. This is important as when the

organization is getting the benefit of allowing incurring more tax the profit after their

taxation would gradually reduce. It would result in the falling of the net income of the

organization and on that the investors and stakeholders of the company will

accordingly give their reactions. Hence, the organization is going to cease its

operation of the business as there are huge chances of the organization to lose the

grip of the market. Hence, it is relevant to analyze the statements of finance by the

users. This is thereby suggested on the basis of the standard of accounting that is,

AS 10 (Barth et al., 2008). Therefore, it had been made compulsory by the Australian

Accounting Standard Board that provides IFRS all across the globe. The standards

of accounting are accepted throughout the globe by the organizations, companies or

business so as to present their statement of finance in a viable manner. The purpose

of the AASB is that it is responsible for the issuance of the guidelines that are in

regard to the structure, content, and presentation of the statements of finance as

conducted by the organizations.

The correct and feasible choices are to be kept up based on the significance of the

announcements of fund. Uplifting mentalities will be displayed by the speculators as

indicated by this setting of accessibility as it is immensely deprived by the

speculators or by the partner because of the way that their indispensable choices are

to be made after the organization uncovers its budget summary (Benson et al.,

2015). The information like the danger of tax assessment is to be exhibited by the

organization in its report of account which would assist the securities exchange with

identifying, comprehend and to settle on authentic choices on the terms of

speculations and uses. It would result in the falling of the net gain of the organization

and on that the speculators and partners of the organization will give their

responses. Henceforth, it is applicable to break down the reporting of account by the

clients. This is along these lines proposed based on the standard of bookkeeping

that is, AS 10 (Barth et al., 2008). In this manner, it had been made obligatory by the

Australian Accounting Standard Board that gives IFRS the whole way across the

globe. The measures of bookkeeping are acknowledged all through the globe by the

associations, organizations or business to display their announcement of fund in a

reasonable way. The reason for the AASB is that it is in charge of the issuance of the

rules that are concerning the structure, substance, and introduction of the

announcements of fund as led by the organization.

The following reasons are provided to provide the effect of the disclosure of the

financial statement by the organizations:

This will assist in portraying of the true and fair value of the assets of the

organizations.

This will also help in the payment of dividends.

There will also be the fair and true value in the price of the assets as listed in

the statements of finance in the organization.

It will assist in showing the true and fair rate of return of the capital those are

employed.

company discloses its financial statement (Benson et al., 2015). The data like the

risk of taxation is to be presented by the organization in its report of finance which

would help the stock market to identify, understand and to make legitimate decisions

on the terms of investments and expenditures. This is important as when the

organization is getting the benefit of allowing incurring more tax the profit after their

taxation would gradually reduce. It would result in the falling of the net income of the

organization and on that the investors and stakeholders of the company will

accordingly give their reactions. Hence, the organization is going to cease its

operation of the business as there are huge chances of the organization to lose the

grip of the market. Hence, it is relevant to analyze the statements of finance by the

users. This is thereby suggested on the basis of the standard of accounting that is,

AS 10 (Barth et al., 2008). Therefore, it had been made compulsory by the Australian

Accounting Standard Board that provides IFRS all across the globe. The standards

of accounting are accepted throughout the globe by the organizations, companies or

business so as to present their statement of finance in a viable manner. The purpose

of the AASB is that it is responsible for the issuance of the guidelines that are in

regard to the structure, content, and presentation of the statements of finance as

conducted by the organizations.

The correct and feasible choices are to be kept up based on the significance of the

announcements of fund. Uplifting mentalities will be displayed by the speculators as

indicated by this setting of accessibility as it is immensely deprived by the

speculators or by the partner because of the way that their indispensable choices are

to be made after the organization uncovers its budget summary (Benson et al.,

2015). The information like the danger of tax assessment is to be exhibited by the

organization in its report of account which would assist the securities exchange with

identifying, comprehend and to settle on authentic choices on the terms of

speculations and uses. It would result in the falling of the net gain of the organization

and on that the speculators and partners of the organization will give their

responses. Henceforth, it is applicable to break down the reporting of account by the

clients. This is along these lines proposed based on the standard of bookkeeping

that is, AS 10 (Barth et al., 2008). In this manner, it had been made obligatory by the

Australian Accounting Standard Board that gives IFRS the whole way across the

globe. The measures of bookkeeping are acknowledged all through the globe by the

associations, organizations or business to display their announcement of fund in a

reasonable way. The reason for the AASB is that it is in charge of the issuance of the

rules that are concerning the structure, substance, and introduction of the

announcements of fund as led by the organization.

The following reasons are provided to provide the effect of the disclosure of the

financial statement by the organizations:

This will assist in portraying of the true and fair value of the assets of the

organizations.

This will also help in the payment of dividends.

There will also be the fair and true value in the price of the assets as listed in

the statements of finance in the organization.

It will assist in showing the true and fair rate of return of the capital those are

employed.

The revaluation of the assets helps in providing the current status and value

of the assets to the investors (Benson et al., 2015).

Conclusion

It can be concluded by saying that it is vital to make the disclosures in the statement

of finance because it will assist the organization to thrive on to the different aspect of

the reporting of finance. The market of securities or the investor or any other

companies get interested in the statement of finance of the company. NCI’s special

effect is to be presented in the statement of finance of the organization. The

organizations which hold a maximum of fifty percent of the share of the subsidiary

company has the right to disclose the NCI as equity of owners. Hence, if there are no

such conditions available then it would not assist the organization to disclose their

rights of voting and equity in the organization. These are the most significant impact

of the process as it helps in giving the fair and true value of report of the

organization.

Reference:

Alfredson, K., Leo, K., Picker, R., Pacter, P., Radford, J. and Wise, V.,

2005. Applying international accounting standards. John Wiley & Sons.

Barth, M.E., Landsman, W.R. and Lang, M.H., 2008. International accounting

standards and accounting quality. Journal of accounting research, 46(3), pp.467-

498.

Benson, K., Clarkson, P.M., Smith, T., and Tutticci, I., 2015. A review of accounting

research in the Asia Pacific region. Australian Journal of Management, 40(1), pp.36-

88.

Chua, Y.L., Cheong, C.S. and Gould, G., 2012. The impact of mandatory IFRS

adoption on accounting quality: Evidence from Australia. Journal of International

accounting research, 11(1), pp.119-146.

Picker, R., Clark, K., Dunn, J., Kolitz, D., Levine, G., Loftus, J. and Van der Tas, L.,

2016. Applying IFRS standards. John Wiley & Sons.

Schührer, S., 2018. Identifying policy entrepreneurs of public sector accounting

agenda setting in Australia. Accounting, Auditing & Accountability Journal, 31(4),

pp.1067-1097.

Walton, P., Haller, A. and Raffournier, B. eds., 2003. International accounting.

Cengage Learning EMEA.

of the assets to the investors (Benson et al., 2015).

Conclusion

It can be concluded by saying that it is vital to make the disclosures in the statement

of finance because it will assist the organization to thrive on to the different aspect of

the reporting of finance. The market of securities or the investor or any other

companies get interested in the statement of finance of the company. NCI’s special

effect is to be presented in the statement of finance of the organization. The

organizations which hold a maximum of fifty percent of the share of the subsidiary

company has the right to disclose the NCI as equity of owners. Hence, if there are no

such conditions available then it would not assist the organization to disclose their

rights of voting and equity in the organization. These are the most significant impact

of the process as it helps in giving the fair and true value of report of the

organization.

Reference:

Alfredson, K., Leo, K., Picker, R., Pacter, P., Radford, J. and Wise, V.,

2005. Applying international accounting standards. John Wiley & Sons.

Barth, M.E., Landsman, W.R. and Lang, M.H., 2008. International accounting

standards and accounting quality. Journal of accounting research, 46(3), pp.467-

498.

Benson, K., Clarkson, P.M., Smith, T., and Tutticci, I., 2015. A review of accounting

research in the Asia Pacific region. Australian Journal of Management, 40(1), pp.36-

88.

Chua, Y.L., Cheong, C.S. and Gould, G., 2012. The impact of mandatory IFRS

adoption on accounting quality: Evidence from Australia. Journal of International

accounting research, 11(1), pp.119-146.

Picker, R., Clark, K., Dunn, J., Kolitz, D., Levine, G., Loftus, J. and Van der Tas, L.,

2016. Applying IFRS standards. John Wiley & Sons.

Schührer, S., 2018. Identifying policy entrepreneurs of public sector accounting

agenda setting in Australia. Accounting, Auditing & Accountability Journal, 31(4),

pp.1067-1097.

Walton, P., Haller, A. and Raffournier, B. eds., 2003. International accounting.

Cengage Learning EMEA.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.