BUACC5933 - Cost and Management Accounting Assignment Analysis

VerifiedAdded on 2021/06/17

|11

|3080

|79

Homework Assignment

AI Summary

This assignment solution for BUACC5933, a cost and management accounting course, covers various aspects of cost accounting and corporate governance. Part 1 focuses on overhead allocation methods, including factory-wide and activity-based costing, along with determining appropriate cost drivers. Part 2 delves into product line profitability, evaluating the impact of discontinuing a product line, and calculating equivalent units using the FIFO method for process costing. Finally, Part 3 examines the significance of accounting information and financial reporting in enhancing corporate governance, emphasizing the role of financial reporting in providing transparency, mitigating information asymmetry, and facilitating effective decision-making by stakeholders. The solution highlights the importance of credible, timely, and relevant financial information for effective corporate governance and contract mechanisms.

qwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmrtyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyuiopas

BUACC5933 – Cost and Management

Accounting

Semester 1 2018

uiopasdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmrtyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyuiopas

BUACC5933 – Cost and Management

Accounting

Semester 1 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting

PART 1

QUESTION1

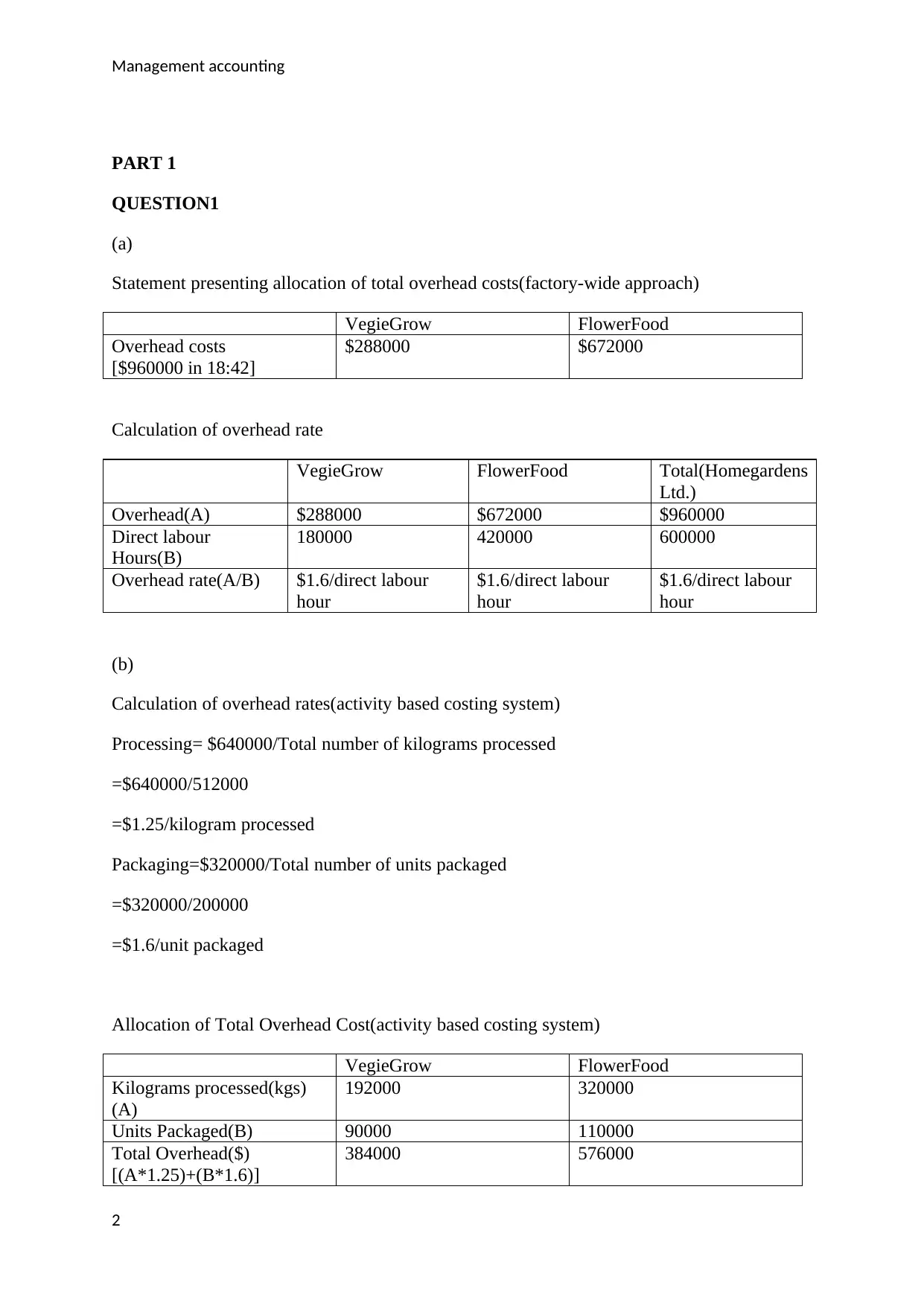

(a)

Statement presenting allocation of total overhead costs(factory-wide approach)

VegieGrow FlowerFood

Overhead costs

[$960000 in 18:42]

$288000 $672000

Calculation of overhead rate

VegieGrow FlowerFood Total(Homegardens

Ltd.)

Overhead(A) $288000 $672000 $960000

Direct labour

Hours(B)

180000 420000 600000

Overhead rate(A/B) $1.6/direct labour

hour

$1.6/direct labour

hour

$1.6/direct labour

hour

(b)

Calculation of overhead rates(activity based costing system)

Processing= $640000/Total number of kilograms processed

=$640000/512000

=$1.25/kilogram processed

Packaging=$320000/Total number of units packaged

=$320000/200000

=$1.6/unit packaged

Allocation of Total Overhead Cost(activity based costing system)

VegieGrow FlowerFood

Kilograms processed(kgs)

(A)

192000 320000

Units Packaged(B) 90000 110000

Total Overhead($)

[(A*1.25)+(B*1.6)]

384000 576000

2

PART 1

QUESTION1

(a)

Statement presenting allocation of total overhead costs(factory-wide approach)

VegieGrow FlowerFood

Overhead costs

[$960000 in 18:42]

$288000 $672000

Calculation of overhead rate

VegieGrow FlowerFood Total(Homegardens

Ltd.)

Overhead(A) $288000 $672000 $960000

Direct labour

Hours(B)

180000 420000 600000

Overhead rate(A/B) $1.6/direct labour

hour

$1.6/direct labour

hour

$1.6/direct labour

hour

(b)

Calculation of overhead rates(activity based costing system)

Processing= $640000/Total number of kilograms processed

=$640000/512000

=$1.25/kilogram processed

Packaging=$320000/Total number of units packaged

=$320000/200000

=$1.6/unit packaged

Allocation of Total Overhead Cost(activity based costing system)

VegieGrow FlowerFood

Kilograms processed(kgs)

(A)

192000 320000

Units Packaged(B) 90000 110000

Total Overhead($)

[(A*1.25)+(B*1.6)]

384000 576000

2

Management accounting

(c) Determination of an appropriate cost driver is very important and usually the following

principles are adopted for such process:

Service or use

Survey method

Ability to bear

A basis once adopted must be reviewed at periodic intervals to improve upon the accuracy of

apportionment.

QUESTION 2

(a)Statement presenting calculation of overhead rates

Scheduling and

travel

Setup time Supervision

Estimated

overhead($)(A)

85000 90000 60000

Cost drivers Hours of travel Number of setups Direct labour costs

Total of cost

drivers(B)

1250 600 400000

Overhead rate(A/B) $68/hour $150/setup $0.15/direct labour$

Assignment of overhead cost to each product line

Product line Details Overhead($)

Commercial [(750*68)+(350*150)+(100000*0.15)=] 118500

Residential [(500*68)+(250*150)+(300000*0.15)=] 116500

(b)Statement presenting operating income(using activity based overhead rates)

Commercial Residential

Revenues($) 300000 480000

Direct material

costs($)

30000 50000

Direct labour

costs($)

100000 300000

Overhead

costs($)

118500 248500 116500 466500

Operating

income/(loss)

($)

51500 13500

3

(c) Determination of an appropriate cost driver is very important and usually the following

principles are adopted for such process:

Service or use

Survey method

Ability to bear

A basis once adopted must be reviewed at periodic intervals to improve upon the accuracy of

apportionment.

QUESTION 2

(a)Statement presenting calculation of overhead rates

Scheduling and

travel

Setup time Supervision

Estimated

overhead($)(A)

85000 90000 60000

Cost drivers Hours of travel Number of setups Direct labour costs

Total of cost

drivers(B)

1250 600 400000

Overhead rate(A/B) $68/hour $150/setup $0.15/direct labour$

Assignment of overhead cost to each product line

Product line Details Overhead($)

Commercial [(750*68)+(350*150)+(100000*0.15)=] 118500

Residential [(500*68)+(250*150)+(300000*0.15)=] 116500

(b)Statement presenting operating income(using activity based overhead rates)

Commercial Residential

Revenues($) 300000 480000

Direct material

costs($)

30000 50000

Direct labour

costs($)

100000 300000

Overhead

costs($)

118500 248500 116500 466500

Operating

income/(loss)

($)

51500 13500

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting

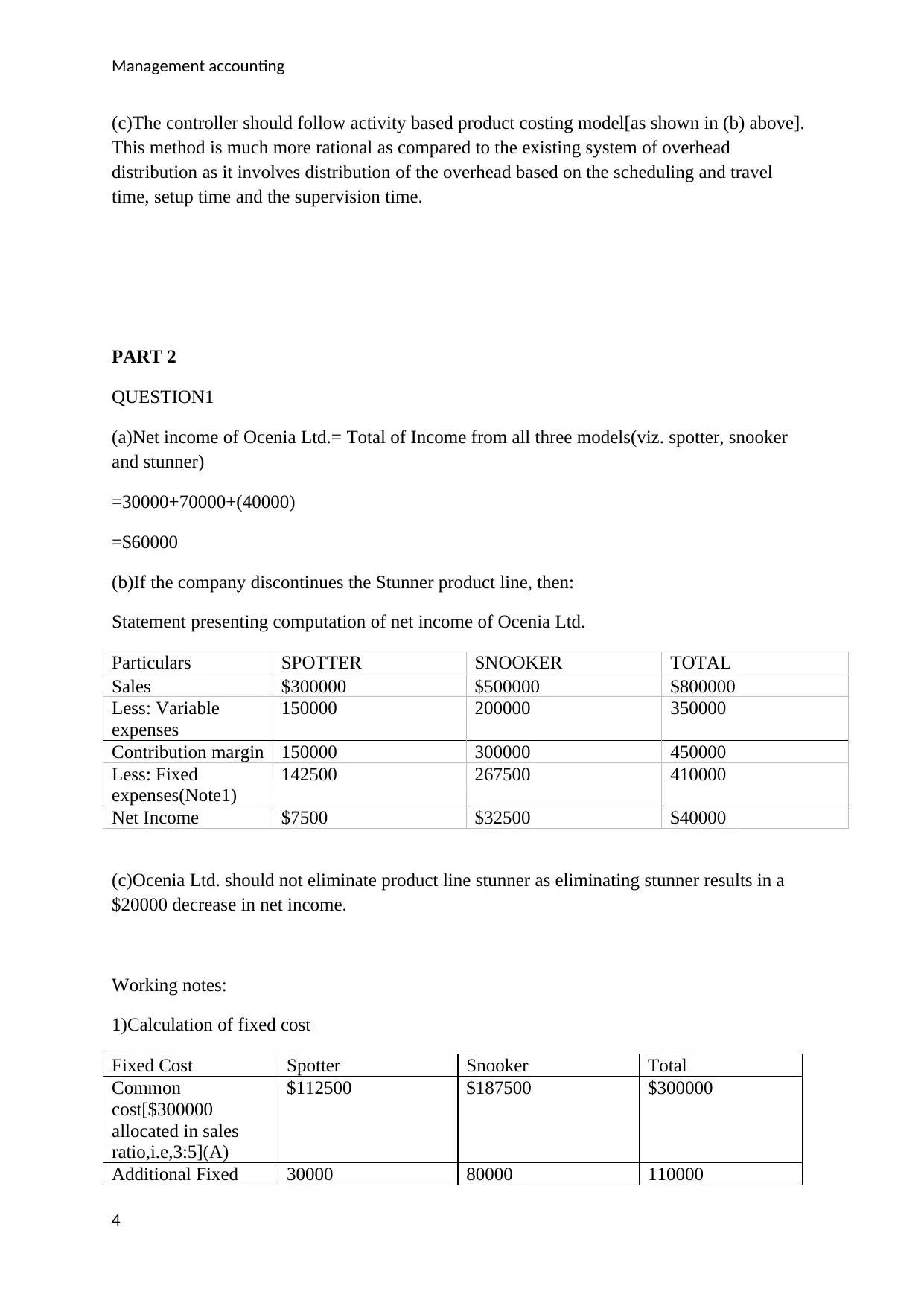

(c)The controller should follow activity based product costing model[as shown in (b) above].

This method is much more rational as compared to the existing system of overhead

distribution as it involves distribution of the overhead based on the scheduling and travel

time, setup time and the supervision time.

PART 2

QUESTION1

(a)Net income of Ocenia Ltd.= Total of Income from all three models(viz. spotter, snooker

and stunner)

=30000+70000+(40000)

=$60000

(b)If the company discontinues the Stunner product line, then:

Statement presenting computation of net income of Ocenia Ltd.

Particulars SPOTTER SNOOKER TOTAL

Sales $300000 $500000 $800000

Less: Variable

expenses

150000 200000 350000

Contribution margin 150000 300000 450000

Less: Fixed

expenses(Note1)

142500 267500 410000

Net Income $7500 $32500 $40000

(c)Ocenia Ltd. should not eliminate product line stunner as eliminating stunner results in a

$20000 decrease in net income.

Working notes:

1)Calculation of fixed cost

Fixed Cost Spotter Snooker Total

Common

cost[$300000

allocated in sales

ratio,i.e,3:5](A)

$112500 $187500 $300000

Additional Fixed 30000 80000 110000

4

(c)The controller should follow activity based product costing model[as shown in (b) above].

This method is much more rational as compared to the existing system of overhead

distribution as it involves distribution of the overhead based on the scheduling and travel

time, setup time and the supervision time.

PART 2

QUESTION1

(a)Net income of Ocenia Ltd.= Total of Income from all three models(viz. spotter, snooker

and stunner)

=30000+70000+(40000)

=$60000

(b)If the company discontinues the Stunner product line, then:

Statement presenting computation of net income of Ocenia Ltd.

Particulars SPOTTER SNOOKER TOTAL

Sales $300000 $500000 $800000

Less: Variable

expenses

150000 200000 350000

Contribution margin 150000 300000 450000

Less: Fixed

expenses(Note1)

142500 267500 410000

Net Income $7500 $32500 $40000

(c)Ocenia Ltd. should not eliminate product line stunner as eliminating stunner results in a

$20000 decrease in net income.

Working notes:

1)Calculation of fixed cost

Fixed Cost Spotter Snooker Total

Common

cost[$300000

allocated in sales

ratio,i.e,3:5](A)

$112500 $187500 $300000

Additional Fixed 30000 80000 110000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting

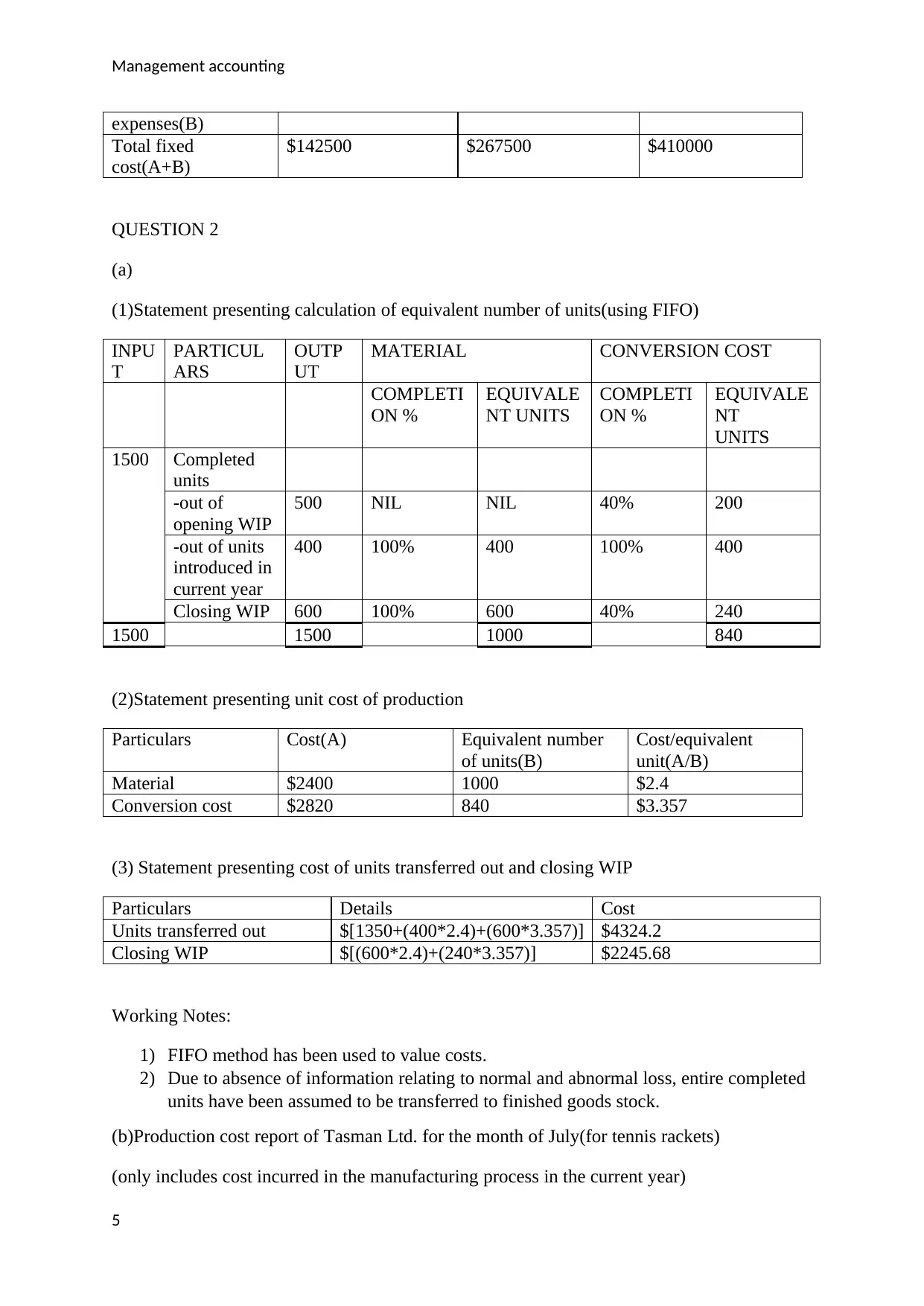

expenses(B)

Total fixed

cost(A+B)

$142500 $267500 $410000

QUESTION 2

(a)

(1)Statement presenting calculation of equivalent number of units(using FIFO)

INPU

T

PARTICUL

ARS

OUTP

UT

MATERIAL CONVERSION COST

COMPLETI

ON %

EQUIVALE

NT UNITS

COMPLETI

ON %

EQUIVALE

NT

UNITS

1500 Completed

units

-out of

opening WIP

500 NIL NIL 40% 200

-out of units

introduced in

current year

400 100% 400 100% 400

Closing WIP 600 100% 600 40% 240

1500 1500 1000 840

(2)Statement presenting unit cost of production

Particulars Cost(A) Equivalent number

of units(B)

Cost/equivalent

unit(A/B)

Material $2400 1000 $2.4

Conversion cost $2820 840 $3.357

(3) Statement presenting cost of units transferred out and closing WIP

Particulars Details Cost

Units transferred out $[1350+(400*2.4)+(600*3.357)] $4324.2

Closing WIP $[(600*2.4)+(240*3.357)] $2245.68

Working Notes:

1) FIFO method has been used to value costs.

2) Due to absence of information relating to normal and abnormal loss, entire completed

units have been assumed to be transferred to finished goods stock.

(b)Production cost report of Tasman Ltd. for the month of July(for tennis rackets)

(only includes cost incurred in the manufacturing process in the current year)

5

expenses(B)

Total fixed

cost(A+B)

$142500 $267500 $410000

QUESTION 2

(a)

(1)Statement presenting calculation of equivalent number of units(using FIFO)

INPU

T

PARTICUL

ARS

OUTP

UT

MATERIAL CONVERSION COST

COMPLETI

ON %

EQUIVALE

NT UNITS

COMPLETI

ON %

EQUIVALE

NT

UNITS

1500 Completed

units

-out of

opening WIP

500 NIL NIL 40% 200

-out of units

introduced in

current year

400 100% 400 100% 400

Closing WIP 600 100% 600 40% 240

1500 1500 1000 840

(2)Statement presenting unit cost of production

Particulars Cost(A) Equivalent number

of units(B)

Cost/equivalent

unit(A/B)

Material $2400 1000 $2.4

Conversion cost $2820 840 $3.357

(3) Statement presenting cost of units transferred out and closing WIP

Particulars Details Cost

Units transferred out $[1350+(400*2.4)+(600*3.357)] $4324.2

Closing WIP $[(600*2.4)+(240*3.357)] $2245.68

Working Notes:

1) FIFO method has been used to value costs.

2) Due to absence of information relating to normal and abnormal loss, entire completed

units have been assumed to be transferred to finished goods stock.

(b)Production cost report of Tasman Ltd. for the month of July(for tennis rackets)

(only includes cost incurred in the manufacturing process in the current year)

5

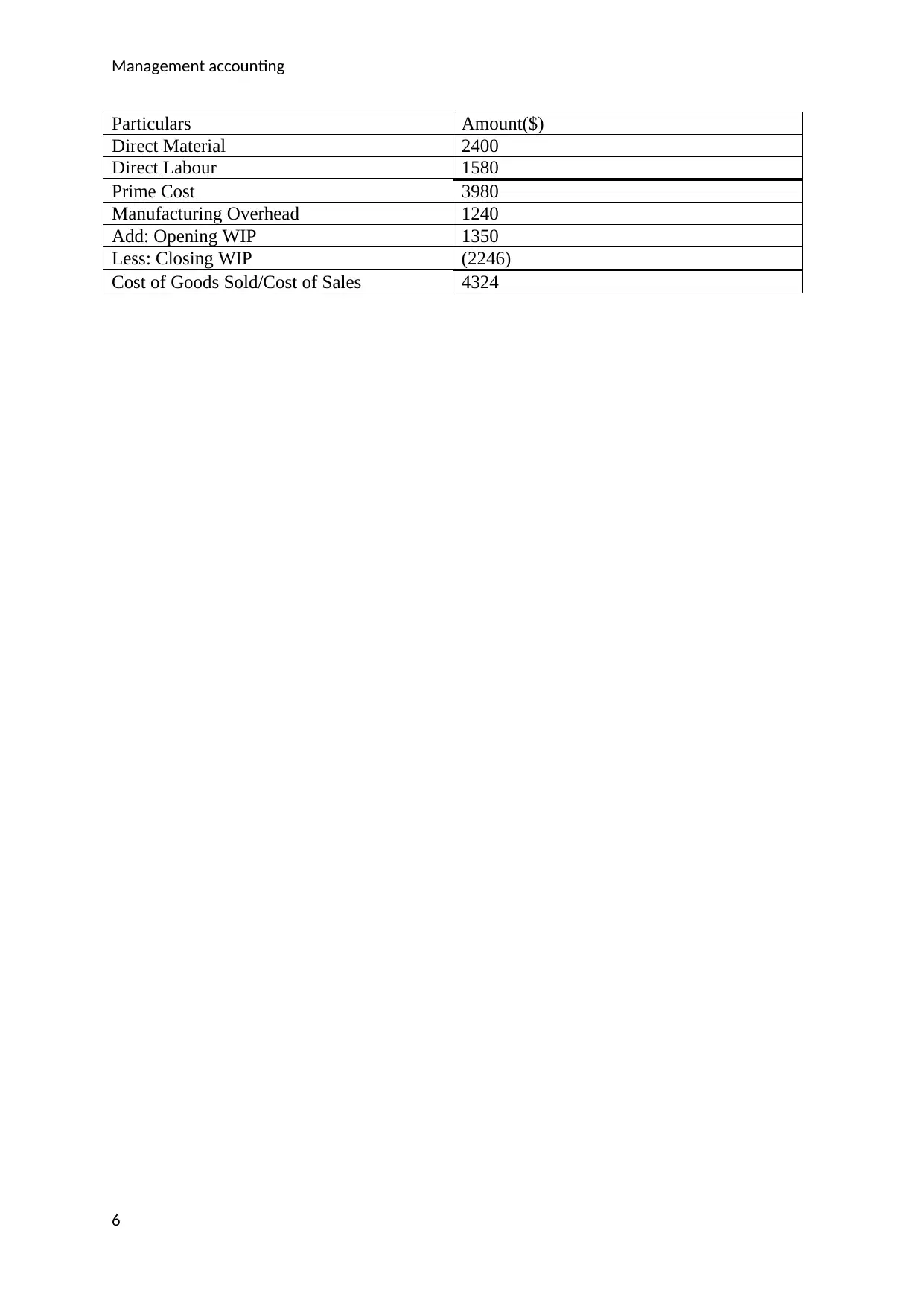

Management accounting

Particulars Amount($)

Direct Material 2400

Direct Labour 1580

Prime Cost 3980

Manufacturing Overhead 1240

Add: Opening WIP 1350

Less: Closing WIP (2246)

Cost of Goods Sold/Cost of Sales 4324

6

Particulars Amount($)

Direct Material 2400

Direct Labour 1580

Prime Cost 3980

Manufacturing Overhead 1240

Add: Opening WIP 1350

Less: Closing WIP (2246)

Cost of Goods Sold/Cost of Sales 4324

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting

Part – 3

Introduction

Processes, institutions, systems, laws, mechanisms, policies, and relations through which

corporations are controlled and directed are known as Corporate Governance. It involves

balancing the main interests of the stakeholders of an organization. It also lays a definition of

the goals for which it is governed apart from managing the relationships among the

stakeholders. Earlier, the corporations used to emphasize mostly on rules and policies in

order to disperse power between agents and principals and also to govern management

activities. In the recent development, it is noticed that the core element of corporate

governance is financial reporting (Mariana & Maria, 2016). The shareholders of a corporate

are unable to evaluate the performance of the management so as to take considerate required

investment decisions without legitimate transparency, relevance and reliable information. A

certain untimely collapse of popular and giant like companies such as Parmalat1, Enron1 or

Worldcom1 along with remarkable financial reporting restatements at Ahold1, Xerox1,

Shell1, etc have not only broken faith in financial reporting but also shaken the confidence in

the financial system totally. This bought global pension systems under enormous pressure

and also made stock markets compensate for many years.

Significance of accounting information and financial reporting in enhancing corporate

governance

In order to have a corporation work under proper corporate governance principles, it is

required for the corporation to treat financial reporting as a central priority and not as a low-

priority bookkeeping. Earlier, the objective behind making financial statements was to

provide information about the financial situation and status of a corporation which might be

of great utility to a large number of users for making economic decisions and keeping a check

on the management’s performance. The main part of the various domestic accounting

systems in context to its financial reporting is its decision oriented objective. The financial

information with regards to the timing, amounts, and uncertainty of the company’s future

cash inflows and outflows is always desired by the investors as these are the factors on which

the decision related to investments are made. It is seen that information is generally required

for 2 major reasons.

7

Part – 3

Introduction

Processes, institutions, systems, laws, mechanisms, policies, and relations through which

corporations are controlled and directed are known as Corporate Governance. It involves

balancing the main interests of the stakeholders of an organization. It also lays a definition of

the goals for which it is governed apart from managing the relationships among the

stakeholders. Earlier, the corporations used to emphasize mostly on rules and policies in

order to disperse power between agents and principals and also to govern management

activities. In the recent development, it is noticed that the core element of corporate

governance is financial reporting (Mariana & Maria, 2016). The shareholders of a corporate

are unable to evaluate the performance of the management so as to take considerate required

investment decisions without legitimate transparency, relevance and reliable information. A

certain untimely collapse of popular and giant like companies such as Parmalat1, Enron1 or

Worldcom1 along with remarkable financial reporting restatements at Ahold1, Xerox1,

Shell1, etc have not only broken faith in financial reporting but also shaken the confidence in

the financial system totally. This bought global pension systems under enormous pressure

and also made stock markets compensate for many years.

Significance of accounting information and financial reporting in enhancing corporate

governance

In order to have a corporation work under proper corporate governance principles, it is

required for the corporation to treat financial reporting as a central priority and not as a low-

priority bookkeeping. Earlier, the objective behind making financial statements was to

provide information about the financial situation and status of a corporation which might be

of great utility to a large number of users for making economic decisions and keeping a check

on the management’s performance. The main part of the various domestic accounting

systems in context to its financial reporting is its decision oriented objective. The financial

information with regards to the timing, amounts, and uncertainty of the company’s future

cash inflows and outflows is always desired by the investors as these are the factors on which

the decision related to investments are made. It is seen that information is generally required

for 2 major reasons.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting

Firstly, financial reporting is one significant and dependable source of information from an

economic view which allows effective and efficient utilization and allocation of capital.

Fabricated statements that carry misleading and fraudulent information might result from

fund investments in ineffective corporations (Viney, 2010). When users who make business

and financial decisions are of the opinion that there is insufficient, biased or misleading

information in the financial statements there are chances for the capital markets to get

crashed. Information gap between the management (insiders) and the investors (outsiders) is

also reduced as a result of financial reporting. The capital market is badly impacted by

improper financial reporting. The financial reporting data is also influenced and affected by

the market performance of an organization.

Secondly, with appropriate, true and fair information in the financial statements, the interests

of the investors are more secured and protected legally. People indulged in manipulating and

fabricating the statements have to go through legal consequences. The information must be

made available to all in such a manner that it reaches the maximum for if fewer outsiders are

informed lesser will they be able to safeguard themselves by making legitimate financial

decisions. With this, it can be concluded as the effective corporate governance system is

dependent on effective information system which is further dependent on an effective

financial reporting system. So, corporate governance can rather be accounted useless in the

absence of an effective financial reporting.

Financial information system facilitates transparency in the financial statements by providing

a high quality of accounting information. In order to reduce and eradicate information gap

and asymmetry between market participants and managers, it is essential for the

organizations to opt for high-quality financial reporting. Incentive problems are one of the

examples of information asymmetry that arises due to the actions of the manager’s that are

unknown to the principal. Contracting and monitoring costs arise due to the occurrence of

such issues and the conflicts of interests between company’s shareholders and management.

Mitigation of agency costs is emphasized with the help of accounting information that plays

an important role in designing contracts. Information relevant to regulating managerial

behavior that is significant for effective contract mechanisms sets limitations for the financial

accounting information to perform its important role. Financial reporting plays an important

role in solving conflicts and issues related to corporate governance as per the evidence. The

incompleteness of the contracts that require being fused with more information is the aspect

on which financial reporting and accounting information in corporate governance is largely

8

Firstly, financial reporting is one significant and dependable source of information from an

economic view which allows effective and efficient utilization and allocation of capital.

Fabricated statements that carry misleading and fraudulent information might result from

fund investments in ineffective corporations (Viney, 2010). When users who make business

and financial decisions are of the opinion that there is insufficient, biased or misleading

information in the financial statements there are chances for the capital markets to get

crashed. Information gap between the management (insiders) and the investors (outsiders) is

also reduced as a result of financial reporting. The capital market is badly impacted by

improper financial reporting. The financial reporting data is also influenced and affected by

the market performance of an organization.

Secondly, with appropriate, true and fair information in the financial statements, the interests

of the investors are more secured and protected legally. People indulged in manipulating and

fabricating the statements have to go through legal consequences. The information must be

made available to all in such a manner that it reaches the maximum for if fewer outsiders are

informed lesser will they be able to safeguard themselves by making legitimate financial

decisions. With this, it can be concluded as the effective corporate governance system is

dependent on effective information system which is further dependent on an effective

financial reporting system. So, corporate governance can rather be accounted useless in the

absence of an effective financial reporting.

Financial information system facilitates transparency in the financial statements by providing

a high quality of accounting information. In order to reduce and eradicate information gap

and asymmetry between market participants and managers, it is essential for the

organizations to opt for high-quality financial reporting. Incentive problems are one of the

examples of information asymmetry that arises due to the actions of the manager’s that are

unknown to the principal. Contracting and monitoring costs arise due to the occurrence of

such issues and the conflicts of interests between company’s shareholders and management.

Mitigation of agency costs is emphasized with the help of accounting information that plays

an important role in designing contracts. Information relevant to regulating managerial

behavior that is significant for effective contract mechanisms sets limitations for the financial

accounting information to perform its important role. Financial reporting plays an important

role in solving conflicts and issues related to corporate governance as per the evidence. The

incompleteness of the contracts that require being fused with more information is the aspect

on which financial reporting and accounting information in corporate governance is largely

8

Management accounting

focused on. The efficiency of governance and contracting mechanisms by having increased

transparency and higher quality of financial reporting can eliminate agency issues and

disputes between shareholder and managers of the company (Goergen & Renneboog, 2011).

The performance evaluation and management rewarding become easy with the identification

of factors that are of no utility to the management. Credibility, timeliness, and relevance of

information in the financial reports are the substantial modes of communication with parties

like independent directors. The monitoring performance of the board of directors can be

enhanced with high-quality financial reports. The demand for public information and

corporate transparency is enormous and unaffected with the board of directors having access

to internal reports because of the various rules and policies and monitoring is done by

auditors for every public disclosure and financial information (Core et. al, 1999).

It is required for the majority of members of the boards to become independent directors due

to recent regulatory pressure so as to improve governance systems in corporations. This is

because of the perception that if the directors are independent and unaffected from corporate

insiders then there might be effective monitoring of management performance. Minimal or

less access to credible, relevant and reliable information is the major threat faced by outside

independent directors and outside shareholders. The quality of information received by the

board constructs the efficiency of a board’s decision-making. The capability of a board to

evaluate the performance of managers effectively is affected by the availability of limited

information. In order to monitor the performance of the board of directors, it is required and

important to have a transparency in the information environment. In order to enhance

governance mechanisms in corporations, the effect of regulations and legal systems is

required as it will not only facilitate but also enforce accounting standards as well.

What catches the attention of regulatory bodies, academics and practitioners are the increased

transparency, effective corporate governance and higher quality of financial reporting. The

efficiency of contracts, transparency in information and governance mechanisms are

interrelated and dependent and closely knitted with each other (Conchon, 2011). Such

transparency can be enhanced and can resolve information gap and asymmetry between

managers, directors and outside shareholders by means of higher quality of financial

reporting and informative accounting earnings that can improve contracting arrangements.

The incentives of management that withhold information and engage in accounting flexibility

like in the case of earnings management can also be reduced with the efficiency of corporate

governance. Agency issues are resolved with the help of such mechanisms as they substitute

9

focused on. The efficiency of governance and contracting mechanisms by having increased

transparency and higher quality of financial reporting can eliminate agency issues and

disputes between shareholder and managers of the company (Goergen & Renneboog, 2011).

The performance evaluation and management rewarding become easy with the identification

of factors that are of no utility to the management. Credibility, timeliness, and relevance of

information in the financial reports are the substantial modes of communication with parties

like independent directors. The monitoring performance of the board of directors can be

enhanced with high-quality financial reports. The demand for public information and

corporate transparency is enormous and unaffected with the board of directors having access

to internal reports because of the various rules and policies and monitoring is done by

auditors for every public disclosure and financial information (Core et. al, 1999).

It is required for the majority of members of the boards to become independent directors due

to recent regulatory pressure so as to improve governance systems in corporations. This is

because of the perception that if the directors are independent and unaffected from corporate

insiders then there might be effective monitoring of management performance. Minimal or

less access to credible, relevant and reliable information is the major threat faced by outside

independent directors and outside shareholders. The quality of information received by the

board constructs the efficiency of a board’s decision-making. The capability of a board to

evaluate the performance of managers effectively is affected by the availability of limited

information. In order to monitor the performance of the board of directors, it is required and

important to have a transparency in the information environment. In order to enhance

governance mechanisms in corporations, the effect of regulations and legal systems is

required as it will not only facilitate but also enforce accounting standards as well.

What catches the attention of regulatory bodies, academics and practitioners are the increased

transparency, effective corporate governance and higher quality of financial reporting. The

efficiency of contracts, transparency in information and governance mechanisms are

interrelated and dependent and closely knitted with each other (Conchon, 2011). Such

transparency can be enhanced and can resolve information gap and asymmetry between

managers, directors and outside shareholders by means of higher quality of financial

reporting and informative accounting earnings that can improve contracting arrangements.

The incentives of management that withhold information and engage in accounting flexibility

like in the case of earnings management can also be reduced with the efficiency of corporate

governance. Agency issues are resolved with the help of such mechanisms as they substitute

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting

or complement one other (Cohen et. al, 2013). The incentives of managers and corporate

insiders are arranged in accordance with the interests of the shareholders so as to maximize

the value of the organization by considering important and legitimate monitoring

mechanisms. This further helps in investigating and evaluating the relationship between

financial accounting information and monitoring mechanisms (Uyar et. al, 2016). The

corporate governance can be strengthened and controlled with improvisations in financial

reporting. Better and improved the financial reporting better will be corporate governance.

Current financial reporting system provides information that recent years accounts scandals.

There has been the ample number of shortcomings in financial reporting such as the

measurement of assets and liabilities at nominal value and the ignorance of intangible assets

and non-financial aspects.

Conclusion

Corporate governance and financial reporting knead together the management and the users

of the information i.e. the outsiders as it is an information gathering system and mechanism.

A better understanding of financial reporting is required along with sufficient resources in

order to fill the expectation gap but it is sad that in maximum scenarios only opposite

happens. It serves a purpose for the users to evaluate decisions regarding making

investments in the company with the help of information derived from the financial

statements of the company.

10

or complement one other (Cohen et. al, 2013). The incentives of managers and corporate

insiders are arranged in accordance with the interests of the shareholders so as to maximize

the value of the organization by considering important and legitimate monitoring

mechanisms. This further helps in investigating and evaluating the relationship between

financial accounting information and monitoring mechanisms (Uyar et. al, 2016). The

corporate governance can be strengthened and controlled with improvisations in financial

reporting. Better and improved the financial reporting better will be corporate governance.

Current financial reporting system provides information that recent years accounts scandals.

There has been the ample number of shortcomings in financial reporting such as the

measurement of assets and liabilities at nominal value and the ignorance of intangible assets

and non-financial aspects.

Conclusion

Corporate governance and financial reporting knead together the management and the users

of the information i.e. the outsiders as it is an information gathering system and mechanism.

A better understanding of financial reporting is required along with sufficient resources in

order to fill the expectation gap but it is sad that in maximum scenarios only opposite

happens. It serves a purpose for the users to evaluate decisions regarding making

investments in the company with the help of information derived from the financial

statements of the company.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting

References

Cohen, D. A., Dey, A., and Z., L. T. (2013) Corporate governance reform and executive

incentives: Implications for investments and risk taking. Contemporary Accounting Research.

[online]. 30(4), p. 1296 – 1332. Doi: https://doi.org/10.1111/j.1911-3846.2012.01189.x

Conchon, A. (2011) Board-level employee representation rights in Europe: Facts and trends.

ETUI. European Trade Union Institute.

Core, J. E., Holthausen, R. W., and Larcker, D. F. (1999) Corporate governance, chief

executive officer compensation, and firm performance. Journal of Financial Economics.

[online]. 51, p. 371–406. Doi: https://doi.org/10.1016/S0304-405X(98)00058-0

Goergen, M. and Renneboog, L. (2011) Managerial compensation. Journal of Corporate

Finance. [online]. 17(4), p. 1068–1077. DOI: 10.1016/j.jcorpfin.2011.06.002

Mariana, M and Maria, C. (2016) Transparency of Accounting Information in Achieving

Good Corporate Governance. True View and Fair. Social Sciences and Education Research

Review. [online]. 3(1), p 41-62. Available from: http://sserr.ro/wp-content/uploads/2016/05/3-

1-41-62.pdf [Accessed 22 May 2018]

Uyar, A., Gungormus, A.H., and Kuzey, C. (2017) Impact of the Accounting Information

System on Corporate Governance: Evidence from Turkish Non-Listed Companies.

Australasian Accounting, Business and Finance Journal. [online].11(1),p. 9-27. Available

from: http://ro.uow.edu.au/cgi/viewcontent.cgi?article=1751&context=aabfj [Accessed 22

May 2018]

Viney, C. (2010) McGrath’s Financial Institutions, Instruments and Markets. Sydney

11

References

Cohen, D. A., Dey, A., and Z., L. T. (2013) Corporate governance reform and executive

incentives: Implications for investments and risk taking. Contemporary Accounting Research.

[online]. 30(4), p. 1296 – 1332. Doi: https://doi.org/10.1111/j.1911-3846.2012.01189.x

Conchon, A. (2011) Board-level employee representation rights in Europe: Facts and trends.

ETUI. European Trade Union Institute.

Core, J. E., Holthausen, R. W., and Larcker, D. F. (1999) Corporate governance, chief

executive officer compensation, and firm performance. Journal of Financial Economics.

[online]. 51, p. 371–406. Doi: https://doi.org/10.1016/S0304-405X(98)00058-0

Goergen, M. and Renneboog, L. (2011) Managerial compensation. Journal of Corporate

Finance. [online]. 17(4), p. 1068–1077. DOI: 10.1016/j.jcorpfin.2011.06.002

Mariana, M and Maria, C. (2016) Transparency of Accounting Information in Achieving

Good Corporate Governance. True View and Fair. Social Sciences and Education Research

Review. [online]. 3(1), p 41-62. Available from: http://sserr.ro/wp-content/uploads/2016/05/3-

1-41-62.pdf [Accessed 22 May 2018]

Uyar, A., Gungormus, A.H., and Kuzey, C. (2017) Impact of the Accounting Information

System on Corporate Governance: Evidence from Turkish Non-Listed Companies.

Australasian Accounting, Business and Finance Journal. [online].11(1),p. 9-27. Available

from: http://ro.uow.edu.au/cgi/viewcontent.cgi?article=1751&context=aabfj [Accessed 22

May 2018]

Viney, C. (2010) McGrath’s Financial Institutions, Instruments and Markets. Sydney

11

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.