Cost Accounting Assignment: Financial vs. Cost Accounting Analysis

VerifiedAdded on 2023/01/16

|20

|4949

|1

Homework Assignment

AI Summary

This assignment delves into the core principles of cost accounting, beginning with a detailed definition of cost accounting, its objectives, and various classifications. It explores the critical differences between financial and cost accounting, highlighting their distinct purposes and applications. The assignment also examines the concept of cost drivers and their role in overhead application rates. A significant portion is dedicated to preparing a cost sheet for AJ Corporation Ltd, utilizing provided financial data to calculate key cost components. Furthermore, the assignment includes variance analysis, breakeven point calculations, and in-depth interpretations of the financial data. The solution addresses all the questions in the assignment brief, providing a comprehensive understanding of cost accounting principles and their practical applications in a business context.

Running head: COST ACCOUNTING

Cost Accounting

Name of the student:

Name of the university:

Author Note:

Cost Accounting

Name of the student:

Name of the university:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COST ACCOUNTING

Executive Summary

The main focus of this conducted assignment is regarding the implication of cost accounting

in a firm. The objectives of cost accounting with the evaluation and the measurement of the

various cost has been ascertained in this assignment. The assignment also deals with the key

factors which are the calculations for helping the managers of the company in making some

of the vital decisions.

Executive Summary

The main focus of this conducted assignment is regarding the implication of cost accounting

in a firm. The objectives of cost accounting with the evaluation and the measurement of the

various cost has been ascertained in this assignment. The assignment also deals with the key

factors which are the calculations for helping the managers of the company in making some

of the vital decisions.

2COST ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................4

Answer to Question 1.............................................................................................................4

Answer to Question 2.............................................................................................................7

Answer to Question 3.............................................................................................................8

Answer to Question 4...........................................................................................................10

Answer to Question 5...........................................................................................................11

Answer to Question 6...........................................................................................................13

Conclusion................................................................................................................................16

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................4

Answer to Question 1.............................................................................................................4

Answer to Question 2.............................................................................................................7

Answer to Question 3.............................................................................................................8

Answer to Question 4...........................................................................................................10

Answer to Question 5...........................................................................................................11

Answer to Question 6...........................................................................................................13

Conclusion................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COST ACCOUNTING

Introduction:

The aim of the assignment deals with the cost accounting where the detailed

definition of cost has been depicted in the conducted study. Effective allocation of the

overheads in the cost management plays significant role in determination of the overall cost

incurred by the firm. In this case study the details regarding the cost driver and the

implication of it in the overhead system has been disclosed accordingly in this study.

The details regarding the main objectives of cost accounting and the implication of it

in the management system of the company has been disclosed in the process. The difference

between the financial accounting and the cost accounting have been depicted and further

significance cost accounting at the time of preparation of the financial report has been

disclosed accordingly in this requirement.

In this assignment the main focus is regarding the preparation of the cost sheet of the

firm along with the evaluation of the variance with breakeven point both in terms of the units

as well as in value. Further in-depth interpretation of the conducted analysis regarding such

evaluation from the provided facts and figures have been recognized and presented

accordingly in this conducted study.

Introduction:

The aim of the assignment deals with the cost accounting where the detailed

definition of cost has been depicted in the conducted study. Effective allocation of the

overheads in the cost management plays significant role in determination of the overall cost

incurred by the firm. In this case study the details regarding the cost driver and the

implication of it in the overhead system has been disclosed accordingly in this study.

The details regarding the main objectives of cost accounting and the implication of it

in the management system of the company has been disclosed in the process. The difference

between the financial accounting and the cost accounting have been depicted and further

significance cost accounting at the time of preparation of the financial report has been

disclosed accordingly in this requirement.

In this assignment the main focus is regarding the preparation of the cost sheet of the

firm along with the evaluation of the variance with breakeven point both in terms of the units

as well as in value. Further in-depth interpretation of the conducted analysis regarding such

evaluation from the provided facts and figures have been recognized and presented

accordingly in this conducted study.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COST ACCOUNTING

Discussion:

Answer to Question 1

Cost accounting refers to the accounting methods tends to capture the cost related to

the production of the company by evaluating the input costs of each step of the production

process, which further includes the fixed cost such as the depreciation of the capital

equipment’s. Cost accounting actually evaluates and further records the individual costs of

the firm and compare the input results with the outputs generated. Such evaluations plays

significant role regarding the measurement of the financial performance of the business

(Bouwens 2017). Cost accounting is often used in the firms for the purpose of decision

making and further firms takes certain measures to improve the facts and the figures.

The main objectives of the cost accounting are as follows:

To determine cost: The main objective of the cost accounting is that to ascertain the

cost of the organization. It is the determination of the actual cost incurred by the

organization. Basically there are two methods of ascertaining the cost of an

organization which are the job costing and the process costing. The application of

these methods varies as per the nature of the business conducted by the organization.

To control cost: The purpose of the cost accounting is to control cost by the

application of the various tools and techniques which are the budgetary control,

standard costing, inventory control and many more.

To provide information for the purpose of decision making: The decision in the cost

accounting is related to whether to make or buy the components of raw materials,

retain or replace the existing machines, whether to increase the production process

and further decision regarding whether to shut down or continue the operations

(Kouvelis, Pang and Ding 2018).

Discussion:

Answer to Question 1

Cost accounting refers to the accounting methods tends to capture the cost related to

the production of the company by evaluating the input costs of each step of the production

process, which further includes the fixed cost such as the depreciation of the capital

equipment’s. Cost accounting actually evaluates and further records the individual costs of

the firm and compare the input results with the outputs generated. Such evaluations plays

significant role regarding the measurement of the financial performance of the business

(Bouwens 2017). Cost accounting is often used in the firms for the purpose of decision

making and further firms takes certain measures to improve the facts and the figures.

The main objectives of the cost accounting are as follows:

To determine cost: The main objective of the cost accounting is that to ascertain the

cost of the organization. It is the determination of the actual cost incurred by the

organization. Basically there are two methods of ascertaining the cost of an

organization which are the job costing and the process costing. The application of

these methods varies as per the nature of the business conducted by the organization.

To control cost: The purpose of the cost accounting is to control cost by the

application of the various tools and techniques which are the budgetary control,

standard costing, inventory control and many more.

To provide information for the purpose of decision making: The decision in the cost

accounting is related to whether to make or buy the components of raw materials,

retain or replace the existing machines, whether to increase the production process

and further decision regarding whether to shut down or continue the operations

(Kouvelis, Pang and Ding 2018).

5COST ACCOUNTING

To identify the selling price: Cost accounting provides certain information related to

cost which are used to determine the selling price of the products or the services. At

the time of depression, the upper level management take decision regarding the

reduction in the selling price.

To identify the costing profit: The objective of the cost accounting is to further

ascertain the costing profit or loss of the business on the basis of matching cost with

the revenue of that activity.

Financial accounting is completely different from the cost accounting. In case of

financial accounting, the financial performance of the company includes the key components

which are the assets and the liabilities of the business (Hair et al. 2015). Cost accounting is an

important tools used in the management of the company for the purpose of budgeting and

also in setting up the cost control programs which will further improve the net profit margin

of the company.

The main or the key difference in the cost accounting and the financial accounting is

that in case of the financial accounting the cost is differentiated on the basis of the

information and the needs provided the upper level management of the company in that case.

Cost accounting is used as the internal tool in the management system of the company which

does not include any specific standard set by the generally accepted accounting principle

(GAAP).

There are various types of cost accounting used in a firm which are the standard cost

accounting, activity based costing, Lean accounting, marginal costing. In cost accounting

there are there lies different types of cost which are the fixed cost, Variable cost, Operating

Cost and Direct Costs. Standard cost accounting refers to that type of cost accounting which

is evaluated by the help of the ratios in order to compare efficient uses of labor and materials

To identify the selling price: Cost accounting provides certain information related to

cost which are used to determine the selling price of the products or the services. At

the time of depression, the upper level management take decision regarding the

reduction in the selling price.

To identify the costing profit: The objective of the cost accounting is to further

ascertain the costing profit or loss of the business on the basis of matching cost with

the revenue of that activity.

Financial accounting is completely different from the cost accounting. In case of

financial accounting, the financial performance of the company includes the key components

which are the assets and the liabilities of the business (Hair et al. 2015). Cost accounting is an

important tools used in the management of the company for the purpose of budgeting and

also in setting up the cost control programs which will further improve the net profit margin

of the company.

The main or the key difference in the cost accounting and the financial accounting is

that in case of the financial accounting the cost is differentiated on the basis of the

information and the needs provided the upper level management of the company in that case.

Cost accounting is used as the internal tool in the management system of the company which

does not include any specific standard set by the generally accepted accounting principle

(GAAP).

There are various types of cost accounting used in a firm which are the standard cost

accounting, activity based costing, Lean accounting, marginal costing. In cost accounting

there are there lies different types of cost which are the fixed cost, Variable cost, Operating

Cost and Direct Costs. Standard cost accounting refers to that type of cost accounting which

is evaluated by the help of the ratios in order to compare efficient uses of labor and materials

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6COST ACCOUNTING

to produce goods and services under some of the standard conditions (Angelopoulos and

Pollalis 2017). Evaluating these difference is called a variance analysis. Traditional cost

accounting refers to the essentially allocation of the costs based on one measure, labor or

machines hours. The reason behind that is overhead cost has risen which is proportionate to

the labor cost since the beginning of standard cost accounting, further allocating the overhead

cost as an overall cost which has end up producing occasionally confusing visions. The issues

associated with the cost accounting is that this type of accounting literally focuses on the

efficiency of the labors despite the facts which makes up the comparatively small amount of

costs for the modern companies.

The another type of costing is the activity based costing which refers to the approach

based on the costing and the monitoring of the activities which further involves outlining the

resources consumption and costing final outputs, resources allocated to the activities which is

based on consumption estimates. Activity based costing collects the overheads from each

departments and are further allocated them to the specific cost objects such as the customers,

service or the products. This type of costing further gives management better idea of the

source from where the time and money is spent (Ellul et al. 2015).

Marginal accounting is considered as the simplified model of cost accounting and it is

also referred to as the cost volume profit analysis, which is an analysis of the relationship

between the sale price of the product or services, the volume of sales, the amount produced,

expenses, cost and profits (Jurek and Stafford 2015). Such specific relationship is referred to

as the contribution margin. The method of calculating the contribution margin is by dividing

revenue minus variable cost by revenue. These are the analytical tools used by the upper level

management of the organization to gain vision into the potential profits as impacted by the

change of costs, types of sales prices establishment and marketing campaigns (Andrei,

Gâlmeanu and Radu 2018).

to produce goods and services under some of the standard conditions (Angelopoulos and

Pollalis 2017). Evaluating these difference is called a variance analysis. Traditional cost

accounting refers to the essentially allocation of the costs based on one measure, labor or

machines hours. The reason behind that is overhead cost has risen which is proportionate to

the labor cost since the beginning of standard cost accounting, further allocating the overhead

cost as an overall cost which has end up producing occasionally confusing visions. The issues

associated with the cost accounting is that this type of accounting literally focuses on the

efficiency of the labors despite the facts which makes up the comparatively small amount of

costs for the modern companies.

The another type of costing is the activity based costing which refers to the approach

based on the costing and the monitoring of the activities which further involves outlining the

resources consumption and costing final outputs, resources allocated to the activities which is

based on consumption estimates. Activity based costing collects the overheads from each

departments and are further allocated them to the specific cost objects such as the customers,

service or the products. This type of costing further gives management better idea of the

source from where the time and money is spent (Ellul et al. 2015).

Marginal accounting is considered as the simplified model of cost accounting and it is

also referred to as the cost volume profit analysis, which is an analysis of the relationship

between the sale price of the product or services, the volume of sales, the amount produced,

expenses, cost and profits (Jurek and Stafford 2015). Such specific relationship is referred to

as the contribution margin. The method of calculating the contribution margin is by dividing

revenue minus variable cost by revenue. These are the analytical tools used by the upper level

management of the organization to gain vision into the potential profits as impacted by the

change of costs, types of sales prices establishment and marketing campaigns (Andrei,

Gâlmeanu and Radu 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7COST ACCOUNTING

Fixed costs are costs that differs depending on the amount of work a company is

performing at the end of the year. Such cost are usually the elements like the payment on a

building or the piece of equipment’s which is depreciated at a fixed monthly rate. Variable

costs are the costs associate with the level of production of the company. Operating costs are

the costs which are associated with the day to day operating expenses of the business.

Depending on the situation of the business this costs can be either fixed or variable. On the

other hand direct costs are the cost which is related to the production incurred by the business

such as the purchase of the raw materials (Bierer et al. 2015). Such direct cost are related to

the finished products of the business which further includes the labor hours.

Answer to Question 2

There are various parameters regarding the cost and the financial accounting which areas

follows:

Financial accounting deals with the preparation of standard set of reports for the

purpose of the outside audience, which includes the investors, creditors, credit rating

agency and other regulatory agencies (Appelbaum et al. 2017). This type of

accounting includes the preparation of the reports required by the managements

needed to run the business of the organizations.

The reports which is prepared under the statement of financial accounting are highly

specific in the content and format as the rules and regulation are set by the generally

accepted accounting principles or international financial reporting standards. It helps

in creating reports by the upper level management of the organization under a

specified format which includes the information related to a specific decision

(Weygandt, Kimmel and Kieso 2015).

Financial accounting further focuses on the interpretation of the results and the

financial position of the entire business entity. The reports related to the cost

Fixed costs are costs that differs depending on the amount of work a company is

performing at the end of the year. Such cost are usually the elements like the payment on a

building or the piece of equipment’s which is depreciated at a fixed monthly rate. Variable

costs are the costs associate with the level of production of the company. Operating costs are

the costs which are associated with the day to day operating expenses of the business.

Depending on the situation of the business this costs can be either fixed or variable. On the

other hand direct costs are the cost which is related to the production incurred by the business

such as the purchase of the raw materials (Bierer et al. 2015). Such direct cost are related to

the finished products of the business which further includes the labor hours.

Answer to Question 2

There are various parameters regarding the cost and the financial accounting which areas

follows:

Financial accounting deals with the preparation of standard set of reports for the

purpose of the outside audience, which includes the investors, creditors, credit rating

agency and other regulatory agencies (Appelbaum et al. 2017). This type of

accounting includes the preparation of the reports required by the managements

needed to run the business of the organizations.

The reports which is prepared under the statement of financial accounting are highly

specific in the content and format as the rules and regulation are set by the generally

accepted accounting principles or international financial reporting standards. It helps

in creating reports by the upper level management of the organization under a

specified format which includes the information related to a specific decision

(Weygandt, Kimmel and Kieso 2015).

Financial accounting further focuses on the interpretation of the results and the

financial position of the entire business entity. The reports related to the cost

8COST ACCOUNTING

accounting deals with the company individual products, product lines, geographical

areas, customers and many more.

The elements considered in the cost accounting which is the cost of raw materials,

work in progress and finished goods where on the other side, financial accounting

deals with the combination of the information’s in the financial reports (Qin et al.

2016).

The format of the financial accounting is governed by the rules and regulations which

is the generally accepted accounting principles. In case of the cost accounting there is

no governing standard or rules and regulation (Van Erdeweghe, Van Bael and

D’haeseleer 2019).

Financial reports includes the combination of all the financial information’s of the

organization which is further recorded in the accounting system. But the information

of the cost accounting contains both the operational as well as the financial

information. The operating information is obtained from the variety of source which

is not under the direct control of the department of accounting of the organization

(Maskell, Baggaley and Grasso 2016).

The issues regarding the financial accounting is reported at the end of the reporting

period. Further the issues of the cost accounting can be reported at any time which is

depended on the needs and requirement of the upper level management of the

organization (Sekaran and Bougie 2016).

Financial accounting is apprehensive with the financial results of the reporting period

which is generally at the end of the year. In case of cost accounting, projection of the

cost is based on the future period.

accounting deals with the company individual products, product lines, geographical

areas, customers and many more.

The elements considered in the cost accounting which is the cost of raw materials,

work in progress and finished goods where on the other side, financial accounting

deals with the combination of the information’s in the financial reports (Qin et al.

2016).

The format of the financial accounting is governed by the rules and regulations which

is the generally accepted accounting principles. In case of the cost accounting there is

no governing standard or rules and regulation (Van Erdeweghe, Van Bael and

D’haeseleer 2019).

Financial reports includes the combination of all the financial information’s of the

organization which is further recorded in the accounting system. But the information

of the cost accounting contains both the operational as well as the financial

information. The operating information is obtained from the variety of source which

is not under the direct control of the department of accounting of the organization

(Maskell, Baggaley and Grasso 2016).

The issues regarding the financial accounting is reported at the end of the reporting

period. Further the issues of the cost accounting can be reported at any time which is

depended on the needs and requirement of the upper level management of the

organization (Sekaran and Bougie 2016).

Financial accounting is apprehensive with the financial results of the reporting period

which is generally at the end of the year. In case of cost accounting, projection of the

cost is based on the future period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9COST ACCOUNTING

Answer to Question 3

Cost driver plays significant role in the cost accounting where it generates the change

in the cost of an activity. This concept is widely used in for the purpose of assigning the

overhead costs to the number of units produced. It can also be used in the analysis of the

activity based costing of the organization for determining the causes of the overhead which

can be further used to determine the overhead cost. The examples of the cost drivers are the

direct labor hours, number of customers contact, number of machine hours worked, number

of product returns of the customers (Schaltegger and Zvezdov 2015).

The perfect example of the cost driver is that suppose if it is needed to determine the

amount of electricity consumed in a particular period of time, then the number of units

consumed regulates the total bills for electricity. In such a case, the number of electricity

consumed is the cost driver (Petronio 2017).

A cost driver is the main causes behind the costs associated with the activities. In

order to identify the cost drivers the first thing which is needed to be considered is the

gathering information and interviewing the key personnel in the organization which are the

purchasing, quality control, production and accounting. Identifying the key drivers in the

production process plays key role in the purchase requisition, setup of machines, machines

hours, direct labor hours and inspection hours. The cost drivers are the key elements of the

cost which are considered in the while performing the cost accounting process of the firm

(Javid et al. 2016).

Allocating the overhead cost of a particular product by using the level of the cost

driver activity which are the purchase of the raw materials, setting up the machines, running

machines, after that assembling the products and at last inspection of the finished products.

Answer to Question 3

Cost driver plays significant role in the cost accounting where it generates the change

in the cost of an activity. This concept is widely used in for the purpose of assigning the

overhead costs to the number of units produced. It can also be used in the analysis of the

activity based costing of the organization for determining the causes of the overhead which

can be further used to determine the overhead cost. The examples of the cost drivers are the

direct labor hours, number of customers contact, number of machine hours worked, number

of product returns of the customers (Schaltegger and Zvezdov 2015).

The perfect example of the cost driver is that suppose if it is needed to determine the

amount of electricity consumed in a particular period of time, then the number of units

consumed regulates the total bills for electricity. In such a case, the number of electricity

consumed is the cost driver (Petronio 2017).

A cost driver is the main causes behind the costs associated with the activities. In

order to identify the cost drivers the first thing which is needed to be considered is the

gathering information and interviewing the key personnel in the organization which are the

purchasing, quality control, production and accounting. Identifying the key drivers in the

production process plays key role in the purchase requisition, setup of machines, machines

hours, direct labor hours and inspection hours. The cost drivers are the key elements of the

cost which are considered in the while performing the cost accounting process of the firm

(Javid et al. 2016).

Allocating the overhead cost of a particular product by using the level of the cost

driver activity which are the purchase of the raw materials, setting up the machines, running

machines, after that assembling the products and at last inspection of the finished products.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10COST ACCOUNTING

The above discussed items are included in the cost associated with the cost drives which are

further considered in the production process (Sakao and Lindahl 2015).

Answer to Question 4

Cost sheet plays significant role in identifying the cost in the production process

which signifies the periodical statement which reflects the detail overview of the cost

incurred by the business on various components during the process of production. The basic

objectives for the preparation of cost sheet is used to determine the cost objective, products,

services or units of cost (Jermias 2017). The classification of the cost sheet is based on the

prime cost, works cost, cost of production and cost of sales. If sales is mentioned during the

computation of profit, then in order to find out the profit it is needed to deduct sales from the

cost of sales in order to find out the profit.

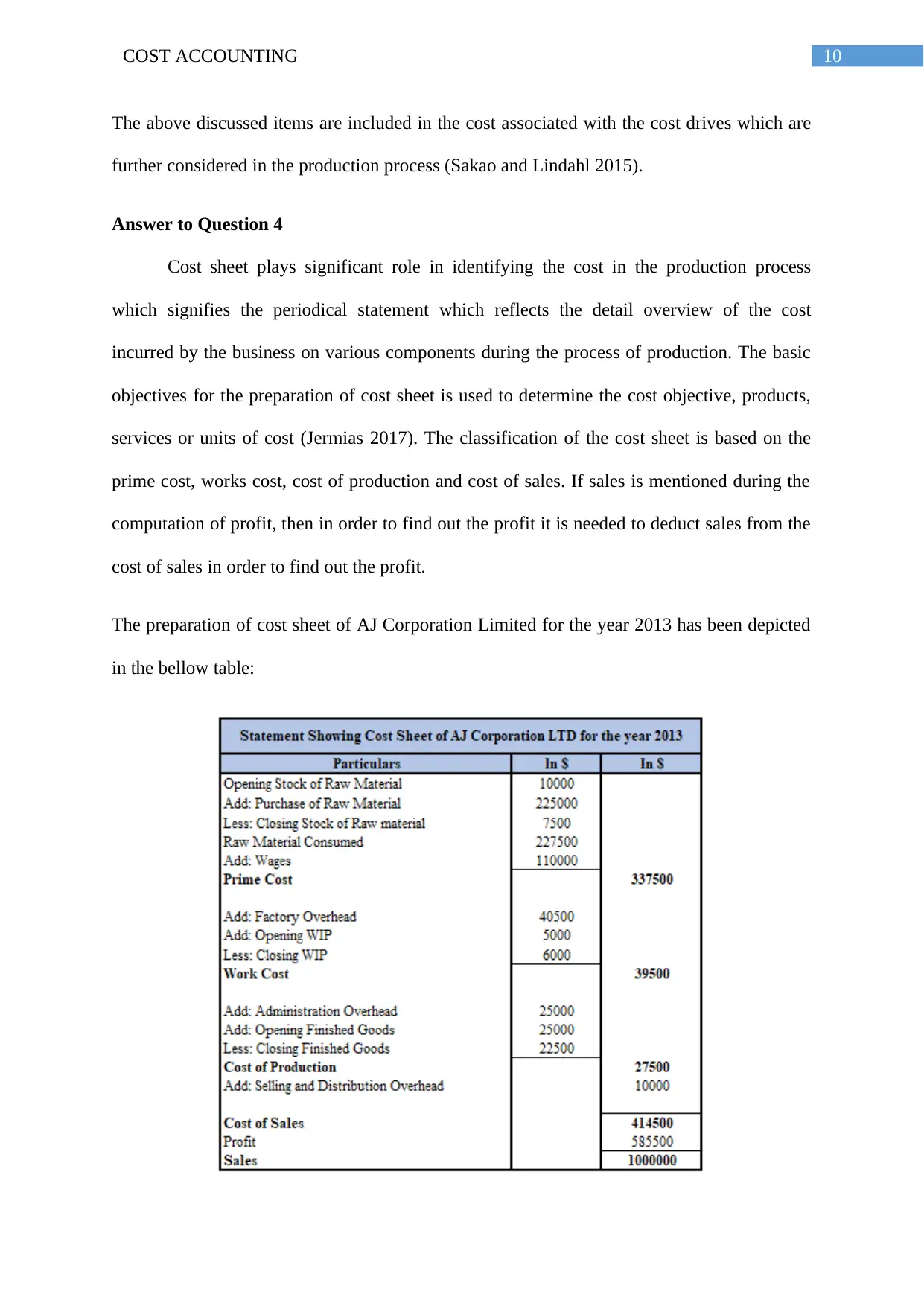

The preparation of cost sheet of AJ Corporation Limited for the year 2013 has been depicted

in the bellow table:

The above discussed items are included in the cost associated with the cost drives which are

further considered in the production process (Sakao and Lindahl 2015).

Answer to Question 4

Cost sheet plays significant role in identifying the cost in the production process

which signifies the periodical statement which reflects the detail overview of the cost

incurred by the business on various components during the process of production. The basic

objectives for the preparation of cost sheet is used to determine the cost objective, products,

services or units of cost (Jermias 2017). The classification of the cost sheet is based on the

prime cost, works cost, cost of production and cost of sales. If sales is mentioned during the

computation of profit, then in order to find out the profit it is needed to deduct sales from the

cost of sales in order to find out the profit.

The preparation of cost sheet of AJ Corporation Limited for the year 2013 has been depicted

in the bellow table:

11COST ACCOUNTING

From the above computation of the cost sheet it can be interpreted that the amount of

profit is calculated by deducting the cost of sales which is 414500 from the total amount of

sales which is 1000000. The resultant outcome is the amount of profit which is the 585500

after the consideration of all the costs associated with the prime cost, work cost, cost of

production, and cost of sales. The summation of all the above discussed cost are included in

the production process of the firm in that case (Garvey, Book and Covert 2016). The detailed

method of calculation has been discussed in the study which is adjusting the consumption of

raw material and further adding the wages along with it result in the prime cost of the firm.

From the prime cost if the factory overhead is adjusted with the opening work in progress

with the closing work in progress it will further result in the total work cost of the firm.

After the calculation of the work cost of the firm then it is needed to adjust the

administration overhead with the opening finished goods with the closing finished goods,

cost of production of the firm is evaluated and after that adding the selling and distribution

overhead of the firm it will result in the outcome of the cost of sales of the firm (Rieckhof,

Bergmann and Guenther 2015).

After evaluation of the cost of sales of the firm and then adjusting the given figures of

sales from the cost of sales of the firm it will be easier to find out the profit portion of the

firm in that case.

Answer to Question 5

In this particular evaluation on behalf of the firm which is the protest industries and

the report is delivered to the managers of the firms in that case. The given element in the

questions are the selling price, variable cost and fixed cost and from the elements which are

further computed is the contribution margin per unit, contribution margin ratio, Break Even

From the above computation of the cost sheet it can be interpreted that the amount of

profit is calculated by deducting the cost of sales which is 414500 from the total amount of

sales which is 1000000. The resultant outcome is the amount of profit which is the 585500

after the consideration of all the costs associated with the prime cost, work cost, cost of

production, and cost of sales. The summation of all the above discussed cost are included in

the production process of the firm in that case (Garvey, Book and Covert 2016). The detailed

method of calculation has been discussed in the study which is adjusting the consumption of

raw material and further adding the wages along with it result in the prime cost of the firm.

From the prime cost if the factory overhead is adjusted with the opening work in progress

with the closing work in progress it will further result in the total work cost of the firm.

After the calculation of the work cost of the firm then it is needed to adjust the

administration overhead with the opening finished goods with the closing finished goods,

cost of production of the firm is evaluated and after that adding the selling and distribution

overhead of the firm it will result in the outcome of the cost of sales of the firm (Rieckhof,

Bergmann and Guenther 2015).

After evaluation of the cost of sales of the firm and then adjusting the given figures of

sales from the cost of sales of the firm it will be easier to find out the profit portion of the

firm in that case.

Answer to Question 5

In this particular evaluation on behalf of the firm which is the protest industries and

the report is delivered to the managers of the firms in that case. The given element in the

questions are the selling price, variable cost and fixed cost and from the elements which are

further computed is the contribution margin per unit, contribution margin ratio, Break Even

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.