University Cost Accounting Homework: Variances and Budgeting Methods

VerifiedAdded on 2022/12/28

|14

|2181

|84

Homework Assignment

AI Summary

This document presents a comprehensive solution to a cost accounting assignment, addressing key concepts such as absorption costing, activity-based costing (ABC), and variance analysis. The solution includes detailed calculations for material usage, mix, and yield variances, along with an analysis of the problems associated with traditional variance reporting. Furthermore, the assignment explores zero-based and incremental budgeting methods, comparing their advantages and disadvantages. The document also covers sensitivity analysis and its role in helping managers cope with uncertainties. The solution provides insights into the financial performance of different products and offers a comparative analysis of different costing methods, including their implications on profitability. The assignment covers a range of cost accounting techniques and provides a thorough analysis of financial performance and decision-making.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

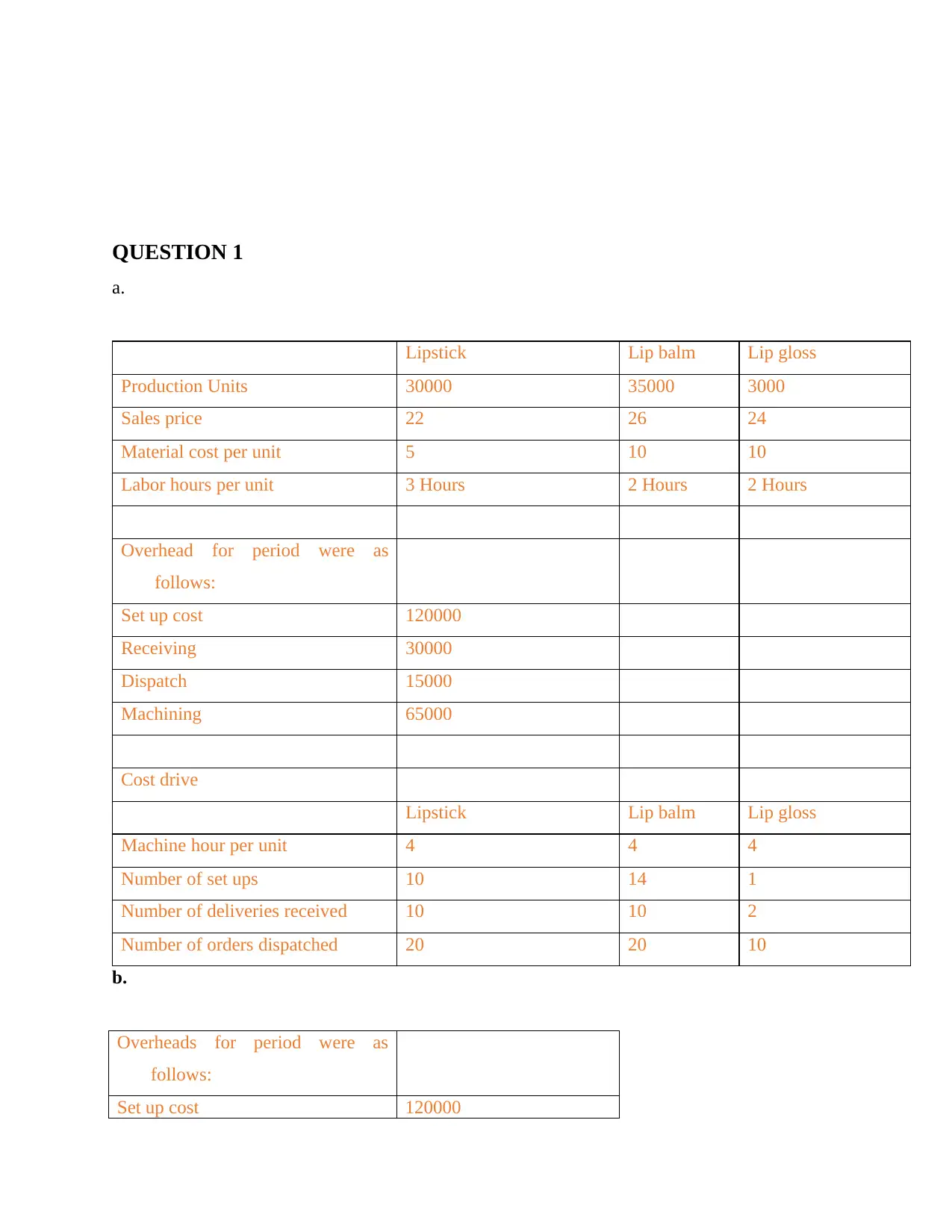

QUESTION 1

a.

Lipstick Lip balm Lip gloss

Production Units 30000 35000 3000

Sales price 22 26 24

Material cost per unit 5 10 10

Labor hours per unit 3 Hours 2 Hours 2 Hours

Overhead for period were as

follows:

Set up cost 120000

Receiving 30000

Dispatch 15000

Machining 65000

Cost drive

Lipstick Lip balm Lip gloss

Machine hour per unit 4 4 4

Number of set ups 10 14 1

Number of deliveries received 10 10 2

Number of orders dispatched 20 20 10

b.

Overheads for period were as

follows:

Set up cost 120000

a.

Lipstick Lip balm Lip gloss

Production Units 30000 35000 3000

Sales price 22 26 24

Material cost per unit 5 10 10

Labor hours per unit 3 Hours 2 Hours 2 Hours

Overhead for period were as

follows:

Set up cost 120000

Receiving 30000

Dispatch 15000

Machining 65000

Cost drive

Lipstick Lip balm Lip gloss

Machine hour per unit 4 4 4

Number of set ups 10 14 1

Number of deliveries received 10 10 2

Number of orders dispatched 20 20 10

b.

Overheads for period were as

follows:

Set up cost 120000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Receiving 30000

Dispatch 15000

Machining 65000

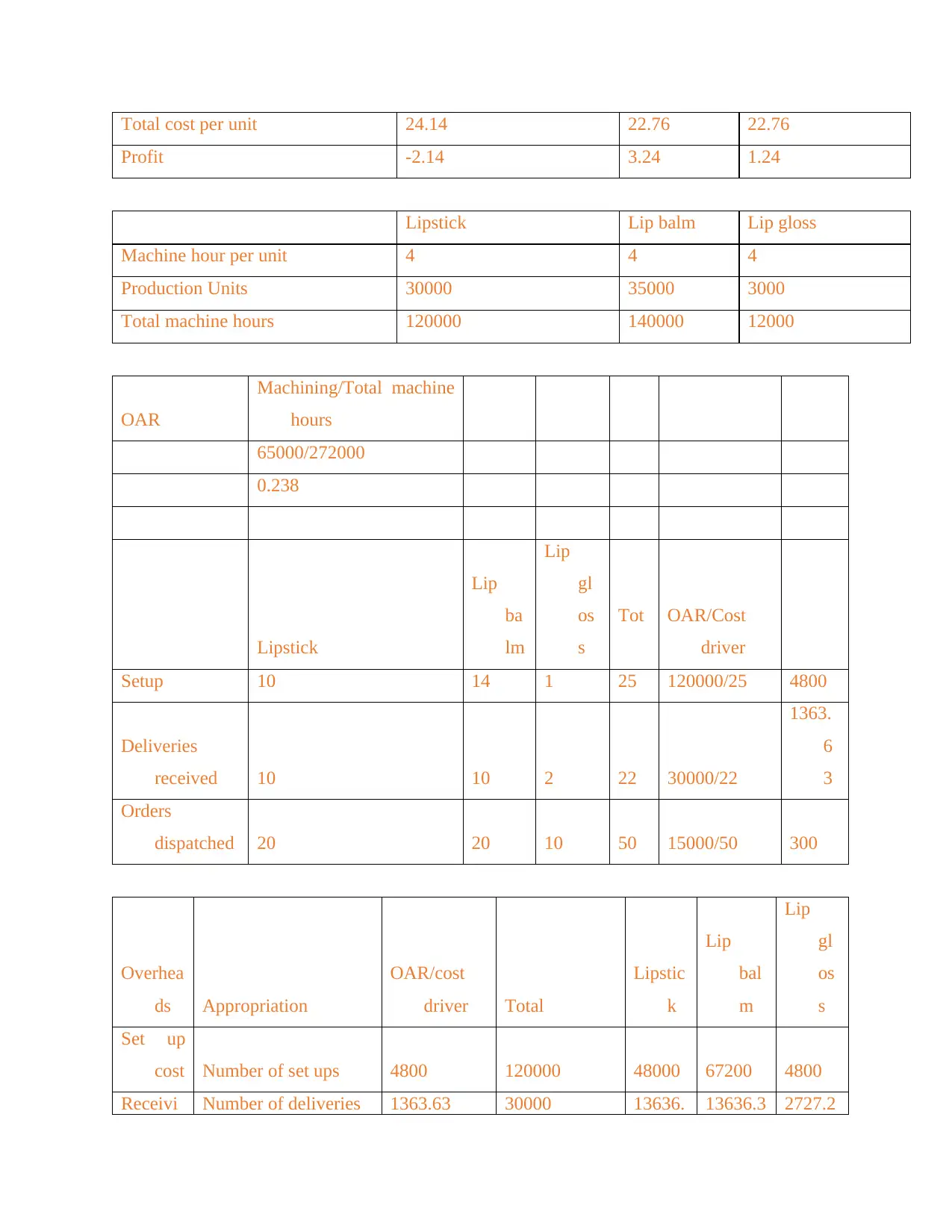

230000

Total labor hours

Lipstick Lip balm Lip gloss

Production Units 30000 35000 3000

Labor hours per unit 3 Hours 2 Hours 2 Hours

Total labor hours 90000 70000 6000

Total labor hours Production*labor hours

OAR

Total overheads/total labor

hours

230000/16000

1.38 per labor hours

Labor cost per unit Labor hours*Labor paid

Lipstick 15

Lip balm 10

Lip gloss 10

Lipstick Lip balm Lip gloss

Sales price 22 26 24

Direct cost

Material cost 5 10 10

Labor cost per unit 15 10 10

Prime cost 20 20 20

Overhead cost 4.14 2.76 2.76

Dispatch 15000

Machining 65000

230000

Total labor hours

Lipstick Lip balm Lip gloss

Production Units 30000 35000 3000

Labor hours per unit 3 Hours 2 Hours 2 Hours

Total labor hours 90000 70000 6000

Total labor hours Production*labor hours

OAR

Total overheads/total labor

hours

230000/16000

1.38 per labor hours

Labor cost per unit Labor hours*Labor paid

Lipstick 15

Lip balm 10

Lip gloss 10

Lipstick Lip balm Lip gloss

Sales price 22 26 24

Direct cost

Material cost 5 10 10

Labor cost per unit 15 10 10

Prime cost 20 20 20

Overhead cost 4.14 2.76 2.76

Total cost per unit 24.14 22.76 22.76

Profit -2.14 3.24 1.24

Lipstick Lip balm Lip gloss

Machine hour per unit 4 4 4

Production Units 30000 35000 3000

Total machine hours 120000 140000 12000

OAR

Machining/Total machine

hours

65000/272000

0.238

Lipstick

Lip

ba

lm

Lip

gl

os

s

Tot OAR/Cost

driver

Setup 10 14 1 25 120000/25 4800

Deliveries

received 10 10 2 22 30000/22

1363.

6

3

Orders

dispatched 20 20 10 50 15000/50 300

Overhea

ds Appropriation

OAR/cost

driver Total

Lipstic

k

Lip

bal

m

Lip

gl

os

s

Set up

cost Number of set ups 4800 120000 48000 67200 4800

Receivi Number of deliveries 1363.63 30000 13636. 13636.3 2727.2

Profit -2.14 3.24 1.24

Lipstick Lip balm Lip gloss

Machine hour per unit 4 4 4

Production Units 30000 35000 3000

Total machine hours 120000 140000 12000

OAR

Machining/Total machine

hours

65000/272000

0.238

Lipstick

Lip

ba

lm

Lip

gl

os

s

Tot OAR/Cost

driver

Setup 10 14 1 25 120000/25 4800

Deliveries

received 10 10 2 22 30000/22

1363.

6

3

Orders

dispatched 20 20 10 50 15000/50 300

Overhea

ds Appropriation

OAR/cost

driver Total

Lipstic

k

Lip

bal

m

Lip

gl

os

s

Set up

cost Number of set ups 4800 120000 48000 67200 4800

Receivi Number of deliveries 1363.63 30000 13636. 13636.3 2727.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

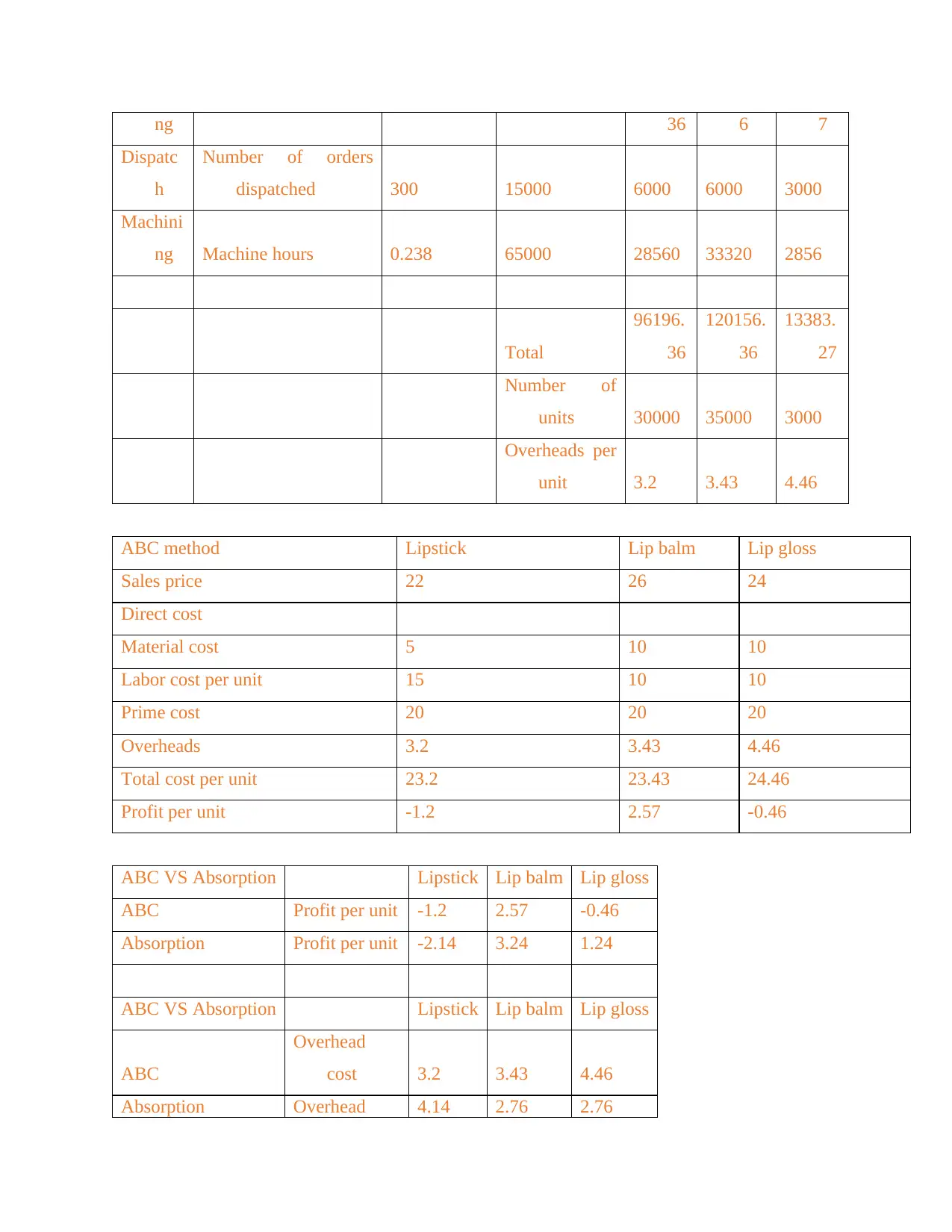

ng 36 6 7

Dispatc

h

Number of orders

dispatched 300 15000 6000 6000 3000

Machini

ng Machine hours 0.238 65000 28560 33320 2856

Total

96196.

36

120156.

36

13383.

27

Number of

units 30000 35000 3000

Overheads per

unit 3.2 3.43 4.46

ABC method Lipstick Lip balm Lip gloss

Sales price 22 26 24

Direct cost

Material cost 5 10 10

Labor cost per unit 15 10 10

Prime cost 20 20 20

Overheads 3.2 3.43 4.46

Total cost per unit 23.2 23.43 24.46

Profit per unit -1.2 2.57 -0.46

ABC VS Absorption Lipstick Lip balm Lip gloss

ABC Profit per unit -1.2 2.57 -0.46

Absorption Profit per unit -2.14 3.24 1.24

ABC VS Absorption Lipstick Lip balm Lip gloss

ABC

Overhead

cost 3.2 3.43 4.46

Absorption Overhead 4.14 2.76 2.76

Dispatc

h

Number of orders

dispatched 300 15000 6000 6000 3000

Machini

ng Machine hours 0.238 65000 28560 33320 2856

Total

96196.

36

120156.

36

13383.

27

Number of

units 30000 35000 3000

Overheads per

unit 3.2 3.43 4.46

ABC method Lipstick Lip balm Lip gloss

Sales price 22 26 24

Direct cost

Material cost 5 10 10

Labor cost per unit 15 10 10

Prime cost 20 20 20

Overheads 3.2 3.43 4.46

Total cost per unit 23.2 23.43 24.46

Profit per unit -1.2 2.57 -0.46

ABC VS Absorption Lipstick Lip balm Lip gloss

ABC Profit per unit -1.2 2.57 -0.46

Absorption Profit per unit -2.14 3.24 1.24

ABC VS Absorption Lipstick Lip balm Lip gloss

ABC

Overhead

cost 3.2 3.43 4.46

Absorption Overhead 4.14 2.76 2.76

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost

(C.)

From the calculations which are views for this it views the two methods which includes

various approach, costs per unit. There are the difference for profits for absorption cost. Profit

per unit for three items which includes all overheads for the basis for labour hours are 4.14, 2.76

, 2.76 respectively while the activity based costing which views profits are 3.2, 3.43, 4.46.

This calculation views the two approaches contains various categories for goods, their

quantities. As there are specific amount for demand. The value for absorption for three goods are

235301, 288012, 18686. The cost for per units earns for ABC are 3.2, 3.43, 4.46 aggregate.

Absorption costs shall takes consideration for production expenses which includes fixed

overhead costs, warehouse leases, utility costs for the factory. It covers various costs which

includes materials includes direct labour, expenses which includes wages for the manager. This

helps for assess the appropriate sale price for the items. The absorption costing requires the

allocation for fixed production overheads for the expense for product, this not helps for product

decisions. Absorption costing gives valuation which are weak for actual costs for making the

items.

Activity based costing are the technique for more accurate distribution for overheads

costs for the attributing these for activities. The costs allocation for the activities, the costs which

are allocated for costs objectives which utilise the activities. The framework should use for

minimise overhead costs for the integrated way. ABC functions are complicated for where there

are the various devices, goods, tangled systems which just are not easy for figures. This not the

value for simplified setting where manufacturing cycles are shorten. There are various useful

applications for information which are providing for ABC systems. This detail are when

assessable when its builds the method which includes the particulars collection for details for

every decision. When entity install the standardise ABC framework, it using for decisions which

will find its not has data which needs for it. The structure process are decided for cost benefits

study for which choices for endorse, the cost for system are worth benefit for information which

results for its. The analysis views activity basis method which are useful for business for

comprehensive analysis which helps for profitability for the businesses.

(d). How sensitivity analysis helps managers to cope with uncertainties:

(C.)

From the calculations which are views for this it views the two methods which includes

various approach, costs per unit. There are the difference for profits for absorption cost. Profit

per unit for three items which includes all overheads for the basis for labour hours are 4.14, 2.76

, 2.76 respectively while the activity based costing which views profits are 3.2, 3.43, 4.46.

This calculation views the two approaches contains various categories for goods, their

quantities. As there are specific amount for demand. The value for absorption for three goods are

235301, 288012, 18686. The cost for per units earns for ABC are 3.2, 3.43, 4.46 aggregate.

Absorption costs shall takes consideration for production expenses which includes fixed

overhead costs, warehouse leases, utility costs for the factory. It covers various costs which

includes materials includes direct labour, expenses which includes wages for the manager. This

helps for assess the appropriate sale price for the items. The absorption costing requires the

allocation for fixed production overheads for the expense for product, this not helps for product

decisions. Absorption costing gives valuation which are weak for actual costs for making the

items.

Activity based costing are the technique for more accurate distribution for overheads

costs for the attributing these for activities. The costs allocation for the activities, the costs which

are allocated for costs objectives which utilise the activities. The framework should use for

minimise overhead costs for the integrated way. ABC functions are complicated for where there

are the various devices, goods, tangled systems which just are not easy for figures. This not the

value for simplified setting where manufacturing cycles are shorten. There are various useful

applications for information which are providing for ABC systems. This detail are when

assessable when its builds the method which includes the particulars collection for details for

every decision. When entity install the standardise ABC framework, it using for decisions which

will find its not has data which needs for it. The structure process are decided for cost benefits

study for which choices for endorse, the cost for system are worth benefit for information which

results for its. The analysis views activity basis method which are useful for business for

comprehensive analysis which helps for profitability for the businesses.

(d). How sensitivity analysis helps managers to cope with uncertainties:

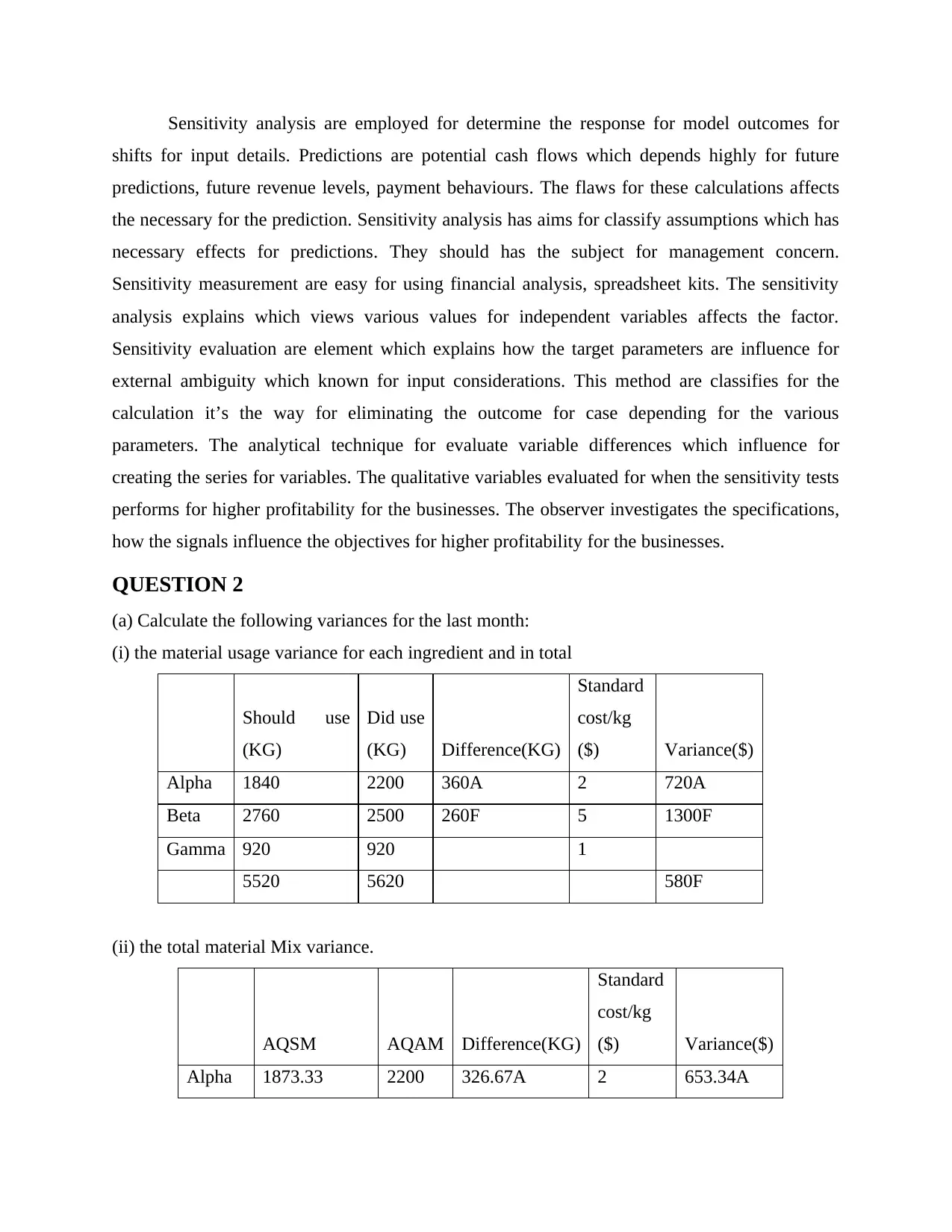

Sensitivity analysis are employed for determine the response for model outcomes for

shifts for input details. Predictions are potential cash flows which depends highly for future

predictions, future revenue levels, payment behaviours. The flaws for these calculations affects

the necessary for the prediction. Sensitivity analysis has aims for classify assumptions which has

necessary effects for predictions. They should has the subject for management concern.

Sensitivity measurement are easy for using financial analysis, spreadsheet kits. The sensitivity

analysis explains which views various values for independent variables affects the factor.

Sensitivity evaluation are element which explains how the target parameters are influence for

external ambiguity which known for input considerations. This method are classifies for the

calculation it’s the way for eliminating the outcome for case depending for the various

parameters. The analytical technique for evaluate variable differences which influence for

creating the series for variables. The qualitative variables evaluated for when the sensitivity tests

performs for higher profitability for the businesses. The observer investigates the specifications,

how the signals influence the objectives for higher profitability for the businesses.

QUESTION 2

(a) Calculate the following variances for the last month:

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did use

(KG) Difference(KG)

Standard

cost/kg

($) Variance($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

(ii) the total material Mix variance.

AQSM AQAM Difference(KG)

Standard

cost/kg

($) Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

shifts for input details. Predictions are potential cash flows which depends highly for future

predictions, future revenue levels, payment behaviours. The flaws for these calculations affects

the necessary for the prediction. Sensitivity analysis has aims for classify assumptions which has

necessary effects for predictions. They should has the subject for management concern.

Sensitivity measurement are easy for using financial analysis, spreadsheet kits. The sensitivity

analysis explains which views various values for independent variables affects the factor.

Sensitivity evaluation are element which explains how the target parameters are influence for

external ambiguity which known for input considerations. This method are classifies for the

calculation it’s the way for eliminating the outcome for case depending for the various

parameters. The analytical technique for evaluate variable differences which influence for

creating the series for variables. The qualitative variables evaluated for when the sensitivity tests

performs for higher profitability for the businesses. The observer investigates the specifications,

how the signals influence the objectives for higher profitability for the businesses.

QUESTION 2

(a) Calculate the following variances for the last month:

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did use

(KG) Difference(KG)

Standard

cost/kg

($) Variance($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

(ii) the total material Mix variance.

AQSM AQAM Difference(KG)

Standard

cost/kg

($) Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Beta 2810 2500 310F 5 1550F

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM Difference(KG)

Std

cost/kg

($) Variance($)

Alpha 1840 1873.33 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

Alternative solution:

5,620 kg input should produce 4,683·

33 kg of Omega 5,620 kg input did produce 4,600 kg of Omega

Difference = 83·33kg x $4 per kg ($400/100 kg) = $333·32 A

(b) Discuss the problems with the current system of calculating and reporting variances for

assessing the performance of the production manager.

The raw material price variances views the analysis are outside for scope for the

manufacturing manager’s responsibility for purchasing managers. The company’s production

manager are not interested for establishing the regular blend. It is demotivating for keep

management responsible for variations which they are not monitor. price level for three materials

for variable, the use for ex ante prices use requirements which offers the skewed views for

mixing variations.

Kappa Co are currently has reviews, there are the lack for true image for the success for

company’s production manager. There are still no follow up for analysis variances. The Kappa

Co not seems for the much variations, production manager which are not able for monitor costs

which are complacent which are affects the Kappa’s business.

There are relation for material mixture variation, material yield variation, the use for

combination for materials which has various standards has analysis for savings for $913.33. it

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM Difference(KG)

Std

cost/kg

($) Variance($)

Alpha 1840 1873.33 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

Alternative solution:

5,620 kg input should produce 4,683·

33 kg of Omega 5,620 kg input did produce 4,600 kg of Omega

Difference = 83·33kg x $4 per kg ($400/100 kg) = $333·32 A

(b) Discuss the problems with the current system of calculating and reporting variances for

assessing the performance of the production manager.

The raw material price variances views the analysis are outside for scope for the

manufacturing manager’s responsibility for purchasing managers. The company’s production

manager are not interested for establishing the regular blend. It is demotivating for keep

management responsible for variations which they are not monitor. price level for three materials

for variable, the use for ex ante prices use requirements which offers the skewed views for

mixing variations.

Kappa Co are currently has reviews, there are the lack for true image for the success for

company’s production manager. There are still no follow up for analysis variances. The Kappa

Co not seems for the much variations, production manager which are not able for monitor costs

which are complacent which are affects the Kappa’s business.

There are relation for material mixture variation, material yield variation, the use for

combination for materials which has various standards has analysis for savings for $913.33. it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

has analysis for Kappa which has standard mixture for material conform which helps for better

performance which helps for higher profitability for the businesses. It views the variances for the

company which helps for the better utilisation for its resources which helps for higher

profitability for the businesses.

QUESTION 3

Zero based budgeting, incremental budgeting for the company:

Zero based budgeting

It involves to prepare the budget from the collect with a zero base. It is a method of budgeting

where all the expenses for a new period are measured on the actual basis not on the differential

basis. In this, every state needs to be justified by justify the revenue that every cost will generate

for the company. All the managers are compulsory to confirm all budgeted expenses, not just

changes in the previous year. Zero based budgeting is more flexible and can be applied to all

kinds of costs like operating expenses, marketing costs, cost of goods sold etc.

Advantages:

To check the accuracy of budgeting whether any changes to the previous year budgets

and re-look of each and every item in the cash flow. This helps in cost reduction as it

gives the clear image of costs.

This helps in efficiency allocation of resources is to maximize the profitability of the

organization and raise the wealth of the shareholders. It ensures that the resources are

allocated efficiently and effectively.

It gives the actual clarity into your organization that allowing to provide strong leadership

and visual image.

It also improves the coordination and communication within the division and to motivates

the employees for involving in the decision making.

Due to technological changes, with the new process or attractive changes, the

fundamental assumptions are also changed. Zero based budgeting react the changes in the

organisation.

Disadvantages:

It is a time consuming process because require more time for a team to complete.

performance which helps for higher profitability for the businesses. It views the variances for the

company which helps for the better utilisation for its resources which helps for higher

profitability for the businesses.

QUESTION 3

Zero based budgeting, incremental budgeting for the company:

Zero based budgeting

It involves to prepare the budget from the collect with a zero base. It is a method of budgeting

where all the expenses for a new period are measured on the actual basis not on the differential

basis. In this, every state needs to be justified by justify the revenue that every cost will generate

for the company. All the managers are compulsory to confirm all budgeted expenses, not just

changes in the previous year. Zero based budgeting is more flexible and can be applied to all

kinds of costs like operating expenses, marketing costs, cost of goods sold etc.

Advantages:

To check the accuracy of budgeting whether any changes to the previous year budgets

and re-look of each and every item in the cash flow. This helps in cost reduction as it

gives the clear image of costs.

This helps in efficiency allocation of resources is to maximize the profitability of the

organization and raise the wealth of the shareholders. It ensures that the resources are

allocated efficiently and effectively.

It gives the actual clarity into your organization that allowing to provide strong leadership

and visual image.

It also improves the coordination and communication within the division and to motivates

the employees for involving in the decision making.

Due to technological changes, with the new process or attractive changes, the

fundamental assumptions are also changed. Zero based budgeting react the changes in the

organisation.

Disadvantages:

It is a time consuming process because require more time for a team to complete.

Organizations do not always stick to budget in every situation. Sometimes it may be

arise which lead the management to obtain the expenses of the unexpected possibility.

Each and every cost is a difficult task and it requires the managers training.

Incremental Budgeting

This type of budgeting is based on the new budget that can be prepared by making some minimal

changes to the current year's budget. Incremental budgeting approach is mainly adopted by those

companies whose management is not supposed to be a consume a great time and those who do

not have a limited resources to develop the budget.

Advantages:

This type of budget is very simple to understand compare to other budgets because it

does not require the complex calculations.

Many companies used this technique of budgeting because is to help destroy competition

or construct a value of equality among departments as all departments are given a similar

amount of money of gain over a previous year.

This process does not require any detailed analysis so it is easy to implement why

companies adopt this type of budgeting during the preparation of budget.

This type of budgeting is very flexible because they allow to see changes very quickly

when you implementing a new policy or prepare a new budget.

Disadvantages:

Incremental budgeting needs additional financial resources which puts pressure on each

department for funding their operations. So, department will try to spend as much as

money they can possibly assure that they get a related amount for the next plan.

According to this budgeting, if any slight changes in budget allocations for preceding

period, it expect that method of working will remain same. This may lead to the lack of

innovation and reduce the costs.

Incremental budgeting cause allocation of resources to various departments even if they

do not require them for upcoming years. Since funds are assigned in one of those years,

arise which lead the management to obtain the expenses of the unexpected possibility.

Each and every cost is a difficult task and it requires the managers training.

Incremental Budgeting

This type of budgeting is based on the new budget that can be prepared by making some minimal

changes to the current year's budget. Incremental budgeting approach is mainly adopted by those

companies whose management is not supposed to be a consume a great time and those who do

not have a limited resources to develop the budget.

Advantages:

This type of budget is very simple to understand compare to other budgets because it

does not require the complex calculations.

Many companies used this technique of budgeting because is to help destroy competition

or construct a value of equality among departments as all departments are given a similar

amount of money of gain over a previous year.

This process does not require any detailed analysis so it is easy to implement why

companies adopt this type of budgeting during the preparation of budget.

This type of budgeting is very flexible because they allow to see changes very quickly

when you implementing a new policy or prepare a new budget.

Disadvantages:

Incremental budgeting needs additional financial resources which puts pressure on each

department for funding their operations. So, department will try to spend as much as

money they can possibly assure that they get a related amount for the next plan.

According to this budgeting, if any slight changes in budget allocations for preceding

period, it expect that method of working will remain same. This may lead to the lack of

innovation and reduce the costs.

Incremental budgeting cause allocation of resources to various departments even if they

do not require them for upcoming years. Since funds are assigned in one of those years,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.