Cost Accounting Assignment: LIFO, FIFO, and Overhead

VerifiedAdded on 2019/09/20

|6

|687

|196

Homework Assignment

AI Summary

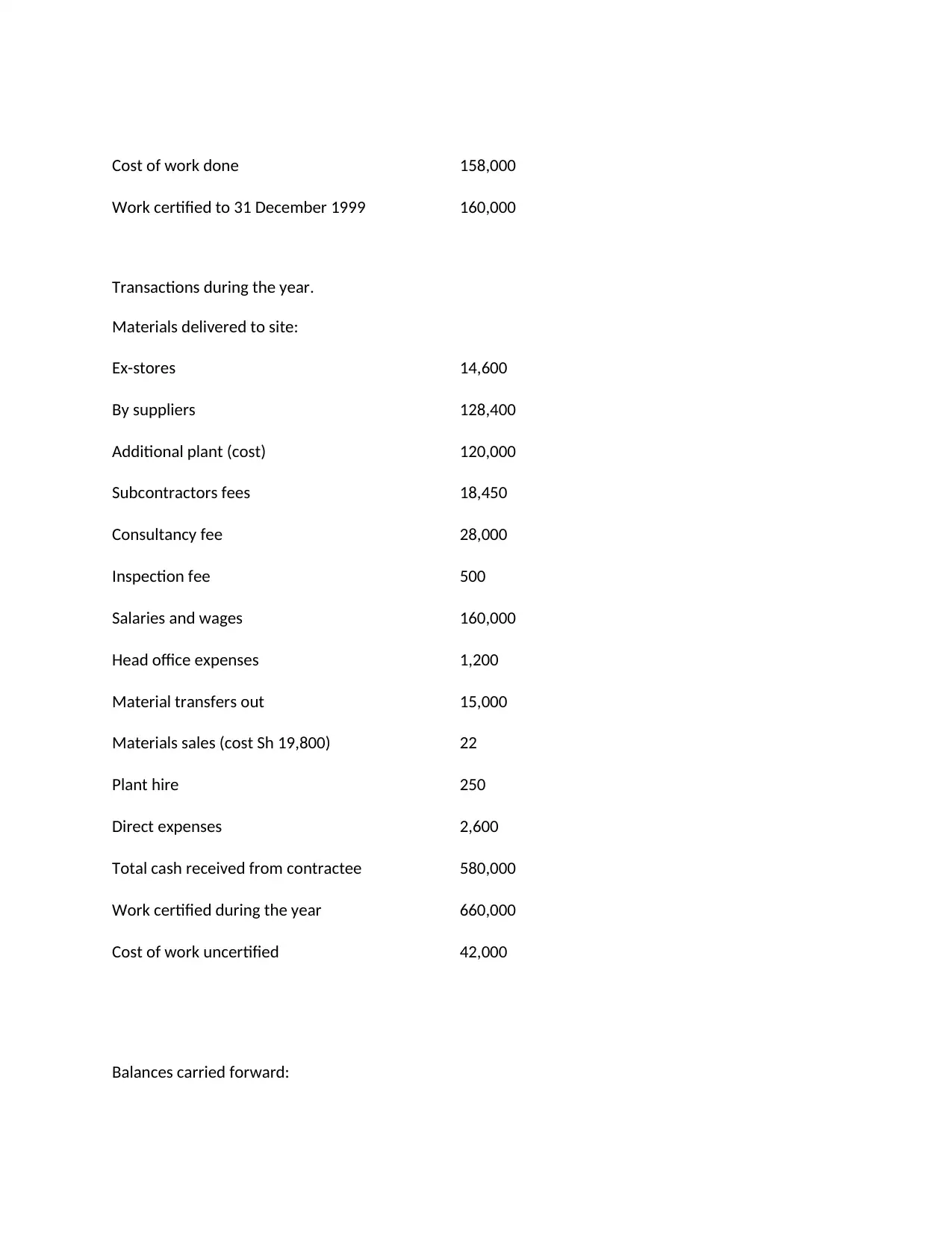

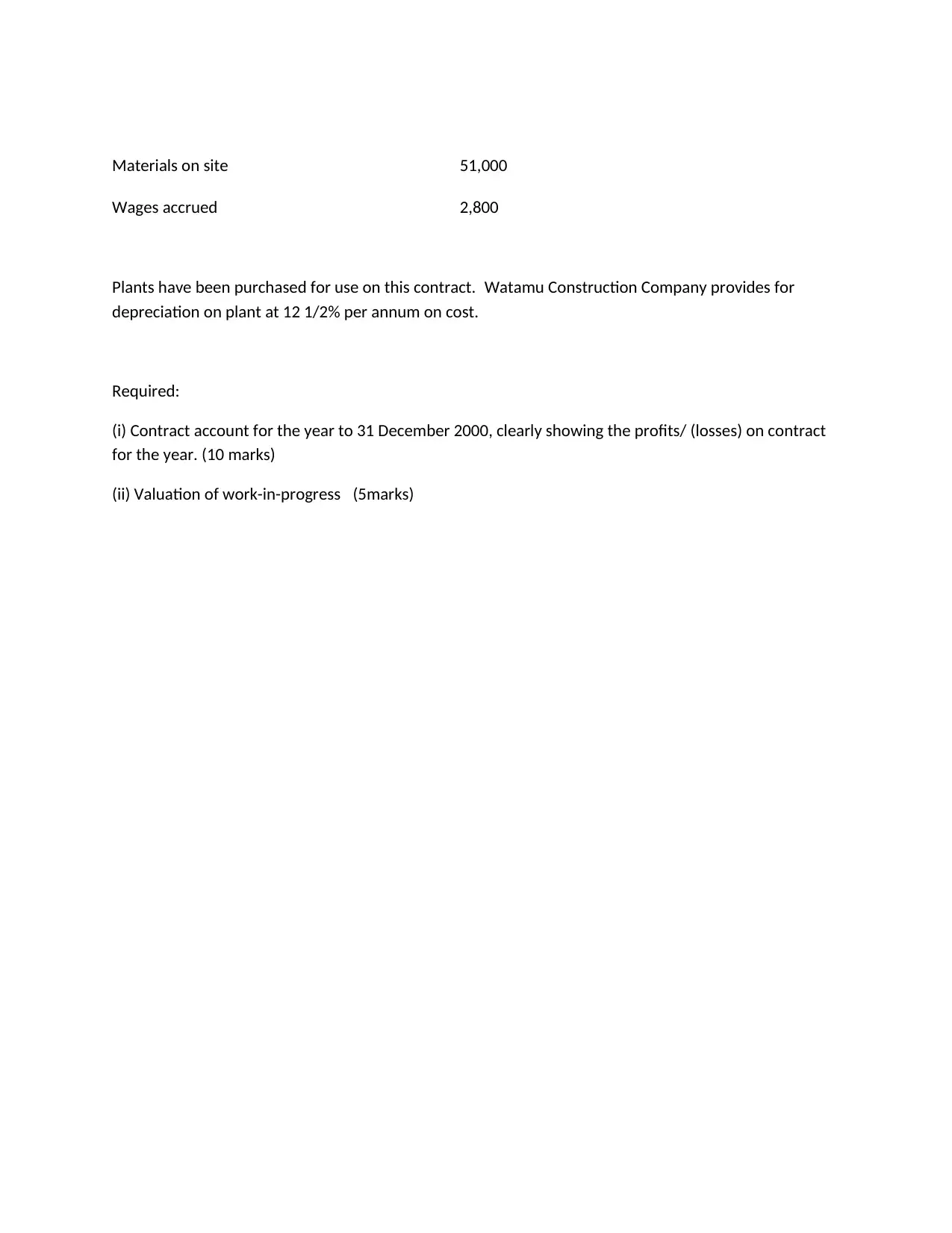

This cost accounting assignment covers several key topics, including inventory valuation using LIFO and FIFO methods, overhead analysis and apportionment across production and service departments, process costing with a focus on the refining process, and contract accounting for a construction project. The assignment includes detailed calculations for inventory records, overhead absorption rates, process accounts, and contract accounts. It also requires the preparation of financial statements such as the contract account, calculation of profit or loss, and valuation of work-in-progress. The assignment also includes scenarios for cost allocation, depreciation, and other accounting principles, providing a comprehensive understanding of cost accounting concepts and practical application.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.