Cost Accounting Principles, Concepts, Techniques and Project Payback

VerifiedAdded on 2023/06/12

|8

|1890

|433

Homework Assignment

AI Summary

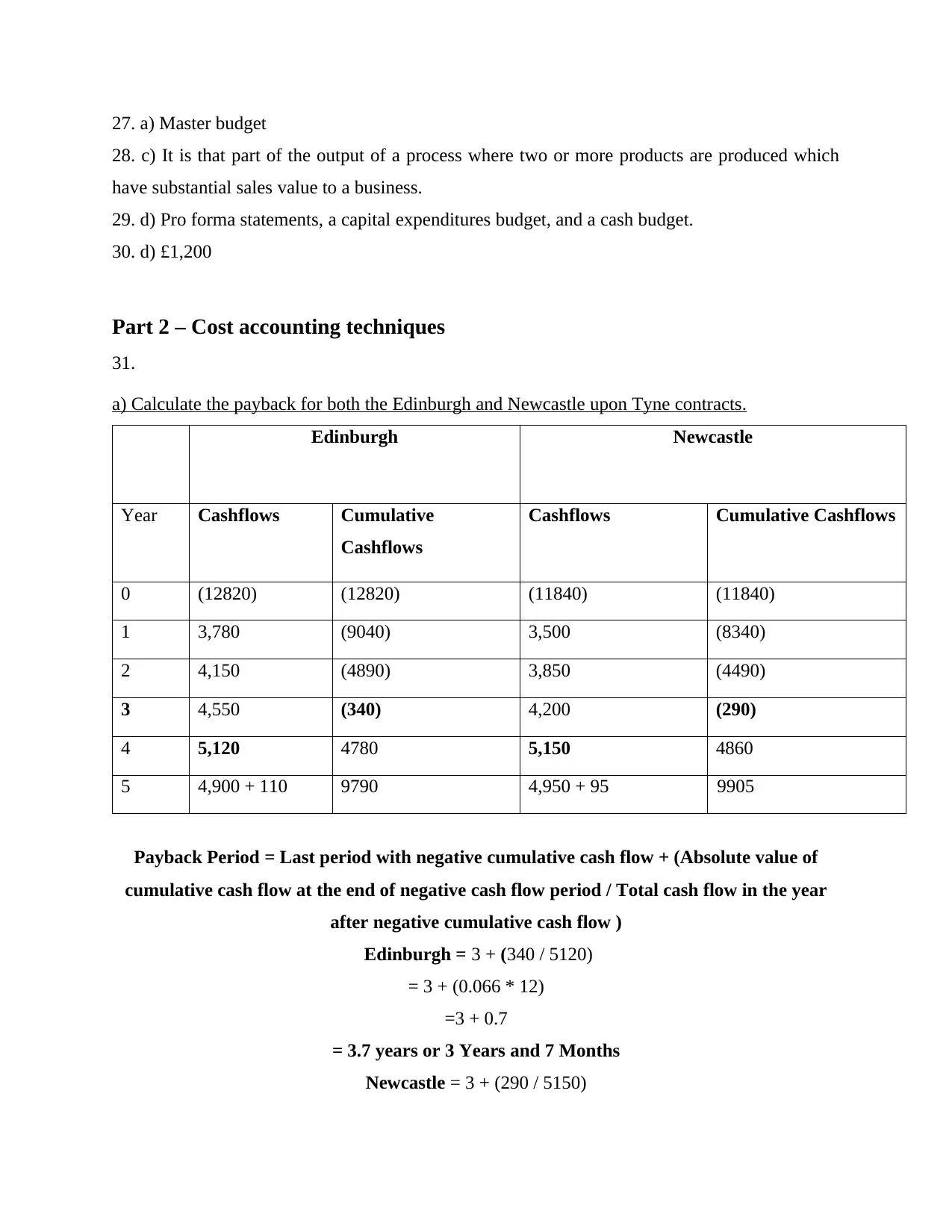

This document provides a comprehensive overview of cost accounting principles, concepts, and techniques, including solutions to multiple-choice questions (MCQs). It delves into cost accounting techniques such as payback period calculation for projects in Edinburgh and Newcastle, critically evaluating the payback technique, and discussing the characteristics of investment appraisal decisions along with the advantages and disadvantages of the Internal Rate of Return (IRR). The analysis includes detailed calculations, interpretations, and critical evaluations supported by relevant academic references, offering a robust understanding of cost accounting and investment appraisal methodologies. Desklib offers a wide array of past papers and solved assignments to aid students in their academic pursuits.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.