Comprehensive Project Report: Cost Accounting Job Costing Analysis

VerifiedAdded on 2021/06/18

|23

|2771

|71

Project

AI Summary

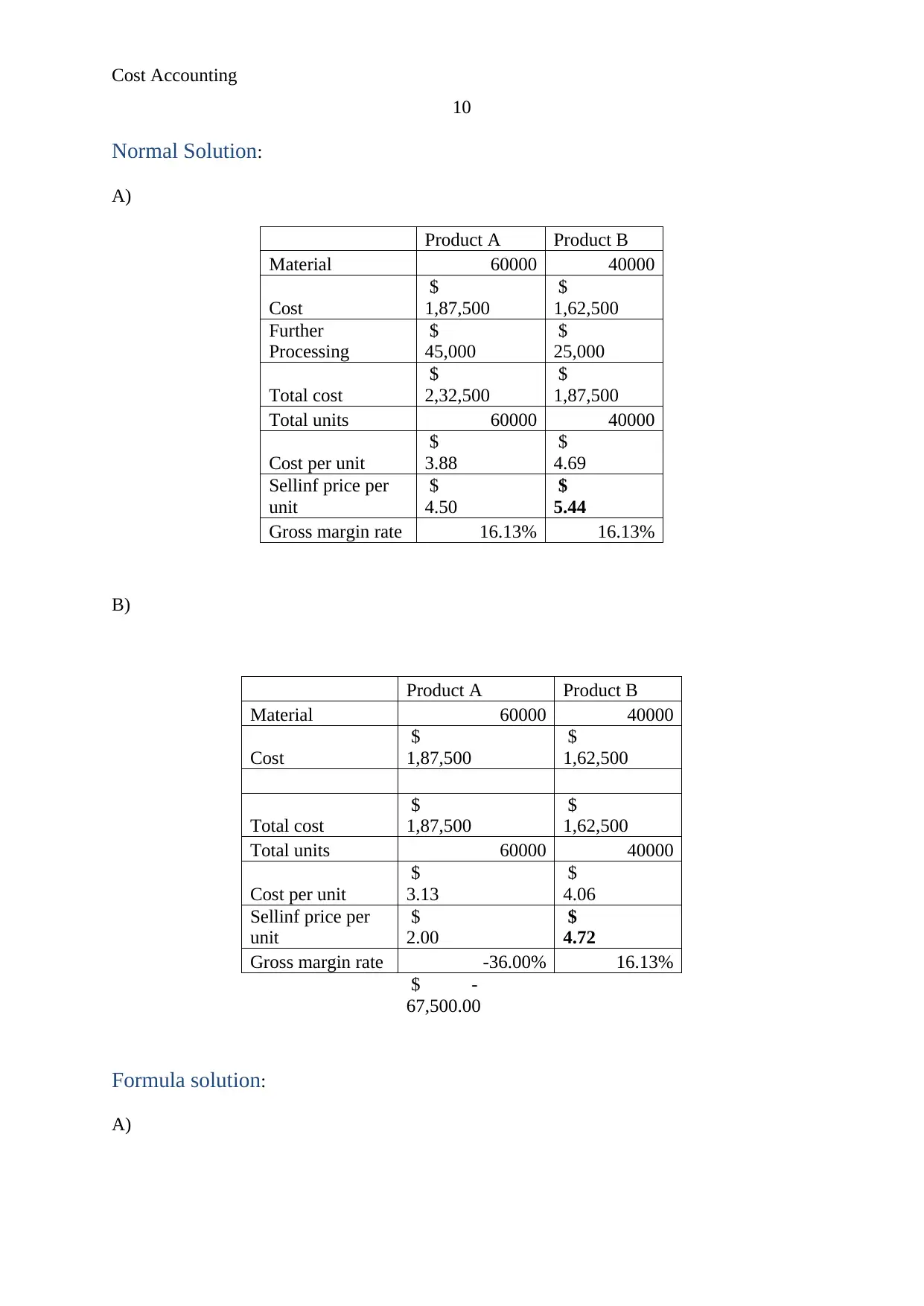

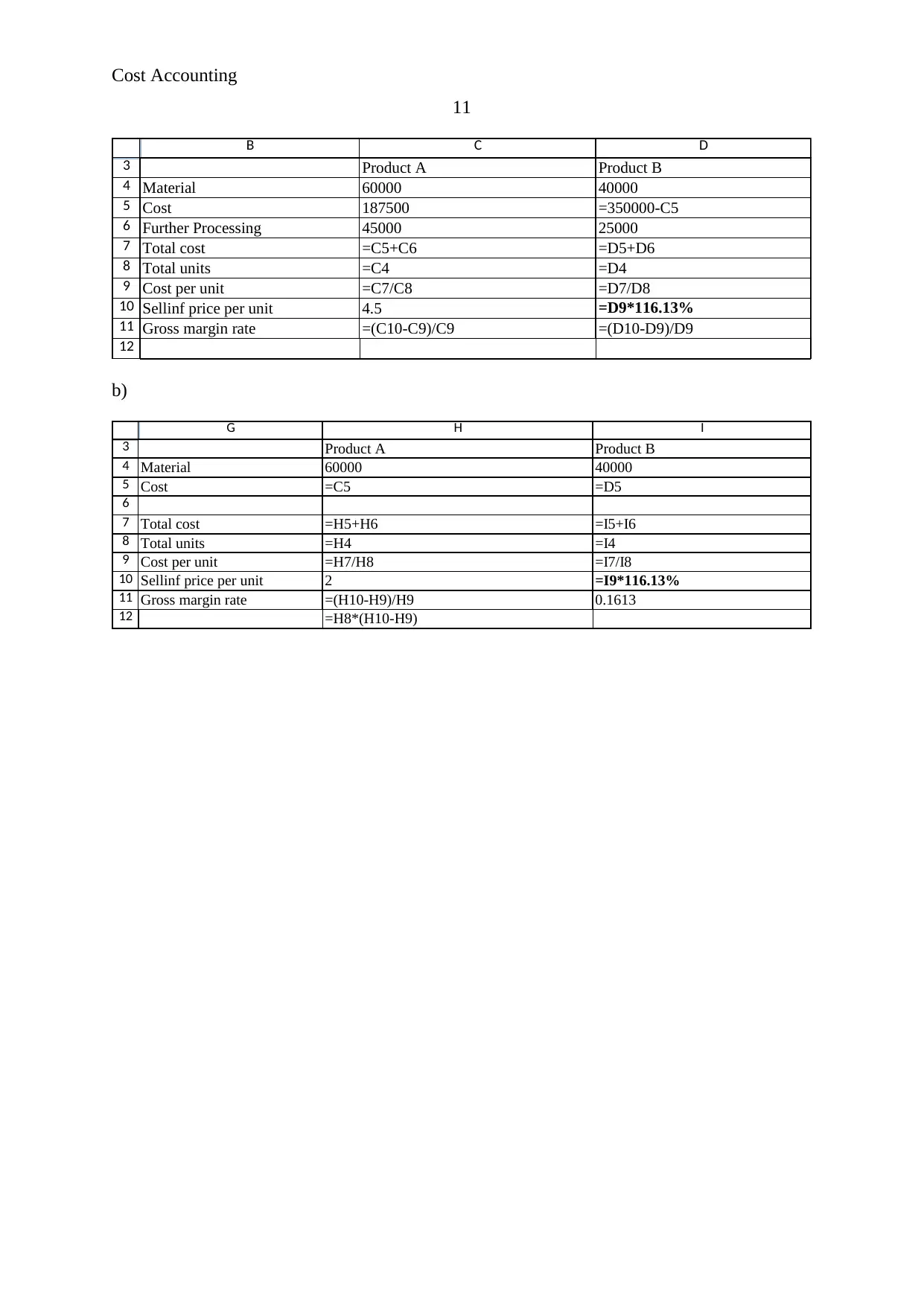

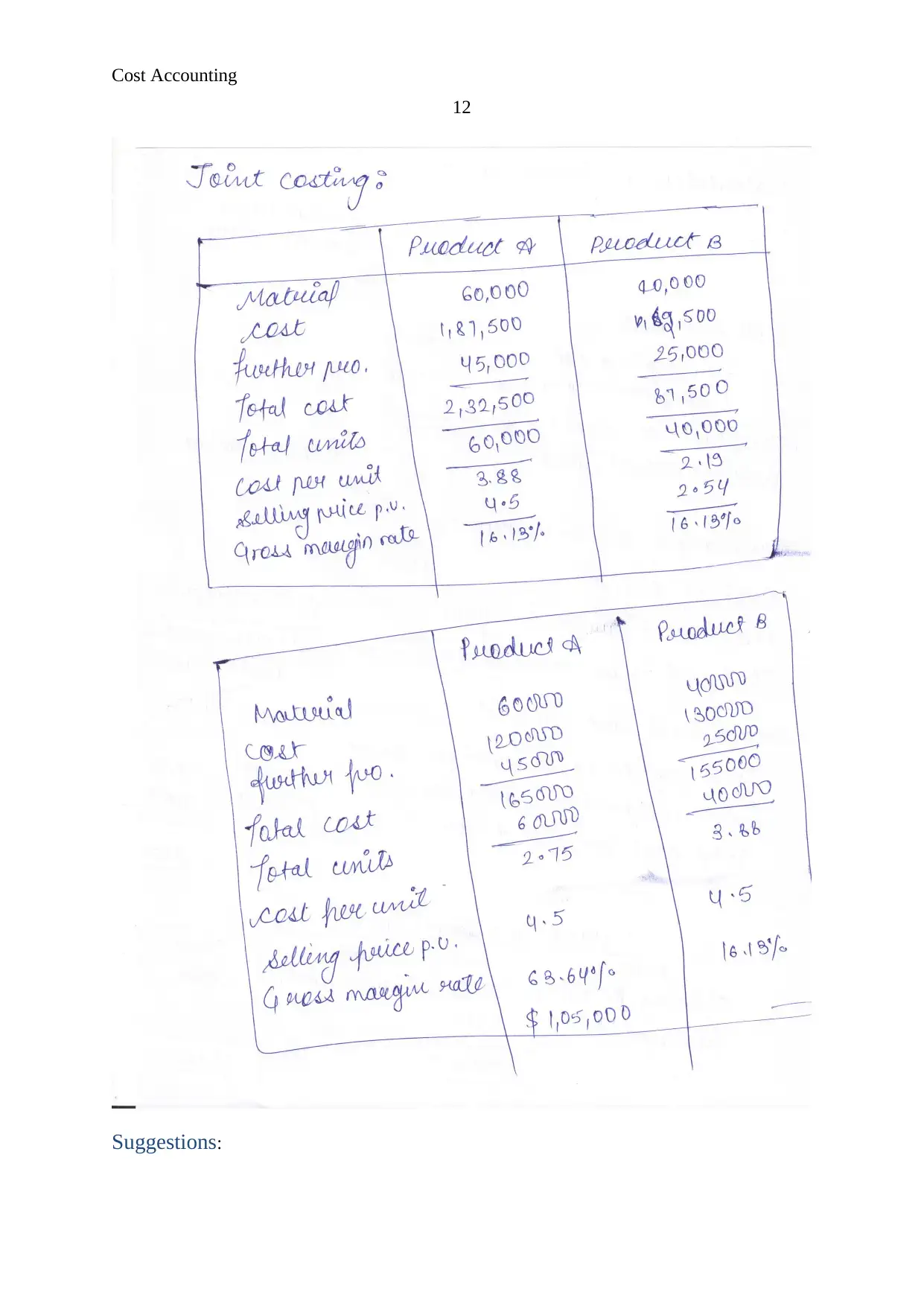

This project report delves into various aspects of cost accounting, presenting detailed analyses of job costing, process costing, and joint costing methods. It includes comprehensive calculations of direct material control, work in process, and finished goods, using both tabular and formulaic solutions. The report extends to variance analysis, demonstrating the calculation of material purchase price and usage variances, along with direct labor variances. Furthermore, it incorporates a business report that emphasizes the importance of variance analysis in evaluating organizational performance, maintaining costs, and forecasting future outcomes. The report provides a robust understanding of cost accounting principles and their practical application within a business context.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.