Cost Accounting Project Report Analysis and Solutions - Finance 101

VerifiedAdded on 2021/06/17

|22

|2659

|46

Project

AI Summary

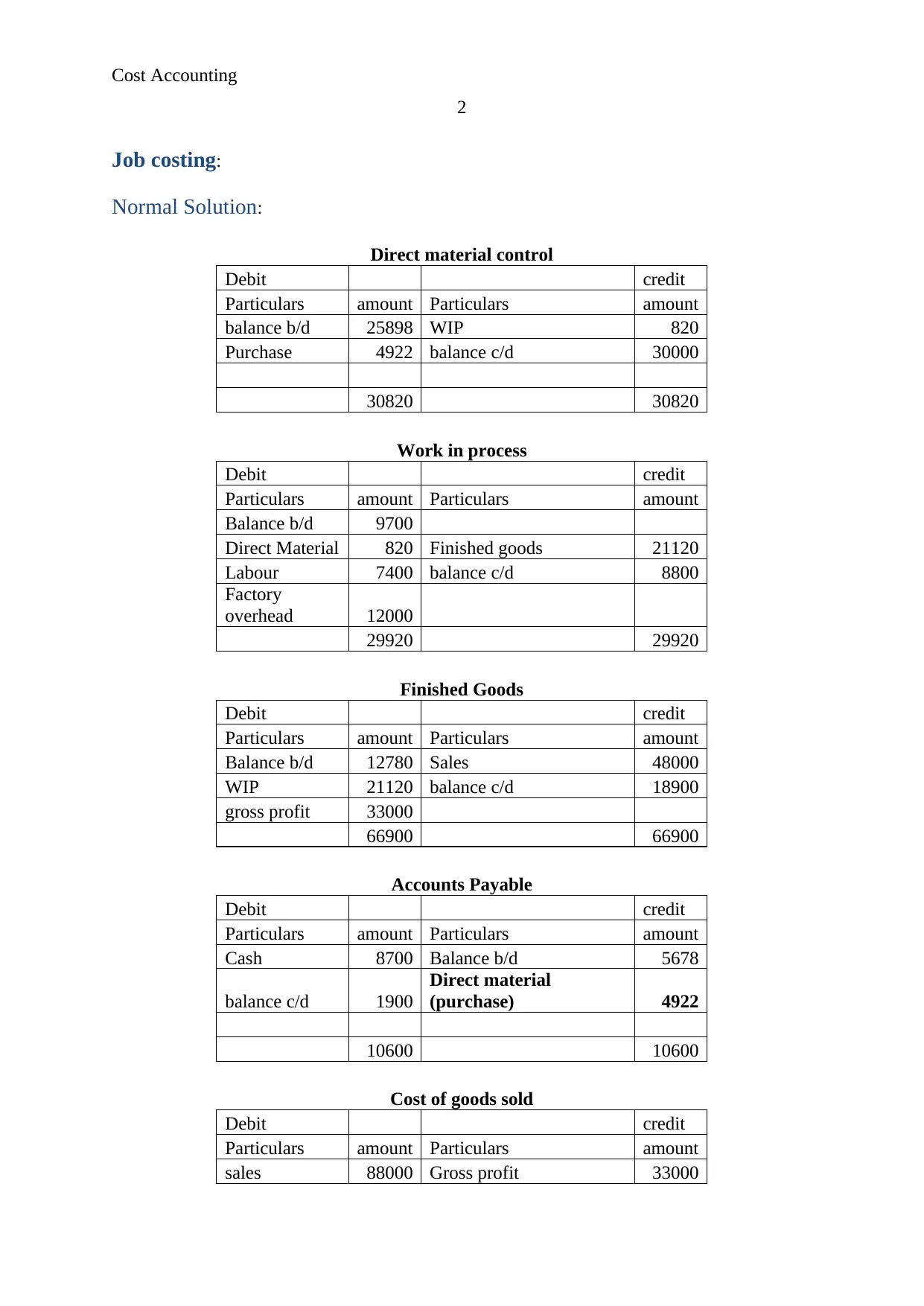

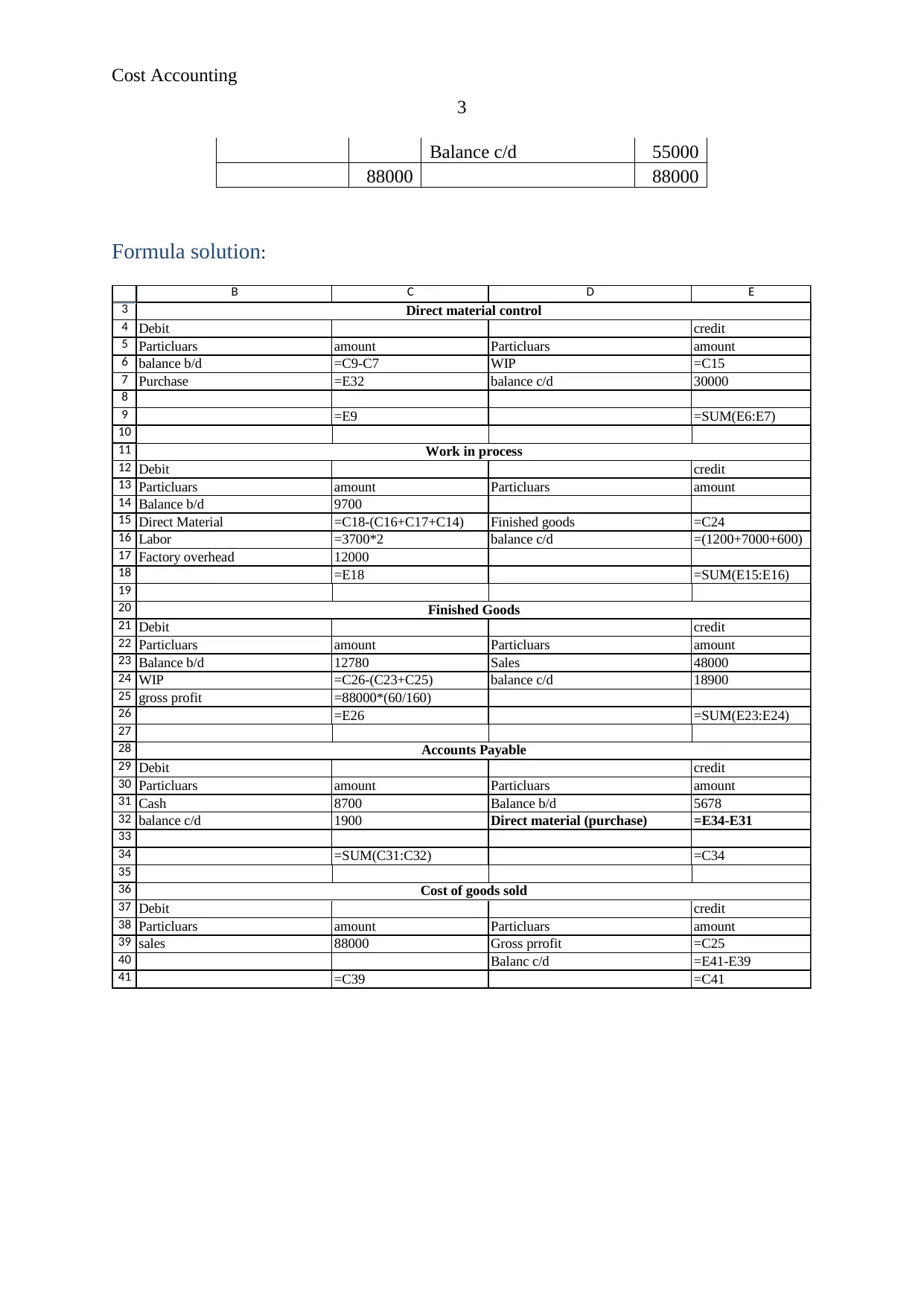

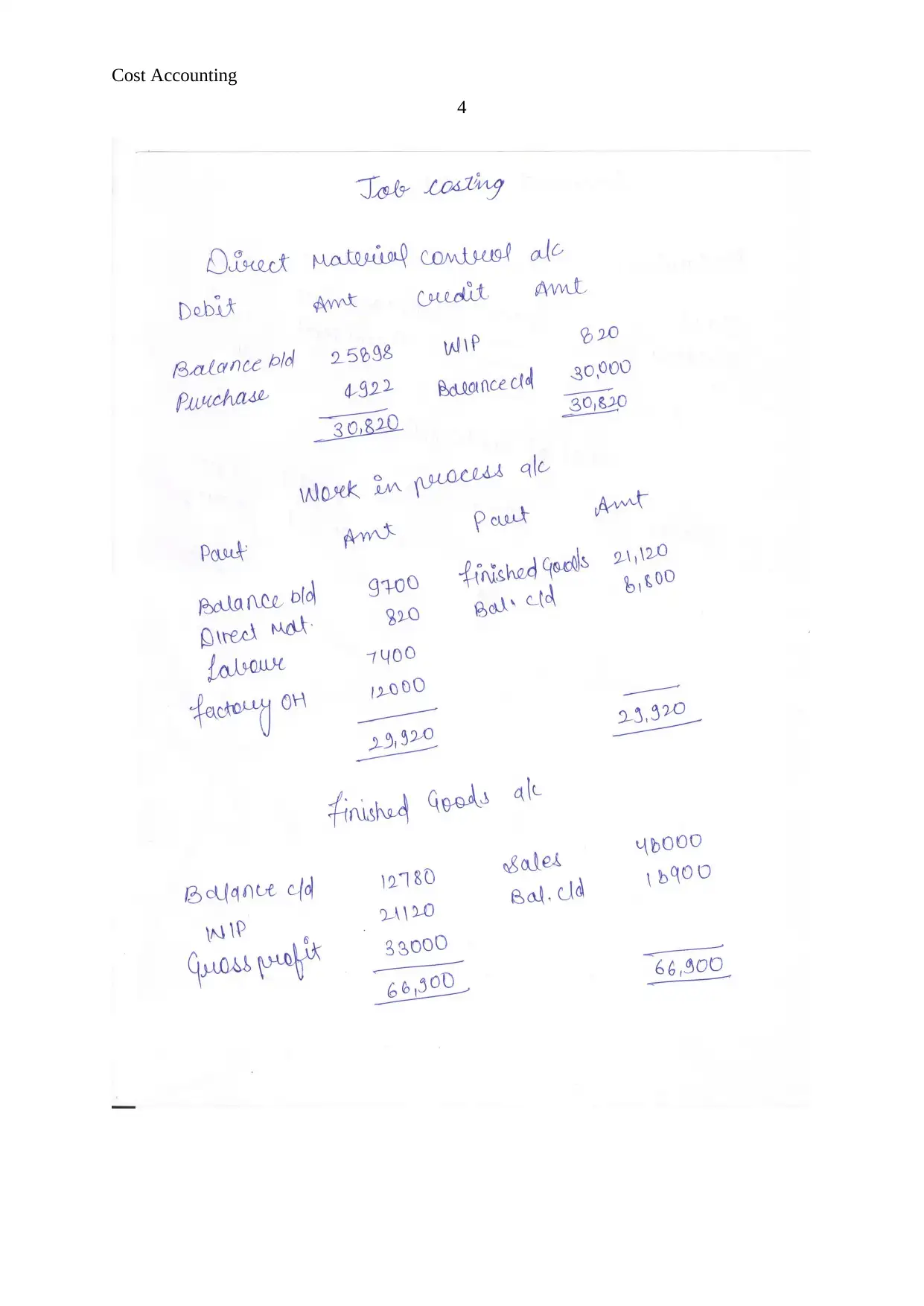

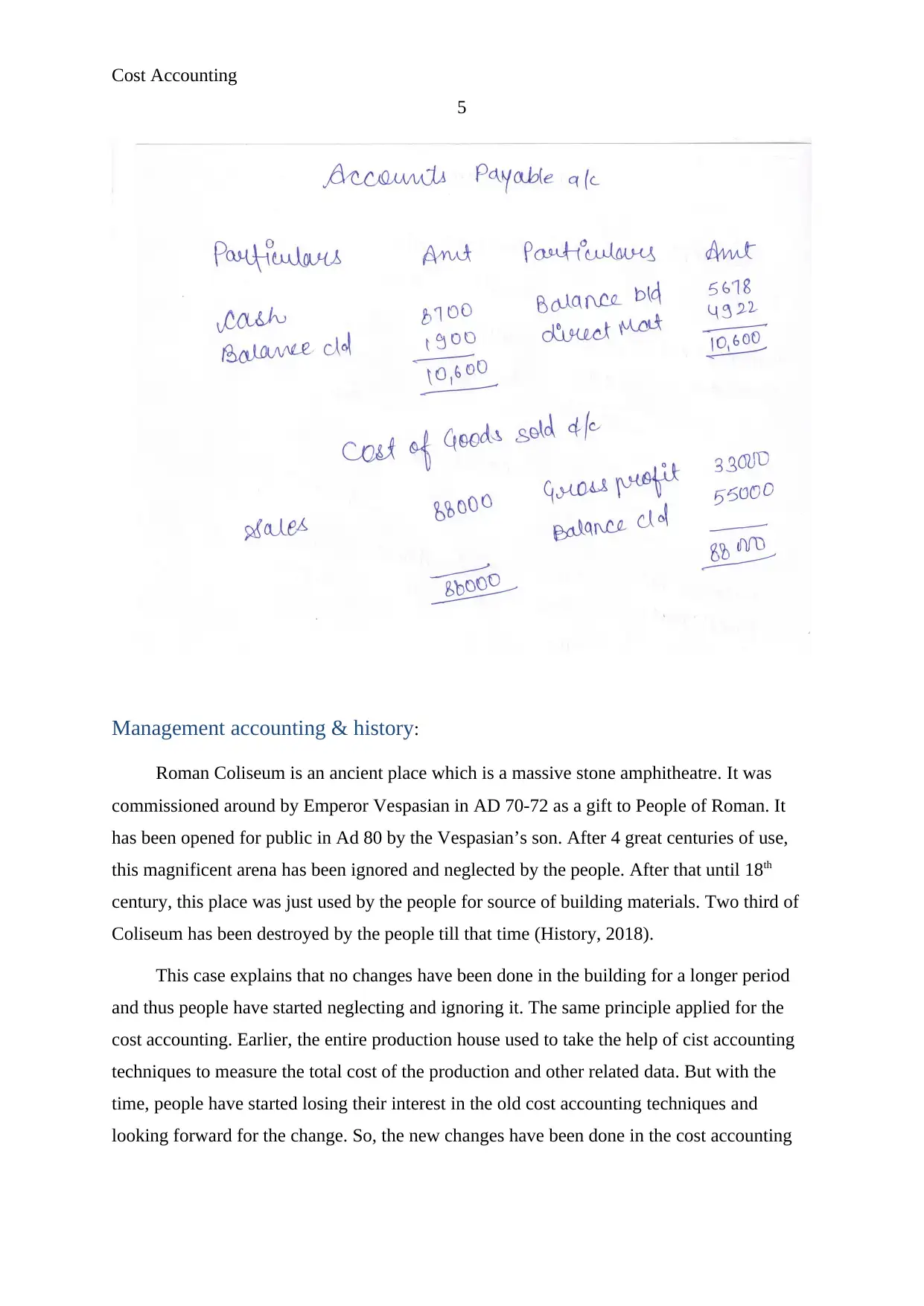

This comprehensive project report delves into various aspects of cost accounting, providing detailed solutions and analyses. It begins with direct material control and work-in-process calculations for job costing, including journal entries and formula-based solutions. The report then explores process costing, presenting a production report and equivalent unit calculations. Furthermore, it covers joint costing, offering solutions for product cost allocation and decision-making regarding further processing. The project also includes a detailed variance analysis, calculating material price and usage variances, as well as labor rate variances. Finally, it culminates in a business report that examines variance analysis, its importance, and overhead variance analysis, with a budget and calculations for cost of goods sold and purchase budget.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.