Multitask Assessment 2: Finance Analysis of Cost Accounting Concepts

VerifiedAdded on 2022/12/19

|9

|1636

|72

Report

AI Summary

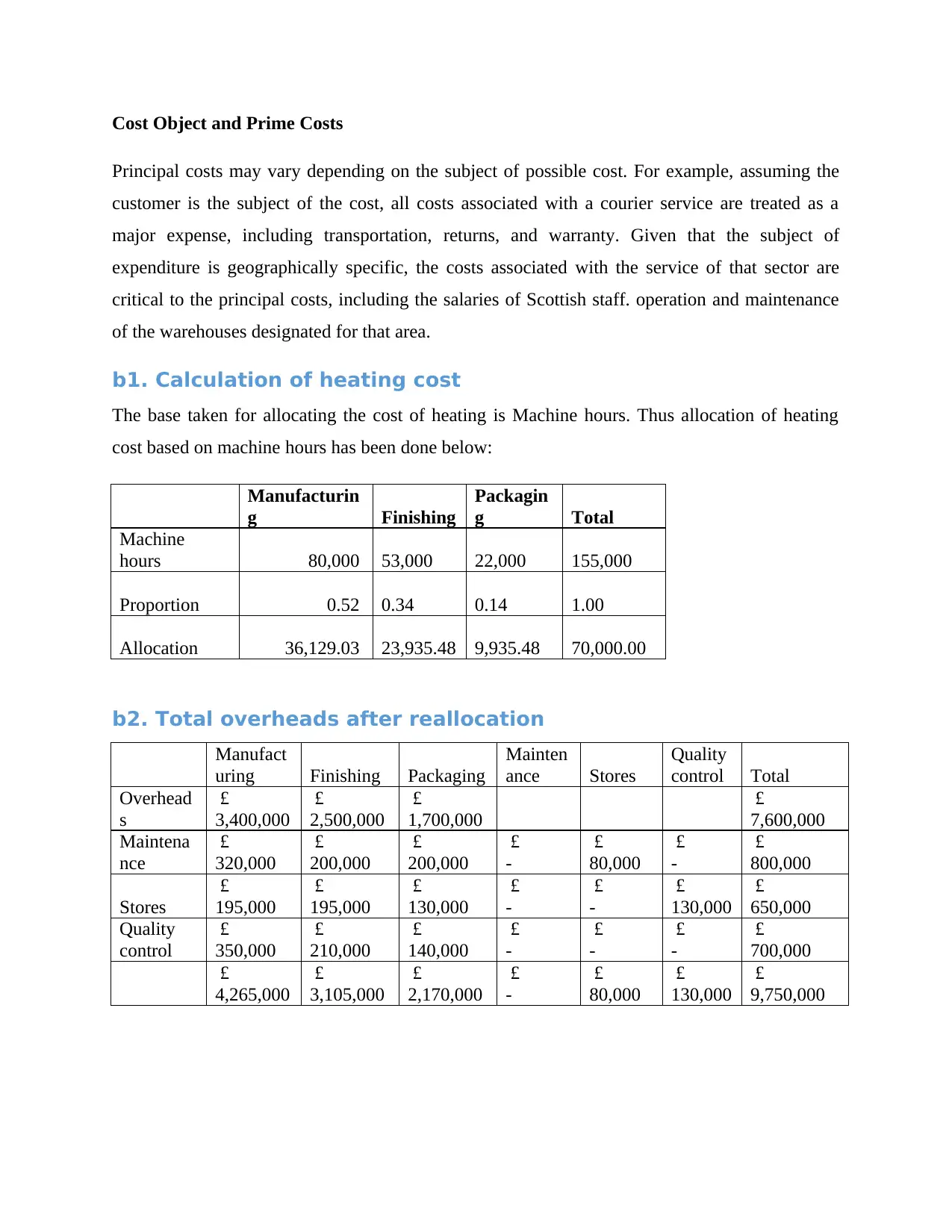

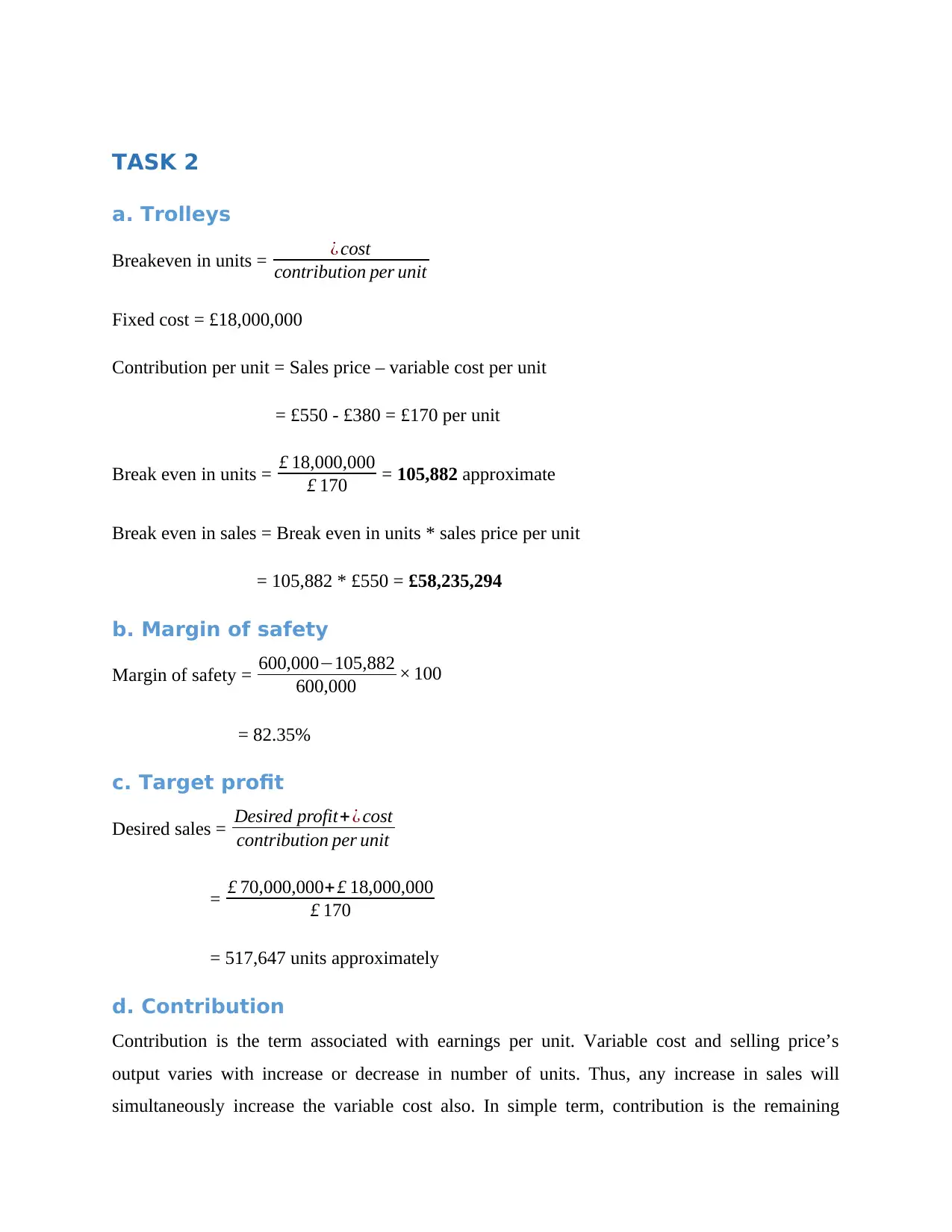

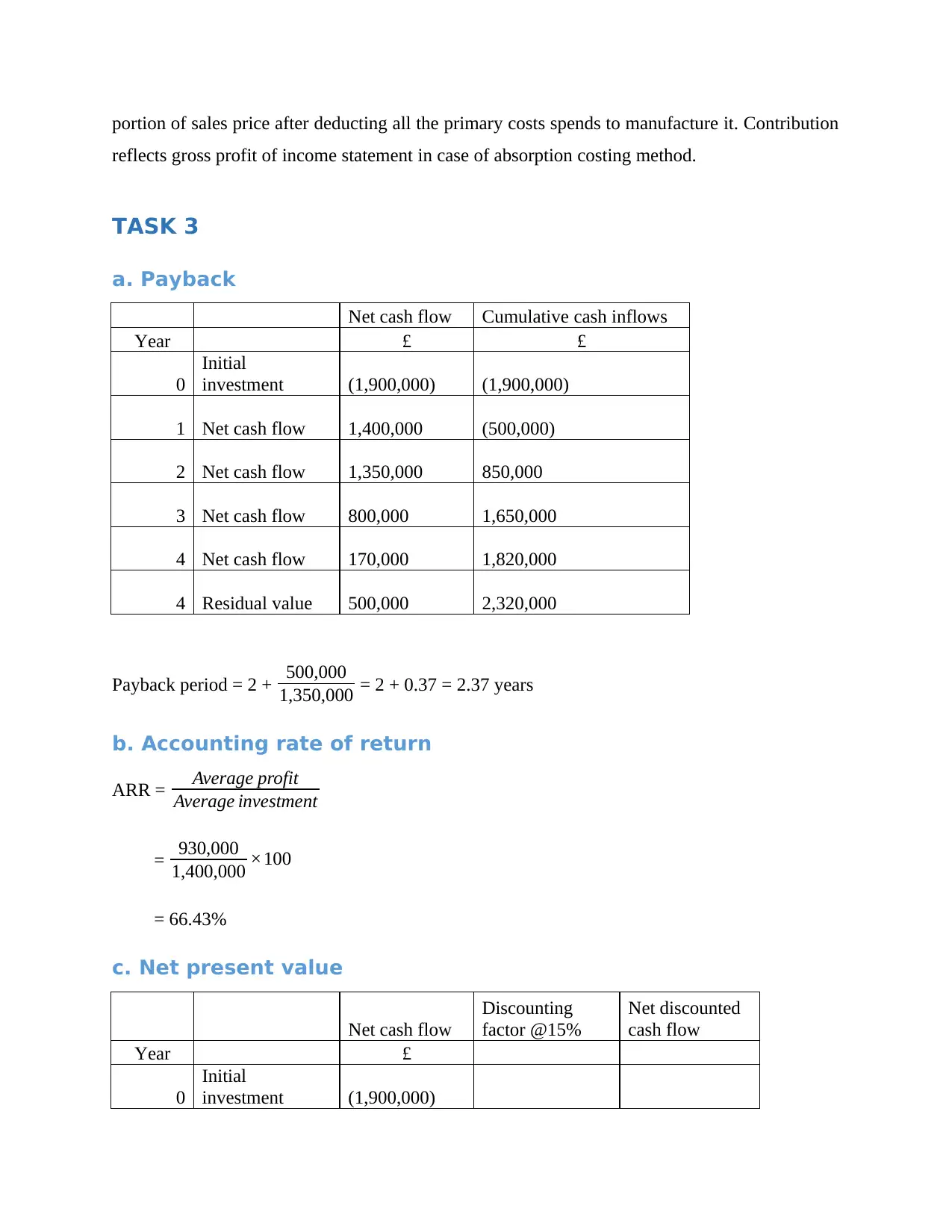

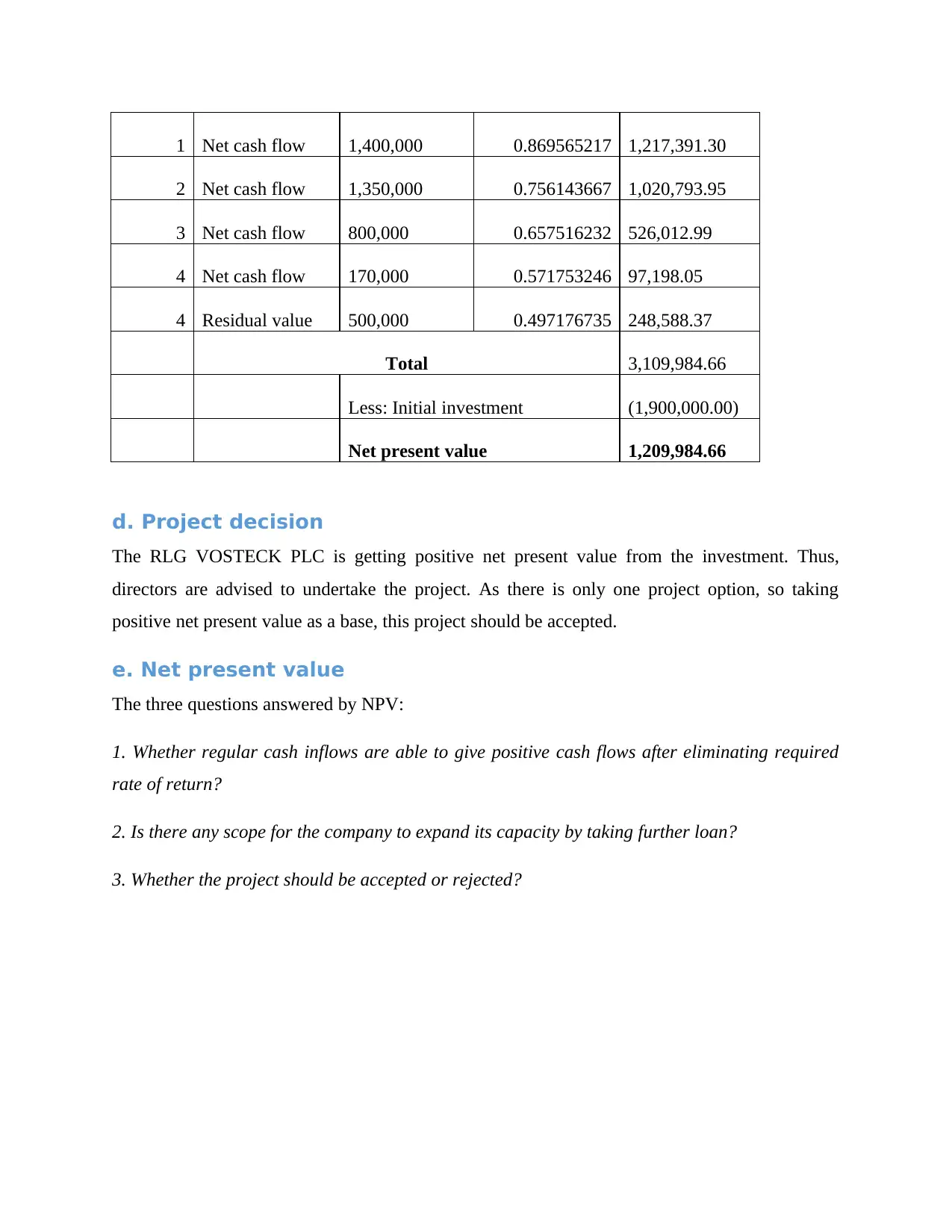

This report presents a comprehensive analysis of cost accounting principles, covering three key tasks. Task 1 focuses on identifying and defining prime costs, including direct materials and direct labor, and calculating overhead allocation based on machine hours, detailing the reallocation of overhead costs across manufacturing, finishing, and packaging departments. Task 2 delves into breakeven analysis, calculating the breakeven point in units and sales, the margin of safety, target profit, and contribution margin for trolleys. Task 3 explores capital budgeting techniques, including payback period, accounting rate of return (ARR), and net present value (NPV) calculations to assess the viability of an investment project, offering insights on project decisions and the interpretation of NPV results. The conclusion highlights the importance of valuation in business decisions.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.