Cost Accounting Project Report: Job Costing and Variance

VerifiedAdded on 2021/06/14

|23

|2626

|93

Project

AI Summary

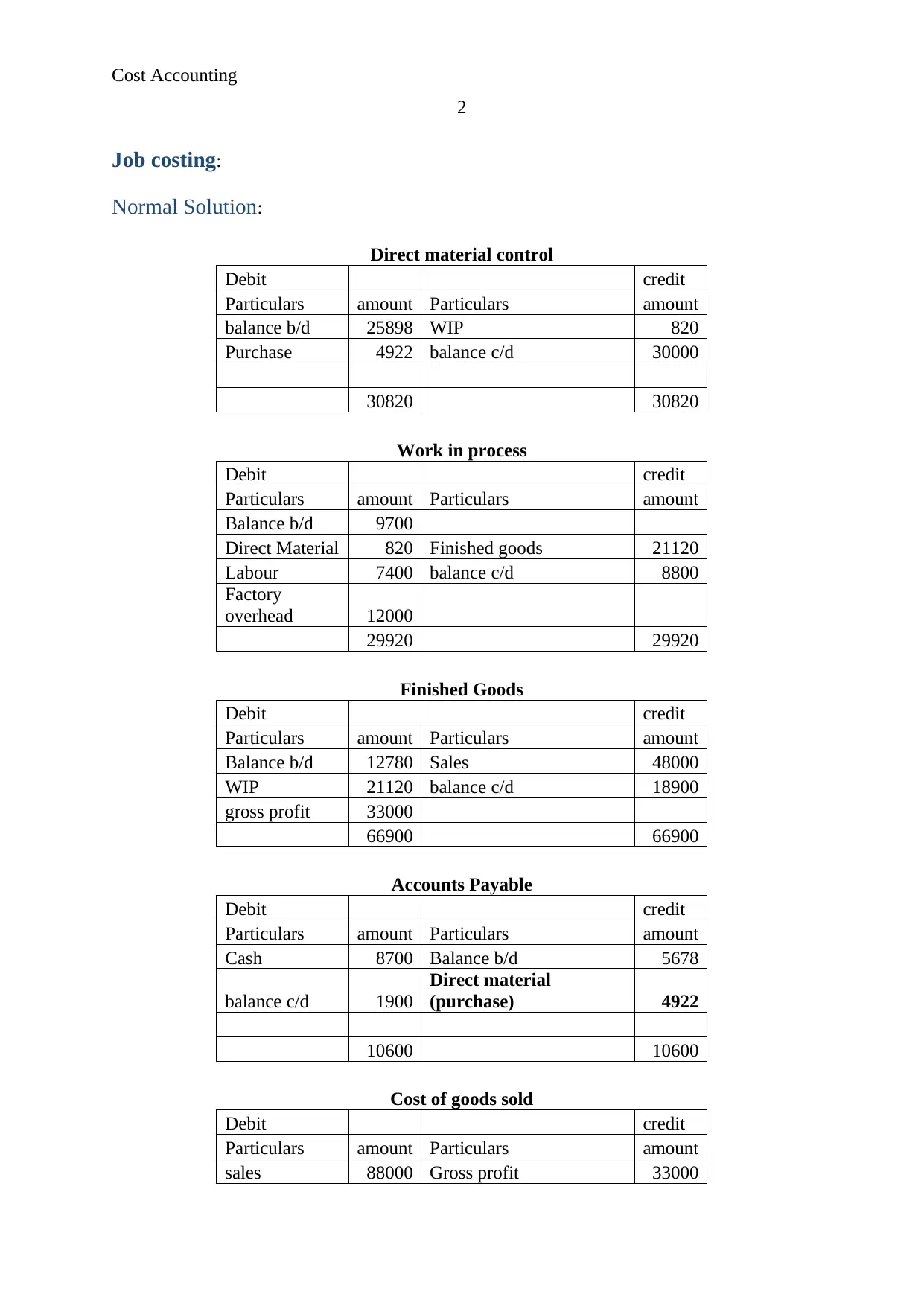

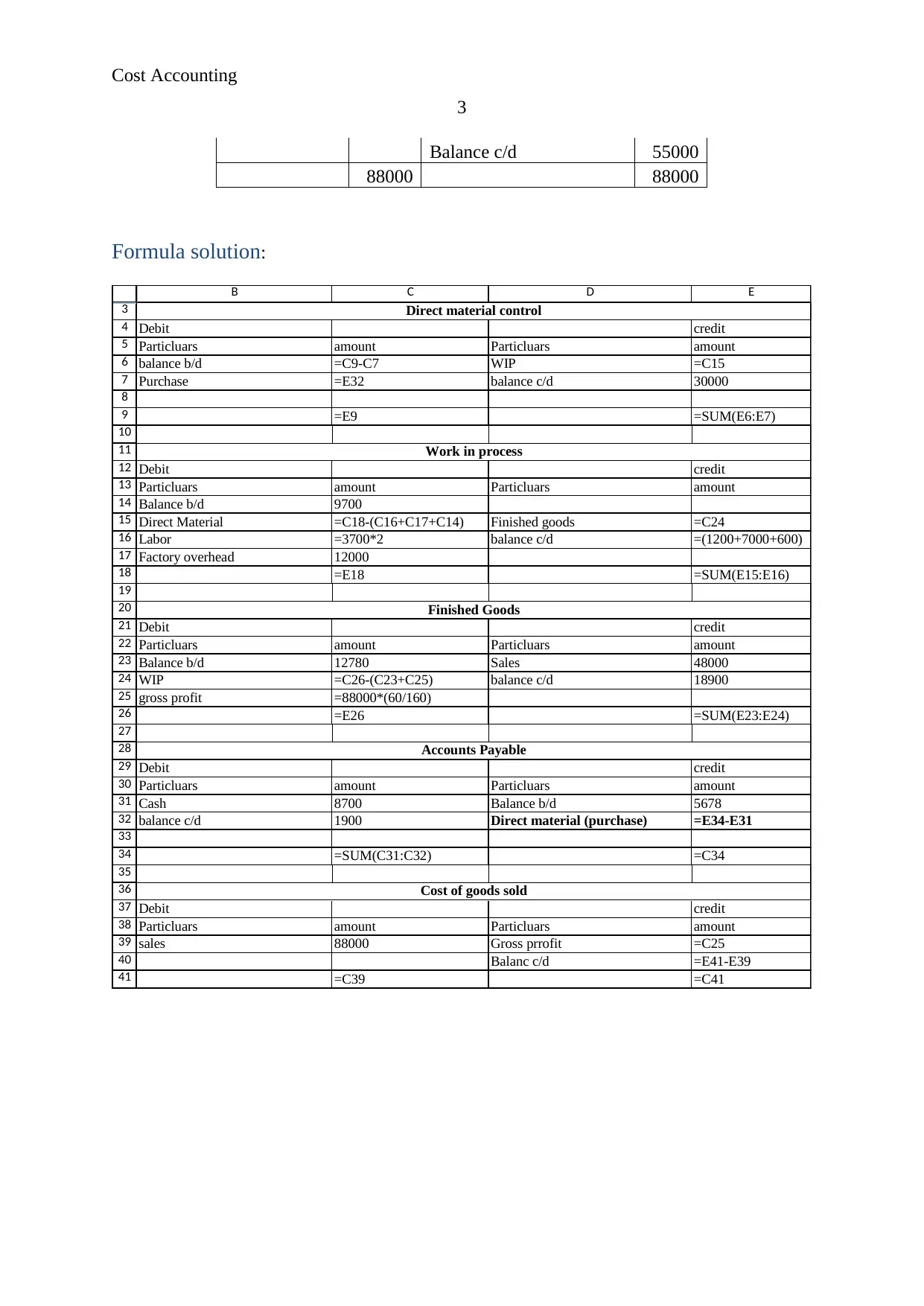

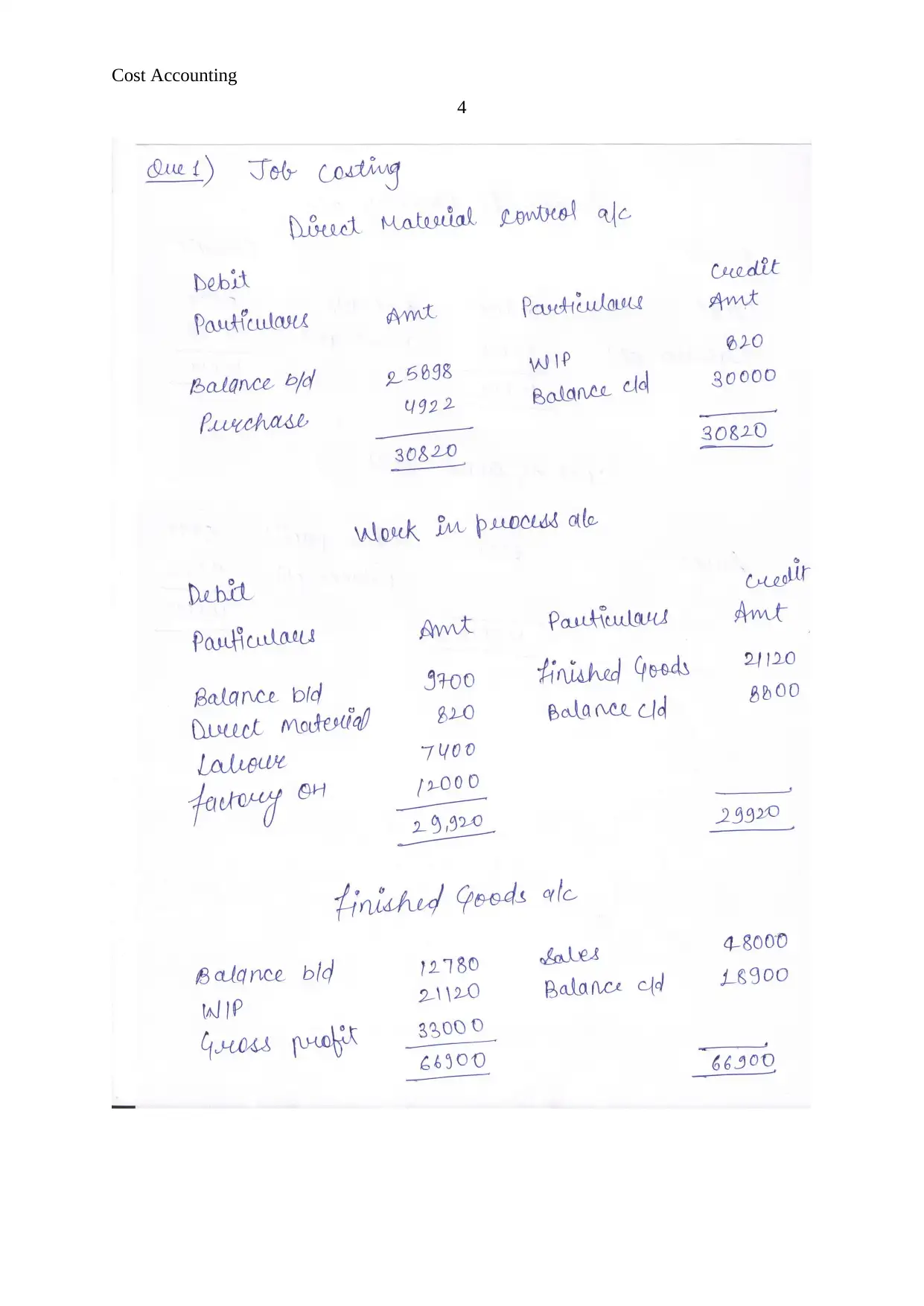

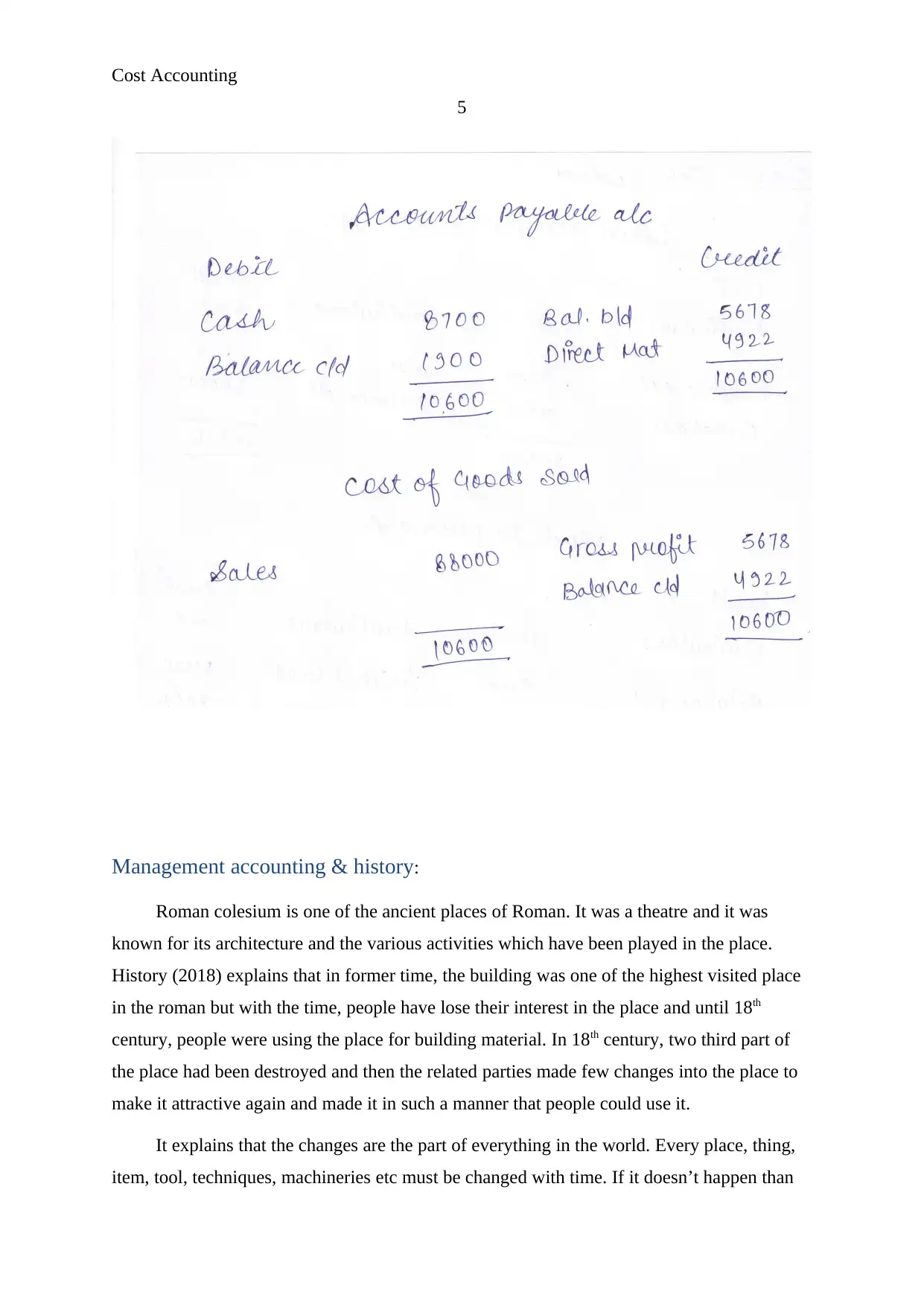

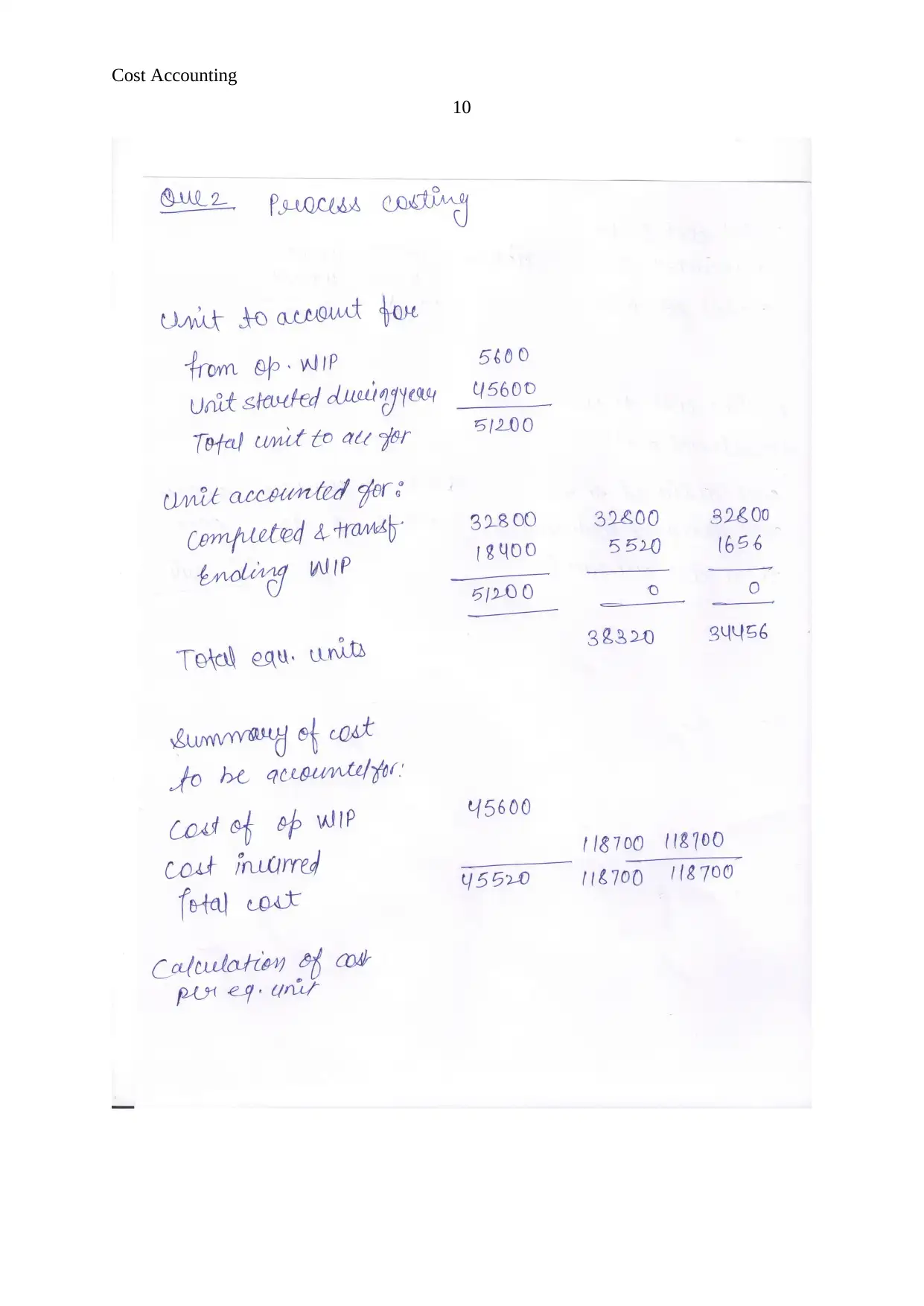

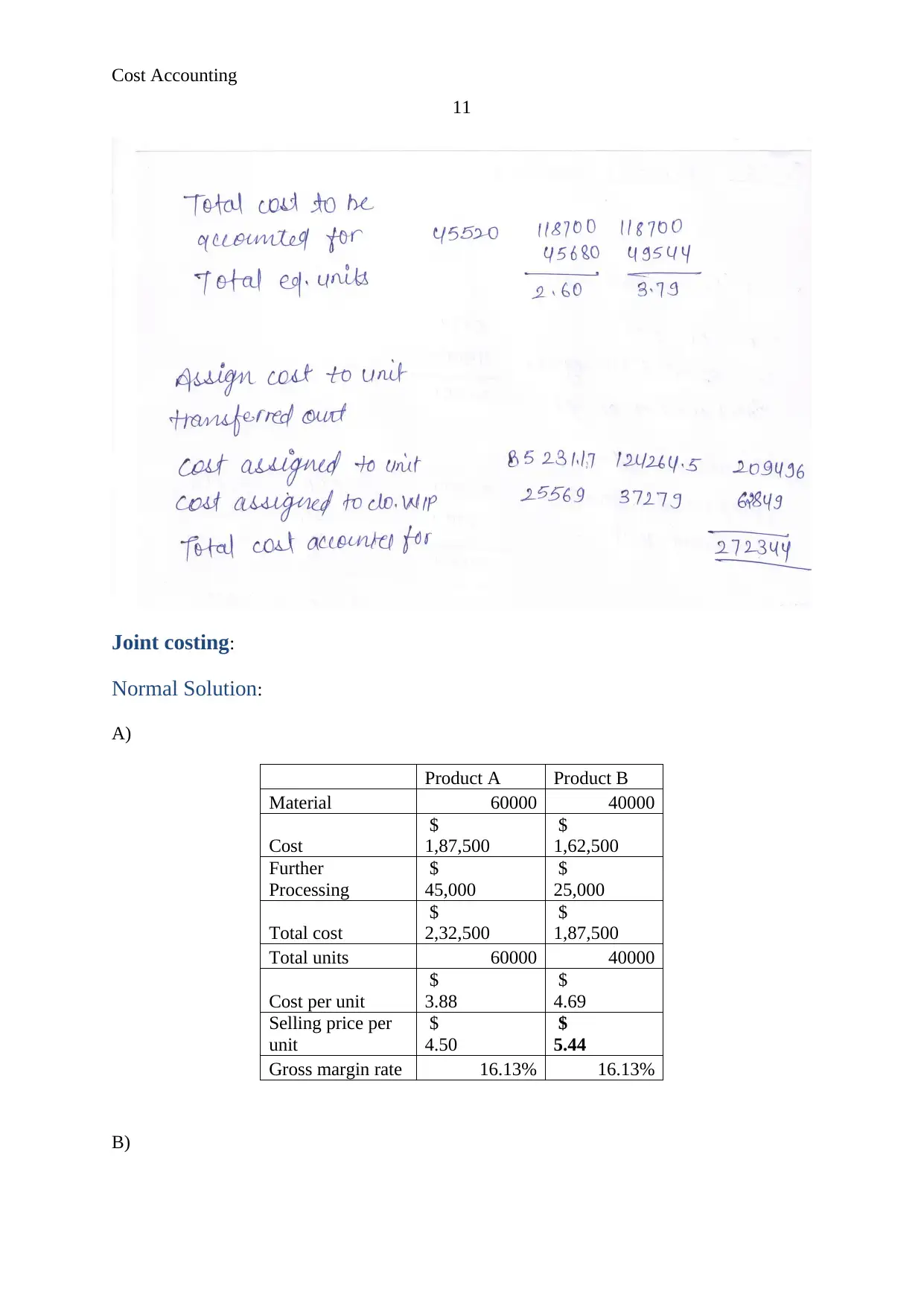

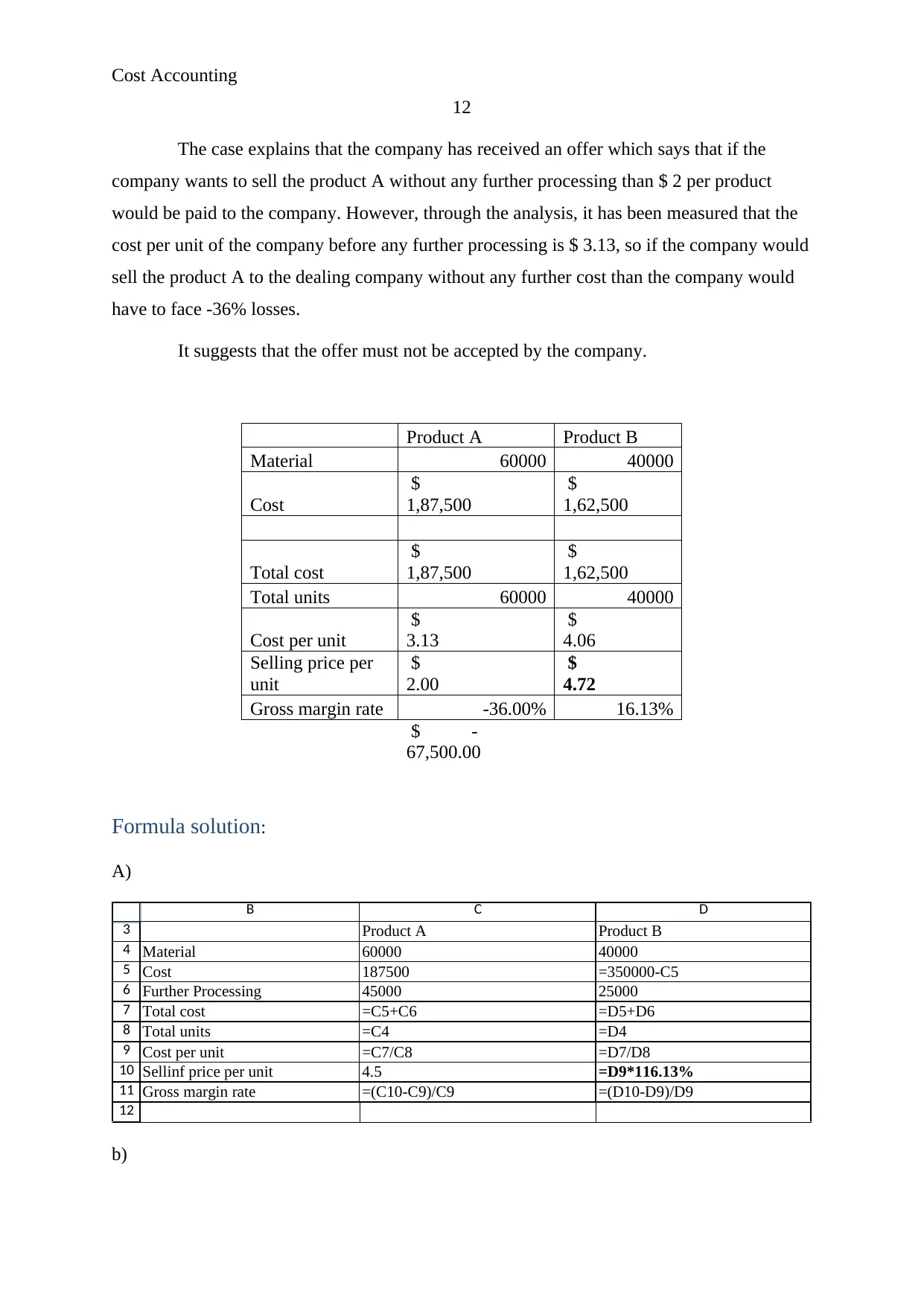

This cost accounting project report provides a detailed analysis of various cost accounting techniques. The report includes solutions for job costing problems, demonstrating the calculation of direct materials, direct labor, and overhead costs. It also covers process costing, joint costing, and variance analysis, including material price and usage variances, and labor rate variances. Additionally, the report presents a business report with an executive summary, introduction, and analysis of overhead variance. The project further incorporates budgeting exercises, including the creation of a purchase budget and cost of goods sold calculations, along with formula solutions and managerial suggestions. This comprehensive report is designed to aid in understanding key cost accounting principles and their application in financial management.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.