Cost Accounting and Control Homework Assignment - Finance Module

VerifiedAdded on 2023/03/21

|13

|2425

|96

Homework Assignment

AI Summary

This assignment solution addresses various aspects of cost accounting and control, including revenue budgeting for Resort Island University with forecasted student growth and fee increases, and explores other budgets such as those related to campus maintenance and canteen operations. It delves into flexible overhead budgets, standard costing, and activity-based costing, calculating overhead costs using different methods and analyzing the reasons for discrepancies. The solution also examines the unit cost of special orders and provides recommendations to management regarding decisions on whether to sell or further process banolide, with financial analysis to support the decision. Furthermore, the assignment presents income statements using both absorption and variable costing methods, compares operating profits, analyzes closing inventory costs, and recommends the appropriate costing method for the company, along with references to relevant literature.

Cost and Cost Accounting Control

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Answer 1..........................................................................................................................................4

Revenue Budget...........................................................................................................................4

Number of staff required to cover classes...................................................................................4

Actions which can be taken in order to accommodate the growing student number..................5

Other budgets...............................................................................................................................5

Answer 2..........................................................................................................................................6

No. of standard clerical hours allowed........................................................................................6

Reason behind formation of Flexible based on number of clerical hours allowed.....................6

Flexible Overhead Budget...........................................................................................................6

Memorandum...............................................................................................................................7

Answer 3..........................................................................................................................................7

Part 1: Total Overhead Cost........................................................................................................7

Part 2: Overhead cost per box......................................................................................................8

Part 3: of overhead rate based on Machine Hours.......................................................................8

Part 4: Calculation of Overhead cost in total and per box of chemical as per requirement three8

Part 5: Reasons of the difference between two methods.............................................................8

Part 6: Calculation of unit cost of special order..........................................................................9

Answer 4..........................................................................................................................................9

Recommendation to management................................................................................................9

Letter to the management of Cool Pool Ltd..............................................................................10

Answer 5........................................................................................................................................11

Operating profit in both costing method....................................................................................12

Closing Inventory cost...............................................................................................................12

Recommendation to management of company..........................................................................12

Answer 1..........................................................................................................................................4

Revenue Budget...........................................................................................................................4

Number of staff required to cover classes...................................................................................4

Actions which can be taken in order to accommodate the growing student number..................5

Other budgets...............................................................................................................................5

Answer 2..........................................................................................................................................6

No. of standard clerical hours allowed........................................................................................6

Reason behind formation of Flexible based on number of clerical hours allowed.....................6

Flexible Overhead Budget...........................................................................................................6

Memorandum...............................................................................................................................7

Answer 3..........................................................................................................................................7

Part 1: Total Overhead Cost........................................................................................................7

Part 2: Overhead cost per box......................................................................................................8

Part 3: of overhead rate based on Machine Hours.......................................................................8

Part 4: Calculation of Overhead cost in total and per box of chemical as per requirement three8

Part 5: Reasons of the difference between two methods.............................................................8

Part 6: Calculation of unit cost of special order..........................................................................9

Answer 4..........................................................................................................................................9

Recommendation to management................................................................................................9

Letter to the management of Cool Pool Ltd..............................................................................10

Answer 5........................................................................................................................................11

Operating profit in both costing method....................................................................................12

Closing Inventory cost...............................................................................................................12

Recommendation to management of company..........................................................................12

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

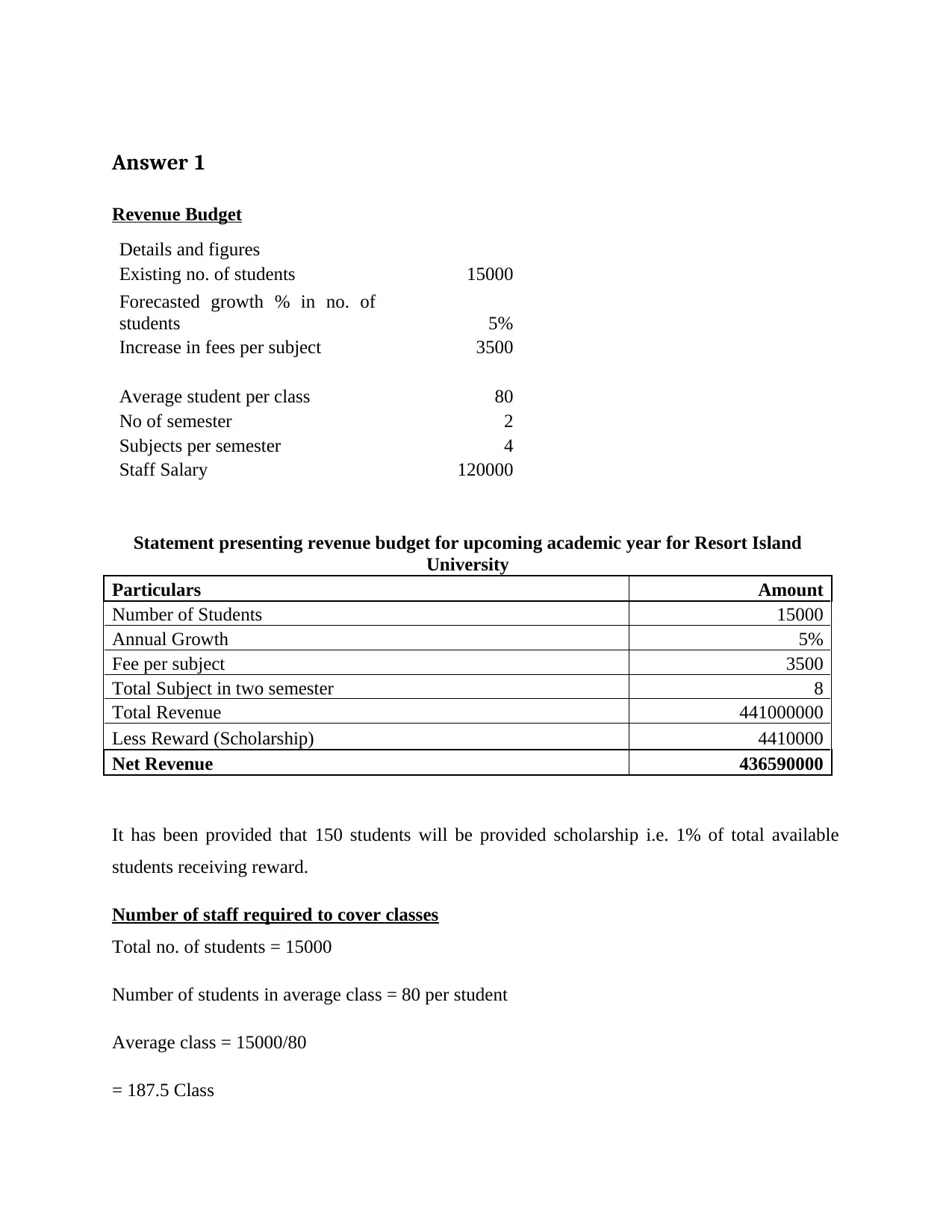

Answer 1

Revenue Budget

Details and figures

Existing no. of students 15000

Forecasted growth % in no. of

students 5%

Increase in fees per subject 3500

Average student per class 80

No of semester 2

Subjects per semester 4

Staff Salary 120000

Statement presenting revenue budget for upcoming academic year for Resort Island

University

Particulars Amount

Number of Students 15000

Annual Growth 5%

Fee per subject 3500

Total Subject in two semester 8

Total Revenue 441000000

Less Reward (Scholarship) 4410000

Net Revenue 436590000

It has been provided that 150 students will be provided scholarship i.e. 1% of total available

students receiving reward.

Number of staff required to cover classes

Total no. of students = 15000

Number of students in average class = 80 per student

Average class = 15000/80

= 187.5 Class

Revenue Budget

Details and figures

Existing no. of students 15000

Forecasted growth % in no. of

students 5%

Increase in fees per subject 3500

Average student per class 80

No of semester 2

Subjects per semester 4

Staff Salary 120000

Statement presenting revenue budget for upcoming academic year for Resort Island

University

Particulars Amount

Number of Students 15000

Annual Growth 5%

Fee per subject 3500

Total Subject in two semester 8

Total Revenue 441000000

Less Reward (Scholarship) 4410000

Net Revenue 436590000

It has been provided that 150 students will be provided scholarship i.e. 1% of total available

students receiving reward.

Number of staff required to cover classes

Total no. of students = 15000

Number of students in average class = 80 per student

Average class = 15000/80

= 187.5 Class

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

No. of subject in one semester = 4 Subject

Total subject = 187.5*4

= 750

One staff cover equivalent of three subjects, therefore number of staff required to cover the class

is: 750/3 i.e. 250 teachers

Actions which can be taken in order to accommodate the growing student number

Providing additional facilities such as sports as well as other hobbies to students.

Provided online lectures to students.

Wi-Fi- Facility in campus.

Extra-classes for weak students (Thaker and etal. 2016).

Cash-prize or other rewards to students attaining high score.

Other budgets

It is expected that in order to maintain the premises an expenditure of $40000000 will be

incurred. Moreover canteen operations will also be outsourced in order to provide facility to

students as well as enhance the profits. It is expected that approximately $1000000 will be

earned from specified source. Moreover, approximately $3500000 will be incurred for

maintenance of library and $41000000 will be incurred for other general and administrative

overheads.

Statement presenting budgeted profit or loss for Resort Island University

Particular Amount in $

Revenue from Students 436590000

Revenue from canteen 10000000

Less

Salary to staff 30000000

Maintenance of library 35000000

Maintenance of premises 40000000

Other general and administrative overhead 41000000

Net Profit 300590000

Total subject = 187.5*4

= 750

One staff cover equivalent of three subjects, therefore number of staff required to cover the class

is: 750/3 i.e. 250 teachers

Actions which can be taken in order to accommodate the growing student number

Providing additional facilities such as sports as well as other hobbies to students.

Provided online lectures to students.

Wi-Fi- Facility in campus.

Extra-classes for weak students (Thaker and etal. 2016).

Cash-prize or other rewards to students attaining high score.

Other budgets

It is expected that in order to maintain the premises an expenditure of $40000000 will be

incurred. Moreover canteen operations will also be outsourced in order to provide facility to

students as well as enhance the profits. It is expected that approximately $1000000 will be

earned from specified source. Moreover, approximately $3500000 will be incurred for

maintenance of library and $41000000 will be incurred for other general and administrative

overheads.

Statement presenting budgeted profit or loss for Resort Island University

Particular Amount in $

Revenue from Students 436590000

Revenue from canteen 10000000

Less

Salary to staff 30000000

Maintenance of library 35000000

Maintenance of premises 40000000

Other general and administrative overhead 41000000

Net Profit 300590000

Answer 2

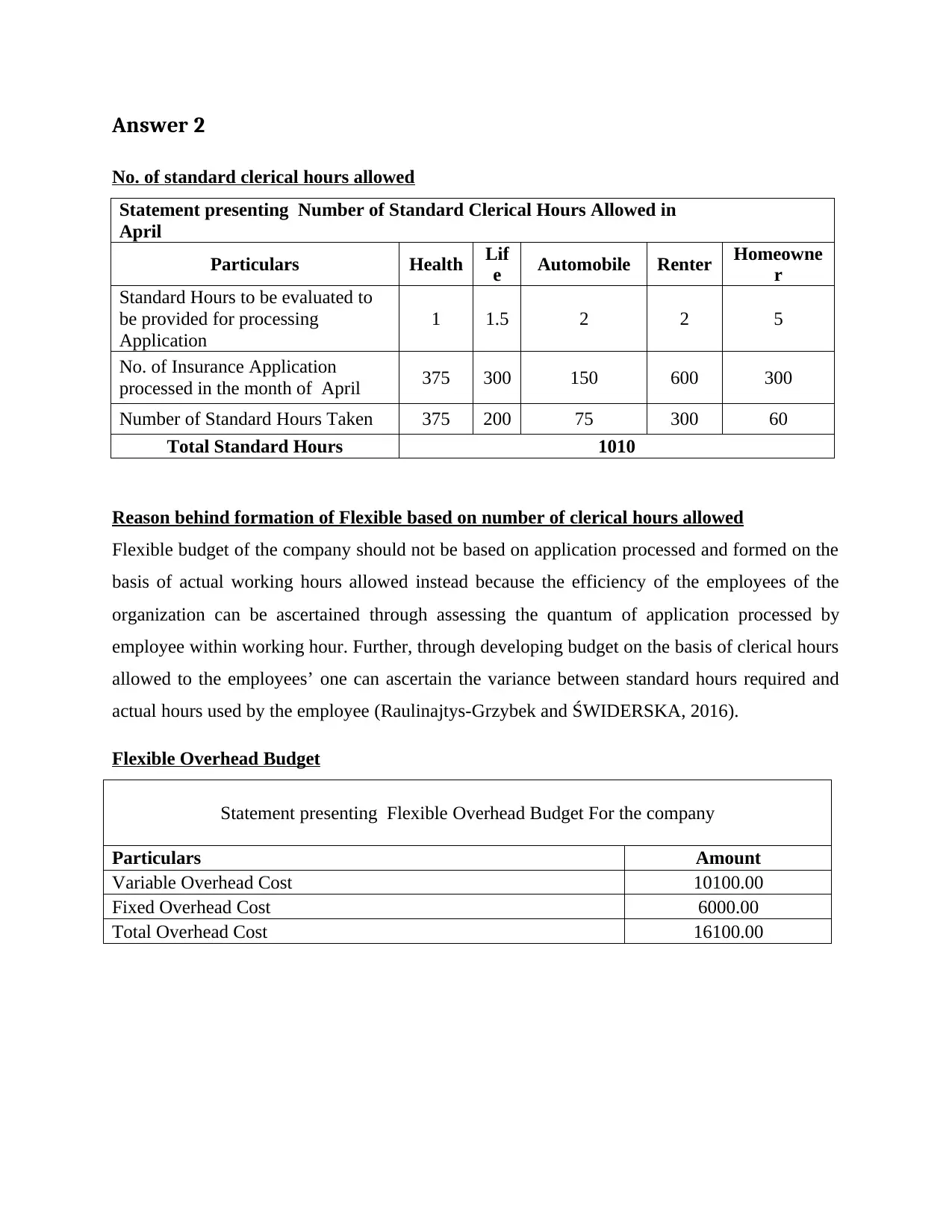

No. of standard clerical hours allowed

Statement presenting Number of Standard Clerical Hours Allowed in

April

Particulars Health Lif

e Automobile Renter Homeowne

r

Standard Hours to be evaluated to

be provided for processing

Application

1 1.5 2 2 5

No. of Insurance Application

processed in the month of April 375 300 150 600 300

Number of Standard Hours Taken 375 200 75 300 60

Total Standard Hours 1010

Reason behind formation of Flexible based on number of clerical hours allowed

Flexible budget of the company should not be based on application processed and formed on the

basis of actual working hours allowed instead because the efficiency of the employees of the

organization can be ascertained through assessing the quantum of application processed by

employee within working hour. Further, through developing budget on the basis of clerical hours

allowed to the employees’ one can ascertain the variance between standard hours required and

actual hours used by the employee (Raulinajtys-Grzybek and ŚWIDERSKA, 2016).

Flexible Overhead Budget

Statement presenting Flexible Overhead Budget For the company

Particulars Amount

Variable Overhead Cost 10100.00

Fixed Overhead Cost 6000.00

Total Overhead Cost 16100.00

No. of standard clerical hours allowed

Statement presenting Number of Standard Clerical Hours Allowed in

April

Particulars Health Lif

e Automobile Renter Homeowne

r

Standard Hours to be evaluated to

be provided for processing

Application

1 1.5 2 2 5

No. of Insurance Application

processed in the month of April 375 300 150 600 300

Number of Standard Hours Taken 375 200 75 300 60

Total Standard Hours 1010

Reason behind formation of Flexible based on number of clerical hours allowed

Flexible budget of the company should not be based on application processed and formed on the

basis of actual working hours allowed instead because the efficiency of the employees of the

organization can be ascertained through assessing the quantum of application processed by

employee within working hour. Further, through developing budget on the basis of clerical hours

allowed to the employees’ one can ascertain the variance between standard hours required and

actual hours used by the employee (Raulinajtys-Grzybek and ŚWIDERSKA, 2016).

Flexible Overhead Budget

Statement presenting Flexible Overhead Budget For the company

Particulars Amount

Variable Overhead Cost 10100.00

Fixed Overhead Cost 6000.00

Total Overhead Cost 16100.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

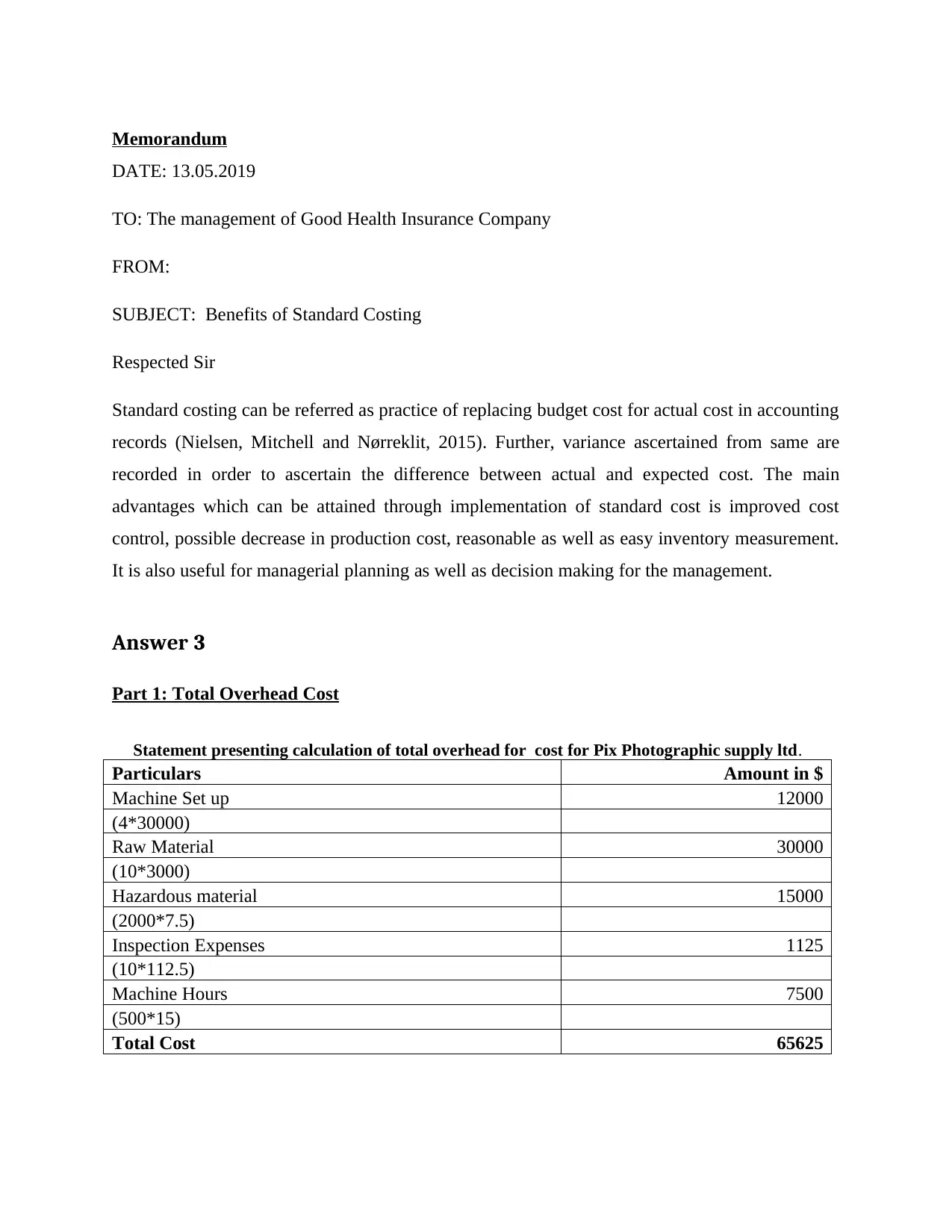

Memorandum

DATE: 13.05.2019

TO: The management of Good Health Insurance Company

FROM:

SUBJECT: Benefits of Standard Costing

Respected Sir

Standard costing can be referred as practice of replacing budget cost for actual cost in accounting

records (Nielsen, Mitchell and Nørreklit, 2015). Further, variance ascertained from same are

recorded in order to ascertain the difference between actual and expected cost. The main

advantages which can be attained through implementation of standard cost is improved cost

control, possible decrease in production cost, reasonable as well as easy inventory measurement.

It is also useful for managerial planning as well as decision making for the management.

Answer 3

Part 1: Total Overhead Cost

Statement presenting calculation of total overhead for cost for Pix Photographic supply ltd.

Particulars Amount in $

Machine Set up 12000

(4*30000)

Raw Material 30000

(10*3000)

Hazardous material 15000

(2000*7.5)

Inspection Expenses 1125

(10*112.5)

Machine Hours 7500

(500*15)

Total Cost 65625

DATE: 13.05.2019

TO: The management of Good Health Insurance Company

FROM:

SUBJECT: Benefits of Standard Costing

Respected Sir

Standard costing can be referred as practice of replacing budget cost for actual cost in accounting

records (Nielsen, Mitchell and Nørreklit, 2015). Further, variance ascertained from same are

recorded in order to ascertain the difference between actual and expected cost. The main

advantages which can be attained through implementation of standard cost is improved cost

control, possible decrease in production cost, reasonable as well as easy inventory measurement.

It is also useful for managerial planning as well as decision making for the management.

Answer 3

Part 1: Total Overhead Cost

Statement presenting calculation of total overhead for cost for Pix Photographic supply ltd.

Particulars Amount in $

Machine Set up 12000

(4*30000)

Raw Material 30000

(10*3000)

Hazardous material 15000

(2000*7.5)

Inspection Expenses 1125

(10*112.5)

Machine Hours 7500

(500*15)

Total Cost 65625

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

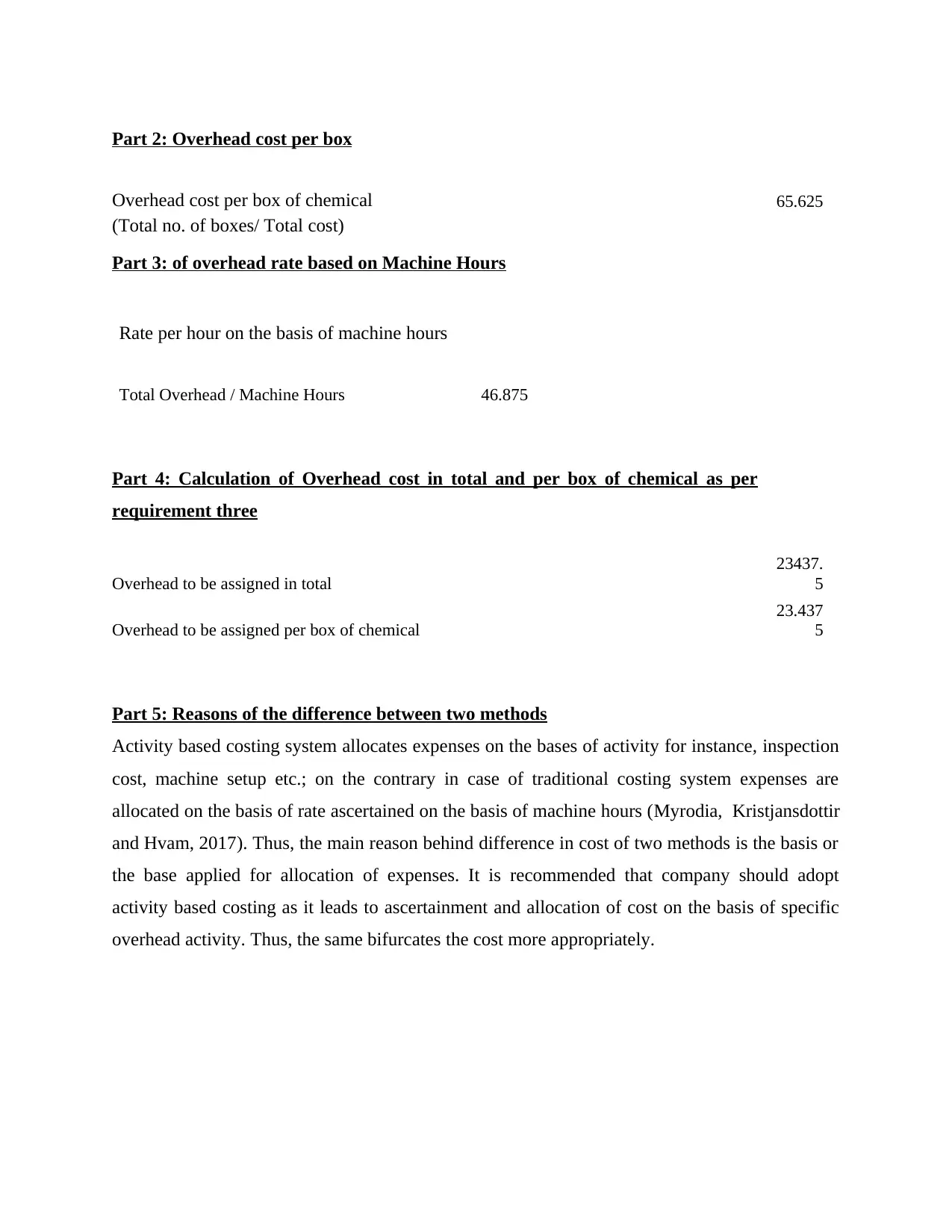

Part 2: Overhead cost per box

Overhead cost per box of chemical 65.625

(Total no. of boxes/ Total cost)

Part 3: of overhead rate based on Machine Hours

Rate per hour on the basis of machine hours

Total Overhead / Machine Hours 46.875

Part 4: Calculation of Overhead cost in total and per box of chemical as per

requirement three

Overhead to be assigned in total

23437.

5

Overhead to be assigned per box of chemical

23.437

5

Part 5: Reasons of the difference between two methods

Activity based costing system allocates expenses on the bases of activity for instance, inspection

cost, machine setup etc.; on the contrary in case of traditional costing system expenses are

allocated on the basis of rate ascertained on the basis of machine hours (Myrodia, Kristjansdottir

and Hvam, 2017). Thus, the main reason behind difference in cost of two methods is the basis or

the base applied for allocation of expenses. It is recommended that company should adopt

activity based costing as it leads to ascertainment and allocation of cost on the basis of specific

overhead activity. Thus, the same bifurcates the cost more appropriately.

Overhead cost per box of chemical 65.625

(Total no. of boxes/ Total cost)

Part 3: of overhead rate based on Machine Hours

Rate per hour on the basis of machine hours

Total Overhead / Machine Hours 46.875

Part 4: Calculation of Overhead cost in total and per box of chemical as per

requirement three

Overhead to be assigned in total

23437.

5

Overhead to be assigned per box of chemical

23.437

5

Part 5: Reasons of the difference between two methods

Activity based costing system allocates expenses on the bases of activity for instance, inspection

cost, machine setup etc.; on the contrary in case of traditional costing system expenses are

allocated on the basis of rate ascertained on the basis of machine hours (Myrodia, Kristjansdottir

and Hvam, 2017). Thus, the main reason behind difference in cost of two methods is the basis or

the base applied for allocation of expenses. It is recommended that company should adopt

activity based costing as it leads to ascertainment and allocation of cost on the basis of specific

overhead activity. Thus, the same bifurcates the cost more appropriately.

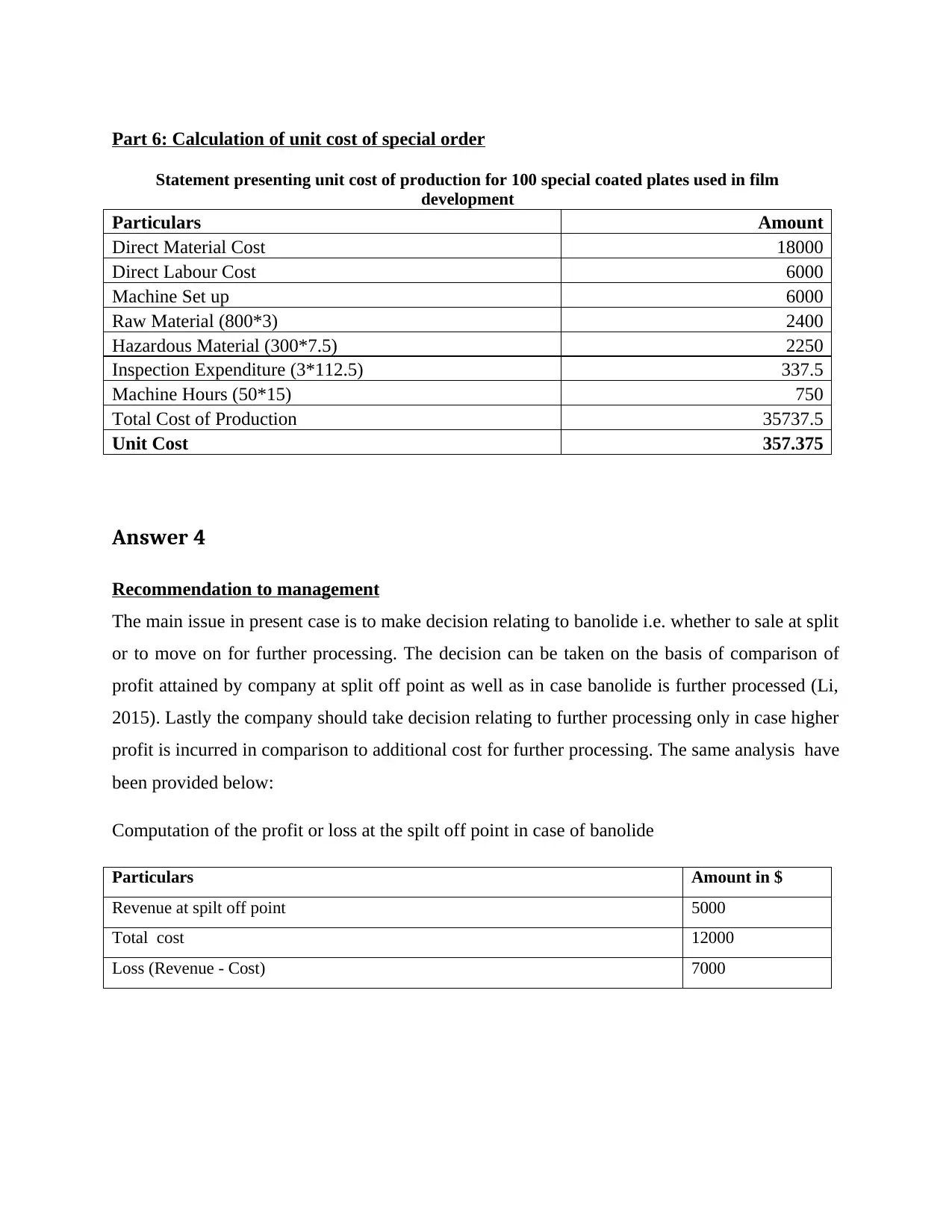

Part 6: Calculation of unit cost of special order

Statement presenting unit cost of production for 100 special coated plates used in film

development

Particulars Amount

Direct Material Cost 18000

Direct Labour Cost 6000

Machine Set up 6000

Raw Material (800*3) 2400

Hazardous Material (300*7.5) 2250

Inspection Expenditure (3*112.5) 337.5

Machine Hours (50*15) 750

Total Cost of Production 35737.5

Unit Cost 357.375

Answer 4

Recommendation to management

The main issue in present case is to make decision relating to banolide i.e. whether to sale at split

or to move on for further processing. The decision can be taken on the basis of comparison of

profit attained by company at split off point as well as in case banolide is further processed (Li,

2015). Lastly the company should take decision relating to further processing only in case higher

profit is incurred in comparison to additional cost for further processing. The same analysis have

been provided below:

Computation of the profit or loss at the spilt off point in case of banolide

Particulars Amount in $

Revenue at spilt off point 5000

Total cost 12000

Loss (Revenue - Cost) 7000

Statement presenting unit cost of production for 100 special coated plates used in film

development

Particulars Amount

Direct Material Cost 18000

Direct Labour Cost 6000

Machine Set up 6000

Raw Material (800*3) 2400

Hazardous Material (300*7.5) 2250

Inspection Expenditure (3*112.5) 337.5

Machine Hours (50*15) 750

Total Cost of Production 35737.5

Unit Cost 357.375

Answer 4

Recommendation to management

The main issue in present case is to make decision relating to banolide i.e. whether to sale at split

or to move on for further processing. The decision can be taken on the basis of comparison of

profit attained by company at split off point as well as in case banolide is further processed (Li,

2015). Lastly the company should take decision relating to further processing only in case higher

profit is incurred in comparison to additional cost for further processing. The same analysis have

been provided below:

Computation of the profit or loss at the spilt off point in case of banolide

Particulars Amount in $

Revenue at spilt off point 5000

Total cost 12000

Loss (Revenue - Cost) 7000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

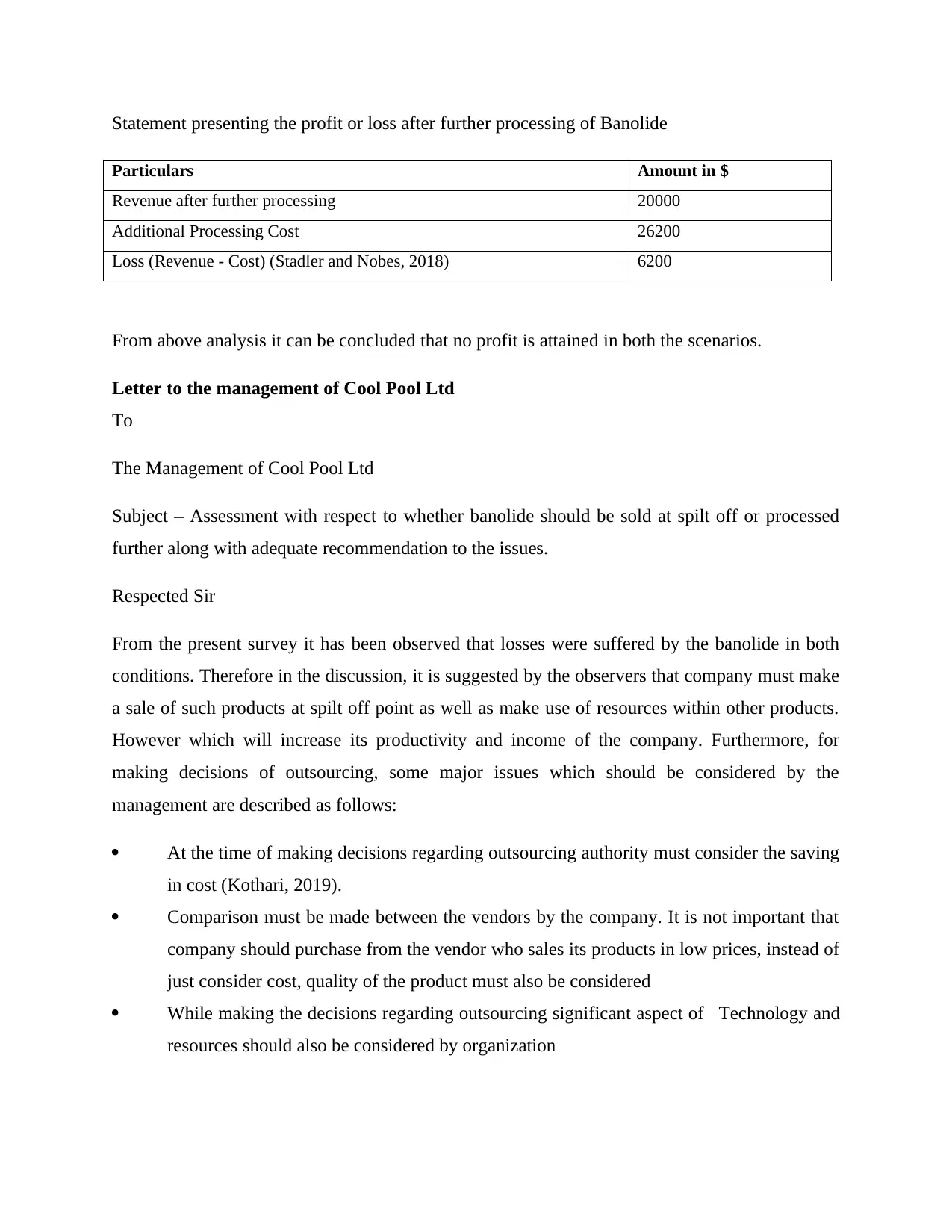

Statement presenting the profit or loss after further processing of Banolide

Particulars Amount in $

Revenue after further processing 20000

Additional Processing Cost 26200

Loss (Revenue - Cost) (Stadler and Nobes, 2018) 6200

From above analysis it can be concluded that no profit is attained in both the scenarios.

Letter to the management of Cool Pool Ltd

To

The Management of Cool Pool Ltd

Subject – Assessment with respect to whether banolide should be sold at spilt off or processed

further along with adequate recommendation to the issues.

Respected Sir

From the present survey it has been observed that losses were suffered by the banolide in both

conditions. Therefore in the discussion, it is suggested by the observers that company must make

a sale of such products at spilt off point as well as make use of resources within other products.

However which will increase its productivity and income of the company. Furthermore, for

making decisions of outsourcing, some major issues which should be considered by the

management are described as follows:

At the time of making decisions regarding outsourcing authority must consider the saving

in cost (Kothari, 2019).

Comparison must be made between the vendors by the company. It is not important that

company should purchase from the vendor who sales its products in low prices, instead of

just consider cost, quality of the product must also be considered

While making the decisions regarding outsourcing significant aspect of Technology and

resources should also be considered by organization

Particulars Amount in $

Revenue after further processing 20000

Additional Processing Cost 26200

Loss (Revenue - Cost) (Stadler and Nobes, 2018) 6200

From above analysis it can be concluded that no profit is attained in both the scenarios.

Letter to the management of Cool Pool Ltd

To

The Management of Cool Pool Ltd

Subject – Assessment with respect to whether banolide should be sold at spilt off or processed

further along with adequate recommendation to the issues.

Respected Sir

From the present survey it has been observed that losses were suffered by the banolide in both

conditions. Therefore in the discussion, it is suggested by the observers that company must make

a sale of such products at spilt off point as well as make use of resources within other products.

However which will increase its productivity and income of the company. Furthermore, for

making decisions of outsourcing, some major issues which should be considered by the

management are described as follows:

At the time of making decisions regarding outsourcing authority must consider the saving

in cost (Kothari, 2019).

Comparison must be made between the vendors by the company. It is not important that

company should purchase from the vendor who sales its products in low prices, instead of

just consider cost, quality of the product must also be considered

While making the decisions regarding outsourcing significant aspect of Technology and

resources should also be considered by organization

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

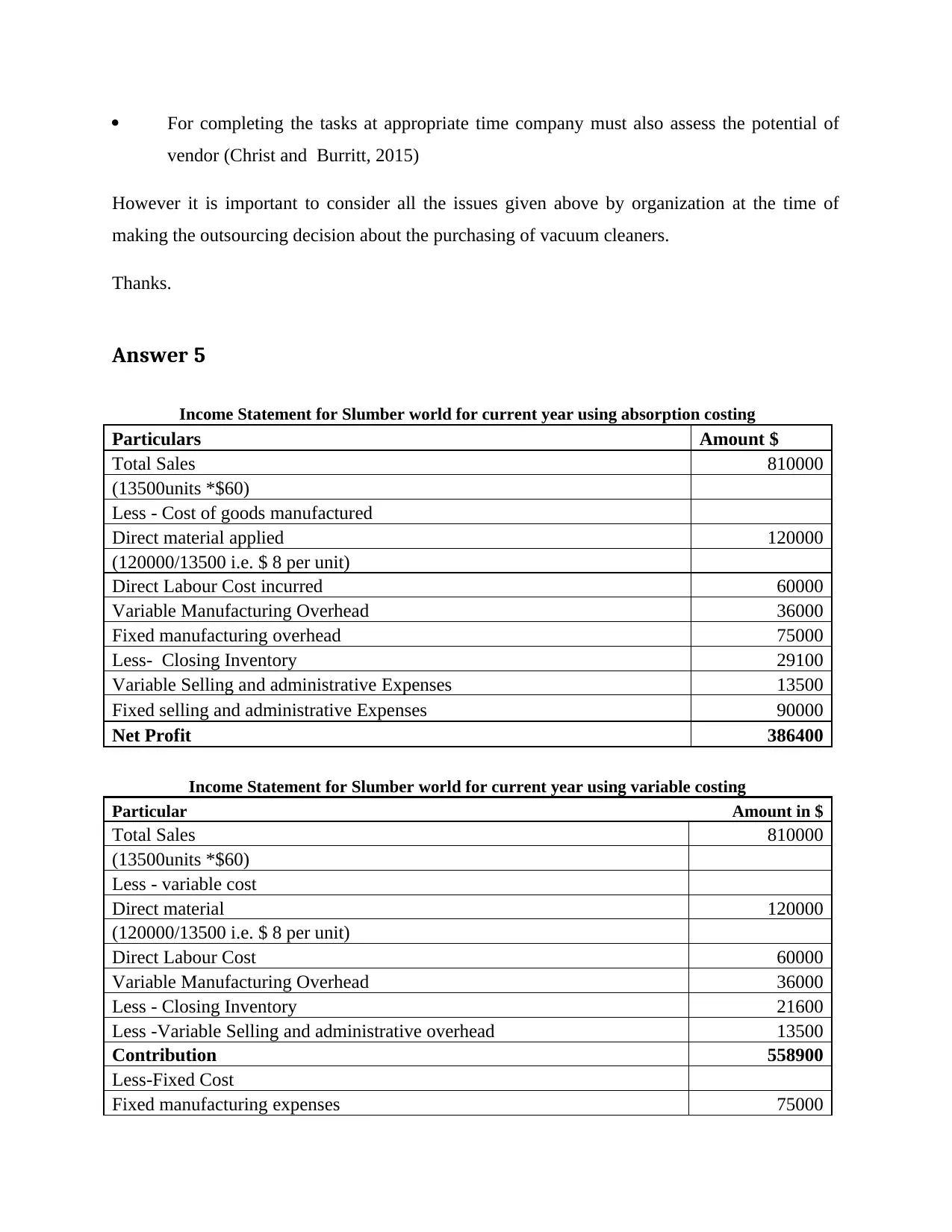

For completing the tasks at appropriate time company must also assess the potential of

vendor (Christ and Burritt, 2015)

However it is important to consider all the issues given above by organization at the time of

making the outsourcing decision about the purchasing of vacuum cleaners.

Thanks.

Answer 5

Income Statement for Slumber world for current year using absorption costing

Particulars Amount $

Total Sales 810000

(13500units *$60)

Less - Cost of goods manufactured

Direct material applied 120000

(120000/13500 i.e. $ 8 per unit)

Direct Labour Cost incurred 60000

Variable Manufacturing Overhead 36000

Fixed manufacturing overhead 75000

Less- Closing Inventory 29100

Variable Selling and administrative Expenses 13500

Fixed selling and administrative Expenses 90000

Net Profit 386400

Income Statement for Slumber world for current year using variable costing

Particular Amount in $

Total Sales 810000

(13500units *$60)

Less - variable cost

Direct material 120000

(120000/13500 i.e. $ 8 per unit)

Direct Labour Cost 60000

Variable Manufacturing Overhead 36000

Less - Closing Inventory 21600

Less -Variable Selling and administrative overhead 13500

Contribution 558900

Less-Fixed Cost

Fixed manufacturing expenses 75000

vendor (Christ and Burritt, 2015)

However it is important to consider all the issues given above by organization at the time of

making the outsourcing decision about the purchasing of vacuum cleaners.

Thanks.

Answer 5

Income Statement for Slumber world for current year using absorption costing

Particulars Amount $

Total Sales 810000

(13500units *$60)

Less - Cost of goods manufactured

Direct material applied 120000

(120000/13500 i.e. $ 8 per unit)

Direct Labour Cost incurred 60000

Variable Manufacturing Overhead 36000

Fixed manufacturing overhead 75000

Less- Closing Inventory 29100

Variable Selling and administrative Expenses 13500

Fixed selling and administrative Expenses 90000

Net Profit 386400

Income Statement for Slumber world for current year using variable costing

Particular Amount in $

Total Sales 810000

(13500units *$60)

Less - variable cost

Direct material 120000

(120000/13500 i.e. $ 8 per unit)

Direct Labour Cost 60000

Variable Manufacturing Overhead 36000

Less - Closing Inventory 21600

Less -Variable Selling and administrative overhead 13500

Contribution 558900

Less-Fixed Cost

Fixed manufacturing expenses 75000

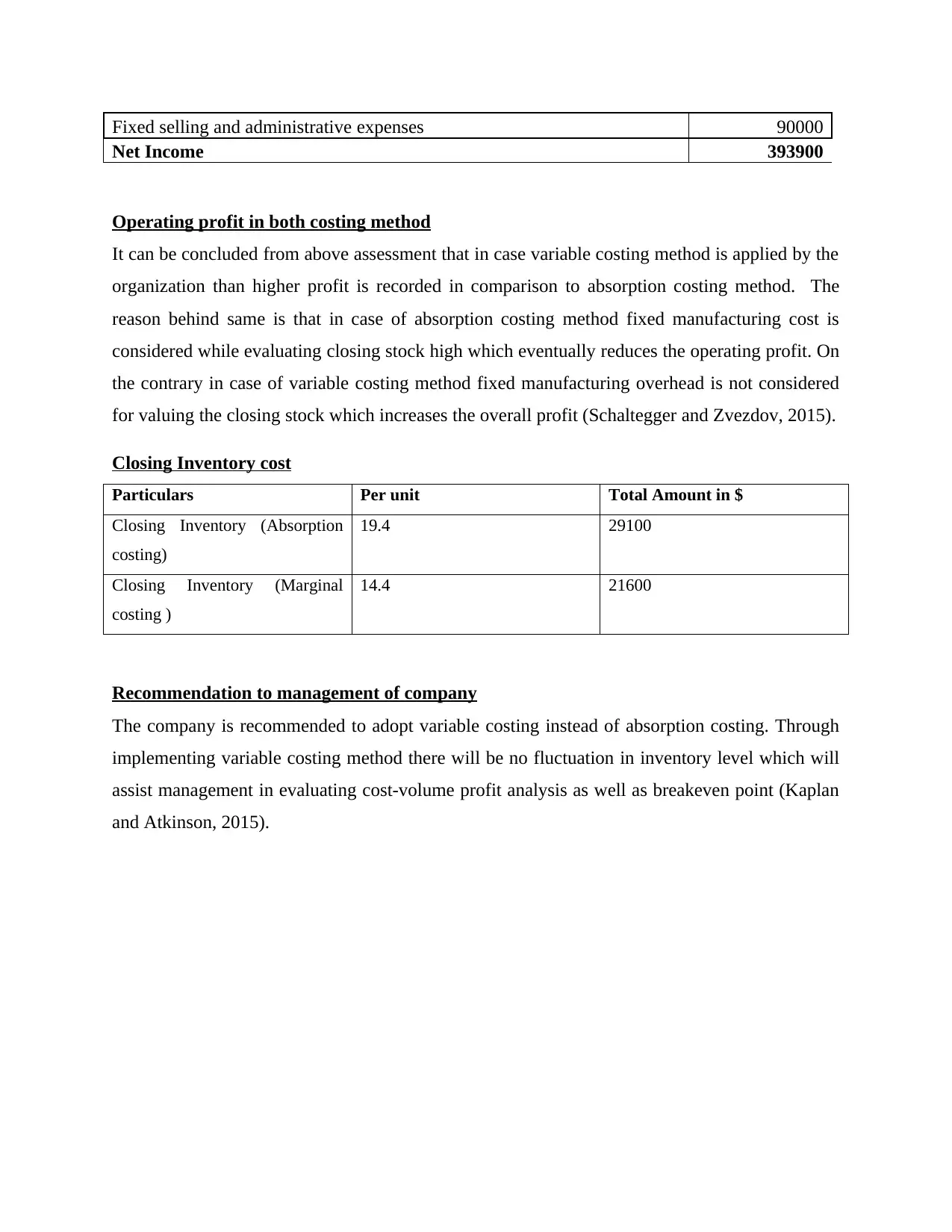

Fixed selling and administrative expenses 90000

Net Income 393900

Operating profit in both costing method

It can be concluded from above assessment that in case variable costing method is applied by the

organization than higher profit is recorded in comparison to absorption costing method. The

reason behind same is that in case of absorption costing method fixed manufacturing cost is

considered while evaluating closing stock high which eventually reduces the operating profit. On

the contrary in case of variable costing method fixed manufacturing overhead is not considered

for valuing the closing stock which increases the overall profit (Schaltegger and Zvezdov, 2015).

Closing Inventory cost

Particulars Per unit Total Amount in $

Closing Inventory (Absorption

costing)

19.4 29100

Closing Inventory (Marginal

costing )

14.4 21600

Recommendation to management of company

The company is recommended to adopt variable costing instead of absorption costing. Through

implementing variable costing method there will be no fluctuation in inventory level which will

assist management in evaluating cost-volume profit analysis as well as breakeven point (Kaplan

and Atkinson, 2015).

Net Income 393900

Operating profit in both costing method

It can be concluded from above assessment that in case variable costing method is applied by the

organization than higher profit is recorded in comparison to absorption costing method. The

reason behind same is that in case of absorption costing method fixed manufacturing cost is

considered while evaluating closing stock high which eventually reduces the operating profit. On

the contrary in case of variable costing method fixed manufacturing overhead is not considered

for valuing the closing stock which increases the overall profit (Schaltegger and Zvezdov, 2015).

Closing Inventory cost

Particulars Per unit Total Amount in $

Closing Inventory (Absorption

costing)

19.4 29100

Closing Inventory (Marginal

costing )

14.4 21600

Recommendation to management of company

The company is recommended to adopt variable costing instead of absorption costing. Through

implementing variable costing method there will be no fluctuation in inventory level which will

assist management in evaluating cost-volume profit analysis as well as breakeven point (Kaplan

and Atkinson, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.