HDIB/2019/014 Cost and Management Accounting Assignment: Solutions

VerifiedAdded on 2020/11/30

|10

|1874

|317

Homework Assignment

AI Summary

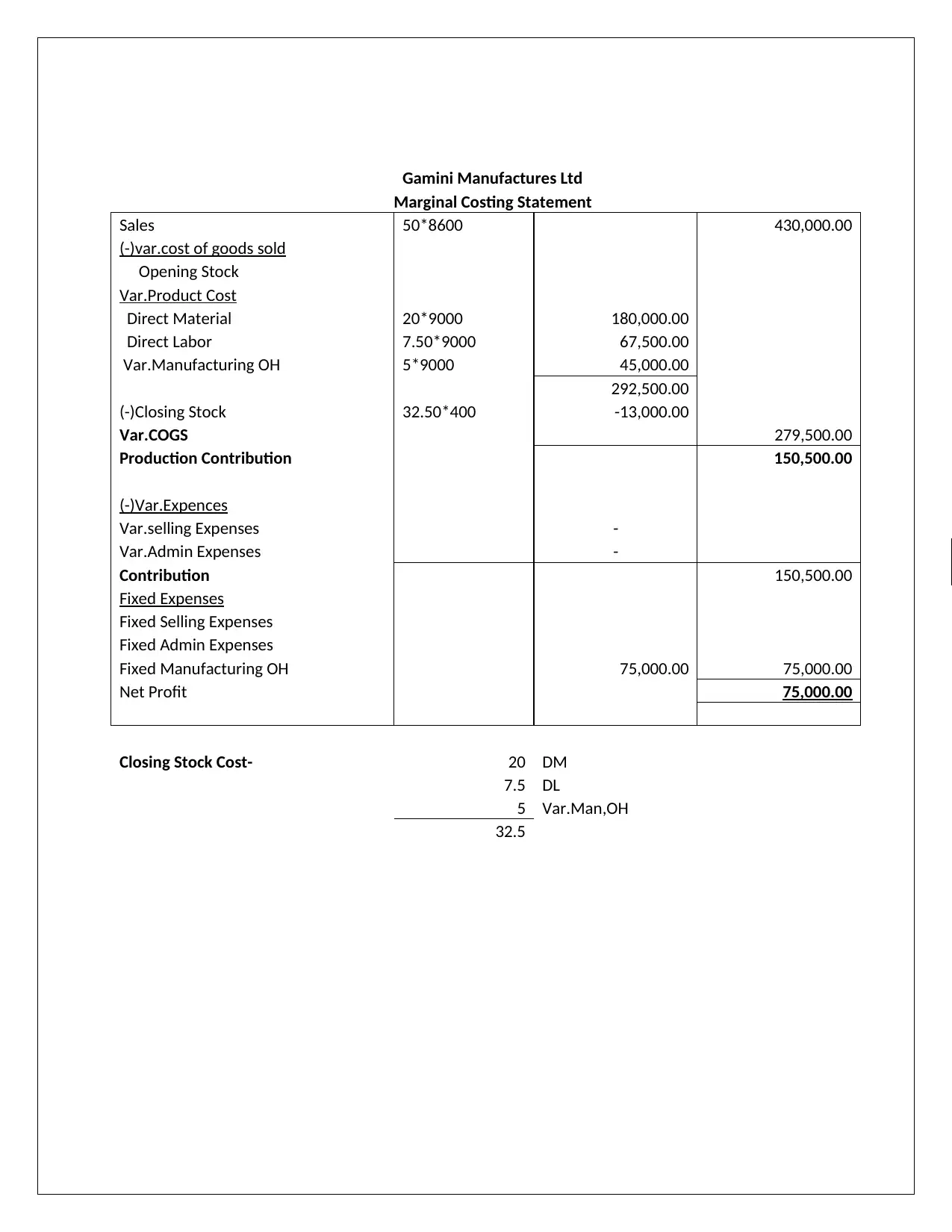

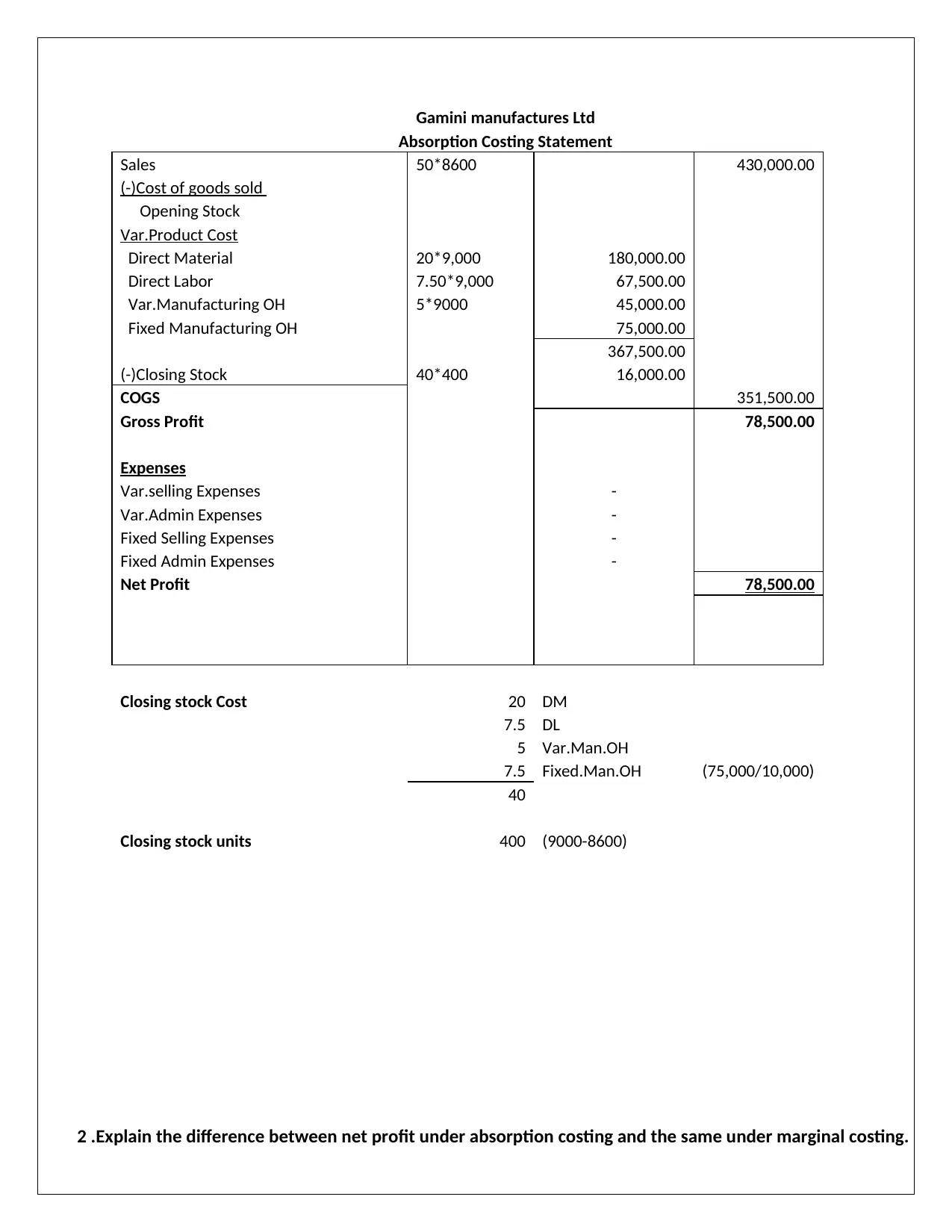

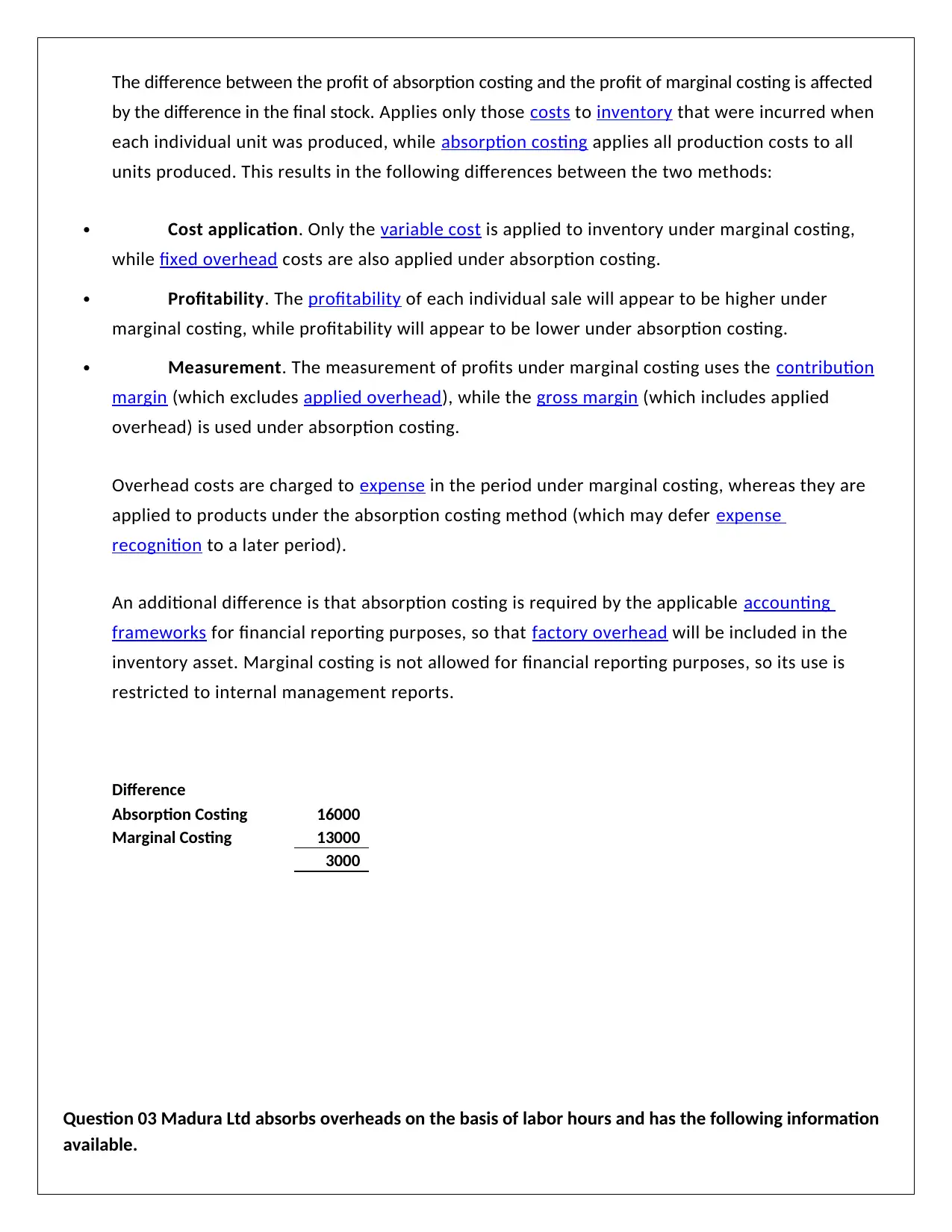

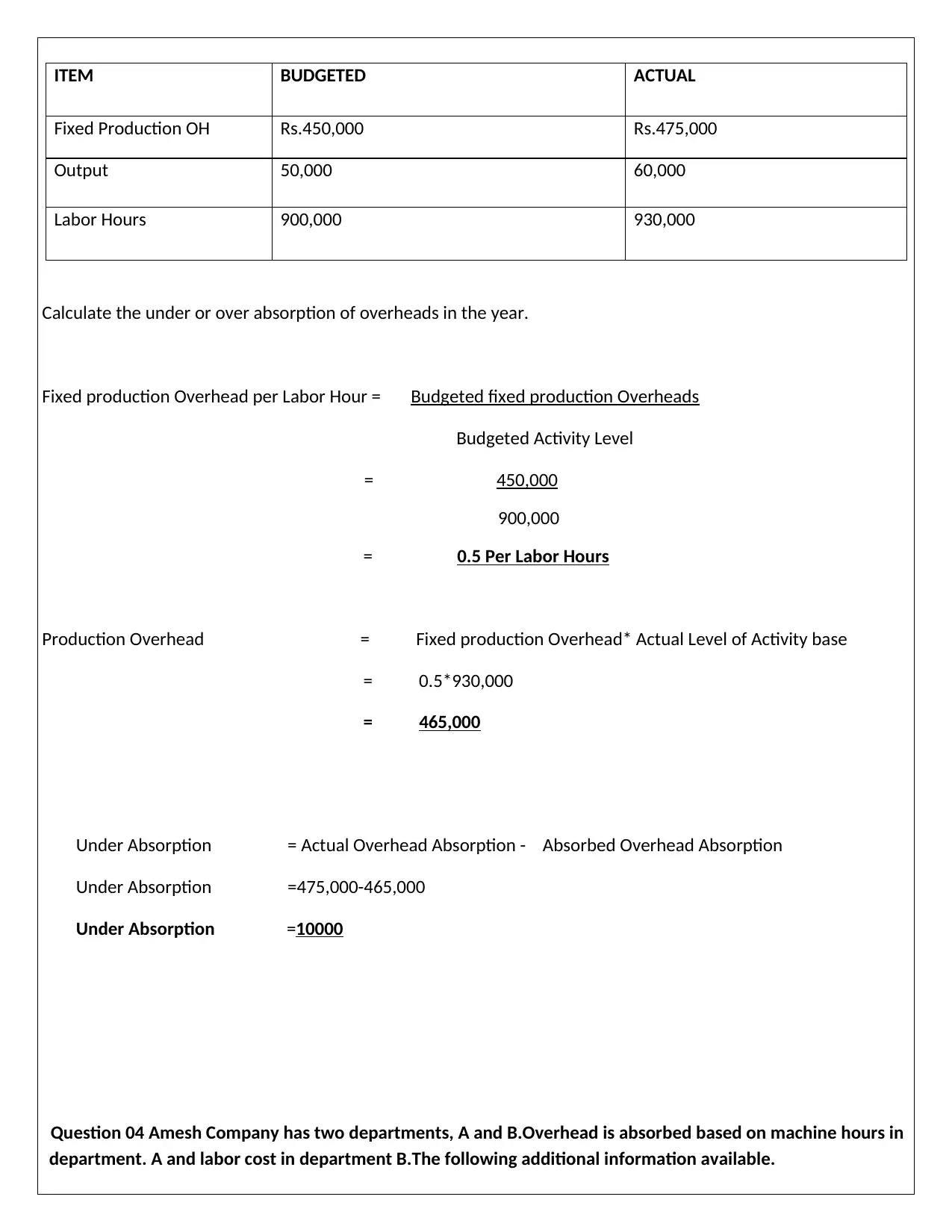

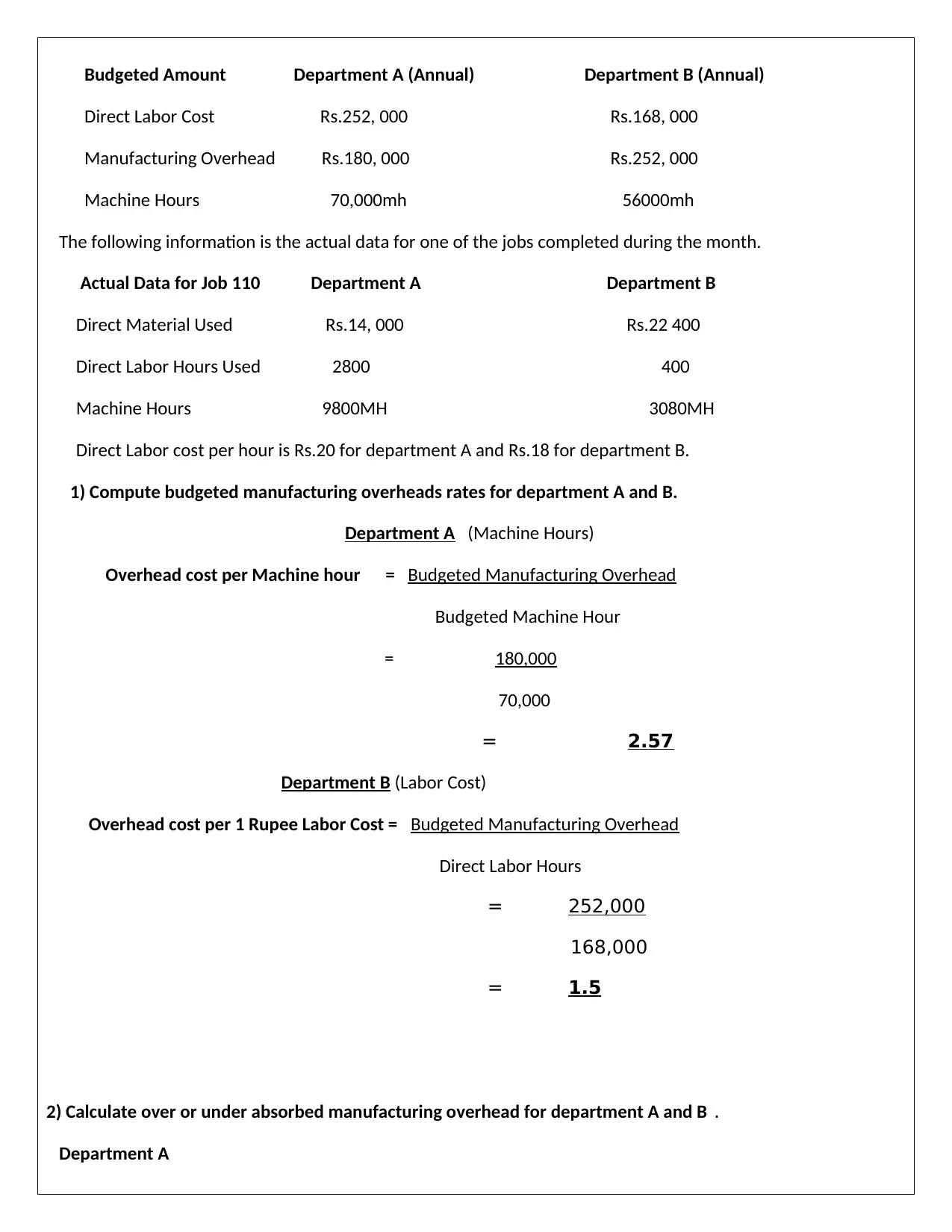

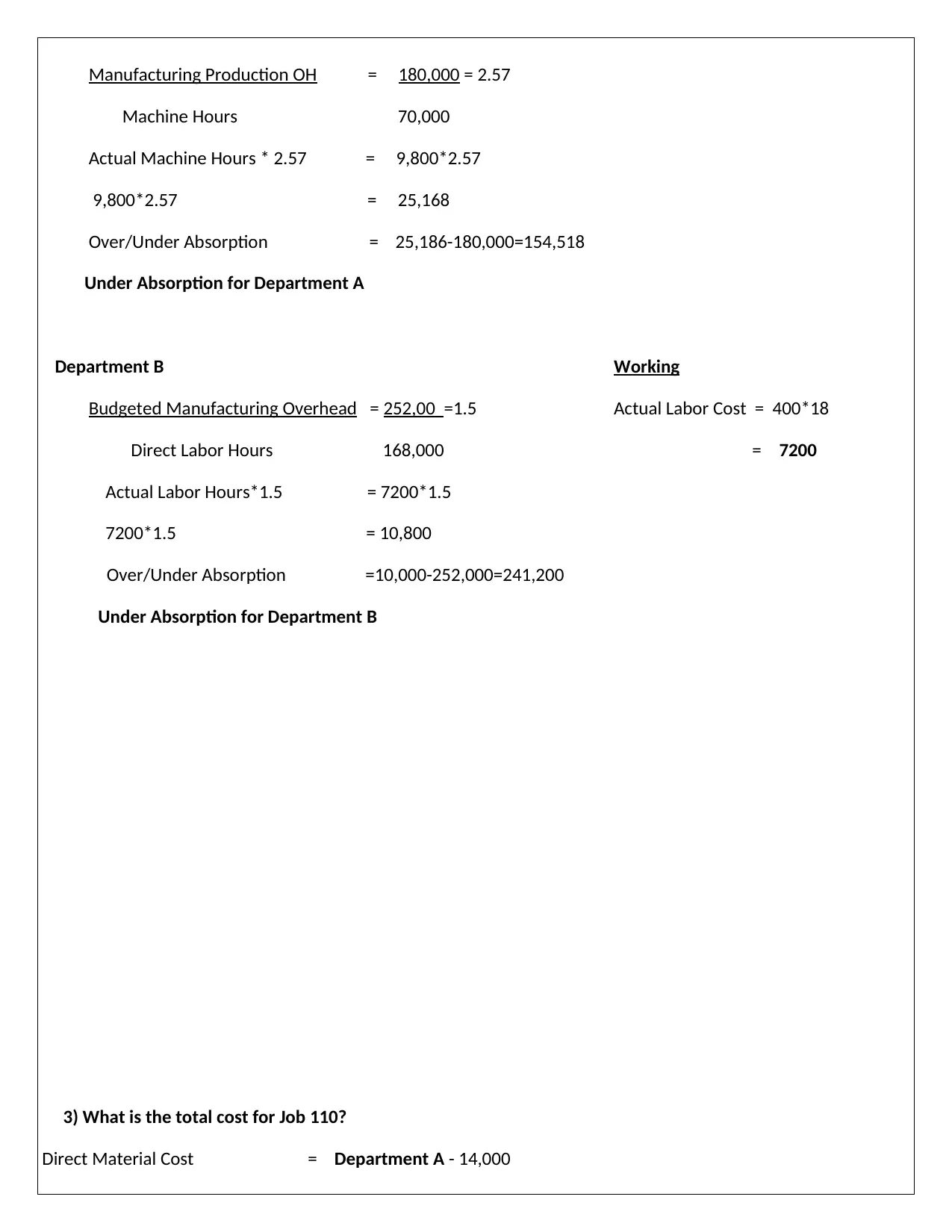

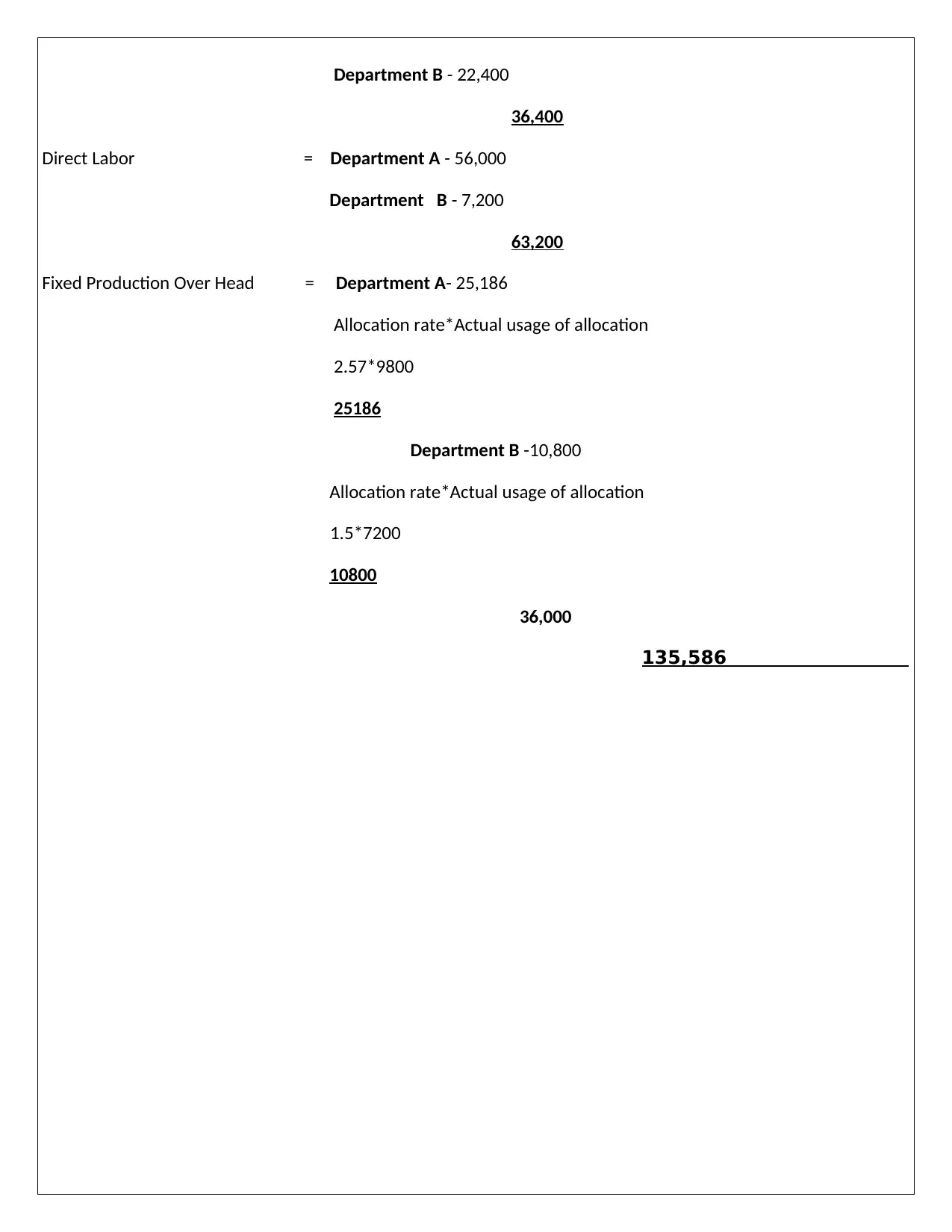

This assignment solution covers key concepts in cost and management accounting, including process costing and specific order costing, with illustrative examples. It delves into the differences between marginal and absorption costing, providing profit statements and explanations. The solution also addresses overhead absorption calculations, demonstrating how to determine under or over absorption. Furthermore, it explores overhead allocation in a multi-departmental scenario, calculating overhead rates and analyzing the total cost of a specific job. The assignment provides a comprehensive understanding of cost accounting principles, making it a valuable resource for students studying finance and accounting.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.