Cost Allocation Report: Methods, Calculations, and Analysis

VerifiedAdded on 2022/11/10

|4

|405

|67

Report

AI Summary

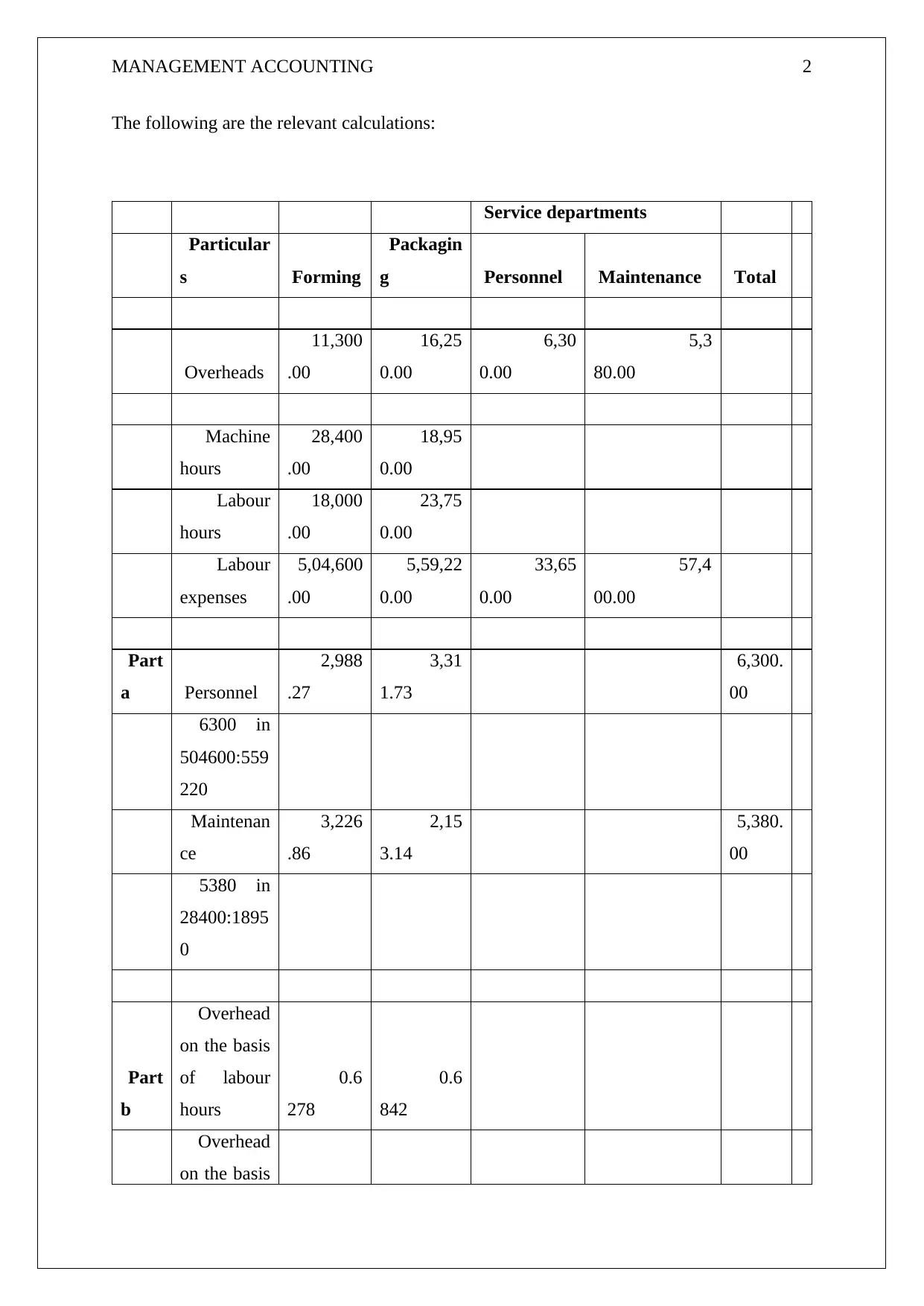

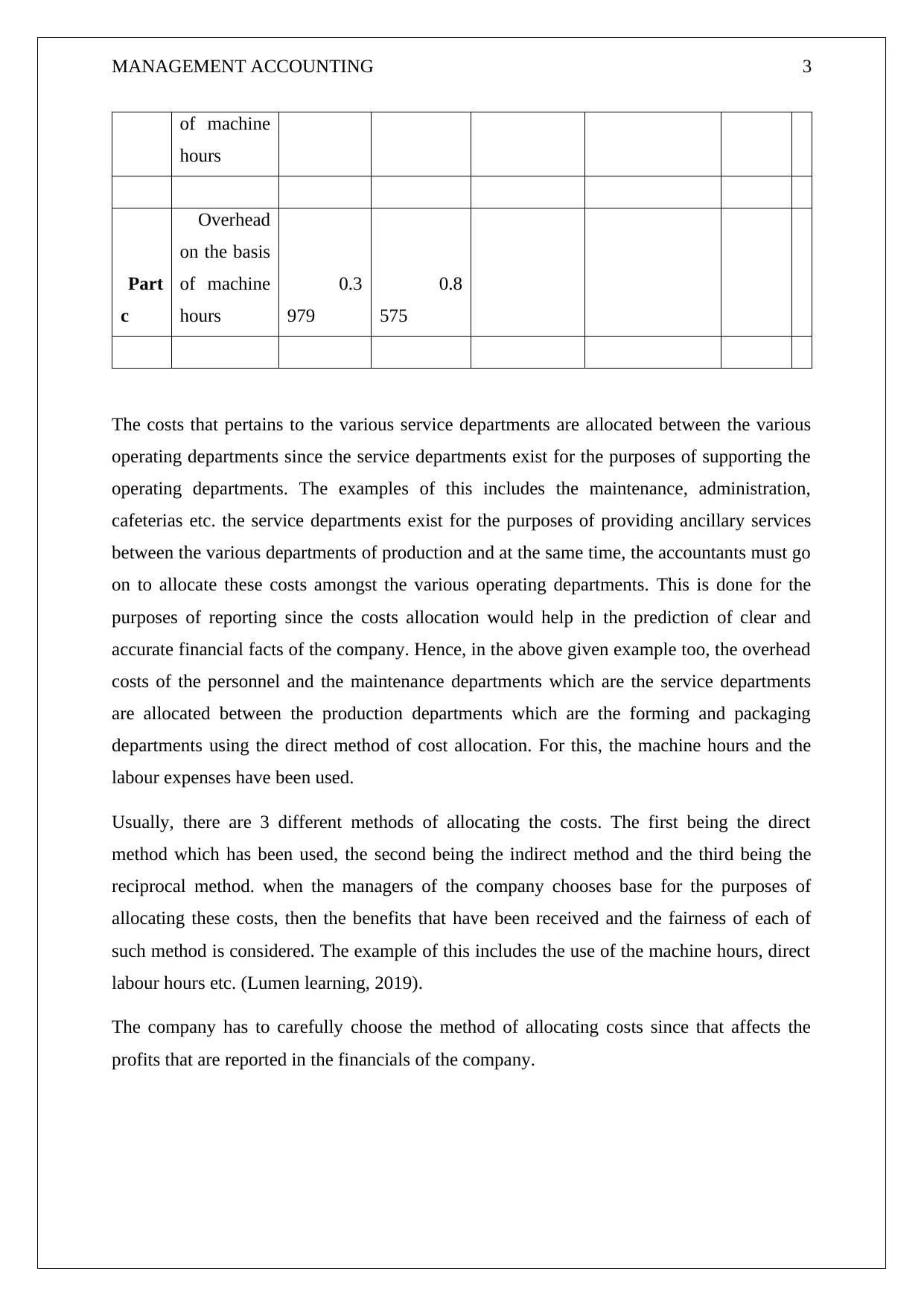

This report delves into the realm of cost allocation within management accounting, focusing on the allocation of service department costs to operating departments. The report highlights the importance of accurate cost allocation for financial reporting and provides calculations for overhead costs based on machine hours and labor expenses. The direct method of cost allocation is employed, with examples of service departments like personnel and maintenance. The report also mentions the existence of other methods, such as indirect and reciprocal methods. The choice of the allocation base, such as machine hours or direct labor hours, is crucial as it directly impacts the reported profits. The report references Lumen learning (2019) to support the concepts discussed.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.