ACC 200 Report: Cost Allocation Methods Analysis at Beztec Limited

VerifiedAdded on 2023/06/05

|15

|2829

|76

Report

AI Summary

This report provides a detailed analysis of cost allocation methods, specifically focusing on traditional costing and activity-based costing (ABC), and their impact on decision-making within an organization, using Beztec Limited as a case study. The report evaluates the importance of selecting the correct costing method, analyzes Beztec Limited's cost data, and offers recommendations to the accountant, Sue Smith, regarding the implementation of ABC. It also includes an analysis of the company's gross profit margin under both costing methods and discusses the treatment of under- or over-recovery of overhead costs. The findings reveal that the initial decision to phase out a product (Lexon) based on traditional costing was flawed and that ABC provides a more accurate representation of product profitability, highlighting the ethical responsibilities of accountants in providing unbiased financial information.

ACC 200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

A detailed analysis of cost allocation method has been carried out in this assignment. It also

states the significance of adopting correct allocation method that is suitable for the

organisation. Certain recommendations are also made at the end of the project.

A detailed analysis of cost allocation method has been carried out in this assignment. It also

states the significance of adopting correct allocation method that is suitable for the

organisation. Certain recommendations are also made at the end of the project.

Contents

Introduction................................................................................................................................4

Traditional costing system.........................................................................................................5

Activity Based Costing..............................................................................................................6

Importance of using correct costing method..............................................................................7

Analysis of cost data of Beztec limited......................................................................................8

Recommendation for Sue Smith (Accountant)........................................................................11

Analysis of gross profit margin of the company......................................................................12

Treatment of under- over recovery of overhead......................................................................13

Recommendation and Conclusion............................................................................................14

Bibliography.............................................................................................................................15

Introduction................................................................................................................................4

Traditional costing system.........................................................................................................5

Activity Based Costing..............................................................................................................6

Importance of using correct costing method..............................................................................7

Analysis of cost data of Beztec limited......................................................................................8

Recommendation for Sue Smith (Accountant)........................................................................11

Analysis of gross profit margin of the company......................................................................12

Treatment of under- over recovery of overhead......................................................................13

Recommendation and Conclusion............................................................................................14

Bibliography.............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

There are many functions that has to be performed by the management. One of the most

important functions that it has to perform is decision making. It is the responsibility of the

management to do product pricing. Product pricing is a difficult job as it requires all the

information related to cost and all the information should be correct and reliable. If the

management uses wrong or past data then it might take wrong decision which might hurt the

financial viability of the company (Atkinson, 2012).

Beztec limited is a company that is engaged in the production of printer. The name of the

printer is Lexon and Protox. The management of the company has decided to stop the

production of Lexon because it is able to generate very low returns. It is important for the

management to evaluate the reason behind this and then take decision. The accountant of the

company is of the view that this financial outcome is because of the inappropriate costing

method.

In this assignment, the two types of cost allocation methods are discussed and explained. A

proper analysis has been done of which method should be adopted and what is the reason for

it (Berry, 2009).

There are many functions that has to be performed by the management. One of the most

important functions that it has to perform is decision making. It is the responsibility of the

management to do product pricing. Product pricing is a difficult job as it requires all the

information related to cost and all the information should be correct and reliable. If the

management uses wrong or past data then it might take wrong decision which might hurt the

financial viability of the company (Atkinson, 2012).

Beztec limited is a company that is engaged in the production of printer. The name of the

printer is Lexon and Protox. The management of the company has decided to stop the

production of Lexon because it is able to generate very low returns. It is important for the

management to evaluate the reason behind this and then take decision. The accountant of the

company is of the view that this financial outcome is because of the inappropriate costing

method.

In this assignment, the two types of cost allocation methods are discussed and explained. A

proper analysis has been done of which method should be adopted and what is the reason for

it (Berry, 2009).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Traditional costing system

In the traditional costing system, the management calculates a pre determined rate based on

all information and data and then this rate is allocated between the different products on the

basis of certain factor such as machine hour or labour hours. However, the joint costs are also

allocated to per unit cost.

This system of costing ignores the actual consumption of resources completely and therefore,

this system is considered to be old (Datar, 2016). This method is usually adopted by

companies that produce only a single type of product and those companies whose production

process is simplified. However, the modern costing method is adopted by companies that

produce multiple products and has a complex process of production. If the process of

production is complex then it becomes more difficult to allocate cost and so modern costing

method is preferred.

It helps to shift the burden of the cost related to overhead from one unit of production to

another. The overhead costs cannot be distributed in an equal proportion because of the

different level of consumption of resources. This leads to wrong product pricing resulting in

overpricing or under pricing of products (Easton, 2010).

The companies nowadays usually adopt modern costing method in order to overcome the

drawbacks of traditional costing system. The modern costing is known as Activity Based

costing.

In the traditional costing system, the management calculates a pre determined rate based on

all information and data and then this rate is allocated between the different products on the

basis of certain factor such as machine hour or labour hours. However, the joint costs are also

allocated to per unit cost.

This system of costing ignores the actual consumption of resources completely and therefore,

this system is considered to be old (Datar, 2016). This method is usually adopted by

companies that produce only a single type of product and those companies whose production

process is simplified. However, the modern costing method is adopted by companies that

produce multiple products and has a complex process of production. If the process of

production is complex then it becomes more difficult to allocate cost and so modern costing

method is preferred.

It helps to shift the burden of the cost related to overhead from one unit of production to

another. The overhead costs cannot be distributed in an equal proportion because of the

different level of consumption of resources. This leads to wrong product pricing resulting in

overpricing or under pricing of products (Easton, 2010).

The companies nowadays usually adopt modern costing method in order to overcome the

drawbacks of traditional costing system. The modern costing is known as Activity Based

costing.

Activity Based Costing

In order to overcome the disadvantages of the traditional costing system, the companies

nowadays have started adopting the modern costing system known as Activity Based

Costing. The management of the company has to carry out proper analysis of the data and

information available under this costing method (Elaine, 2015). The number of units

consumed and the amounts incurred in respect of these activities should be recorded. The cost

per unit of activity consumed is calculated based on the data that has been calculated.

If the unit has utilised certain function then the cost allocation should be done accordingly

and only to the extent to which the consumption has been made. This will help in pricing the

product correctly. The calculation made with the help of this approach is totally reliable.

In order to overcome the disadvantages of the traditional costing system, the companies

nowadays have started adopting the modern costing system known as Activity Based

Costing. The management of the company has to carry out proper analysis of the data and

information available under this costing method (Elaine, 2015). The number of units

consumed and the amounts incurred in respect of these activities should be recorded. The cost

per unit of activity consumed is calculated based on the data that has been calculated.

If the unit has utilised certain function then the cost allocation should be done accordingly

and only to the extent to which the consumption has been made. This will help in pricing the

product correctly. The calculation made with the help of this approach is totally reliable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Importance of using correct costing method

As we have discussed earlier, decision making is one of the most significant function of the

management of the company. A company must make correct choice for the cost allocation

method so that there are no adverse consequences in the future. In the case study provided to

us the management has decided to phase out the production of Lexon as it is not able to

generate high operating income (Fridson & Alvarez, 2012). But if proper and correct cost

allocation method is applied then the results found will be completely different. Therefore,

we can say that implementation of an appropriate costing method is very important. The

management usually takes all its decisions based on the financial data that is available with

them. It is obvious that if there is something incorrect in the data or the data provided is

misarranged then the management may take wrong decision (Girard, 2014). A wrong

decision might lead to various consequences like poor financial performance or worsening

the financial position of the company.

As we have discussed earlier, decision making is one of the most significant function of the

management of the company. A company must make correct choice for the cost allocation

method so that there are no adverse consequences in the future. In the case study provided to

us the management has decided to phase out the production of Lexon as it is not able to

generate high operating income (Fridson & Alvarez, 2012). But if proper and correct cost

allocation method is applied then the results found will be completely different. Therefore,

we can say that implementation of an appropriate costing method is very important. The

management usually takes all its decisions based on the financial data that is available with

them. It is obvious that if there is something incorrect in the data or the data provided is

misarranged then the management may take wrong decision (Girard, 2014). A wrong

decision might lead to various consequences like poor financial performance or worsening

the financial position of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

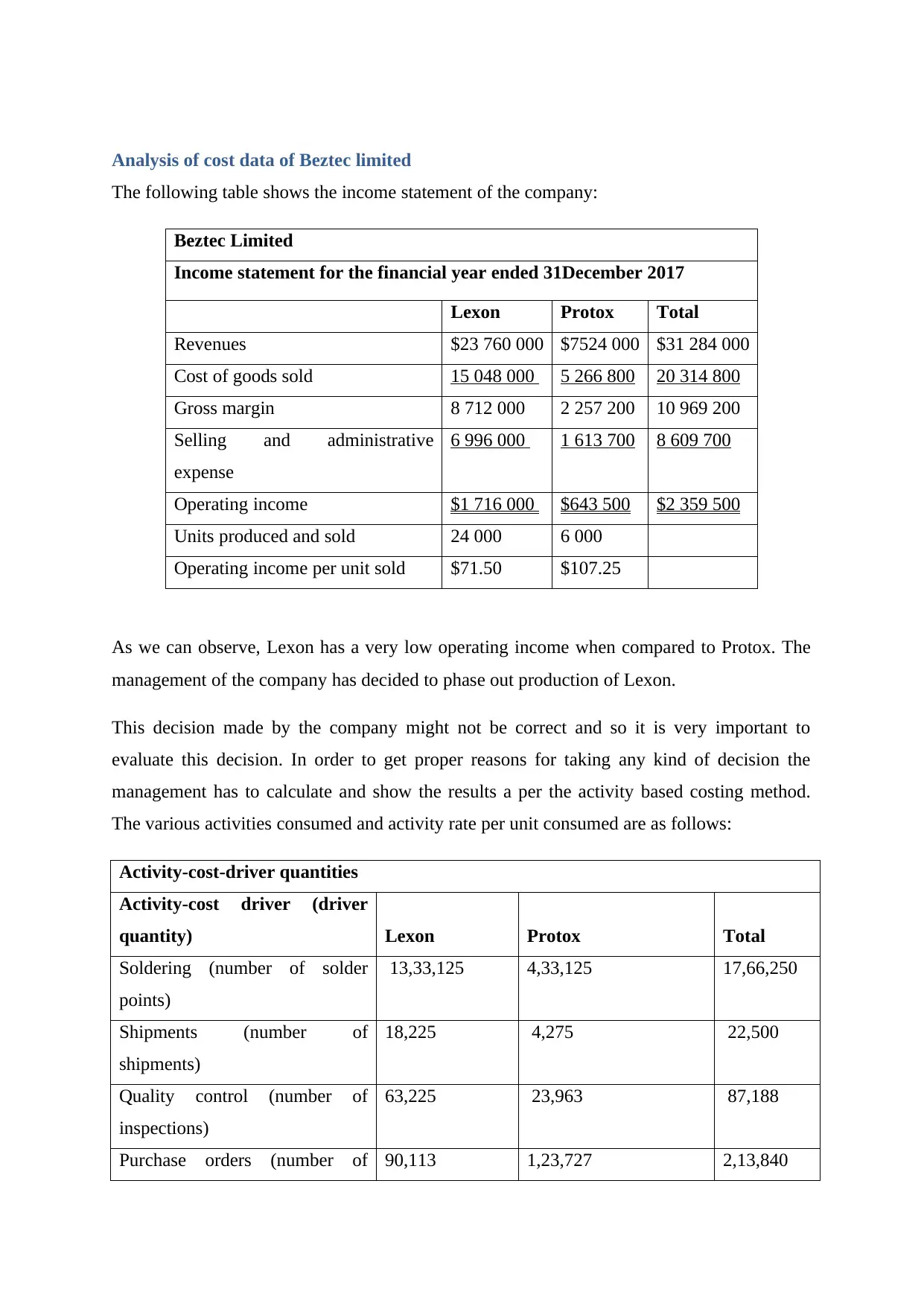

Analysis of cost data of Beztec limited

The following table shows the income statement of the company:

Beztec Limited

Income statement for the financial year ended 31December 2017

Lexon Protox Total

Revenues $23 760 000 $7524 000 $31 284 000

Cost of goods sold 15 048 000 5 266 800 20 314 800

Gross margin 8 712 000 2 257 200 10 969 200

Selling and administrative

expense

6 996 000 1 613 700 8 609 700

Operating income $1 716 000 $643 500 $2 359 500

Units produced and sold 24 000 6 000

Operating income per unit sold $71.50 $107.25

As we can observe, Lexon has a very low operating income when compared to Protox. The

management of the company has decided to phase out production of Lexon.

This decision made by the company might not be correct and so it is very important to

evaluate this decision. In order to get proper reasons for taking any kind of decision the

management has to calculate and show the results a per the activity based costing method.

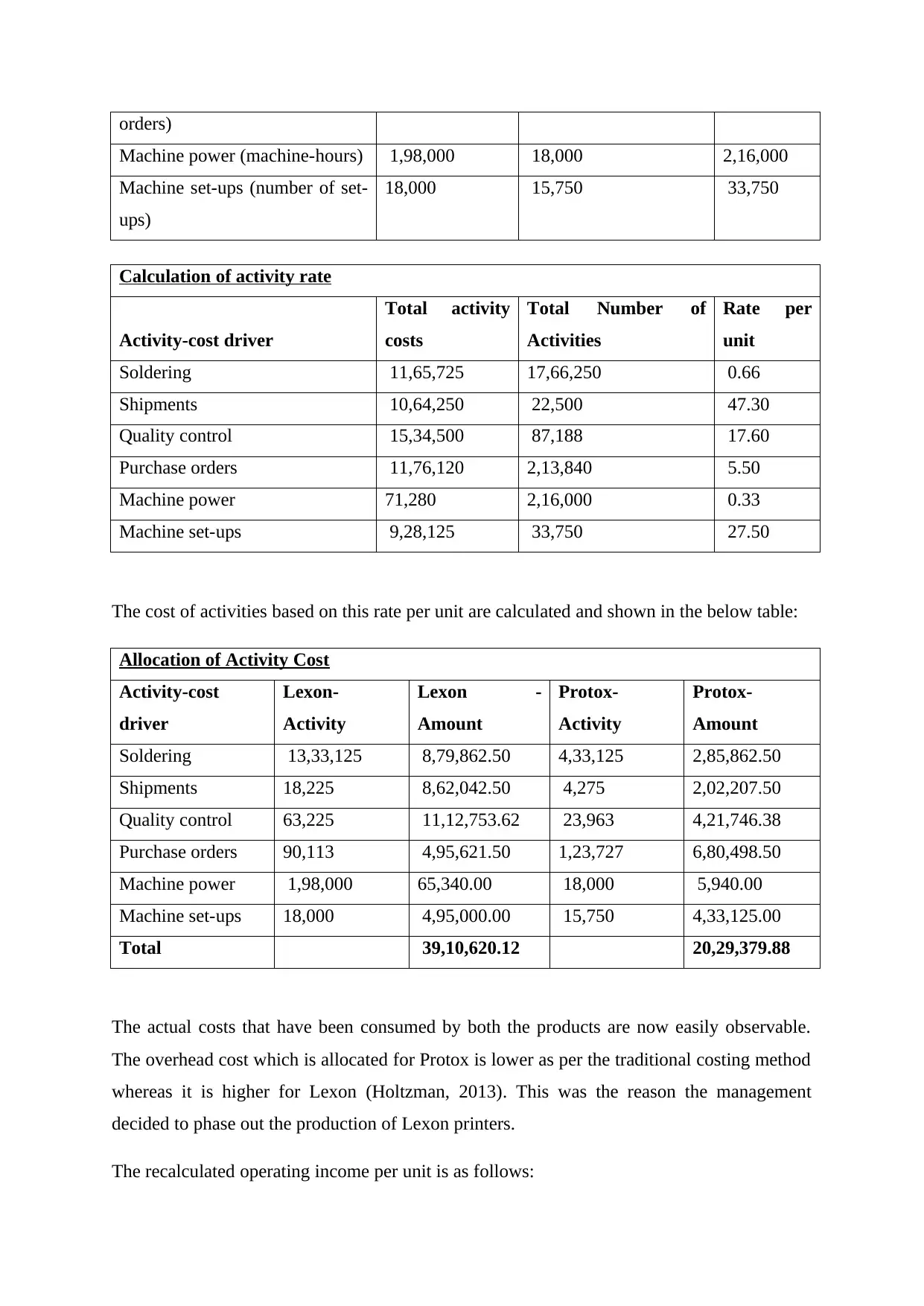

The various activities consumed and activity rate per unit consumed are as follows:

Activity-cost-driver quantities

Activity-cost driver (driver

quantity) Lexon Protox Total

Soldering (number of solder

points)

13,33,125 4,33,125 17,66,250

Shipments (number of

shipments)

18,225 4,275 22,500

Quality control (number of

inspections)

63,225 23,963 87,188

Purchase orders (number of 90,113 1,23,727 2,13,840

The following table shows the income statement of the company:

Beztec Limited

Income statement for the financial year ended 31December 2017

Lexon Protox Total

Revenues $23 760 000 $7524 000 $31 284 000

Cost of goods sold 15 048 000 5 266 800 20 314 800

Gross margin 8 712 000 2 257 200 10 969 200

Selling and administrative

expense

6 996 000 1 613 700 8 609 700

Operating income $1 716 000 $643 500 $2 359 500

Units produced and sold 24 000 6 000

Operating income per unit sold $71.50 $107.25

As we can observe, Lexon has a very low operating income when compared to Protox. The

management of the company has decided to phase out production of Lexon.

This decision made by the company might not be correct and so it is very important to

evaluate this decision. In order to get proper reasons for taking any kind of decision the

management has to calculate and show the results a per the activity based costing method.

The various activities consumed and activity rate per unit consumed are as follows:

Activity-cost-driver quantities

Activity-cost driver (driver

quantity) Lexon Protox Total

Soldering (number of solder

points)

13,33,125 4,33,125 17,66,250

Shipments (number of

shipments)

18,225 4,275 22,500

Quality control (number of

inspections)

63,225 23,963 87,188

Purchase orders (number of 90,113 1,23,727 2,13,840

orders)

Machine power (machine-hours) 1,98,000 18,000 2,16,000

Machine set-ups (number of set-

ups)

18,000 15,750 33,750

Calculation of activity rate

Activity-cost driver

Total activity

costs

Total Number of

Activities

Rate per

unit

Soldering 11,65,725 17,66,250 0.66

Shipments 10,64,250 22,500 47.30

Quality control 15,34,500 87,188 17.60

Purchase orders 11,76,120 2,13,840 5.50

Machine power 71,280 2,16,000 0.33

Machine set-ups 9,28,125 33,750 27.50

The cost of activities based on this rate per unit are calculated and shown in the below table:

Allocation of Activity Cost

Activity-cost

driver

Lexon-

Activity

Lexon -

Amount

Protox-

Activity

Protox-

Amount

Soldering 13,33,125 8,79,862.50 4,33,125 2,85,862.50

Shipments 18,225 8,62,042.50 4,275 2,02,207.50

Quality control 63,225 11,12,753.62 23,963 4,21,746.38

Purchase orders 90,113 4,95,621.50 1,23,727 6,80,498.50

Machine power 1,98,000 65,340.00 18,000 5,940.00

Machine set-ups 18,000 4,95,000.00 15,750 4,33,125.00

Total 39,10,620.12 20,29,379.88

The actual costs that have been consumed by both the products are now easily observable.

The overhead cost which is allocated for Protox is lower as per the traditional costing method

whereas it is higher for Lexon (Holtzman, 2013). This was the reason the management

decided to phase out the production of Lexon printers.

The recalculated operating income per unit is as follows:

Machine power (machine-hours) 1,98,000 18,000 2,16,000

Machine set-ups (number of set-

ups)

18,000 15,750 33,750

Calculation of activity rate

Activity-cost driver

Total activity

costs

Total Number of

Activities

Rate per

unit

Soldering 11,65,725 17,66,250 0.66

Shipments 10,64,250 22,500 47.30

Quality control 15,34,500 87,188 17.60

Purchase orders 11,76,120 2,13,840 5.50

Machine power 71,280 2,16,000 0.33

Machine set-ups 9,28,125 33,750 27.50

The cost of activities based on this rate per unit are calculated and shown in the below table:

Allocation of Activity Cost

Activity-cost

driver

Lexon-

Activity

Lexon -

Amount

Protox-

Activity

Protox-

Amount

Soldering 13,33,125 8,79,862.50 4,33,125 2,85,862.50

Shipments 18,225 8,62,042.50 4,275 2,02,207.50

Quality control 63,225 11,12,753.62 23,963 4,21,746.38

Purchase orders 90,113 4,95,621.50 1,23,727 6,80,498.50

Machine power 1,98,000 65,340.00 18,000 5,940.00

Machine set-ups 18,000 4,95,000.00 15,750 4,33,125.00

Total 39,10,620.12 20,29,379.88

The actual costs that have been consumed by both the products are now easily observable.

The overhead cost which is allocated for Protox is lower as per the traditional costing method

whereas it is higher for Lexon (Holtzman, 2013). This was the reason the management

decided to phase out the production of Lexon printers.

The recalculated operating income per unit is as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

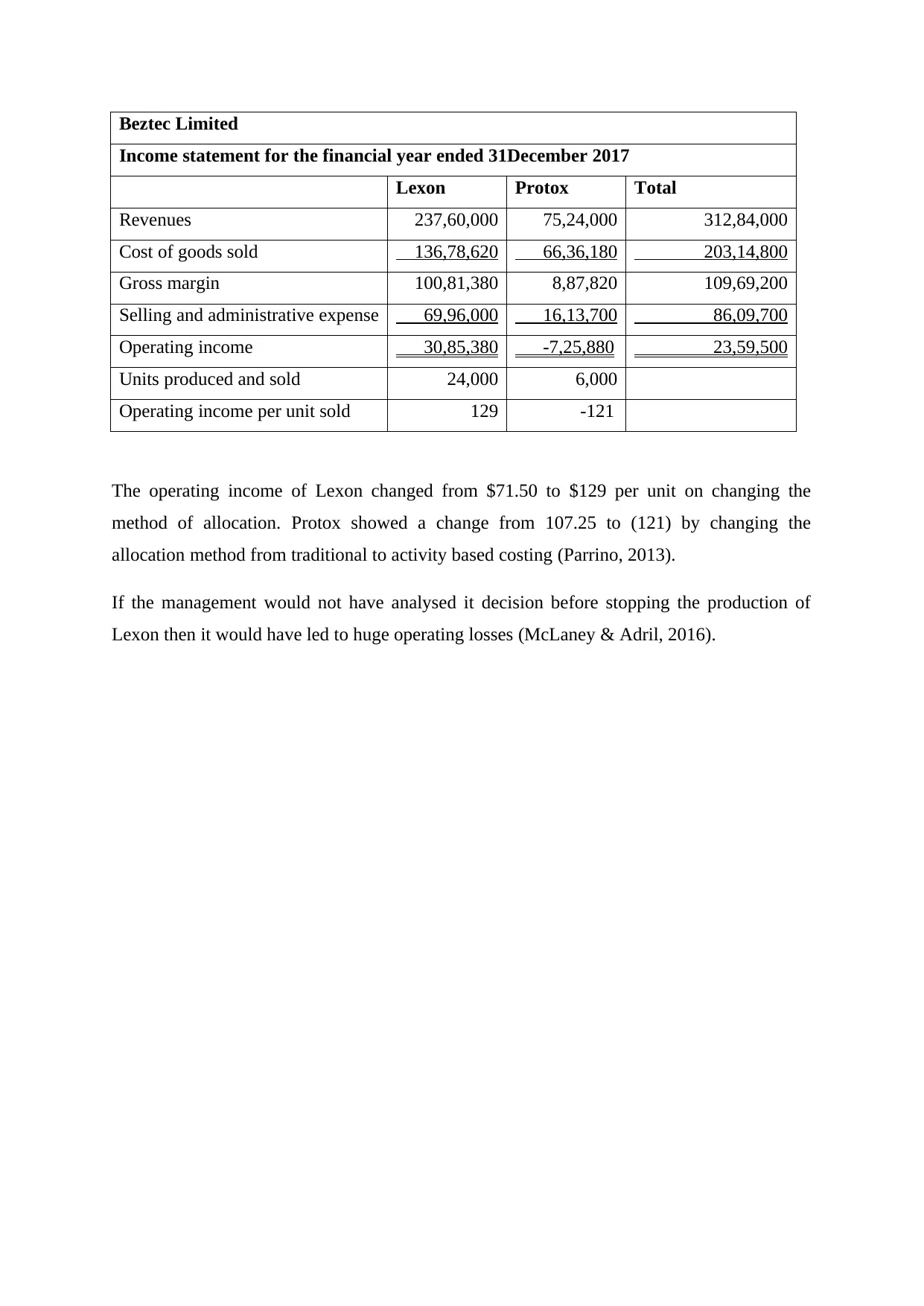

Beztec Limited

Income statement for the financial year ended 31December 2017

Lexon Protox Total

Revenues 237,60,000 75,24,000 312,84,000

Cost of goods sold 136,78,620 66,36,180 203,14,800

Gross margin 100,81,380 8,87,820 109,69,200

Selling and administrative expense 69,96,000 16,13,700 86,09,700

Operating income 30,85,380 -7,25,880 23,59,500

Units produced and sold 24,000 6,000

Operating income per unit sold 129 -121

The operating income of Lexon changed from $71.50 to $129 per unit on changing the

method of allocation. Protox showed a change from 107.25 to (121) by changing the

allocation method from traditional to activity based costing (Parrino, 2013).

If the management would not have analysed it decision before stopping the production of

Lexon then it would have led to huge operating losses (McLaney & Adril, 2016).

Income statement for the financial year ended 31December 2017

Lexon Protox Total

Revenues 237,60,000 75,24,000 312,84,000

Cost of goods sold 136,78,620 66,36,180 203,14,800

Gross margin 100,81,380 8,87,820 109,69,200

Selling and administrative expense 69,96,000 16,13,700 86,09,700

Operating income 30,85,380 -7,25,880 23,59,500

Units produced and sold 24,000 6,000

Operating income per unit sold 129 -121

The operating income of Lexon changed from $71.50 to $129 per unit on changing the

method of allocation. Protox showed a change from 107.25 to (121) by changing the

allocation method from traditional to activity based costing (Parrino, 2013).

If the management would not have analysed it decision before stopping the production of

Lexon then it would have led to huge operating losses (McLaney & Adril, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Recommendation for Sue Smith (Accountant)

Sue Smith is employed in Beztec Limited as an accountant. It is her responsibility to carry

out her responsibilities with integrity and due diligence. She should record all the data and

information in the financial reports in such a manner that it provides true and fair view about

the company’s performance and position.

On the basis of Smith’s knowledge, she advises to follow activity based costing for the

purpose of cost allocation but the CEO of the company disagrees to her because of his

personal interest (Penman, 2012). The CEO of the company wants to continue production of

both the types of printer as it would decrease the revenues of the company which will have a

direct impact on the bonus that he receives from the company. This personal benefit of the

CEO has made his opinion biased. However, it is the duty of Smith to do what is correct for

the company.

It is her responsibility to look after the financial health of the company and carry out all

activities with professionalism. She should carry out her activities independently and should

advice what is best for the company. If smith agrees to the CEO and not expresses her

opinion independently then she will be ethically wrong. So, she should calculate results based

on both the methods and then explain the CEO about the results obtained (Seal, 2012).

Sue Smith is employed in Beztec Limited as an accountant. It is her responsibility to carry

out her responsibilities with integrity and due diligence. She should record all the data and

information in the financial reports in such a manner that it provides true and fair view about

the company’s performance and position.

On the basis of Smith’s knowledge, she advises to follow activity based costing for the

purpose of cost allocation but the CEO of the company disagrees to her because of his

personal interest (Penman, 2012). The CEO of the company wants to continue production of

both the types of printer as it would decrease the revenues of the company which will have a

direct impact on the bonus that he receives from the company. This personal benefit of the

CEO has made his opinion biased. However, it is the duty of Smith to do what is correct for

the company.

It is her responsibility to look after the financial health of the company and carry out all

activities with professionalism. She should carry out her activities independently and should

advice what is best for the company. If smith agrees to the CEO and not expresses her

opinion independently then she will be ethically wrong. So, she should calculate results based

on both the methods and then explain the CEO about the results obtained (Seal, 2012).

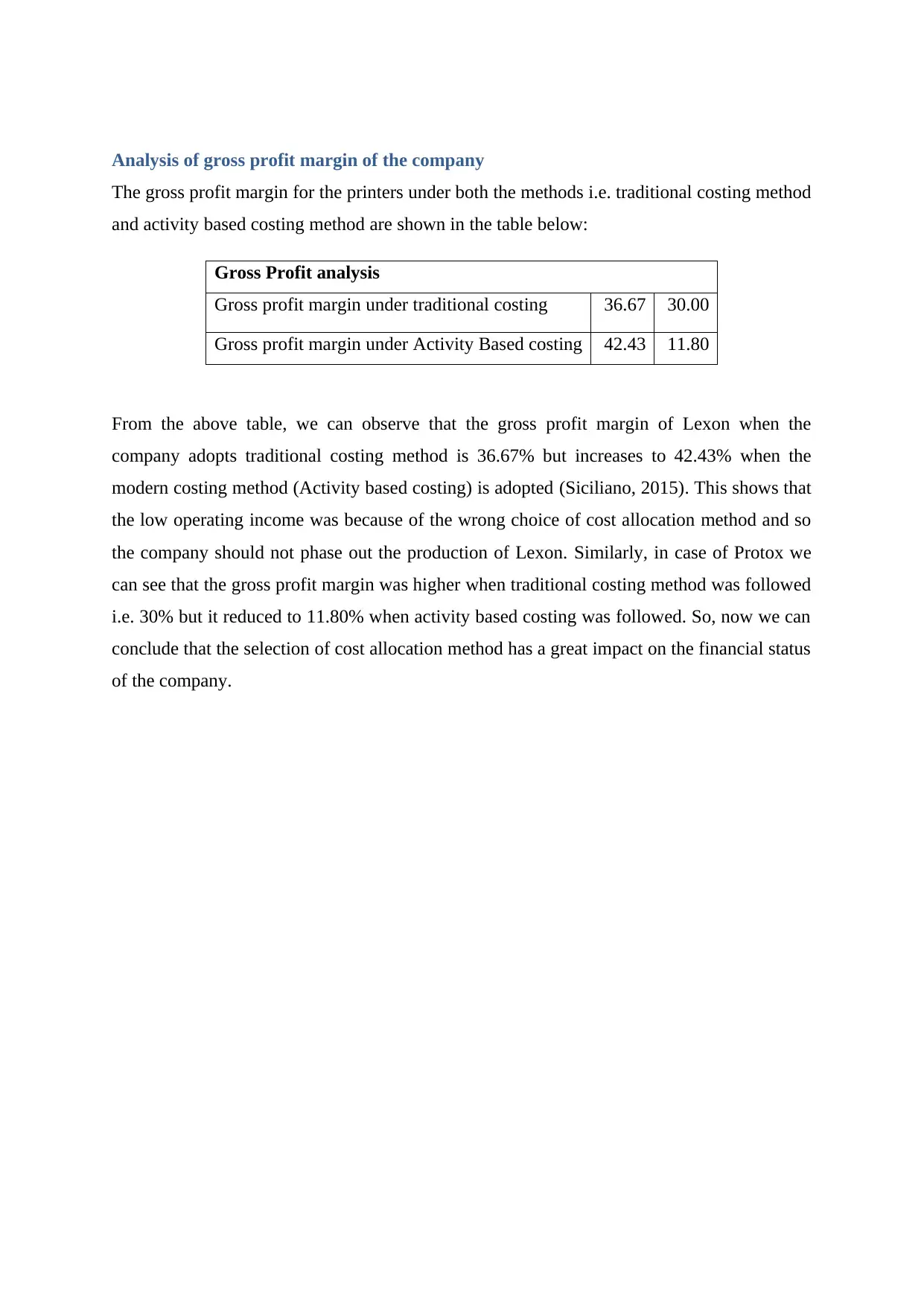

Analysis of gross profit margin of the company

The gross profit margin for the printers under both the methods i.e. traditional costing method

and activity based costing method are shown in the table below:

Gross Profit analysis

Gross profit margin under traditional costing 36.67 30.00

Gross profit margin under Activity Based costing 42.43 11.80

From the above table, we can observe that the gross profit margin of Lexon when the

company adopts traditional costing method is 36.67% but increases to 42.43% when the

modern costing method (Activity based costing) is adopted (Siciliano, 2015). This shows that

the low operating income was because of the wrong choice of cost allocation method and so

the company should not phase out the production of Lexon. Similarly, in case of Protox we

can see that the gross profit margin was higher when traditional costing method was followed

i.e. 30% but it reduced to 11.80% when activity based costing was followed. So, now we can

conclude that the selection of cost allocation method has a great impact on the financial status

of the company.

The gross profit margin for the printers under both the methods i.e. traditional costing method

and activity based costing method are shown in the table below:

Gross Profit analysis

Gross profit margin under traditional costing 36.67 30.00

Gross profit margin under Activity Based costing 42.43 11.80

From the above table, we can observe that the gross profit margin of Lexon when the

company adopts traditional costing method is 36.67% but increases to 42.43% when the

modern costing method (Activity based costing) is adopted (Siciliano, 2015). This shows that

the low operating income was because of the wrong choice of cost allocation method and so

the company should not phase out the production of Lexon. Similarly, in case of Protox we

can see that the gross profit margin was higher when traditional costing method was followed

i.e. 30% but it reduced to 11.80% when activity based costing was followed. So, now we can

conclude that the selection of cost allocation method has a great impact on the financial status

of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.