Analysis of Cost Allocation Methods and its Impact on Decision Making

VerifiedAdded on 2023/06/07

|15

|2950

|50

Report

AI Summary

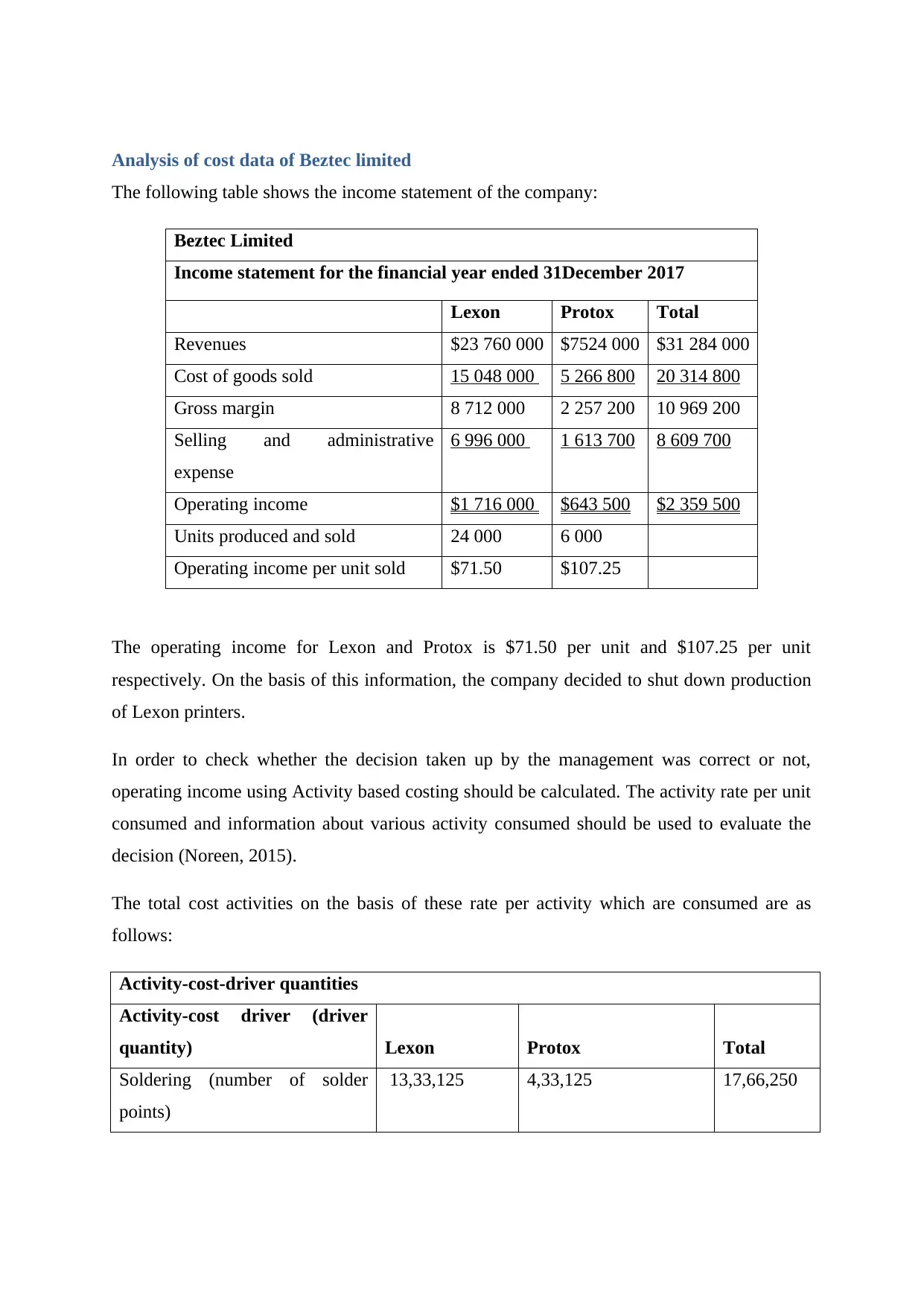

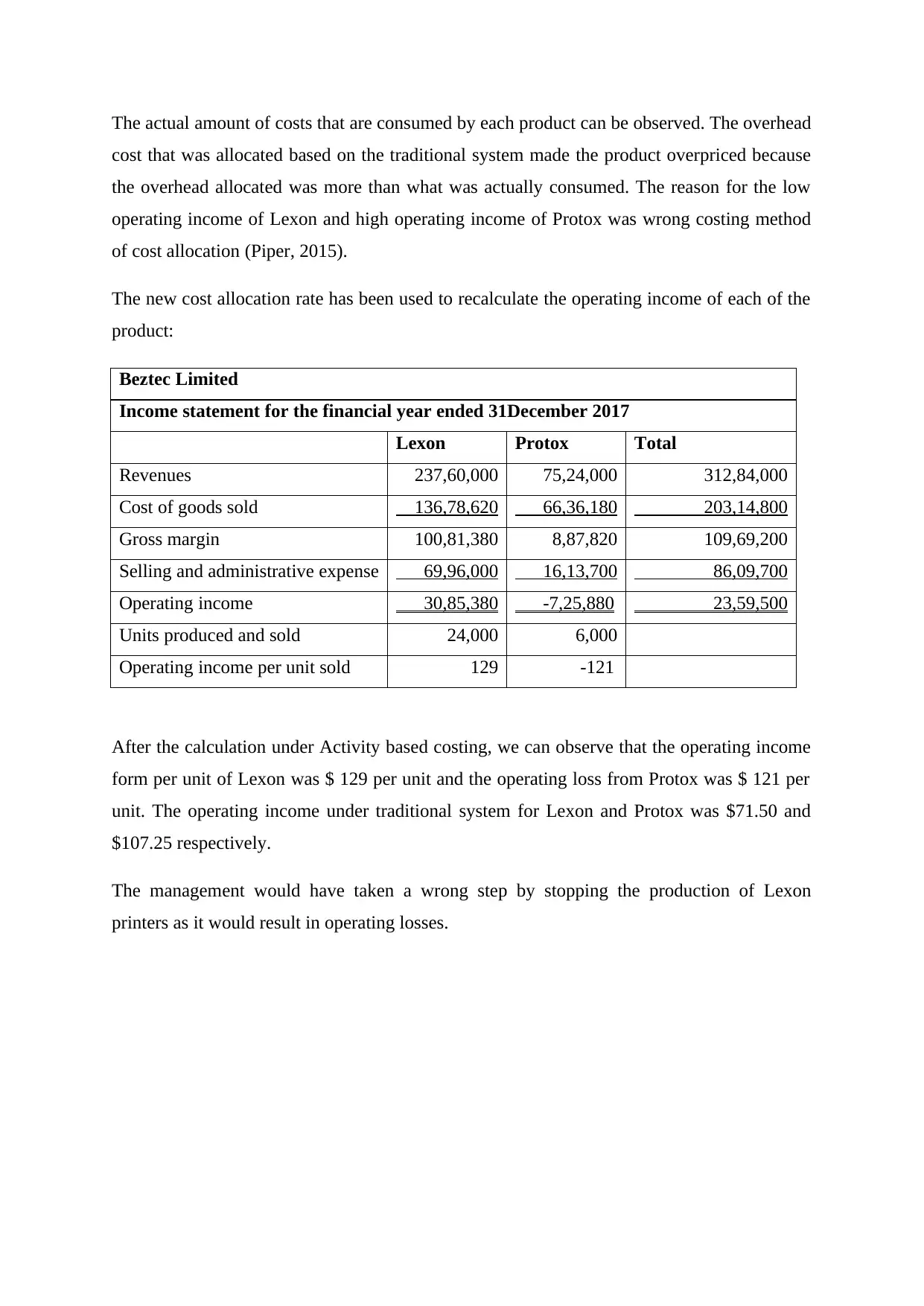

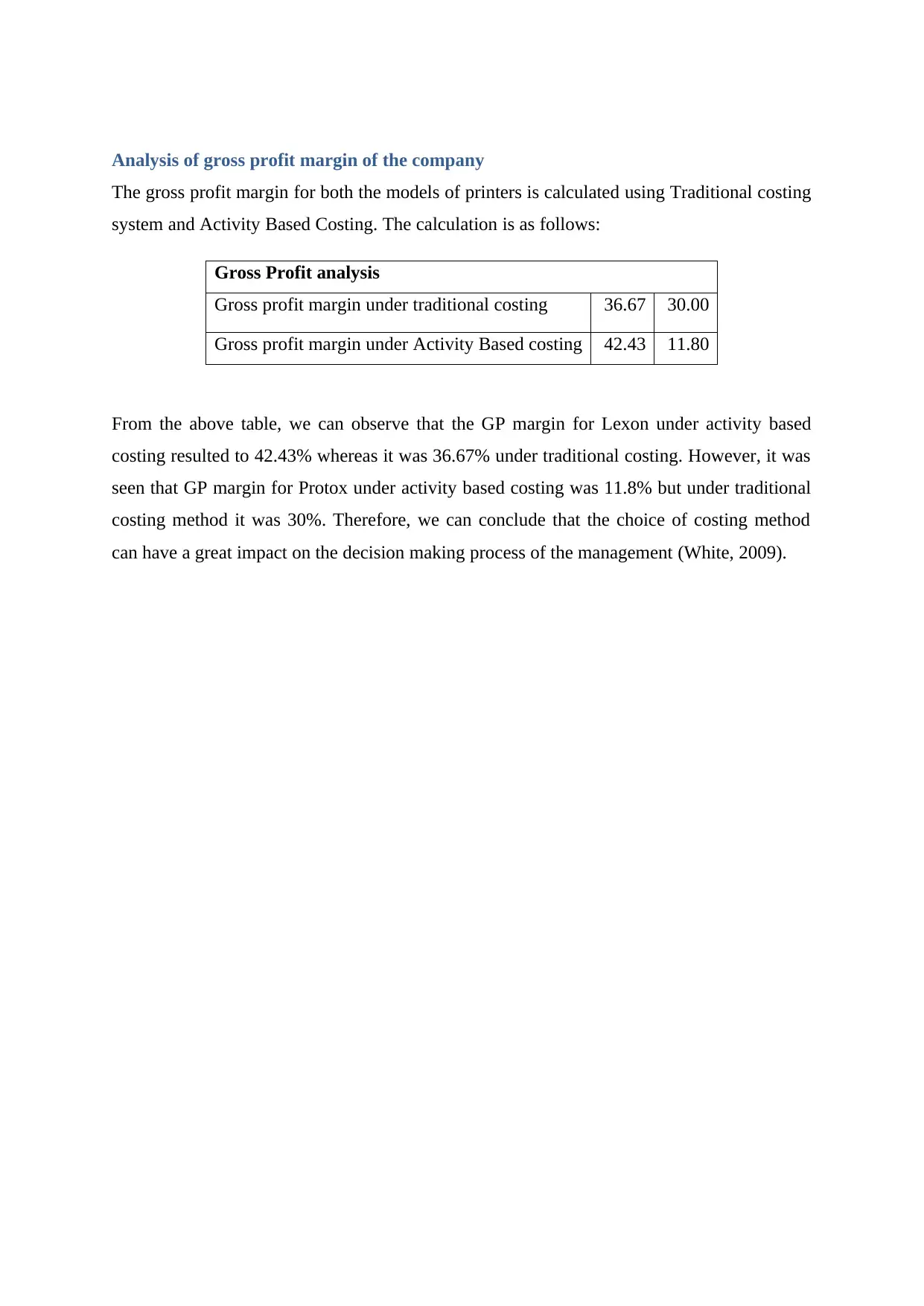

This report examines the cost allocation methods employed by Beztec Limited, focusing on the implications of traditional costing versus activity-based costing (ABC). The analysis reveals the disadvantages of traditional costing, which often leads to inaccurate product costing and potentially flawed decision-making due to the arbitrary allocation of overhead costs. The study demonstrates how ABC provides a more accurate allocation of costs, leading to a revised understanding of product profitability for Beztec's Lexon and Protox printers. The report includes a detailed income statement analysis, calculation of activity rates, and a recalculation of operating income using ABC, highlighting the importance of selecting the correct cost allocation method. Furthermore, the report addresses the ethical considerations for accountants, particularly in situations where personal interests may conflict with the company's best financial interests and the importance of maintaining financial stability. The report also analyzes the gross profit margin under both costing systems and discusses the treatment of under/over recovery of overheads, culminating in recommendations for Beztec's accountant and a final conclusion emphasizing the importance of accurate cost allocation for informed business decisions.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.