Management Accounting: Cost Analysis, Planning, and Problem Solving

VerifiedAdded on 2022/12/30

|16

|4434

|145

Report

AI Summary

This report provides a detailed analysis of management accounting principles and practices, focusing on Capital Joinery, a company specializing in gates, window frames, and wooden floors. It covers core concepts of management accounting, including cost accounting, price optimization, and inventory management systems. The report also explores various methods for management accounting reporting, such as budget reports, trade receivables aging reports, cost-accounting reports, performance reports, and inventory management reports. Furthermore, it delves into cost analysis techniques like marginal costing and absorption costing, illustrating their application with financial statements and variance analysis. The advantages and disadvantages of planning tools for budgetary control are discussed, along with a comparison of how firms adopt management accounting systems to address financial challenges. The report concludes by emphasizing the importance of management accounting in strategic decision-making and financial management.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

P1: Concept of the management accounting including core requirements of different forms of

managerial accounting systems:.............................................................................................3

P2: Multiple methods used for management accounting reporting:.......................................5

TASK 2............................................................................................................................................6

P3 Calculation of cost by using appropriate techniques in cost analysis...............................6

TASK 3..........................................................................................................................................10

P4. Advantage and disadvantage of several types of planning tools utilised for budgetary

control:..................................................................................................................................10

P5. Comparison of how firms are adopting management accounting systems to respond to

financial problems:...............................................................................................................12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

P1: Concept of the management accounting including core requirements of different forms of

managerial accounting systems:.............................................................................................3

P2: Multiple methods used for management accounting reporting:.......................................5

TASK 2............................................................................................................................................6

P3 Calculation of cost by using appropriate techniques in cost analysis...............................6

TASK 3..........................................................................................................................................10

P4. Advantage and disadvantage of several types of planning tools utilised for budgetary

control:..................................................................................................................................10

P5. Comparison of how firms are adopting management accounting systems to respond to

financial problems:...............................................................................................................12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Managerial Accounting relates to structured set of operations whereby raw facts or details

are transformed in meaningful information based on company's longer-term and short-term

targets to assists managing personnel in strategic decision makings. This framework recognises,

evaluates, interprets, modifies and demonstrates the entity's goals to corporation executives. It is

meant to better understand the specifics and making decisions reliably. Management accounting

mechanism are different from company financial accounting aspects, since they see how

knowledge is obtained mainly by internal personnel (Doktoralina and Apollo, 2019). The study-

project focuses on corporation called Capital Joinery, which manufactures a variety of gates,

window frames and wooden floors. The organization has been based majorly in the areas of West

London for about last-20 years. The study-project explores the main components of

the management accounting, its vital/substantial systems, procedures and

reporting approaches relevant for management accounting. The current report also covers

major approaches used to assess costs. Also there is review on the upsides and downsides of the

various methods of planning tools along with comparison of appropriate use/adaption

of multiple MA systems by distinct corporations to handle their fiscal challenges/issues.

TASK 1

P1: Concept of the management accounting including core requirements of different forms of

managerial accounting systems:

Management Accounting term includes the preparation of managerial records and

statements that offer reliable and effective quantitative and analytical information which are

vitally important for executives to render valuable decisions in entity. Differ from financial

accounting, which offers annual accounts, managerial accounting delivers regular financial

updates on frequent basis for audiences within the corporation, like individual departments

administrators and Chief Operating Officer. It is appropriate to introduce different sorts of

management accounting structures as they facilitate for the execution of financial actioning plan

that can assist the company in achieving its strategic objectives both effectively and continually.

They help to monitor the firm's funding and investment schedule and control the reasonable

usage of monetary resources. As a result, profit margins are dependent on the methods adopted

by the firm as well as how consistently these approaches have been implemented. In the scenario

Managerial Accounting relates to structured set of operations whereby raw facts or details

are transformed in meaningful information based on company's longer-term and short-term

targets to assists managing personnel in strategic decision makings. This framework recognises,

evaluates, interprets, modifies and demonstrates the entity's goals to corporation executives. It is

meant to better understand the specifics and making decisions reliably. Management accounting

mechanism are different from company financial accounting aspects, since they see how

knowledge is obtained mainly by internal personnel (Doktoralina and Apollo, 2019). The study-

project focuses on corporation called Capital Joinery, which manufactures a variety of gates,

window frames and wooden floors. The organization has been based majorly in the areas of West

London for about last-20 years. The study-project explores the main components of

the management accounting, its vital/substantial systems, procedures and

reporting approaches relevant for management accounting. The current report also covers

major approaches used to assess costs. Also there is review on the upsides and downsides of the

various methods of planning tools along with comparison of appropriate use/adaption

of multiple MA systems by distinct corporations to handle their fiscal challenges/issues.

TASK 1

P1: Concept of the management accounting including core requirements of different forms of

managerial accounting systems:

Management Accounting term includes the preparation of managerial records and

statements that offer reliable and effective quantitative and analytical information which are

vitally important for executives to render valuable decisions in entity. Differ from financial

accounting, which offers annual accounts, managerial accounting delivers regular financial

updates on frequent basis for audiences within the corporation, like individual departments

administrators and Chief Operating Officer. It is appropriate to introduce different sorts of

management accounting structures as they facilitate for the execution of financial actioning plan

that can assist the company in achieving its strategic objectives both effectively and continually.

They help to monitor the firm's funding and investment schedule and control the reasonable

usage of monetary resources. As a result, profit margins are dependent on the methods adopted

by the firm as well as how consistently these approaches have been implemented. In the scenario

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of Capital Joinery the multiple management accounting systems/structures to be enforced are

discussed here:

Cost-accounting system: This is a mechanism utilised by business entities to measure the costs

incurred on products and facilities they provide their all customers. This is pertinent to consider

when deciding the appropriate costs incurred for what items and assess whether there are ways

to minimize costs Corporation Capital Joinery therefore determines the amount of costs

of their products by performing an analysis and then measures the costs in way that this will

derive benefits for company and maximizes profit. They can monitor the costs of raw materials,

WIPs and final products they sell, in attempt to formulate comprehensive income reports. This is

helpful to mangers as it enables to minimize too much expenditures within business (Laela, and

et. al., 2018).

Price-optimization system: This is indeed a empirical mechanism used by businesses to evaluate

the causative link among both market-demand for the commodity/product in the marketplace and

the pricing of the products and services delivered by entity and also to estimate the suitable

prices that are attractive for the consumer as well as beneficial for entity. It is key system used

by Capital Joinery to grab more buyer segments and to keep more customers by delivering

products at most competitive rates they expect to pay. It is planned out at higher management

level of the company and should be rolled out in constructive way. These practices aid the

corporation to achieve the customer's satisfactions, which is the main requirement of any

organization.

Inventory management system: this component is adopted by firms to administer stock levels

and is vital feature of the business enterprise because the production operations of the business

enterprise depend solely on how efficiently the stocks are handled. It is framework employed by

businesses to control inventories across the value chain, from purchase of products for

production to the ultimate supply of products. In addition to conclude the production process

more efficiently, Respective company can now track the supplies in attempt to ramp up the

income of the business which will significantly impact the outputs of the enterprise (Cooper,

Ezzamel and Qu, 2017). This is important for the company to identify and include storage

records for the products to be ordered when required. There've been three types of inventory-

valuation techniques:

discussed here:

Cost-accounting system: This is a mechanism utilised by business entities to measure the costs

incurred on products and facilities they provide their all customers. This is pertinent to consider

when deciding the appropriate costs incurred for what items and assess whether there are ways

to minimize costs Corporation Capital Joinery therefore determines the amount of costs

of their products by performing an analysis and then measures the costs in way that this will

derive benefits for company and maximizes profit. They can monitor the costs of raw materials,

WIPs and final products they sell, in attempt to formulate comprehensive income reports. This is

helpful to mangers as it enables to minimize too much expenditures within business (Laela, and

et. al., 2018).

Price-optimization system: This is indeed a empirical mechanism used by businesses to evaluate

the causative link among both market-demand for the commodity/product in the marketplace and

the pricing of the products and services delivered by entity and also to estimate the suitable

prices that are attractive for the consumer as well as beneficial for entity. It is key system used

by Capital Joinery to grab more buyer segments and to keep more customers by delivering

products at most competitive rates they expect to pay. It is planned out at higher management

level of the company and should be rolled out in constructive way. These practices aid the

corporation to achieve the customer's satisfactions, which is the main requirement of any

organization.

Inventory management system: this component is adopted by firms to administer stock levels

and is vital feature of the business enterprise because the production operations of the business

enterprise depend solely on how efficiently the stocks are handled. It is framework employed by

businesses to control inventories across the value chain, from purchase of products for

production to the ultimate supply of products. In addition to conclude the production process

more efficiently, Respective company can now track the supplies in attempt to ramp up the

income of the business which will significantly impact the outputs of the enterprise (Cooper,

Ezzamel and Qu, 2017). This is important for the company to identify and include storage

records for the products to be ordered when required. There've been three types of inventory-

valuation techniques:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LIFO approach: This is method wherein assumed that latest purchased stocks are sold at first-

place.

FIFO: according to this framework, stock items are expected to be consumed under the basis the

first purchased/purchased items are issued first.

AVCO: In line with this procedure, inventory goods are measured on the basis of standard

average costs.

P2: Multiple methods used for management accounting reporting:

MA reports in business-context are perceived to be a must for any company as they help to

efficiently complete the success of the enterprise and its place on the sector. When considering

respective company, it is important for the corporation to assure that a credible accounting report

containing precise periodical analysis is formed in attempt to describe the performance of

business within competitive market. MA reports are most sometimes referred to as the financial

state of a company and helps to accurately reflect relevant details for a relevant duration

or period. Such reports could be considered to assess the financial condition of the company in

the marketplace. These also enable the potential presence of industry in data extraction by

determining the present position (Dekker, 2016). Here are major key reports that respective

corporation, as follows:

Budget report: these reports can be commonly alluded to as a primary operational report which

contains all costs and sales that may take place within a given timeline. It is important for the

managers of the company to realise that they ought to manage their spending in the enterprise.

The accompanying study aims to include information in an enterprise that can be accessed by all

divisions for decision-makings and minimize expenditures. The analysis of past spending and the

prediction of projected expenditures shall be carried out in order to draw up budgeting

reports for company. This also lets companies define their expenses efficiently and eliminates

costs at any step of the way in different business units (Pasch, 2019).

Businesses selling credit-goods on a regular basis are necessary to hold trade Receivables

Ageing Reports since they remind the corporation about defaulters/bad-debts, whether payments

could be secured, to making the repayment cycle simpler. Corporation Capital Joinery can

produce this report to keeping informed of the buyers it owing such that they receive the amounts

as per credit schedule and assure that company does not even have bad debts which are favorable

place.

FIFO: according to this framework, stock items are expected to be consumed under the basis the

first purchased/purchased items are issued first.

AVCO: In line with this procedure, inventory goods are measured on the basis of standard

average costs.

P2: Multiple methods used for management accounting reporting:

MA reports in business-context are perceived to be a must for any company as they help to

efficiently complete the success of the enterprise and its place on the sector. When considering

respective company, it is important for the corporation to assure that a credible accounting report

containing precise periodical analysis is formed in attempt to describe the performance of

business within competitive market. MA reports are most sometimes referred to as the financial

state of a company and helps to accurately reflect relevant details for a relevant duration

or period. Such reports could be considered to assess the financial condition of the company in

the marketplace. These also enable the potential presence of industry in data extraction by

determining the present position (Dekker, 2016). Here are major key reports that respective

corporation, as follows:

Budget report: these reports can be commonly alluded to as a primary operational report which

contains all costs and sales that may take place within a given timeline. It is important for the

managers of the company to realise that they ought to manage their spending in the enterprise.

The accompanying study aims to include information in an enterprise that can be accessed by all

divisions for decision-makings and minimize expenditures. The analysis of past spending and the

prediction of projected expenditures shall be carried out in order to draw up budgeting

reports for company. This also lets companies define their expenses efficiently and eliminates

costs at any step of the way in different business units (Pasch, 2019).

Businesses selling credit-goods on a regular basis are necessary to hold trade Receivables

Ageing Reports since they remind the corporation about defaulters/bad-debts, whether payments

could be secured, to making the repayment cycle simpler. Corporation Capital Joinery can

produce this report to keeping informed of the buyers it owing such that they receive the amounts

as per credit schedule and assure that company does not even have bad debts which are favorable

to the enterprise and improve the higher likelihood of receiving money in reasonable time-

duration.

Cost-Accounting Reports: This style of reports provides financial data on costs of producing

goods, operating costs, and direct labors costs etc.. All such factors are accrued and then

categorised together by units generated. This helps the company to check the amount of expenses

and actual fair market values. Capital Joinery using this report to assess the feasibility and to

achieve a consistent outlook of all relevant costs involving in the manufacturing and purchasing

of goods, and perhaps to decrease their aggregate costs, therefore increasing profits.

Performance Reports: One such report was purely dealing with reviewing actual performance

efficiency the staff and divisions of the enterprise. It advises both the effectiveness of each

division and the workforce. This encourages the organisation to undertake a business judgment

that is worthwhile to the corporation. In Capital Joinery corporation, of that kind reports reflect

on full perspectives through the entity 's divisions. This report must therefore

update performance and success factors of the inner divisions and employees of the corporation.

Inventory Management Report: This report provides detailed descriptions of the products and

stock levels needed by the firm to carries out various manufacturing operations. Such a report

incorporates critical information that require administrators to lessen business product costs as

well as to reduce abnormal inventory costs/losses.

TASK 2

P3 Calculation of cost by using appropriate techniques in cost analysis

Marginal costing approach: Such technique is considered to be techniques used to

measure marginal costs of the goods. The main goal of the introduction of these particular

methods is to determine costs of the manufacturing of additional items. Within the corresponding

entity, the supervisors are used to assess the expenses of any new units (Saeidi and et. al., 2018).

Absorption costing methodology is viewed as the techniques used by corporations or firms to

measure costs due to the manufacturing processes of such products. Within the respective

business, this strategy is used by their managers to ensuring that the costs generated as a

consequence of the production of different units are being used on grounds of same level

of sales.

Absorption Costing Income Statement

duration.

Cost-Accounting Reports: This style of reports provides financial data on costs of producing

goods, operating costs, and direct labors costs etc.. All such factors are accrued and then

categorised together by units generated. This helps the company to check the amount of expenses

and actual fair market values. Capital Joinery using this report to assess the feasibility and to

achieve a consistent outlook of all relevant costs involving in the manufacturing and purchasing

of goods, and perhaps to decrease their aggregate costs, therefore increasing profits.

Performance Reports: One such report was purely dealing with reviewing actual performance

efficiency the staff and divisions of the enterprise. It advises both the effectiveness of each

division and the workforce. This encourages the organisation to undertake a business judgment

that is worthwhile to the corporation. In Capital Joinery corporation, of that kind reports reflect

on full perspectives through the entity 's divisions. This report must therefore

update performance and success factors of the inner divisions and employees of the corporation.

Inventory Management Report: This report provides detailed descriptions of the products and

stock levels needed by the firm to carries out various manufacturing operations. Such a report

incorporates critical information that require administrators to lessen business product costs as

well as to reduce abnormal inventory costs/losses.

TASK 2

P3 Calculation of cost by using appropriate techniques in cost analysis

Marginal costing approach: Such technique is considered to be techniques used to

measure marginal costs of the goods. The main goal of the introduction of these particular

methods is to determine costs of the manufacturing of additional items. Within the corresponding

entity, the supervisors are used to assess the expenses of any new units (Saeidi and et. al., 2018).

Absorption costing methodology is viewed as the techniques used by corporations or firms to

measure costs due to the manufacturing processes of such products. Within the respective

business, this strategy is used by their managers to ensuring that the costs generated as a

consequence of the production of different units are being used on grounds of same level

of sales.

Absorption Costing Income Statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

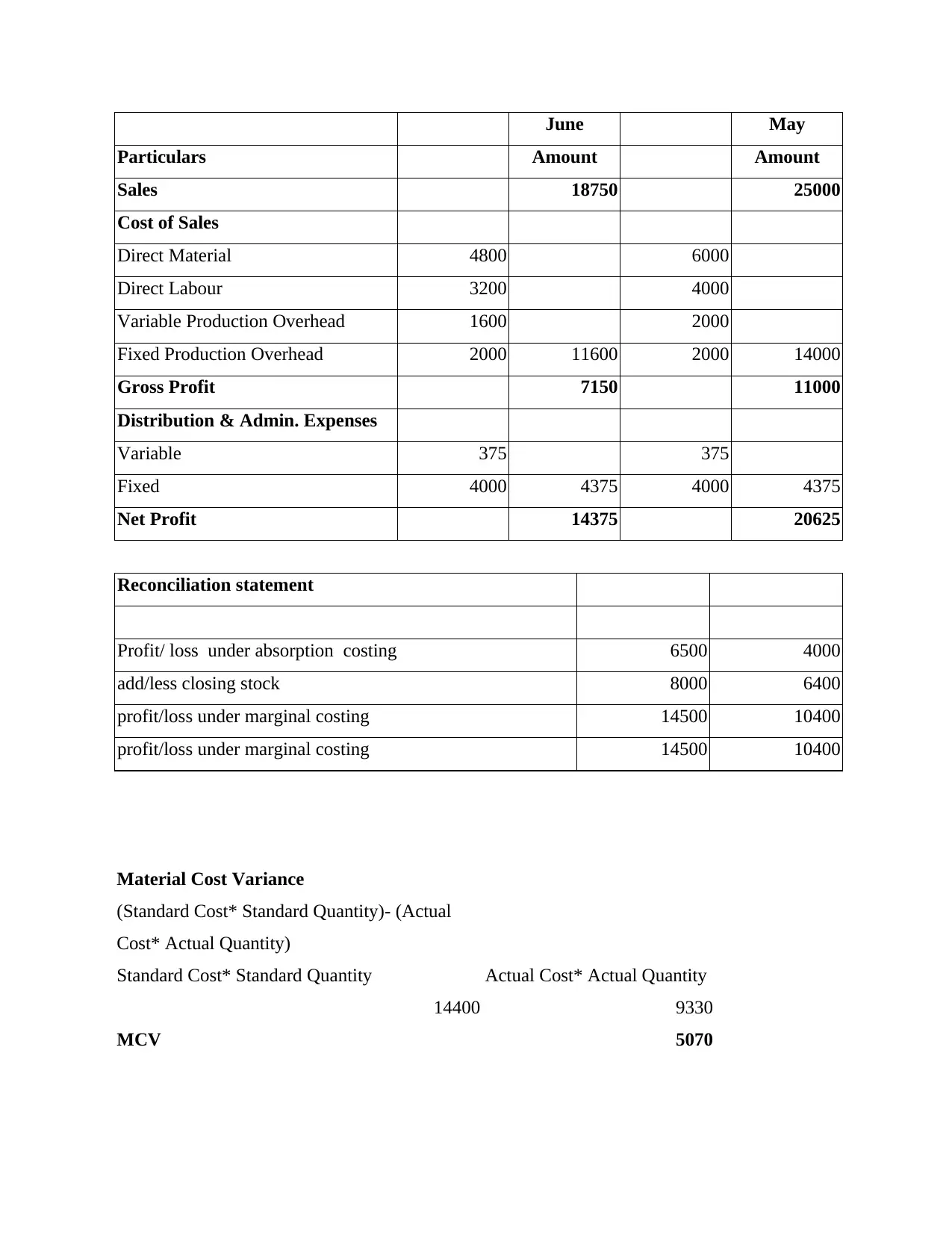

June May

Particulars Amount Amount

Sales 18750 25000

Cost of Sales

Direct Material 4800 6000

Direct Labour 3200 4000

Variable Production Overhead 1600 2000

Fixed Production Overhead 2000 11600 2000 14000

Gross Profit 7150 11000

Distribution & Admin. Expenses

Variable 375 375

Fixed 4000 4375 4000 4375

Net Profit 14375 20625

Reconciliation statement

Profit/ loss under absorption costing 6500 4000

add/less closing stock 8000 6400

profit/loss under marginal costing 14500 10400

profit/loss under marginal costing 14500 10400

Material Cost Variance

(Standard Cost* Standard Quantity)- (Actual

Cost* Actual Quantity)

Standard Cost* Standard Quantity Actual Cost* Actual Quantity

14400 9330

MCV 5070

Particulars Amount Amount

Sales 18750 25000

Cost of Sales

Direct Material 4800 6000

Direct Labour 3200 4000

Variable Production Overhead 1600 2000

Fixed Production Overhead 2000 11600 2000 14000

Gross Profit 7150 11000

Distribution & Admin. Expenses

Variable 375 375

Fixed 4000 4375 4000 4375

Net Profit 14375 20625

Reconciliation statement

Profit/ loss under absorption costing 6500 4000

add/less closing stock 8000 6400

profit/loss under marginal costing 14500 10400

profit/loss under marginal costing 14500 10400

Material Cost Variance

(Standard Cost* Standard Quantity)- (Actual

Cost* Actual Quantity)

Standard Cost* Standard Quantity Actual Cost* Actual Quantity

14400 9330

MCV 5070

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

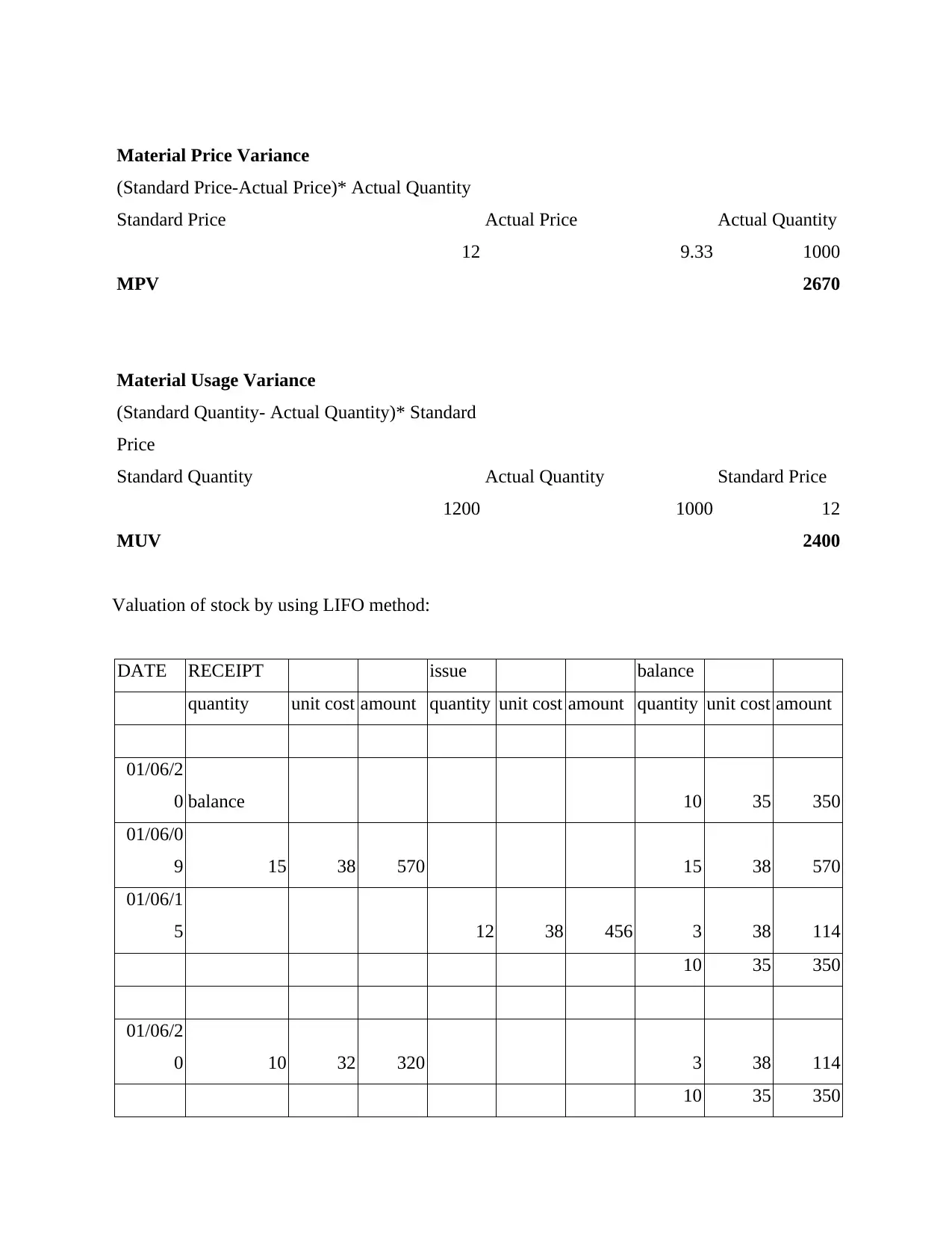

Material Price Variance

(Standard Price-Actual Price)* Actual Quantity

Standard Price Actual Price Actual Quantity

12 9.33 1000

MPV 2670

Material Usage Variance

(Standard Quantity- Actual Quantity)* Standard

Price

Standard Quantity Actual Quantity Standard Price

1200 1000 12

MUV 2400

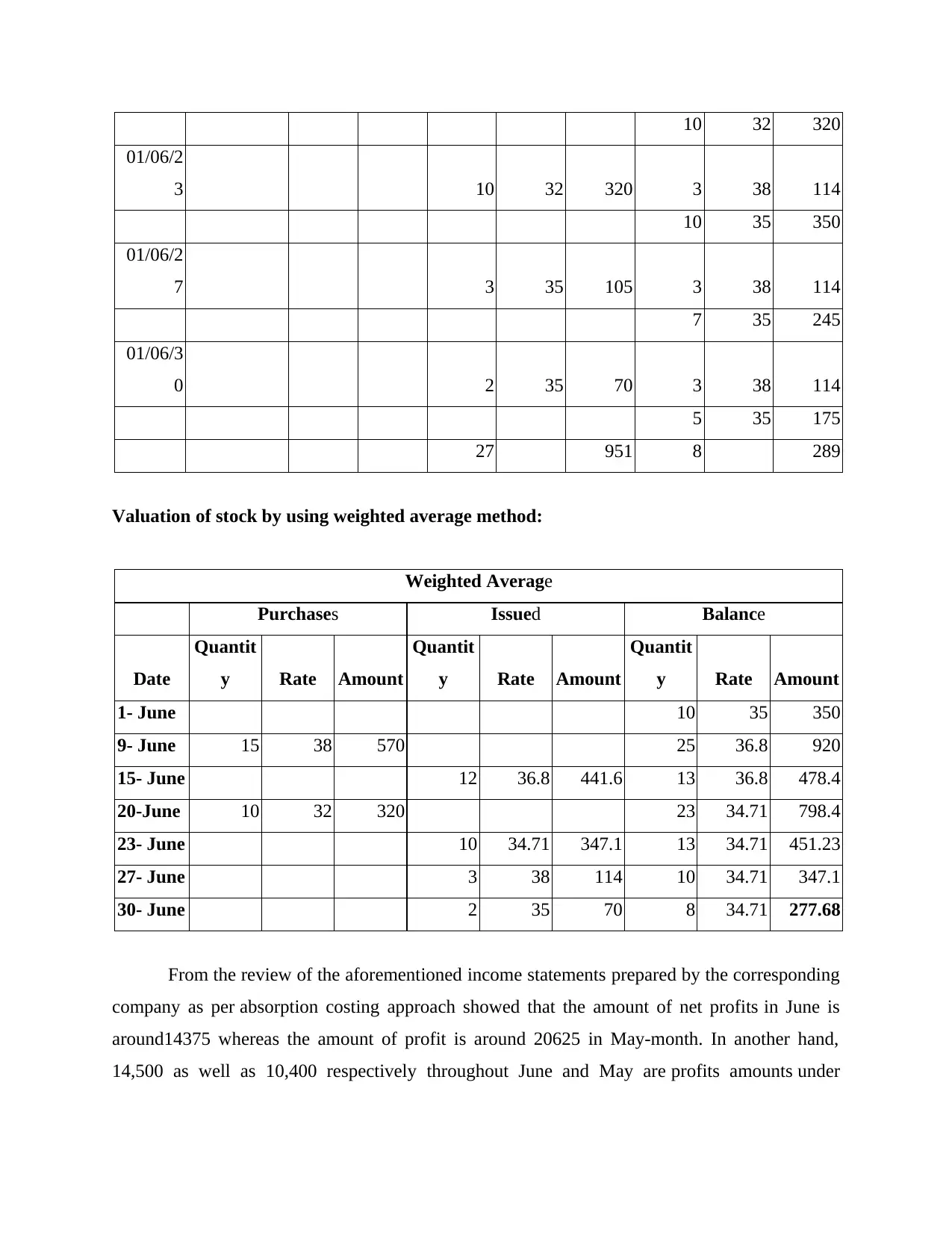

Valuation of stock by using LIFO method:

DATE RECEIPT issue balance

quantity unit cost amount quantity unit cost amount quantity unit cost amount

01/06/2

0 balance 10 35 350

01/06/0

9 15 38 570 15 38 570

01/06/1

5 12 38 456 3 38 114

10 35 350

01/06/2

0 10 32 320 3 38 114

10 35 350

(Standard Price-Actual Price)* Actual Quantity

Standard Price Actual Price Actual Quantity

12 9.33 1000

MPV 2670

Material Usage Variance

(Standard Quantity- Actual Quantity)* Standard

Price

Standard Quantity Actual Quantity Standard Price

1200 1000 12

MUV 2400

Valuation of stock by using LIFO method:

DATE RECEIPT issue balance

quantity unit cost amount quantity unit cost amount quantity unit cost amount

01/06/2

0 balance 10 35 350

01/06/0

9 15 38 570 15 38 570

01/06/1

5 12 38 456 3 38 114

10 35 350

01/06/2

0 10 32 320 3 38 114

10 35 350

10 32 320

01/06/2

3 10 32 320 3 38 114

10 35 350

01/06/2

7 3 35 105 3 38 114

7 35 245

01/06/3

0 2 35 70 3 38 114

5 35 175

27 951 8 289

Valuation of stock by using weighted average method:

Weighted Average

Purchases Issued Balance

Date

Quantit

y Rate Amount

Quantit

y Rate Amount

Quantit

y Rate Amount

1- June 10 35 350

9- June 15 38 570 25 36.8 920

15- June 12 36.8 441.6 13 36.8 478.4

20-June 10 32 320 23 34.71 798.4

23- June 10 34.71 347.1 13 34.71 451.23

27- June 3 38 114 10 34.71 347.1

30- June 2 35 70 8 34.71 277.68

From the review of the aforementioned income statements prepared by the corresponding

company as per absorption costing approach showed that the amount of net profits in June is

around14375 whereas the amount of profit is around 20625 in May-month. In another hand,

14,500 as well as 10,400 respectively throughout June and May are profits amounts under

01/06/2

3 10 32 320 3 38 114

10 35 350

01/06/2

7 3 35 105 3 38 114

7 35 245

01/06/3

0 2 35 70 3 38 114

5 35 175

27 951 8 289

Valuation of stock by using weighted average method:

Weighted Average

Purchases Issued Balance

Date

Quantit

y Rate Amount

Quantit

y Rate Amount

Quantit

y Rate Amount

1- June 10 35 350

9- June 15 38 570 25 36.8 920

15- June 12 36.8 441.6 13 36.8 478.4

20-June 10 32 320 23 34.71 798.4

23- June 10 34.71 347.1 13 34.71 451.23

27- June 3 38 114 10 34.71 347.1

30- June 2 35 70 8 34.71 277.68

From the review of the aforementioned income statements prepared by the corresponding

company as per absorption costing approach showed that the amount of net profits in June is

around14375 whereas the amount of profit is around 20625 in May-month. In another hand,

14,500 as well as 10,400 respectively throughout June and May are profits amounts under

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

marginal costing. Here a disparity in profit numbers derived from different approaches because

of over/under absorptions of fixed overheads costs.

TASK 3

P4. Advantage and disadvantage of several types of planning tools utilised for budgetary control:

The budgets for enterprises such as company Capital Joinery is considered as a financial

roadmap established by administration to bring out next total operations productively. It is

necessary for the enterprise as a whole to recognise that everyone is well coordinated in an effort

to decide the exact organizational position. Establish budgets for preparation of planned costs as

well as revenue for the pursuit of long-term business targets (Cooper, Ezzamel and Qu, 2017).

Budgetary controls are known to be the strategies employed by firm's manager to set

objectives, as well as the financial priorities for the coming years. In addition, there are methods

to estimating range of actual effects from the budgets. With this aid, the respective company will

bring an end to excessive waste of financial capital when its key goal is to maximise income and

control unexpected expenditures. It is also referring to as sustainable way the organisation runs

safely and successfully. They would insure that all funds are used efficiently. When designing

budgets, planner must evaluate the actual stance of the company as well as the requirements for

accessing the required capital.

They shall then devise various approaches to meet all specifications that could be implemented.

Although there are various options that ought to be presented to the appropriate managers and

approved in the context of approval. At the end of the day, approved approaches are employed to

prepare budget and even to run the business in an acceptable way. This is imperative for

the corporation Capital Joinery to generate budgets as well as to employ budgetary controls as it

helps the organisation to recognize the differences and to create strategies to help the business

(Costantini and Zanin, 2017). The advantages and disadvantages are described out below:

Advantages:

• Sets a clear threshold that aims to enhance profitability performance.

• This makes it easier to chart the result by comparison and to follow the strategical objectives.

• If performance is beyond the scope of the goals, it helps to recommend and guide tactics.

Drawbacks:

of over/under absorptions of fixed overheads costs.

TASK 3

P4. Advantage and disadvantage of several types of planning tools utilised for budgetary control:

The budgets for enterprises such as company Capital Joinery is considered as a financial

roadmap established by administration to bring out next total operations productively. It is

necessary for the enterprise as a whole to recognise that everyone is well coordinated in an effort

to decide the exact organizational position. Establish budgets for preparation of planned costs as

well as revenue for the pursuit of long-term business targets (Cooper, Ezzamel and Qu, 2017).

Budgetary controls are known to be the strategies employed by firm's manager to set

objectives, as well as the financial priorities for the coming years. In addition, there are methods

to estimating range of actual effects from the budgets. With this aid, the respective company will

bring an end to excessive waste of financial capital when its key goal is to maximise income and

control unexpected expenditures. It is also referring to as sustainable way the organisation runs

safely and successfully. They would insure that all funds are used efficiently. When designing

budgets, planner must evaluate the actual stance of the company as well as the requirements for

accessing the required capital.

They shall then devise various approaches to meet all specifications that could be implemented.

Although there are various options that ought to be presented to the appropriate managers and

approved in the context of approval. At the end of the day, approved approaches are employed to

prepare budget and even to run the business in an acceptable way. This is imperative for

the corporation Capital Joinery to generate budgets as well as to employ budgetary controls as it

helps the organisation to recognize the differences and to create strategies to help the business

(Costantini and Zanin, 2017). The advantages and disadvantages are described out below:

Advantages:

• Sets a clear threshold that aims to enhance profitability performance.

• This makes it easier to chart the result by comparison and to follow the strategical objectives.

• If performance is beyond the scope of the goals, it helps to recommend and guide tactics.

Drawbacks:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

• Although budgets for the current year including for upcoming years are volatile, there

is monetary disruption.

• It is merely a strategic tool which cannot circumvent management decisions.

• The efficacy of administrative control rests in the hands of senior management, and there's

concern/issue where they do not adhere.

The various strategies used in budgetary management, along with their advantages and obstacles,

are described as below:

Zero-Based Budgeting technique: This is a technique that describes the prior budget as Null

and begun with this period. Unless the expected expenditures are equal to projected expense and

the zero difference. As if not, the modifications are rendered such that it remains null and void. It

is one of most popular budgetary monitoring techniques. Capital Joinery will use this strategy to

show when the estimated earnings are higher than spending and are revised over next projected

budget. Managers/executives accept this shorter-term decision-making strategy to recognize

where prior budgets should be overlooked (Endenich and Trapp, 2020).

Advantages: Disadvantages:

Any pound distributed must be clarified

by upper management. Which explains

both running expenses and the

transactions carried out.

It helps to increase coordination and

interaction among sections that enhance

the productivity of the organisation.

Helps the firm to meet its desired

targets, thereby helping to achieve

organisational goal more productively.

An organisation needs to require more-

time and resources to generate a null-

base budget.

Negligence of the budget for the

previous period could respond to bad

decisions.

This form of budgeting is often

inappropriate to take longer-term

decisions.

Activity-based budgeting: Activity-based budgeting approach is approach that

encourages the costs of any operation within the organisation to be tracked, studied and assessed.

It updates tentative budgets and adds to the development of all operations. Via activity-based

budgeting, businesses can eliminate costs and achieve greater efficiency. Such budgeting may be

used to efficiently allocate all expenses to a variety of tasks for Capital Joinery. Operating

is monetary disruption.

• It is merely a strategic tool which cannot circumvent management decisions.

• The efficacy of administrative control rests in the hands of senior management, and there's

concern/issue where they do not adhere.

The various strategies used in budgetary management, along with their advantages and obstacles,

are described as below:

Zero-Based Budgeting technique: This is a technique that describes the prior budget as Null

and begun with this period. Unless the expected expenditures are equal to projected expense and

the zero difference. As if not, the modifications are rendered such that it remains null and void. It

is one of most popular budgetary monitoring techniques. Capital Joinery will use this strategy to

show when the estimated earnings are higher than spending and are revised over next projected

budget. Managers/executives accept this shorter-term decision-making strategy to recognize

where prior budgets should be overlooked (Endenich and Trapp, 2020).

Advantages: Disadvantages:

Any pound distributed must be clarified

by upper management. Which explains

both running expenses and the

transactions carried out.

It helps to increase coordination and

interaction among sections that enhance

the productivity of the organisation.

Helps the firm to meet its desired

targets, thereby helping to achieve

organisational goal more productively.

An organisation needs to require more-

time and resources to generate a null-

base budget.

Negligence of the budget for the

previous period could respond to bad

decisions.

This form of budgeting is often

inappropriate to take longer-term

decisions.

Activity-based budgeting: Activity-based budgeting approach is approach that

encourages the costs of any operation within the organisation to be tracked, studied and assessed.

It updates tentative budgets and adds to the development of all operations. Via activity-based

budgeting, businesses can eliminate costs and achieve greater efficiency. Such budgeting may be

used to efficiently allocate all expenses to a variety of tasks for Capital Joinery. Operating

activities and their cost are stressed in the activity-based budget planning. It emphasises that

if amount of function is limited, running costs can be managed. Where typical budgeting is

targeted at concentrating on manufacturing costs, a performance-oriented approach is

accompanied by ABB that recognises that operations invest. ABB regards the business as a

collection of activities, which are a strong relation to the operational approach.

Advantages: Disadvantages:

This concept eliminates additional costs

as well as enables the company to

minimise costs, leading to lower costs

that further adds to a feasible market

edge through operations at lower

costs than competing entities.

All companies should be seen as single

component of this budget planning and

are not considered to be segments

which lets the corporation to conduct

business proficiently.

The major purpose is to minimise the

added costs of all staff members to

functions together that also is

instructive when it embraces them

productively.

One such type of budgeting

needs different functional elements and

will make a contribution to insufficient

spending plan even though the decision

- maker does not understand the

budgeting.

Dynamic is core of an operation and

multi-resource capital measurement. In

fact, it is period for company to utilise

all the instruments for its organisation -

wide activities.

This contains skilled workers, which

cannot pursue roles for people who are

just not specialised. Therefore it would

need extra costs, and is therefore

complicated and labour - intensive.

P5. Comparison of how firms are adopting management accounting systems to respond to

financial problems:

Any corporation faces certain problems and fiscal issues/problems because of financial

resources shortage, and most of them are due to poor resources management. An organisation

wants to make efficient use of its resources and to meet financial goals. When companies

develop financial problems, overcoming them seems to be a responsibility. Fiscal problems are

if amount of function is limited, running costs can be managed. Where typical budgeting is

targeted at concentrating on manufacturing costs, a performance-oriented approach is

accompanied by ABB that recognises that operations invest. ABB regards the business as a

collection of activities, which are a strong relation to the operational approach.

Advantages: Disadvantages:

This concept eliminates additional costs

as well as enables the company to

minimise costs, leading to lower costs

that further adds to a feasible market

edge through operations at lower

costs than competing entities.

All companies should be seen as single

component of this budget planning and

are not considered to be segments

which lets the corporation to conduct

business proficiently.

The major purpose is to minimise the

added costs of all staff members to

functions together that also is

instructive when it embraces them

productively.

One such type of budgeting

needs different functional elements and

will make a contribution to insufficient

spending plan even though the decision

- maker does not understand the

budgeting.

Dynamic is core of an operation and

multi-resource capital measurement. In

fact, it is period for company to utilise

all the instruments for its organisation -

wide activities.

This contains skilled workers, which

cannot pursue roles for people who are

just not specialised. Therefore it would

need extra costs, and is therefore

complicated and labour - intensive.

P5. Comparison of how firms are adopting management accounting systems to respond to

financial problems:

Any corporation faces certain problems and fiscal issues/problems because of financial

resources shortage, and most of them are due to poor resources management. An organisation

wants to make efficient use of its resources and to meet financial goals. When companies

develop financial problems, overcoming them seems to be a responsibility. Fiscal problems are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.