Financial Resources Management: Cost Analysis, Budgeting & Forecasting

VerifiedAdded on 2023/06/15

|11

|2647

|226

Report

AI Summary

This report provides a comprehensive overview of managing financial resources, including detailed cost calculations for a business, preparation of a cost sheet, and analysis of budgeting and forecasting techniques. It covers prime cost, production cost, administrative expenses, sales and distribution expenses, and total cost calculations. The report further examines budgeting and forecasting with examples, variance analysis (favorable and adverse), and flexible budgeting. Key financial terms such as labor cost, customer retention rate, food average spend, and food cost of sales ratio are explained with formulas and practical examples, illustrating their importance in financial management and decision-making. This document is available for review and study on Desklib, a platform offering a wide range of academic resources.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK ..............................................................................................................................................3

Question 1: Calculate the different costs for Costa.....................................................................3

Question 4 : Analyse the following with examples....................................................................5

Question 6 : Explain the following terms with their formula and examples..............................8

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION ..........................................................................................................................3

TASK ..............................................................................................................................................3

Question 1: Calculate the different costs for Costa.....................................................................3

Question 4 : Analyse the following with examples....................................................................5

Question 6 : Explain the following terms with their formula and examples..............................8

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Managing financial resources refers to the management of the complicated issues which arise In

an organisation related to the financial planning and control of the business (Plaskova, and et.al.,

2020). The following assessment shows calculations related to different costs which are incurred

in the business and a cost sheet is prepared for the same. The next section of the assessment

shows discusses the different terms used in management of financial resources and are explained

thereunder using examples.

TASK

SECTION A:

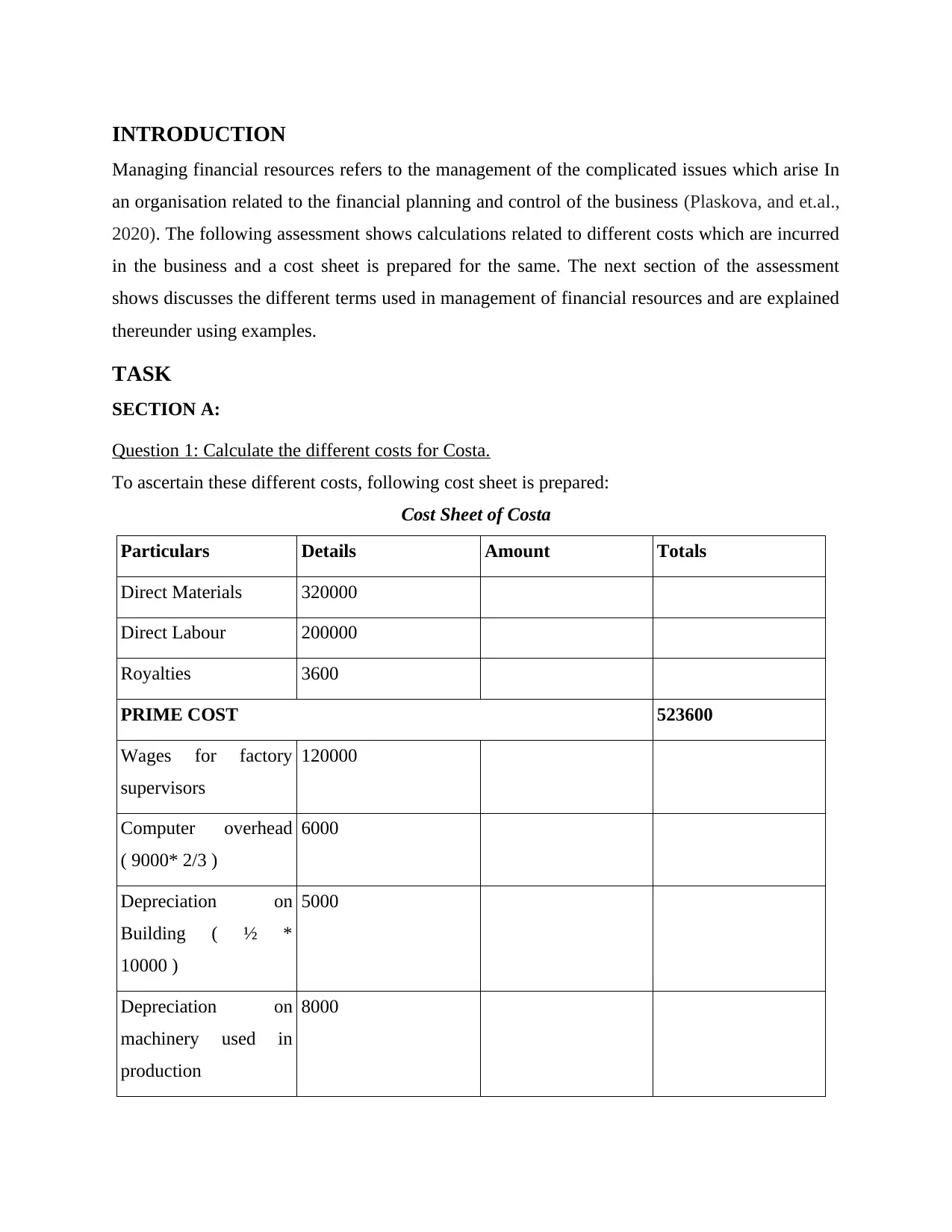

Question 1: Calculate the different costs for Costa.

To ascertain these different costs, following cost sheet is prepared:

Cost Sheet of Costa

Particulars Details Amount Totals

Direct Materials 320000

Direct Labour 200000

Royalties 3600

PRIME COST 523600

Wages for factory

supervisors

120000

Computer overhead

( 9000* 2/3 )

6000

Depreciation on

Building ( ½ *

10000 )

5000

Depreciation on

machinery used in

production

8000

Managing financial resources refers to the management of the complicated issues which arise In

an organisation related to the financial planning and control of the business (Plaskova, and et.al.,

2020). The following assessment shows calculations related to different costs which are incurred

in the business and a cost sheet is prepared for the same. The next section of the assessment

shows discusses the different terms used in management of financial resources and are explained

thereunder using examples.

TASK

SECTION A:

Question 1: Calculate the different costs for Costa.

To ascertain these different costs, following cost sheet is prepared:

Cost Sheet of Costa

Particulars Details Amount Totals

Direct Materials 320000

Direct Labour 200000

Royalties 3600

PRIME COST 523600

Wages for factory

supervisors

120000

Computer overhead

( 9000* 2/3 )

6000

Depreciation on

Building ( ½ *

10000 )

5000

Depreciation on

machinery used in

production

8000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

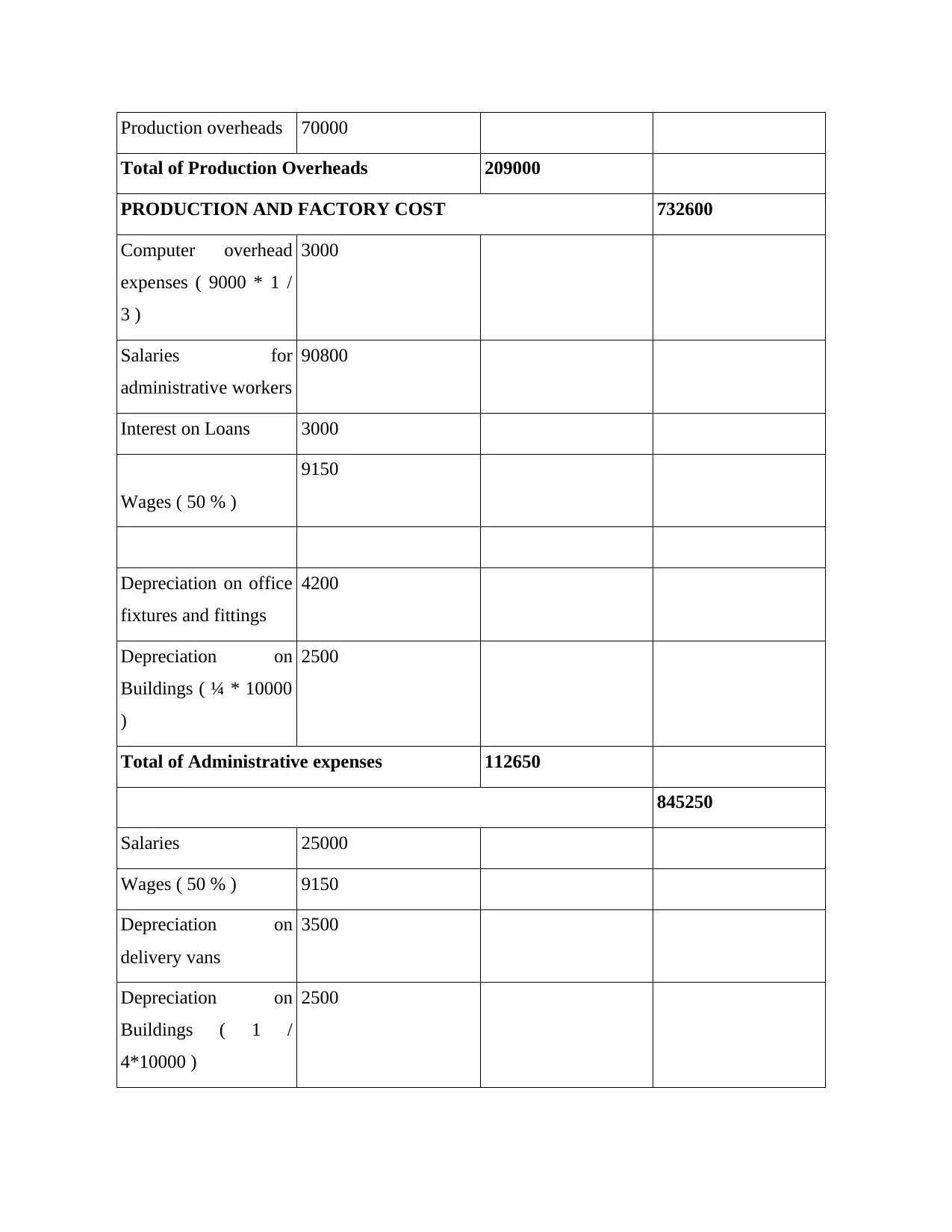

Production overheads 70000

Total of Production Overheads 209000

PRODUCTION AND FACTORY COST 732600

Computer overhead

expenses ( 9000 * 1 /

3 )

3000

Salaries for

administrative workers

90800

Interest on Loans 3000

Wages ( 50 % )

9150

Depreciation on office

fixtures and fittings

4200

Depreciation on

Buildings ( ¼ * 10000

)

2500

Total of Administrative expenses 112650

845250

Salaries 25000

Wages ( 50 % ) 9150

Depreciation on

delivery vans

3500

Depreciation on

Buildings ( 1 /

4*10000 )

2500

Total of Production Overheads 209000

PRODUCTION AND FACTORY COST 732600

Computer overhead

expenses ( 9000 * 1 /

3 )

3000

Salaries for

administrative workers

90800

Interest on Loans 3000

Wages ( 50 % )

9150

Depreciation on office

fixtures and fittings

4200

Depreciation on

Buildings ( ¼ * 10000

)

2500

Total of Administrative expenses 112650

845250

Salaries 25000

Wages ( 50 % ) 9150

Depreciation on

delivery vans

3500

Depreciation on

Buildings ( 1 /

4*10000 )

2500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

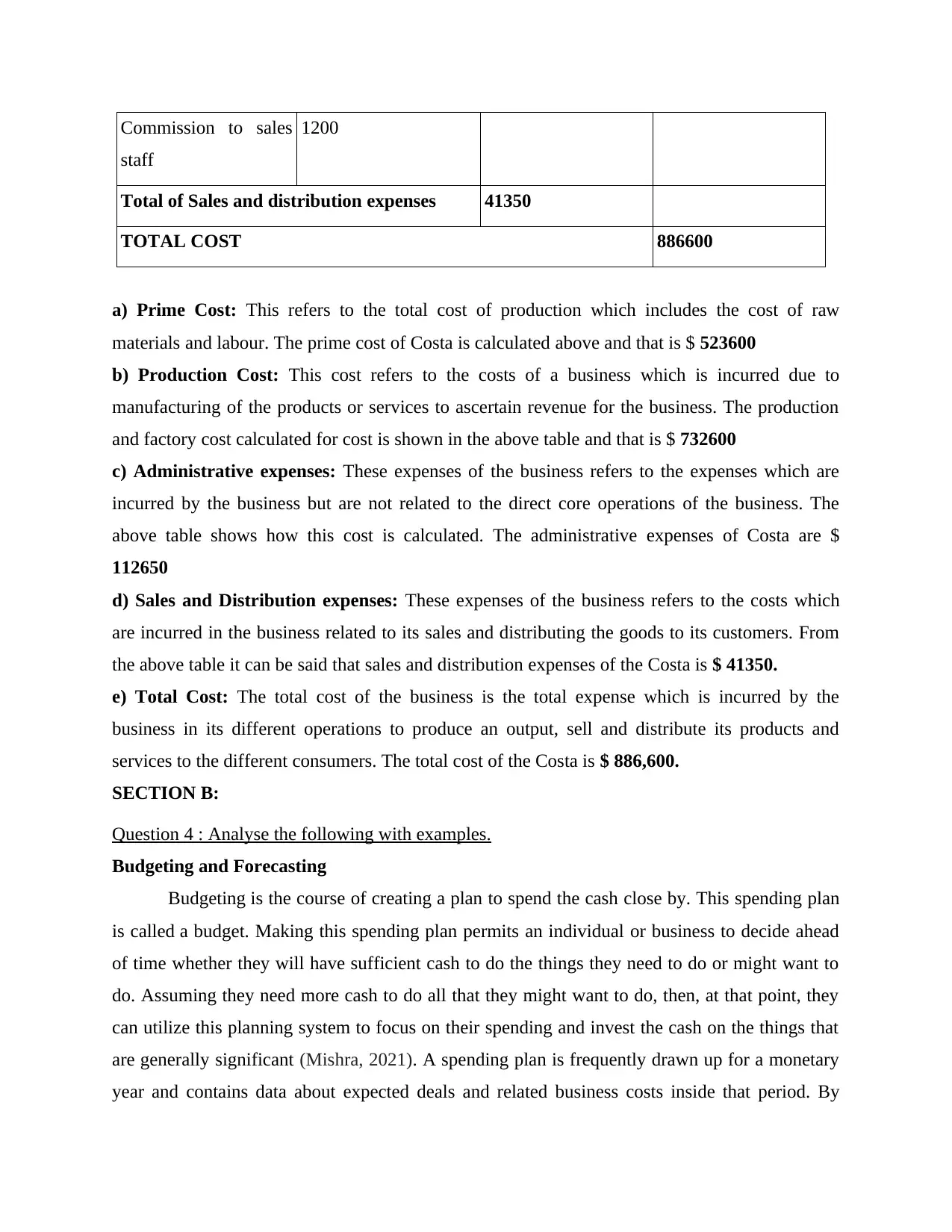

Commission to sales

staff

1200

Total of Sales and distribution expenses 41350

TOTAL COST 886600

a) Prime Cost: This refers to the total cost of production which includes the cost of raw

materials and labour. The prime cost of Costa is calculated above and that is $ 523600

b) Production Cost: This cost refers to the costs of a business which is incurred due to

manufacturing of the products or services to ascertain revenue for the business. The production

and factory cost calculated for cost is shown in the above table and that is $ 732600

c) Administrative expenses: These expenses of the business refers to the expenses which are

incurred by the business but are not related to the direct core operations of the business. The

above table shows how this cost is calculated. The administrative expenses of Costa are $

112650

d) Sales and Distribution expenses: These expenses of the business refers to the costs which

are incurred in the business related to its sales and distributing the goods to its customers. From

the above table it can be said that sales and distribution expenses of the Costa is $ 41350.

e) Total Cost: The total cost of the business is the total expense which is incurred by the

business in its different operations to produce an output, sell and distribute its products and

services to the different consumers. The total cost of the Costa is $ 886,600.

SECTION B:

Question 4 : Analyse the following with examples.

Budgeting and Forecasting

Budgeting is the course of creating a plan to spend the cash close by. This spending plan

is called a budget. Making this spending plan permits an individual or business to decide ahead

of time whether they will have sufficient cash to do the things they need to do or might want to

do. Assuming they need more cash to do all that they might want to do, then, at that point, they

can utilize this planning system to focus on their spending and invest the cash on the things that

are generally significant (Mishra, 2021). A spending plan is frequently drawn up for a monetary

year and contains data about expected deals and related business costs inside that period. By

staff

1200

Total of Sales and distribution expenses 41350

TOTAL COST 886600

a) Prime Cost: This refers to the total cost of production which includes the cost of raw

materials and labour. The prime cost of Costa is calculated above and that is $ 523600

b) Production Cost: This cost refers to the costs of a business which is incurred due to

manufacturing of the products or services to ascertain revenue for the business. The production

and factory cost calculated for cost is shown in the above table and that is $ 732600

c) Administrative expenses: These expenses of the business refers to the expenses which are

incurred by the business but are not related to the direct core operations of the business. The

above table shows how this cost is calculated. The administrative expenses of Costa are $

112650

d) Sales and Distribution expenses: These expenses of the business refers to the costs which

are incurred in the business related to its sales and distributing the goods to its customers. From

the above table it can be said that sales and distribution expenses of the Costa is $ 41350.

e) Total Cost: The total cost of the business is the total expense which is incurred by the

business in its different operations to produce an output, sell and distribute its products and

services to the different consumers. The total cost of the Costa is $ 886,600.

SECTION B:

Question 4 : Analyse the following with examples.

Budgeting and Forecasting

Budgeting is the course of creating a plan to spend the cash close by. This spending plan

is called a budget. Making this spending plan permits an individual or business to decide ahead

of time whether they will have sufficient cash to do the things they need to do or might want to

do. Assuming they need more cash to do all that they might want to do, then, at that point, they

can utilize this planning system to focus on their spending and invest the cash on the things that

are generally significant (Mishra, 2021). A spending plan is frequently drawn up for a monetary

year and contains data about expected deals and related business costs inside that period. By

utilizing this financial plan a business can perceive how well they are hoping to perform inside

the year and genuine execution can be checked against this unique proposed plan. The main role

of these budgets is to help the venture methodology through arranged drives, planned asset

assignment degree to which changes in the climate are affecting the limit of the business to meet

targets.

Forecasting is an evaluation of conceivable future occasions. At the underlying arranging stage,

it is mandatory to plan to estimates potential activities for the business later on. Forecasts

includes deals, creation, cost, acquisition of material, and monetary need of the business. The

figure has some adaptability, through the spending plan having a decent objective.

By and large, budgeting and forecasting are used interchangeably or comprehended as a

similar action (Planning incorporates Anticipating). Notwithstanding, there is a merger line

between both. A budget is a projection of what will occur during the planning time frame at an

association level, by and large incorporate critical livelihoods and consumptions (Panov, and

Larionova, 2021). A forecast might be for long haul or momentary period or utilizing the

hierarchical or wider perspective.

A drawn out budget will give important result to the administration for their essential

strategy. Interestingly, transient estimate is by and large is finished functional and everyday

business needs.

Example of budgeting are, sales budget, production budget, flexed budget etc.

Variance Analysis

Variance Analysis is the investigation of deviations of genuine conduct versus estimated or

arranged conduct in planning or the executives bookkeeping. This is basically worried about how

the distinction of real and arranged practices shows how business execution is being affected.

Variance Analysis change assists organizations with understanding current outgoings and assists

them with planning for future costs. Organizations frequently do Variance Analysis - a

quantitative examination concerning the contrasts among arranged and genuine expenses and

incomes (Block, Hirt, and Danielsen, 2018). Variance Analysis can be applied to the two

incomes and costs. At the point when real outcomes are better compared to arranged, change is

alluded to as 'Favourable'. Assuming that outcomes are more awful than anticipated, fluctuation

is alluded to as ‘adverse’ or ‘unfavourable'. Analysing. For example, the forecasted expense on

the year and genuine execution can be checked against this unique proposed plan. The main role

of these budgets is to help the venture methodology through arranged drives, planned asset

assignment degree to which changes in the climate are affecting the limit of the business to meet

targets.

Forecasting is an evaluation of conceivable future occasions. At the underlying arranging stage,

it is mandatory to plan to estimates potential activities for the business later on. Forecasts

includes deals, creation, cost, acquisition of material, and monetary need of the business. The

figure has some adaptability, through the spending plan having a decent objective.

By and large, budgeting and forecasting are used interchangeably or comprehended as a

similar action (Planning incorporates Anticipating). Notwithstanding, there is a merger line

between both. A budget is a projection of what will occur during the planning time frame at an

association level, by and large incorporate critical livelihoods and consumptions (Panov, and

Larionova, 2021). A forecast might be for long haul or momentary period or utilizing the

hierarchical or wider perspective.

A drawn out budget will give important result to the administration for their essential

strategy. Interestingly, transient estimate is by and large is finished functional and everyday

business needs.

Example of budgeting are, sales budget, production budget, flexed budget etc.

Variance Analysis

Variance Analysis is the investigation of deviations of genuine conduct versus estimated or

arranged conduct in planning or the executives bookkeeping. This is basically worried about how

the distinction of real and arranged practices shows how business execution is being affected.

Variance Analysis change assists organizations with understanding current outgoings and assists

them with planning for future costs. Organizations frequently do Variance Analysis - a

quantitative examination concerning the contrasts among arranged and genuine expenses and

incomes (Block, Hirt, and Danielsen, 2018). Variance Analysis can be applied to the two

incomes and costs. At the point when real outcomes are better compared to arranged, change is

alluded to as 'Favourable'. Assuming that outcomes are more awful than anticipated, fluctuation

is alluded to as ‘adverse’ or ‘unfavourable'. Analysing. For example, the forecasted expense on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the production was 150000 but the actual cost occurred on production is 180000 which means

that the variance is unfavourable.

Adverse Variances

An adverse variance is the place where real pay is not as much as spending plan, or actual

expenditure is more than financial plan. This is equivalent to a expenditure exceeds the available

income. A positive difference is the place where genuine pay is more than financial plan, or real

use is not as much as spending plan. An unfavourable variance can happen because of changing

financial conditions, for example, lower monetary development, lower customer spending, or a

downturn, which prompts higher joblessness. Economic situations can likewise change, for

example, new contenders entering the market with new items and administrations. For example,

the forecasted sales were 18000 but the actual sales occurred is 15000 which means that the

variance is unfavourable or adverse.

Favourable Variances

A Favourable Variances is the place where real pay is more than spending plan, or real use is not

as much as financial plan. This is equivalent to an excess where consumption is not exactly the

accessible income. An ideal fluctuation shows that a business has either produced more income

than anticipated or caused less costs than anticipated. For a cost, this is the abundance of a norm

or planned sum over the genuine sum brought about (Chernov, 2020). At the point when income

is involved, an ideal change is the point at which the real income perceived is more prominent

than the norm or planned sum. For example, the forecasted sales were 18000 but the actual sales

occurred is 20000 which means that the variance is favourable.

Flexible Budget

An flexible budget acclimates to changes in authentic income levels. Real incomes or other

changes measures are gone into the adaptable spending plan once a bookkeeping period has been

finished, and it produces a spending plan that is explicit to the sources of info. The budget is then

contrasted with genuine costs for control purposes. An adaptable spending plan requires

additional opportunity to build, defers the issuance of fiscal reports, doesn't quantify income

differences, and may not be pertinent under specific financial plan models. For example, XYZ

Organization has a spending plan of $10 million in incomes and a $4 million expense of

merchandise sold. Of the $4 million in planned expense of merchandise sold, $1 million is fixed,

and $3 million fluctuates straightforwardly with income. In this way, the variable piece of the

that the variance is unfavourable.

Adverse Variances

An adverse variance is the place where real pay is not as much as spending plan, or actual

expenditure is more than financial plan. This is equivalent to a expenditure exceeds the available

income. A positive difference is the place where genuine pay is more than financial plan, or real

use is not as much as spending plan. An unfavourable variance can happen because of changing

financial conditions, for example, lower monetary development, lower customer spending, or a

downturn, which prompts higher joblessness. Economic situations can likewise change, for

example, new contenders entering the market with new items and administrations. For example,

the forecasted sales were 18000 but the actual sales occurred is 15000 which means that the

variance is unfavourable or adverse.

Favourable Variances

A Favourable Variances is the place where real pay is more than spending plan, or real use is not

as much as financial plan. This is equivalent to an excess where consumption is not exactly the

accessible income. An ideal fluctuation shows that a business has either produced more income

than anticipated or caused less costs than anticipated. For a cost, this is the abundance of a norm

or planned sum over the genuine sum brought about (Chernov, 2020). At the point when income

is involved, an ideal change is the point at which the real income perceived is more prominent

than the norm or planned sum. For example, the forecasted sales were 18000 but the actual sales

occurred is 20000 which means that the variance is favourable.

Flexible Budget

An flexible budget acclimates to changes in authentic income levels. Real incomes or other

changes measures are gone into the adaptable spending plan once a bookkeeping period has been

finished, and it produces a spending plan that is explicit to the sources of info. The budget is then

contrasted with genuine costs for control purposes. An adaptable spending plan requires

additional opportunity to build, defers the issuance of fiscal reports, doesn't quantify income

differences, and may not be pertinent under specific financial plan models. For example, XYZ

Organization has a spending plan of $10 million in incomes and a $4 million expense of

merchandise sold. Of the $4 million in planned expense of merchandise sold, $1 million is fixed,

and $3 million fluctuates straightforwardly with income. In this way, the variable piece of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expense of products sold is 30% of incomes. When the spending plan period has been finished,

XYZ observes that deals were really $9 million. On the off chance that it utilized an adaptable

spending plan, the proper piece of the expense of merchandise sold would in any case be $1

million, yet the variable part would drop to $2.7 million, since it is 30% all the time of incomes.

The outcome is that an adaptable spending plan yields a planned expense of products sold of

$3.7 million at a $9 million income level, rather than the $4 million that would be recorded in a

static financial plan.

Question 6 : Explain the following terms with their formula and examples.

1. Labour Cost:

labour cost is amongst the highest paid expenses in an organisation. In fact, in restaurant

business such cost contributes 5-10% of total revenue. Labour cost is not just wages or salaries

but it also includes payroll taxes, bonus, overtime, training cost, insurance etc.

formula of calculating labour cost are as under:-

Labour cost(as % to sales)= (Total labour/ Total sales*100) and

Labour cost(as % to operating cost)=(Total labour/Total operating cost*100)

For example, in a restaurant business, there is annual labour cost of 84000 pound ,operating cost

is 4,12,000 pound and suppose their revenue during the accounting year is 11,25,600 pound.

Then their labour cost will be:

% to sales= (84000/1125600*100)

=7.46%

% to operating cost=(84000/412000*100)

=20.39%

2. Customer retention rate: It simply means the number of customer, an organisation retains

over the giver period of time. Their is a financial reason to retain existing customer as keeping

existing customer is lot cheaper rather to maintain a new customer base for a company (Barr, and

McClellan, 2018). Loyal and old customers also makes contribution towards wealth of firm by

way of promoting brand in social media, commenting or making regular feedback to improve

products of services.

XYZ observes that deals were really $9 million. On the off chance that it utilized an adaptable

spending plan, the proper piece of the expense of merchandise sold would in any case be $1

million, yet the variable part would drop to $2.7 million, since it is 30% all the time of incomes.

The outcome is that an adaptable spending plan yields a planned expense of products sold of

$3.7 million at a $9 million income level, rather than the $4 million that would be recorded in a

static financial plan.

Question 6 : Explain the following terms with their formula and examples.

1. Labour Cost:

labour cost is amongst the highest paid expenses in an organisation. In fact, in restaurant

business such cost contributes 5-10% of total revenue. Labour cost is not just wages or salaries

but it also includes payroll taxes, bonus, overtime, training cost, insurance etc.

formula of calculating labour cost are as under:-

Labour cost(as % to sales)= (Total labour/ Total sales*100) and

Labour cost(as % to operating cost)=(Total labour/Total operating cost*100)

For example, in a restaurant business, there is annual labour cost of 84000 pound ,operating cost

is 4,12,000 pound and suppose their revenue during the accounting year is 11,25,600 pound.

Then their labour cost will be:

% to sales= (84000/1125600*100)

=7.46%

% to operating cost=(84000/412000*100)

=20.39%

2. Customer retention rate: It simply means the number of customer, an organisation retains

over the giver period of time. Their is a financial reason to retain existing customer as keeping

existing customer is lot cheaper rather to maintain a new customer base for a company (Barr, and

McClellan, 2018). Loyal and old customers also makes contribution towards wealth of firm by

way of promoting brand in social media, commenting or making regular feedback to improve

products of services.

The formula is as under:

(E-N/S*100)

Here E stands for total no of customer, N for total no of new customer and S for total no of

existing customers

Lets say a restaurant has 100 customers(S) at the beginning of the year, and ended with 100

customer(E) and added 10 new customers(N) during the period.

Therefore their customer retention ration will be:

=(100-10/100)*100

=90%

3. Food average spend: As a business owner,our priority is always delighting the customers but

topmost financial priority for any firm is maximising their sales figures with minimum cost. In

restaurant business, food cost percentage is important because proper monitoring on such cost

can help in achieving maximum profits.

Food average spend can be calculated as under:

=(Opening stock+Purchases-Closing Stock/ Food Sales)

Assuming in a restaurant, opening stock is 15000 pound, purchases 4000 pound,closing stock

16000 pound and food sales is 10000 pound.

Therefore food average spend will be:

=(15000+4000-16000)/10000

=30%

4. Food cost of sales ratio: Calculation of food cost and boosting up the profit is a first lesson

anyone would learn working in a business. On an average, food cost of sales would be 30 to 50%

of total sales in any concern. Controlling the cost of sales helps in generating more revenue and

boosting up the profit margin.

Food cost of sales ratio is a financial ratio which compare expenses of an enterprise which their

sales figures. The following in the formula of calculated the same:

=(Food cost of sales/Total Sales or revenue)*100

For e.g., the food cost of sales for an entity is 98000 pound and their revenue during the year is

156000 pound then their ratio will be:

(E-N/S*100)

Here E stands for total no of customer, N for total no of new customer and S for total no of

existing customers

Lets say a restaurant has 100 customers(S) at the beginning of the year, and ended with 100

customer(E) and added 10 new customers(N) during the period.

Therefore their customer retention ration will be:

=(100-10/100)*100

=90%

3. Food average spend: As a business owner,our priority is always delighting the customers but

topmost financial priority for any firm is maximising their sales figures with minimum cost. In

restaurant business, food cost percentage is important because proper monitoring on such cost

can help in achieving maximum profits.

Food average spend can be calculated as under:

=(Opening stock+Purchases-Closing Stock/ Food Sales)

Assuming in a restaurant, opening stock is 15000 pound, purchases 4000 pound,closing stock

16000 pound and food sales is 10000 pound.

Therefore food average spend will be:

=(15000+4000-16000)/10000

=30%

4. Food cost of sales ratio: Calculation of food cost and boosting up the profit is a first lesson

anyone would learn working in a business. On an average, food cost of sales would be 30 to 50%

of total sales in any concern. Controlling the cost of sales helps in generating more revenue and

boosting up the profit margin.

Food cost of sales ratio is a financial ratio which compare expenses of an enterprise which their

sales figures. The following in the formula of calculated the same:

=(Food cost of sales/Total Sales or revenue)*100

For e.g., the food cost of sales for an entity is 98000 pound and their revenue during the year is

156000 pound then their ratio will be:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

=98000/156000*100

= 62.82%

5. Beverage cost of sales: Beverage cost of sales in generally calculated in an hotel industry.

This is calculated to ascertain that what is the amount of contribution is made by the beverages in

the total sales of the organisation.

It is calculated as under:

=(Cost of beverages sold/Total sales *100)

Lets assume that a restaurant owner has calculated their cost of beverages amount to pound

15000 and their total sales made during an accounting period is pound 98000.

Therefore beverage cost of sales would be as under:

=15000/98000*100

=15.31%

CONCLUSION

From the above assessment it can be concluded that managing of financial resources is an

important aspect in the business as it helps the management to eliminate the extra expenses

which might occur in the business. Preparation of cost sheet has highlighted the way business

can bring management into its operations similar to budgets.

= 62.82%

5. Beverage cost of sales: Beverage cost of sales in generally calculated in an hotel industry.

This is calculated to ascertain that what is the amount of contribution is made by the beverages in

the total sales of the organisation.

It is calculated as under:

=(Cost of beverages sold/Total sales *100)

Lets assume that a restaurant owner has calculated their cost of beverages amount to pound

15000 and their total sales made during an accounting period is pound 98000.

Therefore beverage cost of sales would be as under:

=15000/98000*100

=15.31%

CONCLUSION

From the above assessment it can be concluded that managing of financial resources is an

important aspect in the business as it helps the management to eliminate the extra expenses

which might occur in the business. Preparation of cost sheet has highlighted the way business

can bring management into its operations similar to budgets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Plaskova, N.S., and et.al., 2020. Improving Information and Analytical and Methodological

Support for Managing the Structure of Financial Resources of the Organization. Talent

Development & Excellence, 12.

Mishra, S.K., 2021. GMFP Food and Products: Managing Financial Distress. SAGE

Publications: SAGE Business Cases Originals.

Panov, D. and Larionova, I., 2021. Managing the Risks of Financial Intermediaries:

Transforming Approaches and Reality. In Financial Markets Evolution (pp. 261-271).

Palgrave Macmillan, Cham.

Block, S.B., Hirt, G.A. and Danielsen, B.R., 2018. Foundations of financial management.

McGraw-Hill Education.

Chernov, V.A., 2020. Implementation of Digital Technologies in Financial

Management. Ekonomika Regiona, (1), p.283.

Barr, M.J. and McClellan, G.S., 2018. Budgets and financial management in higher education.

John Wiley & Sons.

Books and Journals

Plaskova, N.S., and et.al., 2020. Improving Information and Analytical and Methodological

Support for Managing the Structure of Financial Resources of the Organization. Talent

Development & Excellence, 12.

Mishra, S.K., 2021. GMFP Food and Products: Managing Financial Distress. SAGE

Publications: SAGE Business Cases Originals.

Panov, D. and Larionova, I., 2021. Managing the Risks of Financial Intermediaries:

Transforming Approaches and Reality. In Financial Markets Evolution (pp. 261-271).

Palgrave Macmillan, Cham.

Block, S.B., Hirt, G.A. and Danielsen, B.R., 2018. Foundations of financial management.

McGraw-Hill Education.

Chernov, V.A., 2020. Implementation of Digital Technologies in Financial

Management. Ekonomika Regiona, (1), p.283.

Barr, M.J. and McClellan, G.S., 2018. Budgets and financial management in higher education.

John Wiley & Sons.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.