B12645 Management Accounting: Cost Analysis and Budgeting

VerifiedAdded on 2023/01/12

|25

|4330

|83

Report

AI Summary

This report, focusing on management accounting, explores key concepts and techniques essential for financial analysis and decision-making within organizations. The report is divided into two main parts: Part 1 delves into the fundamentals of management accounting, outlining its definition, essential requirements of different management accounting systems, and various reporting methods. It evaluates the benefits of management accounting systems and their integration within organizational processes. Part 2 focuses on practical applications, including cost analysis techniques to prepare income statements using marginal and absorption costing. The report also covers the application of management accounting techniques in financial reporting, producing financial reports, and interpreting data for a range of business activities. Furthermore, the report addresses budgeting, analyzing how organizations adapt management accounting systems to respond to financial problems, and evaluating planning tools used to improve financial performance and achieve sustainable success. The report utilizes cost cards to illustrate the differences between absorption and marginal costing, providing a clear understanding of their merits and demerits. It also includes calculations for cost of goods sold, cost of ending inventory, and profit using LIFO, FIFO, and AVCO methods. The report culminates with an analysis of how management accounting can help improve financial performance, offering valuable insights for students and professionals alike.

B12645

MANAGEMENT

ACCONTING

MANAGEMENT

ACCONTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

SECTION 1.....................................................................................................................................3

1.1 Explain management accounting and give the essential requirements of different types

of management accounting systems............................................................................................3

1.2 Explain different methods used for management accounting reporting...........................5

1.3 Evaluate the benefits of management accounting systems and their application within

an organizational context.............................................................................................................6

1.4 Critically evaluate how management accounting system and management accounting is

integrated within organizational process.....................................................................................7

SECTION 2.....................................................................................................................................7

2.1 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................7

(a) Prepare a cost card using absorption costing and marginal costing..............................8

(b) Explain the potential merits and demerits of the both methods....................................9

2.2 Accurately apply a range of management accounting techniques and produce a financial

reporting document....................................................................................................................11

2.3 Produce financial reports that accurately apply and interpret data for a range of business

activities.....................................................................................................................................16

(a) High-low method calculate fixed cost and variable cost and estimate the expenses...........16

(c) Calculation of cost of goods sold, cost of ending inventory and profit using LIFO, FIFO

AND AVCO..............................................................................................................................17

PROJECT 2...................................................................................................................................19

Section 3........................................................................................................................................19

3.1 Define and explain the purpose of budget and prepare different budget.............................19

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

SECTION 1.....................................................................................................................................3

1.1 Explain management accounting and give the essential requirements of different types

of management accounting systems............................................................................................3

1.2 Explain different methods used for management accounting reporting...........................5

1.3 Evaluate the benefits of management accounting systems and their application within

an organizational context.............................................................................................................6

1.4 Critically evaluate how management accounting system and management accounting is

integrated within organizational process.....................................................................................7

SECTION 2.....................................................................................................................................7

2.1 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................7

(a) Prepare a cost card using absorption costing and marginal costing..............................8

(b) Explain the potential merits and demerits of the both methods....................................9

2.2 Accurately apply a range of management accounting techniques and produce a financial

reporting document....................................................................................................................11

2.3 Produce financial reports that accurately apply and interpret data for a range of business

activities.....................................................................................................................................16

(a) High-low method calculate fixed cost and variable cost and estimate the expenses...........16

(c) Calculation of cost of goods sold, cost of ending inventory and profit using LIFO, FIFO

AND AVCO..............................................................................................................................17

PROJECT 2...................................................................................................................................19

Section 3........................................................................................................................................19

3.1 Define and explain the purpose of budget and prepare different budget.............................19

3.1.1 Prepare a schedule of expected cash collections for September...................................20

3.1.2 Prepare a schedule of expected cash disbursements for merchandise inventory

purchases in September.........................................................................................................20

3.1.3 Prepare a cash budget for September............................................................................20

Section 4........................................................................................................................................21

4.1 Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................21

4.2 Analyze how management accounting can help to improve the financial performance of

both companies to achieve sustainable success.........................................................................22

4.3 Evaluate the planning tools used in management accounting to reduce the financial

problems to achieve success..........................................................................................................22

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................24

3.1.2 Prepare a schedule of expected cash disbursements for merchandise inventory

purchases in September.........................................................................................................20

3.1.3 Prepare a cash budget for September............................................................................20

Section 4........................................................................................................................................21

4.1 Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................21

4.2 Analyze how management accounting can help to improve the financial performance of

both companies to achieve sustainable success.........................................................................22

4.3 Evaluate the planning tools used in management accounting to reduce the financial

problems to achieve success..........................................................................................................22

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a method to help company achieve objective and restrict cost over the

business. Management accounting involves presenting accounting data to management to make

their decisions. It helps in improving efficiency and achieving organizational goals.

This project report consists of two parts; part1 and 2. First part focuses on understanding of

management accounting system; essential requirement of different types of management

accounting systems and methods for preparing management accounting report. Second part;

critically evaluate advantages and disadvantages of planning tools; use of different planning tools

and methods adopted by organizations to respond financial problems for attaining sustainable

success.

PART 1

SECTION 1

1.1 Explain management accounting and give the essential requirements of

different types of management accounting systems

Management Accounting: The field of managerial accounting is very wide. In this, future

trends are estimated by studying the past and present accounts of a business organization.

Thus, real-time and current study and analysis of accounts and accurate forecast of future

trends comes only in the field of managerial accounting (Malina, 2017).

Essential requirements of different types of management accounting systems:

Management accounting is the efficient tool for managers to analyze performance of the

company. Some of the essential requirements are discussed below:

Management accounting is a method to help company achieve objective and restrict cost over the

business. Management accounting involves presenting accounting data to management to make

their decisions. It helps in improving efficiency and achieving organizational goals.

This project report consists of two parts; part1 and 2. First part focuses on understanding of

management accounting system; essential requirement of different types of management

accounting systems and methods for preparing management accounting report. Second part;

critically evaluate advantages and disadvantages of planning tools; use of different planning tools

and methods adopted by organizations to respond financial problems for attaining sustainable

success.

PART 1

SECTION 1

1.1 Explain management accounting and give the essential requirements of

different types of management accounting systems

Management Accounting: The field of managerial accounting is very wide. In this, future

trends are estimated by studying the past and present accounts of a business organization.

Thus, real-time and current study and analysis of accounts and accurate forecast of future

trends comes only in the field of managerial accounting (Malina, 2017).

Essential requirements of different types of management accounting systems:

Management accounting is the efficient tool for managers to analyze performance of the

company. Some of the essential requirements are discussed below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Style: Management accounting system affects by the way manager follows

management styles. It is essentially required that accountants or managers should follow

certain management principal by defining how the information will be processed to get

desired outcome. There are two types of management styles; Autocratic and democratic.

Organization structure: This factor essentially required to know what type of

information is required to solve particular issue. It mainly depends on level of

organizational structure that what is the risk associated with particular level and what will

be the impact of solution on entire company. Organization structure can be two types:

Functional structure: Decision making is limited to only manager’s functional

level.

Flat structured: Critical decisions taken by managers on the basis of wide range

of data and information’s shown in report.

Information: There is a huge competition for acquiring precious information’s first by

all big organizations. It is the information which makes company responsive and alert for

future expectations of the customer and stakeholders. Information can be classified in

various ways according to essential requirement of the firm:

Sources: Accuracy and durability of information depends on the source from

where it acquired. Genuine source should be preferred to make decisions.

Relevancy: All information’s are not relevant for particular decisions. Hence

relevancy should be tested through sort listing process (Singhvi and

BODHANWALA, 2018).

Accuracy: Accuracy of information is important for error free planning and

decision making.

Reliability: Source is the main factor on which reliability of any information

exists. So authentic source is essentially required to get genuine information.

1.2 Explain different methods used for management accounting reporting

Methods used for management accounting reporting are discussed below:

management styles. It is essentially required that accountants or managers should follow

certain management principal by defining how the information will be processed to get

desired outcome. There are two types of management styles; Autocratic and democratic.

Organization structure: This factor essentially required to know what type of

information is required to solve particular issue. It mainly depends on level of

organizational structure that what is the risk associated with particular level and what will

be the impact of solution on entire company. Organization structure can be two types:

Functional structure: Decision making is limited to only manager’s functional

level.

Flat structured: Critical decisions taken by managers on the basis of wide range

of data and information’s shown in report.

Information: There is a huge competition for acquiring precious information’s first by

all big organizations. It is the information which makes company responsive and alert for

future expectations of the customer and stakeholders. Information can be classified in

various ways according to essential requirement of the firm:

Sources: Accuracy and durability of information depends on the source from

where it acquired. Genuine source should be preferred to make decisions.

Relevancy: All information’s are not relevant for particular decisions. Hence

relevancy should be tested through sort listing process (Singhvi and

BODHANWALA, 2018).

Accuracy: Accuracy of information is important for error free planning and

decision making.

Reliability: Source is the main factor on which reliability of any information

exists. So authentic source is essentially required to get genuine information.

1.2 Explain different methods used for management accounting reporting

Methods used for management accounting reporting are discussed below:

Cost Accounting System: Cost accounting is a special branch of general accounting

under which various expenses related to the production of a commodity or service are

accounted for in such a way that the total and per unit cost of the product or service to be

produced is known and the control and management The information and data required

for guidance can be obtained systematically by the information provided by the cost

accounting analysis and control is possible (Nørreklit, 2017).

Job Order Costing: Job costing refers to a specific costing method where various cost

accounting techniques are used to measure the cost of the product. When goods are

produced only against special orders, job costs are used by firms.

Process Costing: Process costing is a process by which we determine the cost of each

process at each stage of operation. If the product goes through several processes or steps,

the output of one process becomes the input of the next process, and to determine the cost

of each process, the process cost method is applied. It is generally used when units are to

be built, that too in a continuous flow.

Inventory management systems: One of the most important aspects of any business

model is inventory. A close tab on inventory movement can make or break your business

and that is why entrepreneurs always insist on effective inventory management. While

some business owners understand the importance and importance of tracking inventory

regularly, some fail to realize its importance, leaving their business with unseen cracks.

Price optimizing system: Pricing is the process of determining what a company will get

in return for its products. Pricing components are manufacturing cost, market,

competition, market position and product quality. Pricing is also an important influencing

factor in micro-economics price allocation theory. Pricing refers to setting monetary

value in a commodity or service. But in the broadest sense, pricing is the function and

process. Which is determined prior to the sale of the commodity and under which the

pricing objectives, price influencing factors, monetary value of the commodity, price

policies and anecdotes are determined.

under which various expenses related to the production of a commodity or service are

accounted for in such a way that the total and per unit cost of the product or service to be

produced is known and the control and management The information and data required

for guidance can be obtained systematically by the information provided by the cost

accounting analysis and control is possible (Nørreklit, 2017).

Job Order Costing: Job costing refers to a specific costing method where various cost

accounting techniques are used to measure the cost of the product. When goods are

produced only against special orders, job costs are used by firms.

Process Costing: Process costing is a process by which we determine the cost of each

process at each stage of operation. If the product goes through several processes or steps,

the output of one process becomes the input of the next process, and to determine the cost

of each process, the process cost method is applied. It is generally used when units are to

be built, that too in a continuous flow.

Inventory management systems: One of the most important aspects of any business

model is inventory. A close tab on inventory movement can make or break your business

and that is why entrepreneurs always insist on effective inventory management. While

some business owners understand the importance and importance of tracking inventory

regularly, some fail to realize its importance, leaving their business with unseen cracks.

Price optimizing system: Pricing is the process of determining what a company will get

in return for its products. Pricing components are manufacturing cost, market,

competition, market position and product quality. Pricing is also an important influencing

factor in micro-economics price allocation theory. Pricing refers to setting monetary

value in a commodity or service. But in the broadest sense, pricing is the function and

process. Which is determined prior to the sale of the commodity and under which the

pricing objectives, price influencing factors, monetary value of the commodity, price

policies and anecdotes are determined.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.3 Evaluate the benefits of management accounting systems and their

application within an organizational context

Management accounting system is essential for organizations development and decision

making. No organization could achieve its organizational objectives without applying

management accounting planning tools and methods. Some of the benefits and

application of management accounting systems are discussed below:

Relevance: Management accounting system provides relevant reports based on available

information. It makes possible for organizational manager to have judgment and make

decisions based on relevance of reports (Srithongrung, Ermasova and Yusuf, 2019).

Updated Information: Judgment on the basis of outdated information could impact

company negatively for long time. It is very dangerous for the company to analyze

market based on old information and data’s. Hence, management accounting provides

updated information which helps management to more responsive towards upcoming

events.

Reliability: Management accountings produces reliable result and make reports based on

accurate information. Reliability is essential to achieve business goals and objectives

without any failure.

Understandable: It is management accounting system which makes it possible to

understand report by non accounting background managers.

Accuracy: Accuracy of report is based on sources of extracting information.

Management accounting through its effective helps management to extract relevant

information for producing accurate report for top management.

1.4 Critically evaluate how management accounting system and

management accounting is integrated within organizational process

Effectiveness of any management accounting system is depends on its tools and methods.

Outdated tools fail to give desired outcome and needs to be updated with the changes in

application within an organizational context

Management accounting system is essential for organizations development and decision

making. No organization could achieve its organizational objectives without applying

management accounting planning tools and methods. Some of the benefits and

application of management accounting systems are discussed below:

Relevance: Management accounting system provides relevant reports based on available

information. It makes possible for organizational manager to have judgment and make

decisions based on relevance of reports (Srithongrung, Ermasova and Yusuf, 2019).

Updated Information: Judgment on the basis of outdated information could impact

company negatively for long time. It is very dangerous for the company to analyze

market based on old information and data’s. Hence, management accounting provides

updated information which helps management to more responsive towards upcoming

events.

Reliability: Management accountings produces reliable result and make reports based on

accurate information. Reliability is essential to achieve business goals and objectives

without any failure.

Understandable: It is management accounting system which makes it possible to

understand report by non accounting background managers.

Accuracy: Accuracy of report is based on sources of extracting information.

Management accounting through its effective helps management to extract relevant

information for producing accurate report for top management.

1.4 Critically evaluate how management accounting system and

management accounting is integrated within organizational process

Effectiveness of any management accounting system is depends on its tools and methods.

Outdated tools fail to give desired outcome and needs to be updated with the changes in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

industry. Some of the importance of different methods of reporting for the success of

organization is discussed below:

Clarity: Doubt should not have a place in the report, and the reader of the sentiment

should understand it in the same sense in which it is written. The one who writes the

report must be clear.

Accuracy of facts: Accuracy of facts is very important for a good report. All facts and

information should be included in the report, because decisions are taken on the basis of

these facts, if the facts given in the report will be inaccurate, then the management and

organization face a lot of trouble.

Precision: In a good report, the author's objectives of writing the report should be

completely clear i.e. manager should know why he is writing the report. Its research,

analysis and recommendations are directed towards this purpose (Quinn and Oliveira,

2018).

Clear recommendations: If a recommendation is to be made at the end of the report, it

should be objective as well. The recommendation should be made only after thorough

research and analysis. There should be no personal interest of the author in the report. All

the recommendations proposed by him should be complete and clear so that he can reach

his objectives.

SECTION 2

2.1 Calculate costs using appropriate techniques of cost analysis to prepare

an income statement using marginal and absorption costs

(a) Prepare a cost card using absorption costing and marginal costing

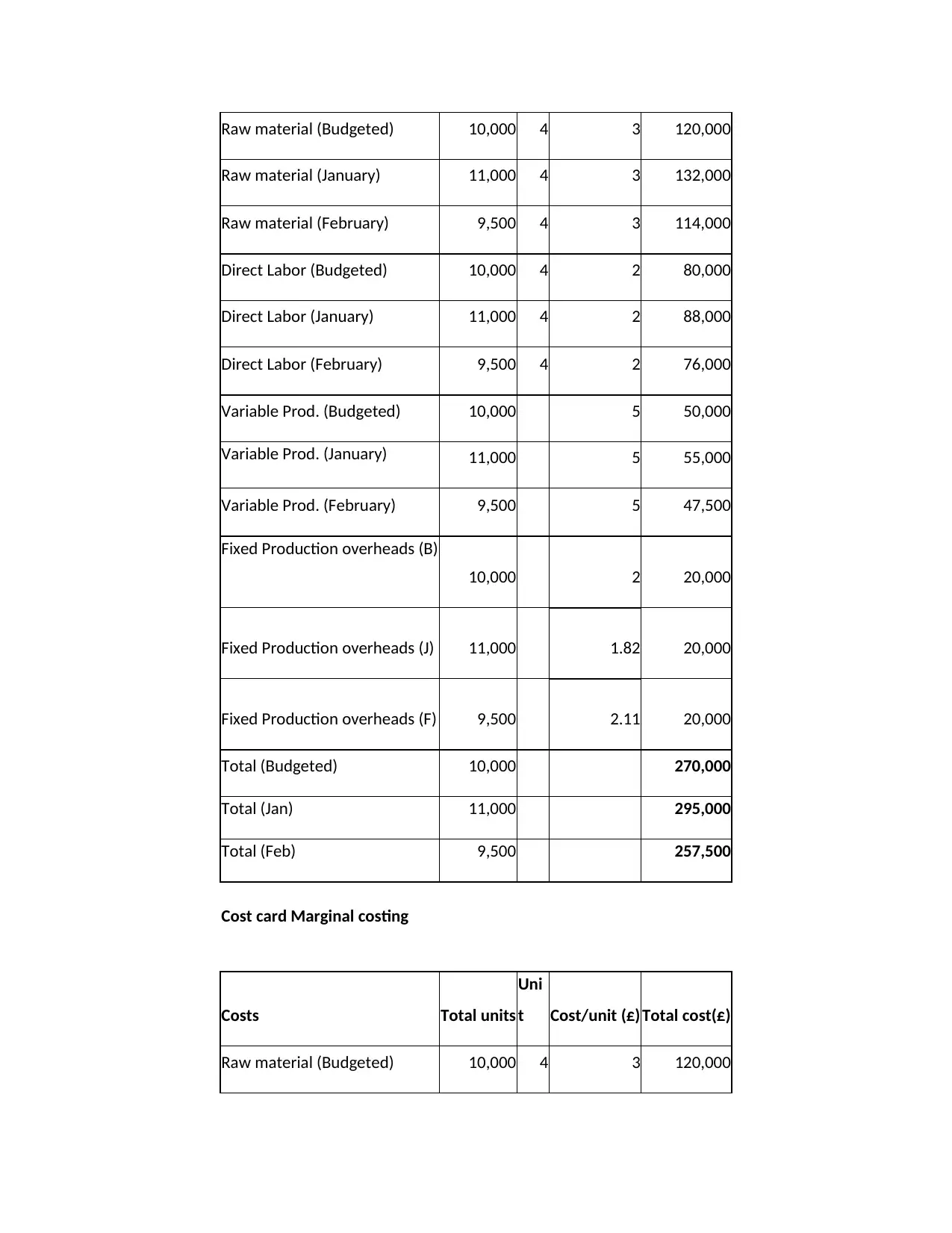

Cost card absorption costing

Costs Total units

Uni

t Cost/unit (£) Total cost(£)

organization is discussed below:

Clarity: Doubt should not have a place in the report, and the reader of the sentiment

should understand it in the same sense in which it is written. The one who writes the

report must be clear.

Accuracy of facts: Accuracy of facts is very important for a good report. All facts and

information should be included in the report, because decisions are taken on the basis of

these facts, if the facts given in the report will be inaccurate, then the management and

organization face a lot of trouble.

Precision: In a good report, the author's objectives of writing the report should be

completely clear i.e. manager should know why he is writing the report. Its research,

analysis and recommendations are directed towards this purpose (Quinn and Oliveira,

2018).

Clear recommendations: If a recommendation is to be made at the end of the report, it

should be objective as well. The recommendation should be made only after thorough

research and analysis. There should be no personal interest of the author in the report. All

the recommendations proposed by him should be complete and clear so that he can reach

his objectives.

SECTION 2

2.1 Calculate costs using appropriate techniques of cost analysis to prepare

an income statement using marginal and absorption costs

(a) Prepare a cost card using absorption costing and marginal costing

Cost card absorption costing

Costs Total units

Uni

t Cost/unit (£) Total cost(£)

Raw material (Budgeted) 10,000 4 3 120,000

Raw material (January) 11,000 4 3 132,000

Raw material (February) 9,500 4 3 114,000

Direct Labor (Budgeted) 10,000 4 2 80,000

Direct Labor (January) 11,000 4 2 88,000

Direct Labor (February) 9,500 4 2 76,000

Variable Prod. (Budgeted) 10,000 5 50,000

Variable Prod. (January) 11,000 5 55,000

Variable Prod. (February) 9,500 5 47,500

Fixed Production overheads (B)

10,000 2 20,000

Fixed Production overheads (J) 11,000 1.82 20,000

Fixed Production overheads (F) 9,500 2.11 20,000

Total (Budgeted) 10,000 270,000

Total (Jan) 11,000 295,000

Total (Feb) 9,500 257,500

Cost card Marginal costing

Costs Total units

Uni

t Cost/unit (£) Total cost(£)

Raw material (Budgeted) 10,000 4 3 120,000

Raw material (January) 11,000 4 3 132,000

Raw material (February) 9,500 4 3 114,000

Direct Labor (Budgeted) 10,000 4 2 80,000

Direct Labor (January) 11,000 4 2 88,000

Direct Labor (February) 9,500 4 2 76,000

Variable Prod. (Budgeted) 10,000 5 50,000

Variable Prod. (January) 11,000 5 55,000

Variable Prod. (February) 9,500 5 47,500

Fixed Production overheads (B)

10,000 2 20,000

Fixed Production overheads (J) 11,000 1.82 20,000

Fixed Production overheads (F) 9,500 2.11 20,000

Total (Budgeted) 10,000 270,000

Total (Jan) 11,000 295,000

Total (Feb) 9,500 257,500

Cost card Marginal costing

Costs Total units

Uni

t Cost/unit (£) Total cost(£)

Raw material (Budgeted) 10,000 4 3 120,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

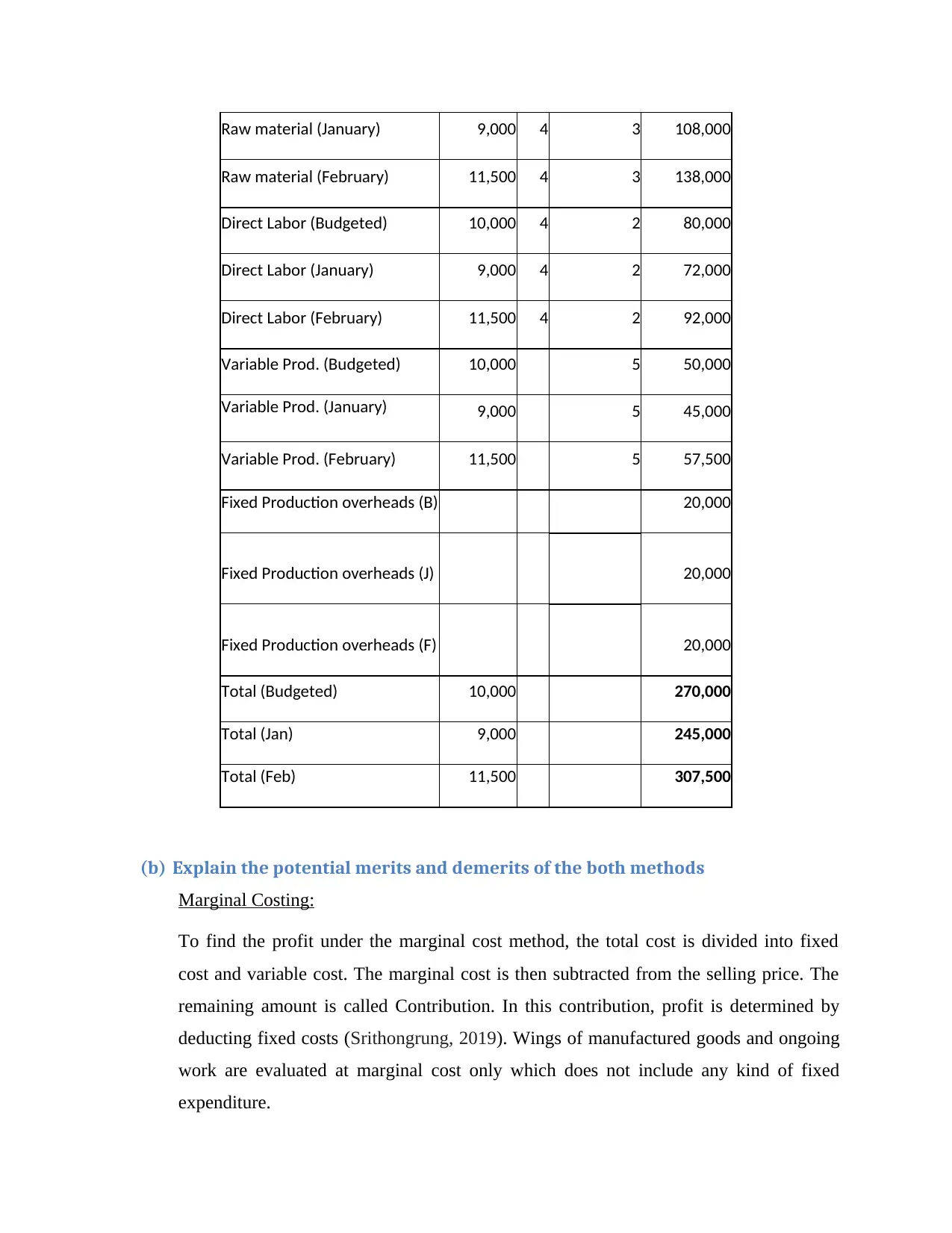

Raw material (January) 9,000 4 3 108,000

Raw material (February) 11,500 4 3 138,000

Direct Labor (Budgeted) 10,000 4 2 80,000

Direct Labor (January) 9,000 4 2 72,000

Direct Labor (February) 11,500 4 2 92,000

Variable Prod. (Budgeted) 10,000 5 50,000

Variable Prod. (January) 9,000 5 45,000

Variable Prod. (February) 11,500 5 57,500

Fixed Production overheads (B) 20,000

Fixed Production overheads (J) 20,000

Fixed Production overheads (F) 20,000

Total (Budgeted) 10,000 270,000

Total (Jan) 9,000 245,000

Total (Feb) 11,500 307,500

(b) Explain the potential merits and demerits of the both methods

Marginal Costing:

To find the profit under the marginal cost method, the total cost is divided into fixed

cost and variable cost. The marginal cost is then subtracted from the selling price. The

remaining amount is called Contribution. In this contribution, profit is determined by

deducting fixed costs (Srithongrung, 2019). Wings of manufactured goods and ongoing

work are evaluated at marginal cost only which does not include any kind of fixed

expenditure.

Raw material (February) 11,500 4 3 138,000

Direct Labor (Budgeted) 10,000 4 2 80,000

Direct Labor (January) 9,000 4 2 72,000

Direct Labor (February) 11,500 4 2 92,000

Variable Prod. (Budgeted) 10,000 5 50,000

Variable Prod. (January) 9,000 5 45,000

Variable Prod. (February) 11,500 5 57,500

Fixed Production overheads (B) 20,000

Fixed Production overheads (J) 20,000

Fixed Production overheads (F) 20,000

Total (Budgeted) 10,000 270,000

Total (Jan) 9,000 245,000

Total (Feb) 11,500 307,500

(b) Explain the potential merits and demerits of the both methods

Marginal Costing:

To find the profit under the marginal cost method, the total cost is divided into fixed

cost and variable cost. The marginal cost is then subtracted from the selling price. The

remaining amount is called Contribution. In this contribution, profit is determined by

deducting fixed costs (Srithongrung, 2019). Wings of manufactured goods and ongoing

work are evaluated at marginal cost only which does not include any kind of fixed

expenditure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Merits of marginal costing:

1. Easy to understand - The marginal cost method is simple to understand. Its process is

easy because it does not include permanent costs, which does not pose a problem of

their exploitation. This can be combined with proof cost.

2. Cost Comparison - In this method, the stock is evaluated at the marginal cost.

Therefore, a part of the permanent costs are not carried over to the next period in the

form of a stock. Hence the costs and benefits are not neutralized and the comparison

of costs is made meaningful (Schaltegger and Burritt, 2017).

3. Study the effects of changes on cost - production or sales volume or sales mix and

how changes in production or sales methods will have an impact on costs and

benefits, can be studied by this method. And help in decision making.

4. Profit planning - Through this method, the study of the relationship between profit

and the components affecting it can be understood well by techniques like break-

even point, profit volume ratio etc. This makes the managers easy in budgeting and

profit planning. Due to this, future profit-plans can be made and they can be

evaluated.

Demerits:

There is a possibility of wrong decisions with Marginal Cost.

Low Evaluation of Wing

Marginal Cost is ignored by Managers.

This is the short term (Alawattage and Wickramasinghe, 2018).

It is used in limited industries.

Some of these assumptions are wrong.

Absorption costing

In this costing system; only production related costs are preferred. All costs incurred at

the time of production are absorbed on the basis of per unit price bases (Adler, 2018).

Merits:

1. Easy to understand - The marginal cost method is simple to understand. Its process is

easy because it does not include permanent costs, which does not pose a problem of

their exploitation. This can be combined with proof cost.

2. Cost Comparison - In this method, the stock is evaluated at the marginal cost.

Therefore, a part of the permanent costs are not carried over to the next period in the

form of a stock. Hence the costs and benefits are not neutralized and the comparison

of costs is made meaningful (Schaltegger and Burritt, 2017).

3. Study the effects of changes on cost - production or sales volume or sales mix and

how changes in production or sales methods will have an impact on costs and

benefits, can be studied by this method. And help in decision making.

4. Profit planning - Through this method, the study of the relationship between profit

and the components affecting it can be understood well by techniques like break-

even point, profit volume ratio etc. This makes the managers easy in budgeting and

profit planning. Due to this, future profit-plans can be made and they can be

evaluated.

Demerits:

There is a possibility of wrong decisions with Marginal Cost.

Low Evaluation of Wing

Marginal Cost is ignored by Managers.

This is the short term (Alawattage and Wickramasinghe, 2018).

It is used in limited industries.

Some of these assumptions are wrong.

Absorption costing

In this costing system; only production related costs are preferred. All costs incurred at

the time of production are absorbed on the basis of per unit price bases (Adler, 2018).

Merits:

It is compliant with GAAP and has an advantage of only requirement of Internal

Revenue Service reporting (Jones, and et.al., 2018).

It considers all costs of productions both variable and fixed expenses.

Calculation of net profit gives more accurate value as compared to marginal

costing method.

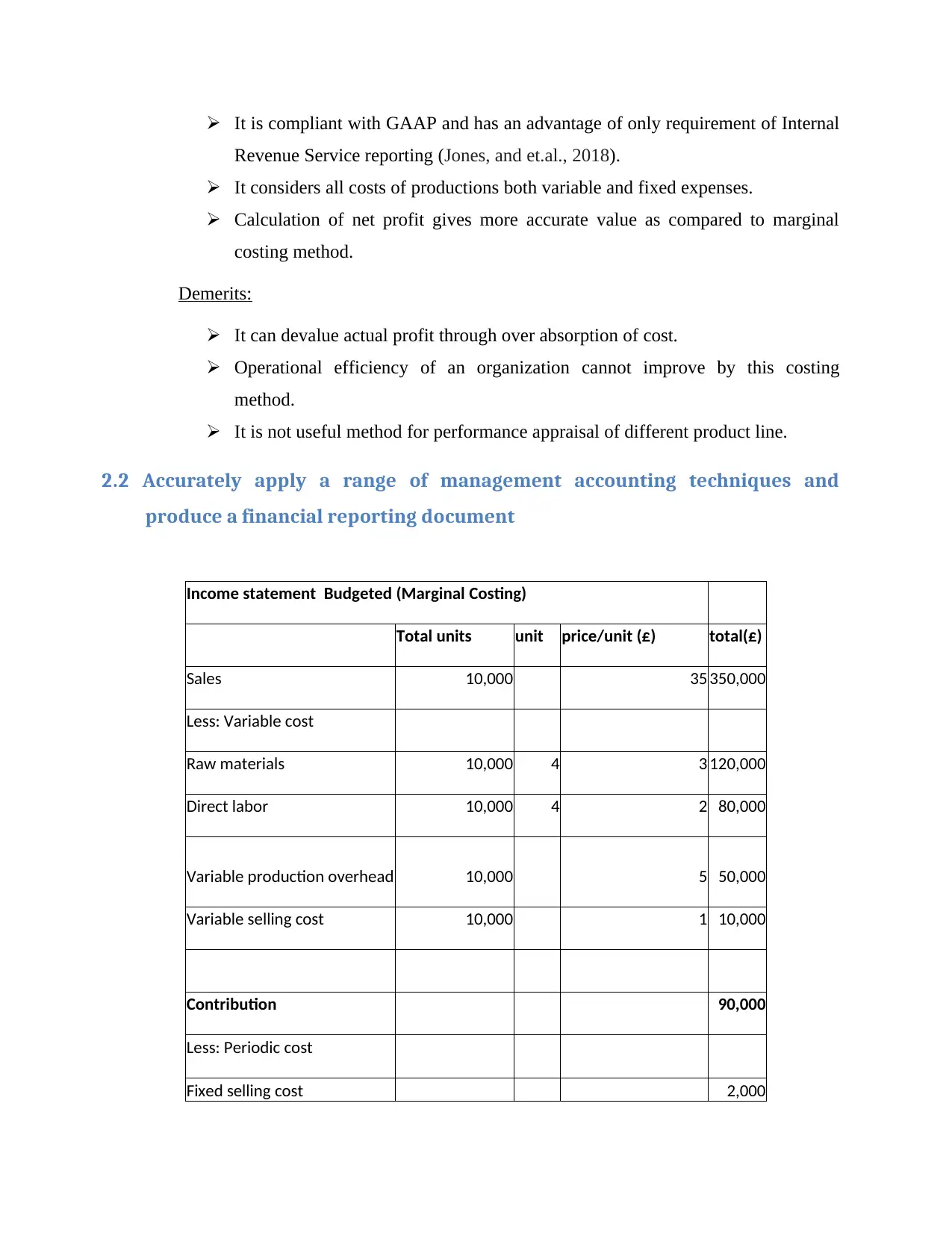

Demerits:

It can devalue actual profit through over absorption of cost.

Operational efficiency of an organization cannot improve by this costing

method.

It is not useful method for performance appraisal of different product line.

2.2 Accurately apply a range of management accounting techniques and

produce a financial reporting document

Income statement Budgeted (Marginal Costing)

Total units unit price/unit (£) total(£)

Sales 10,000 35 350,000

Less: Variable cost

Raw materials 10,000 4 3 120,000

Direct labor 10,000 4 2 80,000

Variable production overhead 10,000 5 50,000

Variable selling cost 10,000 1 10,000

Contribution 90,000

Less: Periodic cost

Fixed selling cost 2,000

Revenue Service reporting (Jones, and et.al., 2018).

It considers all costs of productions both variable and fixed expenses.

Calculation of net profit gives more accurate value as compared to marginal

costing method.

Demerits:

It can devalue actual profit through over absorption of cost.

Operational efficiency of an organization cannot improve by this costing

method.

It is not useful method for performance appraisal of different product line.

2.2 Accurately apply a range of management accounting techniques and

produce a financial reporting document

Income statement Budgeted (Marginal Costing)

Total units unit price/unit (£) total(£)

Sales 10,000 35 350,000

Less: Variable cost

Raw materials 10,000 4 3 120,000

Direct labor 10,000 4 2 80,000

Variable production overhead 10,000 5 50,000

Variable selling cost 10,000 1 10,000

Contribution 90,000

Less: Periodic cost

Fixed selling cost 2,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.