Management Accounting Report: Cost Analysis of Jeffrey & Son's

VerifiedAdded on 2019/12/04

|22

|6570

|35

Report

AI Summary

This management accounting report provides a comprehensive analysis of cost accounting and budgeting principles, using the case of Jeffrey & Son's, a manufacturing company. The report begins by classifying different types of costs, including fixed, variable, and semi-variable costs, and explaining their impact on production. It then demonstrates the calculation of unit and total job costs using job costing methods, followed by the calculation and analysis of the 'cost of exquisite' using machine hours and direct labor hours for overhead allocation. The report then analyzes cost reports, identifies performance indicators for improvement, and suggests methods for cost reduction, value enhancement, and quality improvement. Furthermore, the report covers the nature and purpose of budgeting, the selection of appropriate budgeting methods, and the preparation of production, material purchase, and cash budgets. Finally, it includes variance calculations, identification of causes, recommendations for corrective actions, and an operating statement reconciling budgeted and actual results, concluding with a report to management.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1.1 Classification of different types of Costs.........................................................................1

1.2 Calculation of unit cost and total job cost........................................................................2

1.3 Calculation of Cost of Exquisite.......................................................................................4

1.4 Analysis of Cost of Exquisite...........................................................................................6

TASK 2............................................................................................................................................6

2.1 Analysis of cost report......................................................................................................6

2.2 Performance indicators which used to identify areas for potential improvements..........8

2.3 Ways to reduce costs, enhance value and quality.............................................................9

TASK 3..........................................................................................................................................10

3.1 Nature and Purpose of Budgeting and Budgeting Process.............................................10

3.2 Selection of appropriate budgeting methods .................................................................11

3.3 Preparation of Production and Material Purchase budgets.............................................12

3.4 Preparation of Cash Budget............................................................................................13

TASK 4..........................................................................................................................................14

4.1 Calculation of variances, identification of possible cause and recommendations for

corrective actions..................................................................................................................14

4.2 Operating statement reconciling budgeted and actual results........................................17

4.3 Report the finding to management.................................................................................18

CONCLUSION..............................................................................................................................18

REFERENCES .............................................................................................................................19

INTRODUCTION...........................................................................................................................1

1.1 Classification of different types of Costs.........................................................................1

1.2 Calculation of unit cost and total job cost........................................................................2

1.3 Calculation of Cost of Exquisite.......................................................................................4

1.4 Analysis of Cost of Exquisite...........................................................................................6

TASK 2............................................................................................................................................6

2.1 Analysis of cost report......................................................................................................6

2.2 Performance indicators which used to identify areas for potential improvements..........8

2.3 Ways to reduce costs, enhance value and quality.............................................................9

TASK 3..........................................................................................................................................10

3.1 Nature and Purpose of Budgeting and Budgeting Process.............................................10

3.2 Selection of appropriate budgeting methods .................................................................11

3.3 Preparation of Production and Material Purchase budgets.............................................12

3.4 Preparation of Cash Budget............................................................................................13

TASK 4..........................................................................................................................................14

4.1 Calculation of variances, identification of possible cause and recommendations for

corrective actions..................................................................................................................14

4.2 Operating statement reconciling budgeted and actual results........................................17

4.3 Report the finding to management.................................................................................18

CONCLUSION..............................................................................................................................18

REFERENCES .............................................................................................................................19

INTRODUCTION

Management accounting is the process of developing management reports, accounts and

projects that help in gathering short and timely based statistical and financial information which

are required by management to make short term and day to day decision making (Ahrens and

Chapman, 2006). In production process, all the expenses that are incurred by the organization are

known as cost of production. The cost of production includes different types of cost like direct

material, direct labour and overheads that can be fixed or variable. The systematic and timely

planning is typical in the complex businesses (Ax and Bjørnenak, 2005). Management

Accounting is required in an organization to recognize the financial situation of it. It provides

data, modifies it, analyses and interprets the data as well as serves as a means of communication

to the organization. In this research report, all tasks are solved through keeping in mind the case

of Jeffrey and Son's, manufacturing company.

1.1 Classification of different types of Costs

Cost Accounting is the methodology which is helpful in measuring and analyzing costs

associated with the goods, production and projects so that the correct amounts can be reported in

the financial statements (Brown, Evans III and Moser 2009). There are various kinds of costs

such as fixed costs, variable costs, semi variable costs, marginal costs etc.

The Main elements of cost are Material, labor and expenses which are incurred during

production process. The non production costs are fixed cost, opportunity cost and avoidable cost.

Direct costs are those costs which are directly related to the production process whereas indirect

costs are those, which are not directly related to the production (Burns, Hopper and Yazdifar,

2004). Presenting here the brief description of the types of costs that are incurred by this

manufacturing company.l Fixed Costs : These are the costs that do not change with the change in the output. Fixed

costs remain same in totality and changes in per unit. Example of fixed costs are cost of

building, rent of premises or insurance bills etc.l Variable Costs : These are the costs that changes with the change in output. They remain

same in per unit and fluctuates in totality. Examples of variable costs are material, labor

and overheads.l Semi Variable Costs : These costs are neither completely fixed nor completely variable.

They contain elements of fixed costs and partially variable costs. For example labor

Page 1 of 23

Management accounting is the process of developing management reports, accounts and

projects that help in gathering short and timely based statistical and financial information which

are required by management to make short term and day to day decision making (Ahrens and

Chapman, 2006). In production process, all the expenses that are incurred by the organization are

known as cost of production. The cost of production includes different types of cost like direct

material, direct labour and overheads that can be fixed or variable. The systematic and timely

planning is typical in the complex businesses (Ax and Bjørnenak, 2005). Management

Accounting is required in an organization to recognize the financial situation of it. It provides

data, modifies it, analyses and interprets the data as well as serves as a means of communication

to the organization. In this research report, all tasks are solved through keeping in mind the case

of Jeffrey and Son's, manufacturing company.

1.1 Classification of different types of Costs

Cost Accounting is the methodology which is helpful in measuring and analyzing costs

associated with the goods, production and projects so that the correct amounts can be reported in

the financial statements (Brown, Evans III and Moser 2009). There are various kinds of costs

such as fixed costs, variable costs, semi variable costs, marginal costs etc.

The Main elements of cost are Material, labor and expenses which are incurred during

production process. The non production costs are fixed cost, opportunity cost and avoidable cost.

Direct costs are those costs which are directly related to the production process whereas indirect

costs are those, which are not directly related to the production (Burns, Hopper and Yazdifar,

2004). Presenting here the brief description of the types of costs that are incurred by this

manufacturing company.l Fixed Costs : These are the costs that do not change with the change in the output. Fixed

costs remain same in totality and changes in per unit. Example of fixed costs are cost of

building, rent of premises or insurance bills etc.l Variable Costs : These are the costs that changes with the change in output. They remain

same in per unit and fluctuates in totality. Examples of variable costs are material, labor

and overheads.l Semi Variable Costs : These costs are neither completely fixed nor completely variable.

They contain elements of fixed costs and partially variable costs. For example labor

Page 1 of 23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which can be a semi variable cost . If a firm produces more units of vehicle, it needs more

workers, that is its variable cost. However, if it does not produce vehicles, it still may

need the workers for any other work in the factory, that is its fixed cost.

l Marginal Costs: Cost incurred for producing an extra unit of production. For example if

the total cost of 5 units is 5000, and the total cost of 6 units is 6500. The marginal cost of

the 6th unit is 1500.

Basis of

classification

Type of Costs

Elements On the basis of elements of costs, there are three types of costs such as

material, labour and overhead costs (Burritt and Saka, 2006). The

material and labour cost is variable in nature whereas the overhead cost

can variable or fixed.

Function All the costs of business is divided into production costs, administration

costs, finance costs, selling costs, distribution costs and research and

development costs. Production costs are also of two types direct

production costs and indirect production costs (Chapman, et.al., 2006).

Examples of direct production costs are direct manufacturing costs,

direct raw material and direct labour costs. Indirect production costs

include salaries of supervisors, production heads, technical and planning

staff etc.

Nature On the basis of nature, costs are classified into direct and indirect costs.

Direct costs include direct material, direct labour and other direct

expenses. Indirect costs are those costs that affect the production

indirectly such as selling expenses, distribution and advertisement

expenses etc.

Behaviour On the basis of behaviour, there are three types of costs that is variable,

semi-variable and fixed cost (Davila and Foster, 2005). Variable costs

changes with the change in production but fixed costs remain constant.

Semi variable costs has both elements of variable and fixed costs.

Page 2 of 23

workers, that is its variable cost. However, if it does not produce vehicles, it still may

need the workers for any other work in the factory, that is its fixed cost.

l Marginal Costs: Cost incurred for producing an extra unit of production. For example if

the total cost of 5 units is 5000, and the total cost of 6 units is 6500. The marginal cost of

the 6th unit is 1500.

Basis of

classification

Type of Costs

Elements On the basis of elements of costs, there are three types of costs such as

material, labour and overhead costs (Burritt and Saka, 2006). The

material and labour cost is variable in nature whereas the overhead cost

can variable or fixed.

Function All the costs of business is divided into production costs, administration

costs, finance costs, selling costs, distribution costs and research and

development costs. Production costs are also of two types direct

production costs and indirect production costs (Chapman, et.al., 2006).

Examples of direct production costs are direct manufacturing costs,

direct raw material and direct labour costs. Indirect production costs

include salaries of supervisors, production heads, technical and planning

staff etc.

Nature On the basis of nature, costs are classified into direct and indirect costs.

Direct costs include direct material, direct labour and other direct

expenses. Indirect costs are those costs that affect the production

indirectly such as selling expenses, distribution and advertisement

expenses etc.

Behaviour On the basis of behaviour, there are three types of costs that is variable,

semi-variable and fixed cost (Davila and Foster, 2005). Variable costs

changes with the change in production but fixed costs remain constant.

Semi variable costs has both elements of variable and fixed costs.

Page 2 of 23

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

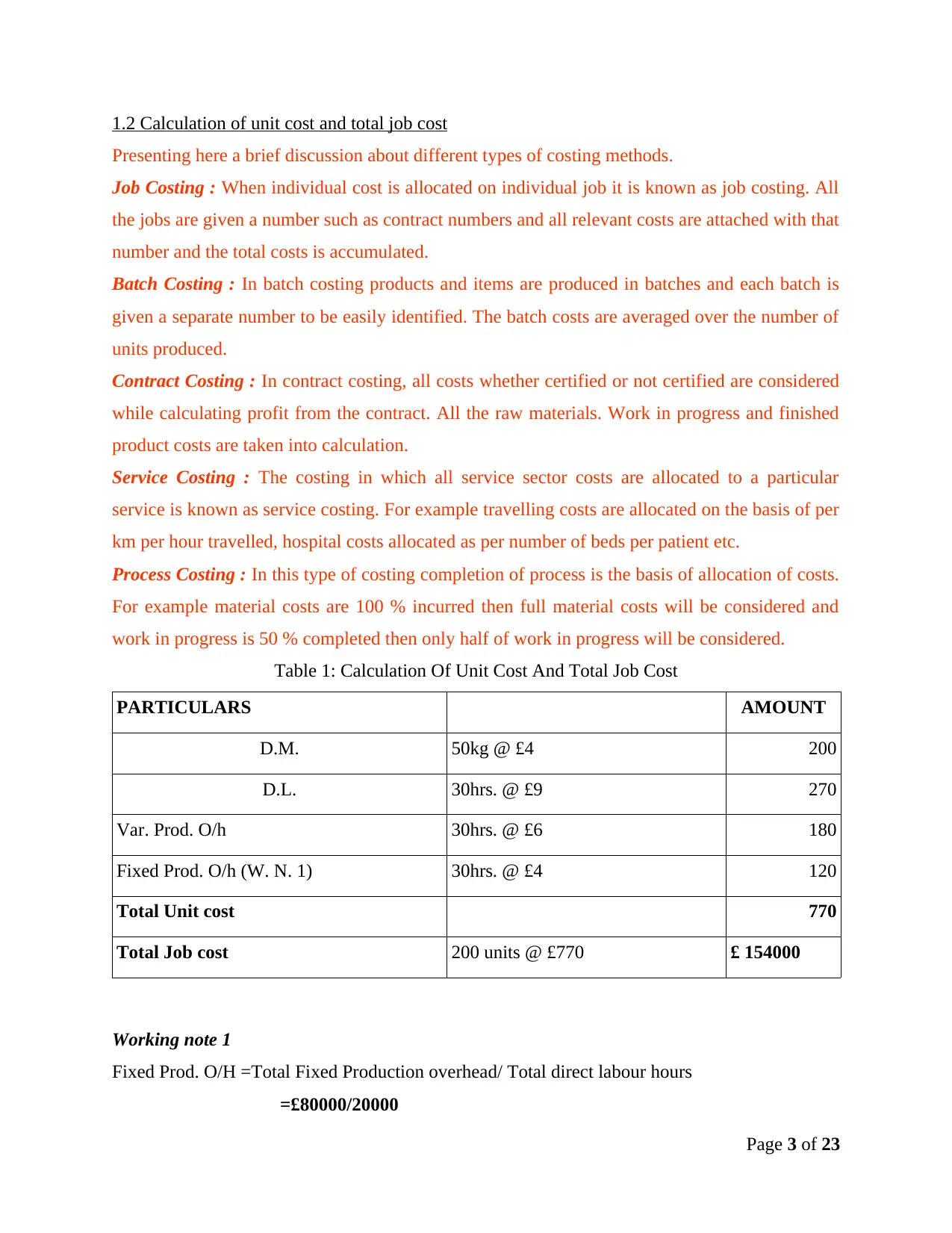

1.2 Calculation of unit cost and total job cost

Presenting here a brief discussion about different types of costing methods.

Job Costing : When individual cost is allocated on individual job it is known as job costing. All

the jobs are given a number such as contract numbers and all relevant costs are attached with that

number and the total costs is accumulated.

Batch Costing : In batch costing products and items are produced in batches and each batch is

given a separate number to be easily identified. The batch costs are averaged over the number of

units produced.

Contract Costing : In contract costing, all costs whether certified or not certified are considered

while calculating profit from the contract. All the raw materials. Work in progress and finished

product costs are taken into calculation.

Service Costing : The costing in which all service sector costs are allocated to a particular

service is known as service costing. For example travelling costs are allocated on the basis of per

km per hour travelled, hospital costs allocated as per number of beds per patient etc.

Process Costing : In this type of costing completion of process is the basis of allocation of costs.

For example material costs are 100 % incurred then full material costs will be considered and

work in progress is 50 % completed then only half of work in progress will be considered.

Table 1: Calculation Of Unit Cost And Total Job Cost

PARTICULARS AMOUNT

D.M. 50kg @ £4 200

D.L. 30hrs. @ £9 270

Var. Prod. O/h 30hrs. @ £6 180

Fixed Prod. O/h (W. N. 1) 30hrs. @ £4 120

Total Unit cost 770

Total Job cost 200 units @ £770 £ 154000

Working note 1

Fixed Prod. O/H =Total Fixed Production overhead/ Total direct labour hours

=£80000/20000

Page 3 of 23

Presenting here a brief discussion about different types of costing methods.

Job Costing : When individual cost is allocated on individual job it is known as job costing. All

the jobs are given a number such as contract numbers and all relevant costs are attached with that

number and the total costs is accumulated.

Batch Costing : In batch costing products and items are produced in batches and each batch is

given a separate number to be easily identified. The batch costs are averaged over the number of

units produced.

Contract Costing : In contract costing, all costs whether certified or not certified are considered

while calculating profit from the contract. All the raw materials. Work in progress and finished

product costs are taken into calculation.

Service Costing : The costing in which all service sector costs are allocated to a particular

service is known as service costing. For example travelling costs are allocated on the basis of per

km per hour travelled, hospital costs allocated as per number of beds per patient etc.

Process Costing : In this type of costing completion of process is the basis of allocation of costs.

For example material costs are 100 % incurred then full material costs will be considered and

work in progress is 50 % completed then only half of work in progress will be considered.

Table 1: Calculation Of Unit Cost And Total Job Cost

PARTICULARS AMOUNT

D.M. 50kg @ £4 200

D.L. 30hrs. @ £9 270

Var. Prod. O/h 30hrs. @ £6 180

Fixed Prod. O/h (W. N. 1) 30hrs. @ £4 120

Total Unit cost 770

Total Job cost 200 units @ £770 £ 154000

Working note 1

Fixed Prod. O/H =Total Fixed Production overhead/ Total direct labour hours

=£80000/20000

Page 3 of 23

=£4

1. In the given case of Jeffrey & Son's Ltd. The cost data have been provided by the

company for Job 444, that are used above to calculate the unit and total job cost. Since

the fixed production overheads are given in totality and the unit cost is per unit so

manager have calculated the Fixed overhead per unit as per working note 1. After adding

all the elements of cost i.e. direct material, direct labour, variable overheads and fixed

overheads, unit cost is identified. And by multiplying the unit cost with no. of units, total

job cost was calculated.

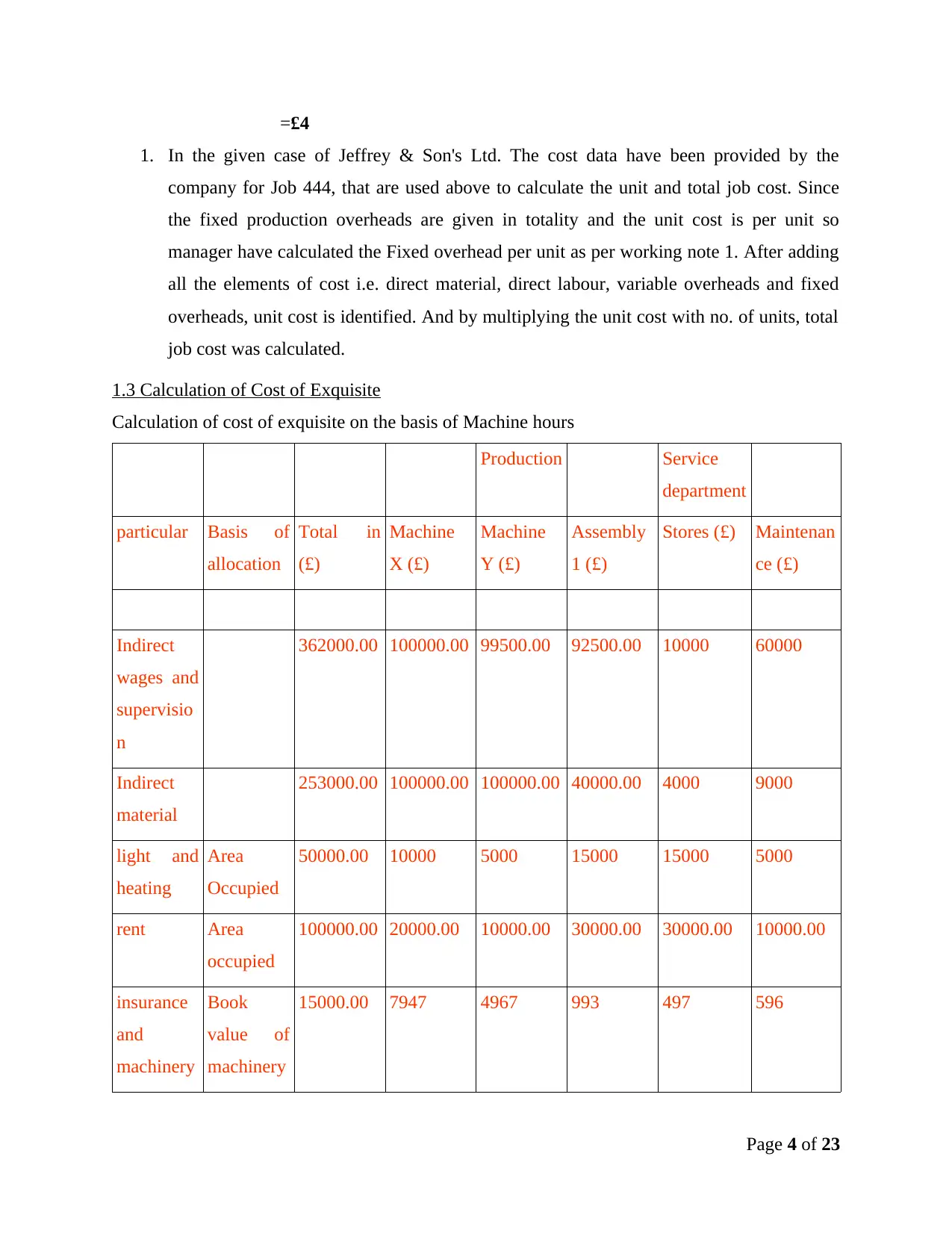

1.3 Calculation of Cost of Exquisite

Calculation of cost of exquisite on the basis of Machine hours

Production Service

department

particular Basis of

allocation

Total in

(£)

Machine

X (£)

Machine

Y (£)

Assembly

1 (£)

Stores (£) Maintenan

ce (£)

Indirect

wages and

supervisio

n

362000.00 100000.00 99500.00 92500.00 10000 60000

Indirect

material

253000.00 100000.00 100000.00 40000.00 4000 9000

light and

heating

Area

Occupied

50000.00 10000 5000 15000 15000 5000

rent Area

occupied

100000.00 20000.00 10000.00 30000.00 30000.00 10000.00

insurance

and

machinery

Book

value of

machinery

15000.00 7947 4967 993 497 596

Page 4 of 23

1. In the given case of Jeffrey & Son's Ltd. The cost data have been provided by the

company for Job 444, that are used above to calculate the unit and total job cost. Since

the fixed production overheads are given in totality and the unit cost is per unit so

manager have calculated the Fixed overhead per unit as per working note 1. After adding

all the elements of cost i.e. direct material, direct labour, variable overheads and fixed

overheads, unit cost is identified. And by multiplying the unit cost with no. of units, total

job cost was calculated.

1.3 Calculation of Cost of Exquisite

Calculation of cost of exquisite on the basis of Machine hours

Production Service

department

particular Basis of

allocation

Total in

(£)

Machine

X (£)

Machine

Y (£)

Assembly

1 (£)

Stores (£) Maintenan

ce (£)

Indirect

wages and

supervisio

n

362000.00 100000.00 99500.00 92500.00 10000 60000

Indirect

material

253000.00 100000.00 100000.00 40000.00 4000 9000

light and

heating

Area

Occupied

50000.00 10000 5000 15000 15000 5000

rent Area

occupied

100000.00 20000.00 10000.00 30000.00 30000.00 10000.00

insurance

and

machinery

Book

value of

machinery

15000.00 7947 4967 993 497 596

Page 4 of 23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

depreciati

on

Book

value of

machinery

150000.00 79740 49669 9934 4967 5960

Insurance

of building

Area

occupied

25000.00 5000.00 2500.00 7500.00 7500.00 2500.00

salaries of

work

manageme

nt

No. of

employees

80000.00 24000.00 16000.00 24000.00 8000.00 8000.00

Total cost 1035000 346417 287636 219927 79964 10156

Particular Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 346417 287636 219927

Stores Direct material 39982 29987 9995

Maintenance Machine hours 48507 32338 20211

Total 434906 349961 250133

c) Overhead absorption rate for each of the production department X, Y and assembly

Overhead absorption rate = Fixed overhead/ machine hours

Overhead absorption rate for department X

= 434906/80000

= £5.44

Overhead absorption rate for department Y

= 349960/60000

= £5.83

Page 5 of 23

on

Book

value of

machinery

150000.00 79740 49669 9934 4967 5960

Insurance

of building

Area

occupied

25000.00 5000.00 2500.00 7500.00 7500.00 2500.00

salaries of

work

manageme

nt

No. of

employees

80000.00 24000.00 16000.00 24000.00 8000.00 8000.00

Total cost 1035000 346417 287636 219927 79964 10156

Particular Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 346417 287636 219927

Stores Direct material 39982 29987 9995

Maintenance Machine hours 48507 32338 20211

Total 434906 349961 250133

c) Overhead absorption rate for each of the production department X, Y and assembly

Overhead absorption rate = Fixed overhead/ machine hours

Overhead absorption rate for department X

= 434906/80000

= £5.44

Overhead absorption rate for department Y

= 349960/60000

= £5.83

Page 5 of 23

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

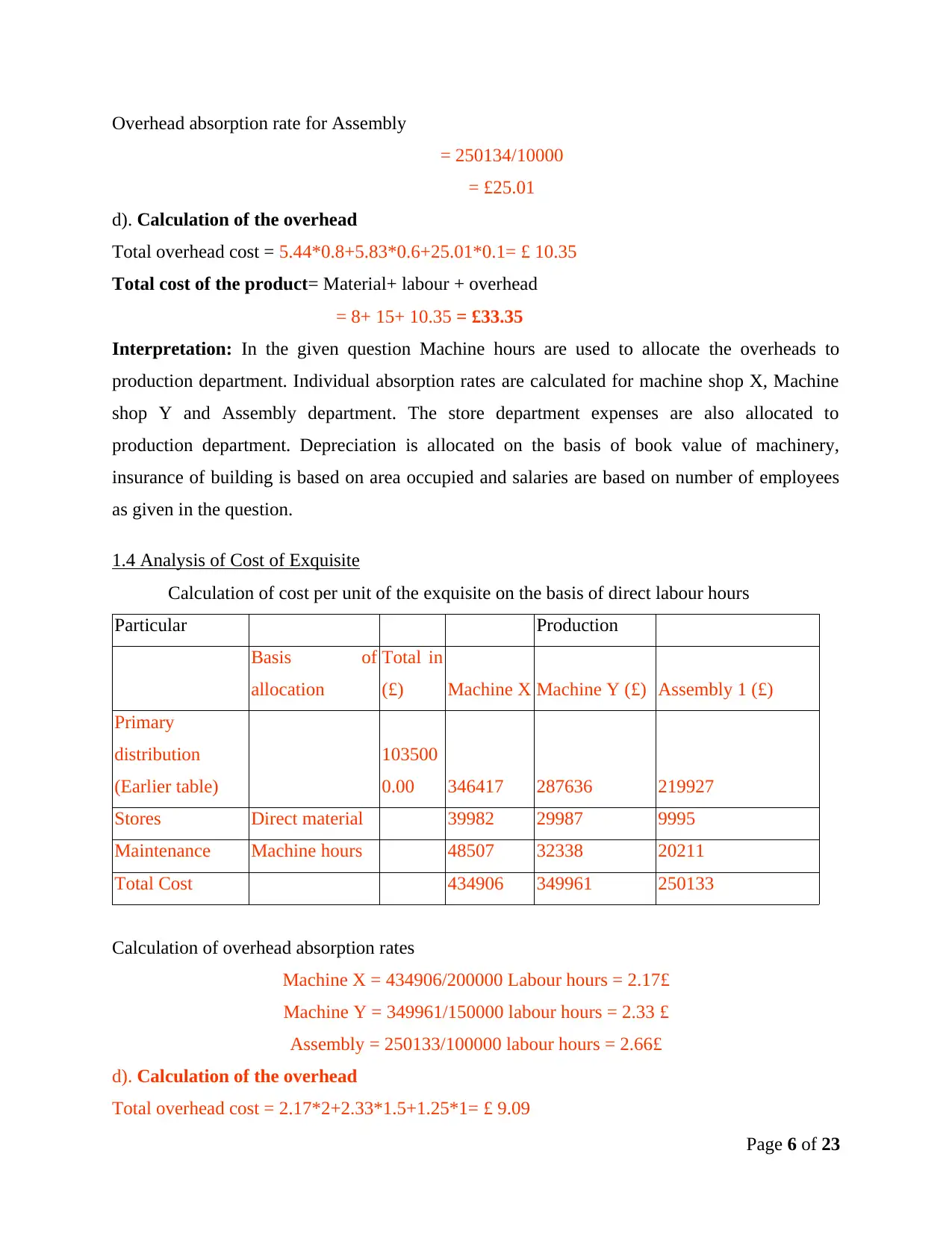

Overhead absorption rate for Assembly

= 250134/10000

= £25.01

d). Calculation of the overhead

Total overhead cost = 5.44*0.8+5.83*0.6+25.01*0.1= £ 10.35

Total cost of the product= Material+ labour + overhead

= 8+ 15+ 10.35 = £33.35

Interpretation: In the given question Machine hours are used to allocate the overheads to

production department. Individual absorption rates are calculated for machine shop X, Machine

shop Y and Assembly department. The store department expenses are also allocated to

production department. Depreciation is allocated on the basis of book value of machinery,

insurance of building is based on area occupied and salaries are based on number of employees

as given in the question.

1.4 Analysis of Cost of Exquisite

Calculation of cost per unit of the exquisite on the basis of direct labour hours

Particular Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 346417 287636 219927

Stores Direct material 39982 29987 9995

Maintenance Machine hours 48507 32338 20211

Total Cost 434906 349961 250133

Calculation of overhead absorption rates

Machine X = 434906/200000 Labour hours = 2.17£

Machine Y = 349961/150000 labour hours = 2.33 £

Assembly = 250133/100000 labour hours = 2.66£

d). Calculation of the overhead

Total overhead cost = 2.17*2+2.33*1.5+1.25*1= £ 9.09

Page 6 of 23

= 250134/10000

= £25.01

d). Calculation of the overhead

Total overhead cost = 5.44*0.8+5.83*0.6+25.01*0.1= £ 10.35

Total cost of the product= Material+ labour + overhead

= 8+ 15+ 10.35 = £33.35

Interpretation: In the given question Machine hours are used to allocate the overheads to

production department. Individual absorption rates are calculated for machine shop X, Machine

shop Y and Assembly department. The store department expenses are also allocated to

production department. Depreciation is allocated on the basis of book value of machinery,

insurance of building is based on area occupied and salaries are based on number of employees

as given in the question.

1.4 Analysis of Cost of Exquisite

Calculation of cost per unit of the exquisite on the basis of direct labour hours

Particular Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 346417 287636 219927

Stores Direct material 39982 29987 9995

Maintenance Machine hours 48507 32338 20211

Total Cost 434906 349961 250133

Calculation of overhead absorption rates

Machine X = 434906/200000 Labour hours = 2.17£

Machine Y = 349961/150000 labour hours = 2.33 £

Assembly = 250133/100000 labour hours = 2.66£

d). Calculation of the overhead

Total overhead cost = 2.17*2+2.33*1.5+1.25*1= £ 9.09

Page 6 of 23

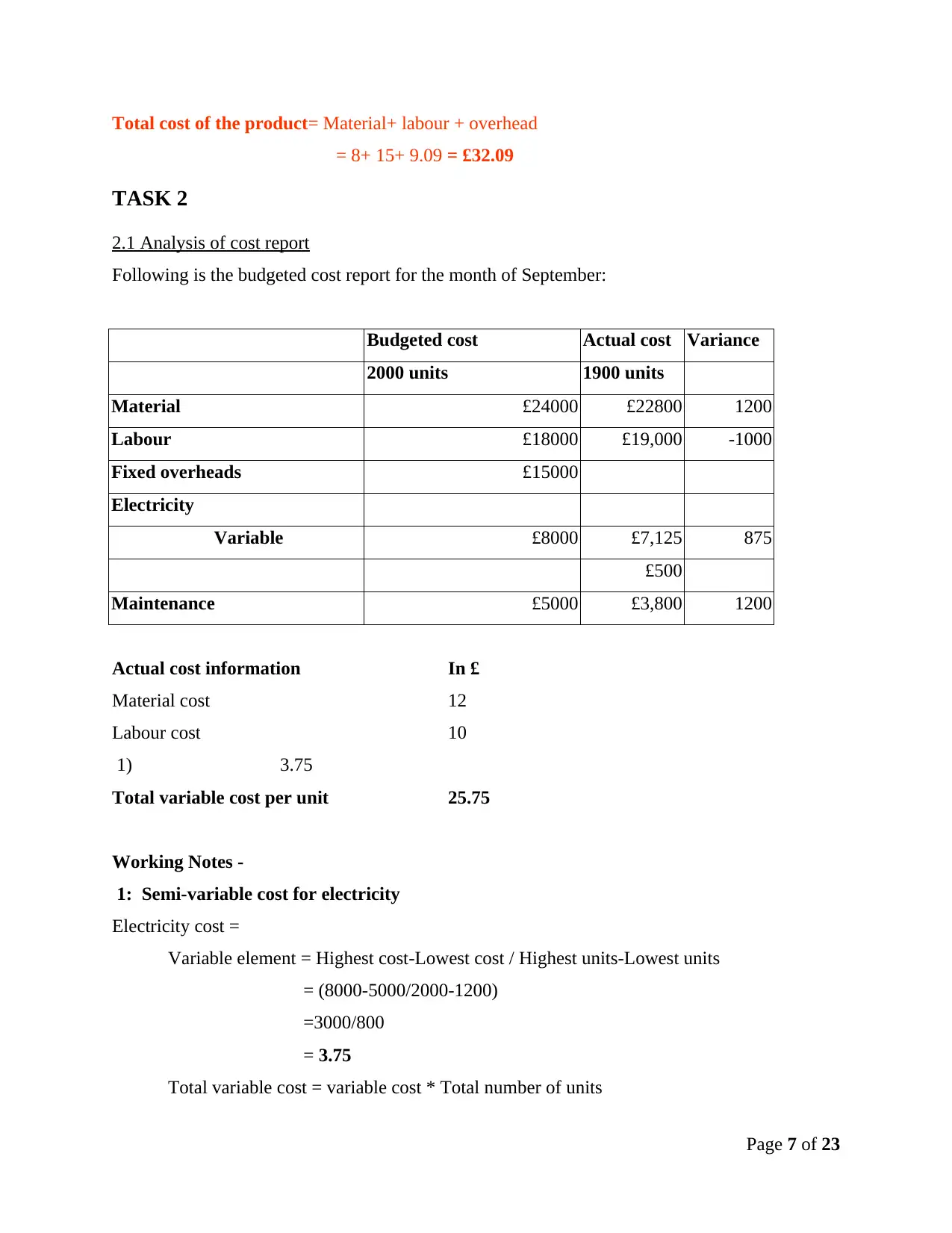

Total cost of the product= Material+ labour + overhead

= 8+ 15+ 9.09 = £32.09

TASK 2

2.1 Analysis of cost report

Following is the budgeted cost report for the month of September:

Budgeted cost Actual cost Variance

2000 units 1900 units

Material £24000 £22800 1200

Labour £18000 £19,000 -1000

Fixed overheads £15000

Electricity

Variable £8000 £7,125 875

£500

Maintenance £5000 £3,800 1200

Actual cost information In £

Material cost 12

Labour cost 10

1) 3.75

Total variable cost per unit 25.75

Working Notes -

1: Semi-variable cost for electricity

Electricity cost =

Variable element = Highest cost-Lowest cost / Highest units-Lowest units

= (8000-5000/2000-1200)

=3000/800

= 3.75

Total variable cost = variable cost * Total number of units

Page 7 of 23

= 8+ 15+ 9.09 = £32.09

TASK 2

2.1 Analysis of cost report

Following is the budgeted cost report for the month of September:

Budgeted cost Actual cost Variance

2000 units 1900 units

Material £24000 £22800 1200

Labour £18000 £19,000 -1000

Fixed overheads £15000

Electricity

Variable £8000 £7,125 875

£500

Maintenance £5000 £3,800 1200

Actual cost information In £

Material cost 12

Labour cost 10

1) 3.75

Total variable cost per unit 25.75

Working Notes -

1: Semi-variable cost for electricity

Electricity cost =

Variable element = Highest cost-Lowest cost / Highest units-Lowest units

= (8000-5000/2000-1200)

=3000/800

= 3.75

Total variable cost = variable cost * Total number of units

Page 7 of 23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 3.75*2000

= 7500

Total fixed cost = Total cost – Variable cost

= 8000 – 7500

= 500

Working Note 2 : Maintenance cost

It is provided that cost increases by 1000 for each 500 units produced.

Actual units produced = 1900

Maintenance cost for 1900 units = 1000/500*1900

= 3800

2.2 Performance indicators which used to identify areas for potential improvements

Performance indicators are the parameters for measuring company's current performance.

These help in identify that how effectively the company is achieving its objectives

(Hirsch, 2000). These are the set of measures which are used by company for gauging its

performance in terms of meeting the organisational goals and objectives. These are varied in

different organisations, and depend on the work of company. These are also known as “key

success indicators” because it help in making decisions. There are various performance

indicators which can use to identify areas for the potential improvement. They are as follows:

Sales – Sales is an important performance indicator for company. Total number of unit sold by

company in specific time period could be taken as a measure. Measurement of sales could

be done on the basis of region wise sales, sales in a month or year, sales of individual

product, etc. Sales could be also measured on the basis of booking of products, number of

orders and sales qualified leads (Reid, 2002). These measurements help company in

identifying its objectives and goals. Further, it also helps in identifying organisation's current

position as compare to target.

Finance – This is another important indicator for company. Finance is related with every activity

of business in both ways directly and indirectly. There are many factors which show the

performance of company (Kastantin, 2005). These include revenue, expenses, profits and

operating margin. All above factors are interdependence on each other. If, expenses are

Page 8 of 23

= 7500

Total fixed cost = Total cost – Variable cost

= 8000 – 7500

= 500

Working Note 2 : Maintenance cost

It is provided that cost increases by 1000 for each 500 units produced.

Actual units produced = 1900

Maintenance cost for 1900 units = 1000/500*1900

= 3800

2.2 Performance indicators which used to identify areas for potential improvements

Performance indicators are the parameters for measuring company's current performance.

These help in identify that how effectively the company is achieving its objectives

(Hirsch, 2000). These are the set of measures which are used by company for gauging its

performance in terms of meeting the organisational goals and objectives. These are varied in

different organisations, and depend on the work of company. These are also known as “key

success indicators” because it help in making decisions. There are various performance

indicators which can use to identify areas for the potential improvement. They are as follows:

Sales – Sales is an important performance indicator for company. Total number of unit sold by

company in specific time period could be taken as a measure. Measurement of sales could

be done on the basis of region wise sales, sales in a month or year, sales of individual

product, etc. Sales could be also measured on the basis of booking of products, number of

orders and sales qualified leads (Reid, 2002). These measurements help company in

identifying its objectives and goals. Further, it also helps in identifying organisation's current

position as compare to target.

Finance – This is another important indicator for company. Finance is related with every activity

of business in both ways directly and indirectly. There are many factors which show the

performance of company (Kastantin, 2005). These include revenue, expenses, profits and

operating margin. All above factors are interdependence on each other. If, expenses are

Page 8 of 23

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increased then it directly impact on the profit of firm. Higher revenue and profit show about

the good performance of company.

Human resources – Human resources are the main part of company because they are the

operators of every activity of business. Good performance of human resources helps

company in improving its own performance as well. This performance can be measured by

identifying satisfaction level of employees as well as the level of employee turnover.

Positive result of such elements shows effective performance of the organisation.

Manufacturing – This is a combination of huge activity which is used to produce final product.

Manufacturing also helps in measuring the performance of business. For measuring the

manufacturing performance of company, some areas need to be focused such as number of

unit manufactured, number of defects and manufacturing times etc. (Shim, and et.al., 2008).

If, defects in product are increased then, this will show bad performance of the business.

2.3 Ways to reduce costs, enhance value and quality

Every organisation wants to reduce its extra cost and increases its product and service

quality (Vanderbeck, 2012). For reducing cost, company has to follow many aspects on the daily

basis. Company should also focus on the style of working in order to enhance quality of products

and services. Organisation should mainly focus on material, labour, sales, energy and expenses.

Cost reduction technique helps company in achieving its objective and goals. Many times, there

is unwanted cost that is incurred during manufacturing and selling activity of business.

Following are the ways to reduce cost and enhance quality of the product: Inventory management – It is an important aspect of reducing cost and enhancing the

quality of work. Inventory management concerns with the raw materials. It also deals

with the time that is required for the arrangement of material (Kaimenaki and Cohen,

2011). For reducing cost, company should store raw material in sufficient quantity so that

requirement can fulfil on time. Company should also arrange warehouse facility for the

storage and focus on delivery practices such as Just-in-time. Company can use various

methods for the inventory management such as LIFO and FIFO. These helps company in

enhancing its work and product quality. Uses of new technologies – Jeffrey and Son's can improve its value and quality by using

new technologies. At the production level, company can use new machinery for the

automation of process and tools in order to reduce cost and improve quality (Hansen,

Page 9 of 23

the good performance of company.

Human resources – Human resources are the main part of company because they are the

operators of every activity of business. Good performance of human resources helps

company in improving its own performance as well. This performance can be measured by

identifying satisfaction level of employees as well as the level of employee turnover.

Positive result of such elements shows effective performance of the organisation.

Manufacturing – This is a combination of huge activity which is used to produce final product.

Manufacturing also helps in measuring the performance of business. For measuring the

manufacturing performance of company, some areas need to be focused such as number of

unit manufactured, number of defects and manufacturing times etc. (Shim, and et.al., 2008).

If, defects in product are increased then, this will show bad performance of the business.

2.3 Ways to reduce costs, enhance value and quality

Every organisation wants to reduce its extra cost and increases its product and service

quality (Vanderbeck, 2012). For reducing cost, company has to follow many aspects on the daily

basis. Company should also focus on the style of working in order to enhance quality of products

and services. Organisation should mainly focus on material, labour, sales, energy and expenses.

Cost reduction technique helps company in achieving its objective and goals. Many times, there

is unwanted cost that is incurred during manufacturing and selling activity of business.

Following are the ways to reduce cost and enhance quality of the product: Inventory management – It is an important aspect of reducing cost and enhancing the

quality of work. Inventory management concerns with the raw materials. It also deals

with the time that is required for the arrangement of material (Kaimenaki and Cohen,

2011). For reducing cost, company should store raw material in sufficient quantity so that

requirement can fulfil on time. Company should also arrange warehouse facility for the

storage and focus on delivery practices such as Just-in-time. Company can use various

methods for the inventory management such as LIFO and FIFO. These helps company in

enhancing its work and product quality. Uses of new technologies – Jeffrey and Son's can improve its value and quality by using

new technologies. At the production level, company can use new machinery for the

automation of process and tools in order to reduce cost and improve quality (Hansen,

Page 9 of 23

Mowen and Guan, 2007). Organisation can also use new technology in promotional

activity such as social media sites, emails and magazine.

Reduction in variation – This can be applied at any production process. Variation in

planned and actual work can become heavy cost to the company. This could be reduced

through product analysis and identification of common components (Kate-Riin , 2012).

Variation can also reduce by redesigning product. This helps organisation in keep control

over process and reduce prices. Effective reduction in variation also helps company in

improving efficiency of work and reducing the time of production.

TASK 3

3.1 Nature and Purpose of Budgeting and Budgeting Process

A budget is a plan for the prospective future incomes and expenses that will be occurred

in business. As time passes, actual expenditures and incomes are compared with the budgeted

figures. In case of any difference between these two, that difference is known as variance.

Budgetary control is the procedure to control the financial position of organisation (Kont, 2013).

It is the prime responsibility of managers to control costs in their budgets and to take corrective

actions for removing adverse variances. Budgets are used for many purposes which are discussed

here.

1. To control the income and expenditure of company.

2. To establish preferences and set targets in figures as well as reports.

3. To convert business goals into practical reality that provides guidance and co-

ordination.

4. To allocate resources and assign jobs to the managers and budget-holders.

5. To inform employees about the targets to be achieved.

6. To promote and motivate the staff.

7. To improve and enhance the efficiency and effectiveness of targets.

8. To monitor and observe performance.

In the systematic budget, managerial responsibilities are always clear and predefined. The

plan of action needs to be taken with the help of individual budgets. In case of results being

different from those expected, the plan is needed to be changed and other corrective actions are

necessary to be taken by company. In case of departures, prior approval from senior management

Page 10 of 23

activity such as social media sites, emails and magazine.

Reduction in variation – This can be applied at any production process. Variation in

planned and actual work can become heavy cost to the company. This could be reduced

through product analysis and identification of common components (Kate-Riin , 2012).

Variation can also reduce by redesigning product. This helps organisation in keep control

over process and reduce prices. Effective reduction in variation also helps company in

improving efficiency of work and reducing the time of production.

TASK 3

3.1 Nature and Purpose of Budgeting and Budgeting Process

A budget is a plan for the prospective future incomes and expenses that will be occurred

in business. As time passes, actual expenditures and incomes are compared with the budgeted

figures. In case of any difference between these two, that difference is known as variance.

Budgetary control is the procedure to control the financial position of organisation (Kont, 2013).

It is the prime responsibility of managers to control costs in their budgets and to take corrective

actions for removing adverse variances. Budgets are used for many purposes which are discussed

here.

1. To control the income and expenditure of company.

2. To establish preferences and set targets in figures as well as reports.

3. To convert business goals into practical reality that provides guidance and co-

ordination.

4. To allocate resources and assign jobs to the managers and budget-holders.

5. To inform employees about the targets to be achieved.

6. To promote and motivate the staff.

7. To improve and enhance the efficiency and effectiveness of targets.

8. To monitor and observe performance.

In the systematic budget, managerial responsibilities are always clear and predefined. The

plan of action needs to be taken with the help of individual budgets. In case of results being

different from those expected, the plan is needed to be changed and other corrective actions are

necessary to be taken by company. In case of departures, prior approval from senior management

Page 10 of 23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.