Financial Resource Management: Cost Analysis and Budgeting for Costa

VerifiedAdded on 2023/06/15

|13

|2945

|393

Report

AI Summary

This report provides a detailed analysis of managing financial resources, focusing on Costa as a case study. It includes calculations of various costs such as production cost, administrative expenses, prime cost, total cost, and sales & distribution expenses. The report further analyzes budgeting and forecasting, variance analysis (favorable and unfavorable), and flexible budgets with examples. Key financial terms like labor cost, customer retention rate, food average spends, food cost of sales ratio, and beverage cost of sales are explained with formulas and examples, offering a comprehensive overview of financial management principles and their practical application in a business context. Desklib offers a variety of solved assignments and resources for students.

MANAGING

FINANCIAL

RESOURCES

FINANCIAL

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................4

Task..................................................................................................................................................4

Question 1: Calculate the different costs for Costa................................................................4

Question 4 - Analyse the following with examples................................................................7

Question 6 : Explain the following terms with their formula and examples........................10

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Introduction......................................................................................................................................4

Task..................................................................................................................................................4

Question 1: Calculate the different costs for Costa................................................................4

Question 4 - Analyse the following with examples................................................................7

Question 6 : Explain the following terms with their formula and examples........................10

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Introduction

Monitoring sources of finance is the process of dealing with the complex and critical

difficulties that develop in an organization in relation to finance strategic decision making In this

evaluation, various kind of cost is follows includes computations for various expenditure in the

firm, as well as a pricing spreadsheet for the very same. The primary motive of this report is to

mainly focus on the financial resources so that the company can manage their operations. The

next portion of the evaluation delves into the various terminologies used in funding managing &

explains them with samples (Plaskova and et.al., 2020).

Task

Section A -

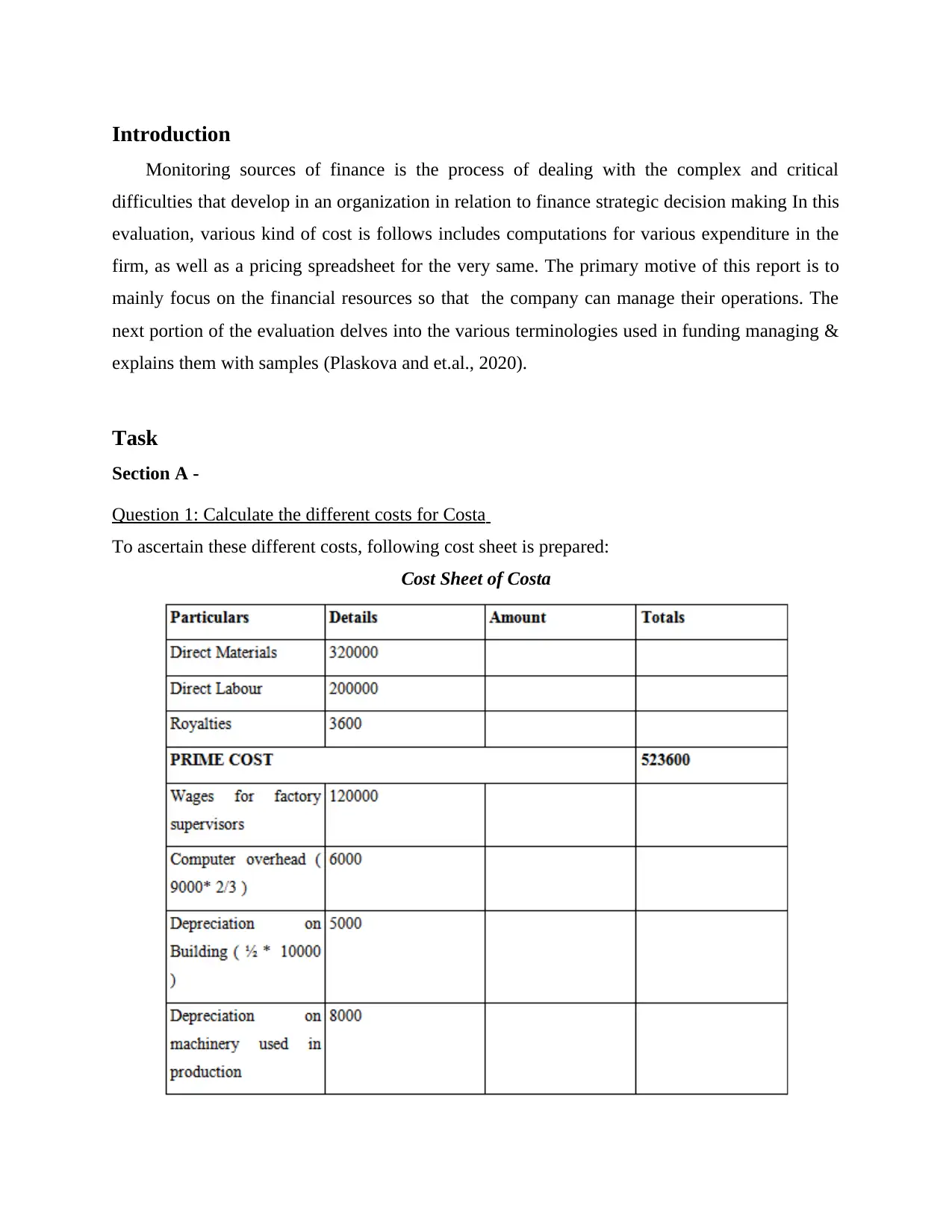

Question 1: Calculate the different costs for Costa

To ascertain these different costs, following cost sheet is prepared:

Cost Sheet of Costa

Monitoring sources of finance is the process of dealing with the complex and critical

difficulties that develop in an organization in relation to finance strategic decision making In this

evaluation, various kind of cost is follows includes computations for various expenditure in the

firm, as well as a pricing spreadsheet for the very same. The primary motive of this report is to

mainly focus on the financial resources so that the company can manage their operations. The

next portion of the evaluation delves into the various terminologies used in funding managing &

explains them with samples (Plaskova and et.al., 2020).

Task

Section A -

Question 1: Calculate the different costs for Costa

To ascertain these different costs, following cost sheet is prepared:

Cost Sheet of Costa

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

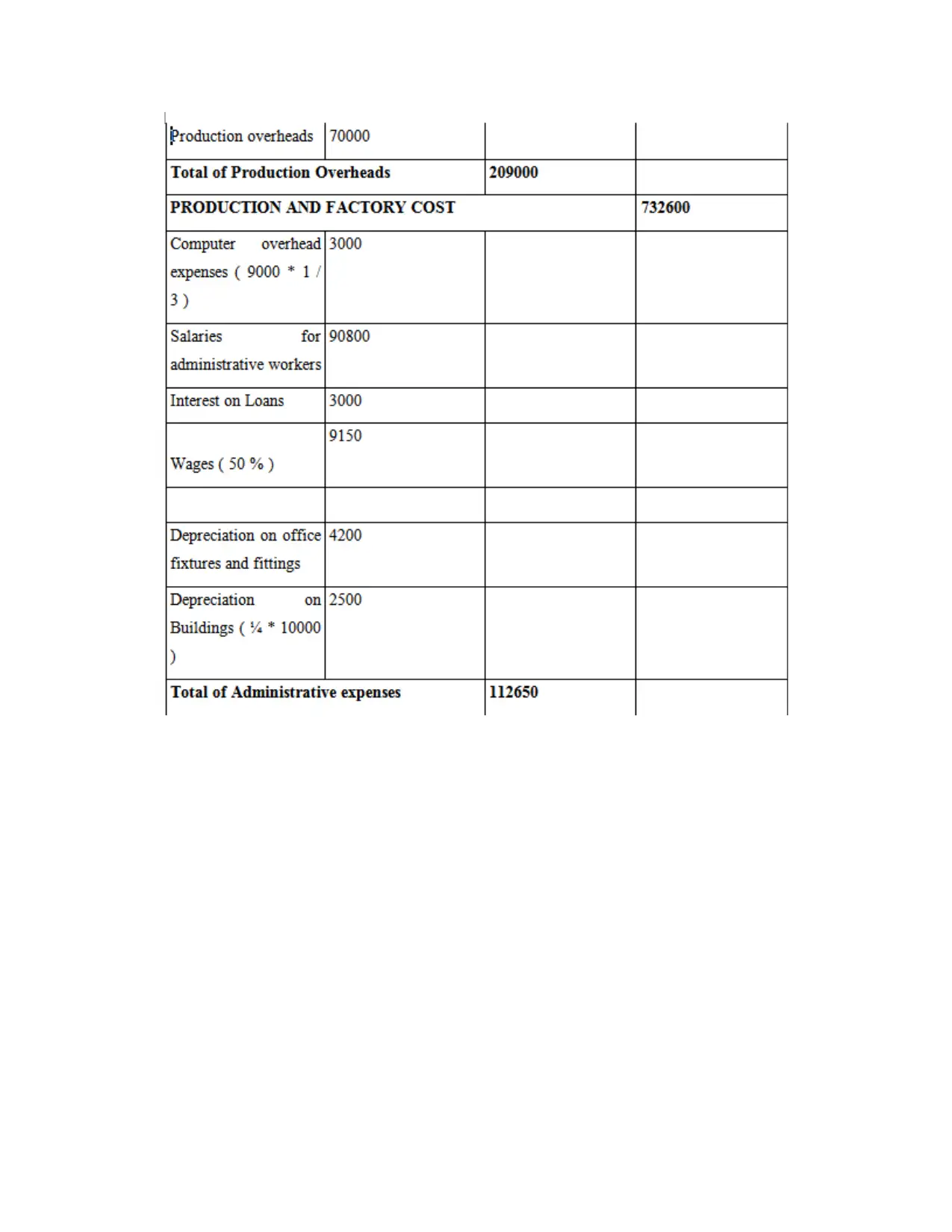

1. Production Cost - This cost mainly represents the specific cost which incurred by a

company as a result of the manufacture of products or services in order to generate more

revenue. The following table shows the manufacturing and factory cost computed for

cost, which is $ 732600 (Mishra, 2021).

2. Administrative expenses - The context of administrative expenses which is considered as

the "business costs" that to expenditure incurred by the organisation that aren't even

directly connected to the company's primary operations. This cost is determined as shown

in the table above. Costa's administrative costs are $ 112650.

3. Prime Cost – Prime cost is considered as the entire cost of production that comprises the

price of raw materials as well as the cost of labour. Costa's prime cost, which is $

523600, is estimated accordingly (Panov and Larionova, 2021).

4. Total Cost - The overall price of company is the totality of all expenses made by the

company in its various activities to generate an outcome, sell & redistribute its goods &

services to various customers. The Costa has a total cost of $ 886,600.

company as a result of the manufacture of products or services in order to generate more

revenue. The following table shows the manufacturing and factory cost computed for

cost, which is $ 732600 (Mishra, 2021).

2. Administrative expenses - The context of administrative expenses which is considered as

the "business costs" that to expenditure incurred by the organisation that aren't even

directly connected to the company's primary operations. This cost is determined as shown

in the table above. Costa's administrative costs are $ 112650.

3. Prime Cost – Prime cost is considered as the entire cost of production that comprises the

price of raw materials as well as the cost of labour. Costa's prime cost, which is $

523600, is estimated accordingly (Panov and Larionova, 2021).

4. Total Cost - The overall price of company is the totality of all expenses made by the

company in its various activities to generate an outcome, sell & redistribute its goods &

services to various customers. The Costa has a total cost of $ 886,600.

5. Sales & Distribution expenses - The phrase "operating costs" relates to a firm’s earnings

which aren't even directly related to the company's principal operations. As stated in the

table above, this cost is calculated. The administrative expenses for Costa are $ 112650.

SECTION B -

Question 4 - Analyse the following with examples

Budgeting & Forecasting

Budgeting is the process of making an intend to spend money in the near future. A budget is the

name for this appropriate spending strategy. Making a budget allows individuals or organisation

to determine ahead of time if they will have enough money to do what they needed to do or what

they might wish to do. If company require more money to achieve all they want to do, they may

use this planning approach to concentrate on overall expenditure and invest the money in the

issues that are important to them. A budget proposal is typically created for a fiscal year &

comprises information about anticipated sales and services organisation expenditures during that

time frame (Block, Hirt and Danielsen, 2018).

A corporation may choose very well how company require doing throughout the year by

using this investment situation & considered relevant can be compared to this unique projected

plan. The fundamental motive of these expenditures is to assist the endeavour approach through

planned objectives, scheduled asset assignments & the amount to which climatic change

influences the organisational ability to fulfil objectives (Chernov, 2020).

which aren't even directly related to the company's principal operations. As stated in the

table above, this cost is calculated. The administrative expenses for Costa are $ 112650.

SECTION B -

Question 4 - Analyse the following with examples

Budgeting & Forecasting

Budgeting is the process of making an intend to spend money in the near future. A budget is the

name for this appropriate spending strategy. Making a budget allows individuals or organisation

to determine ahead of time if they will have enough money to do what they needed to do or what

they might wish to do. If company require more money to achieve all they want to do, they may

use this planning approach to concentrate on overall expenditure and invest the money in the

issues that are important to them. A budget proposal is typically created for a fiscal year &

comprises information about anticipated sales and services organisation expenditures during that

time frame (Block, Hirt and Danielsen, 2018).

A corporation may choose very well how company require doing throughout the year by

using this investment situation & considered relevant can be compared to this unique projected

plan. The fundamental motive of these expenditures is to assist the endeavour approach through

planned objectives, scheduled asset assignments & the amount to which climatic change

influences the organisational ability to fulfil objectives (Chernov, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Forecasting is the assessment of possible future events. There is a requirement to prepare to

anticipate prospective actions for the firm subsequently on at the foundation planning phases.

Deals, development, price, resource purchase & financial needs of the firm are all included in

forecasts. Because the budget has a reasonable goal, the amount has considerable flexibility.

Budgeting and forecasting are often used indiscriminately or equated to the same thing (Planning

incorporates Anticipating). Regardless, there is a dividing line that separates. A budget is an

estimate of what will happen at an organizational level throughout the planning horizon, and it

typically includes important activities & consumptions. A prediction can be made for the long

term or for a specific period of time & it can be determined from a hierarchy or broad viewpoint

(Barr and McClellan, 2018).

A well-thought-out budget will provide significant outcomes for the government's key

agenda. Surprisingly, a temporary estimate is largely comprised of completed functionality &

day-to-day organisation requirements. There are various factors are involved such as Sales

budgets, production budgets, flexible budgets & other types of budgeting are examples of budget

(Plaskova and et. al., 2020).

Variance Analysis

In planning or executive accounting, variation analysis is an assessment of variations in

true behaviour vs. estimated or planned conduct. This is primarily concerned by how the contrast

between genuine & arranged practises affects company performance. Organisations may use

variance measure to appropriate understand current expenses & prepare for future expenditures.

Companies regularly do the Variance Analysis that is a quantitative approach of the differences

between planned and actual costs & earnings. Both earnings & expenses can be subjected to

variance analysis. Change is said to as 'Favourable' when actual outcomes are superior to planned

ones. Variation is said to as 'adverse' or 'unfavourable' when the appropriate consequences are

worse than the expected. Analyzing, for instances, the anticipated production costs was 150000,

but the reality production cost was 180000, indicating that variation which is unfavourable.

anticipate prospective actions for the firm subsequently on at the foundation planning phases.

Deals, development, price, resource purchase & financial needs of the firm are all included in

forecasts. Because the budget has a reasonable goal, the amount has considerable flexibility.

Budgeting and forecasting are often used indiscriminately or equated to the same thing (Planning

incorporates Anticipating). Regardless, there is a dividing line that separates. A budget is an

estimate of what will happen at an organizational level throughout the planning horizon, and it

typically includes important activities & consumptions. A prediction can be made for the long

term or for a specific period of time & it can be determined from a hierarchy or broad viewpoint

(Barr and McClellan, 2018).

A well-thought-out budget will provide significant outcomes for the government's key

agenda. Surprisingly, a temporary estimate is largely comprised of completed functionality &

day-to-day organisation requirements. There are various factors are involved such as Sales

budgets, production budgets, flexible budgets & other types of budgeting are examples of budget

(Plaskova and et. al., 2020).

Variance Analysis

In planning or executive accounting, variation analysis is an assessment of variations in

true behaviour vs. estimated or planned conduct. This is primarily concerned by how the contrast

between genuine & arranged practises affects company performance. Organisations may use

variance measure to appropriate understand current expenses & prepare for future expenditures.

Companies regularly do the Variance Analysis that is a quantitative approach of the differences

between planned and actual costs & earnings. Both earnings & expenses can be subjected to

variance analysis. Change is said to as 'Favourable' when actual outcomes are superior to planned

ones. Variation is said to as 'adverse' or 'unfavourable' when the appropriate consequences are

worse than the expected. Analyzing, for instances, the anticipated production costs was 150000,

but the reality production cost was 180000, indicating that variation which is unfavourable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adverse Variances

It is determined that an unfavourable variance mainly occurs when the actual pay is less

than the budgeted amount, or actual expenditure exceeds the budgeted amount. This means that

the amount of money spent exceeds the amount of money available. It is determined that a

positive distinction is when true pay outweighs financial planning, or when real usage outweighs

expenditure planning. A negative variance can occur as a result of altering financial

circumstances, such as reduced monetary growth, less private consumption, or a slowdown,

which leads to increased unemployment. Economic conditions might also alter, such as new

competitors joining the marketplace with new products and services. For instance, if the

anticipated sales were 18000 however the actual sales were 15000, the variance is the difference

or unfavourable (Popkova and et. al., 2019).

Favourable Variances

A Favourable Variances occur when actual pay exceeds expenditure plan, or when actual

use falls short of budget statement. This is the same as having an excess where expenditure

exceeds available income. It is analysed that, an optimum variation indicates that an organisation

has either generated more revenue or incurred less expenditure than expected (Jones and et. al.,

2018). This is determined that excess of a norm or projected sum above the true sum carried

about at a cost. When it comes to income, one ideal shift would be when the real income is

regarded to be more significant than the usual or projected total. For instance if the anticipated

sales are 18000 but the sales numbers were 20000, the variation is 18000.

Flexible Budget

A flexible budget adjusts to fluctuating real-world revenue levels. Once an accounting

period is completed, real earnings or other changing measurements are entered into the adaptive

proposed budget, which generates a stimulus package that is responsive to pieces of knowledge.

For control reasons, the estimate is then compared to actual expenses (Ueda and et. al., 2020).

An adaptive spending plan require more time to develop, delays the release of budget

summaries, does not measure income variations, and may be irrelevant in some final budget

models. For example, XYZ Company has a $10 million income budget and a $4 million product

expenditure budget. $1 million of the $4 million anticipated expenditure of products sold is set,

It is determined that an unfavourable variance mainly occurs when the actual pay is less

than the budgeted amount, or actual expenditure exceeds the budgeted amount. This means that

the amount of money spent exceeds the amount of money available. It is determined that a

positive distinction is when true pay outweighs financial planning, or when real usage outweighs

expenditure planning. A negative variance can occur as a result of altering financial

circumstances, such as reduced monetary growth, less private consumption, or a slowdown,

which leads to increased unemployment. Economic conditions might also alter, such as new

competitors joining the marketplace with new products and services. For instance, if the

anticipated sales were 18000 however the actual sales were 15000, the variance is the difference

or unfavourable (Popkova and et. al., 2019).

Favourable Variances

A Favourable Variances occur when actual pay exceeds expenditure plan, or when actual

use falls short of budget statement. This is the same as having an excess where expenditure

exceeds available income. It is analysed that, an optimum variation indicates that an organisation

has either generated more revenue or incurred less expenditure than expected (Jones and et. al.,

2018). This is determined that excess of a norm or projected sum above the true sum carried

about at a cost. When it comes to income, one ideal shift would be when the real income is

regarded to be more significant than the usual or projected total. For instance if the anticipated

sales are 18000 but the sales numbers were 20000, the variation is 18000.

Flexible Budget

A flexible budget adjusts to fluctuating real-world revenue levels. Once an accounting

period is completed, real earnings or other changing measurements are entered into the adaptive

proposed budget, which generates a stimulus package that is responsive to pieces of knowledge.

For control reasons, the estimate is then compared to actual expenses (Ueda and et. al., 2020).

An adaptive spending plan require more time to develop, delays the release of budget

summaries, does not measure income variations, and may be irrelevant in some final budget

models. For example, XYZ Company has a $10 million income budget and a $4 million product

expenditure budget. $1 million of the $4 million anticipated expenditure of products sold is set,

whereas $3 million changes directly with income. As an outcome, the variable portion of sales

revenue expenses accounts for 30% of the profits. When the budgeting period is over, XYZ

discovers that the sales were actually $9 million. If it utilised an adaptive spending plan, the

appropriate portion of the appropriate cost of goods sold would still be $1 million, but still the

variable portion will decrease to $2.7 million, because it is determined that 30 % of income all

the times. As a consequence, an adaptive spending plan generates a planned product sales

expenditure of the $3.7 million at a $9 million profit level, instead of just the $4 million that a

static financial plan would generate (Cosenz and Noto, 2018).

Question 6 : Explain the following terms with their formula and examples.

1. Labour Cost – The cost of the labour is one of the largest paid expenditures in every

company. In reality, like expenses account for 5-10% of overall income in the appropaiet

fast food industry. Labour costs encompass not just wages and salary, but also payrolls,

bonuses, overtime, cost of training & insurance.

Formula for determining labour costs in the following areas:-

Labour cost (as % to sales) = (Total labour/ Total sales*100) &

Labour cost (as % to operating cost) = (Total labour/Total operating cost*100)

For instance, in a restaurant business, there is annual labour cost of 84000 pound, operating cost

is 4, 12,000 pound and suppose their revenue during the accounting year is 11,25,600 pound.

Then the labour cost will be -

Percentage to sales= (84000/1125600*100)

=7.46%

Percentage to operating cost=(84000/412000*100)

=20.39%

revenue expenses accounts for 30% of the profits. When the budgeting period is over, XYZ

discovers that the sales were actually $9 million. If it utilised an adaptive spending plan, the

appropriate portion of the appropriate cost of goods sold would still be $1 million, but still the

variable portion will decrease to $2.7 million, because it is determined that 30 % of income all

the times. As a consequence, an adaptive spending plan generates a planned product sales

expenditure of the $3.7 million at a $9 million profit level, instead of just the $4 million that a

static financial plan would generate (Cosenz and Noto, 2018).

Question 6 : Explain the following terms with their formula and examples.

1. Labour Cost – The cost of the labour is one of the largest paid expenditures in every

company. In reality, like expenses account for 5-10% of overall income in the appropaiet

fast food industry. Labour costs encompass not just wages and salary, but also payrolls,

bonuses, overtime, cost of training & insurance.

Formula for determining labour costs in the following areas:-

Labour cost (as % to sales) = (Total labour/ Total sales*100) &

Labour cost (as % to operating cost) = (Total labour/Total operating cost*100)

For instance, in a restaurant business, there is annual labour cost of 84000 pound, operating cost

is 4, 12,000 pound and suppose their revenue during the accounting year is 11,25,600 pound.

Then the labour cost will be -

Percentage to sales= (84000/1125600*100)

=7.46%

Percentage to operating cost=(84000/412000*100)

=20.39%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Customer retention rate – It is simply identified to the quantity of customers retained by

a company over a given period of time. There seems to be a financial motivation to keep

current customers since it is far less expensive to keep existing clients than it is to build a

new client base for a company (Barr, and McClellan, 2018). Clients, both new & old,

contribute to the firm's success by promoting the social media marketing campaign;

leaving comments & providing frequent feedback to aid enhance the customer

experience.

The formula is as under -

(E-N/S*100)

Here E mainly stands for total number of customer, N for total number of new customer and S

for total number of existing customers

Let’s say a restaurant has 100 customers(S) at the beginning of the year & ended with 100

customer(E) & added 10 new customers(N) during the period.

Therefore their customer retention ration will be:

= (100-10/100)*100

= 90%

3. Food average spends – As a small entrepreneur, our main objective is always to pleasure

our customer, but really the leading financial objective for just about any company is to

maximise sales at lowest cost possible. Food cost percentage is significant in the

restaurant company since appropriate cost management may assist achieve optimum

earnings.

Food average spends can be calculated as under:-

= (Opening stock + Purchases-Closing Stock/ Food Sales)

Assuming in a restaurant, opening stock is 15000 pound, purchases 4000 pound, closing stock

16000 pound and food sales is 10000 pound.

a company over a given period of time. There seems to be a financial motivation to keep

current customers since it is far less expensive to keep existing clients than it is to build a

new client base for a company (Barr, and McClellan, 2018). Clients, both new & old,

contribute to the firm's success by promoting the social media marketing campaign;

leaving comments & providing frequent feedback to aid enhance the customer

experience.

The formula is as under -

(E-N/S*100)

Here E mainly stands for total number of customer, N for total number of new customer and S

for total number of existing customers

Let’s say a restaurant has 100 customers(S) at the beginning of the year & ended with 100

customer(E) & added 10 new customers(N) during the period.

Therefore their customer retention ration will be:

= (100-10/100)*100

= 90%

3. Food average spends – As a small entrepreneur, our main objective is always to pleasure

our customer, but really the leading financial objective for just about any company is to

maximise sales at lowest cost possible. Food cost percentage is significant in the

restaurant company since appropriate cost management may assist achieve optimum

earnings.

Food average spends can be calculated as under:-

= (Opening stock + Purchases-Closing Stock/ Food Sales)

Assuming in a restaurant, opening stock is 15000 pound, purchases 4000 pound, closing stock

16000 pound and food sales is 10000 pound.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Therefore food average spends will be:

=(15000+4000-16000)/10000

=30%

4. Food cost of sales ratio - One of the very first lessons everybody who works in a

company learns is how to calculate food costs and increase profit. Food costs of sales, on

average, would account for 30 to half of the global sales in any business. Managing sales

costs aids in producing more revenue and increasing profit margins (Barbos and et. al.,

2018).

The food % of sales ratio is a financial ratio that compares an organization's costs to its sales

statistics. The formula for calculating the same is as follows -

= (Food cost of sales/Total Sales or revenue)*100

For e.g., the food cost of sales for an entity is 98000 pound and their revenue during the year is

156000 pound then their ratio will be:

=98000/156000*100

= 62.82%

5. Beverage cost of sales – In context the hotel sector, beverages cost of sales is often

measured. This is evaluated to find how much the beverages contribute to the

organization's overall sales.

It is calculated as under:

= (Cost of beverages sold/Total sales *100)

Let’s assume that a restaurant owner has calculated cost of beverages amount to pound 15000

and their total sales made during an accounting period is pound 98000.

Therefore beverage cost of sales would be as under:

=15000/98000*100

=15.31%

=(15000+4000-16000)/10000

=30%

4. Food cost of sales ratio - One of the very first lessons everybody who works in a

company learns is how to calculate food costs and increase profit. Food costs of sales, on

average, would account for 30 to half of the global sales in any business. Managing sales

costs aids in producing more revenue and increasing profit margins (Barbos and et. al.,

2018).

The food % of sales ratio is a financial ratio that compares an organization's costs to its sales

statistics. The formula for calculating the same is as follows -

= (Food cost of sales/Total Sales or revenue)*100

For e.g., the food cost of sales for an entity is 98000 pound and their revenue during the year is

156000 pound then their ratio will be:

=98000/156000*100

= 62.82%

5. Beverage cost of sales – In context the hotel sector, beverages cost of sales is often

measured. This is evaluated to find how much the beverages contribute to the

organization's overall sales.

It is calculated as under:

= (Cost of beverages sold/Total sales *100)

Let’s assume that a restaurant owner has calculated cost of beverages amount to pound 15000

and their total sales made during an accounting period is pound 98000.

Therefore beverage cost of sales would be as under:

=15000/98000*100

=15.31%

CONCLUSION

According to this report, it concluded that it is necessary to managing the financial resources

in every organisation. In this report, various types of cost are calculated with the help of various

examples. It is determined that foregoing analysis is necessary in order to analyse the funding

planning which is considered as the vital component for the company. In this report, it is

analysed that for the organisation, it is necessary to avoid the unnecessary cost. In this report, the

development of the project budget is mainly considered by the organisation. Organisation needs

to focus on the managing the financial resources.

According to this report, it concluded that it is necessary to managing the financial resources

in every organisation. In this report, various types of cost are calculated with the help of various

examples. It is determined that foregoing analysis is necessary in order to analyse the funding

planning which is considered as the vital component for the company. In this report, it is

analysed that for the organisation, it is necessary to avoid the unnecessary cost. In this report, the

development of the project budget is mainly considered by the organisation. Organisation needs

to focus on the managing the financial resources.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.