Management Accounting: Cost Analysis, Budgeting and Financial Ratios

VerifiedAdded on 2023/06/10

|16

|3154

|419

Report

AI Summary

This report provides a detailed analysis of various management accounting aspects through different scenarios. It evaluates a make-or-buy decision for Thunder Company, concluding that manufacturing the product internally results in savings. Financial ratios are applied to J.P. Robard Manufacturing Company, revealing a favorable position in the industry. The report highlights how budgeting improves productivity by eliminating non-value-added activities and discusses variance analysis as a tool for identifying deviations from the budget for corrective action. The analysis includes calculations and interpretations of financial metrics like current ratio, inventory turnover, asset turnover, and debt ratio, offering recommendations based on the findings.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING

Executive Summary:

The current report intends to evaluate the various aspects of management accounting

based on different provided scenarios. The first segment has focused on deciding whether to

make or buy a product, in which it has been found that the make decision would help in making

additional savings for Thunder Company. Moreover, after applying the various financial ratios in

the context of J.P. Robard Manufacturing Company, it has been found that the organisation is

placed in a favourable position in the industry. Furthermore, it has been evaluated that budgeting

helps in removing those activities not adding value to the organisation in order to improve the

overall productivity. Finally, variance analysis is an important tool to identify the variations from

budget in order to undertake corrective actions.

1 | P a g e

Executive Summary:

The current report intends to evaluate the various aspects of management accounting

based on different provided scenarios. The first segment has focused on deciding whether to

make or buy a product, in which it has been found that the make decision would help in making

additional savings for Thunder Company. Moreover, after applying the various financial ratios in

the context of J.P. Robard Manufacturing Company, it has been found that the organisation is

placed in a favourable position in the industry. Furthermore, it has been evaluated that budgeting

helps in removing those activities not adding value to the organisation in order to improve the

overall productivity. Finally, variance analysis is an important tool to identify the variations from

budget in order to undertake corrective actions.

1 | P a g e

MANAGEMENT ACCOUNTING

Table of Contents

Question 2(b):..................................................................................................................................3

Requirement 1:.............................................................................................................................3

Requirement 2:.............................................................................................................................3

Question 3:.......................................................................................................................................5

Requirement A:............................................................................................................................5

Requirement B:............................................................................................................................7

Requirement C:............................................................................................................................7

Question 4:.......................................................................................................................................8

Requirement A:............................................................................................................................8

Requirement B:............................................................................................................................8

Question 5:.....................................................................................................................................10

Requirement 1:...........................................................................................................................10

Part a:.....................................................................................................................................10

Part b:.....................................................................................................................................11

Part c:.....................................................................................................................................11

Requirement 2:...........................................................................................................................12

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

2 | P a g e

Table of Contents

Question 2(b):..................................................................................................................................3

Requirement 1:.............................................................................................................................3

Requirement 2:.............................................................................................................................3

Question 3:.......................................................................................................................................5

Requirement A:............................................................................................................................5

Requirement B:............................................................................................................................7

Requirement C:............................................................................................................................7

Question 4:.......................................................................................................................................8

Requirement A:............................................................................................................................8

Requirement B:............................................................................................................................8

Question 5:.....................................................................................................................................10

Requirement 1:...........................................................................................................................10

Part a:.....................................................................................................................................10

Part b:.....................................................................................................................................11

Part c:.....................................................................................................................................11

Requirement 2:...........................................................................................................................12

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING

Question 2(b):

Requirement 1:

As per the provided information, it could be observed that Sparks Limited manufactures

three products A, B and C. However, as Product A is suffering loss of $7,000, the managing

director of the organisation makes arguments in favour of discontinuing the product. However,

sometimes it is necessary to retain the unprofitable product due to the following reasons:

Remaining raw materials:

There might be some raw materials on hand, which are associated only with the Product

A and thus, management would like to draw down such quantities through additional product

sales (Armitage, Webb and Glynn 2016).

Hole in product line:

It might be significant to depict complete product line-up to the customers for refraining

them from using the competitors’ products; in case, hole in the product line is inherent.

Market blocking:

If Sparks Limited decides to retain Product A at a low price point, the rivals would be

kept from making market entry with their own products.

Dependent products:

There might be a chance that the dependent products providing outsized profits could

cover up the losses incurred by one product (Ax and Greve 2017). If the situation is similar for

Sparks Limited, the other two products B and C could cover up the losses generated by Product

A.

Requirement 2:

Make or buy decision is the act of selecting between producing a product internally or

buying the same from an external supplier (Bromwich and Scapens 2016). In this decision, the

3 | P a g e

Question 2(b):

Requirement 1:

As per the provided information, it could be observed that Sparks Limited manufactures

three products A, B and C. However, as Product A is suffering loss of $7,000, the managing

director of the organisation makes arguments in favour of discontinuing the product. However,

sometimes it is necessary to retain the unprofitable product due to the following reasons:

Remaining raw materials:

There might be some raw materials on hand, which are associated only with the Product

A and thus, management would like to draw down such quantities through additional product

sales (Armitage, Webb and Glynn 2016).

Hole in product line:

It might be significant to depict complete product line-up to the customers for refraining

them from using the competitors’ products; in case, hole in the product line is inherent.

Market blocking:

If Sparks Limited decides to retain Product A at a low price point, the rivals would be

kept from making market entry with their own products.

Dependent products:

There might be a chance that the dependent products providing outsized profits could

cover up the losses incurred by one product (Ax and Greve 2017). If the situation is similar for

Sparks Limited, the other two products B and C could cover up the losses generated by Product

A.

Requirement 2:

Make or buy decision is the act of selecting between producing a product internally or

buying the same from an external supplier (Bromwich and Scapens 2016). In this decision, the

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING

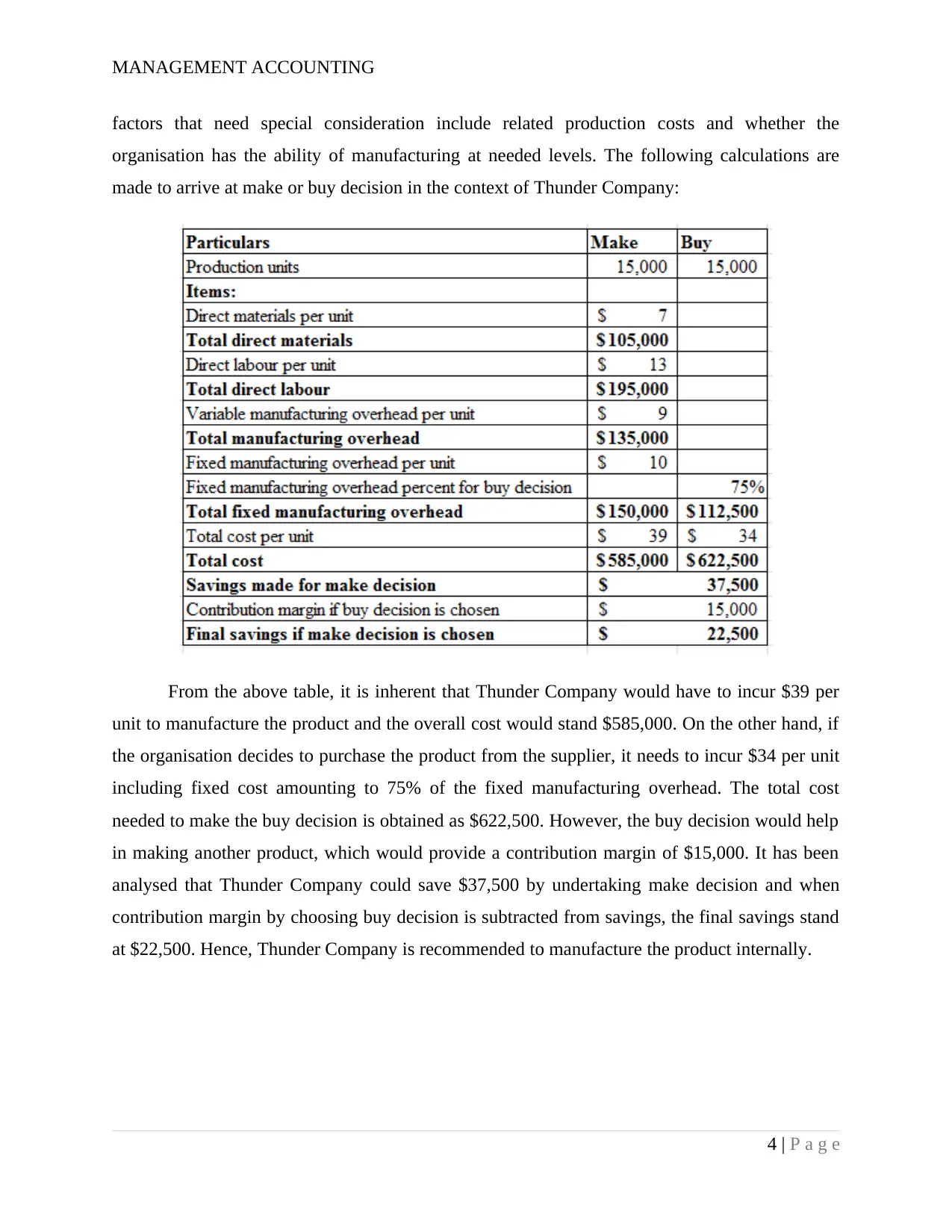

factors that need special consideration include related production costs and whether the

organisation has the ability of manufacturing at needed levels. The following calculations are

made to arrive at make or buy decision in the context of Thunder Company:

From the above table, it is inherent that Thunder Company would have to incur $39 per

unit to manufacture the product and the overall cost would stand $585,000. On the other hand, if

the organisation decides to purchase the product from the supplier, it needs to incur $34 per unit

including fixed cost amounting to 75% of the fixed manufacturing overhead. The total cost

needed to make the buy decision is obtained as $622,500. However, the buy decision would help

in making another product, which would provide a contribution margin of $15,000. It has been

analysed that Thunder Company could save $37,500 by undertaking make decision and when

contribution margin by choosing buy decision is subtracted from savings, the final savings stand

at $22,500. Hence, Thunder Company is recommended to manufacture the product internally.

4 | P a g e

factors that need special consideration include related production costs and whether the

organisation has the ability of manufacturing at needed levels. The following calculations are

made to arrive at make or buy decision in the context of Thunder Company:

From the above table, it is inherent that Thunder Company would have to incur $39 per

unit to manufacture the product and the overall cost would stand $585,000. On the other hand, if

the organisation decides to purchase the product from the supplier, it needs to incur $34 per unit

including fixed cost amounting to 75% of the fixed manufacturing overhead. The total cost

needed to make the buy decision is obtained as $622,500. However, the buy decision would help

in making another product, which would provide a contribution margin of $15,000. It has been

analysed that Thunder Company could save $37,500 by undertaking make decision and when

contribution margin by choosing buy decision is subtracted from savings, the final savings stand

at $22,500. Hence, Thunder Company is recommended to manufacture the product internally.

4 | P a g e

MANAGEMENT ACCOUNTING

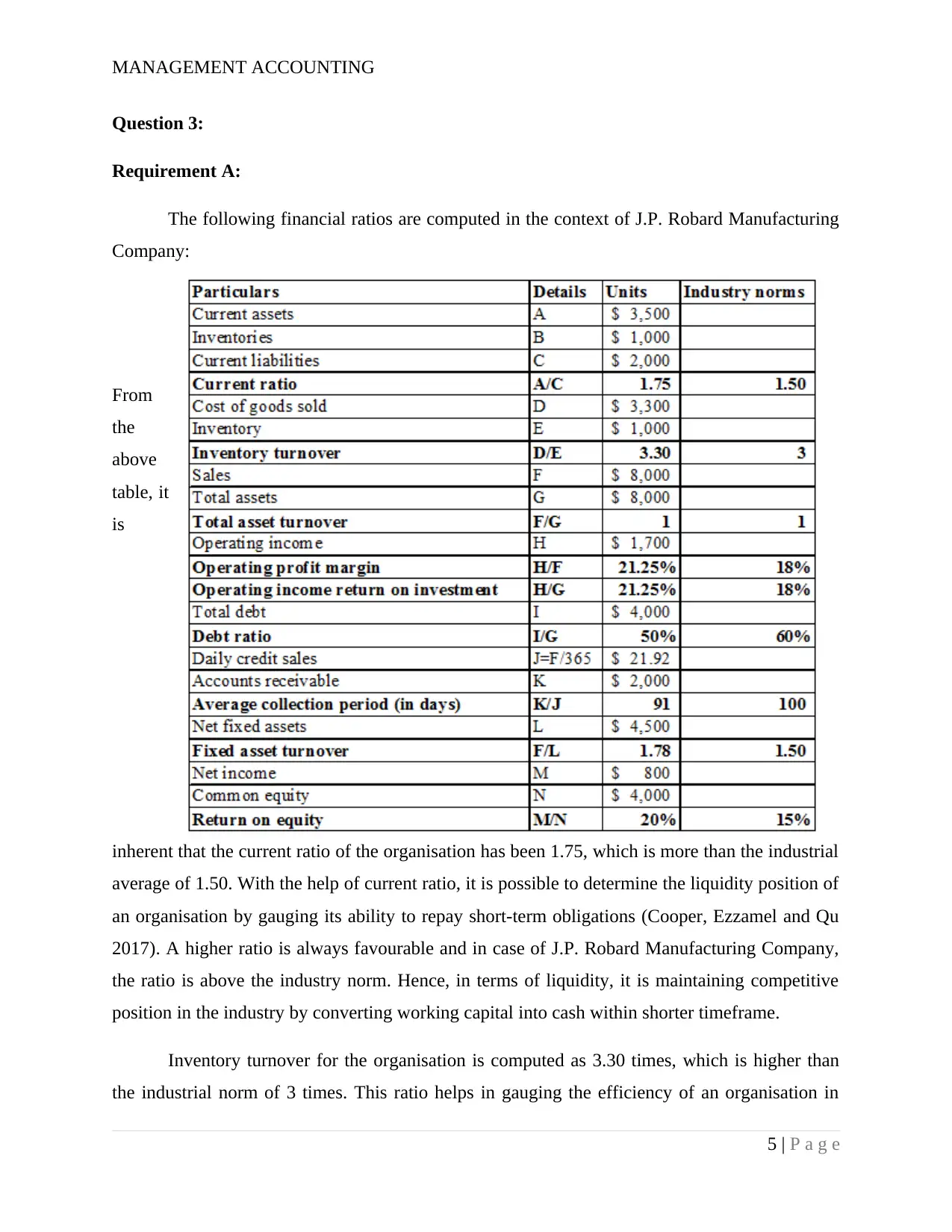

Question 3:

Requirement A:

The following financial ratios are computed in the context of J.P. Robard Manufacturing

Company:

From

the

above

table, it

is

inherent that the current ratio of the organisation has been 1.75, which is more than the industrial

average of 1.50. With the help of current ratio, it is possible to determine the liquidity position of

an organisation by gauging its ability to repay short-term obligations (Cooper, Ezzamel and Qu

2017). A higher ratio is always favourable and in case of J.P. Robard Manufacturing Company,

the ratio is above the industry norm. Hence, in terms of liquidity, it is maintaining competitive

position in the industry by converting working capital into cash within shorter timeframe.

Inventory turnover for the organisation is computed as 3.30 times, which is higher than

the industrial norm of 3 times. This ratio helps in gauging the efficiency of an organisation in

5 | P a g e

Question 3:

Requirement A:

The following financial ratios are computed in the context of J.P. Robard Manufacturing

Company:

From

the

above

table, it

is

inherent that the current ratio of the organisation has been 1.75, which is more than the industrial

average of 1.50. With the help of current ratio, it is possible to determine the liquidity position of

an organisation by gauging its ability to repay short-term obligations (Cooper, Ezzamel and Qu

2017). A higher ratio is always favourable and in case of J.P. Robard Manufacturing Company,

the ratio is above the industry norm. Hence, in terms of liquidity, it is maintaining competitive

position in the industry by converting working capital into cash within shorter timeframe.

Inventory turnover for the organisation is computed as 3.30 times, which is higher than

the industrial norm of 3 times. This ratio helps in gauging the efficiency of an organisation in

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING

controlling its merchandise and thus, a higher figure is desirable for the organisation (Fullerton,

Kennedy and Widener 2014). The ratio is desirable for J.P. Hobard Manufacturing Company due

to increased market demand, which has helped in releasing its merchandise at a faster rate than

its competitors. Asset turnover ratio, on the other hand, gauges the efficacy of an organisation in

utilising its assets for generation of sales revenue (Kokubu and Kitada 2015). A higher turnover

is desirable and in case of J.P. Hobard Manufacturing Company, the ratio is the same as the

industrial yardstick, as it has employed its assets effectively to cope up with the industrial trend.

Operating profit margin of the organisation is obtained as 21.25% in contrast to the

industry norm of 18% and this margin is a key indicator for creditors and investors to analyse the

way an organisation is supporting its operations (Langfield-Smith et al. 2017). In this case, it is

more than the industrial average, as it has lower operating costs in contrast to its competitors.

The similar is the case with return on investment, which denotes that investments are made after

suitable evaluation of projects to maximise the overall returns.

Debt ratio is a measure of solvency that gauges the total liabilities of an organisation as a

percentage of total assets (Lavia López and Hiebl 2014). In case of J.P. Hobard Manufacturing

Company, the ratio is computed as 50%, while the industrial norm is provided as 60%. A lower

ratio is always favourable, since it implies better business stability having the potential of

longevity, as an organisation with lower ratio has lower total debt. In this case, the organisation

has focused on raising funds partly through debt and partly through equity, which has helped in

maintaining optimality in its capital structure. Average collection period denotes the time taken

in order to recover the amounts to be obtained from the credit sales made to the customers by an

organisation. For J.P. Hobard Manufacturing Company, the amounts are recovered within 91

days in opposition to the industrial norm of 100 days. A lower period is desirable, as recovering

money within shorter time helps in increasing the availability of working capital and the case is

similar for the concerned entity as well.

In terms of fixed asset turnover ratio, it is 1.78 for the organisation, while the industry

norm is given as 1.50. A higher turnover is favourable, as it implies that more revenue is

generated through effective utilisation of fixed assets. For J.P. Hobard Manufacturing Company,

the situation is similar, since it might have leased a portion of its unutilised fixed assets for

generating additional revenues in contrast to its rivals. Finally, in terms of return of equity, J.P.

6 | P a g e

controlling its merchandise and thus, a higher figure is desirable for the organisation (Fullerton,

Kennedy and Widener 2014). The ratio is desirable for J.P. Hobard Manufacturing Company due

to increased market demand, which has helped in releasing its merchandise at a faster rate than

its competitors. Asset turnover ratio, on the other hand, gauges the efficacy of an organisation in

utilising its assets for generation of sales revenue (Kokubu and Kitada 2015). A higher turnover

is desirable and in case of J.P. Hobard Manufacturing Company, the ratio is the same as the

industrial yardstick, as it has employed its assets effectively to cope up with the industrial trend.

Operating profit margin of the organisation is obtained as 21.25% in contrast to the

industry norm of 18% and this margin is a key indicator for creditors and investors to analyse the

way an organisation is supporting its operations (Langfield-Smith et al. 2017). In this case, it is

more than the industrial average, as it has lower operating costs in contrast to its competitors.

The similar is the case with return on investment, which denotes that investments are made after

suitable evaluation of projects to maximise the overall returns.

Debt ratio is a measure of solvency that gauges the total liabilities of an organisation as a

percentage of total assets (Lavia López and Hiebl 2014). In case of J.P. Hobard Manufacturing

Company, the ratio is computed as 50%, while the industrial norm is provided as 60%. A lower

ratio is always favourable, since it implies better business stability having the potential of

longevity, as an organisation with lower ratio has lower total debt. In this case, the organisation

has focused on raising funds partly through debt and partly through equity, which has helped in

maintaining optimality in its capital structure. Average collection period denotes the time taken

in order to recover the amounts to be obtained from the credit sales made to the customers by an

organisation. For J.P. Hobard Manufacturing Company, the amounts are recovered within 91

days in opposition to the industrial norm of 100 days. A lower period is desirable, as recovering

money within shorter time helps in increasing the availability of working capital and the case is

similar for the concerned entity as well.

In terms of fixed asset turnover ratio, it is 1.78 for the organisation, while the industry

norm is given as 1.50. A higher turnover is favourable, as it implies that more revenue is

generated through effective utilisation of fixed assets. For J.P. Hobard Manufacturing Company,

the situation is similar, since it might have leased a portion of its unutilised fixed assets for

generating additional revenues in contrast to its rivals. Finally, in terms of return of equity, J.P.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING

Hobard Manufacturing Company has a better ratio of 20% in comparison to the industry norm of

15%, as more equity shares are issued and accordingly, adequate returns have been provided to

the investors and shareholders. Therefore, by taking into consideration all the aspects, J.P.

Hobard Manufacturing Company is placed in a favourable position in comparison to all other

competitors in the industry.

Requirement B:

Based on the above financial evaluation, it is evident that the capital structure of the

organisation is perfectly balanced, as equal weights are assigned to both debt and equity. Since

debt ratio is obtained as 50%, it is obvious that the equity ratio would be 50% as well. Moreover,

J.P. Hobard Manufacturing Company is making adequate profits in contrast to its competitors in

the industry, which implies that the profit earned could be used for investing in business

operations. The liquidity position of the organisation is deemed to be favourable, as the owed

amounts from the debtors have been collected within shorter period. Moreover, the market

demand for the products of the organisation is expected to increase in future, which would help

in generation of additional income (Malmi 2016). Hence, Gulf Bank Plc could sanction bank

loan to J.P. Hobard Manufacturing Company, as it has the ability of repaying its loan amount by

increasing its existing asset base, cash availability and income generated.

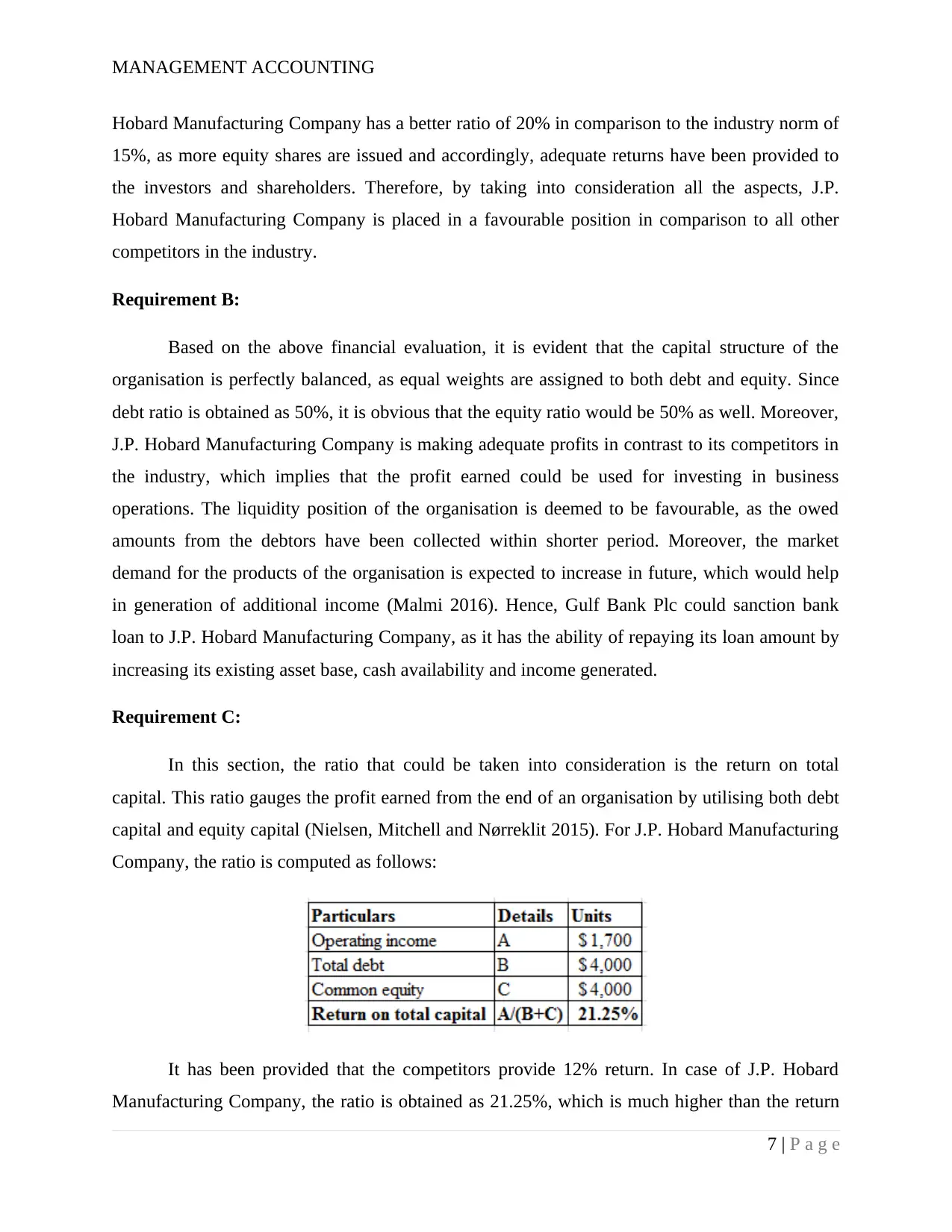

Requirement C:

In this section, the ratio that could be taken into consideration is the return on total

capital. This ratio gauges the profit earned from the end of an organisation by utilising both debt

capital and equity capital (Nielsen, Mitchell and Nørreklit 2015). For J.P. Hobard Manufacturing

Company, the ratio is computed as follows:

It has been provided that the competitors provide 12% return. In case of J.P. Hobard

Manufacturing Company, the ratio is obtained as 21.25%, which is much higher than the return

7 | P a g e

Hobard Manufacturing Company has a better ratio of 20% in comparison to the industry norm of

15%, as more equity shares are issued and accordingly, adequate returns have been provided to

the investors and shareholders. Therefore, by taking into consideration all the aspects, J.P.

Hobard Manufacturing Company is placed in a favourable position in comparison to all other

competitors in the industry.

Requirement B:

Based on the above financial evaluation, it is evident that the capital structure of the

organisation is perfectly balanced, as equal weights are assigned to both debt and equity. Since

debt ratio is obtained as 50%, it is obvious that the equity ratio would be 50% as well. Moreover,

J.P. Hobard Manufacturing Company is making adequate profits in contrast to its competitors in

the industry, which implies that the profit earned could be used for investing in business

operations. The liquidity position of the organisation is deemed to be favourable, as the owed

amounts from the debtors have been collected within shorter period. Moreover, the market

demand for the products of the organisation is expected to increase in future, which would help

in generation of additional income (Malmi 2016). Hence, Gulf Bank Plc could sanction bank

loan to J.P. Hobard Manufacturing Company, as it has the ability of repaying its loan amount by

increasing its existing asset base, cash availability and income generated.

Requirement C:

In this section, the ratio that could be taken into consideration is the return on total

capital. This ratio gauges the profit earned from the end of an organisation by utilising both debt

capital and equity capital (Nielsen, Mitchell and Nørreklit 2015). For J.P. Hobard Manufacturing

Company, the ratio is computed as follows:

It has been provided that the competitors provide 12% return. In case of J.P. Hobard

Manufacturing Company, the ratio is obtained as 21.25%, which is much higher than the return

7 | P a g e

MANAGEMENT ACCOUNTING

provided by the competitors. The reasons identified behind such higher return are the increased

revenue and optimality in capital structure due to which the investors would be provided with

sufficient return on their investment. Hence, it is recommended to the investors to invest in the

organisation, as it would help in maximising their overall return on investment.

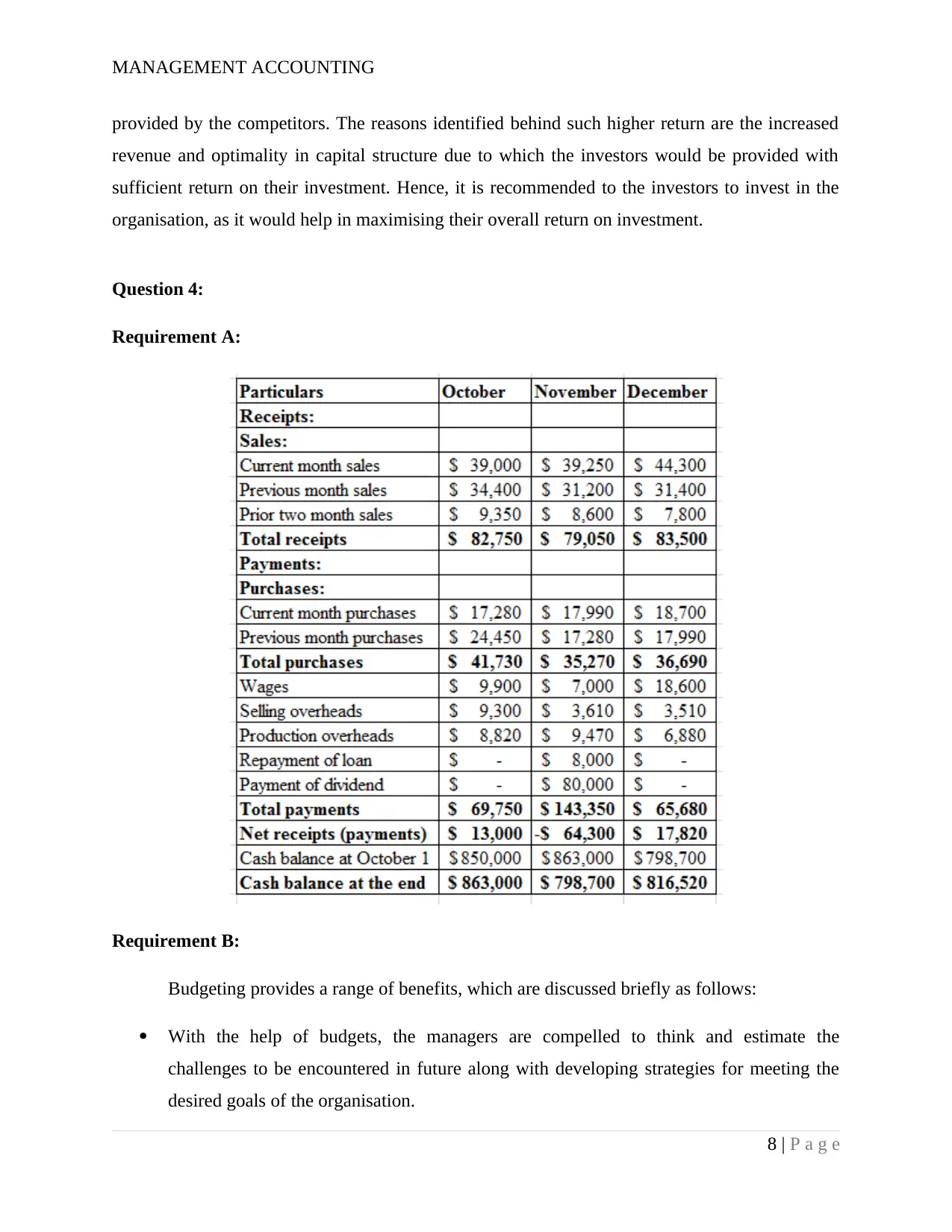

Question 4:

Requirement A:

Requirement B:

Budgeting provides a range of benefits, which are discussed briefly as follows:

With the help of budgets, the managers are compelled to think and estimate the

challenges to be encountered in future along with developing strategies for meeting the

desired goals of the organisation.

8 | P a g e

provided by the competitors. The reasons identified behind such higher return are the increased

revenue and optimality in capital structure due to which the investors would be provided with

sufficient return on their investment. Hence, it is recommended to the investors to invest in the

organisation, as it would help in maximising their overall return on investment.

Question 4:

Requirement A:

Requirement B:

Budgeting provides a range of benefits, which are discussed briefly as follows:

With the help of budgets, the managers are compelled to think and estimate the

challenges to be encountered in future along with developing strategies for meeting the

desired goals of the organisation.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING

Incentives are dependent on the accomplishments in contrast to the budgeted figures.

Therefore, if budgets are formulated realistically, they would help to motivate the

managers and employees in a positive manner (Otley 2016).

In the stages of budgeting, there have been elimination of those activities that do not add

value; instead, new or improved processes are developed for enhancing productivity.

Budgeting is the effective tool for coordinating with all the managerial levels in order to

make future plan, promoting teamwork, goal congruency and process enhancement

between the staffs and the organisation.

By setting up budgets, there are proper segregations of delegation of duties,

responsibilities and authority limit. The top management of the organisation might feel

that they are in complete control of the different business activities with the help of

budgeting.

However, budgeting has a number of limitations, which are enumerated briefly as follows:

The staffs might not be motivated, as they might feel that the budget figures are way too

high to be accomplished.

There is high chance of budgetary slack, as the managers might blow up the budget

figures due to the fact that the higher-level management would reprimand them.

The budgets tend to emphasise on outcomes, rather it ignores the actual reasons.

Unrealistic budgets could result in certain managerial decisions that might be detrimental

to the organisation. For instance, over ambitious sales would result in drastic impact such

as providing steep discount for raising volume (Quattrone 2016).

Regardless of procedures followed in preparing budgets, budgeting does not possess the

ability of reflecting the actual scenario or complexities faced by the organisation.

9 | P a g e

Incentives are dependent on the accomplishments in contrast to the budgeted figures.

Therefore, if budgets are formulated realistically, they would help to motivate the

managers and employees in a positive manner (Otley 2016).

In the stages of budgeting, there have been elimination of those activities that do not add

value; instead, new or improved processes are developed for enhancing productivity.

Budgeting is the effective tool for coordinating with all the managerial levels in order to

make future plan, promoting teamwork, goal congruency and process enhancement

between the staffs and the organisation.

By setting up budgets, there are proper segregations of delegation of duties,

responsibilities and authority limit. The top management of the organisation might feel

that they are in complete control of the different business activities with the help of

budgeting.

However, budgeting has a number of limitations, which are enumerated briefly as follows:

The staffs might not be motivated, as they might feel that the budget figures are way too

high to be accomplished.

There is high chance of budgetary slack, as the managers might blow up the budget

figures due to the fact that the higher-level management would reprimand them.

The budgets tend to emphasise on outcomes, rather it ignores the actual reasons.

Unrealistic budgets could result in certain managerial decisions that might be detrimental

to the organisation. For instance, over ambitious sales would result in drastic impact such

as providing steep discount for raising volume (Quattrone 2016).

Regardless of procedures followed in preparing budgets, budgeting does not possess the

ability of reflecting the actual scenario or complexities faced by the organisation.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING

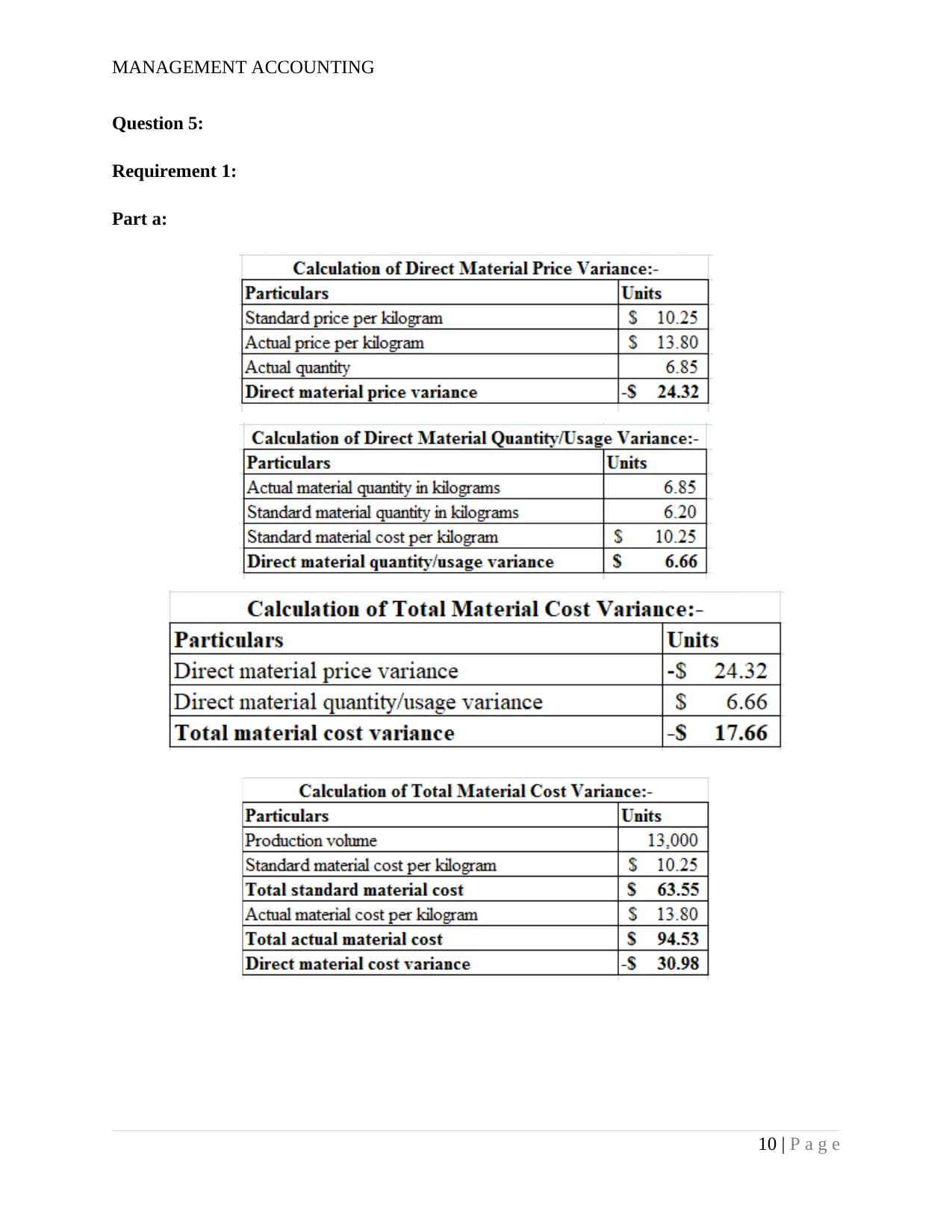

Question 5:

Requirement 1:

Part a:

10 | P a g e

Question 5:

Requirement 1:

Part a:

10 | P a g e

MANAGEMENT ACCOUNTING

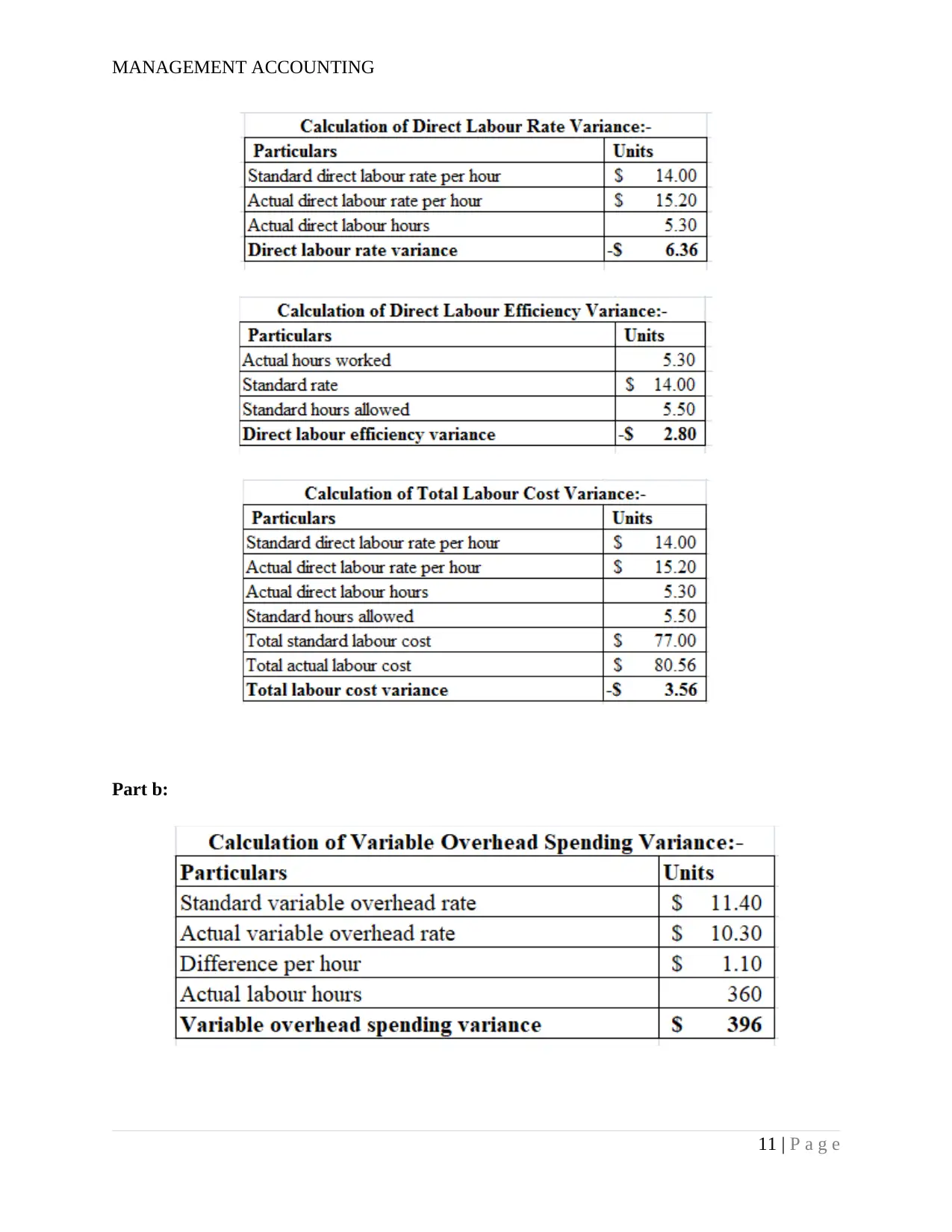

Part b:

11 | P a g e

Part b:

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.