Management Accounting: Costing Techniques and Financial Reporting

VerifiedAdded on 2024/06/21

|24

|5560

|496

Report

AI Summary

This report provides a detailed analysis of management accounting principles, focusing on cost analysis techniques and financial reporting methods. It explains the essential requirements of different management accounting systems and explores the origin, role, and principles of management accounting, highlighting the distinction between management and financial accounting. The report also calculates costs using marginal and absorption costing techniques to prepare income statements, analyzing microeconomic techniques such as cost-volume profit. The report uses Prime Furniture as a case study. Desklib offers a platform to access this and many other solved assignments for students.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

LO1..................................................................................................................................................4

LO2..................................................................................................................................................8

LO3................................................................................................................................................11

LO4................................................................................................................................................14

References......................................................................................................................................17

Appendix........................................................................................................................................19

Introduction......................................................................................................................................3

LO1..................................................................................................................................................4

LO2..................................................................................................................................................8

LO3................................................................................................................................................11

LO4................................................................................................................................................14

References......................................................................................................................................17

Appendix........................................................................................................................................19

Introduction

Management accounting is the process of preparation of business reports for the decision-making

in the organisation. .Budget related decision can be adopted by the organisation in accordance

with this accounting system. Controlling the financial performance of the organisation will be

possible with the help of management accounting. The study will highlight the different types of

planning tools along with different types of management accounting systems. Besides that,

marginal and absorption costing methods will be analysed in accordance with Prime Furniture.

Prime Furniture is a growing London-based company.

Management accounting is the process of preparation of business reports for the decision-making

in the organisation. .Budget related decision can be adopted by the organisation in accordance

with this accounting system. Controlling the financial performance of the organisation will be

possible with the help of management accounting. The study will highlight the different types of

planning tools along with different types of management accounting systems. Besides that,

marginal and absorption costing methods will be analysed in accordance with Prime Furniture.

Prime Furniture is a growing London-based company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO1

(Refer to Appendix)

P1: Explain management accounting and give the essential requirements of different types

of management accounting systems.

Introduction to management accounting

Definition of management accounting.

Management accounting can be defined as a process of providing financial resources and

information to the management for proper decision-making in the organisation (Langfield-Smith

et al., 2018). Internal team of Prime Furniture can utilize these financial reports for the decision-

making in the organisation. Aim of management accounting is to control over the decision-

making of the management of the organisation.

Management accounting system

Management accounting system focuses on internal reports of an organisation for the evaluation

of decision and processes of the management in the entity (Hiebl and Richter, 2018). Prime

Furniture can use different types of management accounting systems. Cost accounting, price

optimisation, job costing and inventory management are parts of management accounting system

of the organisation.

Important to integrate these within an organisation

Management accounting can conduct cost analysis of Prime Furniture. Thereafter, current

expenses can be identified with the help of management accounting in the organisation. Besides

that, future recommendations can be obtained win accordance with that (Honggowati et al.,

2017). Management accounting can help Prime Furniture in the development of buyer persona.

Age, gender along with income level of consumers can be analysed. Prime Furniture will be able

to manufacture products in accordance with the demand and preferences of consumers. For

instance, Prime Furniture can adopt decision of reduction in salaries or overhead expenses in the

organisation to improve the profitability.

Analysis

Explore the origin, role and principles of management accounting

Origin of the management and financial accounting are different. Management accounting has

been invented with the help of Du Pont and General Motors. It has been estimated that the

concept of management accounting has been introduced in 1900s (Hopper and Bui, 2016).

Role of management accounting: Role of management accounting can be stated as to perform a

series of different tasks for the better decision-making in the organisation. Prime Furniture can

be able to ensure financial security and stability with the help of management accounting. Long-

term and short-term planning in the business can be possible with management accounting.

Role of management accounting in Prime Furniture is to raise funds and maintain the capital

structure. Budgets and financial reports can be controlled in accordance with the role of

(Refer to Appendix)

P1: Explain management accounting and give the essential requirements of different types

of management accounting systems.

Introduction to management accounting

Definition of management accounting.

Management accounting can be defined as a process of providing financial resources and

information to the management for proper decision-making in the organisation (Langfield-Smith

et al., 2018). Internal team of Prime Furniture can utilize these financial reports for the decision-

making in the organisation. Aim of management accounting is to control over the decision-

making of the management of the organisation.

Management accounting system

Management accounting system focuses on internal reports of an organisation for the evaluation

of decision and processes of the management in the entity (Hiebl and Richter, 2018). Prime

Furniture can use different types of management accounting systems. Cost accounting, price

optimisation, job costing and inventory management are parts of management accounting system

of the organisation.

Important to integrate these within an organisation

Management accounting can conduct cost analysis of Prime Furniture. Thereafter, current

expenses can be identified with the help of management accounting in the organisation. Besides

that, future recommendations can be obtained win accordance with that (Honggowati et al.,

2017). Management accounting can help Prime Furniture in the development of buyer persona.

Age, gender along with income level of consumers can be analysed. Prime Furniture will be able

to manufacture products in accordance with the demand and preferences of consumers. For

instance, Prime Furniture can adopt decision of reduction in salaries or overhead expenses in the

organisation to improve the profitability.

Analysis

Explore the origin, role and principles of management accounting

Origin of the management and financial accounting are different. Management accounting has

been invented with the help of Du Pont and General Motors. It has been estimated that the

concept of management accounting has been introduced in 1900s (Hopper and Bui, 2016).

Role of management accounting: Role of management accounting can be stated as to perform a

series of different tasks for the better decision-making in the organisation. Prime Furniture can

be able to ensure financial security and stability with the help of management accounting. Long-

term and short-term planning in the business can be possible with management accounting.

Role of management accounting in Prime Furniture is to raise funds and maintain the capital

structure. Budgets and financial reports can be controlled in accordance with the role of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management accounting. Strategies for future goals and objectives can be developed in Prime

Furniture for maintaining cost and performance.

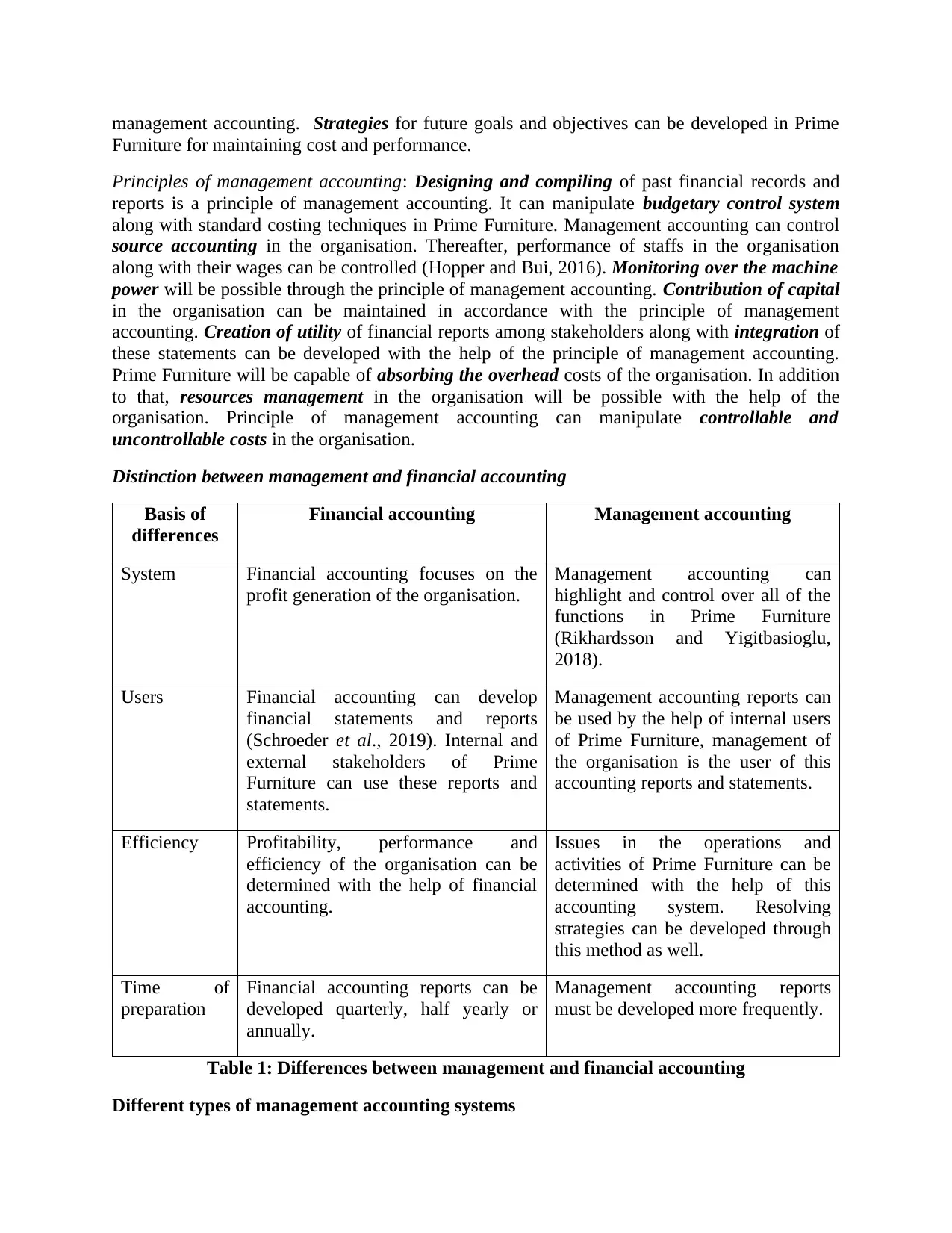

Principles of management accounting: Designing and compiling of past financial records and

reports is a principle of management accounting. It can manipulate budgetary control system

along with standard costing techniques in Prime Furniture. Management accounting can control

source accounting in the organisation. Thereafter, performance of staffs in the organisation

along with their wages can be controlled (Hopper and Bui, 2016). Monitoring over the machine

power will be possible through the principle of management accounting. Contribution of capital

in the organisation can be maintained in accordance with the principle of management

accounting. Creation of utility of financial reports among stakeholders along with integration of

these statements can be developed with the help of the principle of management accounting.

Prime Furniture will be capable of absorbing the overhead costs of the organisation. In addition

to that, resources management in the organisation will be possible with the help of the

organisation. Principle of management accounting can manipulate controllable and

uncontrollable costs in the organisation.

Distinction between management and financial accounting

Basis of

differences

Financial accounting Management accounting

System Financial accounting focuses on the

profit generation of the organisation.

Management accounting can

highlight and control over all of the

functions in Prime Furniture

(Rikhardsson and Yigitbasioglu,

2018).

Users Financial accounting can develop

financial statements and reports

(Schroeder et al., 2019). Internal and

external stakeholders of Prime

Furniture can use these reports and

statements.

Management accounting reports can

be used by the help of internal users

of Prime Furniture, management of

the organisation is the user of this

accounting reports and statements.

Efficiency Profitability, performance and

efficiency of the organisation can be

determined with the help of financial

accounting.

Issues in the operations and

activities of Prime Furniture can be

determined with the help of this

accounting system. Resolving

strategies can be developed through

this method as well.

Time of

preparation

Financial accounting reports can be

developed quarterly, half yearly or

annually.

Management accounting reports

must be developed more frequently.

Table 1: Differences between management and financial accounting

Different types of management accounting systems

Furniture for maintaining cost and performance.

Principles of management accounting: Designing and compiling of past financial records and

reports is a principle of management accounting. It can manipulate budgetary control system

along with standard costing techniques in Prime Furniture. Management accounting can control

source accounting in the organisation. Thereafter, performance of staffs in the organisation

along with their wages can be controlled (Hopper and Bui, 2016). Monitoring over the machine

power will be possible through the principle of management accounting. Contribution of capital

in the organisation can be maintained in accordance with the principle of management

accounting. Creation of utility of financial reports among stakeholders along with integration of

these statements can be developed with the help of the principle of management accounting.

Prime Furniture will be capable of absorbing the overhead costs of the organisation. In addition

to that, resources management in the organisation will be possible with the help of the

organisation. Principle of management accounting can manipulate controllable and

uncontrollable costs in the organisation.

Distinction between management and financial accounting

Basis of

differences

Financial accounting Management accounting

System Financial accounting focuses on the

profit generation of the organisation.

Management accounting can

highlight and control over all of the

functions in Prime Furniture

(Rikhardsson and Yigitbasioglu,

2018).

Users Financial accounting can develop

financial statements and reports

(Schroeder et al., 2019). Internal and

external stakeholders of Prime

Furniture can use these reports and

statements.

Management accounting reports can

be used by the help of internal users

of Prime Furniture, management of

the organisation is the user of this

accounting reports and statements.

Efficiency Profitability, performance and

efficiency of the organisation can be

determined with the help of financial

accounting.

Issues in the operations and

activities of Prime Furniture can be

determined with the help of this

accounting system. Resolving

strategies can be developed through

this method as well.

Time of

preparation

Financial accounting reports can be

developed quarterly, half yearly or

annually.

Management accounting reports

must be developed more frequently.

Table 1: Differences between management and financial accounting

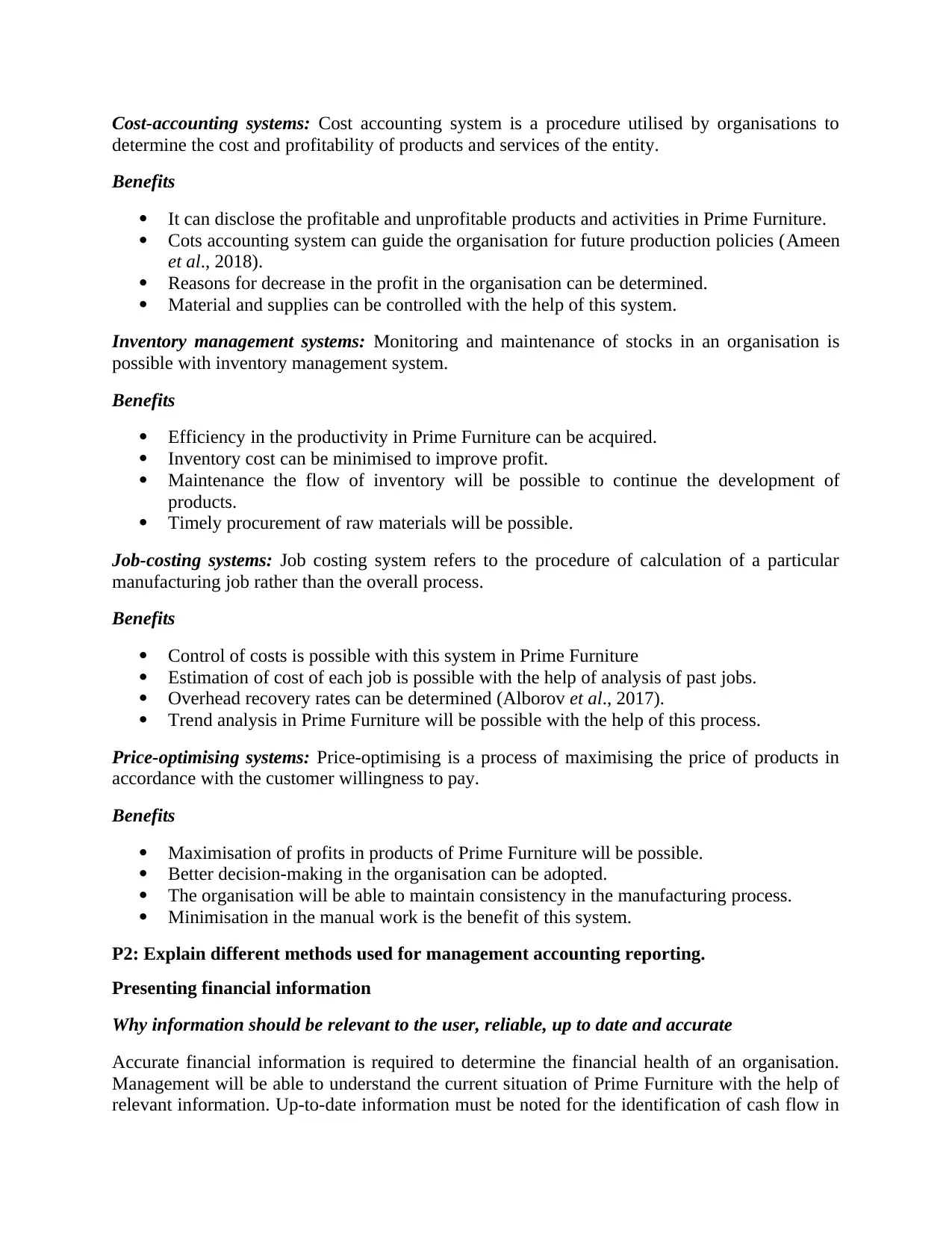

Different types of management accounting systems

Cost-accounting systems: Cost accounting system is a procedure utilised by organisations to

determine the cost and profitability of products and services of the entity.

Benefits

It can disclose the profitable and unprofitable products and activities in Prime Furniture.

Cots accounting system can guide the organisation for future production policies (Ameen

et al., 2018).

Reasons for decrease in the profit in the organisation can be determined.

Material and supplies can be controlled with the help of this system.

Inventory management systems: Monitoring and maintenance of stocks in an organisation is

possible with inventory management system.

Benefits

Efficiency in the productivity in Prime Furniture can be acquired.

Inventory cost can be minimised to improve profit.

Maintenance the flow of inventory will be possible to continue the development of

products.

Timely procurement of raw materials will be possible.

Job-costing systems: Job costing system refers to the procedure of calculation of a particular

manufacturing job rather than the overall process.

Benefits

Control of costs is possible with this system in Prime Furniture

Estimation of cost of each job is possible with the help of analysis of past jobs.

Overhead recovery rates can be determined (Alborov et al., 2017).

Trend analysis in Prime Furniture will be possible with the help of this process.

Price-optimising systems: Price-optimising is a process of maximising the price of products in

accordance with the customer willingness to pay.

Benefits

Maximisation of profits in products of Prime Furniture will be possible.

Better decision-making in the organisation can be adopted.

The organisation will be able to maintain consistency in the manufacturing process.

Minimisation in the manual work is the benefit of this system.

P2: Explain different methods used for management accounting reporting.

Presenting financial information

Why information should be relevant to the user, reliable, up to date and accurate

Accurate financial information is required to determine the financial health of an organisation.

Management will be able to understand the current situation of Prime Furniture with the help of

relevant information. Up-to-date information must be noted for the identification of cash flow in

determine the cost and profitability of products and services of the entity.

Benefits

It can disclose the profitable and unprofitable products and activities in Prime Furniture.

Cots accounting system can guide the organisation for future production policies (Ameen

et al., 2018).

Reasons for decrease in the profit in the organisation can be determined.

Material and supplies can be controlled with the help of this system.

Inventory management systems: Monitoring and maintenance of stocks in an organisation is

possible with inventory management system.

Benefits

Efficiency in the productivity in Prime Furniture can be acquired.

Inventory cost can be minimised to improve profit.

Maintenance the flow of inventory will be possible to continue the development of

products.

Timely procurement of raw materials will be possible.

Job-costing systems: Job costing system refers to the procedure of calculation of a particular

manufacturing job rather than the overall process.

Benefits

Control of costs is possible with this system in Prime Furniture

Estimation of cost of each job is possible with the help of analysis of past jobs.

Overhead recovery rates can be determined (Alborov et al., 2017).

Trend analysis in Prime Furniture will be possible with the help of this process.

Price-optimising systems: Price-optimising is a process of maximising the price of products in

accordance with the customer willingness to pay.

Benefits

Maximisation of profits in products of Prime Furniture will be possible.

Better decision-making in the organisation can be adopted.

The organisation will be able to maintain consistency in the manufacturing process.

Minimisation in the manual work is the benefit of this system.

P2: Explain different methods used for management accounting reporting.

Presenting financial information

Why information should be relevant to the user, reliable, up to date and accurate

Accurate financial information is required to determine the financial health of an organisation.

Management will be able to understand the current situation of Prime Furniture with the help of

relevant information. Up-to-date information must be noted for the identification of cash flow in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the organisation. Investors in Prime Furniture will seek for the up-to-date information for the

decision-making in the organisation. Thereafter, relevant, accurate and up-to-fate information

will be important for the development of financial and management reports and to estimate the

actual business position in the industry (Turner et al., 2017).

Why the way in which the information is presented must be understandable

Reader of the financial information must comprehend the information. Management, owner

along with investors cannot be able to understand difficult principles and tools of accounting

system. However financial information must be presented to stakeholders and they must

understand the same for analysing the current position of Prime Furniture. Thereafter, financial

information must be produced in an understandable method.

Different types of managerial accounting reports

Budgeting reports: Budgeting reports are prepared to forecast the future expenditures and income

in an organisation. Allocation of resources in Prime Furniture is possible with the help of this

budgeting report. Furthermore, a target of profitability can be set for the management and

employees in the organisation. Thereafter, achievement of business goals will be possible with

these reports.

Account receivable reports: Unpaid customer list along with credit memos are being used to

prepare this reports. Prime Function will be able to determine the amount of debt to be

recovered. Besides that, cash flow of the organisation can be improved with the help of this

report. Better debt recovery policies can be implemented in the organisation (Qian et al., 2018).

Job cost report: Cost of raw materials along with the finished products can be determined with

the help of job cost report. Wastage in the production of Prime Furniture can be reduced with the

help of this report. Additionally, cost for each overhead can be calculated with the help of job

cost report.

Inventory report: Information on the summary of inventories in an organisation can be obtained

through the help of inventory report. Procurement of inventory on time is the advantage of this

report in Prime Furniture. Additionally, flow of the production and reduction in wastage in the

organisation can be maintained with the help of this report.

Future development can be planned with the help of management accounting system in the

organisation. Thereafter, Prime Furniture must integrate management accounting within the

organisation for better decision-making and improved efficiency.

decision-making in the organisation. Thereafter, relevant, accurate and up-to-fate information

will be important for the development of financial and management reports and to estimate the

actual business position in the industry (Turner et al., 2017).

Why the way in which the information is presented must be understandable

Reader of the financial information must comprehend the information. Management, owner

along with investors cannot be able to understand difficult principles and tools of accounting

system. However financial information must be presented to stakeholders and they must

understand the same for analysing the current position of Prime Furniture. Thereafter, financial

information must be produced in an understandable method.

Different types of managerial accounting reports

Budgeting reports: Budgeting reports are prepared to forecast the future expenditures and income

in an organisation. Allocation of resources in Prime Furniture is possible with the help of this

budgeting report. Furthermore, a target of profitability can be set for the management and

employees in the organisation. Thereafter, achievement of business goals will be possible with

these reports.

Account receivable reports: Unpaid customer list along with credit memos are being used to

prepare this reports. Prime Function will be able to determine the amount of debt to be

recovered. Besides that, cash flow of the organisation can be improved with the help of this

report. Better debt recovery policies can be implemented in the organisation (Qian et al., 2018).

Job cost report: Cost of raw materials along with the finished products can be determined with

the help of job cost report. Wastage in the production of Prime Furniture can be reduced with the

help of this report. Additionally, cost for each overhead can be calculated with the help of job

cost report.

Inventory report: Information on the summary of inventories in an organisation can be obtained

through the help of inventory report. Procurement of inventory on time is the advantage of this

report in Prime Furniture. Additionally, flow of the production and reduction in wastage in the

organisation can be maintained with the help of this report.

Future development can be planned with the help of management accounting system in the

organisation. Thereafter, Prime Furniture must integrate management accounting within the

organisation for better decision-making and improved efficiency.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO2

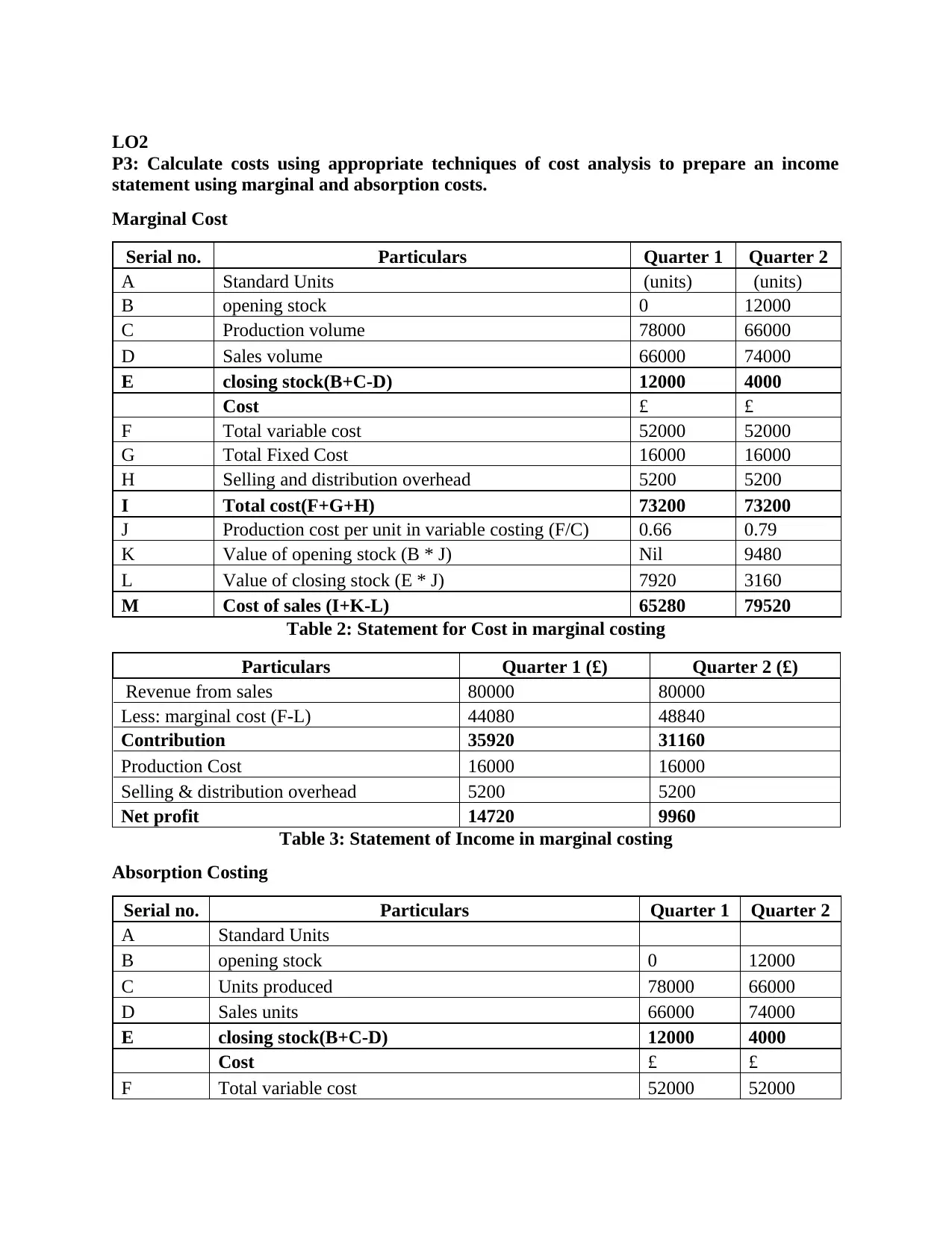

P3: Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Marginal Cost

Serial no. Particulars Quarter 1 Quarter 2

A Standard Units (units) (units)

B opening stock 0 12000

C Production volume 78000 66000

D Sales volume 66000 74000

E closing stock(B+C-D) 12000 4000

Cost £ £

F Total variable cost 52000 52000

G Total Fixed Cost 16000 16000

H Selling and distribution overhead 5200 5200

I Total cost(F+G+H) 73200 73200

J Production cost per unit in variable costing (F/C) 0.66 0.79

K Value of opening stock (B * J) Nil 9480

L Value of closing stock (E * J) 7920 3160

M Cost of sales (I+K-L) 65280 79520

Table 2: Statement for Cost in marginal costing

Particulars Quarter 1 (£) Quarter 2 (£)

Revenue from sales 80000 80000

Less: marginal cost (F-L) 44080 48840

Contribution 35920 31160

Production Cost 16000 16000

Selling & distribution overhead 5200 5200

Net profit 14720 9960

Table 3: Statement of Income in marginal costing

Absorption Costing

Serial no. Particulars Quarter 1 Quarter 2

A Standard Units

B opening stock 0 12000

C Units produced 78000 66000

D Sales units 66000 74000

E closing stock(B+C-D) 12000 4000

Cost £ £

F Total variable cost 52000 52000

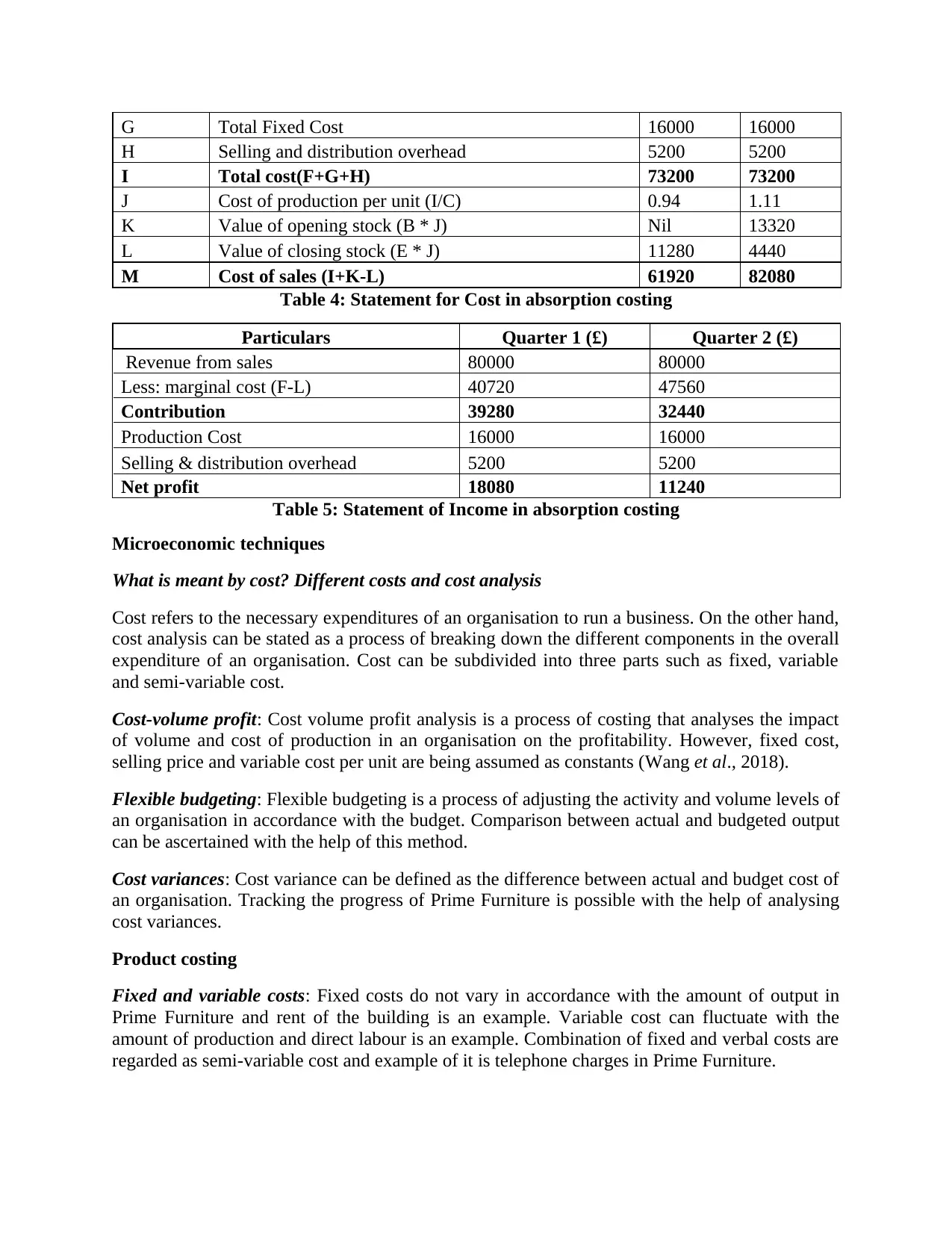

P3: Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Marginal Cost

Serial no. Particulars Quarter 1 Quarter 2

A Standard Units (units) (units)

B opening stock 0 12000

C Production volume 78000 66000

D Sales volume 66000 74000

E closing stock(B+C-D) 12000 4000

Cost £ £

F Total variable cost 52000 52000

G Total Fixed Cost 16000 16000

H Selling and distribution overhead 5200 5200

I Total cost(F+G+H) 73200 73200

J Production cost per unit in variable costing (F/C) 0.66 0.79

K Value of opening stock (B * J) Nil 9480

L Value of closing stock (E * J) 7920 3160

M Cost of sales (I+K-L) 65280 79520

Table 2: Statement for Cost in marginal costing

Particulars Quarter 1 (£) Quarter 2 (£)

Revenue from sales 80000 80000

Less: marginal cost (F-L) 44080 48840

Contribution 35920 31160

Production Cost 16000 16000

Selling & distribution overhead 5200 5200

Net profit 14720 9960

Table 3: Statement of Income in marginal costing

Absorption Costing

Serial no. Particulars Quarter 1 Quarter 2

A Standard Units

B opening stock 0 12000

C Units produced 78000 66000

D Sales units 66000 74000

E closing stock(B+C-D) 12000 4000

Cost £ £

F Total variable cost 52000 52000

G Total Fixed Cost 16000 16000

H Selling and distribution overhead 5200 5200

I Total cost(F+G+H) 73200 73200

J Cost of production per unit (I/C) 0.94 1.11

K Value of opening stock (B * J) Nil 13320

L Value of closing stock (E * J) 11280 4440

M Cost of sales (I+K-L) 61920 82080

Table 4: Statement for Cost in absorption costing

Particulars Quarter 1 (£) Quarter 2 (£)

Revenue from sales 80000 80000

Less: marginal cost (F-L) 40720 47560

Contribution 39280 32440

Production Cost 16000 16000

Selling & distribution overhead 5200 5200

Net profit 18080 11240

Table 5: Statement of Income in absorption costing

Microeconomic techniques

What is meant by cost? Different costs and cost analysis

Cost refers to the necessary expenditures of an organisation to run a business. On the other hand,

cost analysis can be stated as a process of breaking down the different components in the overall

expenditure of an organisation. Cost can be subdivided into three parts such as fixed, variable

and semi-variable cost.

Cost-volume profit: Cost volume profit analysis is a process of costing that analyses the impact

of volume and cost of production in an organisation on the profitability. However, fixed cost,

selling price and variable cost per unit are being assumed as constants (Wang et al., 2018).

Flexible budgeting: Flexible budgeting is a process of adjusting the activity and volume levels of

an organisation in accordance with the budget. Comparison between actual and budgeted output

can be ascertained with the help of this method.

Cost variances: Cost variance can be defined as the difference between actual and budget cost of

an organisation. Tracking the progress of Prime Furniture is possible with the help of analysing

cost variances.

Product costing

Fixed and variable costs: Fixed costs do not vary in accordance with the amount of output in

Prime Furniture and rent of the building is an example. Variable cost can fluctuate with the

amount of production and direct labour is an example. Combination of fixed and verbal costs are

regarded as semi-variable cost and example of it is telephone charges in Prime Furniture.

H Selling and distribution overhead 5200 5200

I Total cost(F+G+H) 73200 73200

J Cost of production per unit (I/C) 0.94 1.11

K Value of opening stock (B * J) Nil 13320

L Value of closing stock (E * J) 11280 4440

M Cost of sales (I+K-L) 61920 82080

Table 4: Statement for Cost in absorption costing

Particulars Quarter 1 (£) Quarter 2 (£)

Revenue from sales 80000 80000

Less: marginal cost (F-L) 40720 47560

Contribution 39280 32440

Production Cost 16000 16000

Selling & distribution overhead 5200 5200

Net profit 18080 11240

Table 5: Statement of Income in absorption costing

Microeconomic techniques

What is meant by cost? Different costs and cost analysis

Cost refers to the necessary expenditures of an organisation to run a business. On the other hand,

cost analysis can be stated as a process of breaking down the different components in the overall

expenditure of an organisation. Cost can be subdivided into three parts such as fixed, variable

and semi-variable cost.

Cost-volume profit: Cost volume profit analysis is a process of costing that analyses the impact

of volume and cost of production in an organisation on the profitability. However, fixed cost,

selling price and variable cost per unit are being assumed as constants (Wang et al., 2018).

Flexible budgeting: Flexible budgeting is a process of adjusting the activity and volume levels of

an organisation in accordance with the budget. Comparison between actual and budgeted output

can be ascertained with the help of this method.

Cost variances: Cost variance can be defined as the difference between actual and budget cost of

an organisation. Tracking the progress of Prime Furniture is possible with the help of analysing

cost variances.

Product costing

Fixed and variable costs: Fixed costs do not vary in accordance with the amount of output in

Prime Furniture and rent of the building is an example. Variable cost can fluctuate with the

amount of production and direct labour is an example. Combination of fixed and verbal costs are

regarded as semi-variable cost and example of it is telephone charges in Prime Furniture.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost allocation: Cost allocation refers to the process of distribution of expenditures among

different business centres and units (Yagi and Kokubu, 2018). Prediction of economic effects of

planning along with measuring the cost of inventory and goods sold is possible with the help of

cost allocation.

Normal and standard costing: Normal costing consists of actual data in accordance with

manufacturing overheads whereas, standard costing method uses budgeted costs for the

calculation.

Activity-based costing: Activity-based costing suggests the assigning of overhead expenditures

to products and services. Accurate pricing decision f products in Prime Furniture is possible with

the help of activity-based costing.

Role of costing in setting price: Underestimation of pricing of products can be avoided with the

help of ascertainment of costs for the products in an organisation. On the contrary, exaggeration

of price of products in Prime Furniture can be prevented with the help of cost evaluation. Costing

of production can help the organisation to determine the pricing strategy and target customer.

Cost of inventory

Inventory costs and different types of inventory costs: Inventory cost can be defined as the total

expenditures of procurement of inventory along with transportation cost. There are three types of

inventory costs including ordering, carrying and stock-out expenditures (Taschner and

Charifzadeh, 2016). Replenishing cost of inventory is ordering expenditures and carrying cost

refers to the static viewpoint on inventory. Stock out costs are incurred at the time when stock

out takes place in Prime Furniture.

Benefits of reducing inventory costs to an organisation: Level of inventory can be monitored in

the organisation with the help of reducing cost. Besides that, wastage can be prevented in

accordance with the help of reduction in inventory. Deterioration in storage cost will be possible.

Additionally, shipping expenses will be lowered and these funds can be utilised in other areas of

the business.

Valuation methods: Inventory valuation method refers to the process of evaluation of cost of

goods sold along with profitability of an organisation. First-in-first-out (FIFO) and Last-in-first-

out (LIFO) are widely recognised inventory valuation methods (Mohr, 2017).

Overhead costs: Overhead expenses can be defined as the expenditures related to supporting

activities of production function and it is not directly related with the product or service. Legal

fees, travel expenses and advertising costs can be regarded as overhead expenses of Prime

Furniture.

different business centres and units (Yagi and Kokubu, 2018). Prediction of economic effects of

planning along with measuring the cost of inventory and goods sold is possible with the help of

cost allocation.

Normal and standard costing: Normal costing consists of actual data in accordance with

manufacturing overheads whereas, standard costing method uses budgeted costs for the

calculation.

Activity-based costing: Activity-based costing suggests the assigning of overhead expenditures

to products and services. Accurate pricing decision f products in Prime Furniture is possible with

the help of activity-based costing.

Role of costing in setting price: Underestimation of pricing of products can be avoided with the

help of ascertainment of costs for the products in an organisation. On the contrary, exaggeration

of price of products in Prime Furniture can be prevented with the help of cost evaluation. Costing

of production can help the organisation to determine the pricing strategy and target customer.

Cost of inventory

Inventory costs and different types of inventory costs: Inventory cost can be defined as the total

expenditures of procurement of inventory along with transportation cost. There are three types of

inventory costs including ordering, carrying and stock-out expenditures (Taschner and

Charifzadeh, 2016). Replenishing cost of inventory is ordering expenditures and carrying cost

refers to the static viewpoint on inventory. Stock out costs are incurred at the time when stock

out takes place in Prime Furniture.

Benefits of reducing inventory costs to an organisation: Level of inventory can be monitored in

the organisation with the help of reducing cost. Besides that, wastage can be prevented in

accordance with the help of reduction in inventory. Deterioration in storage cost will be possible.

Additionally, shipping expenses will be lowered and these funds can be utilised in other areas of

the business.

Valuation methods: Inventory valuation method refers to the process of evaluation of cost of

goods sold along with profitability of an organisation. First-in-first-out (FIFO) and Last-in-first-

out (LIFO) are widely recognised inventory valuation methods (Mohr, 2017).

Overhead costs: Overhead expenses can be defined as the expenditures related to supporting

activities of production function and it is not directly related with the product or service. Legal

fees, travel expenses and advertising costs can be regarded as overhead expenses of Prime

Furniture.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO3

P4: Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Using budgets for planning and control:

Preparing a budget & different types of budgets (e.g. capital and operating).

A budget is an estimation for the evaluation of expenses and revenue for the future period of an

organisation (Grossi et al., 2016). Capital budgeting can be defined as a process of the evaluation

of the capital requirements and investments in different projects in an organisation. On the other

hand, operating budget refers to the future prediction of expenditures and income of an

organisation. Operating costs and income can be ascertained in accordance with the future period

in Prime Furniture.

Alternative methods of budgeting: Traditional, zero-based, priority-based and activity-based

budgeting are alternative methods. Zero-based budgeting is a process of adjustment of cost and

expenditures in accordance with the help of a new period (Kamau et al., 2017). Previous

expenditures and income are not considered in the calculation of this method. Besides that,

priority-based budgeting can ascertain the overall tasks in accordance with the help of priorities

to allocate expenditures in Prime Furniture. Traditional historic budget considers all of the past

expenses and income in budgeting calculation. Thereafter, the budget reflects the effects of the

cost allocation of pervious year. Activity based costing method is used to prepare activity based

budgeting in the study.

Behavioural implications of budgets: Budgeting can develop positive behaviour among staffs in

the organisation for achievement of objectives. Additionally, employees from top management to

bottom level of Prime Furniture must participate in the preparation of budgets. All activities and

expenditures in the organisation can be controlled with the help of the preparation of budgets.

Advantages

Budget can be essential for the maximisation of profits in Prime Furniture.

Aim and objectives of the organisation can be attained (Manasan, 2016).

Performance of the organisation can be measured with the help of budgets.

Disadvantages

Budgets can result in uncertain outcomes of the organisation.

Conflictions among functional units in Prime Furniture can be experienced due to the

poor allocation of resources through the help of budgets.

CVP analysis: Cost volume profit analysis can reflect the impact of cost and volume of

production of a product on the profitability of the organisation.

Advantages

Decision-making of Prime Furniture is possible with the help of CVP analysis.

P4: Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Using budgets for planning and control:

Preparing a budget & different types of budgets (e.g. capital and operating).

A budget is an estimation for the evaluation of expenses and revenue for the future period of an

organisation (Grossi et al., 2016). Capital budgeting can be defined as a process of the evaluation

of the capital requirements and investments in different projects in an organisation. On the other

hand, operating budget refers to the future prediction of expenditures and income of an

organisation. Operating costs and income can be ascertained in accordance with the future period

in Prime Furniture.

Alternative methods of budgeting: Traditional, zero-based, priority-based and activity-based

budgeting are alternative methods. Zero-based budgeting is a process of adjustment of cost and

expenditures in accordance with the help of a new period (Kamau et al., 2017). Previous

expenditures and income are not considered in the calculation of this method. Besides that,

priority-based budgeting can ascertain the overall tasks in accordance with the help of priorities

to allocate expenditures in Prime Furniture. Traditional historic budget considers all of the past

expenses and income in budgeting calculation. Thereafter, the budget reflects the effects of the

cost allocation of pervious year. Activity based costing method is used to prepare activity based

budgeting in the study.

Behavioural implications of budgets: Budgeting can develop positive behaviour among staffs in

the organisation for achievement of objectives. Additionally, employees from top management to

bottom level of Prime Furniture must participate in the preparation of budgets. All activities and

expenditures in the organisation can be controlled with the help of the preparation of budgets.

Advantages

Budget can be essential for the maximisation of profits in Prime Furniture.

Aim and objectives of the organisation can be attained (Manasan, 2016).

Performance of the organisation can be measured with the help of budgets.

Disadvantages

Budgets can result in uncertain outcomes of the organisation.

Conflictions among functional units in Prime Furniture can be experienced due to the

poor allocation of resources through the help of budgets.

CVP analysis: Cost volume profit analysis can reflect the impact of cost and volume of

production of a product on the profitability of the organisation.

Advantages

Decision-making of Prime Furniture is possible with the help of CVP analysis.

Cost calculation in the organisation will be easier in respect with the analysis (Armean

and Ardeleanu, 2017)

CVP analysis is easily understandable by the organisation and the management.

Disadvantages

CVP analysis is prone towards the human errors and that can reflect biased data in the

organisation (Lulaj and Iseni, 2018).

Limited number of products can be used for the calculation of CV analysis in the

organisation.

Cashflow analysis: Balance of cash in the organisation can be determined with the help of

Cashflow planning tool.

Advantages

Liquidity of Prime Furniture can be analysed in accordance with the help of cashflow

analysis.

Budgeting and planning can be ascertained in accordance with the help of cashflow

(Rochim and Ghoniyah, 2017).

Performance of Prime Furniture in respect with its competitors can be evaluated with the

help of cashflow analysis.

Disadvantages

Profit earned by Prime Furniture cannot be reflected in accordance with the help of this

analysis.

Industry comparison is not possible with the help of cashflow analysis.

Pricing strategy

Prime Furniture follows up cost based pricing strategy for its products. On the other hand,

competitors follow value based pricing strategy. Advantages of pricing strategy can be regarded

as enhancement in demand of products in the organisation (Patrick et al., 2018). Besides that,

Prime Furniture can be able to obtain competitive advantage in the industry with the help of this

evaluation. Disadvantages of pricing techniques are short term impact and negative effects on

profit margin.

Common costing systems:

Job costing: Job costing is a process of recording of the expenditures of a manufacturing job

other than the process. Reliable estimation on the value of material can be obtained with the help

of this method in Prime Furniture. However, historic expenditures are disadvantages of this

method.

Process costing: Cost is calculated in each process of production. Process can be significant fir

the determination of expenditures in each process. However, cost errors are common in this

method (Biancone et al., 2019).

Batch costing: It is similar to job costing however, it can be affordable than job costing method.

On the other hand, quality control is required in each batch of production.

and Ardeleanu, 2017)

CVP analysis is easily understandable by the organisation and the management.

Disadvantages

CVP analysis is prone towards the human errors and that can reflect biased data in the

organisation (Lulaj and Iseni, 2018).

Limited number of products can be used for the calculation of CV analysis in the

organisation.

Cashflow analysis: Balance of cash in the organisation can be determined with the help of

Cashflow planning tool.

Advantages

Liquidity of Prime Furniture can be analysed in accordance with the help of cashflow

analysis.

Budgeting and planning can be ascertained in accordance with the help of cashflow

(Rochim and Ghoniyah, 2017).

Performance of Prime Furniture in respect with its competitors can be evaluated with the

help of cashflow analysis.

Disadvantages

Profit earned by Prime Furniture cannot be reflected in accordance with the help of this

analysis.

Industry comparison is not possible with the help of cashflow analysis.

Pricing strategy

Prime Furniture follows up cost based pricing strategy for its products. On the other hand,

competitors follow value based pricing strategy. Advantages of pricing strategy can be regarded

as enhancement in demand of products in the organisation (Patrick et al., 2018). Besides that,

Prime Furniture can be able to obtain competitive advantage in the industry with the help of this

evaluation. Disadvantages of pricing techniques are short term impact and negative effects on

profit margin.

Common costing systems:

Job costing: Job costing is a process of recording of the expenditures of a manufacturing job

other than the process. Reliable estimation on the value of material can be obtained with the help

of this method in Prime Furniture. However, historic expenditures are disadvantages of this

method.

Process costing: Cost is calculated in each process of production. Process can be significant fir

the determination of expenditures in each process. However, cost errors are common in this

method (Biancone et al., 2019).

Batch costing: It is similar to job costing however, it can be affordable than job costing method.

On the other hand, quality control is required in each batch of production.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.