Management Accounting: Cost Analysis & Financial Reporting Methods

VerifiedAdded on 2023/01/12

|20

|4161

|75

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and techniques, focusing on cost analysis, financial reporting, and budgeting. It begins by explaining management accounting and its essential requirements, detailing various reporting methods. The report then delves into cost calculation using different techniques, including marginal and absorption costing, and applies management accounting techniques to produce financial reporting documents. It also defines the purpose of budgeting and prepares different budgets, comparing how organizations adapt management accounting systems to respond to financial problems. Finally, it analyzes how management accounting can improve financial performance and evaluates planning tools used to reduce financial problems, offering insights into achieving sustainable success. Desklib provides access to similar solved assignments and past papers for students.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION..................................................................................................................3

PART 1...................................................................................................................................3

Section 1.................................................................................................................................3

1.1) Explain management accounting and various essential requirements of different

types of management accounting systems...................................................................................3

1.2) Explain different methods used for management accounting reporting.....................4

Section 2.................................................................................................................................5

2.1) Calculate costs using appropriate techniques of cost analysis....................................5

2.2) Apply a range of management accounting techniques and produce a financial

reporting document......................................................................................................................8

2.3) Produce financial reports by accurately applying methods and interpret data.........10

PART 2.................................................................................................................................12

Section 3...............................................................................................................................12

3.1) Define and explain the purpose of budget and prepare different budget..................12

Section 4...............................................................................................................................17

4.1) Compare how organisations are adapting management accounting systems to

respond to financial problems....................................................................................................17

4.2) Analyse how management accounting can help to improve the financial

performance of companies to achieve the sustainable success..................................................18

4.3) Evaluate the tools of planning used in management accounting to reduce financial

problems to achieve success......................................................................................................19

CONCLUSION....................................................................................................................19

REFERENCES.....................................................................................................................20

2

INTRODUCTION..................................................................................................................3

PART 1...................................................................................................................................3

Section 1.................................................................................................................................3

1.1) Explain management accounting and various essential requirements of different

types of management accounting systems...................................................................................3

1.2) Explain different methods used for management accounting reporting.....................4

Section 2.................................................................................................................................5

2.1) Calculate costs using appropriate techniques of cost analysis....................................5

2.2) Apply a range of management accounting techniques and produce a financial

reporting document......................................................................................................................8

2.3) Produce financial reports by accurately applying methods and interpret data.........10

PART 2.................................................................................................................................12

Section 3...............................................................................................................................12

3.1) Define and explain the purpose of budget and prepare different budget..................12

Section 4...............................................................................................................................17

4.1) Compare how organisations are adapting management accounting systems to

respond to financial problems....................................................................................................17

4.2) Analyse how management accounting can help to improve the financial

performance of companies to achieve the sustainable success..................................................18

4.3) Evaluate the tools of planning used in management accounting to reduce financial

problems to achieve success......................................................................................................19

CONCLUSION....................................................................................................................19

REFERENCES.....................................................................................................................20

2

INTRODUCTION

Management accounting is an accounting system with the help of which the managers of

the organisation identify, analyse various financial information about the organisation that helps

the financial department to take various decisions (Otley, 2016). Various managerial accounting

reports are formulated by the managers which enable them to supervise all the internal matters

within the organisation and to identify key areas. This report is based on UK based Furniture

Company, UCK furniture. This reports aims to develop an understanding of various aspects of

management accounting, its system and various reporting framework. Apart from this various

methods of estimating the cost are discussed along with their application. It also includes the use

of various planning tools that facilitate an organisation in responding to various financial

problem so faced by the company.

PART 1

Section 1

1.1) Explain management accounting and various essential requirements of different types of

management accounting systems

Management accounting is the process with the help of which the companies analyses and

manages their cost of operations and business. With the help of this various reports are

formulated that facilitate internal management in the decision making process (Renz, 2016).

According to institute of cost and management accounting, it is related with the application of

professional skills for managing various accounting information in such a manner that the

organisation can formulate various policies and strategies so that they can achieve their

objectives. UCK furniture can use different management accounting system that can help them in

improving their productivity and profitability:

Cost management system: This accounting system is considered to be one of the most

important system as with the help of this the UCK determines the total of their final products i.e.,

their furniture. The valuation of inventory is done; the cost of labour is estimated with the help of

the profitability is estimated. It enables the managers of UCK in identifying the area from where

they can reduce the cost for the company, also this enables them to ensure the efficient utilisation

of the resources (Akbar, 2010).

3

Management accounting is an accounting system with the help of which the managers of

the organisation identify, analyse various financial information about the organisation that helps

the financial department to take various decisions (Otley, 2016). Various managerial accounting

reports are formulated by the managers which enable them to supervise all the internal matters

within the organisation and to identify key areas. This report is based on UK based Furniture

Company, UCK furniture. This reports aims to develop an understanding of various aspects of

management accounting, its system and various reporting framework. Apart from this various

methods of estimating the cost are discussed along with their application. It also includes the use

of various planning tools that facilitate an organisation in responding to various financial

problem so faced by the company.

PART 1

Section 1

1.1) Explain management accounting and various essential requirements of different types of

management accounting systems

Management accounting is the process with the help of which the companies analyses and

manages their cost of operations and business. With the help of this various reports are

formulated that facilitate internal management in the decision making process (Renz, 2016).

According to institute of cost and management accounting, it is related with the application of

professional skills for managing various accounting information in such a manner that the

organisation can formulate various policies and strategies so that they can achieve their

objectives. UCK furniture can use different management accounting system that can help them in

improving their productivity and profitability:

Cost management system: This accounting system is considered to be one of the most

important system as with the help of this the UCK determines the total of their final products i.e.,

their furniture. The valuation of inventory is done; the cost of labour is estimated with the help of

the profitability is estimated. It enables the managers of UCK in identifying the area from where

they can reduce the cost for the company, also this enables them to ensure the efficient utilisation

of the resources (Akbar, 2010).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price optimisation system: With the help of this system the best price for the product can

be determined by the organisation as per the willingness to pay of the customer. The UCK

furniture can set prices for the furniture as per the reactions of the customers so that they can be

satisfied. With the help of this they can identify the scope for the promotional activities,

discounts that they can provide to the clients and many more as they has to be adjusted within the

cost of the furniture.

Inventory management system: Management of the inventory is important for each and

every organisation as with this they can efficient manage their cost. For UCK furniture it

includes the management of the flow of the material in the organisation and flow of the finished

goods, also in this the production of the furniture must be scheduled efficiently so that the stock

can be made available all the time. They can use various methods such as LIFO, FIFO method

which ensures the flow of the inventory. With LIFO method, the material which is purchased in

the last must be sold first as they believed that the last item is priced more than the previous

material. While in FIFO method the material first purchase must be sold first as with this they

can manage their cost which is recorded first against sales. For UCK furniture FIFO method is

suitable as with this they can manage their records efficiently and their designs of furniture will

also not become outdated (Senftlechner and Hiebl, 2015).

All these methods will enable UCK furniture to utilise all their financial information so

that they can make efficient decisions related to the reduction of the overall cost of the company.

Also with the help of this they can formulate various strategies that can help UCK furniture in

achieving their goals by improving their profitability and productivity.

1.2) Explain different methods used for management accounting reporting

The organisations need to use various management accounting reporting so that they can

let their management know about the exact situation prevailing in the organisation. These reports

are formulated by the managers on the basis of information received by the cost accountant

managers from other departments (Hopper and Bui, 2016). The reports that UCK furniture need

to prepare are:

Cost accounting managerial report: With the help of this report the prices of the

product so produced by the company can be estimated as it includes cost of all the items such as

raw material, labour, other indirect cost etc. The cost sheet is prepared with which per unit cost is

estimated by dividing the total cost with the number of units produced by the company. This cost

4

be determined by the organisation as per the willingness to pay of the customer. The UCK

furniture can set prices for the furniture as per the reactions of the customers so that they can be

satisfied. With the help of this they can identify the scope for the promotional activities,

discounts that they can provide to the clients and many more as they has to be adjusted within the

cost of the furniture.

Inventory management system: Management of the inventory is important for each and

every organisation as with this they can efficient manage their cost. For UCK furniture it

includes the management of the flow of the material in the organisation and flow of the finished

goods, also in this the production of the furniture must be scheduled efficiently so that the stock

can be made available all the time. They can use various methods such as LIFO, FIFO method

which ensures the flow of the inventory. With LIFO method, the material which is purchased in

the last must be sold first as they believed that the last item is priced more than the previous

material. While in FIFO method the material first purchase must be sold first as with this they

can manage their cost which is recorded first against sales. For UCK furniture FIFO method is

suitable as with this they can manage their records efficiently and their designs of furniture will

also not become outdated (Senftlechner and Hiebl, 2015).

All these methods will enable UCK furniture to utilise all their financial information so

that they can make efficient decisions related to the reduction of the overall cost of the company.

Also with the help of this they can formulate various strategies that can help UCK furniture in

achieving their goals by improving their profitability and productivity.

1.2) Explain different methods used for management accounting reporting

The organisations need to use various management accounting reporting so that they can

let their management know about the exact situation prevailing in the organisation. These reports

are formulated by the managers on the basis of information received by the cost accountant

managers from other departments (Hopper and Bui, 2016). The reports that UCK furniture need

to prepare are:

Cost accounting managerial report: With the help of this report the prices of the

product so produced by the company can be estimated as it includes cost of all the items such as

raw material, labour, other indirect cost etc. The cost sheet is prepared with which per unit cost is

estimated by dividing the total cost with the number of units produced by the company. This cost

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

report will make the managers of UCK capable of understanding the impact of various factors on

the total cost so that they can be managed efficiently.

Performance report: The performance report will enable the managers of UCK furniture

in analysing the performance of the company. This report can be prepared on the basis of the

reports of different departments. On the basis of this the managers take the necessary decisions

so that they can improve the performances and can achieve the objectives. The departments

which are not performing well must be identified and various strategies must be formulated for

them so that their performances can be improved (Honggowati and et.al., 2017).

Critically evaluate how management accounting system and management accounting is

integrated in the organisational processes

It is analysed that for each and every organisation it is very important to adopt various

management accounting system and reporting methods so that they can take necessary decisions

and improve their performances. The reports such as performances reports enable the investors

and other stakeholders of the company in analysing their profitability according to which they

take their decisions regarding investments. Along with this the internal management can be

efficient enough to manage their costs and expenses by analysing them.

Section 2

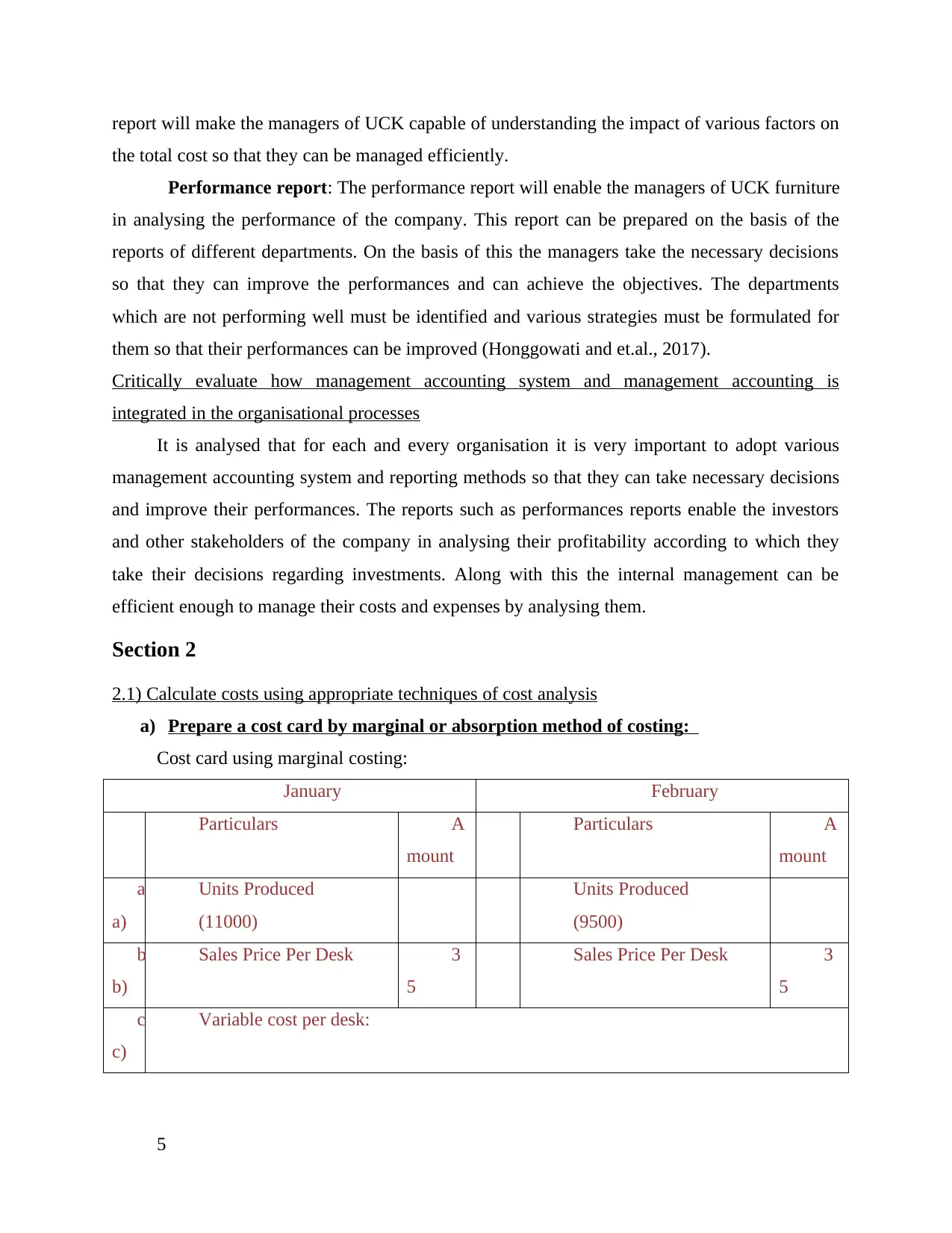

2.1) Calculate costs using appropriate techniques of cost analysis

a) Prepare a cost card by marginal or absorption method of costing:

Cost card using marginal costing:

January February

Particulars A

mount

Particulars A

mount

a

a)

Units Produced

(11000)

Units Produced

(9500)

b

b)

Sales Price Per Desk 3

5

Sales Price Per Desk 3

5

c

c)

Variable cost per desk:

5

the total cost so that they can be managed efficiently.

Performance report: The performance report will enable the managers of UCK furniture

in analysing the performance of the company. This report can be prepared on the basis of the

reports of different departments. On the basis of this the managers take the necessary decisions

so that they can improve the performances and can achieve the objectives. The departments

which are not performing well must be identified and various strategies must be formulated for

them so that their performances can be improved (Honggowati and et.al., 2017).

Critically evaluate how management accounting system and management accounting is

integrated in the organisational processes

It is analysed that for each and every organisation it is very important to adopt various

management accounting system and reporting methods so that they can take necessary decisions

and improve their performances. The reports such as performances reports enable the investors

and other stakeholders of the company in analysing their profitability according to which they

take their decisions regarding investments. Along with this the internal management can be

efficient enough to manage their costs and expenses by analysing them.

Section 2

2.1) Calculate costs using appropriate techniques of cost analysis

a) Prepare a cost card by marginal or absorption method of costing:

Cost card using marginal costing:

January February

Particulars A

mount

Particulars A

mount

a

a)

Units Produced

(11000)

Units Produced

(9500)

b

b)

Sales Price Per Desk 3

5

Sales Price Per Desk 3

5

c

c)

Variable cost per desk:

5

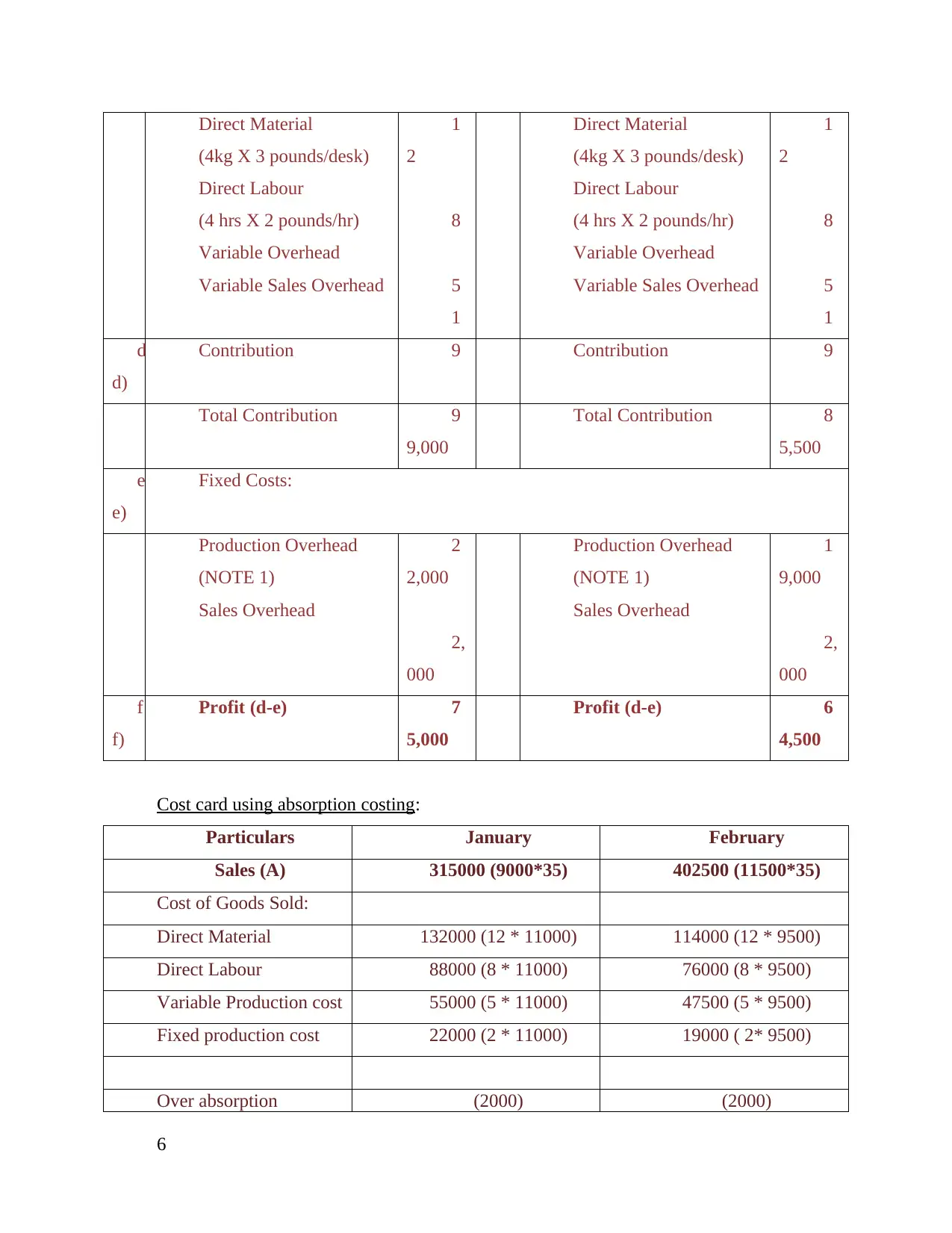

Direct Material

(4kg X 3 pounds/desk)

Direct Labour

(4 hrs X 2 pounds/hr)

Variable Overhead

Variable Sales Overhead

1

2

8

5

1

Direct Material

(4kg X 3 pounds/desk)

Direct Labour

(4 hrs X 2 pounds/hr)

Variable Overhead

Variable Sales Overhead

1

2

8

5

1

d

d)

Contribution 9 Contribution 9

Total Contribution 9

9,000

Total Contribution 8

5,500

e

e)

Fixed Costs:

Production Overhead

(NOTE 1)

Sales Overhead

2

2,000

2,

000

Production Overhead

(NOTE 1)

Sales Overhead

1

9,000

2,

000

f

f)

Profit (d-e) 7

5,000

Profit (d-e) 6

4,500

Cost card using absorption costing:

Particulars January February

Sales (A) 315000 (9000*35) 402500 (11500*35)

Cost of Goods Sold:

Direct Material 132000 (12 * 11000) 114000 (12 * 9500)

Direct Labour 88000 (8 * 11000) 76000 (8 * 9500)

Variable Production cost 55000 (5 * 11000) 47500 (5 * 9500)

Fixed production cost 22000 (2 * 11000) 19000 ( 2* 9500)

Over absorption (2000) (2000)

6

(4kg X 3 pounds/desk)

Direct Labour

(4 hrs X 2 pounds/hr)

Variable Overhead

Variable Sales Overhead

1

2

8

5

1

Direct Material

(4kg X 3 pounds/desk)

Direct Labour

(4 hrs X 2 pounds/hr)

Variable Overhead

Variable Sales Overhead

1

2

8

5

1

d

d)

Contribution 9 Contribution 9

Total Contribution 9

9,000

Total Contribution 8

5,500

e

e)

Fixed Costs:

Production Overhead

(NOTE 1)

Sales Overhead

2

2,000

2,

000

Production Overhead

(NOTE 1)

Sales Overhead

1

9,000

2,

000

f

f)

Profit (d-e) 7

5,000

Profit (d-e) 6

4,500

Cost card using absorption costing:

Particulars January February

Sales (A) 315000 (9000*35) 402500 (11500*35)

Cost of Goods Sold:

Direct Material 132000 (12 * 11000) 114000 (12 * 9500)

Direct Labour 88000 (8 * 11000) 76000 (8 * 9500)

Variable Production cost 55000 (5 * 11000) 47500 (5 * 9500)

Fixed production cost 22000 (2 * 11000) 19000 ( 2* 9500)

Over absorption (2000) (2000)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Loosing stock (27 *

2000)

(54000) (54000)

Total (B) 241000 200500

Profit (A-B) 74,000 202,000

NOTE1

Production overhead is considered taking into account average production each month, i.e.

10000 units.

Hence, for January overhead amount = (20,000 / 10,000) * 11000

Hence, for February, the overhead amount = (20,000 / 10,000) * 9500

b) Potential merits and demerits of absorption costing and marginal costing

Merits and Demerits of Absorption costing:

Merits: With the help of absorption costing all the cost related to the production can be taken

into consideration as while making calculation all the fixed cost are considered. This will enable

the management of UCK furniture in getting the true picture of the total cost of the company.

Along with this accurate picture of the profitability of the company can be drawn as all the cost

will be deducted. The managers can be held responsible for the cost and services of different

departments as correct allocation is facilitated by this method of costing.

Demerits: As in this both fixed and variable cost is included it cannot be used by the managers

for the decision making and planning as in this the current situation needs to be analysed which

require assessment of the variable cost. Also it does not reflect the appropriate performance of

the organisation (Chenhall and Moers, 2015).

Merits and Demerits of Marginal costing:

Merits: With the help of this costing method the cost can be classified into variable and fixed

cost and this enable the management to focus upon the variable cost so that they can control the

total cost of the company. Along with this the performance of each department can be evaluated

as in this with additional cost the performance can be compared. In addition to this the decision

7

2000)

(54000) (54000)

Total (B) 241000 200500

Profit (A-B) 74,000 202,000

NOTE1

Production overhead is considered taking into account average production each month, i.e.

10000 units.

Hence, for January overhead amount = (20,000 / 10,000) * 11000

Hence, for February, the overhead amount = (20,000 / 10,000) * 9500

b) Potential merits and demerits of absorption costing and marginal costing

Merits and Demerits of Absorption costing:

Merits: With the help of absorption costing all the cost related to the production can be taken

into consideration as while making calculation all the fixed cost are considered. This will enable

the management of UCK furniture in getting the true picture of the total cost of the company.

Along with this accurate picture of the profitability of the company can be drawn as all the cost

will be deducted. The managers can be held responsible for the cost and services of different

departments as correct allocation is facilitated by this method of costing.

Demerits: As in this both fixed and variable cost is included it cannot be used by the managers

for the decision making and planning as in this the current situation needs to be analysed which

require assessment of the variable cost. Also it does not reflect the appropriate performance of

the organisation (Chenhall and Moers, 2015).

Merits and Demerits of Marginal costing:

Merits: With the help of this costing method the cost can be classified into variable and fixed

cost and this enable the management to focus upon the variable cost so that they can control the

total cost of the company. Along with this the performance of each department can be evaluated

as in this with additional cost the performance can be compared. In addition to this the decision

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

making with this method of costing becomes easier as on the basis of additional cost selling price

decisions, selection of suitable product mix can be taken easily.

Demerits: The exclusion of the fixed cost from the total cost affects the fair picture of the

performance. The relation of the variable expenses with the output may not be linear at different

operating level due to which it may affect the decisions. Also the separation of the cost among

fixed and variable is considered difficult as per marginal costing method (Modell, 2014).

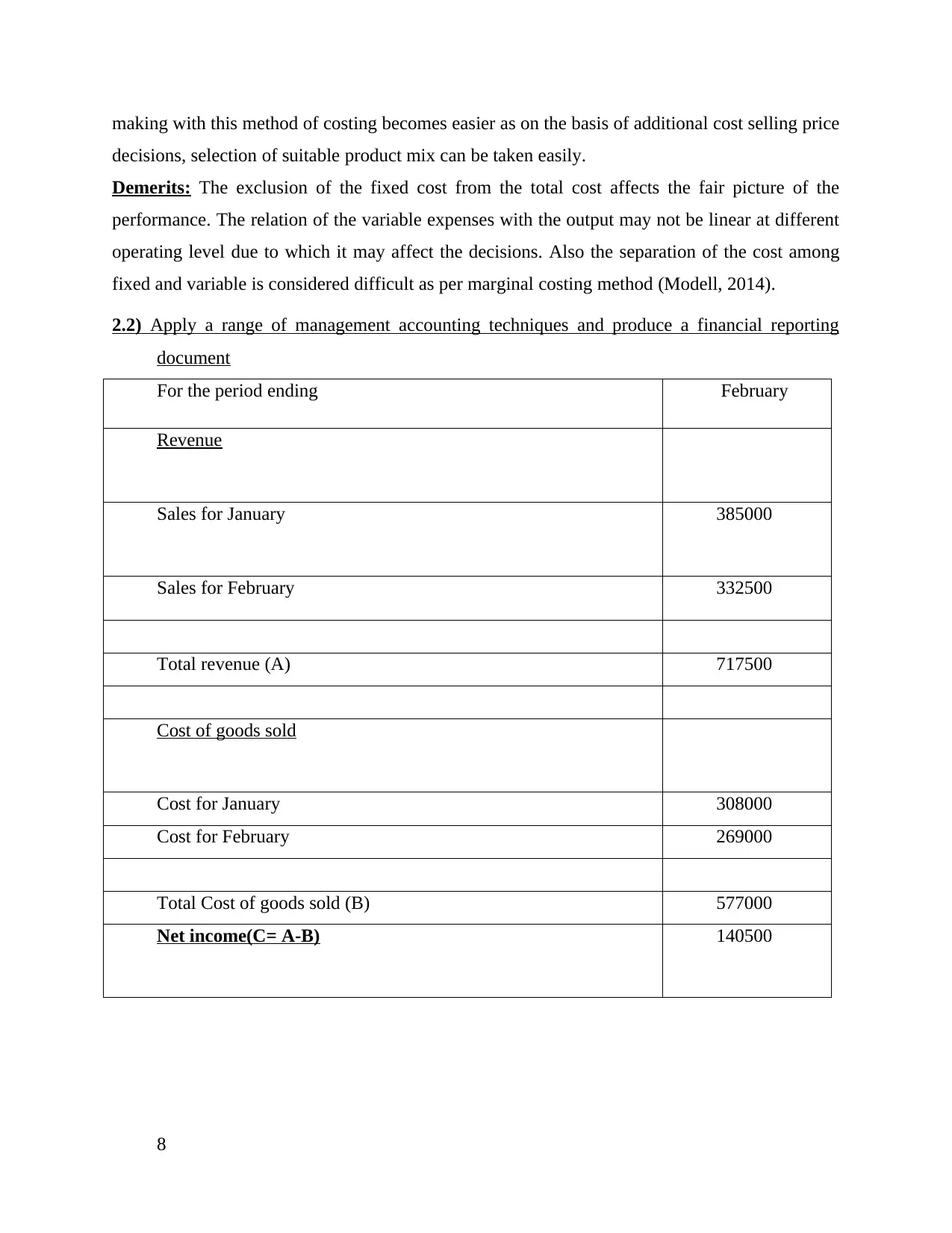

2.2) Apply a range of management accounting techniques and produce a financial reporting

document

For the period ending February

Revenue

Sales for January 385000

Sales for February 332500

Total revenue (A) 717500

Cost of goods sold

Cost for January 308000

Cost for February 269000

Total Cost of goods sold (B) 577000

Net income(C= A-B) 140500

8

decisions, selection of suitable product mix can be taken easily.

Demerits: The exclusion of the fixed cost from the total cost affects the fair picture of the

performance. The relation of the variable expenses with the output may not be linear at different

operating level due to which it may affect the decisions. Also the separation of the cost among

fixed and variable is considered difficult as per marginal costing method (Modell, 2014).

2.2) Apply a range of management accounting techniques and produce a financial reporting

document

For the period ending February

Revenue

Sales for January 385000

Sales for February 332500

Total revenue (A) 717500

Cost of goods sold

Cost for January 308000

Cost for February 269000

Total Cost of goods sold (B) 577000

Net income(C= A-B) 140500

8

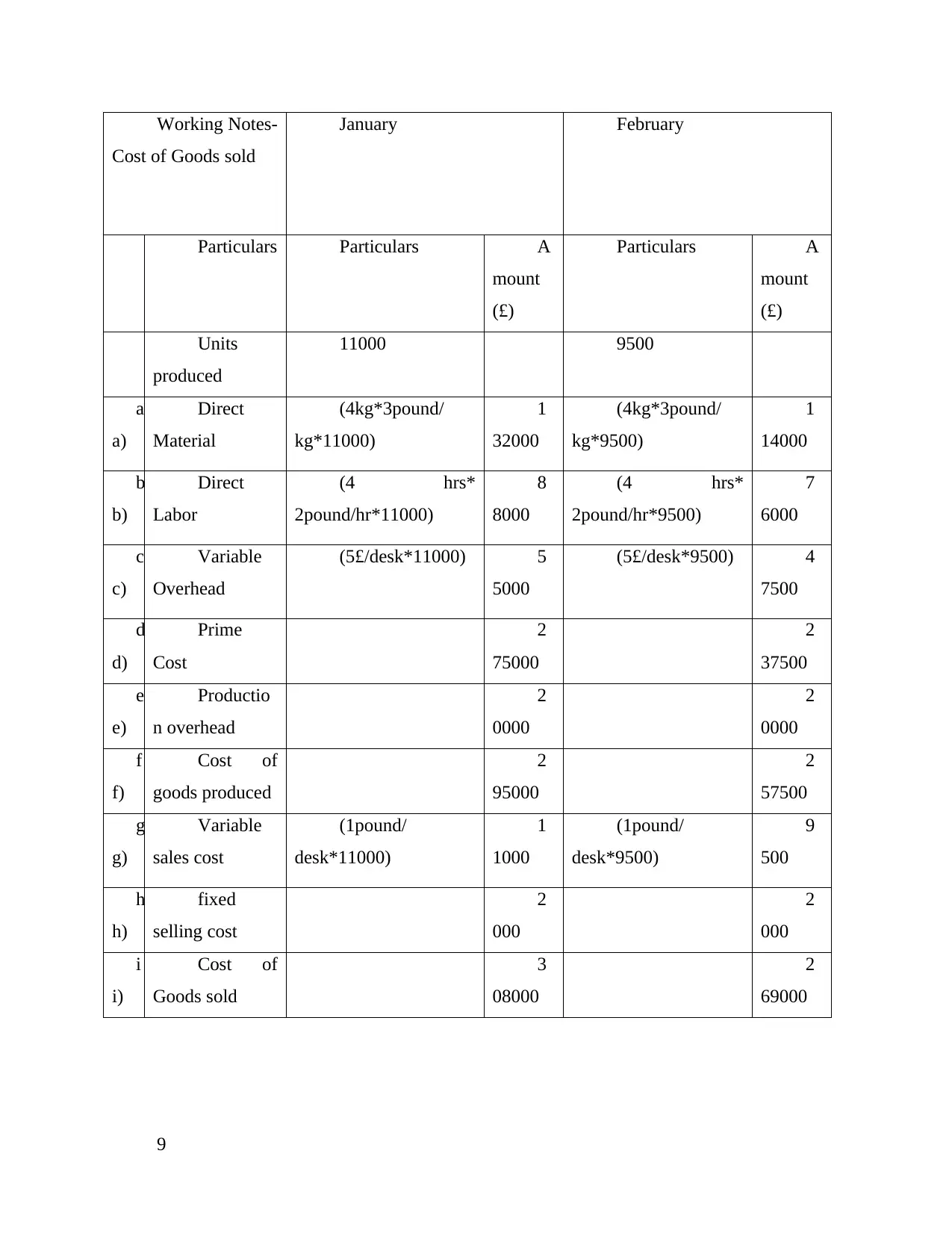

Working Notes-

Cost of Goods sold

January February

Particulars Particulars A

mount

(£)

Particulars A

mount

(£)

Units

produced

11000 9500

a

a)

Direct

Material

(4kg*3pound/

kg*11000)

1

32000

(4kg*3pound/

kg*9500)

1

14000

b

b)

Direct

Labor

(4 hrs*

2pound/hr*11000)

8

8000

(4 hrs*

2pound/hr*9500)

7

6000

c

c)

Variable

Overhead

(5£/desk*11000) 5

5000

(5£/desk*9500) 4

7500

d

d)

Prime

Cost

2

75000

2

37500

e

e)

Productio

n overhead

2

0000

2

0000

f

f)

Cost of

goods produced

2

95000

2

57500

g

g)

Variable

sales cost

(1pound/

desk*11000)

1

1000

(1pound/

desk*9500)

9

500

h

h)

fixed

selling cost

2

000

2

000

i

i)

Cost of

Goods sold

3

08000

2

69000

9

Cost of Goods sold

January February

Particulars Particulars A

mount

(£)

Particulars A

mount

(£)

Units

produced

11000 9500

a

a)

Direct

Material

(4kg*3pound/

kg*11000)

1

32000

(4kg*3pound/

kg*9500)

1

14000

b

b)

Direct

Labor

(4 hrs*

2pound/hr*11000)

8

8000

(4 hrs*

2pound/hr*9500)

7

6000

c

c)

Variable

Overhead

(5£/desk*11000) 5

5000

(5£/desk*9500) 4

7500

d

d)

Prime

Cost

2

75000

2

37500

e

e)

Productio

n overhead

2

0000

2

0000

f

f)

Cost of

goods produced

2

95000

2

57500

g

g)

Variable

sales cost

(1pound/

desk*11000)

1

1000

(1pound/

desk*9500)

9

500

h

h)

fixed

selling cost

2

000

2

000

i

i)

Cost of

Goods sold

3

08000

2

69000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Here, absorption method of costing is used as with the help of this method of costing all

the cost incurred to the company in making the product a finial good are included. All such

cost are merged in one cost i.e, cost of producing the good.

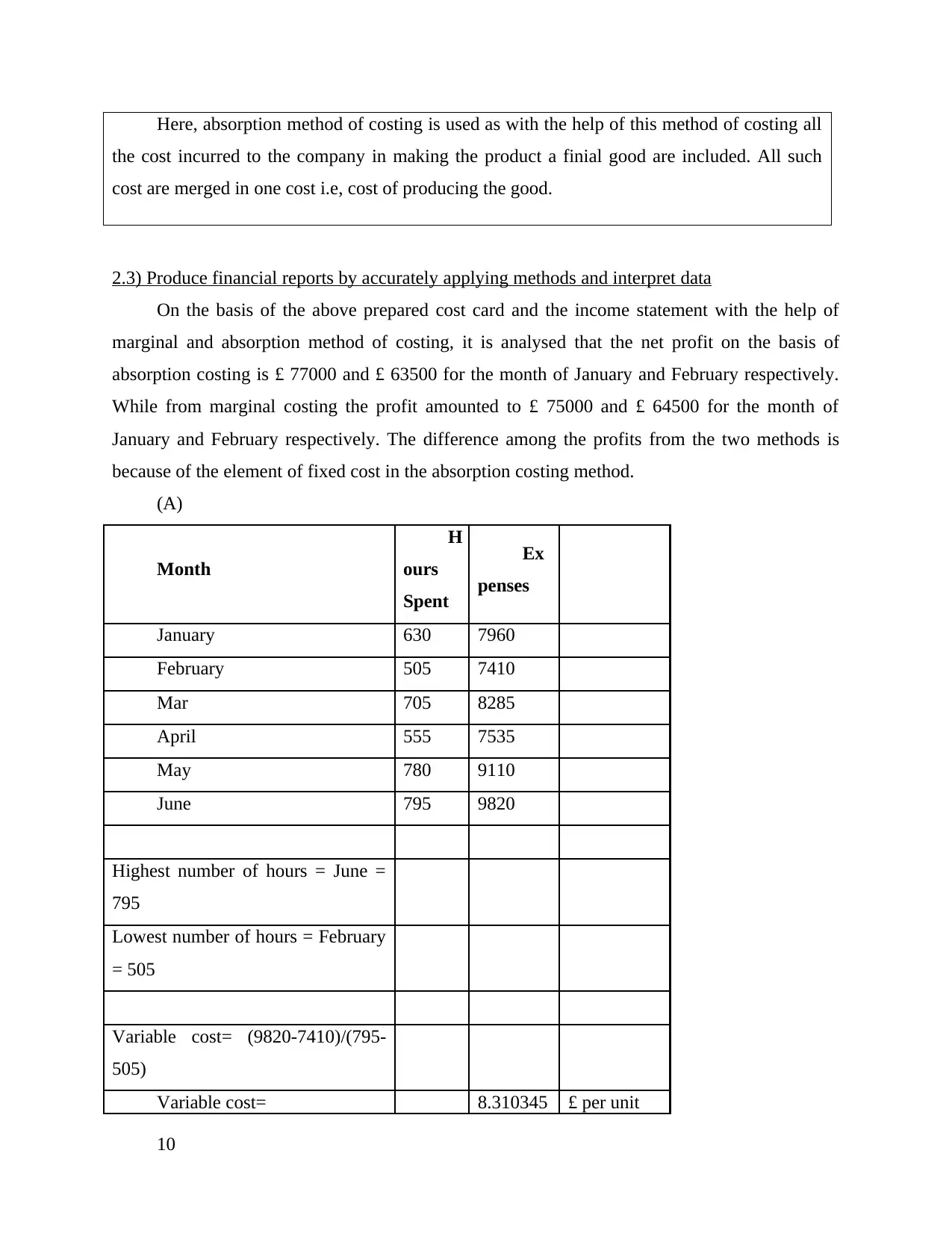

2.3) Produce financial reports by accurately applying methods and interpret data

On the basis of the above prepared cost card and the income statement with the help of

marginal and absorption method of costing, it is analysed that the net profit on the basis of

absorption costing is £ 77000 and £ 63500 for the month of January and February respectively.

While from marginal costing the profit amounted to £ 75000 and £ 64500 for the month of

January and February respectively. The difference among the profits from the two methods is

because of the element of fixed cost in the absorption costing method.

(A)

Month

H

ours

Spent

Ex

penses

January 630 7960

February 505 7410

Mar 705 8285

April 555 7535

May 780 9110

June 795 9820

Highest number of hours = June =

795

Lowest number of hours = February

= 505

Variable cost= (9820-7410)/(795-

505)

Variable cost= 8.310345 £ per unit

10

the cost incurred to the company in making the product a finial good are included. All such

cost are merged in one cost i.e, cost of producing the good.

2.3) Produce financial reports by accurately applying methods and interpret data

On the basis of the above prepared cost card and the income statement with the help of

marginal and absorption method of costing, it is analysed that the net profit on the basis of

absorption costing is £ 77000 and £ 63500 for the month of January and February respectively.

While from marginal costing the profit amounted to £ 75000 and £ 64500 for the month of

January and February respectively. The difference among the profits from the two methods is

because of the element of fixed cost in the absorption costing method.

(A)

Month

H

ours

Spent

Ex

penses

January 630 7960

February 505 7410

Mar 705 8285

April 555 7535

May 780 9110

June 795 9820

Highest number of hours = June =

795

Lowest number of hours = February

= 505

Variable cost= (9820-7410)/(795-

505)

Variable cost= 8.310345 £ per unit

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

fixed cost= 9820 - (795*8.31)

fixed cost= 3213.55 £

expenses for july= 3213.55 +

(650*8.31)

expenses for july= 8615.05 £

expenses for august= 3213.55

+ (750*8.31)

expenses for august= 9446.05 £

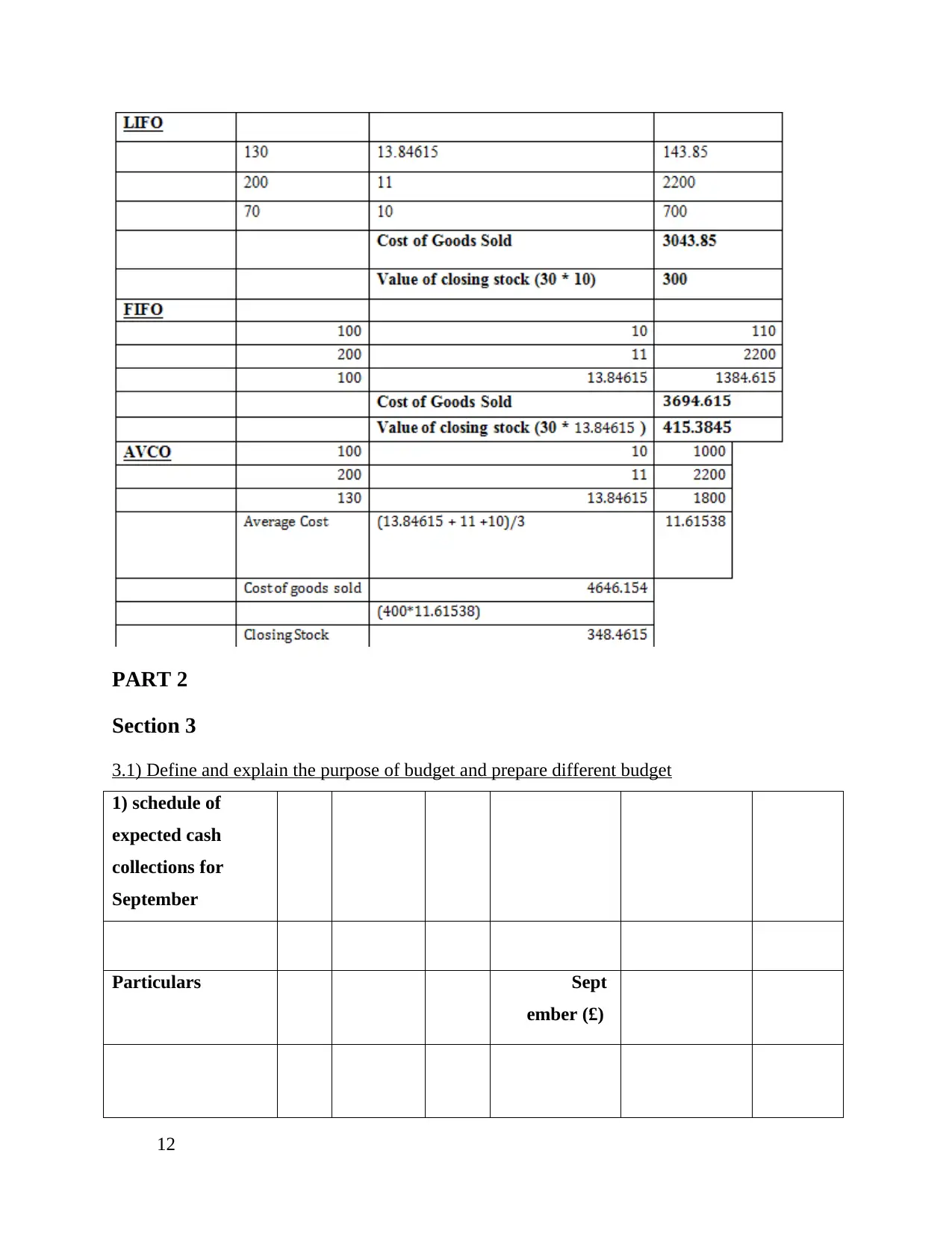

(B)

11

fixed cost= 3213.55 £

expenses for july= 3213.55 +

(650*8.31)

expenses for july= 8615.05 £

expenses for august= 3213.55

+ (750*8.31)

expenses for august= 9446.05 £

(B)

11

PART 2

Section 3

3.1) Define and explain the purpose of budget and prepare different budget

1) schedule of

expected cash

collections for

September

Particulars Sept

ember (£)

12

Section 3

3.1) Define and explain the purpose of budget and prepare different budget

1) schedule of

expected cash

collections for

September

Particulars Sept

ember (£)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.