ACCT6004: Cost Accounting Analysis, Inventory Management, and Ethics

VerifiedAdded on 2024/07/12

|8

|1113

|55

Homework Assignment

AI Summary

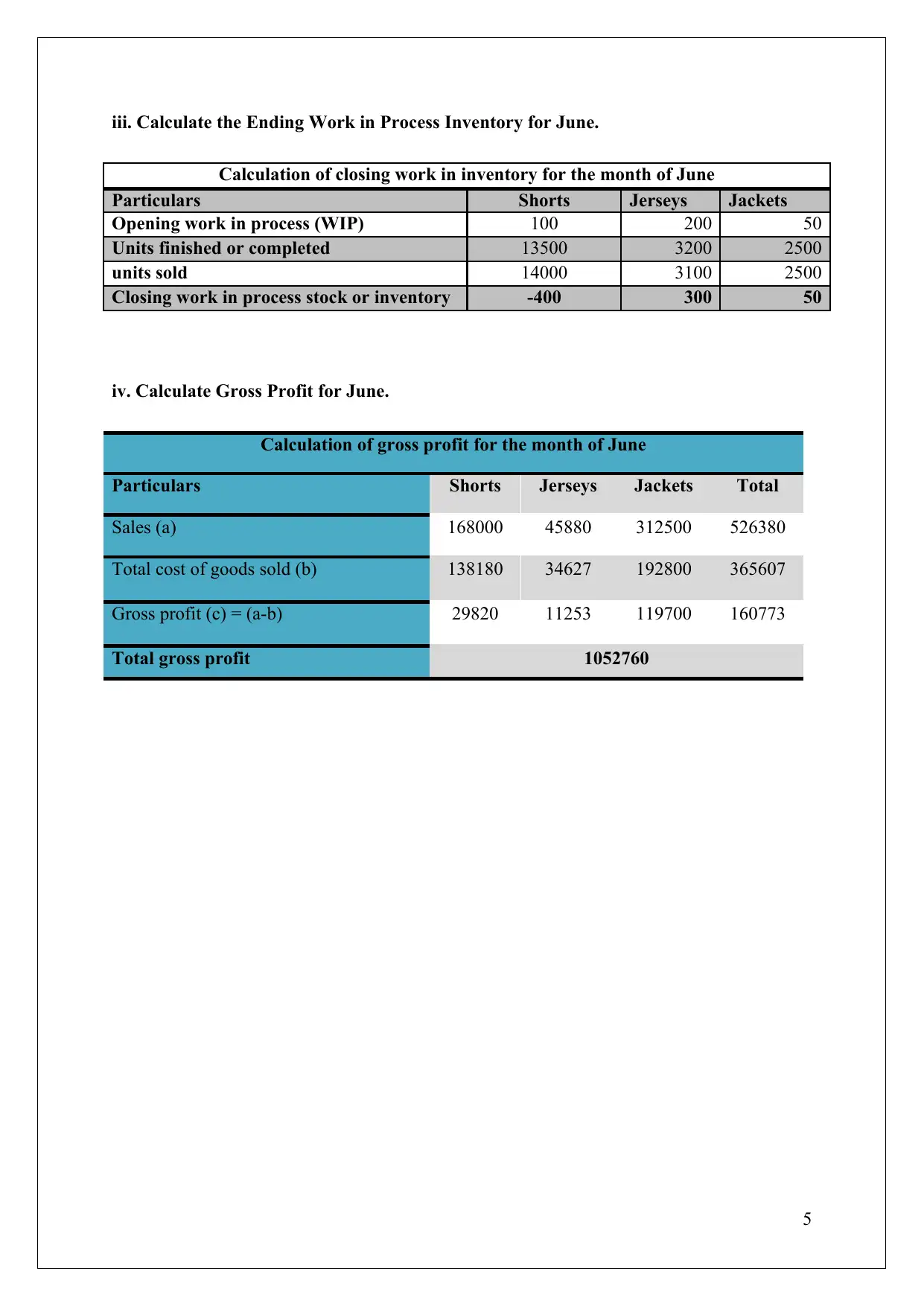

This assignment solution provides a detailed analysis of manufacturing costs, cost of goods manufactured, and ending work-in-process inventory for J&B Sports. It includes calculations for predetermined overhead rates, gross profit, and an assessment of inventory changes for shorts, jerseys, and jackets. The solution also addresses the ethical implications of accounting adjustments, referencing the Australian Accounting code of ethics, and discusses potential monetary and non-monetary costs associated with unethical practices. Desklib offers a platform for students to access similar solved assignments and study resources.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.