Management Accounting: Techniques, Reporting, and Cost Analysis

VerifiedAdded on 2023/01/03

|20

|4179

|66

Report

AI Summary

This report provides a detailed analysis of management accounting, emphasizing its techniques in financial reporting for companies. It explores how management accounting aids managers in making informed decisions to achieve both short-term and long-term business objectives. The report covers various aspects, including cost analysis, inventory valuation, investment analysis, cash flow analysis, constraint analysis, and financial leverage. It also discusses different methods used for management accounting reporting, such as budget reports, pro forma cash flow statements, sales reports, item cost reports, job costing, inventory valuation, order information reports, opportunity reports, and performance reports. Furthermore, the report includes a cost analysis comparing absorption and marginal costing, along with practical examples and inventory ledger using LIFO and average cost methods. The study highlights how organizations address financial challenges using management accounting techniques, making it a valuable resource for understanding financial planning and budgetary control. Desklib provides access to this and other solved assignments for students.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

P1 Management accounting and importance of its different types..............................................3

P2 Methods used for management accounting reporting............................................................6

P3 Cost analysis...........................................................................................................................8

P4 Planning tools used for budgetary control............................................................................13

P5 Comparison of companies of how they have responded to financial problems using

management accounting............................................................................................................15

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................3

P1 Management accounting and importance of its different types..............................................3

P2 Methods used for management accounting reporting............................................................6

P3 Cost analysis...........................................................................................................................8

P4 Planning tools used for budgetary control............................................................................13

P5 Comparison of companies of how they have responded to financial problems using

management accounting............................................................................................................15

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

This study discusses management accounting and its techniques in financial reports of a

company. Management accounting is the reports of accounting statements used by managers in

which process identifies, interprets and analyses information used to achieve business objectives.

The management accounting techniques help a business understand its finances and allocates

them in right proportion to help cost management. Several types of planning tools are discussed

which help understand financial planning and ways to achieve the goals with budgetary control.

Light has been thrown on comparisons of how organisations are dealing with financial problems

with management accounting techniques.

P1 Management accounting and importance of its different types

Management accounting is used by managers in a business to make reports about business

operations that help them in taking decisions of how to achieve short term and long-term

objectives of the company. The main purpose of using management accounting is to achieve

business goals for the company. Some functions of management accounting are as listed:

a) Forecasting: It helps in forecasting whether a decision to buy an equipment, to

venture in new markets or to go for acquisition would be benefiting to the company

or not thus doing the analysis on future possibilities (Ameen, Ahmed and Abd

Hafez, , 2018).

b) Management accounting has a know how of costs and production department and

thus helps in decision-making of whether to go with purchases of material or not.

c) Management accounting helps in knowing where the funds are going to come from

and what will be the expenses occurred in a project.

Types of Management Accounting

There are few types of managerial accounting involving different aspects. Some of them are:

This study discusses management accounting and its techniques in financial reports of a

company. Management accounting is the reports of accounting statements used by managers in

which process identifies, interprets and analyses information used to achieve business objectives.

The management accounting techniques help a business understand its finances and allocates

them in right proportion to help cost management. Several types of planning tools are discussed

which help understand financial planning and ways to achieve the goals with budgetary control.

Light has been thrown on comparisons of how organisations are dealing with financial problems

with management accounting techniques.

P1 Management accounting and importance of its different types

Management accounting is used by managers in a business to make reports about business

operations that help them in taking decisions of how to achieve short term and long-term

objectives of the company. The main purpose of using management accounting is to achieve

business goals for the company. Some functions of management accounting are as listed:

a) Forecasting: It helps in forecasting whether a decision to buy an equipment, to

venture in new markets or to go for acquisition would be benefiting to the company

or not thus doing the analysis on future possibilities (Ameen, Ahmed and Abd

Hafez, , 2018).

b) Management accounting has a know how of costs and production department and

thus helps in decision-making of whether to go with purchases of material or not.

c) Management accounting helps in knowing where the funds are going to come from

and what will be the expenses occurred in a project.

Types of Management Accounting

There are few types of managerial accounting involving different aspects. Some of them are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost Analysis

The costs going in manufacturing products from the process of acquiring raw materials,

converting them in finished goods involve costs of fixed and variable expenses along with

overheads. All the costs are taken in consideration and added up to form the total production cost

of manufacturing products. After knowing the cost valuation the total amount of goods produced

is calculated. Then the total costs are divided by the total quantity produced to get the per unit

cost of goods. A profit margin is then set after doing market survey and thus the selling price of

products is determined. Apart from this inventory valuation is also done which is according to

per square foot cost of storing inventory (Abdusalomova, 2019).

Inventory Turnover Analysis

Calculation of the number of times inventory has been sold and replaced is done. The faster the

inventory is sold out the better it is for the company as sales are increased with utilisation of

current assets and storage costs are reduced. It also helps in knowing when to place the orders for

the next inventory batch.

Investment Analysis

A company is faced with decision-making between projects as to which project will be more

investment worthy. Management accounting helps in assessing the rate of return on projects with

discounted cash flows estimated to accommodate the time value of money concept. These

financial calculations help in zeroing on the project which can maximize returns (Ameen,

Ahmed and Abd Hafez, 2018).

Cash flow Analysis

Management accounting helps know the cash impact on the business and follow accrual

accounting in which the income and expense are recorded together to give a clear picture of

company’s liquidity. It helps in balancing net working capital required for managing business

operations. It ensures the cash flow is there to fulfil the short-term obligations of the business. In

investment projects, it lays down cash flow estimates which will be received apart from the cash

outflow. In purchasing equipment it lays down options of whether to use company’s equity or a

loan at interest and gauging which will be a better option.

The costs going in manufacturing products from the process of acquiring raw materials,

converting them in finished goods involve costs of fixed and variable expenses along with

overheads. All the costs are taken in consideration and added up to form the total production cost

of manufacturing products. After knowing the cost valuation the total amount of goods produced

is calculated. Then the total costs are divided by the total quantity produced to get the per unit

cost of goods. A profit margin is then set after doing market survey and thus the selling price of

products is determined. Apart from this inventory valuation is also done which is according to

per square foot cost of storing inventory (Abdusalomova, 2019).

Inventory Turnover Analysis

Calculation of the number of times inventory has been sold and replaced is done. The faster the

inventory is sold out the better it is for the company as sales are increased with utilisation of

current assets and storage costs are reduced. It also helps in knowing when to place the orders for

the next inventory batch.

Investment Analysis

A company is faced with decision-making between projects as to which project will be more

investment worthy. Management accounting helps in assessing the rate of return on projects with

discounted cash flows estimated to accommodate the time value of money concept. These

financial calculations help in zeroing on the project which can maximize returns (Ameen,

Ahmed and Abd Hafez, 2018).

Cash flow Analysis

Management accounting helps know the cash impact on the business and follow accrual

accounting in which the income and expense are recorded together to give a clear picture of

company’s liquidity. It helps in balancing net working capital required for managing business

operations. It ensures the cash flow is there to fulfil the short-term obligations of the business. In

investment projects, it lays down cash flow estimates which will be received apart from the cash

outflow. In purchasing equipment it lays down options of whether to use company’s equity or a

loan at interest and gauging which will be a better option.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Constraint Analysis

Management accounting helps in realising constraints in the line of production and sales. An

optimum utilisation of assets is good but sometimes it may happen that goods are manufactured

according to the set rhythm but sales is not up to the mark. This will result in piling up of

inventory and storage costs increase but no increase in revenues. Management accounting sees to

it which constraints can come in between company’s set goal and makes aware of measures to

remove constraints timely.

Financial Leverage

Company has to rely both on equity and debt in order to successfully accomplish its operations.

Management accounting sees that company makes use of equity and debt in a balanced way

which helps in managing company’s net working capital and at the same time not piling only

debts on the company. The leverage taken has to be put to optimal use to generate returns for the

company and also it can be paid back on time (Abdusalomova, 2019).

Accounts Receivables

Management accounting keeps a track of pending payments from debtors known as account

receivables in a time range order for e.g. 30 days or 30-60 days credit period etc. If a debtor is

seen extending the term many times or defaulting sometimes, company can take a decision to

review its credit policy and business policy with them. It helps in tracking payments to reach on

time and thus increase cash in hand to improve liquidity of the company.

Budget Analysis

Management accounting helps in forming of budget with financial planning for various

departments considering the previous year statements and current demand of a particular section.

A financial analysis of various departments help the accountants in allotment of finance to a

particular section. It also sees for the deviations in the actual performance from the standard

norms while preparing budget for a particular section. This can be done by variance analysis

along with other methods. This has also helped where excess costs are taking up place and apt

Management accounting helps in realising constraints in the line of production and sales. An

optimum utilisation of assets is good but sometimes it may happen that goods are manufactured

according to the set rhythm but sales is not up to the mark. This will result in piling up of

inventory and storage costs increase but no increase in revenues. Management accounting sees to

it which constraints can come in between company’s set goal and makes aware of measures to

remove constraints timely.

Financial Leverage

Company has to rely both on equity and debt in order to successfully accomplish its operations.

Management accounting sees that company makes use of equity and debt in a balanced way

which helps in managing company’s net working capital and at the same time not piling only

debts on the company. The leverage taken has to be put to optimal use to generate returns for the

company and also it can be paid back on time (Abdusalomova, 2019).

Accounts Receivables

Management accounting keeps a track of pending payments from debtors known as account

receivables in a time range order for e.g. 30 days or 30-60 days credit period etc. If a debtor is

seen extending the term many times or defaulting sometimes, company can take a decision to

review its credit policy and business policy with them. It helps in tracking payments to reach on

time and thus increase cash in hand to improve liquidity of the company.

Budget Analysis

Management accounting helps in forming of budget with financial planning for various

departments considering the previous year statements and current demand of a particular section.

A financial analysis of various departments help the accountants in allotment of finance to a

particular section. It also sees for the deviations in the actual performance from the standard

norms while preparing budget for a particular section. This can be done by variance analysis

along with other methods. This has also helped where excess costs are taking up place and apt

measures to be taken. Market trends are also taken in consideration of product demand while

forming the budget.

P2 Methods used for management accounting reporting

The methods for reporting of management accounting are as follows:

Budget Reports

It helps in distributing finance allocation while assessing the performance of a department in a

year or quarter as per the requirement. The budget estimates are according to the previous year

financials. Budgets are increased or decreased as per the need, performance and market trends

regarding a section. Employees can also be provided bonuses for doing well by managers by

budgeting funds. Further a company has to achieve its goals within the budget for the next

financial year (Rikhardsson and Yigitbasioglu, 2018).

Pro forma cash flow

This method states how much money or cash flow can be expected in short term and medium-

term accounting periods and how much spending can be done. It helps to know when surpluses

can be expected and when cash shortage can be expected. Accordingly, the management can be

prepared beforehand to deal with the situation.

Sales Reports

Sales reports show which segment of products is performing well and which are under

performing thus indicating the sources of revenue as well as where company is suffering losses.

Simultaneously it also helps management know which sales person are doing well and achieving

goals and who are lacking and need motivation (Burritt and et.al., 2019).

Item cost reports

It breaks down costs gone in products category wise and shows expenses incurred in categories

like labour, raw material, purchasing licenses for products etc. It is then subtracted from sales of

forming the budget.

P2 Methods used for management accounting reporting

The methods for reporting of management accounting are as follows:

Budget Reports

It helps in distributing finance allocation while assessing the performance of a department in a

year or quarter as per the requirement. The budget estimates are according to the previous year

financials. Budgets are increased or decreased as per the need, performance and market trends

regarding a section. Employees can also be provided bonuses for doing well by managers by

budgeting funds. Further a company has to achieve its goals within the budget for the next

financial year (Rikhardsson and Yigitbasioglu, 2018).

Pro forma cash flow

This method states how much money or cash flow can be expected in short term and medium-

term accounting periods and how much spending can be done. It helps to know when surpluses

can be expected and when cash shortage can be expected. Accordingly, the management can be

prepared beforehand to deal with the situation.

Sales Reports

Sales reports show which segment of products is performing well and which are under

performing thus indicating the sources of revenue as well as where company is suffering losses.

Simultaneously it also helps management know which sales person are doing well and achieving

goals and who are lacking and need motivation (Burritt and et.al., 2019).

Item cost reports

It breaks down costs gone in products category wise and shows expenses incurred in categories

like labour, raw material, purchasing licenses for products etc. It is then subtracted from sales of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that category and net profit is known for the particular segments. This report helps management

know in detail which category product is generating revenues for the company.

Job costing

This breaks a project in segments known as jobs. It can be seen from the revenues earned

whether a job is profitable or not. It indicates whether a project will generate returns and is worth

continuing or not.

Inventory Valuation

The report helps in calculating overheads per unit, labour cost, inventory storage cost, damaged

inventories cost and thus knowing the value of inventory. Managers are able to prepare budget

for inventory separately and also think of measures where cost control can be done and how

much inventory turnover should be to manage the inventory costs.

Order Information Report

It depicts all the costs associated with an order placed and shows management the ways to

achieve low cost on placing of orders and managing them (Rikhardsson and Yigitbasioglu,

2018).

Opportunity Reports

The reports show the area of opportunities to the managers to convert it into business for the

company and achieve profits.

Performance Reports

These reports are generally made at the year’s end which evaluates company’s performance to its

business goals. It also makes report of every department within the organisation as to how it has

set the parameters in its functions and compare with the previous year performance. Performance

of employees is also measured through set parameters or in general. The departments which have

know in detail which category product is generating revenues for the company.

Job costing

This breaks a project in segments known as jobs. It can be seen from the revenues earned

whether a job is profitable or not. It indicates whether a project will generate returns and is worth

continuing or not.

Inventory Valuation

The report helps in calculating overheads per unit, labour cost, inventory storage cost, damaged

inventories cost and thus knowing the value of inventory. Managers are able to prepare budget

for inventory separately and also think of measures where cost control can be done and how

much inventory turnover should be to manage the inventory costs.

Order Information Report

It depicts all the costs associated with an order placed and shows management the ways to

achieve low cost on placing of orders and managing them (Rikhardsson and Yigitbasioglu,

2018).

Opportunity Reports

The reports show the area of opportunities to the managers to convert it into business for the

company and achieve profits.

Performance Reports

These reports are generally made at the year’s end which evaluates company’s performance to its

business goals. It also makes report of every department within the organisation as to how it has

set the parameters in its functions and compare with the previous year performance. Performance

of employees is also measured through set parameters or in general. The departments which have

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

done well are appreciated along with the employees being rewarded for their contribution. The

areas where business has not performed well are considered for taking measures to improve in

future.

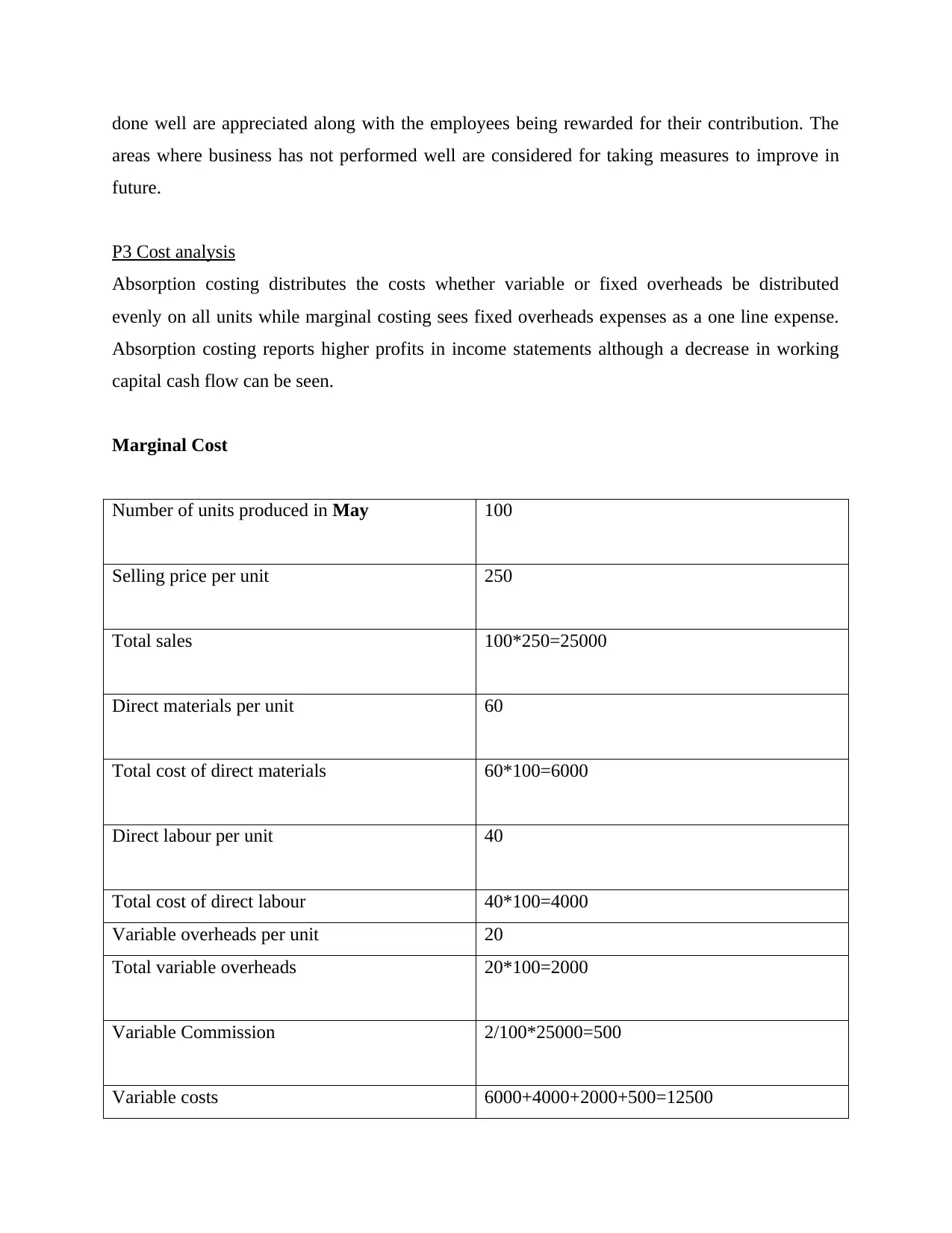

P3 Cost analysis

Absorption costing distributes the costs whether variable or fixed overheads be distributed

evenly on all units while marginal costing sees fixed overheads expenses as a one line expense.

Absorption costing reports higher profits in income statements although a decrease in working

capital cash flow can be seen.

Marginal Cost

Number of units produced in May 100

Selling price per unit 250

Total sales 100*250=25000

Direct materials per unit 60

Total cost of direct materials 60*100=6000

Direct labour per unit 40

Total cost of direct labour 40*100=4000

Variable overheads per unit 20

Total variable overheads 20*100=2000

Variable Commission 2/100*25000=500

Variable costs 6000+4000+2000+500=12500

areas where business has not performed well are considered for taking measures to improve in

future.

P3 Cost analysis

Absorption costing distributes the costs whether variable or fixed overheads be distributed

evenly on all units while marginal costing sees fixed overheads expenses as a one line expense.

Absorption costing reports higher profits in income statements although a decrease in working

capital cash flow can be seen.

Marginal Cost

Number of units produced in May 100

Selling price per unit 250

Total sales 100*250=25000

Direct materials per unit 60

Total cost of direct materials 60*100=6000

Direct labour per unit 40

Total cost of direct labour 40*100=4000

Variable overheads per unit 20

Total variable overheads 20*100=2000

Variable Commission 2/100*25000=500

Variable costs 6000+4000+2000+500=12500

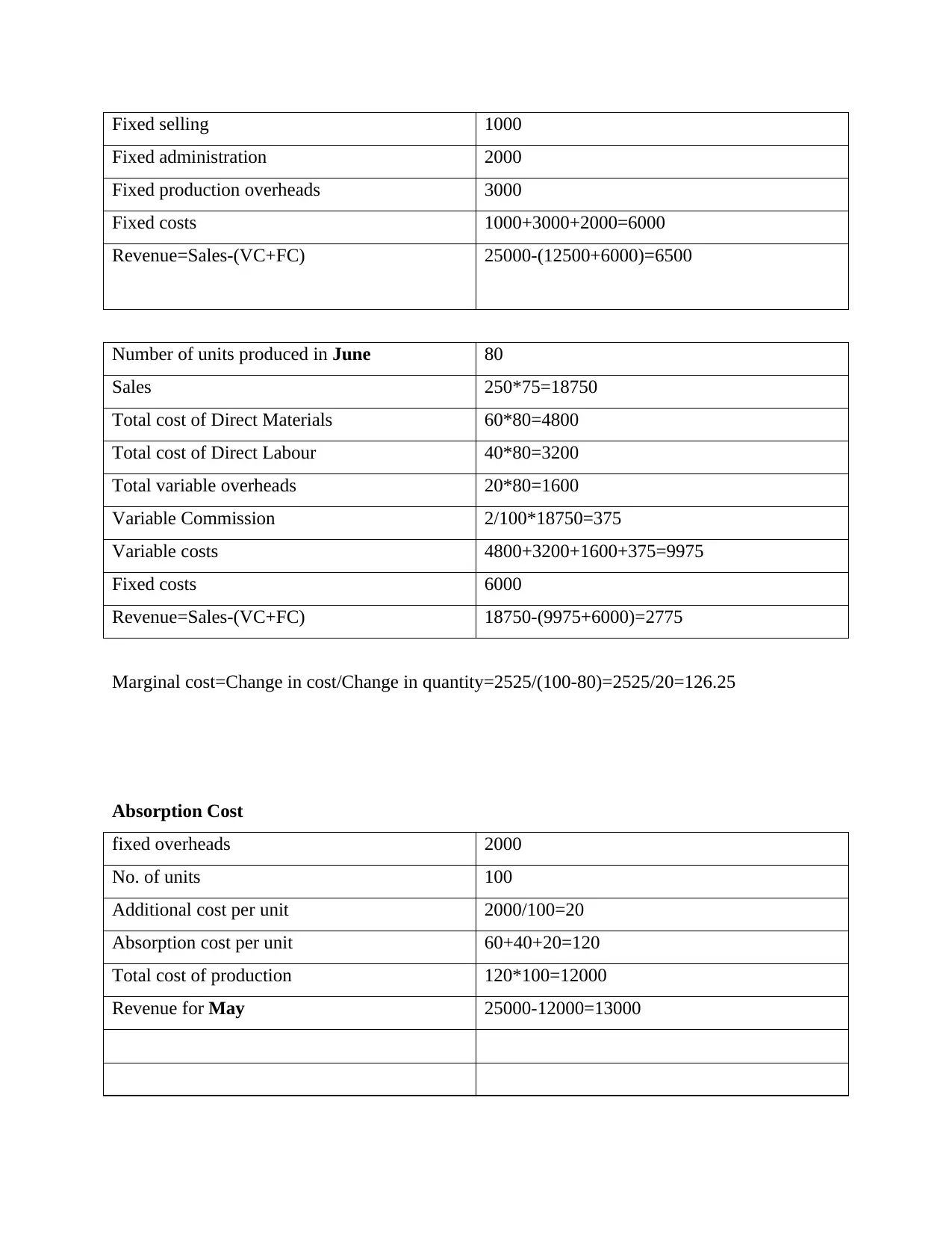

Fixed selling 1000

Fixed administration 2000

Fixed production overheads 3000

Fixed costs 1000+3000+2000=6000

Revenue=Sales-(VC+FC) 25000-(12500+6000)=6500

Number of units produced in June 80

Sales 250*75=18750

Total cost of Direct Materials 60*80=4800

Total cost of Direct Labour 40*80=3200

Total variable overheads 20*80=1600

Variable Commission 2/100*18750=375

Variable costs 4800+3200+1600+375=9975

Fixed costs 6000

Revenue=Sales-(VC+FC) 18750-(9975+6000)=2775

Marginal cost=Change in cost/Change in quantity=2525/(100-80)=2525/20=126.25

Absorption Cost

fixed overheads 2000

No. of units 100

Additional cost per unit 2000/100=20

Absorption cost per unit 60+40+20=120

Total cost of production 120*100=12000

Revenue for May 25000-12000=13000

Fixed administration 2000

Fixed production overheads 3000

Fixed costs 1000+3000+2000=6000

Revenue=Sales-(VC+FC) 25000-(12500+6000)=6500

Number of units produced in June 80

Sales 250*75=18750

Total cost of Direct Materials 60*80=4800

Total cost of Direct Labour 40*80=3200

Total variable overheads 20*80=1600

Variable Commission 2/100*18750=375

Variable costs 4800+3200+1600+375=9975

Fixed costs 6000

Revenue=Sales-(VC+FC) 18750-(9975+6000)=2775

Marginal cost=Change in cost/Change in quantity=2525/(100-80)=2525/20=126.25

Absorption Cost

fixed overheads 2000

No. of units 100

Additional cost per unit 2000/100=20

Absorption cost per unit 60+40+20=120

Total cost of production 120*100=12000

Revenue for May 25000-12000=13000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

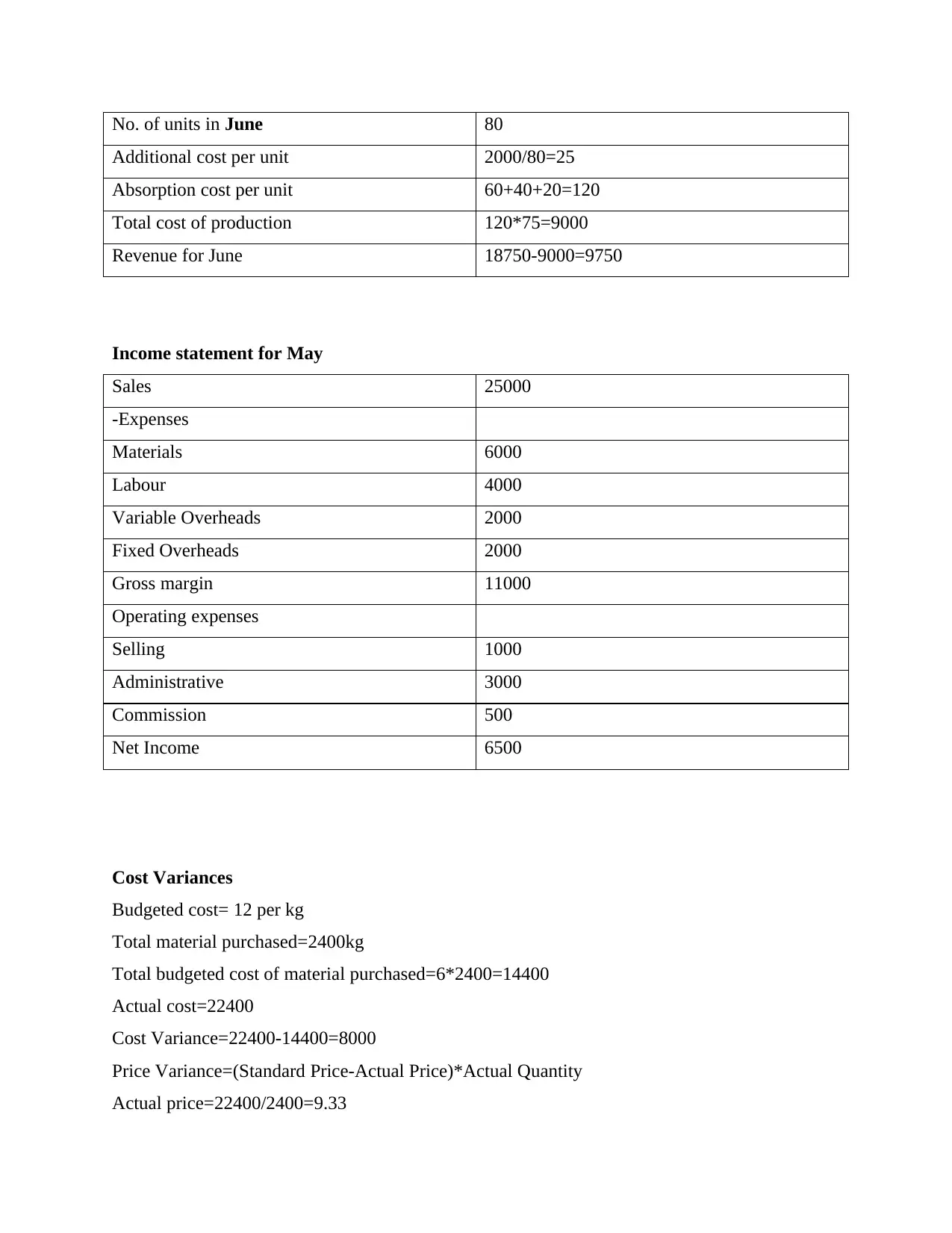

No. of units in June 80

Additional cost per unit 2000/80=25

Absorption cost per unit 60+40+20=120

Total cost of production 120*75=9000

Revenue for June 18750-9000=9750

Income statement for May

Sales 25000

-Expenses

Materials 6000

Labour 4000

Variable Overheads 2000

Fixed Overheads 2000

Gross margin 11000

Operating expenses

Selling 1000

Administrative 3000

Commission 500

Net Income 6500

Cost Variances

Budgeted cost= 12 per kg

Total material purchased=2400kg

Total budgeted cost of material purchased=6*2400=14400

Actual cost=22400

Cost Variance=22400-14400=8000

Price Variance=(Standard Price-Actual Price)*Actual Quantity

Actual price=22400/2400=9.33

Additional cost per unit 2000/80=25

Absorption cost per unit 60+40+20=120

Total cost of production 120*75=9000

Revenue for June 18750-9000=9750

Income statement for May

Sales 25000

-Expenses

Materials 6000

Labour 4000

Variable Overheads 2000

Fixed Overheads 2000

Gross margin 11000

Operating expenses

Selling 1000

Administrative 3000

Commission 500

Net Income 6500

Cost Variances

Budgeted cost= 12 per kg

Total material purchased=2400kg

Total budgeted cost of material purchased=6*2400=14400

Actual cost=22400

Cost Variance=22400-14400=8000

Price Variance=(Standard Price-Actual Price)*Actual Quantity

Actual price=22400/2400=9.33

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

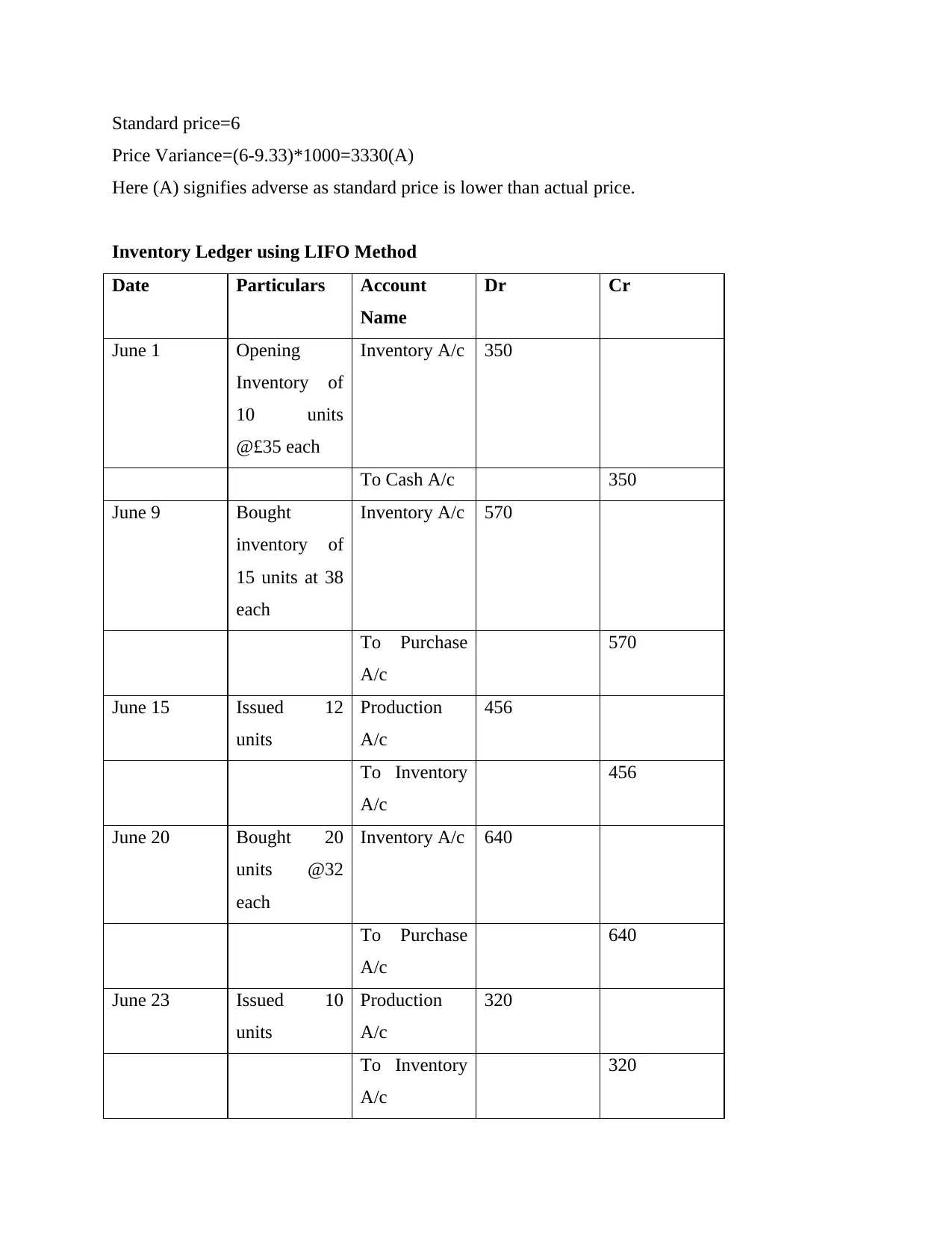

Standard price=6

Price Variance=(6-9.33)*1000=3330(A)

Here (A) signifies adverse as standard price is lower than actual price.

Inventory Ledger using LIFO Method

Date Particulars Account

Name

Dr Cr

June 1 Opening

Inventory of

10 units

@£35 each

Inventory A/c 350

To Cash A/c 350

June 9 Bought

inventory of

15 units at 38

each

Inventory A/c 570

To Purchase

A/c

570

June 15 Issued 12

units

Production

A/c

456

To Inventory

A/c

456

June 20 Bought 20

units @32

each

Inventory A/c 640

To Purchase

A/c

640

June 23 Issued 10

units

Production

A/c

320

To Inventory

A/c

320

Price Variance=(6-9.33)*1000=3330(A)

Here (A) signifies adverse as standard price is lower than actual price.

Inventory Ledger using LIFO Method

Date Particulars Account

Name

Dr Cr

June 1 Opening

Inventory of

10 units

@£35 each

Inventory A/c 350

To Cash A/c 350

June 9 Bought

inventory of

15 units at 38

each

Inventory A/c 570

To Purchase

A/c

570

June 15 Issued 12

units

Production

A/c

456

To Inventory

A/c

456

June 20 Bought 20

units @32

each

Inventory A/c 640

To Purchase

A/c

640

June 23 Issued 10

units

Production

A/c

320

To Inventory

A/c

320

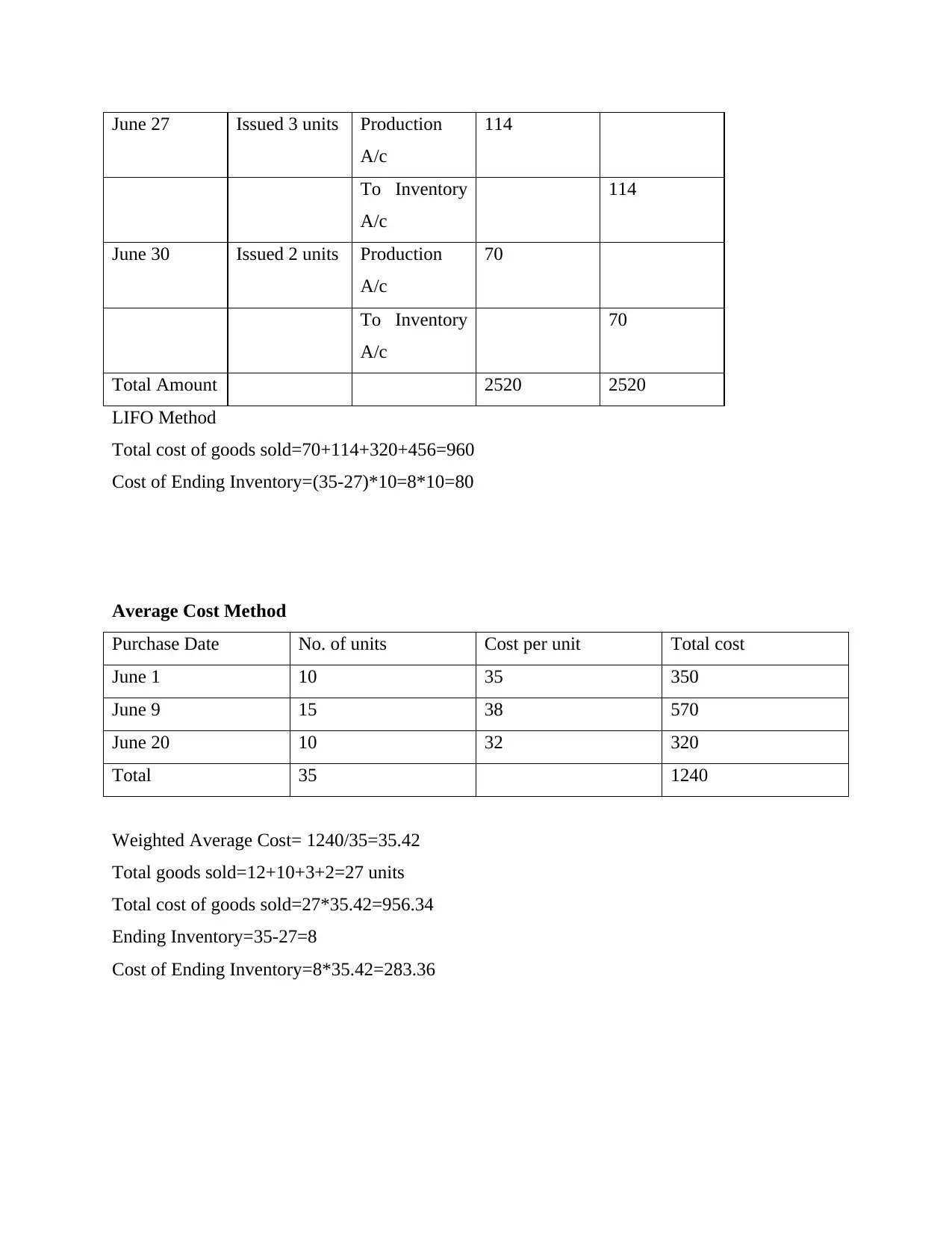

June 27 Issued 3 units Production

A/c

114

To Inventory

A/c

114

June 30 Issued 2 units Production

A/c

70

To Inventory

A/c

70

Total Amount 2520 2520

LIFO Method

Total cost of goods sold=70+114+320+456=960

Cost of Ending Inventory=(35-27)*10=8*10=80

Average Cost Method

Purchase Date No. of units Cost per unit Total cost

June 1 10 35 350

June 9 15 38 570

June 20 10 32 320

Total 35 1240

Weighted Average Cost= 1240/35=35.42

Total goods sold=12+10+3+2=27 units

Total cost of goods sold=27*35.42=956.34

Ending Inventory=35-27=8

Cost of Ending Inventory=8*35.42=283.36

A/c

114

To Inventory

A/c

114

June 30 Issued 2 units Production

A/c

70

To Inventory

A/c

70

Total Amount 2520 2520

LIFO Method

Total cost of goods sold=70+114+320+456=960

Cost of Ending Inventory=(35-27)*10=8*10=80

Average Cost Method

Purchase Date No. of units Cost per unit Total cost

June 1 10 35 350

June 9 15 38 570

June 20 10 32 320

Total 35 1240

Weighted Average Cost= 1240/35=35.42

Total goods sold=12+10+3+2=27 units

Total cost of goods sold=27*35.42=956.34

Ending Inventory=35-27=8

Cost of Ending Inventory=8*35.42=283.36

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.