Cost Analysis and Management Report

VerifiedAdded on 2020/02/19

|10

|2104

|135

Report

AI Summary

This report presents a comprehensive analysis of various costing methods, including process costing, activity-based costing, and their implications for financial management. It covers physical flow analysis, equivalent units calculation, cost reconciliation, and the impact of sustainability on financial decisions. The report also discusses the differences between absorption and variable costing, providing detailed income statements and recommendations for improved cost management strategies.

Question 1 Process costing system

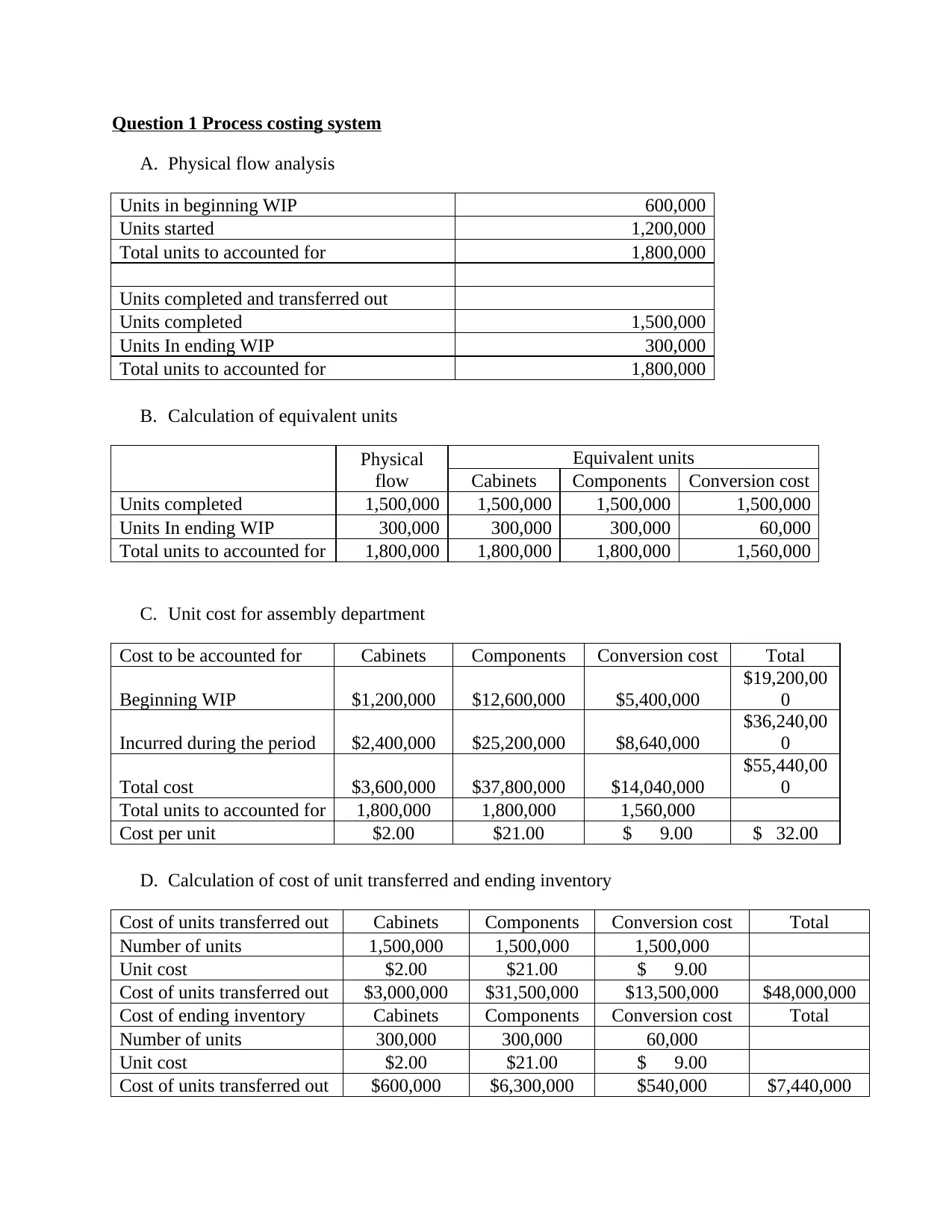

A. Physical flow analysis

Units in beginning WIP 600,000

Units started 1,200,000

Total units to accounted for 1,800,000

Units completed and transferred out

Units completed 1,500,000

Units In ending WIP 300,000

Total units to accounted for 1,800,000

B. Calculation of equivalent units

Physical

flow

Equivalent units

Cabinets Components Conversion cost

Units completed 1,500,000 1,500,000 1,500,000 1,500,000

Units In ending WIP 300,000 300,000 300,000 60,000

Total units to accounted for 1,800,000 1,800,000 1,800,000 1,560,000

C. Unit cost for assembly department

Cost to be accounted for Cabinets Components Conversion cost Total

Beginning WIP $1,200,000 $12,600,000 $5,400,000

$19,200,00

0

Incurred during the period $2,400,000 $25,200,000 $8,640,000

$36,240,00

0

Total cost $3,600,000 $37,800,000 $14,040,000

$55,440,00

0

Total units to accounted for 1,800,000 1,800,000 1,560,000

Cost per unit $2.00 $21.00 $ 9.00 $ 32.00

D. Calculation of cost of unit transferred and ending inventory

Cost of units transferred out Cabinets Components Conversion cost Total

Number of units 1,500,000 1,500,000 1,500,000

Unit cost $2.00 $21.00 $ 9.00

Cost of units transferred out $3,000,000 $31,500,000 $13,500,000 $48,000,000

Cost of ending inventory Cabinets Components Conversion cost Total

Number of units 300,000 300,000 60,000

Unit cost $2.00 $21.00 $ 9.00

Cost of units transferred out $600,000 $6,300,000 $540,000 $7,440,000

A. Physical flow analysis

Units in beginning WIP 600,000

Units started 1,200,000

Total units to accounted for 1,800,000

Units completed and transferred out

Units completed 1,500,000

Units In ending WIP 300,000

Total units to accounted for 1,800,000

B. Calculation of equivalent units

Physical

flow

Equivalent units

Cabinets Components Conversion cost

Units completed 1,500,000 1,500,000 1,500,000 1,500,000

Units In ending WIP 300,000 300,000 300,000 60,000

Total units to accounted for 1,800,000 1,800,000 1,800,000 1,560,000

C. Unit cost for assembly department

Cost to be accounted for Cabinets Components Conversion cost Total

Beginning WIP $1,200,000 $12,600,000 $5,400,000

$19,200,00

0

Incurred during the period $2,400,000 $25,200,000 $8,640,000

$36,240,00

0

Total cost $3,600,000 $37,800,000 $14,040,000

$55,440,00

0

Total units to accounted for 1,800,000 1,800,000 1,560,000

Cost per unit $2.00 $21.00 $ 9.00 $ 32.00

D. Calculation of cost of unit transferred and ending inventory

Cost of units transferred out Cabinets Components Conversion cost Total

Number of units 1,500,000 1,500,000 1,500,000

Unit cost $2.00 $21.00 $ 9.00

Cost of units transferred out $3,000,000 $31,500,000 $13,500,000 $48,000,000

Cost of ending inventory Cabinets Components Conversion cost Total

Number of units 300,000 300,000 60,000

Unit cost $2.00 $21.00 $ 9.00

Cost of units transferred out $600,000 $6,300,000 $540,000 $7,440,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

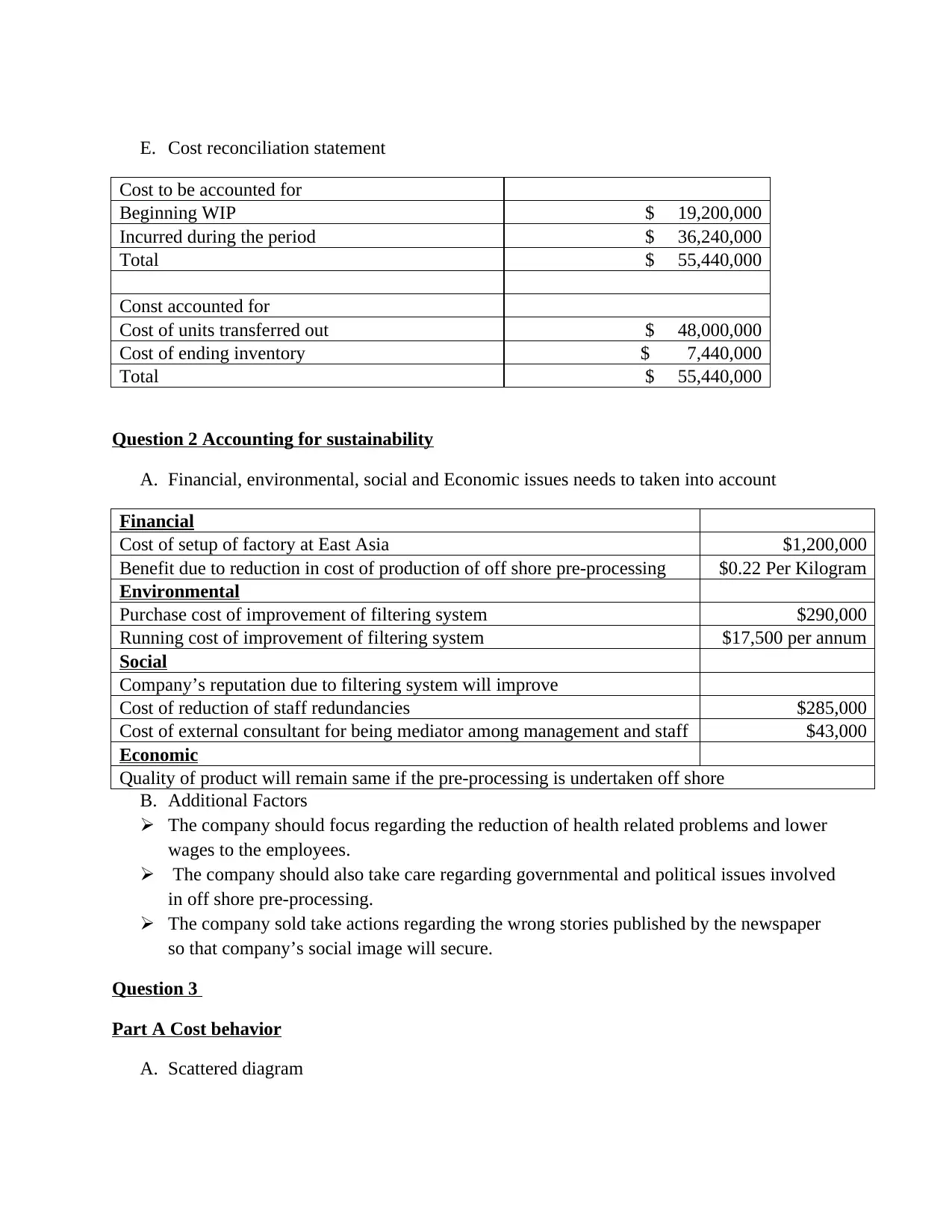

E. Cost reconciliation statement

Cost to be accounted for

Beginning WIP $ 19,200,000

Incurred during the period $ 36,240,000

Total $ 55,440,000

Const accounted for

Cost of units transferred out $ 48,000,000

Cost of ending inventory $ 7,440,000

Total $ 55,440,000

Question 2 Accounting for sustainability

A. Financial, environmental, social and Economic issues needs to taken into account

Financial

Cost of setup of factory at East Asia $1,200,000

Benefit due to reduction in cost of production of off shore pre-processing $0.22 Per Kilogram

Environmental

Purchase cost of improvement of filtering system $290,000

Running cost of improvement of filtering system $17,500 per annum

Social

Company’s reputation due to filtering system will improve

Cost of reduction of staff redundancies $285,000

Cost of external consultant for being mediator among management and staff $43,000

Economic

Quality of product will remain same if the pre-processing is undertaken off shore

B. Additional Factors

The company should focus regarding the reduction of health related problems and lower

wages to the employees.

The company should also take care regarding governmental and political issues involved

in off shore pre-processing.

The company sold take actions regarding the wrong stories published by the newspaper

so that company’s social image will secure.

Question 3

Part A Cost behavior

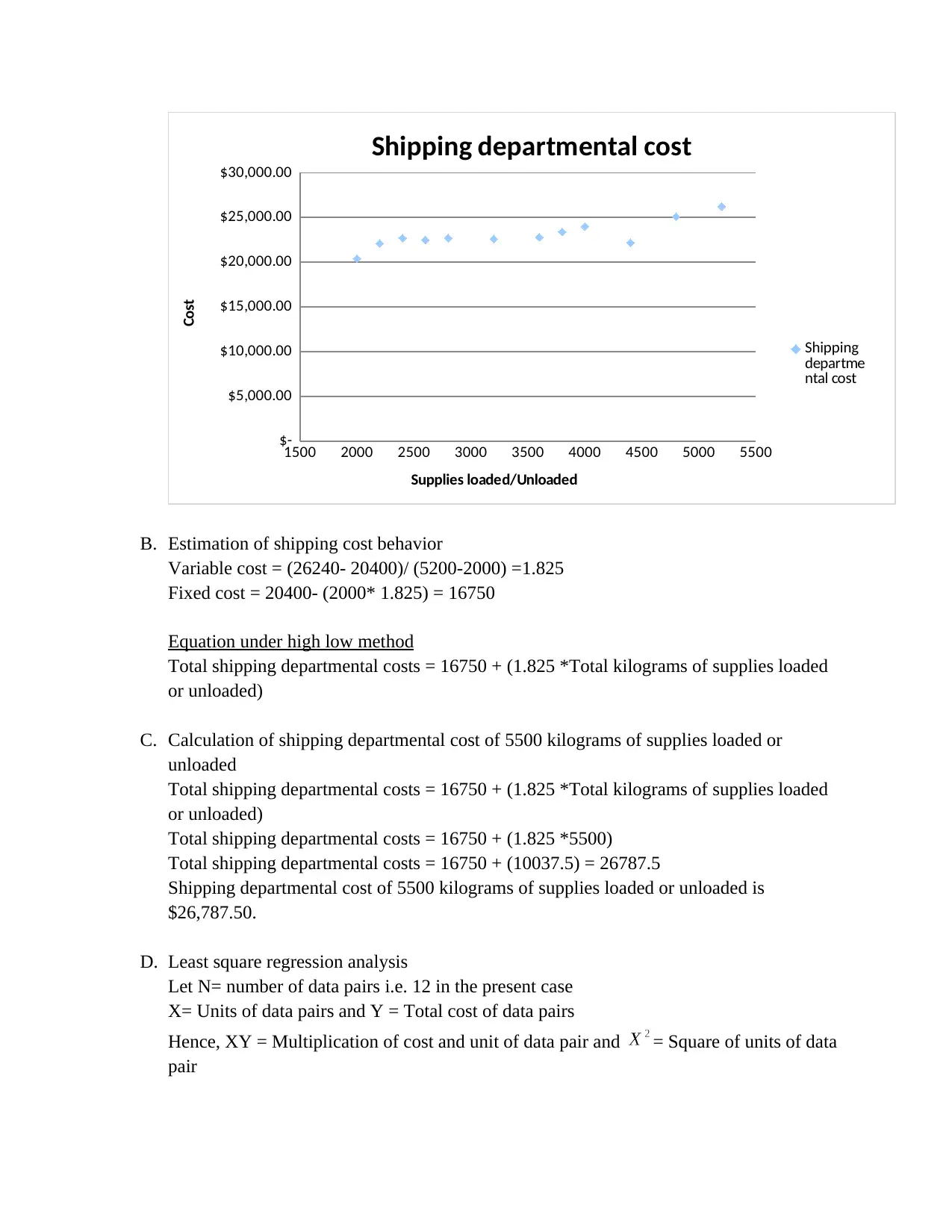

A. Scattered diagram

Cost to be accounted for

Beginning WIP $ 19,200,000

Incurred during the period $ 36,240,000

Total $ 55,440,000

Const accounted for

Cost of units transferred out $ 48,000,000

Cost of ending inventory $ 7,440,000

Total $ 55,440,000

Question 2 Accounting for sustainability

A. Financial, environmental, social and Economic issues needs to taken into account

Financial

Cost of setup of factory at East Asia $1,200,000

Benefit due to reduction in cost of production of off shore pre-processing $0.22 Per Kilogram

Environmental

Purchase cost of improvement of filtering system $290,000

Running cost of improvement of filtering system $17,500 per annum

Social

Company’s reputation due to filtering system will improve

Cost of reduction of staff redundancies $285,000

Cost of external consultant for being mediator among management and staff $43,000

Economic

Quality of product will remain same if the pre-processing is undertaken off shore

B. Additional Factors

The company should focus regarding the reduction of health related problems and lower

wages to the employees.

The company should also take care regarding governmental and political issues involved

in off shore pre-processing.

The company sold take actions regarding the wrong stories published by the newspaper

so that company’s social image will secure.

Question 3

Part A Cost behavior

A. Scattered diagram

1500 2000 2500 3000 3500 4000 4500 5000 5500

$-

$5,000.00

$10,000.00

$15,000.00

$20,000.00

$25,000.00

$30,000.00

Shipping departmental cost

Shipping

departme

ntal cost

Supplies loaded/Unloaded

Cost

B. Estimation of shipping cost behavior

Variable cost = (26240- 20400)/ (5200-2000) =1.825

Fixed cost = 20400- (2000* 1.825) = 16750

Equation under high low method

Total shipping departmental costs = 16750 + (1.825 *Total kilograms of supplies loaded

or unloaded)

C. Calculation of shipping departmental cost of 5500 kilograms of supplies loaded or

unloaded

Total shipping departmental costs = 16750 + (1.825 *Total kilograms of supplies loaded

or unloaded)

Total shipping departmental costs = 16750 + (1.825 *5500)

Total shipping departmental costs = 16750 + (10037.5) = 26787.5

Shipping departmental cost of 5500 kilograms of supplies loaded or unloaded is

$26,787.50.

D. Least square regression analysis

Let N= number of data pairs i.e. 12 in the present case

X= Units of data pairs and Y = Total cost of data pairs

Hence, XY = Multiplication of cost and unit of data pair and = Square of units of data

pair

$-

$5,000.00

$10,000.00

$15,000.00

$20,000.00

$25,000.00

$30,000.00

Shipping departmental cost

Shipping

departme

ntal cost

Supplies loaded/Unloaded

Cost

B. Estimation of shipping cost behavior

Variable cost = (26240- 20400)/ (5200-2000) =1.825

Fixed cost = 20400- (2000* 1.825) = 16750

Equation under high low method

Total shipping departmental costs = 16750 + (1.825 *Total kilograms of supplies loaded

or unloaded)

C. Calculation of shipping departmental cost of 5500 kilograms of supplies loaded or

unloaded

Total shipping departmental costs = 16750 + (1.825 *Total kilograms of supplies loaded

or unloaded)

Total shipping departmental costs = 16750 + (1.825 *5500)

Total shipping departmental costs = 16750 + (10037.5) = 26787.5

Shipping departmental cost of 5500 kilograms of supplies loaded or unloaded is

$26,787.50.

D. Least square regression analysis

Let N= number of data pairs i.e. 12 in the present case

X= Units of data pairs and Y = Total cost of data pairs

Hence, XY = Multiplication of cost and unit of data pair and = Square of units of data

pair

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

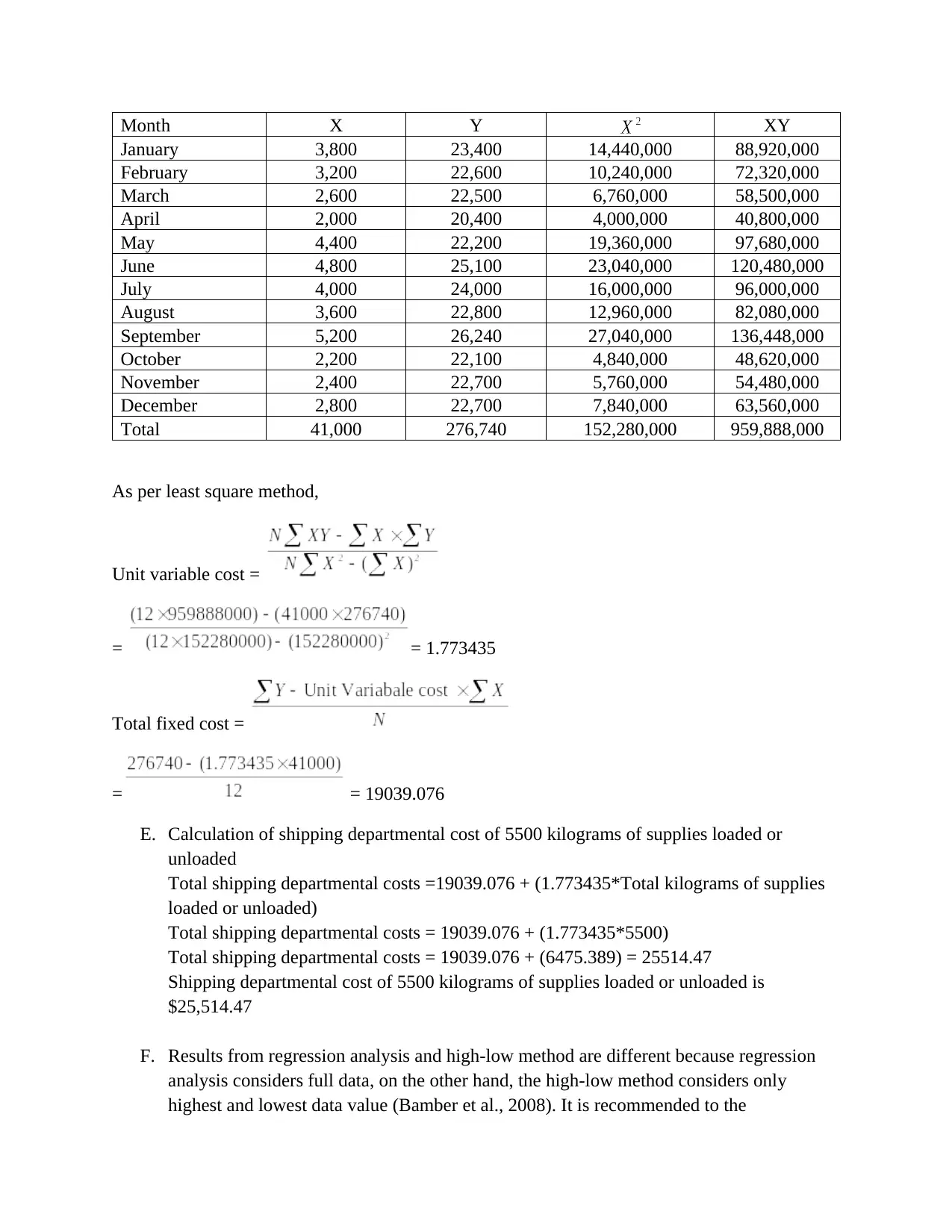

Month X Y XY

January 3,800 23,400 14,440,000 88,920,000

February 3,200 22,600 10,240,000 72,320,000

March 2,600 22,500 6,760,000 58,500,000

April 2,000 20,400 4,000,000 40,800,000

May 4,400 22,200 19,360,000 97,680,000

June 4,800 25,100 23,040,000 120,480,000

July 4,000 24,000 16,000,000 96,000,000

August 3,600 22,800 12,960,000 82,080,000

September 5,200 26,240 27,040,000 136,448,000

October 2,200 22,100 4,840,000 48,620,000

November 2,400 22,700 5,760,000 54,480,000

December 2,800 22,700 7,840,000 63,560,000

Total 41,000 276,740 152,280,000 959,888,000

As per least square method,

Unit variable cost =

= = 1.773435

Total fixed cost =

= = 19039.076

E. Calculation of shipping departmental cost of 5500 kilograms of supplies loaded or

unloaded

Total shipping departmental costs =19039.076 + (1.773435*Total kilograms of supplies

loaded or unloaded)

Total shipping departmental costs = 19039.076 + (1.773435*5500)

Total shipping departmental costs = 19039.076 + (6475.389) = 25514.47

Shipping departmental cost of 5500 kilograms of supplies loaded or unloaded is

$25,514.47

F. Results from regression analysis and high-low method are different because regression

analysis considers full data, on the other hand, the high-low method considers only

highest and lowest data value (Bamber et al., 2008). It is recommended to the

January 3,800 23,400 14,440,000 88,920,000

February 3,200 22,600 10,240,000 72,320,000

March 2,600 22,500 6,760,000 58,500,000

April 2,000 20,400 4,000,000 40,800,000

May 4,400 22,200 19,360,000 97,680,000

June 4,800 25,100 23,040,000 120,480,000

July 4,000 24,000 16,000,000 96,000,000

August 3,600 22,800 12,960,000 82,080,000

September 5,200 26,240 27,040,000 136,448,000

October 2,200 22,100 4,840,000 48,620,000

November 2,400 22,700 5,760,000 54,480,000

December 2,800 22,700 7,840,000 63,560,000

Total 41,000 276,740 152,280,000 959,888,000

As per least square method,

Unit variable cost =

= = 1.773435

Total fixed cost =

= = 19039.076

E. Calculation of shipping departmental cost of 5500 kilograms of supplies loaded or

unloaded

Total shipping departmental costs =19039.076 + (1.773435*Total kilograms of supplies

loaded or unloaded)

Total shipping departmental costs = 19039.076 + (1.773435*5500)

Total shipping departmental costs = 19039.076 + (6475.389) = 25514.47

Shipping departmental cost of 5500 kilograms of supplies loaded or unloaded is

$25,514.47

F. Results from regression analysis and high-low method are different because regression

analysis considers full data, on the other hand, the high-low method considers only

highest and lowest data value (Bamber et al., 2008). It is recommended to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

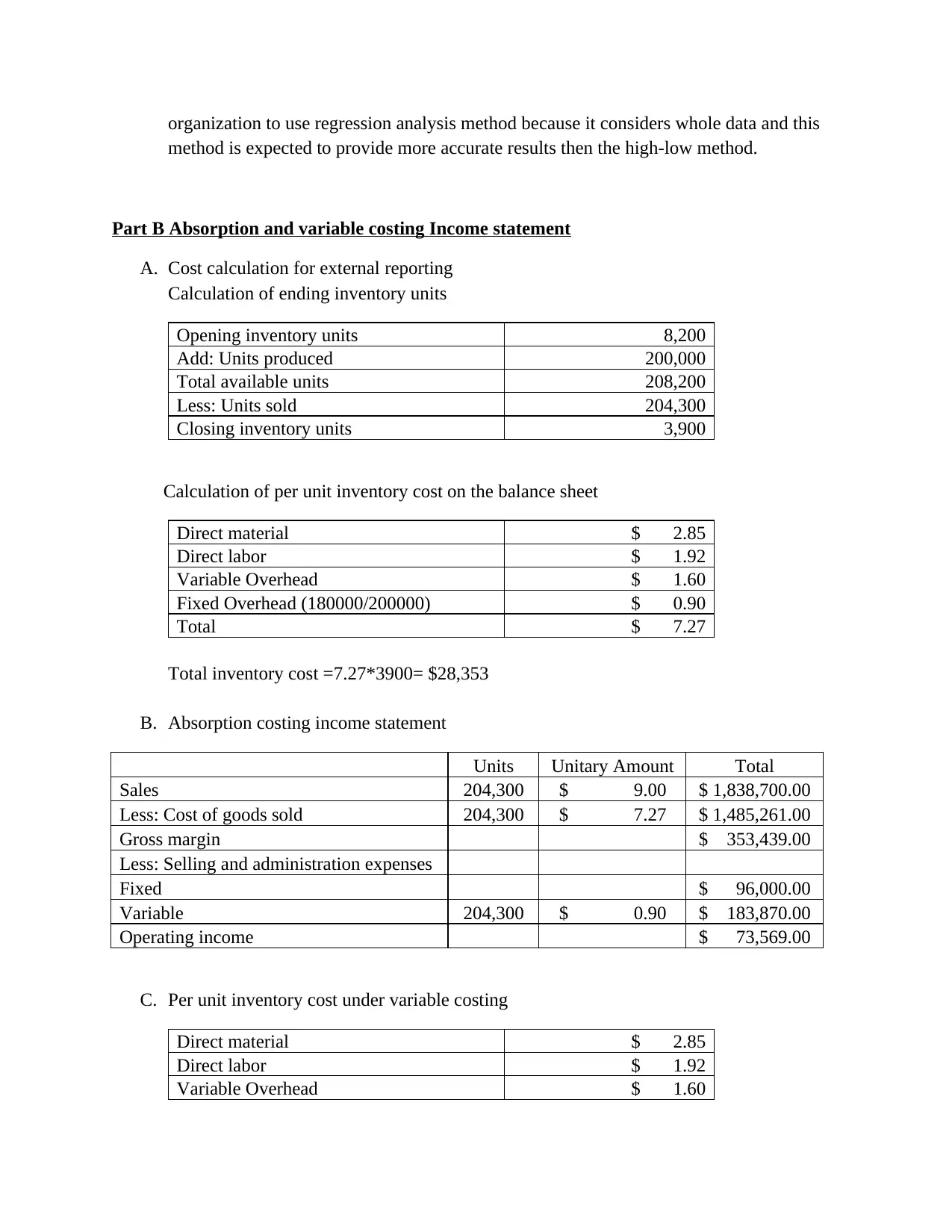

organization to use regression analysis method because it considers whole data and this

method is expected to provide more accurate results then the high-low method.

Part B Absorption and variable costing Income statement

A. Cost calculation for external reporting

Calculation of ending inventory units

Opening inventory units 8,200

Add: Units produced 200,000

Total available units 208,200

Less: Units sold 204,300

Closing inventory units 3,900

Calculation of per unit inventory cost on the balance sheet

Direct material $ 2.85

Direct labor $ 1.92

Variable Overhead $ 1.60

Fixed Overhead (180000/200000) $ 0.90

Total $ 7.27

Total inventory cost =7.27*3900= $28,353

B. Absorption costing income statement

Units Unitary Amount Total

Sales 204,300 $ 9.00 $ 1,838,700.00

Less: Cost of goods sold 204,300 $ 7.27 $ 1,485,261.00

Gross margin $ 353,439.00

Less: Selling and administration expenses

Fixed $ 96,000.00

Variable 204,300 $ 0.90 $ 183,870.00

Operating income $ 73,569.00

C. Per unit inventory cost under variable costing

Direct material $ 2.85

Direct labor $ 1.92

Variable Overhead $ 1.60

method is expected to provide more accurate results then the high-low method.

Part B Absorption and variable costing Income statement

A. Cost calculation for external reporting

Calculation of ending inventory units

Opening inventory units 8,200

Add: Units produced 200,000

Total available units 208,200

Less: Units sold 204,300

Closing inventory units 3,900

Calculation of per unit inventory cost on the balance sheet

Direct material $ 2.85

Direct labor $ 1.92

Variable Overhead $ 1.60

Fixed Overhead (180000/200000) $ 0.90

Total $ 7.27

Total inventory cost =7.27*3900= $28,353

B. Absorption costing income statement

Units Unitary Amount Total

Sales 204,300 $ 9.00 $ 1,838,700.00

Less: Cost of goods sold 204,300 $ 7.27 $ 1,485,261.00

Gross margin $ 353,439.00

Less: Selling and administration expenses

Fixed $ 96,000.00

Variable 204,300 $ 0.90 $ 183,870.00

Operating income $ 73,569.00

C. Per unit inventory cost under variable costing

Direct material $ 2.85

Direct labor $ 1.92

Variable Overhead $ 1.60

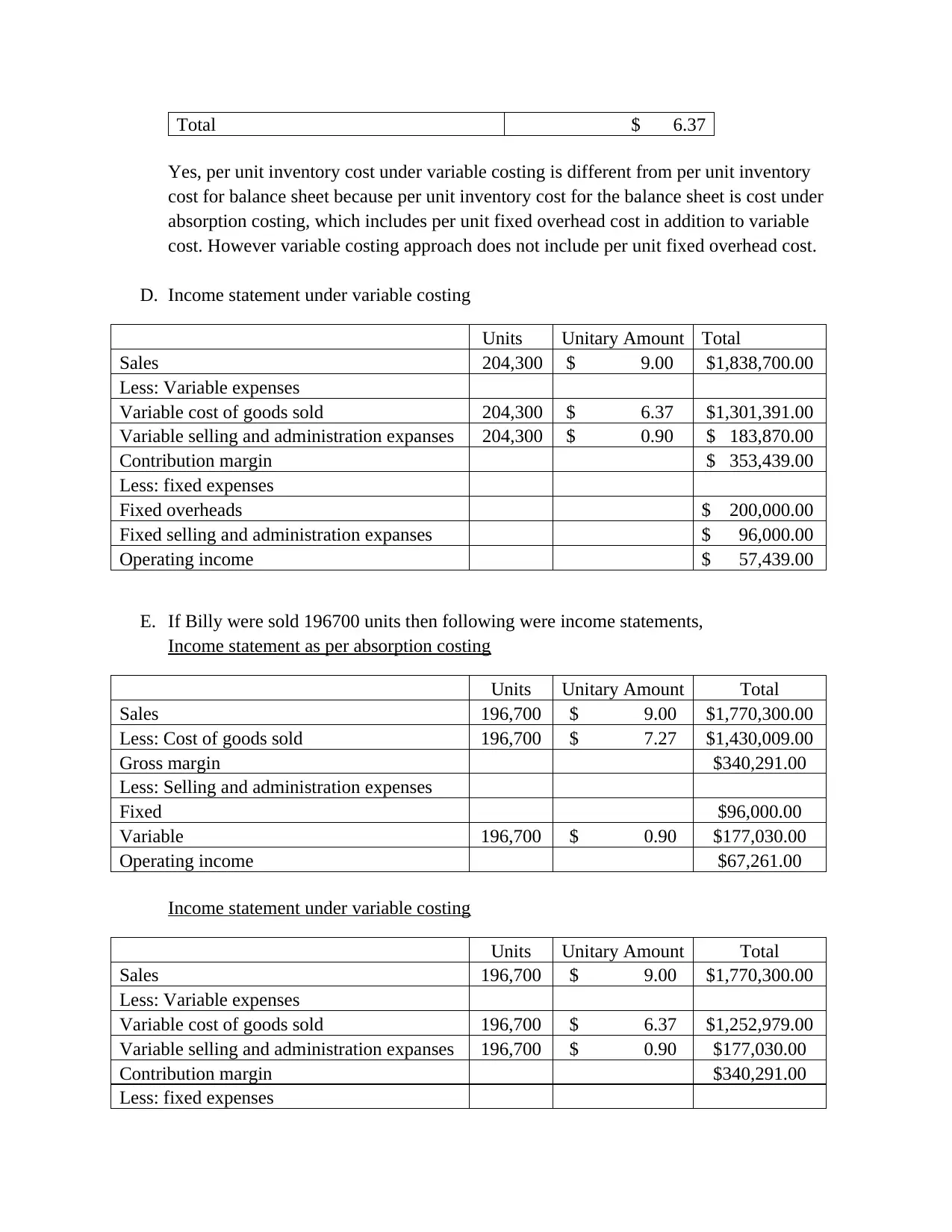

Total $ 6.37

Yes, per unit inventory cost under variable costing is different from per unit inventory

cost for balance sheet because per unit inventory cost for the balance sheet is cost under

absorption costing, which includes per unit fixed overhead cost in addition to variable

cost. However variable costing approach does not include per unit fixed overhead cost.

D. Income statement under variable costing

Units Unitary Amount Total

Sales 204,300 $ 9.00 $1,838,700.00

Less: Variable expenses

Variable cost of goods sold 204,300 $ 6.37 $1,301,391.00

Variable selling and administration expanses 204,300 $ 0.90 $ 183,870.00

Contribution margin $ 353,439.00

Less: fixed expenses

Fixed overheads $ 200,000.00

Fixed selling and administration expanses $ 96,000.00

Operating income $ 57,439.00

E. If Billy were sold 196700 units then following were income statements,

Income statement as per absorption costing

Units Unitary Amount Total

Sales 196,700 $ 9.00 $1,770,300.00

Less: Cost of goods sold 196,700 $ 7.27 $1,430,009.00

Gross margin $340,291.00

Less: Selling and administration expenses

Fixed $96,000.00

Variable 196,700 $ 0.90 $177,030.00

Operating income $67,261.00

Income statement under variable costing

Units Unitary Amount Total

Sales 196,700 $ 9.00 $1,770,300.00

Less: Variable expenses

Variable cost of goods sold 196,700 $ 6.37 $1,252,979.00

Variable selling and administration expanses 196,700 $ 0.90 $177,030.00

Contribution margin $340,291.00

Less: fixed expenses

Yes, per unit inventory cost under variable costing is different from per unit inventory

cost for balance sheet because per unit inventory cost for the balance sheet is cost under

absorption costing, which includes per unit fixed overhead cost in addition to variable

cost. However variable costing approach does not include per unit fixed overhead cost.

D. Income statement under variable costing

Units Unitary Amount Total

Sales 204,300 $ 9.00 $1,838,700.00

Less: Variable expenses

Variable cost of goods sold 204,300 $ 6.37 $1,301,391.00

Variable selling and administration expanses 204,300 $ 0.90 $ 183,870.00

Contribution margin $ 353,439.00

Less: fixed expenses

Fixed overheads $ 200,000.00

Fixed selling and administration expanses $ 96,000.00

Operating income $ 57,439.00

E. If Billy were sold 196700 units then following were income statements,

Income statement as per absorption costing

Units Unitary Amount Total

Sales 196,700 $ 9.00 $1,770,300.00

Less: Cost of goods sold 196,700 $ 7.27 $1,430,009.00

Gross margin $340,291.00

Less: Selling and administration expenses

Fixed $96,000.00

Variable 196,700 $ 0.90 $177,030.00

Operating income $67,261.00

Income statement under variable costing

Units Unitary Amount Total

Sales 196,700 $ 9.00 $1,770,300.00

Less: Variable expenses

Variable cost of goods sold 196,700 $ 6.37 $1,252,979.00

Variable selling and administration expanses 196,700 $ 0.90 $177,030.00

Contribution margin $340,291.00

Less: fixed expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed overheads $200,000.00

Fixed selling and administration expanses $96,000.00

Operating income $44,291.00

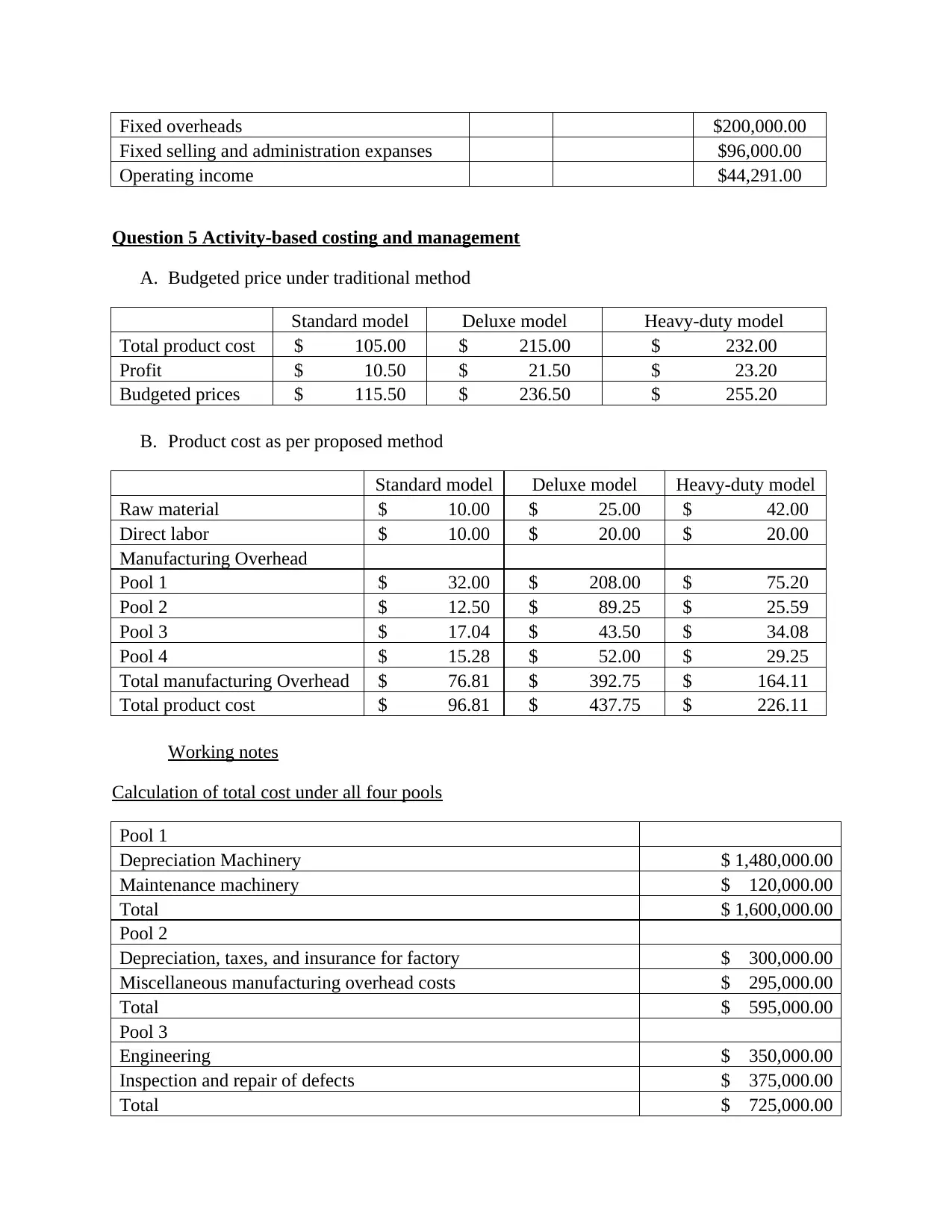

Question 5 Activity-based costing and management

A. Budgeted price under traditional method

Standard model Deluxe model Heavy-duty model

Total product cost $ 105.00 $ 215.00 $ 232.00

Profit $ 10.50 $ 21.50 $ 23.20

Budgeted prices $ 115.50 $ 236.50 $ 255.20

B. Product cost as per proposed method

Standard model Deluxe model Heavy-duty model

Raw material $ 10.00 $ 25.00 $ 42.00

Direct labor $ 10.00 $ 20.00 $ 20.00

Manufacturing Overhead

Pool 1 $ 32.00 $ 208.00 $ 75.20

Pool 2 $ 12.50 $ 89.25 $ 25.59

Pool 3 $ 17.04 $ 43.50 $ 34.08

Pool 4 $ 15.28 $ 52.00 $ 29.25

Total manufacturing Overhead $ 76.81 $ 392.75 $ 164.11

Total product cost $ 96.81 $ 437.75 $ 226.11

Working notes

Calculation of total cost under all four pools

Pool 1

Depreciation Machinery $ 1,480,000.00

Maintenance machinery $ 120,000.00

Total $ 1,600,000.00

Pool 2

Depreciation, taxes, and insurance for factory $ 300,000.00

Miscellaneous manufacturing overhead costs $ 295,000.00

Total $ 595,000.00

Pool 3

Engineering $ 350,000.00

Inspection and repair of defects $ 375,000.00

Total $ 725,000.00

Fixed selling and administration expanses $96,000.00

Operating income $44,291.00

Question 5 Activity-based costing and management

A. Budgeted price under traditional method

Standard model Deluxe model Heavy-duty model

Total product cost $ 105.00 $ 215.00 $ 232.00

Profit $ 10.50 $ 21.50 $ 23.20

Budgeted prices $ 115.50 $ 236.50 $ 255.20

B. Product cost as per proposed method

Standard model Deluxe model Heavy-duty model

Raw material $ 10.00 $ 25.00 $ 42.00

Direct labor $ 10.00 $ 20.00 $ 20.00

Manufacturing Overhead

Pool 1 $ 32.00 $ 208.00 $ 75.20

Pool 2 $ 12.50 $ 89.25 $ 25.59

Pool 3 $ 17.04 $ 43.50 $ 34.08

Pool 4 $ 15.28 $ 52.00 $ 29.25

Total manufacturing Overhead $ 76.81 $ 392.75 $ 164.11

Total product cost $ 96.81 $ 437.75 $ 226.11

Working notes

Calculation of total cost under all four pools

Pool 1

Depreciation Machinery $ 1,480,000.00

Maintenance machinery $ 120,000.00

Total $ 1,600,000.00

Pool 2

Depreciation, taxes, and insurance for factory $ 300,000.00

Miscellaneous manufacturing overhead costs $ 295,000.00

Total $ 595,000.00

Pool 3

Engineering $ 350,000.00

Inspection and repair of defects $ 375,000.00

Total $ 725,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

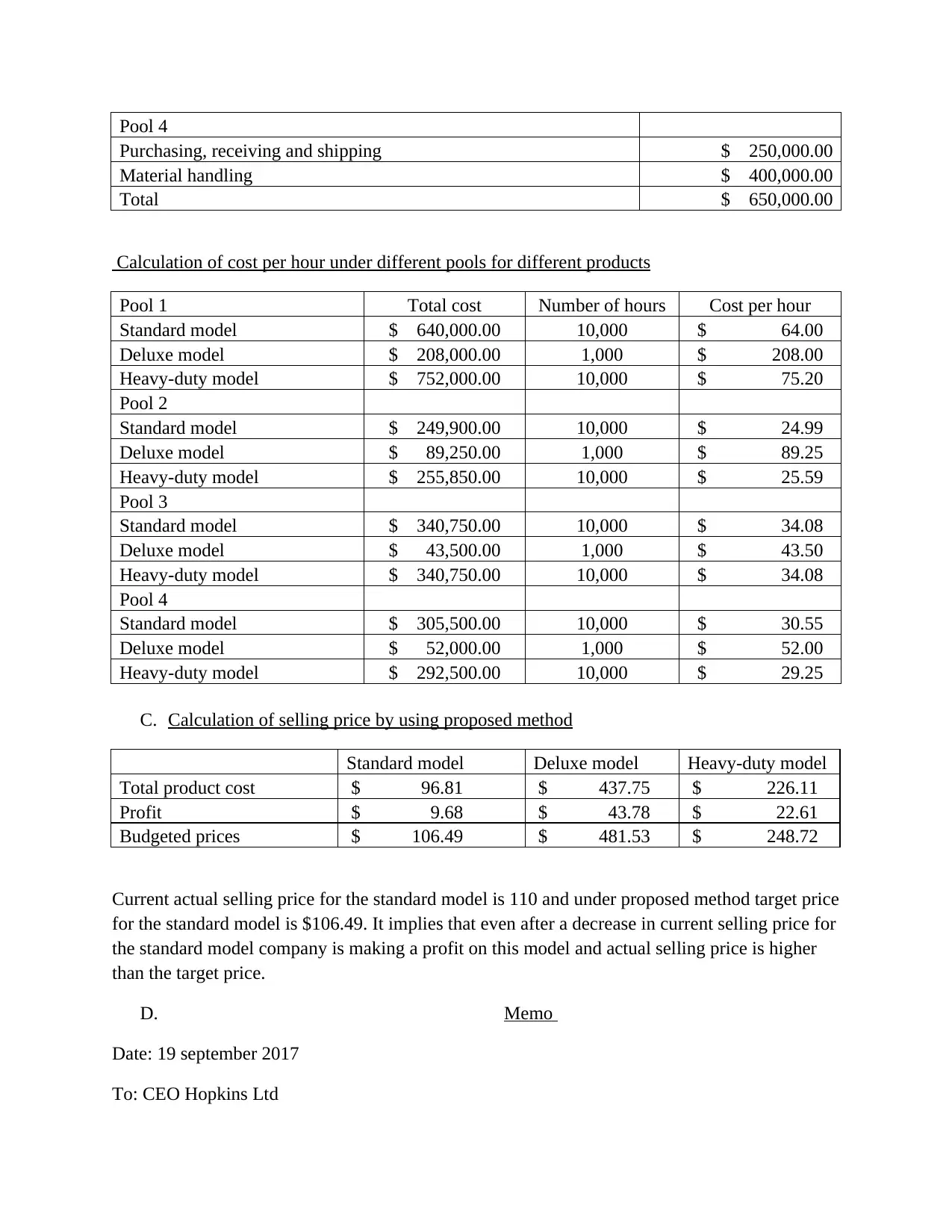

Pool 4

Purchasing, receiving and shipping $ 250,000.00

Material handling $ 400,000.00

Total $ 650,000.00

Calculation of cost per hour under different pools for different products

Pool 1 Total cost Number of hours Cost per hour

Standard model $ 640,000.00 10,000 $ 64.00

Deluxe model $ 208,000.00 1,000 $ 208.00

Heavy-duty model $ 752,000.00 10,000 $ 75.20

Pool 2

Standard model $ 249,900.00 10,000 $ 24.99

Deluxe model $ 89,250.00 1,000 $ 89.25

Heavy-duty model $ 255,850.00 10,000 $ 25.59

Pool 3

Standard model $ 340,750.00 10,000 $ 34.08

Deluxe model $ 43,500.00 1,000 $ 43.50

Heavy-duty model $ 340,750.00 10,000 $ 34.08

Pool 4

Standard model $ 305,500.00 10,000 $ 30.55

Deluxe model $ 52,000.00 1,000 $ 52.00

Heavy-duty model $ 292,500.00 10,000 $ 29.25

C. Calculation of selling price by using proposed method

Standard model Deluxe model Heavy-duty model

Total product cost $ 96.81 $ 437.75 $ 226.11

Profit $ 9.68 $ 43.78 $ 22.61

Budgeted prices $ 106.49 $ 481.53 $ 248.72

Current actual selling price for the standard model is 110 and under proposed method target price

for the standard model is $106.49. It implies that even after a decrease in current selling price for

the standard model company is making a profit on this model and actual selling price is higher

than the target price.

D. Memo

Date: 19 september 2017

To: CEO Hopkins Ltd

Purchasing, receiving and shipping $ 250,000.00

Material handling $ 400,000.00

Total $ 650,000.00

Calculation of cost per hour under different pools for different products

Pool 1 Total cost Number of hours Cost per hour

Standard model $ 640,000.00 10,000 $ 64.00

Deluxe model $ 208,000.00 1,000 $ 208.00

Heavy-duty model $ 752,000.00 10,000 $ 75.20

Pool 2

Standard model $ 249,900.00 10,000 $ 24.99

Deluxe model $ 89,250.00 1,000 $ 89.25

Heavy-duty model $ 255,850.00 10,000 $ 25.59

Pool 3

Standard model $ 340,750.00 10,000 $ 34.08

Deluxe model $ 43,500.00 1,000 $ 43.50

Heavy-duty model $ 340,750.00 10,000 $ 34.08

Pool 4

Standard model $ 305,500.00 10,000 $ 30.55

Deluxe model $ 52,000.00 1,000 $ 52.00

Heavy-duty model $ 292,500.00 10,000 $ 29.25

C. Calculation of selling price by using proposed method

Standard model Deluxe model Heavy-duty model

Total product cost $ 96.81 $ 437.75 $ 226.11

Profit $ 9.68 $ 43.78 $ 22.61

Budgeted prices $ 106.49 $ 481.53 $ 248.72

Current actual selling price for the standard model is 110 and under proposed method target price

for the standard model is $106.49. It implies that even after a decrease in current selling price for

the standard model company is making a profit on this model and actual selling price is higher

than the target price.

D. Memo

Date: 19 september 2017

To: CEO Hopkins Ltd

From: Student name

Subject: Regarding the costing of product

As per the data provided by the traditional system of overhead cost allocation, standard model

was not a highly profitable model because the total cost of the product was $105 and total sale

price of the model was $110. The product costing system applied by the organization is

inaccurate and out dated due to which cost was distorted for the product line. Competitors were

selling the same model was for $106, it implies that actual product cost must be lower than the

$106. It also implies that actual product cost is must be lower than the previously calculated cost

of the product i.e. $105.

However, the implication of activity based costing system to calculate product cost reversed the

results because it results that actually total cost of the standard model is $96.81 and target selling

price of the product of $106.49. This price is consistent with the selling price of competitors.

Furthermore, in case of the deluxe model, new pricing system revels that target selling price of

the product from this model is $481.53 and previously under the traditional system, it was

$236.50.

E. Strategic option

The company should apply and use new proposed system i.e. activity based costing system.

Under this system targeted price for standard model will reduce to $106 per unit. This will

enable the company to competite with its competitor and increase its demand.

Furthermore, in case of the deluxe model, new pricing system revels that target selling price of

the product from this model is $481.53 and previously under the traditional system, it was

$236.50. Hence company should move towards to enhance price for this product line and if it is

not possible to sale this product near revised targeted price i.e. $481.53, then the company should

discontinue this model.

The company should make a small reduction in the price of Heavy-duty model i.e. from $255.20

to $248.73. However, this product is not highly responsible for price distortion.

F. Statement showing total cost distortion for entire product line

Standard model Deluxe model Heavy-duty model

Product cost under traditional Method $105.00 $215.00 $232.00

Product cost under proposed model $96.81 $437.75 $226.11

cost distortion per unit $8.19 $ (222.75) $5.89

Product volume 20000 1000 10000

Cost distortion for entire product line $163,850.00 $ (222,750.00) $58,900.00

Subject: Regarding the costing of product

As per the data provided by the traditional system of overhead cost allocation, standard model

was not a highly profitable model because the total cost of the product was $105 and total sale

price of the model was $110. The product costing system applied by the organization is

inaccurate and out dated due to which cost was distorted for the product line. Competitors were

selling the same model was for $106, it implies that actual product cost must be lower than the

$106. It also implies that actual product cost is must be lower than the previously calculated cost

of the product i.e. $105.

However, the implication of activity based costing system to calculate product cost reversed the

results because it results that actually total cost of the standard model is $96.81 and target selling

price of the product of $106.49. This price is consistent with the selling price of competitors.

Furthermore, in case of the deluxe model, new pricing system revels that target selling price of

the product from this model is $481.53 and previously under the traditional system, it was

$236.50.

E. Strategic option

The company should apply and use new proposed system i.e. activity based costing system.

Under this system targeted price for standard model will reduce to $106 per unit. This will

enable the company to competite with its competitor and increase its demand.

Furthermore, in case of the deluxe model, new pricing system revels that target selling price of

the product from this model is $481.53 and previously under the traditional system, it was

$236.50. Hence company should move towards to enhance price for this product line and if it is

not possible to sale this product near revised targeted price i.e. $481.53, then the company should

discontinue this model.

The company should make a small reduction in the price of Heavy-duty model i.e. from $255.20

to $248.73. However, this product is not highly responsible for price distortion.

F. Statement showing total cost distortion for entire product line

Standard model Deluxe model Heavy-duty model

Product cost under traditional Method $105.00 $215.00 $232.00

Product cost under proposed model $96.81 $437.75 $226.11

cost distortion per unit $8.19 $ (222.75) $5.89

Product volume 20000 1000 10000

Cost distortion for entire product line $163,850.00 $ (222,750.00) $58,900.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total cost distortion for entire product line $163,850.00+ $ (222,750.00)+ $58,900.00= 0

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.