Management Accounting Report: Cost Analysis & Profit Implementation

VerifiedAdded on 2023/06/08

|15

|2435

|147

Report

AI Summary

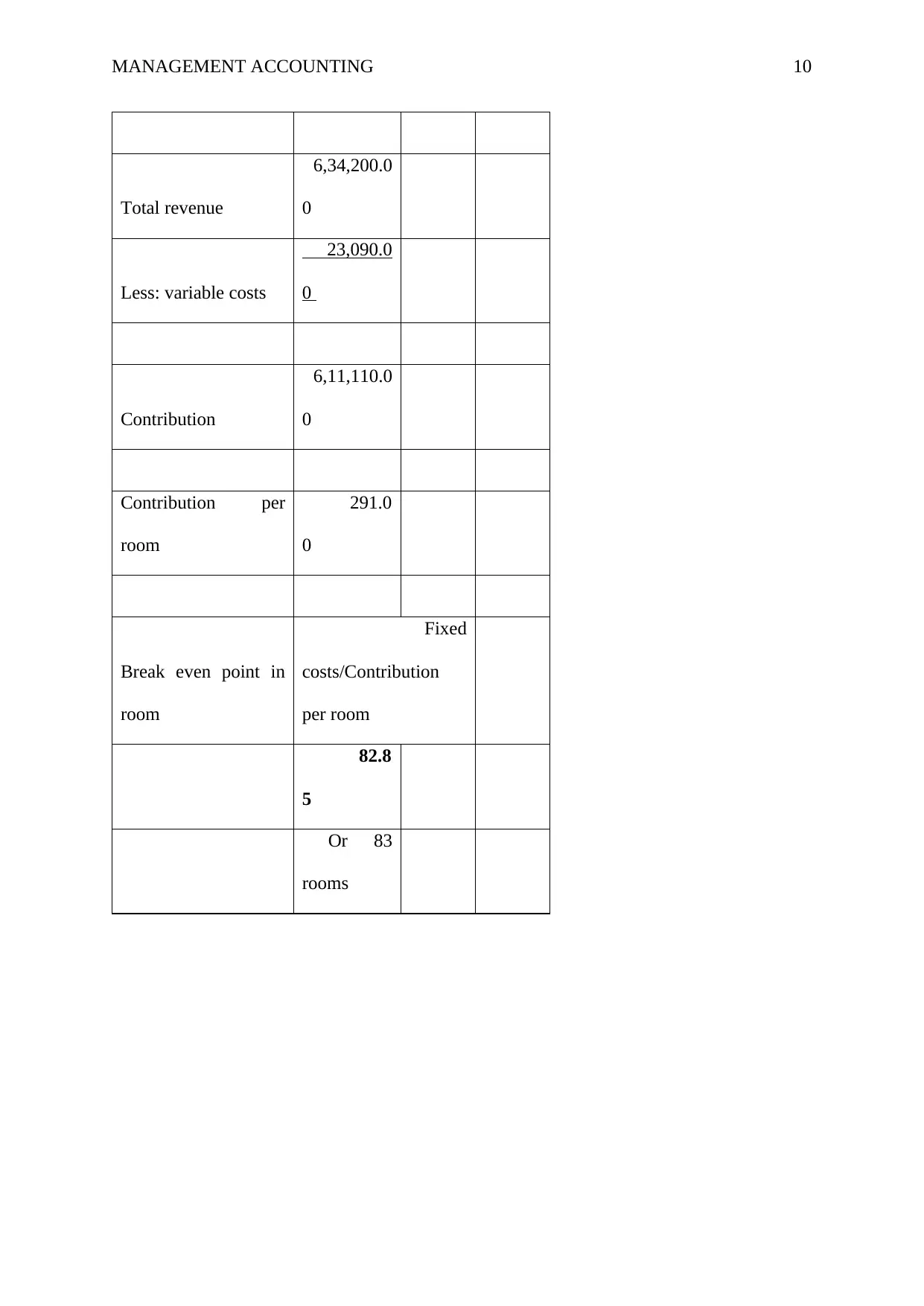

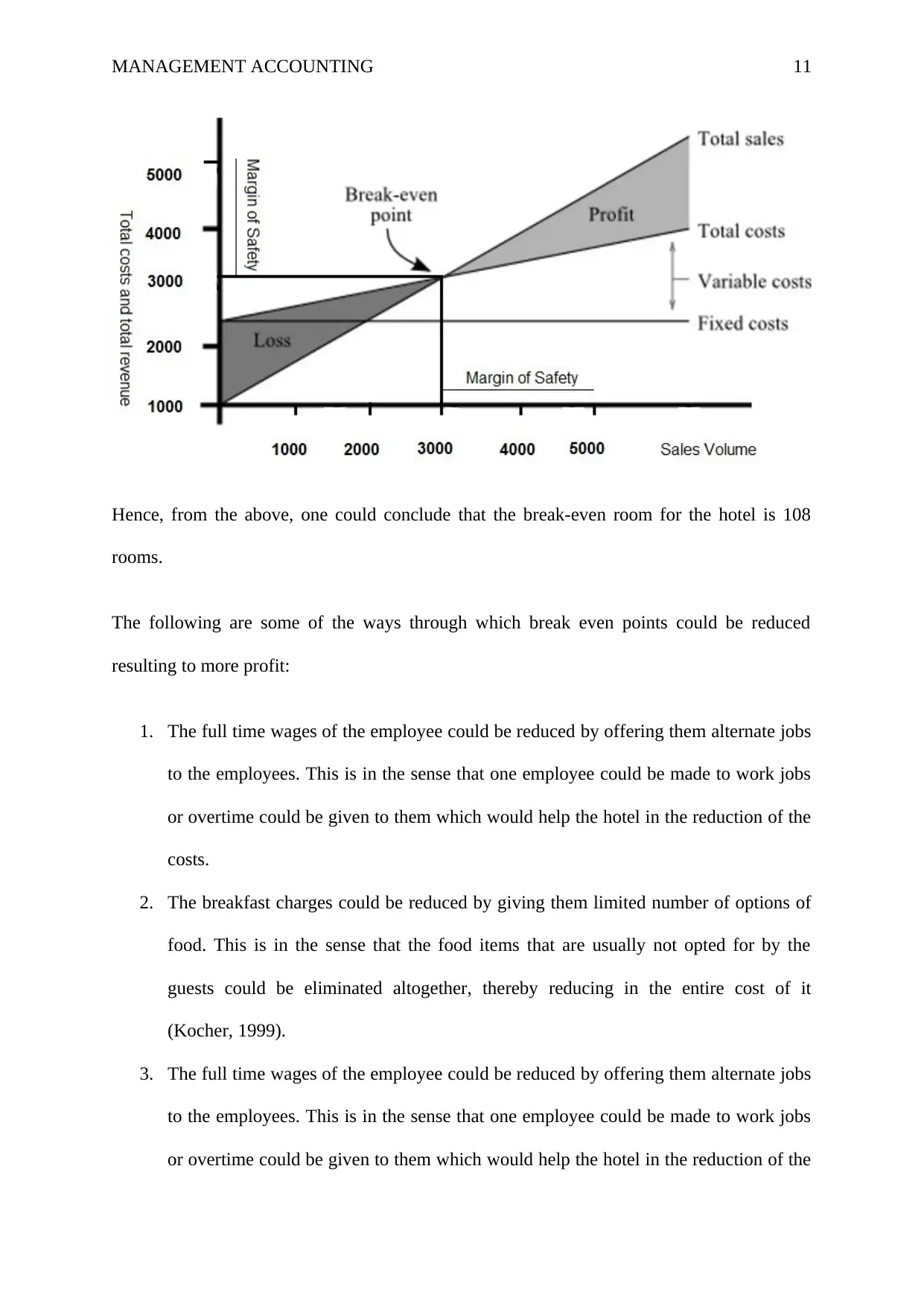

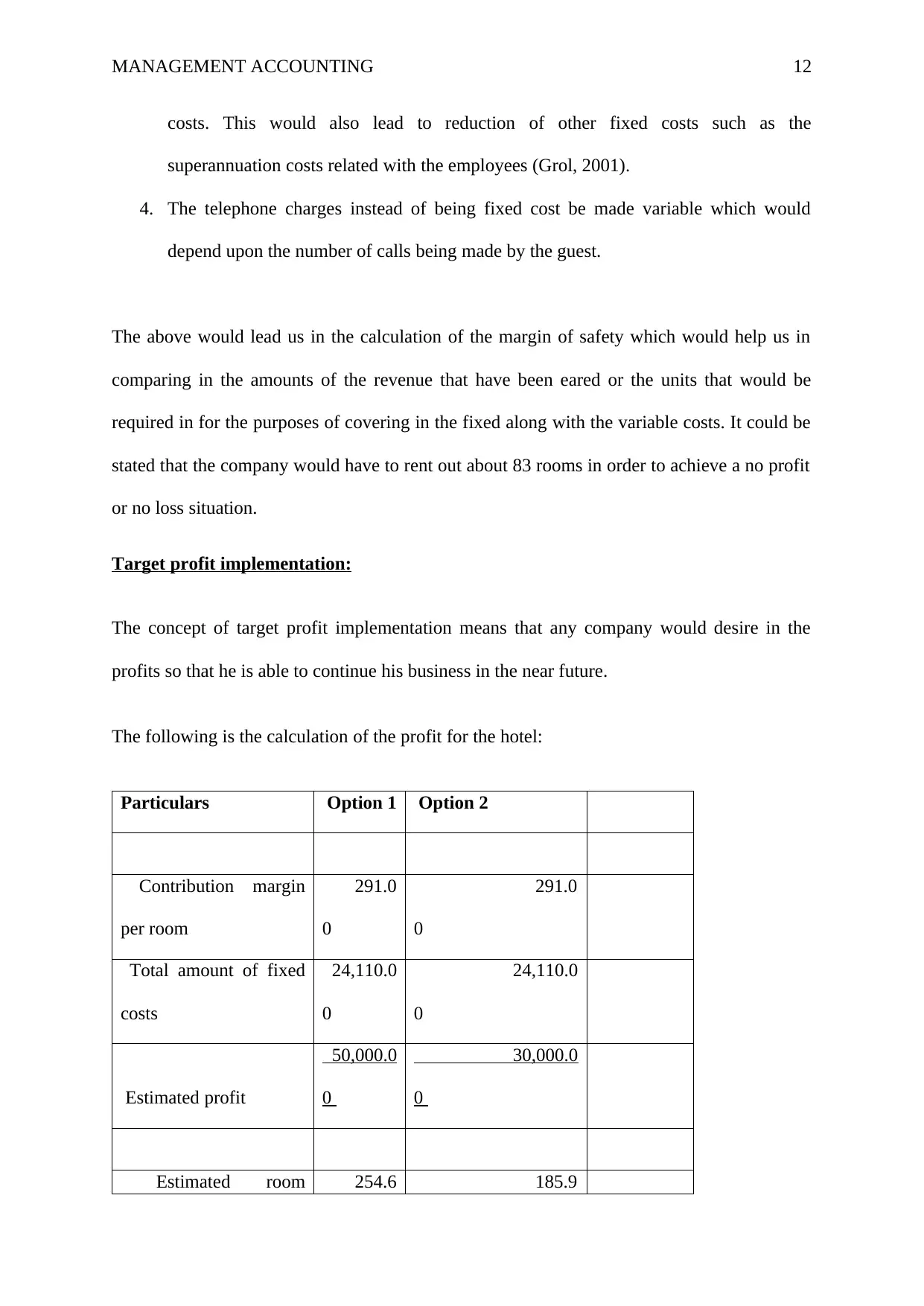

This management accounting report provides a detailed analysis of cost drivers and cost behavior, distinguishing between fixed and variable costs. It includes an identification of cost drivers within a hospitality context, specifically examining internet charges, complimentary breakfasts, electricity, insurance, marketing, super-annuation, telephone expenses, and waste removal. The report features a break-even analysis, calculating the break-even point for a hotel and suggesting strategies to reduce it, such as optimizing employee wages, limiting breakfast options, and converting fixed telephone charges to variable. Furthermore, it discusses target profit implementation, comparing different options for achieving a desired profit level through room bookings, and concludes that choosing options with lesser number of rooms being occupied will lead to more generation of revenue for the hotel. Desklib offers a wealth of resources for students, including solved assignments and past papers.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.