Management Accounting: Cost Analysis, Reporting, and Adaptation

VerifiedAdded on 2024/05/29

|17

|4224

|273

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its essential requirements, reporting methods, and adaptation to financial challenges. It explains management accounting's role in organizational success, highlighting its principles of value creation, stakeholder trust, and performance encouragement. The report details various management accounting systems, including cost accounting, inventory management, job-costing, and price optimization. It further explores different reporting methods such as budgets, departmental reports (sales, production, inventory), and capital budgeting reports, emphasizing the importance of clear and understandable information presentation. Practical application of absorption and marginal costing is demonstrated through income statement preparation. Finally, the report examines how organizations adapt management accounting systems to address financial problems and the advantages and disadvantages of planning tools used in budgetary control. Desklib provides access to this document and other solved assignments.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Introduction................................................................................................................................3

P1. Explain management accounting and give the essential requirements of different types of

management accounting.............................................................................................................4

P2. Explain different methods used for management accounting reporting..............................6

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing......................................................................7

P4. Explain the advantages and disadvantages of different types of planning tools used in

budgetary control.....................................................................................................................10

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems....................................................................................................................12

Conclusion................................................................................................................................14

Reference list............................................................................................................................15

2 | P a g e

Introduction................................................................................................................................3

P1. Explain management accounting and give the essential requirements of different types of

management accounting.............................................................................................................4

P2. Explain different methods used for management accounting reporting..............................6

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing......................................................................7

P4. Explain the advantages and disadvantages of different types of planning tools used in

budgetary control.....................................................................................................................10

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems....................................................................................................................12

Conclusion................................................................................................................................14

Reference list............................................................................................................................15

2 | P a g e

Introduction

Management accounting is a wider organizational system that takes care of the entire

activities of the business. In one hand, management accounting controls the cost level of the

business; on the other hand, it takes care of the revenue flow in the business. The use of

management accounting system is increasing in the business world because of the large

contribution that it makes in business success.

In this study, the effectiveness of management accounting system in business growth will be

analyzed by considering the business scenario of Zylla Company. Zylla is a multinational

organization that is operating business in UK for several years. However, the management of

the company is recently focusing on the management accounting system. The aim of this

study is to help the managers at Zylla Company understanding usefulness of management

accounting system.

3 | P a g e

Management accounting is a wider organizational system that takes care of the entire

activities of the business. In one hand, management accounting controls the cost level of the

business; on the other hand, it takes care of the revenue flow in the business. The use of

management accounting system is increasing in the business world because of the large

contribution that it makes in business success.

In this study, the effectiveness of management accounting system in business growth will be

analyzed by considering the business scenario of Zylla Company. Zylla is a multinational

organization that is operating business in UK for several years. However, the management of

the company is recently focusing on the management accounting system. The aim of this

study is to help the managers at Zylla Company understanding usefulness of management

accounting system.

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P1. Explain management accounting and give the essential requirements of different

types of management accounting

Management accounting is a continuous process that aims to make the business successful.

Ahmad (2017) has defined management accounting as the key factor behind organizational

success in the current competitive scenario. The process of management accounting starts

with developing effective plans for the business activities and after that it guides the

managers until the objectives of the company are achieved (Ax and Greve, 2017).

The concept of management accounting was originated with the industrial revolution in

Western countries. At the initial period, the aim of management accounting was controlling

the cost level of the business (Taipaleenmaki and Ikaheimo, 2013). However, gradually the

use of management accounting technique expanded to other areas of business. Management

accounting follows certain key principles, which are mentioned below:

Principle of value creation

Principle of achieving stakeholders’ trust

Principle of encouraging managers for better performance

Principle of generating and providing relevant data and information to the users (Le et

al., 2017)

Considering the role of management accounting, the following can be identified:

Management accounting is a major player in developing effective plans for the

business. It means if the managers at Zylla Company adopt the management

accounting technique or system, developing effective plans will be easier.

Management accounting is also a major player in role of inventory management. This

particular system provides several techniques of inventory management that helps the

managers maintaining inventory at the standard level (Ahmad, 2017).

Another important role management accounting plays is controlling organizational

activities. Adopting the management accounting system, the managers at Zylla

Company will be able to control the business activities efficiently.

In this context, it is important to mention that management accounting is not similar to

financial accounting. There are the following differences between the two:

4 | P a g e

types of management accounting

Management accounting is a continuous process that aims to make the business successful.

Ahmad (2017) has defined management accounting as the key factor behind organizational

success in the current competitive scenario. The process of management accounting starts

with developing effective plans for the business activities and after that it guides the

managers until the objectives of the company are achieved (Ax and Greve, 2017).

The concept of management accounting was originated with the industrial revolution in

Western countries. At the initial period, the aim of management accounting was controlling

the cost level of the business (Taipaleenmaki and Ikaheimo, 2013). However, gradually the

use of management accounting technique expanded to other areas of business. Management

accounting follows certain key principles, which are mentioned below:

Principle of value creation

Principle of achieving stakeholders’ trust

Principle of encouraging managers for better performance

Principle of generating and providing relevant data and information to the users (Le et

al., 2017)

Considering the role of management accounting, the following can be identified:

Management accounting is a major player in developing effective plans for the

business. It means if the managers at Zylla Company adopt the management

accounting technique or system, developing effective plans will be easier.

Management accounting is also a major player in role of inventory management. This

particular system provides several techniques of inventory management that helps the

managers maintaining inventory at the standard level (Ahmad, 2017).

Another important role management accounting plays is controlling organizational

activities. Adopting the management accounting system, the managers at Zylla

Company will be able to control the business activities efficiently.

In this context, it is important to mention that management accounting is not similar to

financial accounting. There are the following differences between the two:

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

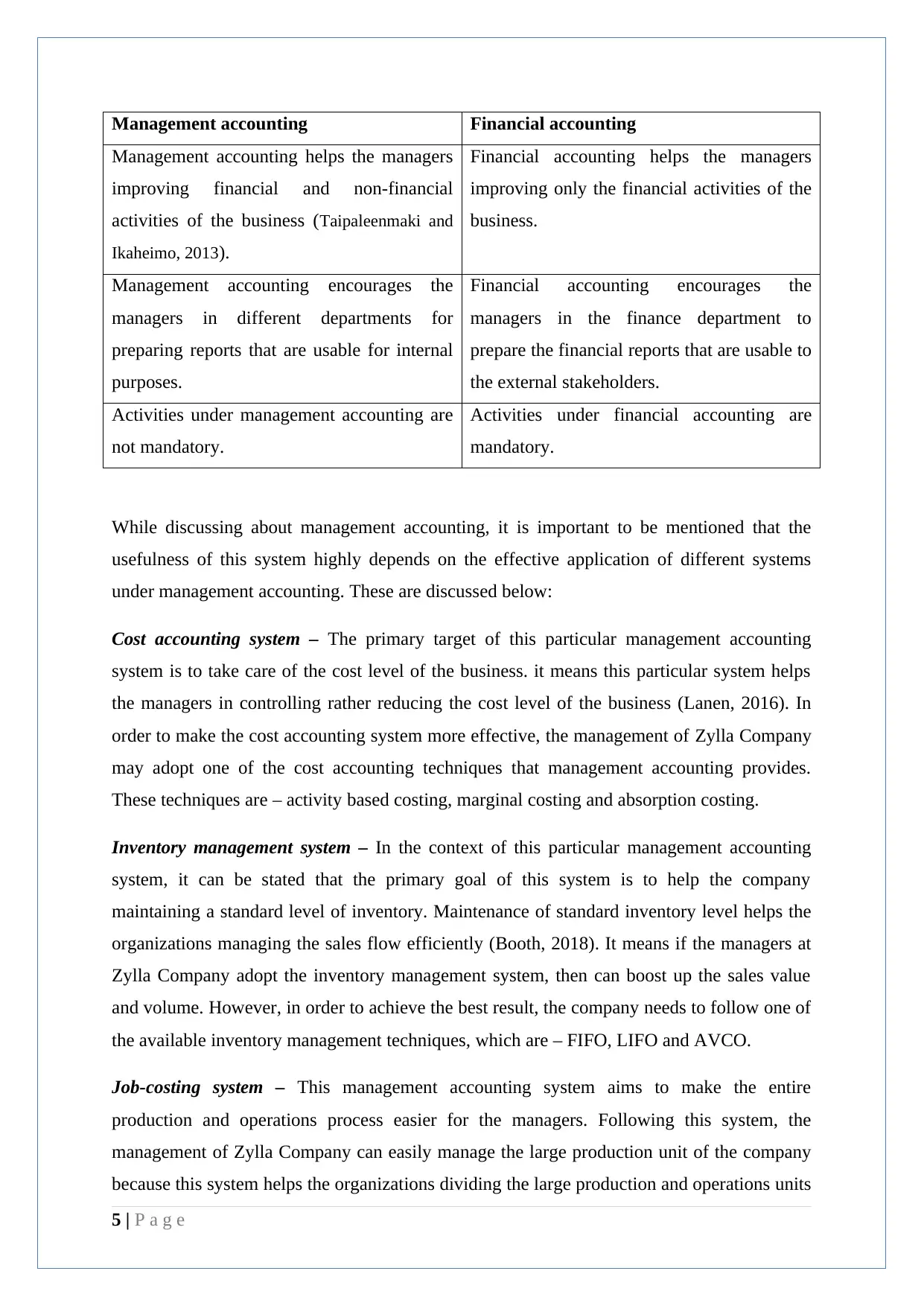

Management accounting Financial accounting

Management accounting helps the managers

improving financial and non-financial

activities of the business (Taipaleenmaki and

Ikaheimo, 2013).

Financial accounting helps the managers

improving only the financial activities of the

business.

Management accounting encourages the

managers in different departments for

preparing reports that are usable for internal

purposes.

Financial accounting encourages the

managers in the finance department to

prepare the financial reports that are usable to

the external stakeholders.

Activities under management accounting are

not mandatory.

Activities under financial accounting are

mandatory.

While discussing about management accounting, it is important to be mentioned that the

usefulness of this system highly depends on the effective application of different systems

under management accounting. These are discussed below:

Cost accounting system – The primary target of this particular management accounting

system is to take care of the cost level of the business. it means this particular system helps

the managers in controlling rather reducing the cost level of the business (Lanen, 2016). In

order to make the cost accounting system more effective, the management of Zylla Company

may adopt one of the cost accounting techniques that management accounting provides.

These techniques are – activity based costing, marginal costing and absorption costing.

Inventory management system – In the context of this particular management accounting

system, it can be stated that the primary goal of this system is to help the company

maintaining a standard level of inventory. Maintenance of standard inventory level helps the

organizations managing the sales flow efficiently (Booth, 2018). It means if the managers at

Zylla Company adopt the inventory management system, then can boost up the sales value

and volume. However, in order to achieve the best result, the company needs to follow one of

the available inventory management techniques, which are – FIFO, LIFO and AVCO.

Job-costing system – This management accounting system aims to make the entire

production and operations process easier for the managers. Following this system, the

management of Zylla Company can easily manage the large production unit of the company

because this system helps the organizations dividing the large production and operations units

5 | P a g e

Management accounting helps the managers

improving financial and non-financial

activities of the business (Taipaleenmaki and

Ikaheimo, 2013).

Financial accounting helps the managers

improving only the financial activities of the

business.

Management accounting encourages the

managers in different departments for

preparing reports that are usable for internal

purposes.

Financial accounting encourages the

managers in the finance department to

prepare the financial reports that are usable to

the external stakeholders.

Activities under management accounting are

not mandatory.

Activities under financial accounting are

mandatory.

While discussing about management accounting, it is important to be mentioned that the

usefulness of this system highly depends on the effective application of different systems

under management accounting. These are discussed below:

Cost accounting system – The primary target of this particular management accounting

system is to take care of the cost level of the business. it means this particular system helps

the managers in controlling rather reducing the cost level of the business (Lanen, 2016). In

order to make the cost accounting system more effective, the management of Zylla Company

may adopt one of the cost accounting techniques that management accounting provides.

These techniques are – activity based costing, marginal costing and absorption costing.

Inventory management system – In the context of this particular management accounting

system, it can be stated that the primary goal of this system is to help the company

maintaining a standard level of inventory. Maintenance of standard inventory level helps the

organizations managing the sales flow efficiently (Booth, 2018). It means if the managers at

Zylla Company adopt the inventory management system, then can boost up the sales value

and volume. However, in order to achieve the best result, the company needs to follow one of

the available inventory management techniques, which are – FIFO, LIFO and AVCO.

Job-costing system – This management accounting system aims to make the entire

production and operations process easier for the managers. Following this system, the

management of Zylla Company can easily manage the large production unit of the company

because this system helps the organizations dividing the large production and operations units

5 | P a g e

into small jobs, which are easy to handle (Parker and Fleischman, 2017). Hence, application

of this system will make the business process easier.

Price optimization system – This is the system of management accounting that aims to

develop the right pricing strategy for the business. Identifying the right strategy of pricing the

management of Zylla Company will be able to capture the market more effectively. However,

in order to enjoy the benefits of price optimization system, the company needs to analyze its

internal and external business environments properly (Ismail et al., 2018).

P2. Explain different methods used for management accounting reporting

Management accounting generates relevant reports that make the business operations easier

for the companies. These reports are discussed below:

Budgets – This is considered to be one of the most important reports that management

accounting helps to generate. Budget is nothing but the financial plan for the business. Using

budget, managers at Zylla Company will be able to allocate the resources efficiently, so that

the income of the company reaches to the highest level. At the time of developing budgets,

the managers need to analyze several factors like, business environments, resource capacity

and efficiency level of the business (Smith et al., 2017).

Departmental reports:

Sales report – This report is prepared under the management accounting system to keep track

on the sales level of the business. In the sales report of the company, the managers of Sales

department must include all detailed information regarding sales value, sales volume and cost

of sales in the particular financial year (Ahmad, 2017).

Production report – This report provides the information about the production level of the

company. In this report of management accounting, detailed information regarding quantity

of production, amount o raw materials used, cost of production and many other production

related information is available (Ax and Greve, 2017). Preparing the production report

management can understand, whether they need to improve the production system in the

coming years.

Inventory report – This is another most important management accounting report that

provides information regarding the inventory level of the business. using this particular

6 | P a g e

of this system will make the business process easier.

Price optimization system – This is the system of management accounting that aims to

develop the right pricing strategy for the business. Identifying the right strategy of pricing the

management of Zylla Company will be able to capture the market more effectively. However,

in order to enjoy the benefits of price optimization system, the company needs to analyze its

internal and external business environments properly (Ismail et al., 2018).

P2. Explain different methods used for management accounting reporting

Management accounting generates relevant reports that make the business operations easier

for the companies. These reports are discussed below:

Budgets – This is considered to be one of the most important reports that management

accounting helps to generate. Budget is nothing but the financial plan for the business. Using

budget, managers at Zylla Company will be able to allocate the resources efficiently, so that

the income of the company reaches to the highest level. At the time of developing budgets,

the managers need to analyze several factors like, business environments, resource capacity

and efficiency level of the business (Smith et al., 2017).

Departmental reports:

Sales report – This report is prepared under the management accounting system to keep track

on the sales level of the business. In the sales report of the company, the managers of Sales

department must include all detailed information regarding sales value, sales volume and cost

of sales in the particular financial year (Ahmad, 2017).

Production report – This report provides the information about the production level of the

company. In this report of management accounting, detailed information regarding quantity

of production, amount o raw materials used, cost of production and many other production

related information is available (Ax and Greve, 2017). Preparing the production report

management can understand, whether they need to improve the production system in the

coming years.

Inventory report – This is another most important management accounting report that

provides information regarding the inventory level of the business. using this particular

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

report, the manages in the production and sales department can understand how many

quantity they need to produce and sale.

Capital budgeting report:

Investment appraisal report – This report is developed while making any capital investment

decision. This report helps to understand whether a particular investment option is suitable

for the company or the company needs to ignore the same. The investment appraisal report

indicates the suitability from different perspectives like, internal return, time span required to

return the initial investment and profitability of the project (Alkhamis et al., 2017).

While preparing different departmental and other reports, the management accountant at

Zylla Company must ensure that the information in the reports must be understandable. It

means presentation of information in the reports must be in proper format. The reports must

include complete information regarding the business. Fair, understandable and complete

representation of the report is important because these reports play major role in

organizational decision-making process (Ismail et al., 2018). If the reports or information in

the reports are not presented in the proper format, it will be difficult for the higher

management to understand the information rightly and due to that decision-making will be

delayed. Moreover, improper representation of information may lead to wrong business

decision. Hence, presenting the information in understandable manner is very important for

every company.

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing

Cost is the term that is used to indicate the amount of spending incurred by an organization in

a particular financial year. In an organization, cost can be of different types like, fixed costs,

variable costs and semi-variable costs (Parker and Fleischman, 2017). Considering the

behaviour, costs of an organization can be divided in to two parts – direct costs and indirect

costs.

Absorption and marginal costing are the two different costing techniques under management

accounting. The use of absorption costing and marginal costing can be better understood with

the help of following example:

Application of absorption costing technique in the context of Bailey Plc example:

7 | P a g e

quantity they need to produce and sale.

Capital budgeting report:

Investment appraisal report – This report is developed while making any capital investment

decision. This report helps to understand whether a particular investment option is suitable

for the company or the company needs to ignore the same. The investment appraisal report

indicates the suitability from different perspectives like, internal return, time span required to

return the initial investment and profitability of the project (Alkhamis et al., 2017).

While preparing different departmental and other reports, the management accountant at

Zylla Company must ensure that the information in the reports must be understandable. It

means presentation of information in the reports must be in proper format. The reports must

include complete information regarding the business. Fair, understandable and complete

representation of the report is important because these reports play major role in

organizational decision-making process (Ismail et al., 2018). If the reports or information in

the reports are not presented in the proper format, it will be difficult for the higher

management to understand the information rightly and due to that decision-making will be

delayed. Moreover, improper representation of information may lead to wrong business

decision. Hence, presenting the information in understandable manner is very important for

every company.

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing

Cost is the term that is used to indicate the amount of spending incurred by an organization in

a particular financial year. In an organization, cost can be of different types like, fixed costs,

variable costs and semi-variable costs (Parker and Fleischman, 2017). Considering the

behaviour, costs of an organization can be divided in to two parts – direct costs and indirect

costs.

Absorption and marginal costing are the two different costing techniques under management

accounting. The use of absorption costing and marginal costing can be better understood with

the help of following example:

Application of absorption costing technique in the context of Bailey Plc example:

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

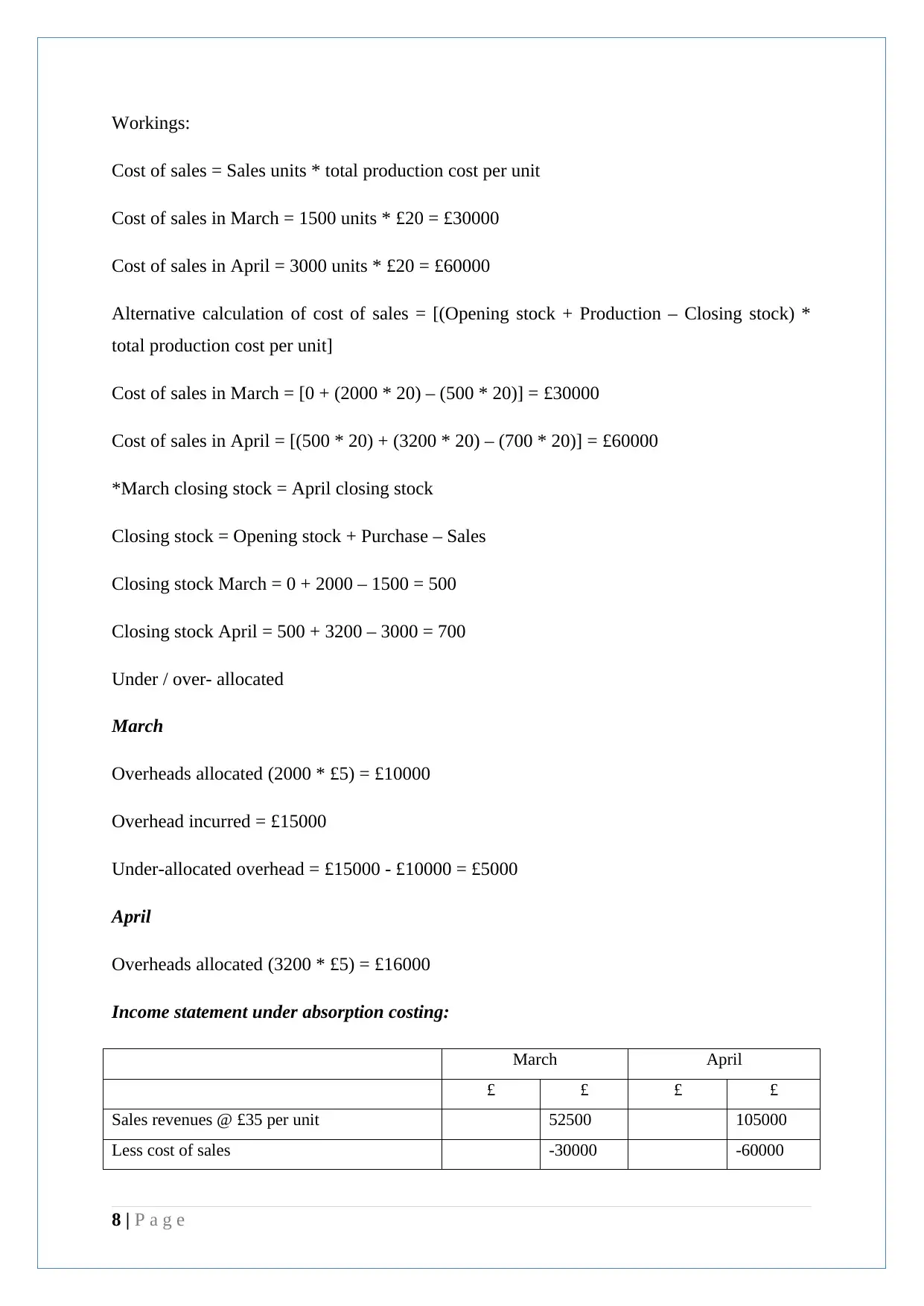

Workings:

Cost of sales = Sales units * total production cost per unit

Cost of sales in March = 1500 units * £20 = £30000

Cost of sales in April = 3000 units * £20 = £60000

Alternative calculation of cost of sales = [(Opening stock + Production – Closing stock) *

total production cost per unit]

Cost of sales in March = [0 + (2000 * 20) – (500 * 20)] = £30000

Cost of sales in April = [(500 * 20) + (3200 * 20) – (700 * 20)] = £60000

*March closing stock = April closing stock

Closing stock = Opening stock + Purchase – Sales

Closing stock March = 0 + 2000 – 1500 = 500

Closing stock April = 500 + 3200 – 3000 = 700

Under / over- allocated

March

Overheads allocated (2000 * £5) = £10000

Overhead incurred = £15000

Under-allocated overhead = £15000 - £10000 = £5000

April

Overheads allocated (3200 * £5) = £16000

Income statement under absorption costing:

March April

£ £ £ £

Sales revenues @ £35 per unit 52500 105000

Less cost of sales -30000 -60000

8 | P a g e

Cost of sales = Sales units * total production cost per unit

Cost of sales in March = 1500 units * £20 = £30000

Cost of sales in April = 3000 units * £20 = £60000

Alternative calculation of cost of sales = [(Opening stock + Production – Closing stock) *

total production cost per unit]

Cost of sales in March = [0 + (2000 * 20) – (500 * 20)] = £30000

Cost of sales in April = [(500 * 20) + (3200 * 20) – (700 * 20)] = £60000

*March closing stock = April closing stock

Closing stock = Opening stock + Purchase – Sales

Closing stock March = 0 + 2000 – 1500 = 500

Closing stock April = 500 + 3200 – 3000 = 700

Under / over- allocated

March

Overheads allocated (2000 * £5) = £10000

Overhead incurred = £15000

Under-allocated overhead = £15000 - £10000 = £5000

April

Overheads allocated (3200 * £5) = £16000

Income statement under absorption costing:

March April

£ £ £ £

Sales revenues @ £35 per unit 52500 105000

Less cost of sales -30000 -60000

8 | P a g e

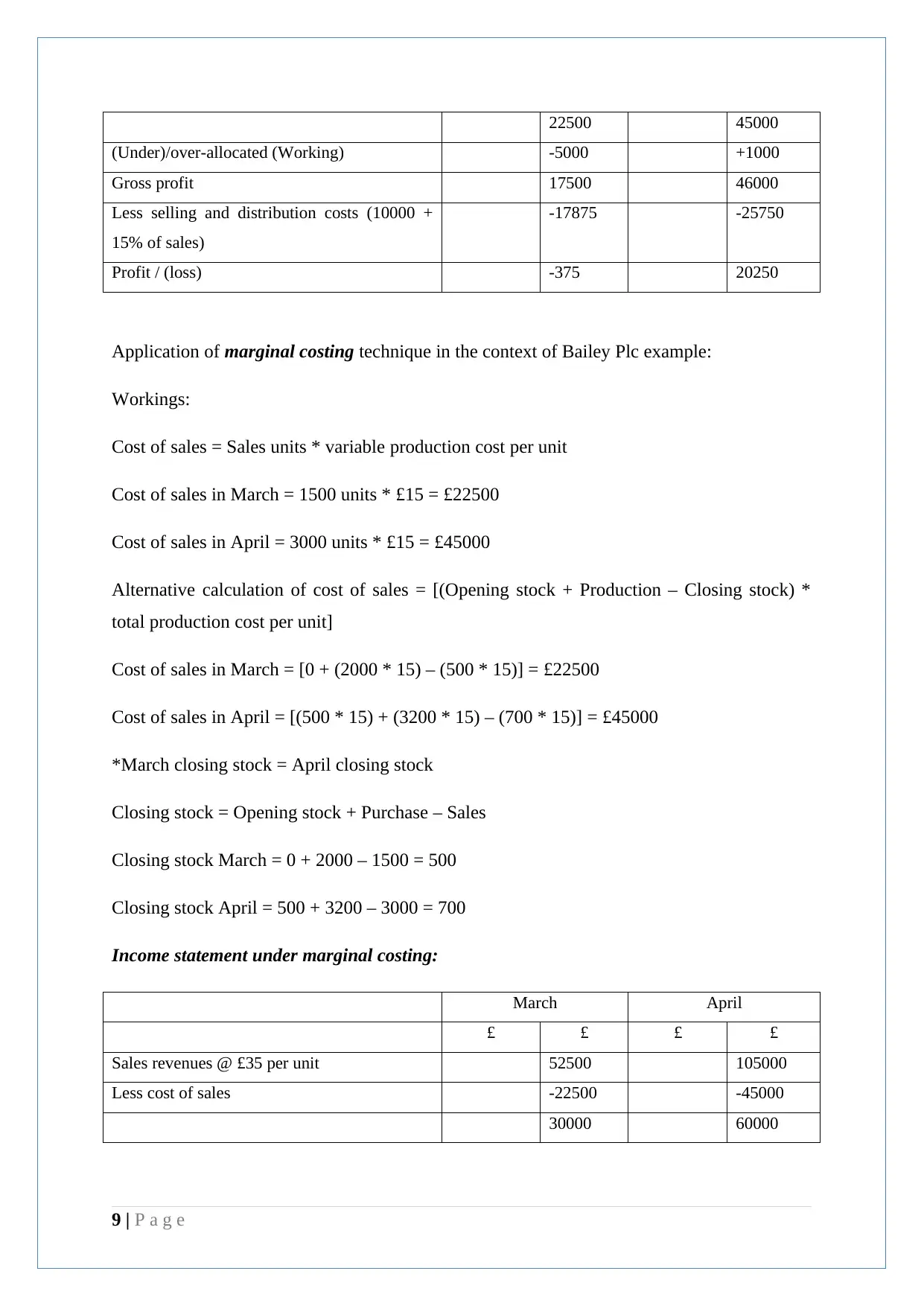

22500 45000

(Under)/over-allocated (Working) -5000 +1000

Gross profit 17500 46000

Less selling and distribution costs (10000 +

15% of sales)

-17875 -25750

Profit / (loss) -375 20250

Application of marginal costing technique in the context of Bailey Plc example:

Workings:

Cost of sales = Sales units * variable production cost per unit

Cost of sales in March = 1500 units * £15 = £22500

Cost of sales in April = 3000 units * £15 = £45000

Alternative calculation of cost of sales = [(Opening stock + Production – Closing stock) *

total production cost per unit]

Cost of sales in March = [0 + (2000 * 15) – (500 * 15)] = £22500

Cost of sales in April = [(500 * 15) + (3200 * 15) – (700 * 15)] = £45000

*March closing stock = April closing stock

Closing stock = Opening stock + Purchase – Sales

Closing stock March = 0 + 2000 – 1500 = 500

Closing stock April = 500 + 3200 – 3000 = 700

Income statement under marginal costing:

March April

£ £ £ £

Sales revenues @ £35 per unit 52500 105000

Less cost of sales -22500 -45000

30000 60000

9 | P a g e

(Under)/over-allocated (Working) -5000 +1000

Gross profit 17500 46000

Less selling and distribution costs (10000 +

15% of sales)

-17875 -25750

Profit / (loss) -375 20250

Application of marginal costing technique in the context of Bailey Plc example:

Workings:

Cost of sales = Sales units * variable production cost per unit

Cost of sales in March = 1500 units * £15 = £22500

Cost of sales in April = 3000 units * £15 = £45000

Alternative calculation of cost of sales = [(Opening stock + Production – Closing stock) *

total production cost per unit]

Cost of sales in March = [0 + (2000 * 15) – (500 * 15)] = £22500

Cost of sales in April = [(500 * 15) + (3200 * 15) – (700 * 15)] = £45000

*March closing stock = April closing stock

Closing stock = Opening stock + Purchase – Sales

Closing stock March = 0 + 2000 – 1500 = 500

Closing stock April = 500 + 3200 – 3000 = 700

Income statement under marginal costing:

March April

£ £ £ £

Sales revenues @ £35 per unit 52500 105000

Less cost of sales -22500 -45000

30000 60000

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

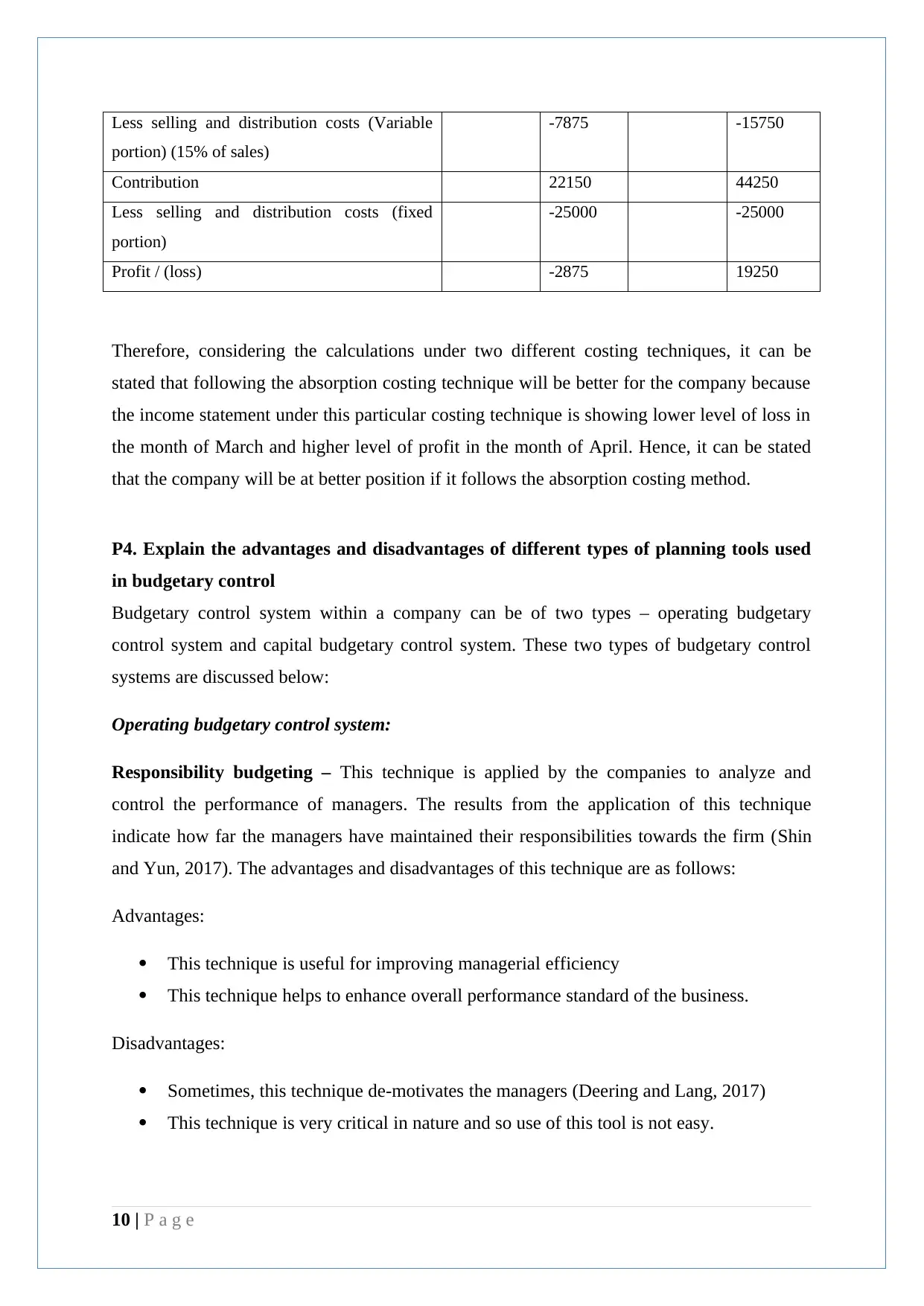

Less selling and distribution costs (Variable

portion) (15% of sales)

-7875 -15750

Contribution 22150 44250

Less selling and distribution costs (fixed

portion)

-25000 -25000

Profit / (loss) -2875 19250

Therefore, considering the calculations under two different costing techniques, it can be

stated that following the absorption costing technique will be better for the company because

the income statement under this particular costing technique is showing lower level of loss in

the month of March and higher level of profit in the month of April. Hence, it can be stated

that the company will be at better position if it follows the absorption costing method.

P4. Explain the advantages and disadvantages of different types of planning tools used

in budgetary control

Budgetary control system within a company can be of two types – operating budgetary

control system and capital budgetary control system. These two types of budgetary control

systems are discussed below:

Operating budgetary control system:

Responsibility budgeting – This technique is applied by the companies to analyze and

control the performance of managers. The results from the application of this technique

indicate how far the managers have maintained their responsibilities towards the firm (Shin

and Yun, 2017). The advantages and disadvantages of this technique are as follows:

Advantages:

This technique is useful for improving managerial efficiency

This technique helps to enhance overall performance standard of the business.

Disadvantages:

Sometimes, this technique de-motivates the managers (Deering and Lang, 2017)

This technique is very critical in nature and so use of this tool is not easy.

10 | P a g e

portion) (15% of sales)

-7875 -15750

Contribution 22150 44250

Less selling and distribution costs (fixed

portion)

-25000 -25000

Profit / (loss) -2875 19250

Therefore, considering the calculations under two different costing techniques, it can be

stated that following the absorption costing technique will be better for the company because

the income statement under this particular costing technique is showing lower level of loss in

the month of March and higher level of profit in the month of April. Hence, it can be stated

that the company will be at better position if it follows the absorption costing method.

P4. Explain the advantages and disadvantages of different types of planning tools used

in budgetary control

Budgetary control system within a company can be of two types – operating budgetary

control system and capital budgetary control system. These two types of budgetary control

systems are discussed below:

Operating budgetary control system:

Responsibility budgeting – This technique is applied by the companies to analyze and

control the performance of managers. The results from the application of this technique

indicate how far the managers have maintained their responsibilities towards the firm (Shin

and Yun, 2017). The advantages and disadvantages of this technique are as follows:

Advantages:

This technique is useful for improving managerial efficiency

This technique helps to enhance overall performance standard of the business.

Disadvantages:

Sometimes, this technique de-motivates the managers (Deering and Lang, 2017)

This technique is very critical in nature and so use of this tool is not easy.

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard costing – This technique or tool is also used by the companies for operating

budgetary control. Under this method, the cost level of the company can be planned in a

better way by identifying the performance gaps in the business. The advantages and

disadvantages of the tool are as follows:

Advantages:

This tool is very useful in controlling the cost level of the business (Smith et al.,

2017)

Standard costing tool can also be used for managing the inventory level in a better

way.

Disadvantages:

The application of this tool is time consuming and critical

This tool is mainly applicable to the financial activities. The non-financial

performance standards cannot be measured using this technique.

Capital budgetary control tools:

Net present value method – This method is considered to be the mostly used method or tool

for capital budgetary control. This method analyzes the capital investment option by

considering present value of future cash flows (Shaban et al., 2017). The advantages and

disadvantages of the method are as follows:

Advantages:

This method considers the time value of money

This method considers the profitability factor of the investment option (Abor, 2017)

Disadvantages:

This method is time consuming and critical to understand

The results from this method may differ due to sensitivity of discounting rates

Payback period – This method is considered to be the easiest capital budgetary control

method available to the companies. The advantages and disadvantages of this method are as

follows:

Advantages:

11 | P a g e

budgetary control. Under this method, the cost level of the company can be planned in a

better way by identifying the performance gaps in the business. The advantages and

disadvantages of the tool are as follows:

Advantages:

This tool is very useful in controlling the cost level of the business (Smith et al.,

2017)

Standard costing tool can also be used for managing the inventory level in a better

way.

Disadvantages:

The application of this tool is time consuming and critical

This tool is mainly applicable to the financial activities. The non-financial

performance standards cannot be measured using this technique.

Capital budgetary control tools:

Net present value method – This method is considered to be the mostly used method or tool

for capital budgetary control. This method analyzes the capital investment option by

considering present value of future cash flows (Shaban et al., 2017). The advantages and

disadvantages of the method are as follows:

Advantages:

This method considers the time value of money

This method considers the profitability factor of the investment option (Abor, 2017)

Disadvantages:

This method is time consuming and critical to understand

The results from this method may differ due to sensitivity of discounting rates

Payback period – This method is considered to be the easiest capital budgetary control

method available to the companies. The advantages and disadvantages of this method are as

follows:

Advantages:

11 | P a g e

Payback period method is simple to understand (Hayward et al., 2017)

This method provides the assurance of getting back the initial investment

Disadvantages:

The time value of money is ignored under this method (Nawaiseh et al., 2017)

This method does not consider the profitability factor of the capital investment option

P5. Compare how organisations are adapting management accounting systems to

respond to financial problems

Managing financial problems effectively is very important for the future growth of the

business. If Zylla Company faces financial trouble, the management needs to adopt some

effective techniques to deal with the situation. In this context, it can be stated that the

management of Zylla Company can easily handle the financial problem of the organization

efficiently. There are some techniques that can be used for handling the financial problem

within the company. These techniques are discussed below:

Benchmarking – This process is very effective for dealing with the financial problem at the

organization. In this technique, the organization needs to select a particular standard, which is

considered as the benchmark performance standard for the company. In order to identify the

perfect benchmark, the company may consider the performance level of the top performer in

the industry (ElMaraghy et al., 2017). After setting the benchmark, the higher authority

encourages the departmental heads for achieving the benchmarked performance standard

within the particular time span. This entire process takes some time, but this is very easy

method that Zylla Company may follow while dealing with any financial trouble.

Key performance indicators – There are certain financial factors considering which the

management can easily understand the performance trend of the business. These factors are

known as the key performance indicators of the business (Maté et al., 2017). The most useful

key performance indicators that can help the management of Zylla Company understanding

the financial performance standards and loopholes in the performance are – revenue, cost of

sales, net profit, cash flows and many others. These factors indicate the areas where the

company is lacking behind. Considering the key performance indicators management can

make decisions very easily and within the limited time span.

12 | P a g e

This method provides the assurance of getting back the initial investment

Disadvantages:

The time value of money is ignored under this method (Nawaiseh et al., 2017)

This method does not consider the profitability factor of the capital investment option

P5. Compare how organisations are adapting management accounting systems to

respond to financial problems

Managing financial problems effectively is very important for the future growth of the

business. If Zylla Company faces financial trouble, the management needs to adopt some

effective techniques to deal with the situation. In this context, it can be stated that the

management of Zylla Company can easily handle the financial problem of the organization

efficiently. There are some techniques that can be used for handling the financial problem

within the company. These techniques are discussed below:

Benchmarking – This process is very effective for dealing with the financial problem at the

organization. In this technique, the organization needs to select a particular standard, which is

considered as the benchmark performance standard for the company. In order to identify the

perfect benchmark, the company may consider the performance level of the top performer in

the industry (ElMaraghy et al., 2017). After setting the benchmark, the higher authority

encourages the departmental heads for achieving the benchmarked performance standard

within the particular time span. This entire process takes some time, but this is very easy

method that Zylla Company may follow while dealing with any financial trouble.

Key performance indicators – There are certain financial factors considering which the

management can easily understand the performance trend of the business. These factors are

known as the key performance indicators of the business (Maté et al., 2017). The most useful

key performance indicators that can help the management of Zylla Company understanding

the financial performance standards and loopholes in the performance are – revenue, cost of

sales, net profit, cash flows and many others. These factors indicate the areas where the

company is lacking behind. Considering the key performance indicators management can

make decisions very easily and within the limited time span.

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.