Analysing Cost, Reporting Methods and Adapting Accounting Systems

VerifiedAdded on 2023/06/08

|17

|4887

|402

Report

AI Summary

This report defines management accounting and its systems, explaining their role and principles. It uses techniques like marginal and absorption costing to analyze costs and prepare income statements. Different planning tools for budgetary control are evaluated, highlighting their advantages and disadvantages. Furthermore, it discusses how organizations adapt their management accounting systems to respond to financial challenges, specifically referencing Airdri Group. The report covers cost-bookkeeping, stock administration, cost streamlining, and job costing frameworks. Methods for management accounting reporting, including cost, budget, performance, and inventory management reports, are also explored.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

P1 Define management accounting and also give important requirements of various kinds of

management accounting system..................................................................................................3

P2 Explain different methods used for management accounting reporting................................5

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................6

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control......................................................................................................................10

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................12

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

P1 Define management accounting and also give important requirements of various kinds of

management accounting system..................................................................................................3

P2 Explain different methods used for management accounting reporting................................5

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................6

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control......................................................................................................................10

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................12

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is a type of method which is passed in every business for

making various reports by analysing the fundamentals of organisation. It is an exercise for

identification, measurement, examining and interpreting the fundamentals or financial

information to manager for achieving the goal of an organisation. It differs from financial

accounting because the intention or the motive of managerial accounting is to provide help to the

internal users of the organisation to achieve the goals of the company. Airdri Group was founded

in year 1974 by two mechanical and electrical engineers. By starting of best exercises and

maintaining the honesty Airdri Group try to fulfill duties with regard to environment, providing

trustworthy and innovative commodities that presents dedication of Airdri group by not wasting

or saving of energy, decreasing in level of noise and purify air. In the year 2020, Airdri has

established SteraSpace, a changing the best in class air and sanitisers for surface, that are

assembled in a particular manner that make sure 99.6% of bacteria and germs are eliminated

(Bagherzadegan, and Khanmohammadi, 2019).The report consists of two parts. The first part

includes the role and principle of management accounting and its systems which are explained in

detail using the techniques and method of marginal and absorption costing. Further, the part is

summed up by describing the integration and benefits of it in the entity. The second part takes

into consideration the different planning tools. Also the financial problems of Airdri Group are

discussed in the following report.

MAIN BODY

P1 Define management accounting and also give important requirements of various kinds of

management accounting system.

Management Accounting

It is also named as managerial accounting. It is a method of accounting that aids in

generating of statements, reports and documents that assists the management in the process of

decision making which are linked with the performance of business. It is mainly used for internal

operations of an organisation. It assists the management to perform all its functions including

planning, organizing, staffing, directing and controlling (Baxter, and Chua, 2019).

Influence: Communicating with impact facilitates decision making about strategy application at

all level of the organisation. This concerns to how decisions are made, basis on which the

Management accounting is a type of method which is passed in every business for

making various reports by analysing the fundamentals of organisation. It is an exercise for

identification, measurement, examining and interpreting the fundamentals or financial

information to manager for achieving the goal of an organisation. It differs from financial

accounting because the intention or the motive of managerial accounting is to provide help to the

internal users of the organisation to achieve the goals of the company. Airdri Group was founded

in year 1974 by two mechanical and electrical engineers. By starting of best exercises and

maintaining the honesty Airdri Group try to fulfill duties with regard to environment, providing

trustworthy and innovative commodities that presents dedication of Airdri group by not wasting

or saving of energy, decreasing in level of noise and purify air. In the year 2020, Airdri has

established SteraSpace, a changing the best in class air and sanitisers for surface, that are

assembled in a particular manner that make sure 99.6% of bacteria and germs are eliminated

(Bagherzadegan, and Khanmohammadi, 2019).The report consists of two parts. The first part

includes the role and principle of management accounting and its systems which are explained in

detail using the techniques and method of marginal and absorption costing. Further, the part is

summed up by describing the integration and benefits of it in the entity. The second part takes

into consideration the different planning tools. Also the financial problems of Airdri Group are

discussed in the following report.

MAIN BODY

P1 Define management accounting and also give important requirements of various kinds of

management accounting system.

Management Accounting

It is also named as managerial accounting. It is a method of accounting that aids in

generating of statements, reports and documents that assists the management in the process of

decision making which are linked with the performance of business. It is mainly used for internal

operations of an organisation. It assists the management to perform all its functions including

planning, organizing, staffing, directing and controlling (Baxter, and Chua, 2019).

Influence: Communicating with impact facilitates decision making about strategy application at

all level of the organisation. This concerns to how decisions are made, basis on which the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decisions are tailored. It also shows the break down how conclusion have been reached. In a

manufacturing unit like Airdrie group. Decisions are to be made at each level, effective

communication and transparency of decision taken should be given. This makes sure the smooth

operation of the enterprise.

Value: The causality principle which depicts that input and output cause and effect should be

base of operations. The cost involved in production should be directly proportional to its

productivity. In this case, Airdrie group is involved in manufacturing Renewable source of

energy semiconductor. This principle is applied through analysis of all the production unit their

productivity and cost involved in manufacturing. The results of the analysis help in production

decisions.

Relevant: Validity of information, its sources from where it is extracts should relevant to the

organisational plan. This is important when making strategies and applying them in the

organisation. This involves maintaining a proper balance between the financial, non-financial,

past trends analysis, future projections and internal-external information about environment of

the company. Airdrie group decisions to achieve the organisational goal are made considering all

those factors. So that effective and efficient decisions can be taken.

Principle of analogy: The fourth principal of management is the application of management

accounting through directing, controlling and motivating. These activities are done by analysing

insights from past trends and future estimations. This is basically applied by top management

level of the company.

Role of management accounting and its systems.

It refers to an process that usually centres about observing and evaluating stratified

objectives to refer distinctive monetary and non-monetary data to higher governing body of

organisation. Administrators can uses this information for making various financial plans and

implementation of reports. The executive accounting is surely have more unpredicted content as

compared to organised summaries of budget. Main difference between them is that the prior one

is ready in affiliation with inner cycles on the contrary the last one is brought up for outsiders

such as investors. It generally assist in predicting future patterns and incomes of company

function which also advises in making plans related to spending.

The accounting framework is a tool of supervising and effecting employees just as

various costs which are primary for accomplishing important goals (Boyle, Boyle, and

manufacturing unit like Airdrie group. Decisions are to be made at each level, effective

communication and transparency of decision taken should be given. This makes sure the smooth

operation of the enterprise.

Value: The causality principle which depicts that input and output cause and effect should be

base of operations. The cost involved in production should be directly proportional to its

productivity. In this case, Airdrie group is involved in manufacturing Renewable source of

energy semiconductor. This principle is applied through analysis of all the production unit their

productivity and cost involved in manufacturing. The results of the analysis help in production

decisions.

Relevant: Validity of information, its sources from where it is extracts should relevant to the

organisational plan. This is important when making strategies and applying them in the

organisation. This involves maintaining a proper balance between the financial, non-financial,

past trends analysis, future projections and internal-external information about environment of

the company. Airdrie group decisions to achieve the organisational goal are made considering all

those factors. So that effective and efficient decisions can be taken.

Principle of analogy: The fourth principal of management is the application of management

accounting through directing, controlling and motivating. These activities are done by analysing

insights from past trends and future estimations. This is basically applied by top management

level of the company.

Role of management accounting and its systems.

It refers to an process that usually centres about observing and evaluating stratified

objectives to refer distinctive monetary and non-monetary data to higher governing body of

organisation. Administrators can uses this information for making various financial plans and

implementation of reports. The executive accounting is surely have more unpredicted content as

compared to organised summaries of budget. Main difference between them is that the prior one

is ready in affiliation with inner cycles on the contrary the last one is brought up for outsiders

such as investors. It generally assist in predicting future patterns and incomes of company

function which also advises in making plans related to spending.

The accounting framework is a tool of supervising and effecting employees just as

various costs which are primary for accomplishing important goals (Boyle, Boyle, and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hermanson, 2020). Compulsory implementation of the accounting framework in Airdri Group is

beneficial as it provides different experiences which helps in direction and organising

procedures.

Some of the Management accounting systems are:

Cost-bookkeeping framework is a strategy wise system which aids in associating in

evaluating item cost for providing advantageous and stock valuation. It is beneficial for

the company as it aids in administration of beneficial items for activities in business. This

strategy initially helps the bookkeepers of foundation in easily availability of fiscal

report. It includes of occupation request and strategies of cycling cost.

Stock administration system is concerned with anticipation and changes in bookkeeping

changes in inventory at various stages. Businesses includes this model to expand its deals

and increase net revenues. Stock of businesses are of three types, to be specific,

unprocessed components, work underway and accomplished commodities. Its action is

usually required in organisations to increase operational ability and duration of business

project. It assists the organisation in differentiating direct cost related with acquiring and

thoroughgoing away interactivity. It also assists entity in holding additional stock which

aids in occurrence of deficiencies (Campbell, Mauler, and Pierce, 2019).

Cost streamlining framework arithmetic model which aids an organisation in fall down

and assessment of requests and the level of volatility is high with the changes in

administration or value of an item. The collected information within the model is

compiled with cost and inventory and recommendation that promotes in increasing the

productivity level. Airdrie indulges this model for collecting information about trends in

market, request of clients and propensity for better working of operational activities.

Job costing framework is a plan of collecting different kind of data for pursuing and

analyse cost with interpreted work. It requires for absorbing various data in context with

direct material, cost and upward. Airdrie includes this model for winding up of accurate

of its analysing framework which aids it in promoting cost valuation of items.

Furthermore, it helps association in development sensible benefit. Basics of this model in

an consortium is constantly analysing of creation procedure which aids with

acknowledging all conflicts and making adaption for any new injure scenario (Chung,

and Cho, 2018).

beneficial as it provides different experiences which helps in direction and organising

procedures.

Some of the Management accounting systems are:

Cost-bookkeeping framework is a strategy wise system which aids in associating in

evaluating item cost for providing advantageous and stock valuation. It is beneficial for

the company as it aids in administration of beneficial items for activities in business. This

strategy initially helps the bookkeepers of foundation in easily availability of fiscal

report. It includes of occupation request and strategies of cycling cost.

Stock administration system is concerned with anticipation and changes in bookkeeping

changes in inventory at various stages. Businesses includes this model to expand its deals

and increase net revenues. Stock of businesses are of three types, to be specific,

unprocessed components, work underway and accomplished commodities. Its action is

usually required in organisations to increase operational ability and duration of business

project. It assists the organisation in differentiating direct cost related with acquiring and

thoroughgoing away interactivity. It also assists entity in holding additional stock which

aids in occurrence of deficiencies (Campbell, Mauler, and Pierce, 2019).

Cost streamlining framework arithmetic model which aids an organisation in fall down

and assessment of requests and the level of volatility is high with the changes in

administration or value of an item. The collected information within the model is

compiled with cost and inventory and recommendation that promotes in increasing the

productivity level. Airdrie indulges this model for collecting information about trends in

market, request of clients and propensity for better working of operational activities.

Job costing framework is a plan of collecting different kind of data for pursuing and

analyse cost with interpreted work. It requires for absorbing various data in context with

direct material, cost and upward. Airdrie includes this model for winding up of accurate

of its analysing framework which aids it in promoting cost valuation of items.

Furthermore, it helps association in development sensible benefit. Basics of this model in

an consortium is constantly analysing of creation procedure which aids with

acknowledging all conflicts and making adaption for any new injure scenario (Chung,

and Cho, 2018).

P2 Explain different methods used for management accounting reporting.

It is used for designing, controlling, decision making purpose and measurement of

performance. These reports are consistently created through the accounting and auditing period

according to necessities. The outcomes of management accounting is in form of periodic reports

for the organisation's department managers and CEO. For instance, current creation of sales

revenue, the recent position or condition of the entity's accounts payable and accounts

receivables etc. Management reporting looks in the business in a more elaborated manner and

represents outcomes from different sections. Instead on focusing on the entire organisation,

management reports emphasis on a specific job, department or team.

Methods used for management accounting reporting are:

Cost report: While doing a business in Airdrie group, management accounting examines

different types of costs for manufacturing items. In accordance with, cost report is

executed in Airdrie group, as it analysis all labour costs, raw material above any types of

additional cost in creating the report of management accounting. The completed

information is then properly compiled with cost report. Consequently, the method in

administrations in controlling and planning of the profit margins (Lehner, and Harrer,

2019).

Budget report: This specific procedure plays a vital role in world of management

accounting in Airdrie for describing as it focuses on maintaining and diverging budgets

with various kinds of units in company. The report of budget highlights on performance

of Airdrie group, firm and is regularized in an entity. Report represents that managers as

a guide for rearrange terms with suppliers and vendors, good employee incentives and

cutting the cost on products. Managers also work for increasing the demand in sales and

decreasing the expenses because of saving the money.

Performance report: It can be termed as a detailing statement which calculates result of

particular activities which is related to the growth of company in specified time frame.

Management accountants of Airdrie group, making optimised use of budgets for

comparison of real expenses with revenues which are related to budgeted variables and

them list or upgrading information on performance of report. When a report is build

managers plans the demand of its future for customers and the need of a product in

market and accordingly makes changes in prices (Li, 2018).

It is used for designing, controlling, decision making purpose and measurement of

performance. These reports are consistently created through the accounting and auditing period

according to necessities. The outcomes of management accounting is in form of periodic reports

for the organisation's department managers and CEO. For instance, current creation of sales

revenue, the recent position or condition of the entity's accounts payable and accounts

receivables etc. Management reporting looks in the business in a more elaborated manner and

represents outcomes from different sections. Instead on focusing on the entire organisation,

management reports emphasis on a specific job, department or team.

Methods used for management accounting reporting are:

Cost report: While doing a business in Airdrie group, management accounting examines

different types of costs for manufacturing items. In accordance with, cost report is

executed in Airdrie group, as it analysis all labour costs, raw material above any types of

additional cost in creating the report of management accounting. The completed

information is then properly compiled with cost report. Consequently, the method in

administrations in controlling and planning of the profit margins (Lehner, and Harrer,

2019).

Budget report: This specific procedure plays a vital role in world of management

accounting in Airdrie for describing as it focuses on maintaining and diverging budgets

with various kinds of units in company. The report of budget highlights on performance

of Airdrie group, firm and is regularized in an entity. Report represents that managers as

a guide for rearrange terms with suppliers and vendors, good employee incentives and

cutting the cost on products. Managers also work for increasing the demand in sales and

decreasing the expenses because of saving the money.

Performance report: It can be termed as a detailing statement which calculates result of

particular activities which is related to the growth of company in specified time frame.

Management accountants of Airdrie group, making optimised use of budgets for

comparison of real expenses with revenues which are related to budgeted variables and

them list or upgrading information on performance of report. When a report is build

managers plans the demand of its future for customers and the need of a product in

market and accordingly makes changes in prices (Li, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management report: It is an abstract of remaining stock and stills

information of such quantity of stock is accessible, products that are sold the most and

fastest, category performance etc linked to status together with presentation of inventory.

For profitably growth of Airdrie group,it is important for management inventory level in

correct and ideally ways as possible. It is authority of purchase manager of the company

to make sure that correct stock levels are sustained in accordance for manufacturing and

selling of different varieties of products. The revealing method that records all kinds of

deals which are related to diversification of inventory to different compartments and their

end results.

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Cost: It can be termed as an amount which can be paid in place of getting product or

service. In accordance with business, cost is valuation of money with sources, risk incurred,

opportunities forgone, materials, consumption of time and utilities in producing with product

delivery or any services. For analysing cost of preparation of income statement, financial

analysts uses various kinds of techniques and methods (Li, 2022,May).

Absorption Costing: In this , managers uses a method for making external financial as

well as reporting of income tax also. Analysis of techniques related to cost capturers all cost

which is related with production or selling a product.

Cost per unit -Absorption costing approach

2020 2021

Absorption cost per

unit(B) Absorption cost per unit (C)

Direct Labour cost £ 11 Direct Labour cost £ 11

Direct material cost £ 17 Direct material cost £ 17

variable expenses £ 7 variable expenses £ 7

Fixed indirect production

cost £ 24 Fixed indirect production cost £ 20

(Fixed cost per annum/production units

2020)

(Fixed cost per annum/production units

2021)

information of such quantity of stock is accessible, products that are sold the most and

fastest, category performance etc linked to status together with presentation of inventory.

For profitably growth of Airdrie group,it is important for management inventory level in

correct and ideally ways as possible. It is authority of purchase manager of the company

to make sure that correct stock levels are sustained in accordance for manufacturing and

selling of different varieties of products. The revealing method that records all kinds of

deals which are related to diversification of inventory to different compartments and their

end results.

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Cost: It can be termed as an amount which can be paid in place of getting product or

service. In accordance with business, cost is valuation of money with sources, risk incurred,

opportunities forgone, materials, consumption of time and utilities in producing with product

delivery or any services. For analysing cost of preparation of income statement, financial

analysts uses various kinds of techniques and methods (Li, 2022,May).

Absorption Costing: In this , managers uses a method for making external financial as

well as reporting of income tax also. Analysis of techniques related to cost capturers all cost

which is related with production or selling a product.

Cost per unit -Absorption costing approach

2020 2021

Absorption cost per

unit(B) Absorption cost per unit (C)

Direct Labour cost £ 11 Direct Labour cost £ 11

Direct material cost £ 17 Direct material cost £ 17

variable expenses £ 7 variable expenses £ 7

Fixed indirect production

cost £ 24 Fixed indirect production cost £ 20

(Fixed cost per annum/production units

2020)

(Fixed cost per annum/production units

2021)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total cost per unit £ 59 Total cost per unit £ 55

Income statement 2020 and 2021:

Profitability statement using absorption costing method

2020 2021

Particulars

Sales 4000 * 95 380000 4500 * 95 427500

COGS (opening

stock + purchase -

less closing stock)

Opening stock 1500 * 59 =

88500

1000 * 59 = 59000

Production

Direct labour 3500 * 11 =

38500

4200 * 11

= 46200

Direct material 3500 * 17 =

59500

4200 * 17

= 71400

Variable expenses 3500 * 7 = 24500 4200 * 7

= 29400

Fixed production

cost per annum

3500 * 24 =

84000

4200 * 20

= 84000

Less: closing

stock

1000 * 59 =

59000

236000 700 * 55

= 38500

251500

GP 144000 176000

Less:

Administrative

overhead

11000 11000

Net Profit 133000 165000

Income statement 2020 and 2021:

Profitability statement using absorption costing method

2020 2021

Particulars

Sales 4000 * 95 380000 4500 * 95 427500

COGS (opening

stock + purchase -

less closing stock)

Opening stock 1500 * 59 =

88500

1000 * 59 = 59000

Production

Direct labour 3500 * 11 =

38500

4200 * 11

= 46200

Direct material 3500 * 17 =

59500

4200 * 17

= 71400

Variable expenses 3500 * 7 = 24500 4200 * 7

= 29400

Fixed production

cost per annum

3500 * 24 =

84000

4200 * 20

= 84000

Less: closing

stock

1000 * 59 =

59000

236000 700 * 55

= 38500

251500

GP 144000 176000

Less:

Administrative

overhead

11000 11000

Net Profit 133000 165000

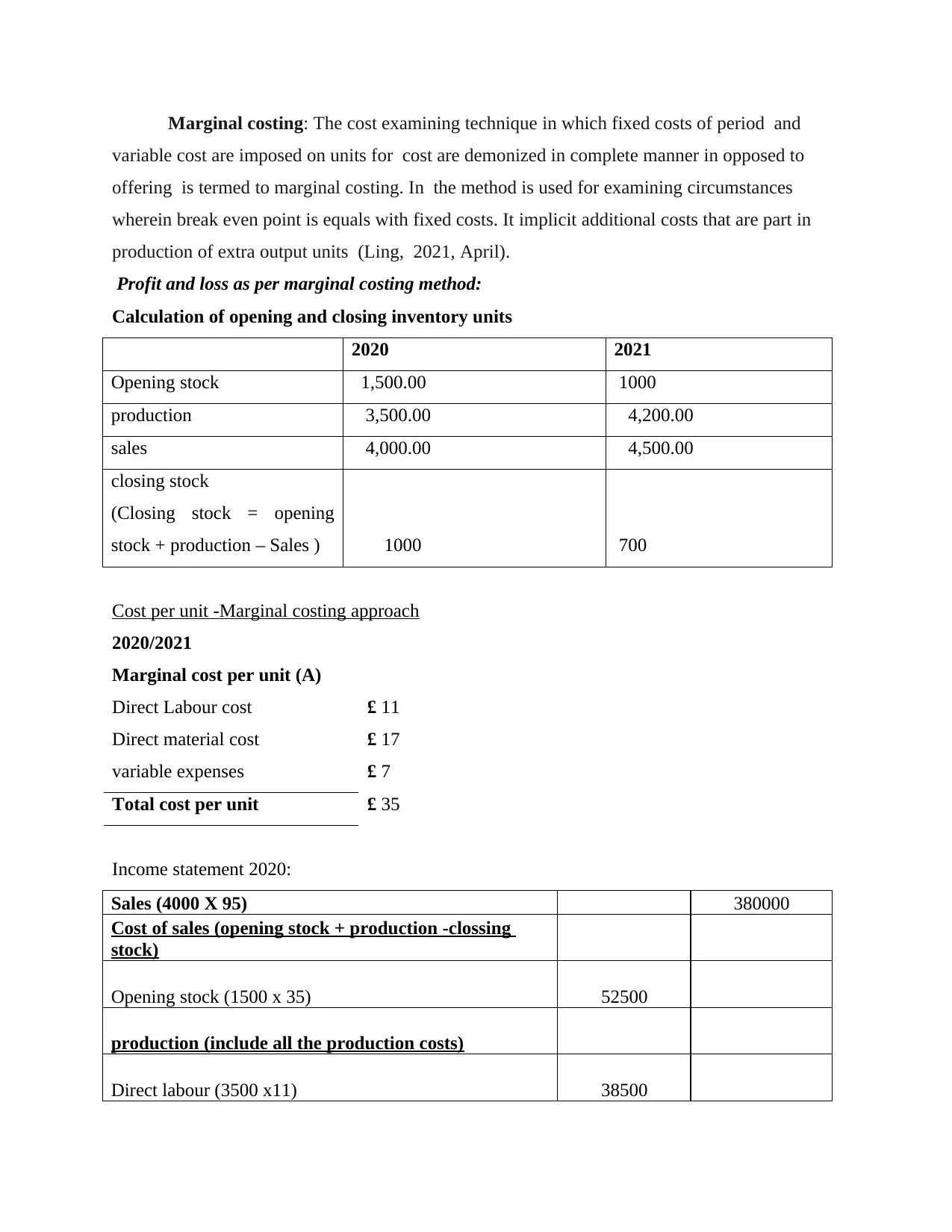

Marginal costing: The cost examining technique in which fixed costs of period and

variable cost are imposed on units for cost are demonized in complete manner in opposed to

offering is termed to marginal costing. In the method is used for examining circumstances

wherein break even point is equals with fixed costs. It implicit additional costs that are part in

production of extra output units (Ling, 2021, April).

Profit and loss as per marginal costing method:

Calculation of opening and closing inventory units

2020 2021

Opening stock 1,500.00 1000

production 3,500.00 4,200.00

sales 4,000.00 4,500.00

closing stock

(Closing stock = opening

stock + production – Sales ) 1000 700

Cost per unit -Marginal costing approach

2020/2021

Marginal cost per unit (A)

Direct Labour cost £ 11

Direct material cost £ 17

variable expenses £ 7

Total cost per unit £ 35

Income statement 2020:

Sales (4000 X 95) 380000

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1500 x 35) 52500

production (include all the production costs)

Direct labour (3500 x11) 38500

variable cost are imposed on units for cost are demonized in complete manner in opposed to

offering is termed to marginal costing. In the method is used for examining circumstances

wherein break even point is equals with fixed costs. It implicit additional costs that are part in

production of extra output units (Ling, 2021, April).

Profit and loss as per marginal costing method:

Calculation of opening and closing inventory units

2020 2021

Opening stock 1,500.00 1000

production 3,500.00 4,200.00

sales 4,000.00 4,500.00

closing stock

(Closing stock = opening

stock + production – Sales ) 1000 700

Cost per unit -Marginal costing approach

2020/2021

Marginal cost per unit (A)

Direct Labour cost £ 11

Direct material cost £ 17

variable expenses £ 7

Total cost per unit £ 35

Income statement 2020:

Sales (4000 X 95) 380000

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1500 x 35) 52500

production (include all the production costs)

Direct labour (3500 x11) 38500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

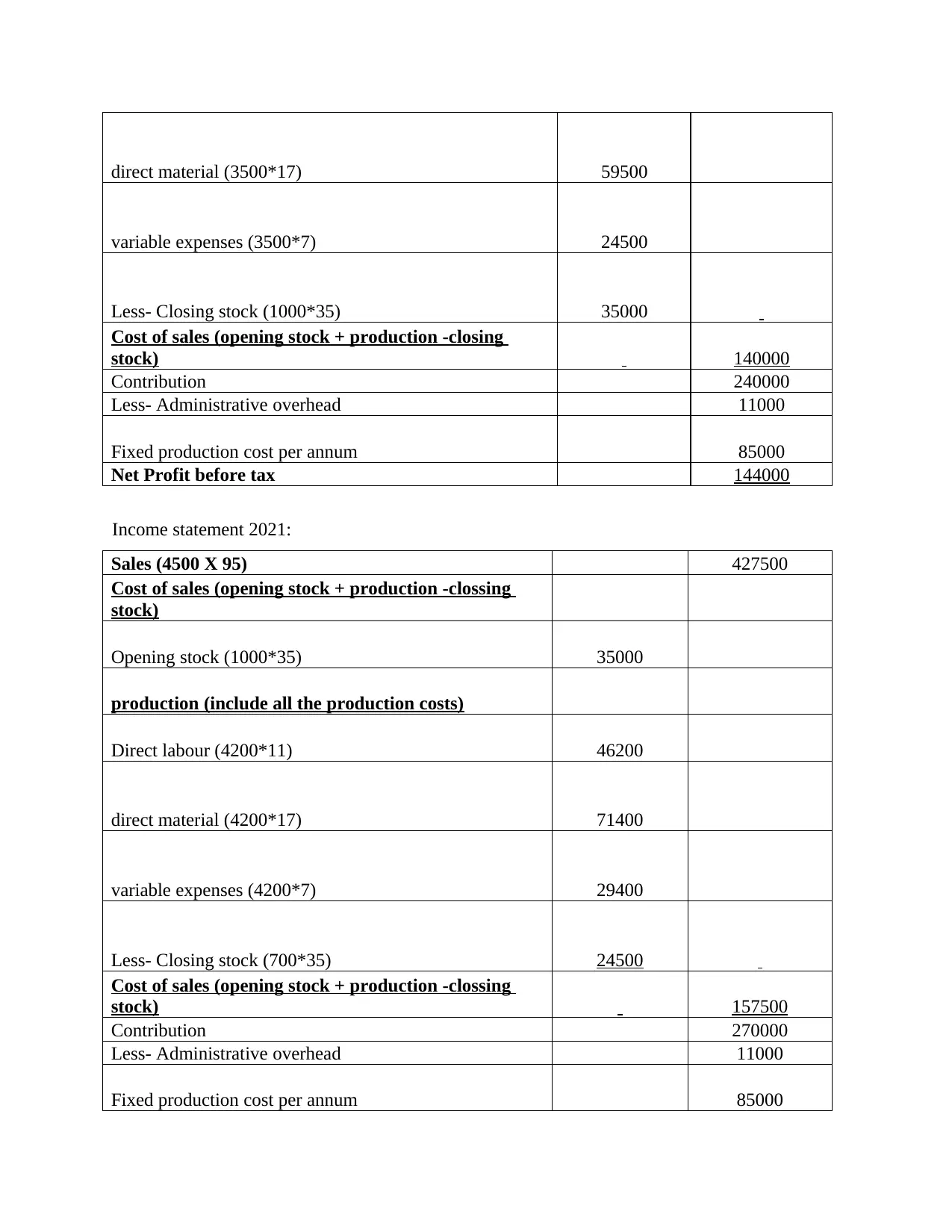

direct material (3500*17) 59500

variable expenses (3500*7) 24500

Less- Closing stock (1000*35) 35000

Cost of sales (opening stock + production -closing

stock) 140000

Contribution 240000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Net Profit before tax 144000

Income statement 2021:

Sales (4500 X 95) 427500

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1000*35) 35000

production (include all the production costs)

Direct labour (4200*11) 46200

direct material (4200*17) 71400

variable expenses (4200*7) 29400

Less- Closing stock (700*35) 24500

Cost of sales (opening stock + production -clossing

stock) 157500

Contribution 270000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

variable expenses (3500*7) 24500

Less- Closing stock (1000*35) 35000

Cost of sales (opening stock + production -closing

stock) 140000

Contribution 240000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Net Profit before tax 144000

Income statement 2021:

Sales (4500 X 95) 427500

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1000*35) 35000

production (include all the production costs)

Direct labour (4200*11) 46200

direct material (4200*17) 71400

variable expenses (4200*7) 29400

Less- Closing stock (700*35) 24500

Cost of sales (opening stock + production -clossing

stock) 157500

Contribution 270000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Profit before tax 174000

The income statement shows that through absorption costing, net profit of £ 133000 is

made in year 2020 while in year 2021, Airdrie group, achieved net profit of £ 165000. At same

time, through marginal costings, net profit of £ 144000 in year 2020 and in year 2021, net profit

of £ 174000 is generated by the company (Montenegro, and Rodrigues, 2020).

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Budgetary control process

The finance department of the organisation incorporates a variety of budgets for different

activities. On basis of which it takes corrective and directive actions for the company. A

responsibility centres are identified for a operational unit which is lead by a team leader who is

held responsible. In simple words it is a technique where actual results are being compared with

budgeted result. There are different types of methods, techniques, planning tools, used in

management accounting which can impact the outcome in efficient and effective working of a

business. There are many advantages and disadvantages which are linked with management

accounting which helps the business to grow, expansion and which can also cause obstacles in

the way (Narayanan, and Boyce, 2019).Budgetary control is the utilisation of actual expenditure

with some levels which are strictly set up the organisation. Planning tools are the instruments

which provides observation and following up the operations for implementing a specified plan

or project. Supervisors of Airdri Group are using different types of planning tools for the

properly control of the budgeting system. Some planning tools are discussed below:

Operating budget: It can be termed as a budget which is in place in accordance with all the

operations which revenues and activities related to expense as well. Supervisors of Airdrie

group use this budget for managing and controlling expense related activities in relation to

business. It also helps in prediction of issues which are related to future happenings, expenses

and take precautionary course of actions in advance. There are 3 major components of operating

budget which can be termed as revenue, variable costs, fixed costs (Ng, 2018).

The income statement shows that through absorption costing, net profit of £ 133000 is

made in year 2020 while in year 2021, Airdrie group, achieved net profit of £ 165000. At same

time, through marginal costings, net profit of £ 144000 in year 2020 and in year 2021, net profit

of £ 174000 is generated by the company (Montenegro, and Rodrigues, 2020).

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Budgetary control process

The finance department of the organisation incorporates a variety of budgets for different

activities. On basis of which it takes corrective and directive actions for the company. A

responsibility centres are identified for a operational unit which is lead by a team leader who is

held responsible. In simple words it is a technique where actual results are being compared with

budgeted result. There are different types of methods, techniques, planning tools, used in

management accounting which can impact the outcome in efficient and effective working of a

business. There are many advantages and disadvantages which are linked with management

accounting which helps the business to grow, expansion and which can also cause obstacles in

the way (Narayanan, and Boyce, 2019).Budgetary control is the utilisation of actual expenditure

with some levels which are strictly set up the organisation. Planning tools are the instruments

which provides observation and following up the operations for implementing a specified plan

or project. Supervisors of Airdri Group are using different types of planning tools for the

properly control of the budgeting system. Some planning tools are discussed below:

Operating budget: It can be termed as a budget which is in place in accordance with all the

operations which revenues and activities related to expense as well. Supervisors of Airdrie

group use this budget for managing and controlling expense related activities in relation to

business. It also helps in prediction of issues which are related to future happenings, expenses

and take precautionary course of actions in advance. There are 3 major components of operating

budget which can be termed as revenue, variable costs, fixed costs (Ng, 2018).

Advantages Disadvantages

It can have a fruitful result in Airdri

Group for calculating costs and

management on expenses of the

business functional activities for

accomplishing the main motive of

business in the long period of time. This

method can assists in making the best

available possibility to enlarge business.

It is not suitable for Airdri Group as it do not

encourage any assistance for evaluating the difference

between standard and actual costs. This method is not

considered suitable and is not flexible in nature and

working. Modifications cannot be made in policies

which are formed during the year.

Zero based budgeting: Zero based budgeting is a technique which elaborates the causes of the

expenses which are occurred in the financial year. It is used by Unilever for analysing the best

feasible uses of resources allocated at different places. There are certain advantages and

disadvantages for Airdrie group,

Advantage Disadvantages

This method assists Airdri Group in

determining the areas which aid in creation of

profits and the operational activities in which it

utilized. This provides a better, clearer and

more applicable data for understanding the

working of company and analysing of business

performance that would assists in management

of the budgets and have a proper control over

them.

It is understood as a challenging, time

consuming and an pricey process. It is

considered as tough task to detailed the usage of

expenses and creation of profit in budgets. Any

decrement in the profit margin or revenue of the

company can effect the brand image of the

company.

Capital budgeting: It is an assessment acknowledged by an organisation for the determination

and estimation of potential for essential projects and investments. For instance, planning for

investing a huge amount in machinery and new technology for long term success of operations of

entity. This technique assists Airdri Group in researching and selection of beneficial decisions

for accomplishing long term success of organisation. Its merits and demerits in context Airdri

Group are:

It can have a fruitful result in Airdri

Group for calculating costs and

management on expenses of the

business functional activities for

accomplishing the main motive of

business in the long period of time. This

method can assists in making the best

available possibility to enlarge business.

It is not suitable for Airdri Group as it do not

encourage any assistance for evaluating the difference

between standard and actual costs. This method is not

considered suitable and is not flexible in nature and

working. Modifications cannot be made in policies

which are formed during the year.

Zero based budgeting: Zero based budgeting is a technique which elaborates the causes of the

expenses which are occurred in the financial year. It is used by Unilever for analysing the best

feasible uses of resources allocated at different places. There are certain advantages and

disadvantages for Airdrie group,

Advantage Disadvantages

This method assists Airdri Group in

determining the areas which aid in creation of

profits and the operational activities in which it

utilized. This provides a better, clearer and

more applicable data for understanding the

working of company and analysing of business

performance that would assists in management

of the budgets and have a proper control over

them.

It is understood as a challenging, time

consuming and an pricey process. It is

considered as tough task to detailed the usage of

expenses and creation of profit in budgets. Any

decrement in the profit margin or revenue of the

company can effect the brand image of the

company.

Capital budgeting: It is an assessment acknowledged by an organisation for the determination

and estimation of potential for essential projects and investments. For instance, planning for

investing a huge amount in machinery and new technology for long term success of operations of

entity. This technique assists Airdri Group in researching and selection of beneficial decisions

for accomplishing long term success of organisation. Its merits and demerits in context Airdri

Group are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.