Management Accounting Systems: Costing, Reporting & Planning Analysis

VerifiedAdded on 2023/06/18

|16

|4993

|449

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and techniques, focusing on cost analysis, reporting methods, and planning tools. It defines management accounting and its crucial requirements, elaborates on various reporting methods, and demonstrates the computation of costs for income statement preparation using marginal and absorption costing. The report also analyzes the advantages and disadvantages of different planning tools and draws an analogy among firms for adopting management accounting systems to respond to financial concerns. Practical examples, such as Essentra Packing, are used to illustrate key concepts and applications, including job costing, price optimization, inventory management, and cost accounting systems. The report further explores various types of management accounting reports, such as inventory management, budget, performance, and accounts receivable aging reports. Additionally, it includes detailed calculations of material variances and inventory ledger records using LIFO and average cost methods.

Management Accounting

Systems & Techniques

Systems & Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P1. Define management accounting and their crucial requirements of their types................1

P2. Elaborate methods of management accounting reporting................................................3

P3. Computation of costs for preparation of income statement through marginal and

absorption costs......................................................................................................................4

P4. Assets and detriment of various kinds of planning tools.................................................9

P5. Analogy among firms for adoption of management accounting system for responding to

financial................................................................................................................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

INTRODUCTION...........................................................................................................................1

P1. Define management accounting and their crucial requirements of their types................1

P2. Elaborate methods of management accounting reporting................................................3

P3. Computation of costs for preparation of income statement through marginal and

absorption costs......................................................................................................................4

P4. Assets and detriment of various kinds of planning tools.................................................9

P5. Analogy among firms for adoption of management accounting system for responding to

financial................................................................................................................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

INTRODUCTION

Financial reporting, also known as corporate finance, relates to the procedure of providing

economic data and knowledge to supervisors in order for them to make judgements (Alsharari,

2016). Managerial bookkeeping intends to use numerical information to make effective and

precise decisions, as well as to handle venture, advancement, and financial dealings. Essentially,

this involves the utilization of capabilities and advanced abilities for the creation of accountancy

and finance-related data. Furthermore, it helps the organisation in the formulation of budgeting,

monitoring of activities, and making plans for them appropriately. Berkeley Associates was

established in 1990 to help people comprehend the notion of strategic management. Companies

provide varied services to its customer companies in the shape of autonomous middle managers.

Essentra Packing, a production company that specialises in tearing tape, is among its clients.

This chapter is on budgetary control, including the many kinds and techniques of report. In

particular, various prices were computed, and the benefits and drawbacks of various business

plans are being presented. Moreover, a correlation of management accountancy to economic

concerns has also been demonstrated.

P1. Define management accounting and their crucial requirements of their types

Managerial accountancy relates to the procedure of preparing statements and projections

that provide administrators with accurate, comprehensive analytical and economic data required

to make short-term choices on day-to-day operations. It might help Essentra Packing develop

strategies and objectives based on the actions company must conduct through. This should help

companies with productivity monitoring by generating hypotheses for strategy, planning,

forecasts, and other tasks. In broadly, it consists of providing accounting-related statistics.

Administrative accountancy provides a broad variety of resources which may be used by

Essentra package to achieve its objectives in an effective way.

Administrative accountancy tools are internally platforms used among organisations to

evaluate and quantify productivity. Essentra Packaging could utilize such methods to create rules

for every division based on its achievement in order to achieve good outcomes. This will provide

managers with accurate data, allowing them to make educated choices. Therefore, Essentra

Packing must employ this instrument because it works with both financial and non-financial

information which could aid companies in conducting out their company activities.

Financial reporting, also known as corporate finance, relates to the procedure of providing

economic data and knowledge to supervisors in order for them to make judgements (Alsharari,

2016). Managerial bookkeeping intends to use numerical information to make effective and

precise decisions, as well as to handle venture, advancement, and financial dealings. Essentially,

this involves the utilization of capabilities and advanced abilities for the creation of accountancy

and finance-related data. Furthermore, it helps the organisation in the formulation of budgeting,

monitoring of activities, and making plans for them appropriately. Berkeley Associates was

established in 1990 to help people comprehend the notion of strategic management. Companies

provide varied services to its customer companies in the shape of autonomous middle managers.

Essentra Packing, a production company that specialises in tearing tape, is among its clients.

This chapter is on budgetary control, including the many kinds and techniques of report. In

particular, various prices were computed, and the benefits and drawbacks of various business

plans are being presented. Moreover, a correlation of management accountancy to economic

concerns has also been demonstrated.

P1. Define management accounting and their crucial requirements of their types

Managerial accountancy relates to the procedure of preparing statements and projections

that provide administrators with accurate, comprehensive analytical and economic data required

to make short-term choices on day-to-day operations. It might help Essentra Packing develop

strategies and objectives based on the actions company must conduct through. This should help

companies with productivity monitoring by generating hypotheses for strategy, planning,

forecasts, and other tasks. In broadly, it consists of providing accounting-related statistics.

Administrative accountancy provides a broad variety of resources which may be used by

Essentra package to achieve its objectives in an effective way.

Administrative accountancy tools are internally platforms used among organisations to

evaluate and quantify productivity. Essentra Packaging could utilize such methods to create rules

for every division based on its achievement in order to achieve good outcomes. This will provide

managers with accurate data, allowing them to make educated choices. Therefore, Essentra

Packing must employ this instrument because it works with both financial and non-financial

information which could aid companies in conducting out their company activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

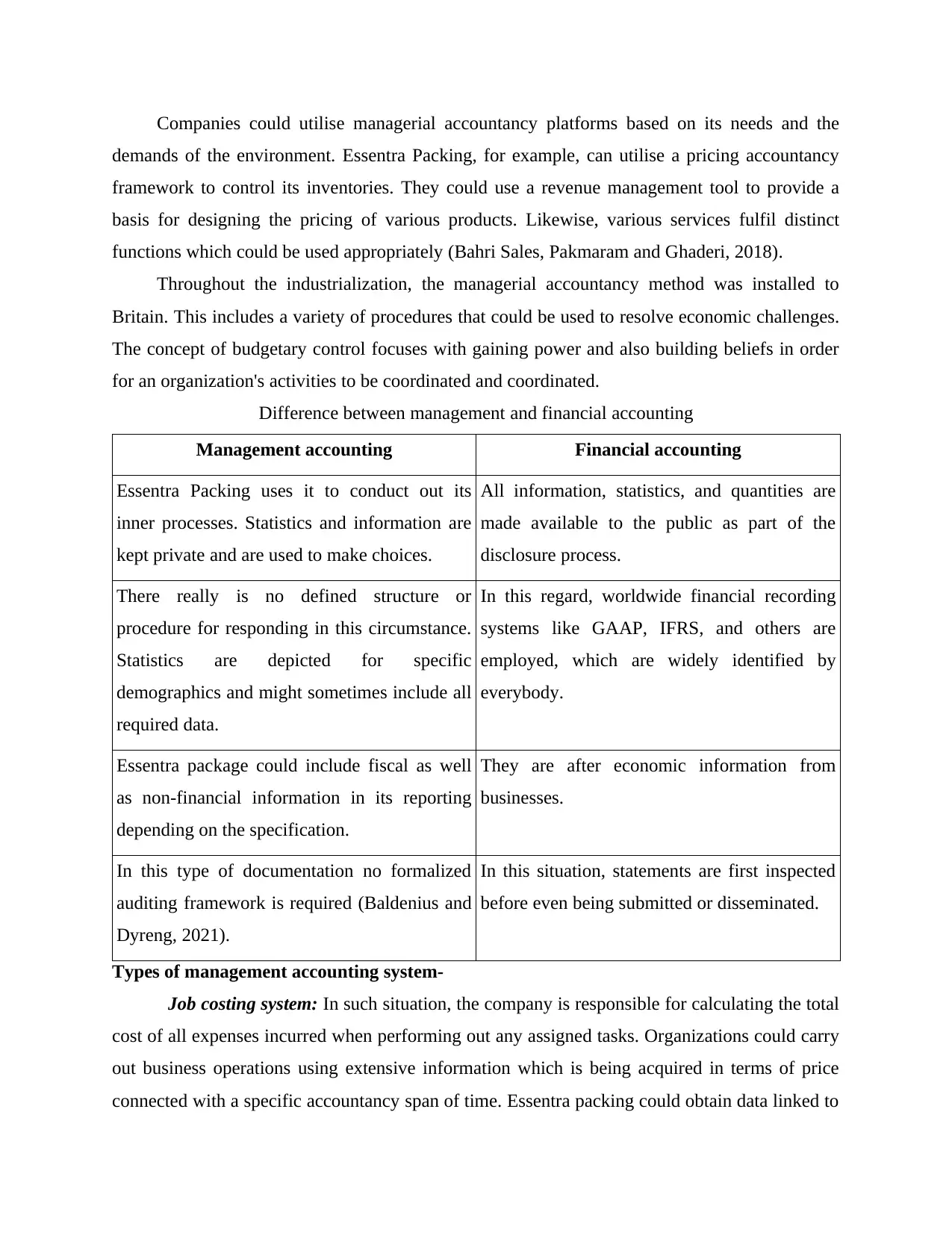

Companies could utilise managerial accountancy platforms based on its needs and the

demands of the environment. Essentra Packing, for example, can utilise a pricing accountancy

framework to control its inventories. They could use a revenue management tool to provide a

basis for designing the pricing of various products. Likewise, various services fulfil distinct

functions which could be used appropriately (Bahri Sales, Pakmaram and Ghaderi, 2018).

Throughout the industrialization, the managerial accountancy method was installed to

Britain. This includes a variety of procedures that could be used to resolve economic challenges.

The concept of budgetary control focuses with gaining power and also building beliefs in order

for an organization's activities to be coordinated and coordinated.

Difference between management and financial accounting

Management accounting Financial accounting

Essentra Packing uses it to conduct out its

inner processes. Statistics and information are

kept private and are used to make choices.

All information, statistics, and quantities are

made available to the public as part of the

disclosure process.

There really is no defined structure or

procedure for responding in this circumstance.

Statistics are depicted for specific

demographics and might sometimes include all

required data.

In this regard, worldwide financial recording

systems like GAAP, IFRS, and others are

employed, which are widely identified by

everybody.

Essentra package could include fiscal as well

as non-financial information in its reporting

depending on the specification.

They are after economic information from

businesses.

In this type of documentation no formalized

auditing framework is required (Baldenius and

Dyreng, 2021).

In this situation, statements are first inspected

before even being submitted or disseminated.

Types of management accounting system-

Job costing system: In such situation, the company is responsible for calculating the total

cost of all expenses incurred when performing out any assigned tasks. Organizations could carry

out business operations using extensive information which is being acquired in terms of price

connected with a specific accountancy span of time. Essentra packing could obtain data linked to

demands of the environment. Essentra Packing, for example, can utilise a pricing accountancy

framework to control its inventories. They could use a revenue management tool to provide a

basis for designing the pricing of various products. Likewise, various services fulfil distinct

functions which could be used appropriately (Bahri Sales, Pakmaram and Ghaderi, 2018).

Throughout the industrialization, the managerial accountancy method was installed to

Britain. This includes a variety of procedures that could be used to resolve economic challenges.

The concept of budgetary control focuses with gaining power and also building beliefs in order

for an organization's activities to be coordinated and coordinated.

Difference between management and financial accounting

Management accounting Financial accounting

Essentra Packing uses it to conduct out its

inner processes. Statistics and information are

kept private and are used to make choices.

All information, statistics, and quantities are

made available to the public as part of the

disclosure process.

There really is no defined structure or

procedure for responding in this circumstance.

Statistics are depicted for specific

demographics and might sometimes include all

required data.

In this regard, worldwide financial recording

systems like GAAP, IFRS, and others are

employed, which are widely identified by

everybody.

Essentra package could include fiscal as well

as non-financial information in its reporting

depending on the specification.

They are after economic information from

businesses.

In this type of documentation no formalized

auditing framework is required (Baldenius and

Dyreng, 2021).

In this situation, statements are first inspected

before even being submitted or disseminated.

Types of management accounting system-

Job costing system: In such situation, the company is responsible for calculating the total

cost of all expenses incurred when performing out any assigned tasks. Organizations could carry

out business operations using extensive information which is being acquired in terms of price

connected with a specific accountancy span of time. Essentra packing could obtain data linked to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

job responsibilities in regards of price connected with each via it. This should cause the business

to calculate the total expense involved with the project so that revenues may be forecasted.

Price optimisation system: In a dynamic environment it is critical for businesses to

establish pricing for its goods or commodities in a specific structure, because it would help

companies improve total profitability. The firm must effectively understand marketplace values

and also consumer requests. This should help managers to assess consumer perceptions,

inclinations, and interests for products. This would have a positive effect on total Essentra

package revenue, resulting in increased profitability for business merchandise (Bertheussen,

2017).

Inventory management system: Inside the company, there have been 2 important

processes: producing and assembly, which control supply, inventories, and the command

characteristics. This will allow Essentra Packing to precisely verify company stock, while also

reducing waste and resulting in a higher revenue margins. Organizations can develop methods to

improve production by ensuring that assets are used in the most efficient and effective way

possible.

Cost accounting system: This refers to a methodology which organisations use to

estimate the costs connected with particular goods for sales revenue, controlling costs, and

financial accounting. It is an important factor since estimating the precise prices of inventory is

challenging for lucrative operations. Essentra packing should handle items which could result in

increased revenues, but this is only achievable if servicing costs are appropriately forecasted. It

signifies that the company would be capable to trace their stock levels in addition to different

phases of manufacturing. Firms could use it for price identification, distribution, categorization,

aggregate, and monitoring, allowing them to compare prices (Cheng, 2019).

P2. Elaborate methods of management accounting reporting

Managerial accountancy reports relates to the procedure of providing guidance to higher-

level executives for making operational choices. Essentra Packing could use these statistics to

monitor the effectiveness of its personnel. Just few statistics were addressed below-

Inventory management report: It is among the key important activities associated with

creating reporting so they'll have complete sales data. Essentra Packing must detect numerous

viewpoints such as installation costs, inventory closings, and so on. Furthermore, such papers

provide information regarding securities as well as techniques which might be used to obtain

to calculate the total expense involved with the project so that revenues may be forecasted.

Price optimisation system: In a dynamic environment it is critical for businesses to

establish pricing for its goods or commodities in a specific structure, because it would help

companies improve total profitability. The firm must effectively understand marketplace values

and also consumer requests. This should help managers to assess consumer perceptions,

inclinations, and interests for products. This would have a positive effect on total Essentra

package revenue, resulting in increased profitability for business merchandise (Bertheussen,

2017).

Inventory management system: Inside the company, there have been 2 important

processes: producing and assembly, which control supply, inventories, and the command

characteristics. This will allow Essentra Packing to precisely verify company stock, while also

reducing waste and resulting in a higher revenue margins. Organizations can develop methods to

improve production by ensuring that assets are used in the most efficient and effective way

possible.

Cost accounting system: This refers to a methodology which organisations use to

estimate the costs connected with particular goods for sales revenue, controlling costs, and

financial accounting. It is an important factor since estimating the precise prices of inventory is

challenging for lucrative operations. Essentra packing should handle items which could result in

increased revenues, but this is only achievable if servicing costs are appropriately forecasted. It

signifies that the company would be capable to trace their stock levels in addition to different

phases of manufacturing. Firms could use it for price identification, distribution, categorization,

aggregate, and monitoring, allowing them to compare prices (Cheng, 2019).

P2. Elaborate methods of management accounting reporting

Managerial accountancy reports relates to the procedure of providing guidance to higher-

level executives for making operational choices. Essentra Packing could use these statistics to

monitor the effectiveness of its personnel. Just few statistics were addressed below-

Inventory management report: It is among the key important activities associated with

creating reporting so they'll have complete sales data. Essentra Packing must detect numerous

viewpoints such as installation costs, inventory closings, and so on. Furthermore, such papers

provide information regarding securities as well as techniques which might be used to obtain

them. This seeks to strike an equilibrium between both the operations provided to consumers and

stock control.

Budget Report: Essentra Packing must provide manufacturing statistics in the upcoming

as this will help companies conduct off its activities in a systematic format. Essentially, it

provides details on benefits which are being offered to them in order to enhance employee

attitude and enable them to execute their activities more effectively. This would assist the

business in ensuring that total efficiency could be enhanced in respect of how activities are

conducted effectively (Datar and Rajan, 2018).

Performance report: Assessments are performed out to assess organizational

effectiveness. It includes thorough information about the rewards offered to staff. This could

assist Essentra Packing in inspiring staff by allowing members to evaluate total profitability and

develop methods for accelerating company development. It would also aid managers in

formulating what improvements need to be made in order to improve worker productivity.

Accounts receivable ageing report: It will produce critical information in the

framework of bills issued to consumers in relation to allowances. As a result, Essentra Packing

determines the sum to be given as well as credit notes. It is a technology that helps organisations

achieves positive results in terms of financial efficiency, collections, and past-due repayments

(Debnath, 2017).

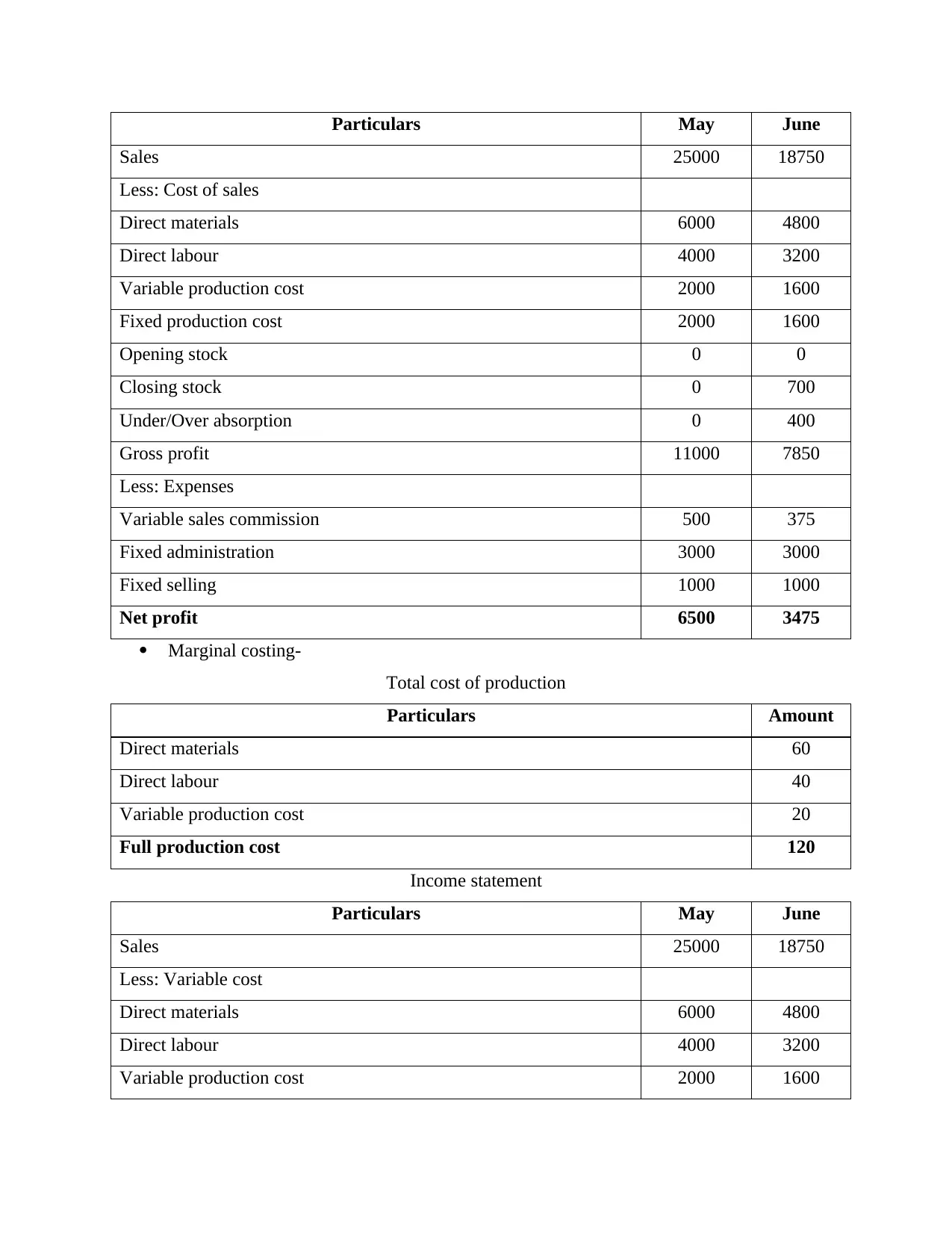

P3. Computation of costs for preparation of income statement through marginal and absorption

costs

Calculation of costs-

Absorption costing-

Total cost of production

Particulars Amount

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement

stock control.

Budget Report: Essentra Packing must provide manufacturing statistics in the upcoming

as this will help companies conduct off its activities in a systematic format. Essentially, it

provides details on benefits which are being offered to them in order to enhance employee

attitude and enable them to execute their activities more effectively. This would assist the

business in ensuring that total efficiency could be enhanced in respect of how activities are

conducted effectively (Datar and Rajan, 2018).

Performance report: Assessments are performed out to assess organizational

effectiveness. It includes thorough information about the rewards offered to staff. This could

assist Essentra Packing in inspiring staff by allowing members to evaluate total profitability and

develop methods for accelerating company development. It would also aid managers in

formulating what improvements need to be made in order to improve worker productivity.

Accounts receivable ageing report: It will produce critical information in the

framework of bills issued to consumers in relation to allowances. As a result, Essentra Packing

determines the sum to be given as well as credit notes. It is a technology that helps organisations

achieves positive results in terms of financial efficiency, collections, and past-due repayments

(Debnath, 2017).

P3. Computation of costs for preparation of income statement through marginal and absorption

costs

Calculation of costs-

Absorption costing-

Total cost of production

Particulars Amount

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing-

Total cost of production

Particulars Amount

Direct materials 60

Direct labour 40

Variable production cost 20

Full production cost 120

Income statement

Particulars May June

Sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing-

Total cost of production

Particulars Amount

Direct materials 60

Direct labour 40

Variable production cost 20

Full production cost 120

Income statement

Particulars May June

Sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Reconciliation statement

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Calculation of material variances

Particulars Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Date Description Sale/Purchases Balance

Units Cost Total Units Total

Jun-01 Opening Inventory 10 £35 £350 10 £350

Jun-09 Purchases 15 £38 £570 25 £920

Jun-15 Issued -12 £38 -£456 13 £464

Jun-20 Purchases 10 £32 £320 23 £784

Jun-23 Issued -10 £32 -£320 13 £464

Jun-27 Issued -3 £38 -£114 10 £350

Jun-30 Issued -2 £35 -£70 8 £280

Average cost methods

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Reconciliation statement

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Calculation of material variances

Particulars Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Date Description Sale/Purchases Balance

Units Cost Total Units Total

Jun-01 Opening Inventory 10 £35 £350 10 £350

Jun-09 Purchases 15 £38 £570 25 £920

Jun-15 Issued -12 £38 -£456 13 £464

Jun-20 Purchases 10 £32 £320 23 £784

Jun-23 Issued -10 £32 -£320 13 £464

Jun-27 Issued -3 £38 -£114 10 £350

Jun-30 Issued -2 £35 -£70 8 £280

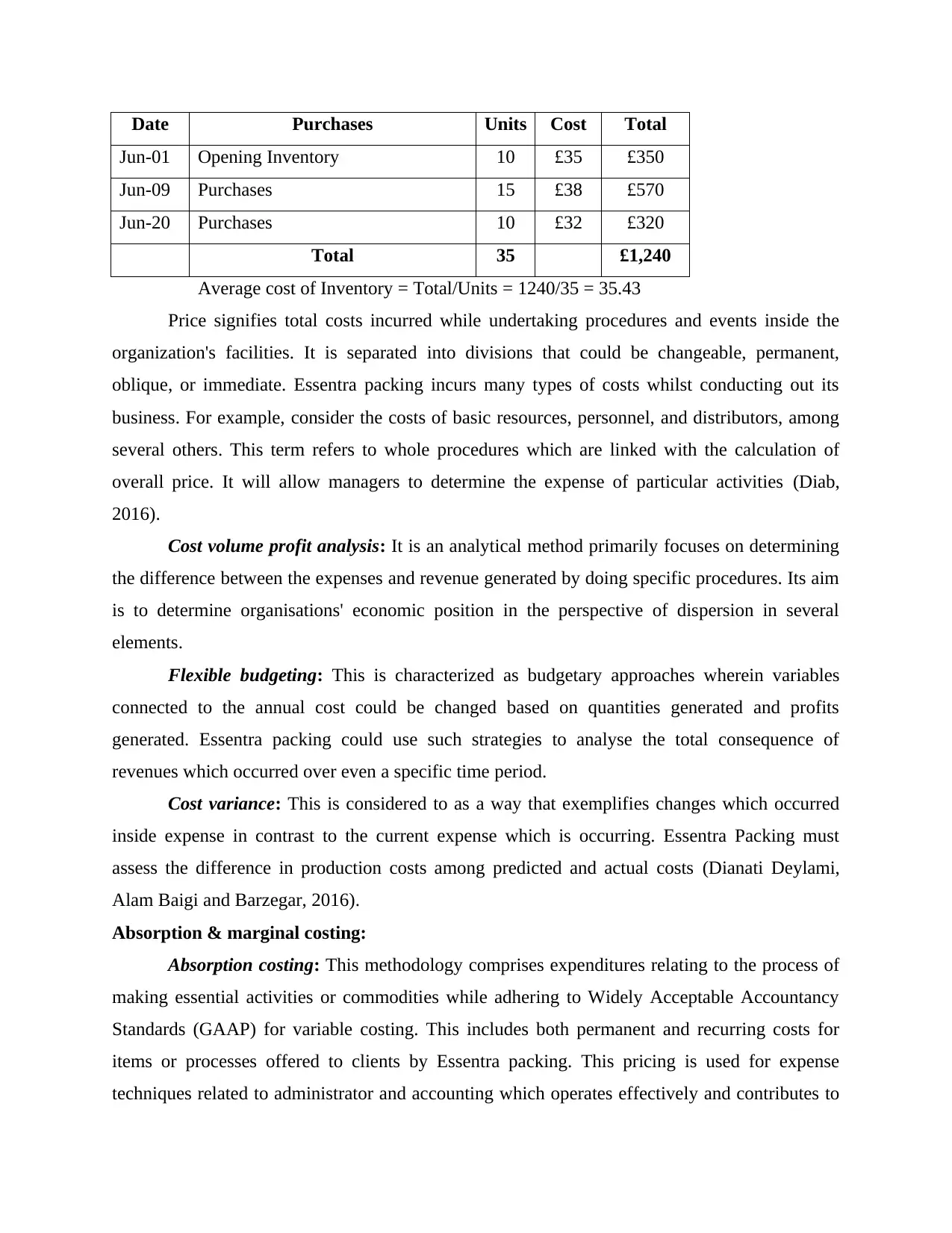

Average cost methods

Date Purchases Units Cost Total

Jun-01 Opening Inventory 10 £35 £350

Jun-09 Purchases 15 £38 £570

Jun-20 Purchases 10 £32 £320

Total 35 £1,240

Average cost of Inventory = Total/Units = 1240/35 = 35.43

Price signifies total costs incurred while undertaking procedures and events inside the

organization's facilities. It is separated into divisions that could be changeable, permanent,

oblique, or immediate. Essentra packing incurs many types of costs whilst conducting out its

business. For example, consider the costs of basic resources, personnel, and distributors, among

several others. This term refers to whole procedures which are linked with the calculation of

overall price. It will allow managers to determine the expense of particular activities (Diab,

2016).

Cost volume profit analysis: It is an analytical method primarily focuses on determining

the difference between the expenses and revenue generated by doing specific procedures. Its aim

is to determine organisations' economic position in the perspective of dispersion in several

elements.

Flexible budgeting: This is characterized as budgetary approaches wherein variables

connected to the annual cost could be changed based on quantities generated and profits

generated. Essentra packing could use such strategies to analyse the total consequence of

revenues which occurred over even a specific time period.

Cost variance: This is considered to as a way that exemplifies changes which occurred

inside expense in contrast to the current expense which is occurring. Essentra Packing must

assess the difference in production costs among predicted and actual costs (Dianati Deylami,

Alam Baigi and Barzegar, 2016).

Absorption & marginal costing:

Absorption costing: This methodology comprises expenditures relating to the process of

making essential activities or commodities while adhering to Widely Acceptable Accountancy

Standards (GAAP) for variable costing. This includes both permanent and recurring costs for

items or processes offered to clients by Essentra packing. This pricing is used for expense

techniques related to administrator and accounting which operates effectively and contributes to

Jun-01 Opening Inventory 10 £35 £350

Jun-09 Purchases 15 £38 £570

Jun-20 Purchases 10 £32 £320

Total 35 £1,240

Average cost of Inventory = Total/Units = 1240/35 = 35.43

Price signifies total costs incurred while undertaking procedures and events inside the

organization's facilities. It is separated into divisions that could be changeable, permanent,

oblique, or immediate. Essentra packing incurs many types of costs whilst conducting out its

business. For example, consider the costs of basic resources, personnel, and distributors, among

several others. This term refers to whole procedures which are linked with the calculation of

overall price. It will allow managers to determine the expense of particular activities (Diab,

2016).

Cost volume profit analysis: It is an analytical method primarily focuses on determining

the difference between the expenses and revenue generated by doing specific procedures. Its aim

is to determine organisations' economic position in the perspective of dispersion in several

elements.

Flexible budgeting: This is characterized as budgetary approaches wherein variables

connected to the annual cost could be changed based on quantities generated and profits

generated. Essentra packing could use such strategies to analyse the total consequence of

revenues which occurred over even a specific time period.

Cost variance: This is considered to as a way that exemplifies changes which occurred

inside expense in contrast to the current expense which is occurring. Essentra Packing must

assess the difference in production costs among predicted and actual costs (Dianati Deylami,

Alam Baigi and Barzegar, 2016).

Absorption & marginal costing:

Absorption costing: This methodology comprises expenditures relating to the process of

making essential activities or commodities while adhering to Widely Acceptable Accountancy

Standards (GAAP) for variable costing. This includes both permanent and recurring costs for

items or processes offered to clients by Essentra packing. This pricing is used for expense

techniques related to administrator and accounting which operates effectively and contributes to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

corporate success. Moreover, fluctuating and permanent costs, operating expenses, and

remuneration would all contribute to price increases. This would aid company leadership in

developing effective methods for dealing with circumstances that arise during the course of the

company's business activities. The attention throughout this section would be on the costs that

have been internalized, as well as technological instruments which could be considered by the

institution's administration.

Marginal costing: This signifies an increase or decrease in total manufacturing costs for

producing additional units of commodities, and it is referred to as incremental price. This depicts

the fee which is imposed every price each unit. It includes permanent and marketing costs as

well as administrative and administrative expenditure. Marginal costs would aid Essentra

package in having a representation of profitability, and its effectiveness should be carried into

consideration effectively by management. This should result in increased economic assets, which

would be identified in accountancy. The following equation could be used to calculate

incremental expense-

Cost allocation: It refers to the procedure of allocating operating costs based on the tasks

which have been completed. Essentra package, for instance, allocates spending based on several

tasks associated with the production processes (Feger and Mermet, 2017).

Fixed cost: Permanent costs are those typically will never change as a result of a drop or

rise in the quantity of activities and items delivered. In summary, it refers to the whole

expenditures or expenses involved by Essentra Packing in conducting out its activities.

Variable cost: Volatile costs are business expenditures that change in relation to the

percentage of productivity growth. It goes up or down in the environment of manufacturing

within the company's capacity, since it rises with manufacturing inventiveness and decreases if

total output decreases. In the case of Essentra, the expense of supplies as well as changeable

overhead costs would be incorporated.

Normal costing: This includes the expense of commodities in terms of commodity costs,

wage costs, and numerous additional costs which occur in a company whilst it (Essentra

packing) is providing its operations.

Standard costing: It relates to predetermined costs that are expected in the framework of

prospective possibilities for providing diverse activities. This occurs in contrast to the real

remuneration would all contribute to price increases. This would aid company leadership in

developing effective methods for dealing with circumstances that arise during the course of the

company's business activities. The attention throughout this section would be on the costs that

have been internalized, as well as technological instruments which could be considered by the

institution's administration.

Marginal costing: This signifies an increase or decrease in total manufacturing costs for

producing additional units of commodities, and it is referred to as incremental price. This depicts

the fee which is imposed every price each unit. It includes permanent and marketing costs as

well as administrative and administrative expenditure. Marginal costs would aid Essentra

package in having a representation of profitability, and its effectiveness should be carried into

consideration effectively by management. This should result in increased economic assets, which

would be identified in accountancy. The following equation could be used to calculate

incremental expense-

Cost allocation: It refers to the procedure of allocating operating costs based on the tasks

which have been completed. Essentra package, for instance, allocates spending based on several

tasks associated with the production processes (Feger and Mermet, 2017).

Fixed cost: Permanent costs are those typically will never change as a result of a drop or

rise in the quantity of activities and items delivered. In summary, it refers to the whole

expenditures or expenses involved by Essentra Packing in conducting out its activities.

Variable cost: Volatile costs are business expenditures that change in relation to the

percentage of productivity growth. It goes up or down in the environment of manufacturing

within the company's capacity, since it rises with manufacturing inventiveness and decreases if

total output decreases. In the case of Essentra, the expense of supplies as well as changeable

overhead costs would be incorporated.

Normal costing: This includes the expense of commodities in terms of commodity costs,

wage costs, and numerous additional costs which occur in a company whilst it (Essentra

packing) is providing its operations.

Standard costing: It relates to predetermined costs that are expected in the framework of

prospective possibilities for providing diverse activities. This occurs in contrast to the real

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

achievements delivered by the business. Essentra packing, for instance, uses pricing to calculate

actual expenses associated with all this (Georgantopoulos, Poutos and Eriotis, 2018).

Activity based costing: It relates to an accountancy methodology which organisations

could use to determine the price of administrative activities as well as its merchandise. These are

entirely dependent on processes and activity, and pricing programs are implemented accordingly.

Inventory cost: This includes costs associated with acquiring, shipping, storing, and a

variety of other actions that the business is required to perform. Essentra packing could detect

stock expenditures for administration of periodical expenditure which have occurred and

therefore are happening.

Valuation methods:

LIFO: This figure depicts working capital predictions and is an acronym for last in first

out. Essentra Packing could utilise this way to capture stock that really is editable in order to

keep track of things that have been originally supplied by company. As per cost of sales, the

expenses involved with the most recent things manufactured are the first to be expended

(COGS). For instance, the Essentra package production person decided to use manufactured

goods that arrived later.

FIFO: It refers for first up, first off and is related with the prices of items transferred out

as well as the assets connected with inventories. In this instance, previous charges would be

included as upfront investment. This expense would be removed from the financial accounts and

replaced with an upfront investment that would appear as the very first expense in the financial

declarations. Essentra Ltd, for instance, uses manufactured goods that have been acquired at the

beginning such that its grade does not deteriorate over period (GOVDYA and KHROMOVA,

2018).

Overhead: This indicates an expenditure related to personnel and commodity costs. They

are set for a specific pay.

P4. Assets and detriment of various kinds of planning tools

A budgeting is a monetary strategy for a set period of time. This includes evidence

amounts, price and spending, obligations, working capital, and a variety of other factors.

Furthermore, this is used to predict capital structure as well as the corporation's situation for the

following period. In effort to attain achievement the organization's management manages a

strategy based on long-term goals. Essentra package administrators create many areas of

actual expenses associated with all this (Georgantopoulos, Poutos and Eriotis, 2018).

Activity based costing: It relates to an accountancy methodology which organisations

could use to determine the price of administrative activities as well as its merchandise. These are

entirely dependent on processes and activity, and pricing programs are implemented accordingly.

Inventory cost: This includes costs associated with acquiring, shipping, storing, and a

variety of other actions that the business is required to perform. Essentra packing could detect

stock expenditures for administration of periodical expenditure which have occurred and

therefore are happening.

Valuation methods:

LIFO: This figure depicts working capital predictions and is an acronym for last in first

out. Essentra Packing could utilise this way to capture stock that really is editable in order to

keep track of things that have been originally supplied by company. As per cost of sales, the

expenses involved with the most recent things manufactured are the first to be expended

(COGS). For instance, the Essentra package production person decided to use manufactured

goods that arrived later.

FIFO: It refers for first up, first off and is related with the prices of items transferred out

as well as the assets connected with inventories. In this instance, previous charges would be

included as upfront investment. This expense would be removed from the financial accounts and

replaced with an upfront investment that would appear as the very first expense in the financial

declarations. Essentra Ltd, for instance, uses manufactured goods that have been acquired at the

beginning such that its grade does not deteriorate over period (GOVDYA and KHROMOVA,

2018).

Overhead: This indicates an expenditure related to personnel and commodity costs. They

are set for a specific pay.

P4. Assets and detriment of various kinds of planning tools

A budgeting is a monetary strategy for a set period of time. This includes evidence

amounts, price and spending, obligations, working capital, and a variety of other factors.

Furthermore, this is used to predict capital structure as well as the corporation's situation for the

following period. In effort to attain achievement the organization's management manages a

strategy based on long-term goals. Essentra package administrators create many areas of

operation to determine whether or not large segments are employing monetary supplies

effectively and economically. It focuses on financial management to prevent excessive spending

of finances. This is defined as the processes for establishing economic and operational goals for a

specific time period in order to achieve development and prosperity (Gusc and van Veen-Dirks,

2017).

To prepare budgeting, the management of Essentra package explains goals and gathers

necessary knowledge in regards to the company's demands. The collected data is then reviewed

via these to determine its validity. Following research, it prepares expenditures and presents

them to high management teams for authorization. So, after it is authorised, executives will put it

into action on behalf of the organisation. Several stages are followed at the management team to

efficiently prepare the budgets.

Zero based budgeting: This really is the strategy which is created from the ground up.

This aids firm executives in justifying all expenditures incurred while carrying out the entity's

operations. In Essentra packing, this one is generated by leadership to analyse the needs and the

price of all actions conducted by companies. As a result, the following benefits and drawbacks

are debated-

Advantages:

With the use of technology, managers may explain the total expenditures which occur

whilst conducting costs incurred in addition to forecast future spending and earnings. This helps to identify operations which are not profitable in order to reduce the likelihood

of damages.

Disadvantages:

It is a tough instrument for budgeting process because it ignores entire prior annual

activities (Holm and Ax, 2020).

Additional time is required to prepare this budgeting, and it is not feasible for entire

enterprises to commit additional effort in this processes.

Operating budget: This relates to an action's yearly budgeting which is stated in terms of

spending plan identify exactly, pay rise, and development teams. This involves estimating the

total amount of capital required for operational execution that comprises refundable tasks or

activities for someone else. This plan could be prepared by the management of Essentra Packing

for capturing non-financial expenditures. Another of them would be amortization, which is a

effectively and economically. It focuses on financial management to prevent excessive spending

of finances. This is defined as the processes for establishing economic and operational goals for a

specific time period in order to achieve development and prosperity (Gusc and van Veen-Dirks,

2017).

To prepare budgeting, the management of Essentra package explains goals and gathers

necessary knowledge in regards to the company's demands. The collected data is then reviewed

via these to determine its validity. Following research, it prepares expenditures and presents

them to high management teams for authorization. So, after it is authorised, executives will put it

into action on behalf of the organisation. Several stages are followed at the management team to

efficiently prepare the budgets.

Zero based budgeting: This really is the strategy which is created from the ground up.

This aids firm executives in justifying all expenditures incurred while carrying out the entity's

operations. In Essentra packing, this one is generated by leadership to analyse the needs and the

price of all actions conducted by companies. As a result, the following benefits and drawbacks

are debated-

Advantages:

With the use of technology, managers may explain the total expenditures which occur

whilst conducting costs incurred in addition to forecast future spending and earnings. This helps to identify operations which are not profitable in order to reduce the likelihood

of damages.

Disadvantages:

It is a tough instrument for budgeting process because it ignores entire prior annual

activities (Holm and Ax, 2020).

Additional time is required to prepare this budgeting, and it is not feasible for entire

enterprises to commit additional effort in this processes.

Operating budget: This relates to an action's yearly budgeting which is stated in terms of

spending plan identify exactly, pay rise, and development teams. This involves estimating the

total amount of capital required for operational execution that comprises refundable tasks or

activities for someone else. This plan could be prepared by the management of Essentra Packing

for capturing non-financial expenditures. Another of them would be amortization, which is a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.