Analyzing Costs & Revenue Metrics in Financial Resource Management

VerifiedAdded on 2023/06/15

|11

|2462

|205

Report

AI Summary

This report provides a detailed analysis of managing financial resources, focusing on cost components and revenue metrics. It differentiates between fixed and variable costs, illustrating their impact on an organization's financial performance. The report includes calculations for average daily rate (ADR), revenue per available room (RevPAR), average length of stay, and average rate index. Furthermore, it examines key performance indicators such as food and beverage cost of sales ratios, revenue per seat hour, labor costs, and customer retention rates. The analysis demonstrates how these metrics are crucial for effective financial management and decision-making within hospitality and other sectors, highlighting the importance of understanding cost structures and revenue generation strategies to achieve financial goals. Desklib provides access to this and many other solved assignments.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

INTRODUCTION...........................................................................................................................3

Section A.........................................................................................................................................3

Question 2....................................................................................................................................3

Section B.........................................................................................................................................5

Question 5....................................................................................................................................5

Question 6....................................................................................................................................8

CONCLUSION.............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

INTRODUCTION...........................................................................................................................3

Section A.........................................................................................................................................3

Question 2....................................................................................................................................3

Section B.........................................................................................................................................5

Question 5....................................................................................................................................5

Question 6....................................................................................................................................8

CONCLUSION.............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

In this project description about the fixed and variable component will be given.

Furthermore, the project will discuss the various types of cost incurred by the organisation.

Section A

Question 2

(a)

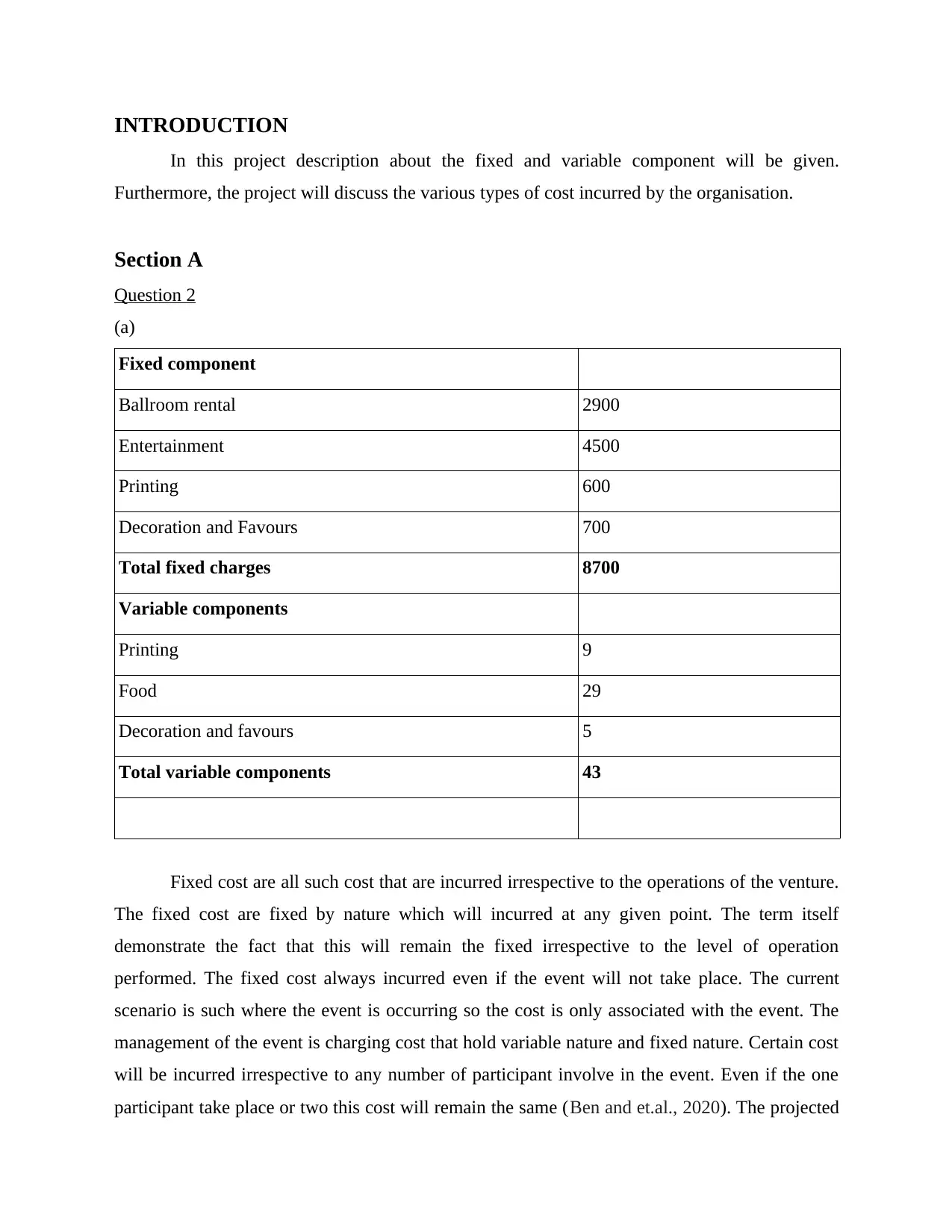

Fixed component

Ballroom rental 2900

Entertainment 4500

Printing 600

Decoration and Favours 700

Total fixed charges 8700

Variable components

Printing 9

Food 29

Decoration and favours 5

Total variable components 43

Fixed cost are all such cost that are incurred irrespective to the operations of the venture.

The fixed cost are fixed by nature which will incurred at any given point. The term itself

demonstrate the fact that this will remain the fixed irrespective to the level of operation

performed. The fixed cost always incurred even if the event will not take place. The current

scenario is such where the event is occurring so the cost is only associated with the event. The

management of the event is charging cost that hold variable nature and fixed nature. Certain cost

will be incurred irrespective to any number of participant involve in the event. Even if the one

participant take place or two this cost will remain the same (Ben and et.al., 2020). The projected

In this project description about the fixed and variable component will be given.

Furthermore, the project will discuss the various types of cost incurred by the organisation.

Section A

Question 2

(a)

Fixed component

Ballroom rental 2900

Entertainment 4500

Printing 600

Decoration and Favours 700

Total fixed charges 8700

Variable components

Printing 9

Food 29

Decoration and favours 5

Total variable components 43

Fixed cost are all such cost that are incurred irrespective to the operations of the venture.

The fixed cost are fixed by nature which will incurred at any given point. The term itself

demonstrate the fact that this will remain the fixed irrespective to the level of operation

performed. The fixed cost always incurred even if the event will not take place. The current

scenario is such where the event is occurring so the cost is only associated with the event. The

management of the event is charging cost that hold variable nature and fixed nature. Certain cost

will be incurred irrespective to any number of participant involve in the event. Even if the one

participant take place or two this cost will remain the same (Ben and et.al., 2020). The projected

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

scenario reflect that ballroom rental hold the fixed cost involve ballroom rental, entertainment,

pricing and decoration and favour related cost. All thee cost hold fixed in nature. The nature of

fixed component is such that it will incur even if any participant do not take place. On the other

hand variable cost is the one that will only take place if some activity is taken. This cost will

only incurred if the people would take participate in the event. In case the person is not being

able to participate in the event than this cost will not take any place in the event. The role of

variable cost is such that if the participants are involved in the event than this cost will take

place. The above scenario include variable cost involve printing, food, decoration and favour

related cost. This cost is variable in nature. This cost will only incurred if the participant involve

in the event activity.

The above projected scenario reflect that the total fixed cost that will be incurred

amounted as 8700 whereas the variable cost on the other hand will incurred at the rate of 43 per

person. The nature of the variable cost involve this will be based on the total numb er of

participant included in the event. If the total number of participants increases this would further

increase this cost. Fixed cost amounted of 8700 will incurred even if the participants do not get

involve in the event. In case the event take place with one participant than still this cost will take

place abnd management have to bear the same (Eriksson and et.al., 2019). The basic different

between fixed cost and variable cost is such that the fixed cost will incurred in the same manner

even if any number of participant take part in thee event this cost will remain the same for the

management. There will be no change address in the scale of this cost even if one participant

involve and even the 100 participant take place this cost will remain the same for the

management. On the other hand variable cost contain the nature or the fact that this cost will be

based on the total number of participant involve in the event.

There are certain cost which is semi variable in nature. This is a cost that is partially

variable by nature and partially fixed by nature., This cost is also included and incurred by the

organisation. These cost included printing cost, decorations and favour related cost. These cost

are semi variable cost that will hold the nature of both the type of costs such as variable cost and

fixed cost.

(b)

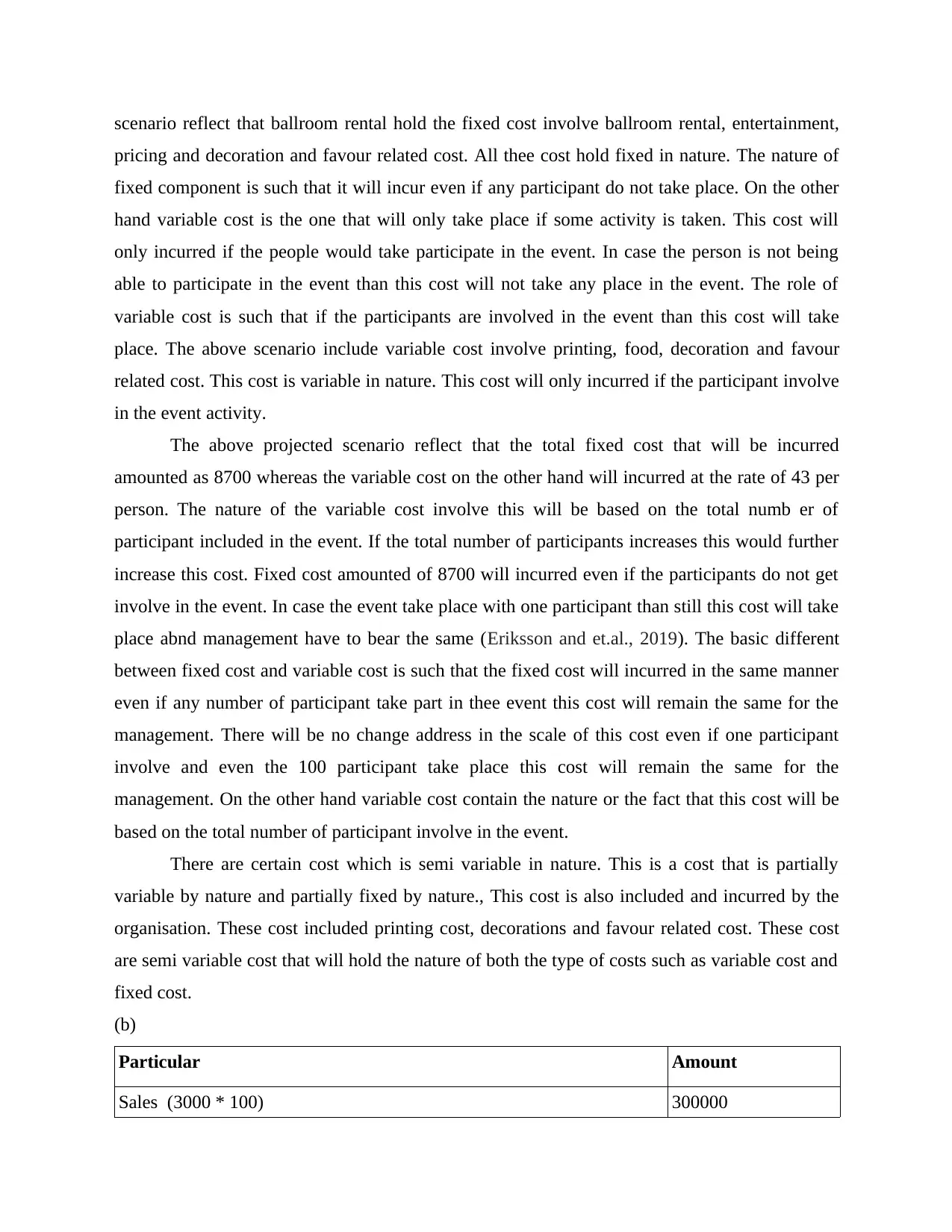

Particular Amount

Sales (3000 * 100) 300000

pricing and decoration and favour related cost. All thee cost hold fixed in nature. The nature of

fixed component is such that it will incur even if any participant do not take place. On the other

hand variable cost is the one that will only take place if some activity is taken. This cost will

only incurred if the people would take participate in the event. In case the person is not being

able to participate in the event than this cost will not take any place in the event. The role of

variable cost is such that if the participants are involved in the event than this cost will take

place. The above scenario include variable cost involve printing, food, decoration and favour

related cost. This cost is variable in nature. This cost will only incurred if the participant involve

in the event activity.

The above projected scenario reflect that the total fixed cost that will be incurred

amounted as 8700 whereas the variable cost on the other hand will incurred at the rate of 43 per

person. The nature of the variable cost involve this will be based on the total numb er of

participant included in the event. If the total number of participants increases this would further

increase this cost. Fixed cost amounted of 8700 will incurred even if the participants do not get

involve in the event. In case the event take place with one participant than still this cost will take

place abnd management have to bear the same (Eriksson and et.al., 2019). The basic different

between fixed cost and variable cost is such that the fixed cost will incurred in the same manner

even if any number of participant take part in thee event this cost will remain the same for the

management. There will be no change address in the scale of this cost even if one participant

involve and even the 100 participant take place this cost will remain the same for the

management. On the other hand variable cost contain the nature or the fact that this cost will be

based on the total number of participant involve in the event.

There are certain cost which is semi variable in nature. This is a cost that is partially

variable by nature and partially fixed by nature., This cost is also included and incurred by the

organisation. These cost included printing cost, decorations and favour related cost. These cost

are semi variable cost that will hold the nature of both the type of costs such as variable cost and

fixed cost.

(b)

Particular Amount

Sales (3000 * 100) 300000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

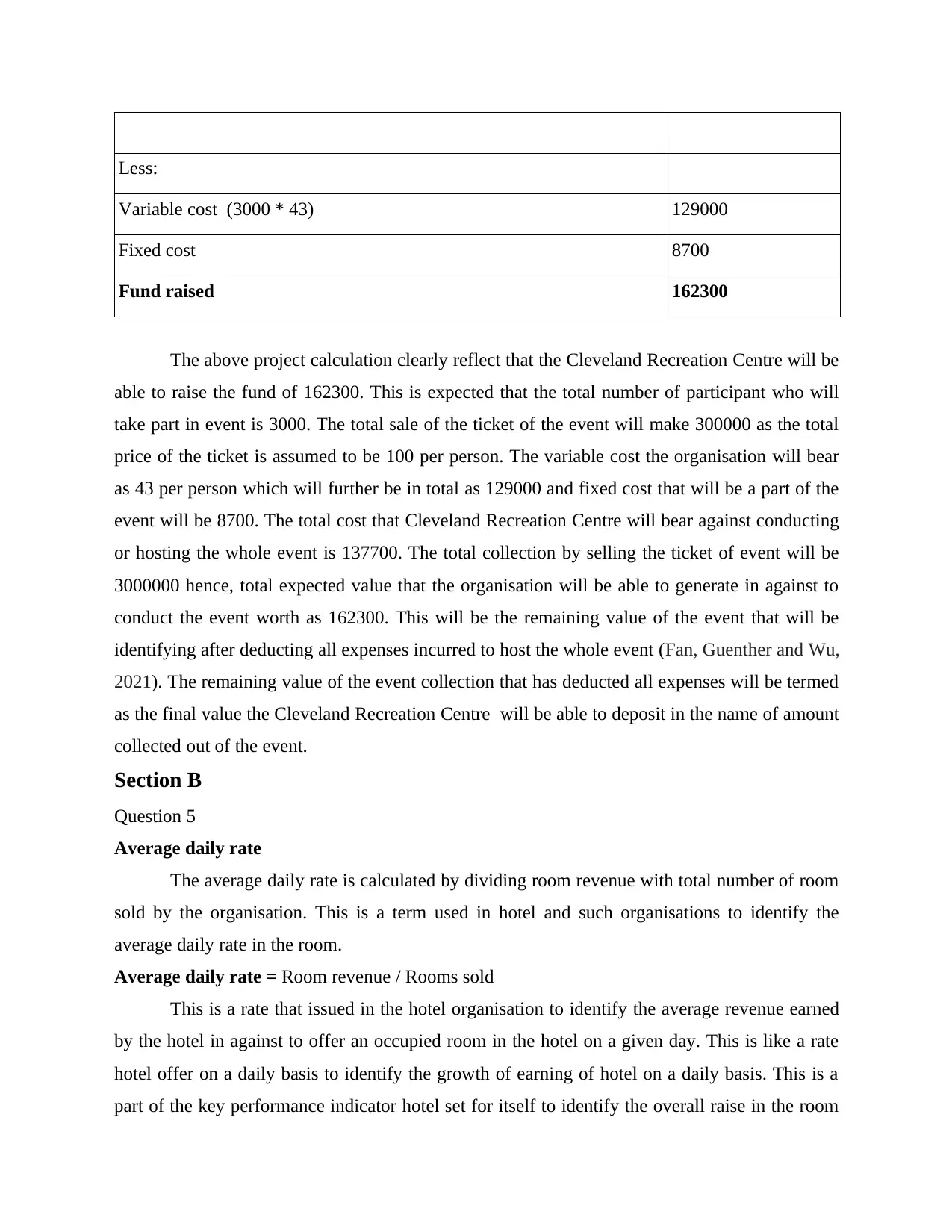

Less:

Variable cost (3000 * 43) 129000

Fixed cost 8700

Fund raised 162300

The above project calculation clearly reflect that the Cleveland Recreation Centre will be

able to raise the fund of 162300. This is expected that the total number of participant who will

take part in event is 3000. The total sale of the ticket of the event will make 300000 as the total

price of the ticket is assumed to be 100 per person. The variable cost the organisation will bear

as 43 per person which will further be in total as 129000 and fixed cost that will be a part of the

event will be 8700. The total cost that Cleveland Recreation Centre will bear against conducting

or hosting the whole event is 137700. The total collection by selling the ticket of event will be

3000000 hence, total expected value that the organisation will be able to generate in against to

conduct the event worth as 162300. This will be the remaining value of the event that will be

identifying after deducting all expenses incurred to host the whole event (Fan, Guenther and Wu,

2021). The remaining value of the event collection that has deducted all expenses will be termed

as the final value the Cleveland Recreation Centre will be able to deposit in the name of amount

collected out of the event.

Section B

Question 5

Average daily rate

The average daily rate is calculated by dividing room revenue with total number of room

sold by the organisation. This is a term used in hotel and such organisations to identify the

average daily rate in the room.

Average daily rate = Room revenue / Rooms sold

This is a rate that issued in the hotel organisation to identify the average revenue earned

by the hotel in against to offer an occupied room in the hotel on a given day. This is like a rate

hotel offer on a daily basis to identify the growth of earning of hotel on a daily basis. This is a

part of the key performance indicator hotel set for itself to identify the overall raise in the room

Variable cost (3000 * 43) 129000

Fixed cost 8700

Fund raised 162300

The above project calculation clearly reflect that the Cleveland Recreation Centre will be

able to raise the fund of 162300. This is expected that the total number of participant who will

take part in event is 3000. The total sale of the ticket of the event will make 300000 as the total

price of the ticket is assumed to be 100 per person. The variable cost the organisation will bear

as 43 per person which will further be in total as 129000 and fixed cost that will be a part of the

event will be 8700. The total cost that Cleveland Recreation Centre will bear against conducting

or hosting the whole event is 137700. The total collection by selling the ticket of event will be

3000000 hence, total expected value that the organisation will be able to generate in against to

conduct the event worth as 162300. This will be the remaining value of the event that will be

identifying after deducting all expenses incurred to host the whole event (Fan, Guenther and Wu,

2021). The remaining value of the event collection that has deducted all expenses will be termed

as the final value the Cleveland Recreation Centre will be able to deposit in the name of amount

collected out of the event.

Section B

Question 5

Average daily rate

The average daily rate is calculated by dividing room revenue with total number of room

sold by the organisation. This is a term used in hotel and such organisations to identify the

average daily rate in the room.

Average daily rate = Room revenue / Rooms sold

This is a rate that issued in the hotel organisation to identify the average revenue earned

by the hotel in against to offer an occupied room in the hotel on a given day. This is like a rate

hotel offer on a daily basis to identify the growth of earning of hotel on a daily basis. This is a

part of the key performance indicator hotel set for itself to identify the overall raise in the room

earning of the hotel (Ngin, Chhom and Neef, 2020). This entire concept measure the available

rental revenue hotel incur against offering the rooms to the customer visited the hotel. The rise in

the average daily rate demonstrate the facty that the hotel is increasing its revenue in the

business.

Example:

Room revenue: 60000

Room sold = 600

Average daily rate = 60000 / 600

= 100

Revenue per available room

Revenue per available room is a metric that is used in the hospitality organisations to

identify and measure the overall performance of the hotel chain. The rate is a comparison

between room revenue in hotel and total available room with the hotel.

Revenue per available room= average daily room rate / occupancy rate

This is a performance matrix that compare the average daily room rate and the occupancy

rate available with the hotel. This is one of the major key performance indicator which hotel is

using in order to monitor and assess the overall performance of the organisation. The increase in

the revenue per available room indicate the fact that average room rate offer by the hotel; along

with the occupancy rate both are improving for the hospitality organisation. The increased rate is

a good indicator for the performance of the venture (Pornprakun and et.al., 2018). Revenue per

available room reflect the ability of the property to fill its room availability or capacity. The

another key fact associated with this is that increased revenue per available room does not

necessarily mean that the gross profit of the organisation or hotel has improved. The gross profit

further involve many factors that needed to consider while identifying the respective term.

Examples:

Average income per night= 1000

Occupancy rate= 10 rooms

Revenue per available room= 1000 / 10

= 100

Average length of stay

rental revenue hotel incur against offering the rooms to the customer visited the hotel. The rise in

the average daily rate demonstrate the facty that the hotel is increasing its revenue in the

business.

Example:

Room revenue: 60000

Room sold = 600

Average daily rate = 60000 / 600

= 100

Revenue per available room

Revenue per available room is a metric that is used in the hospitality organisations to

identify and measure the overall performance of the hotel chain. The rate is a comparison

between room revenue in hotel and total available room with the hotel.

Revenue per available room= average daily room rate / occupancy rate

This is a performance matrix that compare the average daily room rate and the occupancy

rate available with the hotel. This is one of the major key performance indicator which hotel is

using in order to monitor and assess the overall performance of the organisation. The increase in

the revenue per available room indicate the fact that average room rate offer by the hotel; along

with the occupancy rate both are improving for the hospitality organisation. The increased rate is

a good indicator for the performance of the venture (Pornprakun and et.al., 2018). Revenue per

available room reflect the ability of the property to fill its room availability or capacity. The

another key fact associated with this is that increased revenue per available room does not

necessarily mean that the gross profit of the organisation or hotel has improved. The gross profit

further involve many factors that needed to consider while identifying the respective term.

Examples:

Average income per night= 1000

Occupancy rate= 10 rooms

Revenue per available room= 1000 / 10

= 100

Average length of stay

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Average length of stay is defined as on an average basis how long the visitor stay in the

hotel. This is like disclosing a fact that on average basis how long or duration the travellers or

the visitors in the hotel stay. The more the average length of stay is will further improve the

revenue of the hotel.

Average length of stay: total length of stay of each customer/ number of discharge customer in

month

This rate disclose the fact that the total length or duration a customer or travellers stay in

hotel room. Length of stay is always a key aspect hospitality organisation consider while

remaining policies on how to improve the revenue of the hotel (Tresidder and Martin, 2018).

This concept solely contribute for the hotel in improving the overall revenue of the hospitality

chain. This considers as one of the wide key performance indicator for the organisation.

Example:

Total length of stay of each customer=

Victor = 3 days

Jhonson = 4 days

Maria = 5 days

John = 3 days

Mani = 7 days

Moria = 3 days

Total discharge = 6

Average length of stay = 3 + 4 + 5 + 3 + 7 + 3 / 6

= 4.16 days

This disclose the fact that on an average 4.16 days each customer visited the hotel stay in

the hotel.

Average rate index

Average rate index is a comparison between the average daily rate of the organisation by

comparing it with the industry average of average daily rate.

Formula= ADR / Industry average ADR

hotel. This is like disclosing a fact that on average basis how long or duration the travellers or

the visitors in the hotel stay. The more the average length of stay is will further improve the

revenue of the hotel.

Average length of stay: total length of stay of each customer/ number of discharge customer in

month

This rate disclose the fact that the total length or duration a customer or travellers stay in

hotel room. Length of stay is always a key aspect hospitality organisation consider while

remaining policies on how to improve the revenue of the hotel (Tresidder and Martin, 2018).

This concept solely contribute for the hotel in improving the overall revenue of the hospitality

chain. This considers as one of the wide key performance indicator for the organisation.

Example:

Total length of stay of each customer=

Victor = 3 days

Jhonson = 4 days

Maria = 5 days

John = 3 days

Mani = 7 days

Moria = 3 days

Total discharge = 6

Average length of stay = 3 + 4 + 5 + 3 + 7 + 3 / 6

= 4.16 days

This disclose the fact that on an average 4.16 days each customer visited the hotel stay in

the hotel.

Average rate index

Average rate index is a comparison between the average daily rate of the organisation by

comparing it with the industry average of average daily rate.

Formula= ADR / Industry average ADR

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is a comparison of the average daily rate of the respective entity by comparing it

with the industry average rate.

Example:

ADR = 100

Industry average ADR = 120

Average rate index = 100 / 120

= .83

Customer satisfaction

Customer satisfaction is a concept disclose the level of customer satisfaction company

hold.

Formula = Total number of satisfied customer / total number of responses

Examples:

Total number of satisfied customer = 12

Total responses = 30

Customer satisfaction = 12 / 30

= .4

Question 6

Food cost of sales ratio

This is a ratio of the food cost restaurant incurred against the sales made by the

organisation (Vij, 2019). This is a total cost that organisation bear against selling food or making

the food in against to the total revenue company generate against making the respective sales.

Formula= cost of food / sales price * 100

Example:

Food cost = 5

Sales price = 10

Food cost of sales ratio = 5 / 10 * 100

= 50%

Beverage cost of sales ratio

with the industry average rate.

Example:

ADR = 100

Industry average ADR = 120

Average rate index = 100 / 120

= .83

Customer satisfaction

Customer satisfaction is a concept disclose the level of customer satisfaction company

hold.

Formula = Total number of satisfied customer / total number of responses

Examples:

Total number of satisfied customer = 12

Total responses = 30

Customer satisfaction = 12 / 30

= .4

Question 6

Food cost of sales ratio

This is a ratio of the food cost restaurant incurred against the sales made by the

organisation (Vij, 2019). This is a total cost that organisation bear against selling food or making

the food in against to the total revenue company generate against making the respective sales.

Formula= cost of food / sales price * 100

Example:

Food cost = 5

Sales price = 10

Food cost of sales ratio = 5 / 10 * 100

= 50%

Beverage cost of sales ratio

The beverage cost of sales ratio demonstrate the comparison between the total cost

company incurred against selling beverages in against to the total sales price charge for such

beverage.

Formula = cost of beverage / sales value

Example:

Cost of beverage = 70

Sales = 100

= 70 / 100 * 100

= 70%

Revenue per seat hour

This is the revenue hospitality or restaurant chain make against the total number of hours

customers stay on the seat. This is a difference between the total revenue restaurant is making

and the total number of hours customers were there on the seat of the restaurant.

Formula= Total revenue / total number seat hours

Example:

Total revenue = 30000

Total seat hours = 3000

= 30000 / 3000

= 10

Labour cost

Labour cost is a hourly cost of appointing a qualified person over the job role. This

involve salary plus taxes plus benefits. All this included in the labour cost.

Formula= Hourly salary + taxes + benefits

Example:

Hourly salary = 1000

Taxes = 100

Benefits = 500

Labour cost = 1000 + 100 + 500

= 1600

Customer retention rate

company incurred against selling beverages in against to the total sales price charge for such

beverage.

Formula = cost of beverage / sales value

Example:

Cost of beverage = 70

Sales = 100

= 70 / 100 * 100

= 70%

Revenue per seat hour

This is the revenue hospitality or restaurant chain make against the total number of hours

customers stay on the seat. This is a difference between the total revenue restaurant is making

and the total number of hours customers were there on the seat of the restaurant.

Formula= Total revenue / total number seat hours

Example:

Total revenue = 30000

Total seat hours = 3000

= 30000 / 3000

= 10

Labour cost

Labour cost is a hourly cost of appointing a qualified person over the job role. This

involve salary plus taxes plus benefits. All this included in the labour cost.

Formula= Hourly salary + taxes + benefits

Example:

Hourly salary = 1000

Taxes = 100

Benefits = 500

Labour cost = 1000 + 100 + 500

= 1600

Customer retention rate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Customer retention rate demonstrate about how the restaurant is able to retained its

customers.

Formula = CE – CN / CS * 100

Formula=

CE = 3000

CN = 1000

CS = 5000

= 3000 – 1000 / 5000 * 100

= 40%

CONCLUSION

The fixed cost remain fixed irrespective to the scale of operation whereas, variable cost

keep on changing based on the scale of operations. The cost accounting measure various cost

that involve retention rate, labour cost and many other in order to monitor the performance of the

organisation.

customers.

Formula = CE – CN / CS * 100

Formula=

CE = 3000

CN = 1000

CS = 5000

= 3000 – 1000 / 5000 * 100

= 40%

CONCLUSION

The fixed cost remain fixed irrespective to the scale of operation whereas, variable cost

keep on changing based on the scale of operations. The cost accounting measure various cost

that involve retention rate, labour cost and many other in order to monitor the performance of the

organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journal

Ben, L. H. B. and et.al., 2020. FIXED CONVENTIONAL SPRINKLER IRRIGATION

SYSTEM: COMPONENTS OF COST AND ECONOMY OF SCALE. Revista

Engenharia na Agricultura-Reveng. 28. pp.235-244.

Eriksson, M. and et.al., 2019. What gets measured gets managed–Or does it? Connection

between food waste quantification and food waste reduction in the hospitality

sector. Resources, Conservation & Recycling: X, 4. p.100021.

Fan, Q., Guenther, D. A. and Wu, K., 2020. Fixed and Variable Tax Expense and the Cost of

Equity Capital. Available at SSRN 3575256.

Ngin, C., Chhom, C. and Neef, A., 2020. Climate change impacts and disaster resilience among

micro businesses in the tourism and hospitality sector: The case of Kratie,

Cambodia. Environmental research. 186. p.109557.

Pornprakun, W. and et.al., 2018, March. An Optimization Model of Sugarcane Harvesting with

Fixed and Variable Costs Approximated by Fourier and Cubic Functions.

In International MultiConference of Engineers and Computer Scientists (pp. 338-353).

Springer, Singapore.

Tresidder, R. and Martin, E., 2018. Deviant behaviour in the hospitality industry: A problem of

space and time. Hospitality & Society. 8(1). pp.3-22.

Vij, M., 2019. The emerging importance of risk management and enterprise risk management

strategies in the Indian hospitality industry: Senior managements’

perspective. Worldwide Hospitality and Tourism Themes.

Books and Journal

Ben, L. H. B. and et.al., 2020. FIXED CONVENTIONAL SPRINKLER IRRIGATION

SYSTEM: COMPONENTS OF COST AND ECONOMY OF SCALE. Revista

Engenharia na Agricultura-Reveng. 28. pp.235-244.

Eriksson, M. and et.al., 2019. What gets measured gets managed–Or does it? Connection

between food waste quantification and food waste reduction in the hospitality

sector. Resources, Conservation & Recycling: X, 4. p.100021.

Fan, Q., Guenther, D. A. and Wu, K., 2020. Fixed and Variable Tax Expense and the Cost of

Equity Capital. Available at SSRN 3575256.

Ngin, C., Chhom, C. and Neef, A., 2020. Climate change impacts and disaster resilience among

micro businesses in the tourism and hospitality sector: The case of Kratie,

Cambodia. Environmental research. 186. p.109557.

Pornprakun, W. and et.al., 2018, March. An Optimization Model of Sugarcane Harvesting with

Fixed and Variable Costs Approximated by Fourier and Cubic Functions.

In International MultiConference of Engineers and Computer Scientists (pp. 338-353).

Springer, Singapore.

Tresidder, R. and Martin, E., 2018. Deviant behaviour in the hospitality industry: A problem of

space and time. Hospitality & Society. 8(1). pp.3-22.

Vij, M., 2019. The emerging importance of risk management and enterprise risk management

strategies in the Indian hospitality industry: Senior managements’

perspective. Worldwide Hospitality and Tourism Themes.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.