Cost Accounting Chapter 2: Cost Classifications and Analysis

VerifiedAdded on 2022/09/02

|30

|7186

|23

Homework Assignment

AI Summary

This assignment delves into the core concepts of cost accounting, as outlined in Chapter 2. It begins by defining a cost object and differentiating between direct and indirect costs. The document then explores various cost classifications, including manufacturing and non-manufacturing costs, with detailed explanations of direct materials, direct labor, and manufacturing overhead. It further distinguishes between product and period costs, emphasizing the matching principle. The assignment also covers cost behavior, analyzing variable, fixed, and mixed costs, and their implications. Finally, it examines cost classifications for decision-making, including differential, opportunity, and sunk costs. The content provides a comprehensive guide to understanding cost accounting principles and their practical applications. This assignment is a comprehensive guide for students to understand the cost accounting principles and their practical applications.

COST ACCOUNTING

Chapter 2 (Garrison)

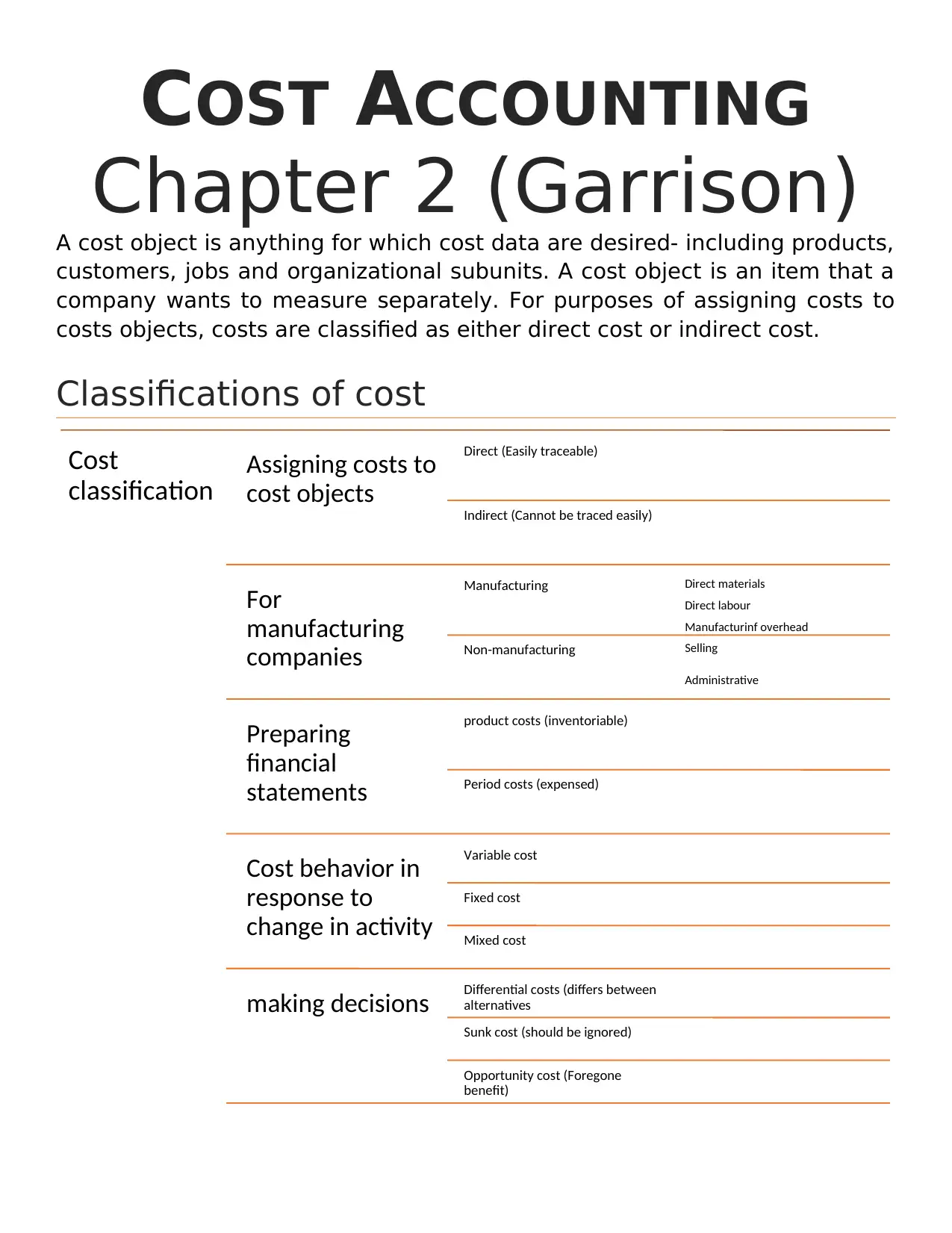

A cost object is anything for which cost data are desired- including products,

customers, jobs and organizational subunits. A cost object is an item that a

company wants to measure separately. For purposes of assigning costs to

costs objects, costs are classified as either direct cost or indirect cost.

Classifications of cost

Cost

classification Assigning costs to

cost objects

Direct (Easily traceable)

Indirect (Cannot be traced easily)

For

manufacturing

companies

Manufacturing Direct materials

Direct labour

Manufacturinf overhead

Non-manufacturing Selling

Administrative

Preparing

financial

statements

product costs (inventoriable)

Period costs (expensed)

Cost behavior in

response to

change in activity

Variable cost

Fixed cost

Mixed cost

making decisions Differential costs (differs between

alternatives

Sunk cost (should be ignored)

Opportunity cost (Foregone

benefit)

Chapter 2 (Garrison)

A cost object is anything for which cost data are desired- including products,

customers, jobs and organizational subunits. A cost object is an item that a

company wants to measure separately. For purposes of assigning costs to

costs objects, costs are classified as either direct cost or indirect cost.

Classifications of cost

Cost

classification Assigning costs to

cost objects

Direct (Easily traceable)

Indirect (Cannot be traced easily)

For

manufacturing

companies

Manufacturing Direct materials

Direct labour

Manufacturinf overhead

Non-manufacturing Selling

Administrative

Preparing

financial

statements

product costs (inventoriable)

Period costs (expensed)

Cost behavior in

response to

change in activity

Variable cost

Fixed cost

Mixed cost

making decisions Differential costs (differs between

alternatives

Sunk cost (should be ignored)

Opportunity cost (Foregone

benefit)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

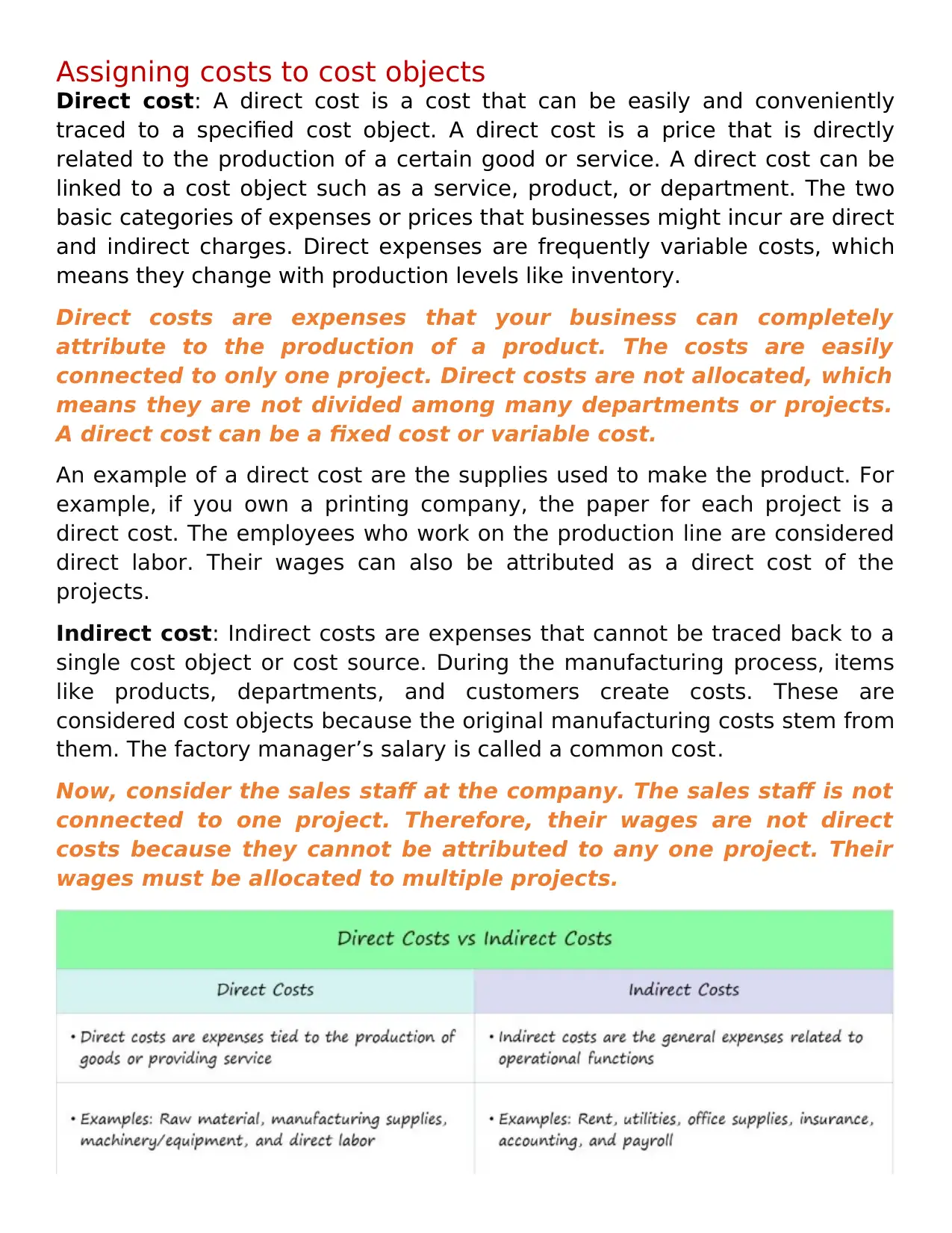

Assigning costs to cost objects

Direct cost: A direct cost is a cost that can be easily and conveniently

traced to a specified cost object. A direct cost is a price that is directly

related to the production of a certain good or service. A direct cost can be

linked to a cost object such as a service, product, or department. The two

basic categories of expenses or prices that businesses might incur are direct

and indirect charges. Direct expenses are frequently variable costs, which

means they change with production levels like inventory.

Direct costs are expenses that your business can completely

attribute to the production of a product. The costs are easily

connected to only one project. Direct costs are not allocated, which

means they are not divided among many departments or projects.

A direct cost can be a fixed cost or variable cost.

An example of a direct cost are the supplies used to make the product. For

example, if you own a printing company, the paper for each project is a

direct cost. The employees who work on the production line are considered

direct labor. Their wages can also be attributed as a direct cost of the

projects.

Indirect cost: Indirect costs are expenses that cannot be traced back to a

single cost object or cost source. During the manufacturing process, items

like products, departments, and customers create costs. These are

considered cost objects because the original manufacturing costs stem from

them. The factory manager’s salary is called a common cost.

Now, consider the sales staff at the company. The sales staff is not

connected to one project. Therefore, their wages are not direct

costs because they cannot be attributed to any one project. Their

wages must be allocated to multiple projects.

Direct cost: A direct cost is a cost that can be easily and conveniently

traced to a specified cost object. A direct cost is a price that is directly

related to the production of a certain good or service. A direct cost can be

linked to a cost object such as a service, product, or department. The two

basic categories of expenses or prices that businesses might incur are direct

and indirect charges. Direct expenses are frequently variable costs, which

means they change with production levels like inventory.

Direct costs are expenses that your business can completely

attribute to the production of a product. The costs are easily

connected to only one project. Direct costs are not allocated, which

means they are not divided among many departments or projects.

A direct cost can be a fixed cost or variable cost.

An example of a direct cost are the supplies used to make the product. For

example, if you own a printing company, the paper for each project is a

direct cost. The employees who work on the production line are considered

direct labor. Their wages can also be attributed as a direct cost of the

projects.

Indirect cost: Indirect costs are expenses that cannot be traced back to a

single cost object or cost source. During the manufacturing process, items

like products, departments, and customers create costs. These are

considered cost objects because the original manufacturing costs stem from

them. The factory manager’s salary is called a common cost.

Now, consider the sales staff at the company. The sales staff is not

connected to one project. Therefore, their wages are not direct

costs because they cannot be attributed to any one project. Their

wages must be allocated to multiple projects.

Cost classification for manufacturing companies

Costs may be classified as manufacturing costs and non-manufacturing

costs. This classification is usually used by manufacturing companies.

Manufacturing costs

Most manufacturing companies separate their manufacturing costs into two

direct cost categories, direct-materials and direct labor and in one indirect

cost categories, manufacturing overhead.

Direct materials

Direct labor

Manufacturing overhead

Direct materials: Direct material is the physical items built into a product.

For example, the direct materials for a baker include flour, eggs,

yeast, sugar, oil, and water. The direct materials concept is used in cost

accounting, where this cost is separately classified in several types of

financial analysis. Direct materials are rolled into the total cost of goods

produced, which is then subdivided into the cost of goods sold (which

appears in the income statement) and ending inventory (which appears in

the balance sheet). The finished product of a company may become raw

material of another company. For example, cement is a finished product for

manufacturers of cement and raw materials for companies involved in

construction business.

Direct labor: Direct labor refers to the salaries and wages paid to workers

directly involved in the manufacture of a specific product or in performing a

service. The work performed must be related to the specific task. For a

business that provides services to its customers, direct labor is the work

performed by the workers who provide the service directly to the

customers, such as auditors, lawyers, and consultants. Examples of direct

labor cost include labor cost of machine operators and painters in a

manufacturing company. Like direct materials, it comprises of a

significant portion of total manufacturing cost.

The sum of direct materials cost and direct labor cost is known as

prime cost. Prime cost = Direct materials cost + Direct labor cost

Manufacturing overhead: Manufacturing costs other than direct materials

and direct labor are categorized as manufacturing overhead cost (also

known as factory overhead costs). They usually include indirect materials,

Costs may be classified as manufacturing costs and non-manufacturing

costs. This classification is usually used by manufacturing companies.

Manufacturing costs

Most manufacturing companies separate their manufacturing costs into two

direct cost categories, direct-materials and direct labor and in one indirect

cost categories, manufacturing overhead.

Direct materials

Direct labor

Manufacturing overhead

Direct materials: Direct material is the physical items built into a product.

For example, the direct materials for a baker include flour, eggs,

yeast, sugar, oil, and water. The direct materials concept is used in cost

accounting, where this cost is separately classified in several types of

financial analysis. Direct materials are rolled into the total cost of goods

produced, which is then subdivided into the cost of goods sold (which

appears in the income statement) and ending inventory (which appears in

the balance sheet). The finished product of a company may become raw

material of another company. For example, cement is a finished product for

manufacturers of cement and raw materials for companies involved in

construction business.

Direct labor: Direct labor refers to the salaries and wages paid to workers

directly involved in the manufacture of a specific product or in performing a

service. The work performed must be related to the specific task. For a

business that provides services to its customers, direct labor is the work

performed by the workers who provide the service directly to the

customers, such as auditors, lawyers, and consultants. Examples of direct

labor cost include labor cost of machine operators and painters in a

manufacturing company. Like direct materials, it comprises of a

significant portion of total manufacturing cost.

The sum of direct materials cost and direct labor cost is known as

prime cost. Prime cost = Direct materials cost + Direct labor cost

Manufacturing overhead: Manufacturing costs other than direct materials

and direct labor are categorized as manufacturing overhead cost (also

known as factory overhead costs). They usually include indirect materials,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

indirect labor, salary of supervisor, lighting, heat and insurance cost of

factory etc. Mostly, manufacturing overhead costs cannot be easily traced

to individual units of finished products. The three types of overhead costs

are:

Fixed: These costs do not change each month. Also, business activity

does not cause these costs to change. Fixed overhead costs include

rent, mortgage, government fees and property taxes.

Variable: These are costs that can change with production output.

These items include some operational utilities such as electric, gas and

trash service. Output can also impact shipping costs, maintenance

situations, legal fees and advertising.

Semi-variable: These items might change over time with increased or

decreased business activity. Business activities may determine the

initial costs but over time, as activity changes, these costs may

increase or decrease. Some examples of semi-variable costs may

include operational utilities, rent or leasing and insurance.

The sum of direct labor cost and manufacturing overhead cost is

known as conversion cost. Conversion cost = Direct labor cost +

Manufacturing overhead cost.

Non-manufacturing costs

Non-manufacturing costs are further divided into the following categories:

Marketing and selling costs

Administrative costs

Examples of marketing and selling costs include advertising costs, order

taking costs and salaries of sales persons etc. Examples of administrative

costs include salaries of executives, accounting costs, and general

administration costs etc.

Selling costs include all costs that are incurred to secure customer orders

and get the finished product to the customer. These costs are sometimes

called as order-getting and order-filling costs.

Administrative costs include all costs associated with the general

management of an organization rather than with manufacturing or selling.

Examples of administrative costs include executive compensation, general

accounting, pubic relations and similar costs.

factory etc. Mostly, manufacturing overhead costs cannot be easily traced

to individual units of finished products. The three types of overhead costs

are:

Fixed: These costs do not change each month. Also, business activity

does not cause these costs to change. Fixed overhead costs include

rent, mortgage, government fees and property taxes.

Variable: These are costs that can change with production output.

These items include some operational utilities such as electric, gas and

trash service. Output can also impact shipping costs, maintenance

situations, legal fees and advertising.

Semi-variable: These items might change over time with increased or

decreased business activity. Business activities may determine the

initial costs but over time, as activity changes, these costs may

increase or decrease. Some examples of semi-variable costs may

include operational utilities, rent or leasing and insurance.

The sum of direct labor cost and manufacturing overhead cost is

known as conversion cost. Conversion cost = Direct labor cost +

Manufacturing overhead cost.

Non-manufacturing costs

Non-manufacturing costs are further divided into the following categories:

Marketing and selling costs

Administrative costs

Examples of marketing and selling costs include advertising costs, order

taking costs and salaries of sales persons etc. Examples of administrative

costs include salaries of executives, accounting costs, and general

administration costs etc.

Selling costs include all costs that are incurred to secure customer orders

and get the finished product to the customer. These costs are sometimes

called as order-getting and order-filling costs.

Administrative costs include all costs associated with the general

management of an organization rather than with manufacturing or selling.

Examples of administrative costs include executive compensation, general

accounting, pubic relations and similar costs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost classifications for preparing financial statements

When preparing a balance sheet and an income statement, companies need

to classify their costs as product cost and period cost. To understand the

differences between product cost and period costs, we must first discuss the

matching principle from financial accounting. The matching principle is

based on the accrual concept the costs incurred to generate a particular

revenue should be recognized as expenses in the same period that the

revenue is recognized. Matching Principle is a common accounting concept.

Under this, a company should report an expense in the income statement in

the same period when it earns the revenue.

Product costs

Product cost refers to the costs incurred to create a product. These costs

include direct labor, direct materials, consumable production supplies, and

factory overhead. Product cost can also be considered the cost of the labor

required to deliver a service to a customer. The cost of a product on a unit

basis is typically derived by compiling the costs associated with a batch of

units that were produced as a group, and dividing by the number of units

manufactured. The calculation is:

(Total direct labor + Total direct materials + Consumable supplies

+ Total allocated overhead) ÷ Total number of units = Product unit

cost

These costs are also known as inventoriable costs.

Period costs

Period costs are costs that cannot be capitalized on a company’s balance

sheet. In other words, they are expensed in the period incurred and appear

on the income statement. Period costs are also called period expenses. In

managerial and cost accounting, period costs refer to costs that are not tied

to or related to the production of inventory. Examples include selling,

general and administrative (SG&A) expenses, marketing expenses, CEO

salary, and rent expense relating to a corporate office. The costs are not

related to the production of inventory and are therefore expensed in the

period incurred. In short, all costs that are not involved in the production of

a product (product costs) are period costs.

Prime cost and conversion cost

When preparing a balance sheet and an income statement, companies need

to classify their costs as product cost and period cost. To understand the

differences between product cost and period costs, we must first discuss the

matching principle from financial accounting. The matching principle is

based on the accrual concept the costs incurred to generate a particular

revenue should be recognized as expenses in the same period that the

revenue is recognized. Matching Principle is a common accounting concept.

Under this, a company should report an expense in the income statement in

the same period when it earns the revenue.

Product costs

Product cost refers to the costs incurred to create a product. These costs

include direct labor, direct materials, consumable production supplies, and

factory overhead. Product cost can also be considered the cost of the labor

required to deliver a service to a customer. The cost of a product on a unit

basis is typically derived by compiling the costs associated with a batch of

units that were produced as a group, and dividing by the number of units

manufactured. The calculation is:

(Total direct labor + Total direct materials + Consumable supplies

+ Total allocated overhead) ÷ Total number of units = Product unit

cost

These costs are also known as inventoriable costs.

Period costs

Period costs are costs that cannot be capitalized on a company’s balance

sheet. In other words, they are expensed in the period incurred and appear

on the income statement. Period costs are also called period expenses. In

managerial and cost accounting, period costs refer to costs that are not tied

to or related to the production of inventory. Examples include selling,

general and administrative (SG&A) expenses, marketing expenses, CEO

salary, and rent expense relating to a corporate office. The costs are not

related to the production of inventory and are therefore expensed in the

period incurred. In short, all costs that are not involved in the production of

a product (product costs) are period costs.

Prime cost and conversion cost

Prime costs are the sum of direct material costs and

direct labor costs. Conversion cost is the sum of direct

labor costs and manufacturing overhead.

Cost classifications for predicting cost behavior

Variable cost

Variable costs are expenses that vary in proportion to the volume of goods

or services that a business produces. In other words, they are costs that

vary depending on the volume of activity. The costs increase as the volume

of activities increases and decrease as the volume of activities decreases.

For a cost to be variable, it must be variable with respect to something. That

something is its activity based. An activity base is a measure of whatever

causes the incurrence of a variable cost. A activity base is sometimes

referred to as a cost driver.

Fixed cost

The term fixed cost refers to a cost that does not change with an increase or

decrease in the number of goods or services produced or sold. Fixed costs

are expenses that have to be paid by a company, independent of any

specific business activities. This means fixed costs are generally indirect, in

that they don't apply to a company's production of any goods or services.

Let us say, in a milk factory, the monthly payments for the

phone lines and security system and the monthly rent for the

facilities are fixed costs as they do not change according to

how much milk the factory produces. On the other hand, the

factory’s wage costs are variable as it will need to hire more

workers if the production increases. An analytical formula can

track the relationship between fixed cost and variable cost in

management accounting. It is important to know how total

costs are divided between the two types of costs. The division

of the costs is critical, and forecasting the earnings generated

by various changes in unit sales affects future planned

marketing campaigns. Discretionary fixed costs usually come

about from decisions made by management to spend on

certain fixed cost items. Examples of discretionary costs

include advertising, machinery maintenance, and research and

development (R&D) expenditures.

Committed fixed costs represent organizational investments with a

multiyear planning horizon that cannot be significantly reduced

direct labor costs. Conversion cost is the sum of direct

labor costs and manufacturing overhead.

Cost classifications for predicting cost behavior

Variable cost

Variable costs are expenses that vary in proportion to the volume of goods

or services that a business produces. In other words, they are costs that

vary depending on the volume of activity. The costs increase as the volume

of activities increases and decrease as the volume of activities decreases.

For a cost to be variable, it must be variable with respect to something. That

something is its activity based. An activity base is a measure of whatever

causes the incurrence of a variable cost. A activity base is sometimes

referred to as a cost driver.

Fixed cost

The term fixed cost refers to a cost that does not change with an increase or

decrease in the number of goods or services produced or sold. Fixed costs

are expenses that have to be paid by a company, independent of any

specific business activities. This means fixed costs are generally indirect, in

that they don't apply to a company's production of any goods or services.

Let us say, in a milk factory, the monthly payments for the

phone lines and security system and the monthly rent for the

facilities are fixed costs as they do not change according to

how much milk the factory produces. On the other hand, the

factory’s wage costs are variable as it will need to hire more

workers if the production increases. An analytical formula can

track the relationship between fixed cost and variable cost in

management accounting. It is important to know how total

costs are divided between the two types of costs. The division

of the costs is critical, and forecasting the earnings generated

by various changes in unit sales affects future planned

marketing campaigns. Discretionary fixed costs usually come

about from decisions made by management to spend on

certain fixed cost items. Examples of discretionary costs

include advertising, machinery maintenance, and research and

development (R&D) expenditures.

Committed fixed costs represent organizational investments with a

multiyear planning horizon that cannot be significantly reduced

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ever for short period of time without making fundamental changes.

Discretionary fixed costs usually arise from annual decisions by

management to spend on certain fixed cost items.

Mixed costs

A mixed cost is an expense that has attributes of both fixed and variable

costs. In other words, it’s a cost that changes with the volume of production

like a variable cost and can’t be completely eliminated like a fixed cost.

Wage costs for employees who are paid a monthly salary plus commissions

are a good example of mixed costs. This is a common compensation

package for salesmen and sales reps. They usually receive a small base

salary and commissions based on how many sales they make during the

period.

The monthly salary is a fixed cost because it can’t be eliminated. Even if the

salesperson doesn’t sell anything during the month, the company still has to

pay the base salary.

The commission, on the other hand, acts more like a variable cost because

it’s based on the productivity of the employee. The more the employee sells

the greater the sales commission expense becomes. The company can

eliminate this expense altogether if it doesn’t sell anything for the month.

Cost classifications for decision making

Differential cost and revenue

A difference in costs between two alternatives is known as a differential

cost. A difference in revenues between two alternatives is known as

differential revenue.

A differential cost is also known as an incremental cost, although technically

an incremental cost should refer only to an increase in cost from one

alternative to another; decreases in costs should be referred to as

decremental cost. Differential cost is a broader term, encompassing both

cost increases and cost decreases between alternatives.

Opportunity cost and sunk cost

Opportunity cost is the potential benefit that is given up when one

alternative is selected over another. A sunk cost is a cost that has already

been incurred and that cannot be changed by any decision made now or in

the future. Because sunk costs cannot be changed by any decision made

Discretionary fixed costs usually arise from annual decisions by

management to spend on certain fixed cost items.

Mixed costs

A mixed cost is an expense that has attributes of both fixed and variable

costs. In other words, it’s a cost that changes with the volume of production

like a variable cost and can’t be completely eliminated like a fixed cost.

Wage costs for employees who are paid a monthly salary plus commissions

are a good example of mixed costs. This is a common compensation

package for salesmen and sales reps. They usually receive a small base

salary and commissions based on how many sales they make during the

period.

The monthly salary is a fixed cost because it can’t be eliminated. Even if the

salesperson doesn’t sell anything during the month, the company still has to

pay the base salary.

The commission, on the other hand, acts more like a variable cost because

it’s based on the productivity of the employee. The more the employee sells

the greater the sales commission expense becomes. The company can

eliminate this expense altogether if it doesn’t sell anything for the month.

Cost classifications for decision making

Differential cost and revenue

A difference in costs between two alternatives is known as a differential

cost. A difference in revenues between two alternatives is known as

differential revenue.

A differential cost is also known as an incremental cost, although technically

an incremental cost should refer only to an increase in cost from one

alternative to another; decreases in costs should be referred to as

decremental cost. Differential cost is a broader term, encompassing both

cost increases and cost decreases between alternatives.

Opportunity cost and sunk cost

Opportunity cost is the potential benefit that is given up when one

alternative is selected over another. A sunk cost is a cost that has already

been incurred and that cannot be changed by any decision made now or in

the future. Because sunk costs cannot be changed by any decision made

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

now or in the future. And because only differential costs are relevant in a

decision, sunk costs always be ignored.

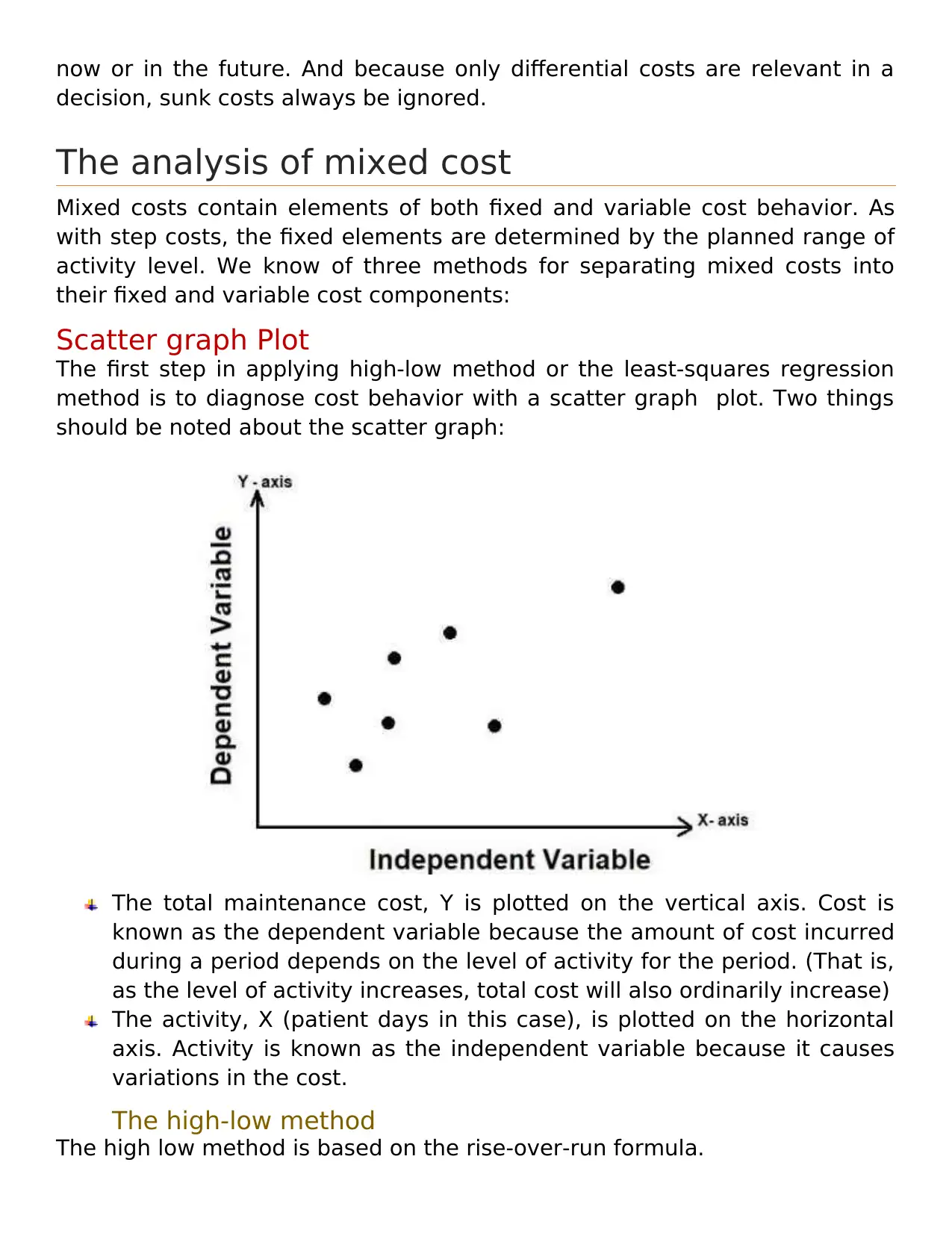

The analysis of mixed cost

Mixed costs contain elements of both fixed and variable cost behavior. As

with step costs, the fixed elements are determined by the planned range of

activity level. We know of three methods for separating mixed costs into

their fixed and variable cost components:

Scatter graph Plot

The first step in applying high-low method or the least-squares regression

method is to diagnose cost behavior with a scatter graph plot. Two things

should be noted about the scatter graph:

The total maintenance cost, Y is plotted on the vertical axis. Cost is

known as the dependent variable because the amount of cost incurred

during a period depends on the level of activity for the period. (That is,

as the level of activity increases, total cost will also ordinarily increase)

The activity, X (patient days in this case), is plotted on the horizontal

axis. Activity is known as the independent variable because it causes

variations in the cost.

The high-low method

The high low method is based on the rise-over-run formula.

decision, sunk costs always be ignored.

The analysis of mixed cost

Mixed costs contain elements of both fixed and variable cost behavior. As

with step costs, the fixed elements are determined by the planned range of

activity level. We know of three methods for separating mixed costs into

their fixed and variable cost components:

Scatter graph Plot

The first step in applying high-low method or the least-squares regression

method is to diagnose cost behavior with a scatter graph plot. Two things

should be noted about the scatter graph:

The total maintenance cost, Y is plotted on the vertical axis. Cost is

known as the dependent variable because the amount of cost incurred

during a period depends on the level of activity for the period. (That is,

as the level of activity increases, total cost will also ordinarily increase)

The activity, X (patient days in this case), is plotted on the horizontal

axis. Activity is known as the independent variable because it causes

variations in the cost.

The high-low method

The high low method is based on the rise-over-run formula.

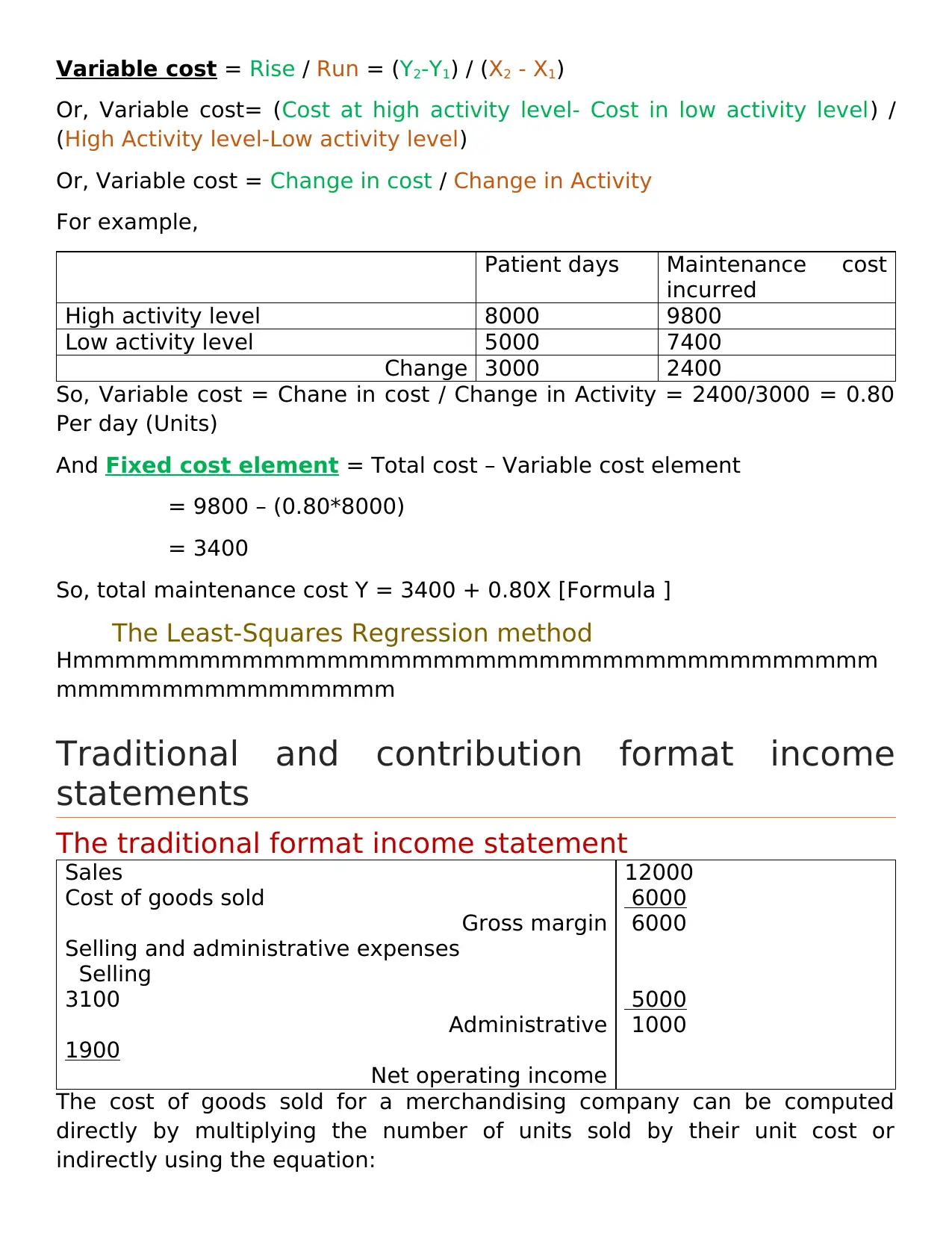

Variable cost = Rise / Run = (Y2-Y1) / (X2 - X1)

Or, Variable cost= (Cost at high activity level- Cost in low activity level) /

(High Activity level-Low activity level)

Or, Variable cost = Change in cost / Change in Activity

For example,

Patient days Maintenance cost

incurred

High activity level 8000 9800

Low activity level 5000 7400

Change 3000 2400

So, Variable cost = Chane in cost / Change in Activity = 2400/3000 = 0.80

Per day (Units)

And Fixed cost element = Total cost – Variable cost element

= 9800 – (0.80*8000)

= 3400

So, total maintenance cost Y = 3400 + 0.80X [Formula ]

The Least-Squares Regression method

Hmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmm

mmmmmmmmmmmmmmmm

Traditional and contribution format income

statements

The traditional format income statement

Sales

Cost of goods sold

Gross margin

Selling and administrative expenses

Selling

3100

Administrative

1900

Net operating income

12000

6000

6000

5000

1000

The cost of goods sold for a merchandising company can be computed

directly by multiplying the number of units sold by their unit cost or

indirectly using the equation:

Or, Variable cost= (Cost at high activity level- Cost in low activity level) /

(High Activity level-Low activity level)

Or, Variable cost = Change in cost / Change in Activity

For example,

Patient days Maintenance cost

incurred

High activity level 8000 9800

Low activity level 5000 7400

Change 3000 2400

So, Variable cost = Chane in cost / Change in Activity = 2400/3000 = 0.80

Per day (Units)

And Fixed cost element = Total cost – Variable cost element

= 9800 – (0.80*8000)

= 3400

So, total maintenance cost Y = 3400 + 0.80X [Formula ]

The Least-Squares Regression method

Hmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmm

mmmmmmmmmmmmmmmm

Traditional and contribution format income

statements

The traditional format income statement

Sales

Cost of goods sold

Gross margin

Selling and administrative expenses

Selling

3100

Administrative

1900

Net operating income

12000

6000

6000

5000

1000

The cost of goods sold for a merchandising company can be computed

directly by multiplying the number of units sold by their unit cost or

indirectly using the equation:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

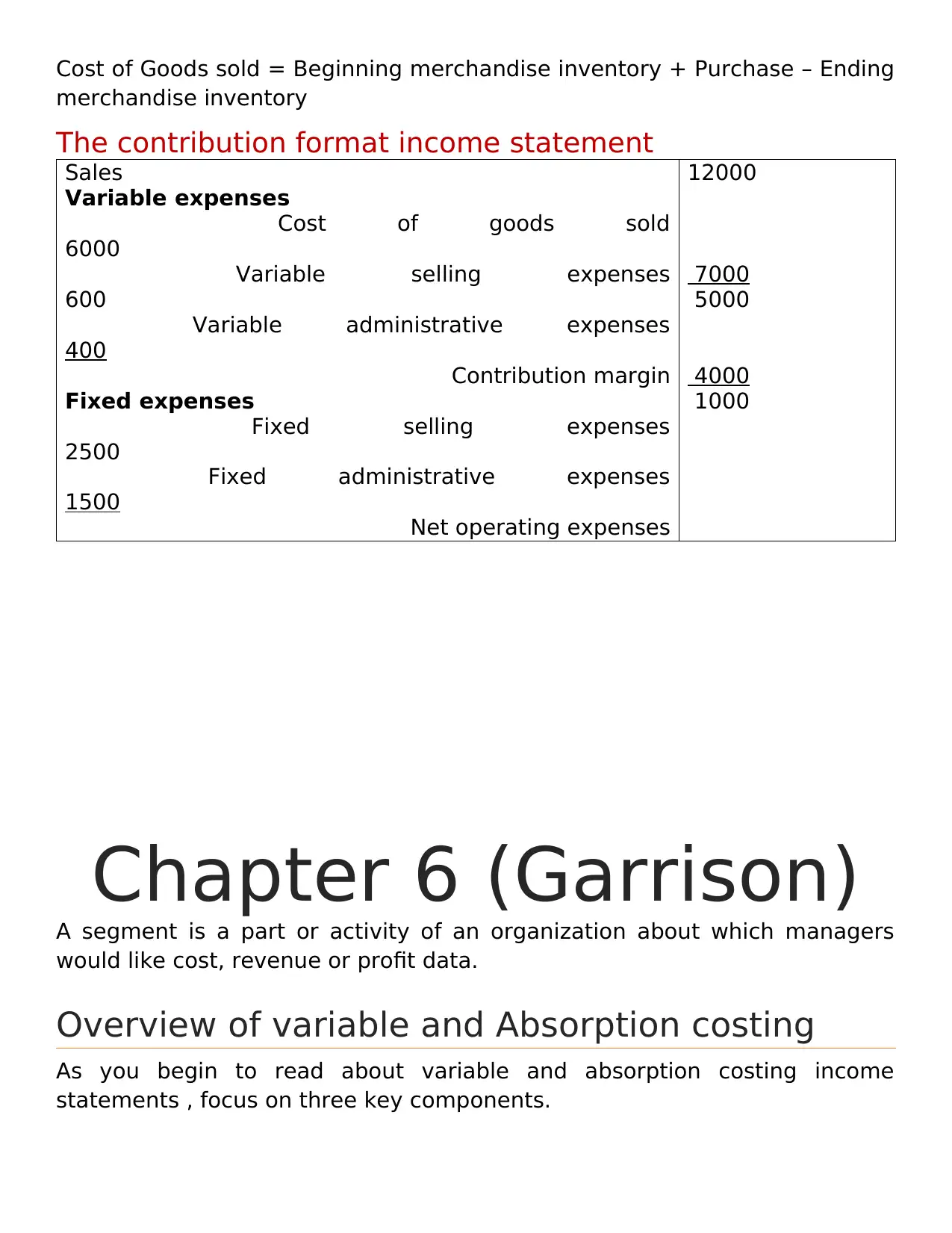

Cost of Goods sold = Beginning merchandise inventory + Purchase – Ending

merchandise inventory

The contribution format income statement

Sales

Variable expenses

Cost of goods sold

6000

Variable selling expenses

600

Variable administrative expenses

400

Contribution margin

Fixed expenses

Fixed selling expenses

2500

Fixed administrative expenses

1500

Net operating expenses

12000

7000

5000

4000

1000

Chapter 6 (Garrison)

A segment is a part or activity of an organization about which managers

would like cost, revenue or profit data.

Overview of variable and Absorption costing

As you begin to read about variable and absorption costing income

statements , focus on three key components.

merchandise inventory

The contribution format income statement

Sales

Variable expenses

Cost of goods sold

6000

Variable selling expenses

600

Variable administrative expenses

400

Contribution margin

Fixed expenses

Fixed selling expenses

2500

Fixed administrative expenses

1500

Net operating expenses

12000

7000

5000

4000

1000

Chapter 6 (Garrison)

A segment is a part or activity of an organization about which managers

would like cost, revenue or profit data.

Overview of variable and Absorption costing

As you begin to read about variable and absorption costing income

statements , focus on three key components.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

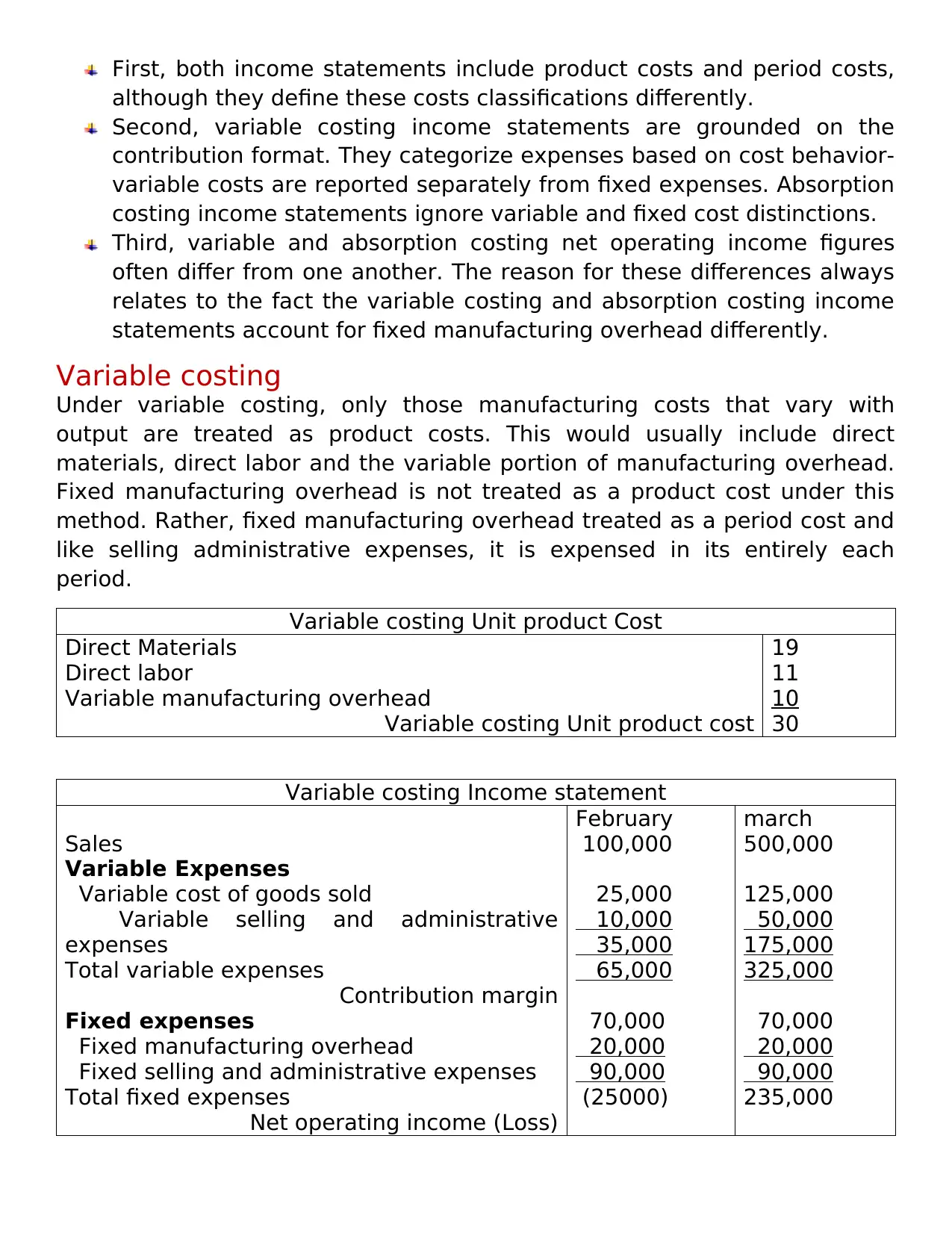

First, both income statements include product costs and period costs,

although they define these costs classifications differently.

Second, variable costing income statements are grounded on the

contribution format. They categorize expenses based on cost behavior-

variable costs are reported separately from fixed expenses. Absorption

costing income statements ignore variable and fixed cost distinctions.

Third, variable and absorption costing net operating income figures

often differ from one another. The reason for these differences always

relates to the fact the variable costing and absorption costing income

statements account for fixed manufacturing overhead differently.

Variable costing

Under variable costing, only those manufacturing costs that vary with

output are treated as product costs. This would usually include direct

materials, direct labor and the variable portion of manufacturing overhead.

Fixed manufacturing overhead is not treated as a product cost under this

method. Rather, fixed manufacturing overhead treated as a period cost and

like selling administrative expenses, it is expensed in its entirely each

period.

Variable costing Unit product Cost

Direct Materials

Direct labor

Variable manufacturing overhead

Variable costing Unit product cost

19

11

10

30

Variable costing Income statement

Sales

Variable Expenses

Variable cost of goods sold

Variable selling and administrative

expenses

Total variable expenses

Contribution margin

Fixed expenses

Fixed manufacturing overhead

Fixed selling and administrative expenses

Total fixed expenses

Net operating income (Loss)

February

100,000

25,000

10,000

35,000

65,000

70,000

20,000

90,000

(25000)

march

500,000

125,000

50,000

175,000

325,000

70,000

20,000

90,000

235,000

although they define these costs classifications differently.

Second, variable costing income statements are grounded on the

contribution format. They categorize expenses based on cost behavior-

variable costs are reported separately from fixed expenses. Absorption

costing income statements ignore variable and fixed cost distinctions.

Third, variable and absorption costing net operating income figures

often differ from one another. The reason for these differences always

relates to the fact the variable costing and absorption costing income

statements account for fixed manufacturing overhead differently.

Variable costing

Under variable costing, only those manufacturing costs that vary with

output are treated as product costs. This would usually include direct

materials, direct labor and the variable portion of manufacturing overhead.

Fixed manufacturing overhead is not treated as a product cost under this

method. Rather, fixed manufacturing overhead treated as a period cost and

like selling administrative expenses, it is expensed in its entirely each

period.

Variable costing Unit product Cost

Direct Materials

Direct labor

Variable manufacturing overhead

Variable costing Unit product cost

19

11

10

30

Variable costing Income statement

Sales

Variable Expenses

Variable cost of goods sold

Variable selling and administrative

expenses

Total variable expenses

Contribution margin

Fixed expenses

Fixed manufacturing overhead

Fixed selling and administrative expenses

Total fixed expenses

Net operating income (Loss)

February

100,000

25,000

10,000

35,000

65,000

70,000

20,000

90,000

(25000)

march

500,000

125,000

50,000

175,000

325,000

70,000

20,000

90,000

235,000

Absorption costing

Absorption costing treats all manufacturing costs as product costs,

regardless of whether they are variable or fixed. The cost of a unit of

product under the absorption costing method consist of direct materials,

direct labor and both variable and fixed manufacturing overhead. Thus,

absorption costing allocates a portion of fixed manufacturing overhead cost

to each unit of product, along with the variable manufacturing costs.

Because absorption costing includes all manufacturing costs in product

costs, it is frequently referred as the full cost method.

Absorption costing Unit product Cost

Direct Materials

Direct labor

Variable manufacturing overhead

Fixed manufacturing overhead

Variable costing Unit product cost

19

11

10

30

60

Absorption costing Income statement

Sales

Cost of goods sold (Unit product cost * total units)

Gross margin

Selling and administrative expenses

Net operating margin

Reconciliation of Variable costing with

absorption costing income

Step 1: The net operating incomes are reconciled as follows:

Year 1 Year 2

Units in beginning inventory

+ Units produced

- Units sold

= Units in ending inventory

0

50,000

40,000

10,000

10,000

40,000

50,000

0

Step 2:

Year 1 Year 2

Fixed manufacturing overhead in ending inventory

- fixed manufacturing overhead in beginning

inventory

= Manufacturing overhead differed in (released from)

inventory

50000

0

50000

0

50000

(50000)

Absorption costing treats all manufacturing costs as product costs,

regardless of whether they are variable or fixed. The cost of a unit of

product under the absorption costing method consist of direct materials,

direct labor and both variable and fixed manufacturing overhead. Thus,

absorption costing allocates a portion of fixed manufacturing overhead cost

to each unit of product, along with the variable manufacturing costs.

Because absorption costing includes all manufacturing costs in product

costs, it is frequently referred as the full cost method.

Absorption costing Unit product Cost

Direct Materials

Direct labor

Variable manufacturing overhead

Fixed manufacturing overhead

Variable costing Unit product cost

19

11

10

30

60

Absorption costing Income statement

Sales

Cost of goods sold (Unit product cost * total units)

Gross margin

Selling and administrative expenses

Net operating margin

Reconciliation of Variable costing with

absorption costing income

Step 1: The net operating incomes are reconciled as follows:

Year 1 Year 2

Units in beginning inventory

+ Units produced

- Units sold

= Units in ending inventory

0

50,000

40,000

10,000

10,000

40,000

50,000

0

Step 2:

Year 1 Year 2

Fixed manufacturing overhead in ending inventory

- fixed manufacturing overhead in beginning

inventory

= Manufacturing overhead differed in (released from)

inventory

50000

0

50000

0

50000

(50000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.