Analysis of Cost, Budgeting and Variance in Financial Resources

VerifiedAdded on 2023/06/15

|13

|2623

|292

Report

AI Summary

This report provides a detailed analysis of managing financial resources, covering key aspects such as cost calculation (prime cost, production cost, sales & distribution cost, administration expenses, and total cost), budgeting and forecasting techniques, variance analysis, and different types of budgets including flexible and static budgets. Furthermore, it delves into specific financial ratios relevant to the food industry, such as food cost of sales ratio, food average spend ratio, revenue per available seat hour, and labor cost ratio, illustrating their importance in optimizing profitability and operational efficiency. The report uses examples and calculations to demonstrate these concepts, offering a comprehensive overview of financial management principles and their practical application.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

MAIN BODY..................................................................................................................................1

SECTION A.....................................................................................................................................1

QUESTION 1.............................................................................................................................1

SECTION B....................................................................................................................................4

Question 4....................................................................................................................................4

Question 6....................................................................................................................................8

REFERENCES..............................................................................................................................11

MAIN BODY..................................................................................................................................1

SECTION A.....................................................................................................................................1

QUESTION 1.............................................................................................................................1

SECTION B....................................................................................................................................4

Question 4....................................................................................................................................4

Question 6....................................................................................................................................8

REFERENCES..............................................................................................................................11

MAIN BODY

SECTION A

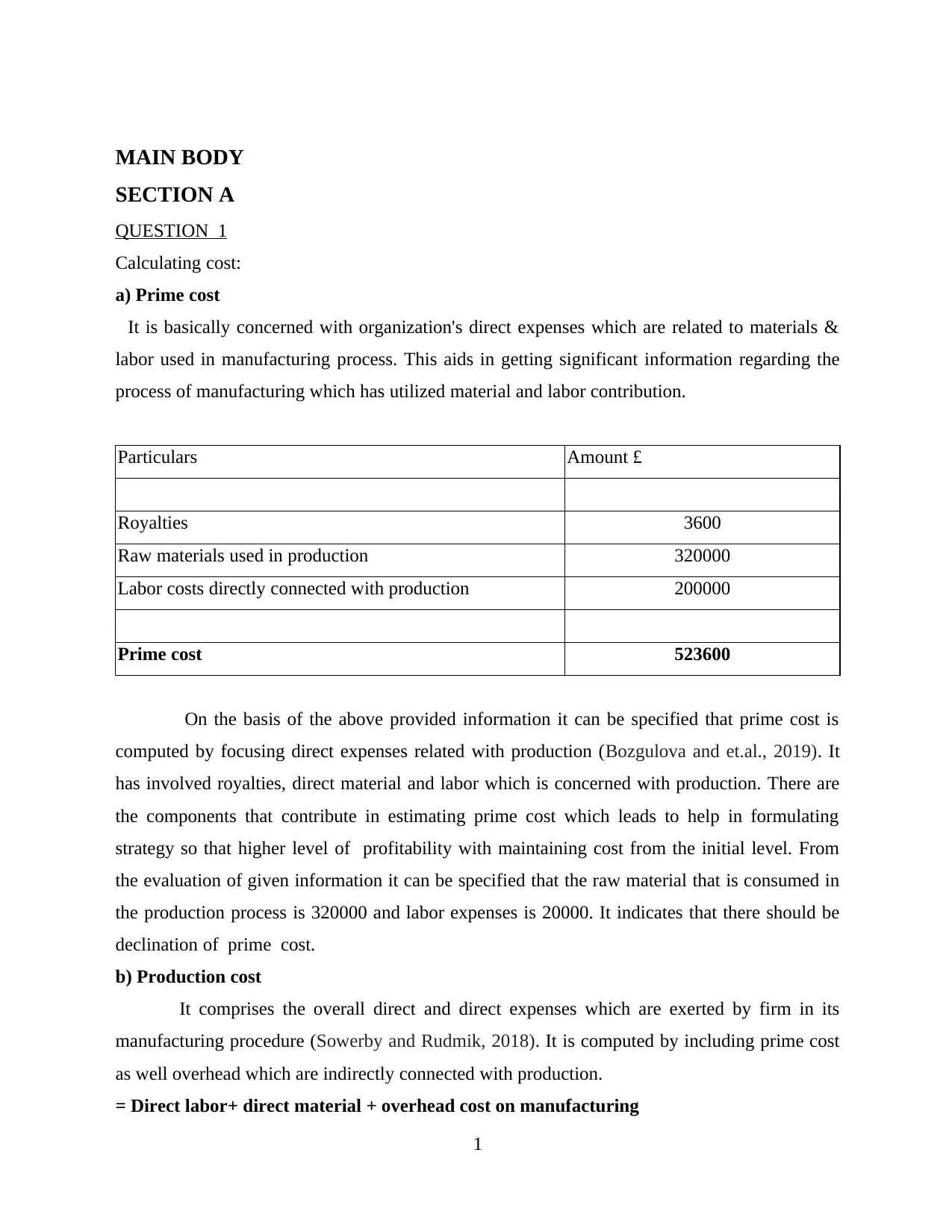

QUESTION 1

Calculating cost:

a) Prime cost

It is basically concerned with organization's direct expenses which are related to materials &

labor used in manufacturing process. This aids in getting significant information regarding the

process of manufacturing which has utilized material and labor contribution.

Particulars Amount £

Royalties 3600

Raw materials used in production 320000

Labor costs directly connected with production 200000

Prime cost 523600

On the basis of the above provided information it can be specified that prime cost is

computed by focusing direct expenses related with production (Bozgulova and et.al., 2019). It

has involved royalties, direct material and labor which is concerned with production. There are

the components that contribute in estimating prime cost which leads to help in formulating

strategy so that higher level of profitability with maintaining cost from the initial level. From

the evaluation of given information it can be specified that the raw material that is consumed in

the production process is 320000 and labor expenses is 20000. It indicates that there should be

declination of prime cost.

b) Production cost

It comprises the overall direct and direct expenses which are exerted by firm in its

manufacturing procedure (Sowerby and Rudmik, 2018). It is computed by including prime cost

as well overhead which are indirectly connected with production.

= Direct labor+ direct material + overhead cost on manufacturing

1

SECTION A

QUESTION 1

Calculating cost:

a) Prime cost

It is basically concerned with organization's direct expenses which are related to materials &

labor used in manufacturing process. This aids in getting significant information regarding the

process of manufacturing which has utilized material and labor contribution.

Particulars Amount £

Royalties 3600

Raw materials used in production 320000

Labor costs directly connected with production 200000

Prime cost 523600

On the basis of the above provided information it can be specified that prime cost is

computed by focusing direct expenses related with production (Bozgulova and et.al., 2019). It

has involved royalties, direct material and labor which is concerned with production. There are

the components that contribute in estimating prime cost which leads to help in formulating

strategy so that higher level of profitability with maintaining cost from the initial level. From

the evaluation of given information it can be specified that the raw material that is consumed in

the production process is 320000 and labor expenses is 20000. It indicates that there should be

declination of prime cost.

b) Production cost

It comprises the overall direct and direct expenses which are exerted by firm in its

manufacturing procedure (Sowerby and Rudmik, 2018). It is computed by including prime cost

as well overhead which are indirectly connected with production.

= Direct labor+ direct material + overhead cost on manufacturing

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Amount £

Royalties 3600

Raw materials used in production 320000

Labor costs of production 200000

Wages of factory supervisors 120000

Computer overhead 6000

Depreciation 13000

Other production overhead 70000

Total production cost 732600

From the evaluation of the provided table illustrated it can be taken into consideration

by enterprise that there are several costs which are incurred by specified organization. It includes

raw material, labour, wages of factory supervisors, depreciation and other production overhead.

On the basis of this, it can be stated that these are the manufacturing expenses which are need to

be implemented by company for gaining the ability to produce the products. In respect to this, it

is articulated that to be successful declining particular cost with maintaining quality can

provide assistance in accomplishing organizational objectives. It plays significant role in

estimation of price in turn margin of profitability can be derived.

Working note:

Depreciation for production Amount £

machinery 8000

Building 5000

Total depreciation 13000

c)

Sales & Distribution cost

There are several expenses which are incurred by firm in order to manage the

operational activities. Selling the produced goods to market require enterprise to concentrate on

2

Royalties 3600

Raw materials used in production 320000

Labor costs of production 200000

Wages of factory supervisors 120000

Computer overhead 6000

Depreciation 13000

Other production overhead 70000

Total production cost 732600

From the evaluation of the provided table illustrated it can be taken into consideration

by enterprise that there are several costs which are incurred by specified organization. It includes

raw material, labour, wages of factory supervisors, depreciation and other production overhead.

On the basis of this, it can be stated that these are the manufacturing expenses which are need to

be implemented by company for gaining the ability to produce the products. In respect to this, it

is articulated that to be successful declining particular cost with maintaining quality can

provide assistance in accomplishing organizational objectives. It plays significant role in

estimation of price in turn margin of profitability can be derived.

Working note:

Depreciation for production Amount £

machinery 8000

Building 5000

Total depreciation 13000

c)

Sales & Distribution cost

There are several expenses which are incurred by firm in order to manage the

operational activities. Selling the produced goods to market require enterprise to concentrate on

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

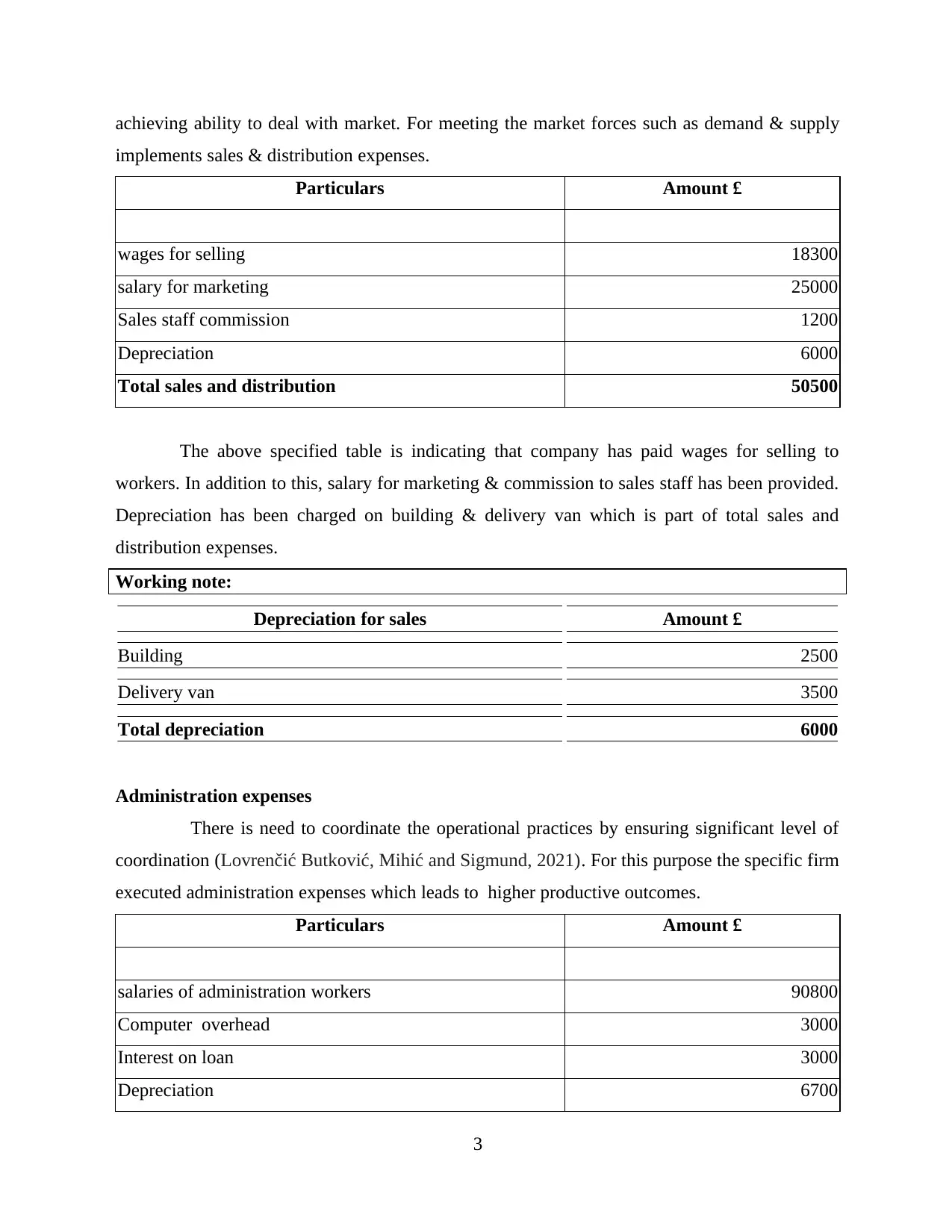

achieving ability to deal with market. For meeting the market forces such as demand & supply

implements sales & distribution expenses.

Particulars Amount £

wages for selling 18300

salary for marketing 25000

Sales staff commission 1200

Depreciation 6000

Total sales and distribution 50500

The above specified table is indicating that company has paid wages for selling to

workers. In addition to this, salary for marketing & commission to sales staff has been provided.

Depreciation has been charged on building & delivery van which is part of total sales and

distribution expenses.

Working note:

Depreciation for sales Amount £

Building 2500

Delivery van 3500

Total depreciation 6000

Administration expenses

There is need to coordinate the operational practices by ensuring significant level of

coordination (Lovrenčić Butković, Mihić and Sigmund, 2021). For this purpose the specific firm

executed administration expenses which leads to higher productive outcomes.

Particulars Amount £

salaries of administration workers 90800

Computer overhead 3000

Interest on loan 3000

Depreciation 6700

3

implements sales & distribution expenses.

Particulars Amount £

wages for selling 18300

salary for marketing 25000

Sales staff commission 1200

Depreciation 6000

Total sales and distribution 50500

The above specified table is indicating that company has paid wages for selling to

workers. In addition to this, salary for marketing & commission to sales staff has been provided.

Depreciation has been charged on building & delivery van which is part of total sales and

distribution expenses.

Working note:

Depreciation for sales Amount £

Building 2500

Delivery van 3500

Total depreciation 6000

Administration expenses

There is need to coordinate the operational practices by ensuring significant level of

coordination (Lovrenčić Butković, Mihić and Sigmund, 2021). For this purpose the specific firm

executed administration expenses which leads to higher productive outcomes.

Particulars Amount £

salaries of administration workers 90800

Computer overhead 3000

Interest on loan 3000

Depreciation 6700

3

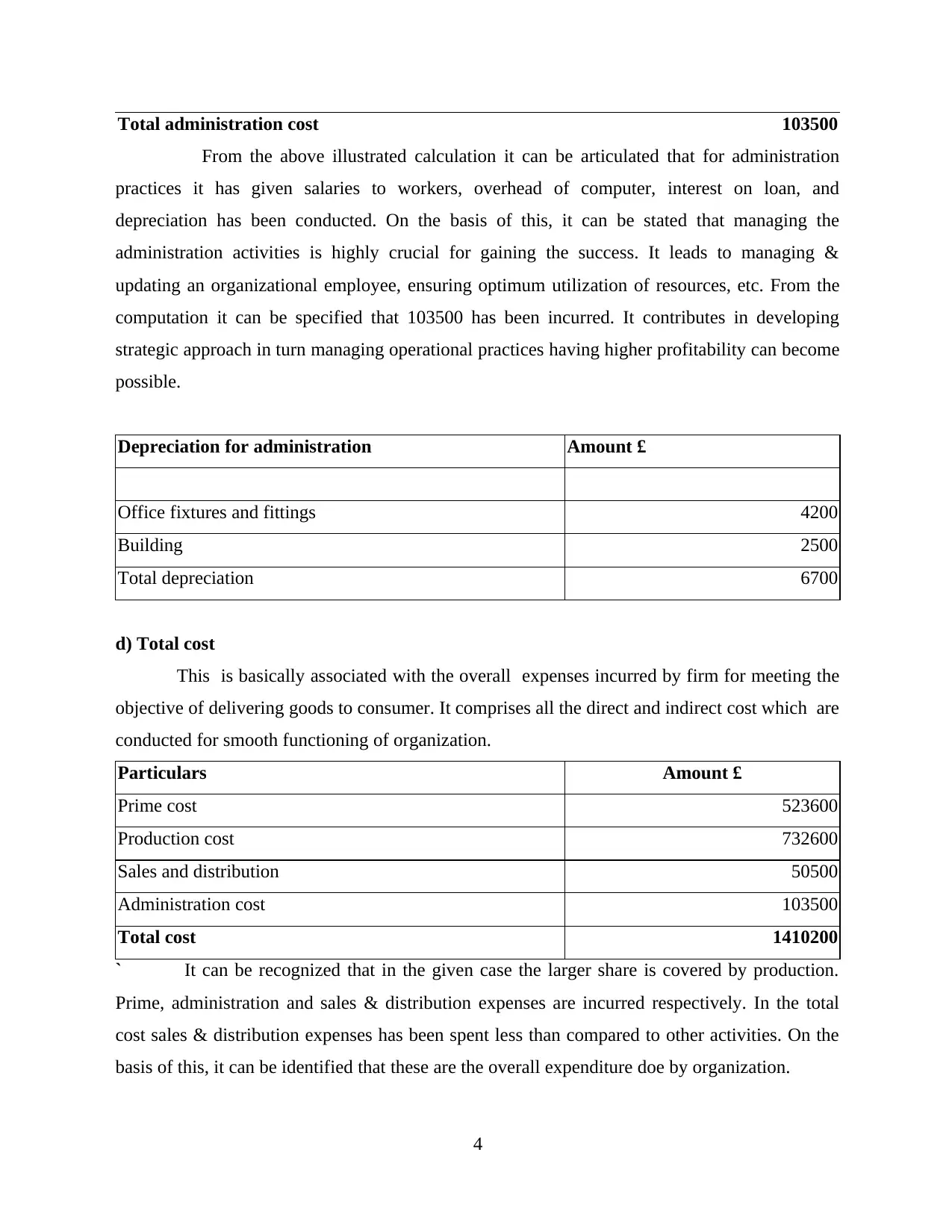

Total administration cost 103500

From the above illustrated calculation it can be articulated that for administration

practices it has given salaries to workers, overhead of computer, interest on loan, and

depreciation has been conducted. On the basis of this, it can be stated that managing the

administration activities is highly crucial for gaining the success. It leads to managing &

updating an organizational employee, ensuring optimum utilization of resources, etc. From the

computation it can be specified that 103500 has been incurred. It contributes in developing

strategic approach in turn managing operational practices having higher profitability can become

possible.

Depreciation for administration Amount £

Office fixtures and fittings 4200

Building 2500

Total depreciation 6700

d) Total cost

This is basically associated with the overall expenses incurred by firm for meeting the

objective of delivering goods to consumer. It comprises all the direct and indirect cost which are

conducted for smooth functioning of organization.

Particulars Amount £

Prime cost 523600

Production cost 732600

Sales and distribution 50500

Administration cost 103500

Total cost 1410200

` It can be recognized that in the given case the larger share is covered by production.

Prime, administration and sales & distribution expenses are incurred respectively. In the total

cost sales & distribution expenses has been spent less than compared to other activities. On the

basis of this, it can be identified that these are the overall expenditure doe by organization.

4

From the above illustrated calculation it can be articulated that for administration

practices it has given salaries to workers, overhead of computer, interest on loan, and

depreciation has been conducted. On the basis of this, it can be stated that managing the

administration activities is highly crucial for gaining the success. It leads to managing &

updating an organizational employee, ensuring optimum utilization of resources, etc. From the

computation it can be specified that 103500 has been incurred. It contributes in developing

strategic approach in turn managing operational practices having higher profitability can become

possible.

Depreciation for administration Amount £

Office fixtures and fittings 4200

Building 2500

Total depreciation 6700

d) Total cost

This is basically associated with the overall expenses incurred by firm for meeting the

objective of delivering goods to consumer. It comprises all the direct and indirect cost which are

conducted for smooth functioning of organization.

Particulars Amount £

Prime cost 523600

Production cost 732600

Sales and distribution 50500

Administration cost 103500

Total cost 1410200

` It can be recognized that in the given case the larger share is covered by production.

Prime, administration and sales & distribution expenses are incurred respectively. In the total

cost sales & distribution expenses has been spent less than compared to other activities. On the

basis of this, it can be identified that these are the overall expenditure doe by organization.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SECTION B

Question 4

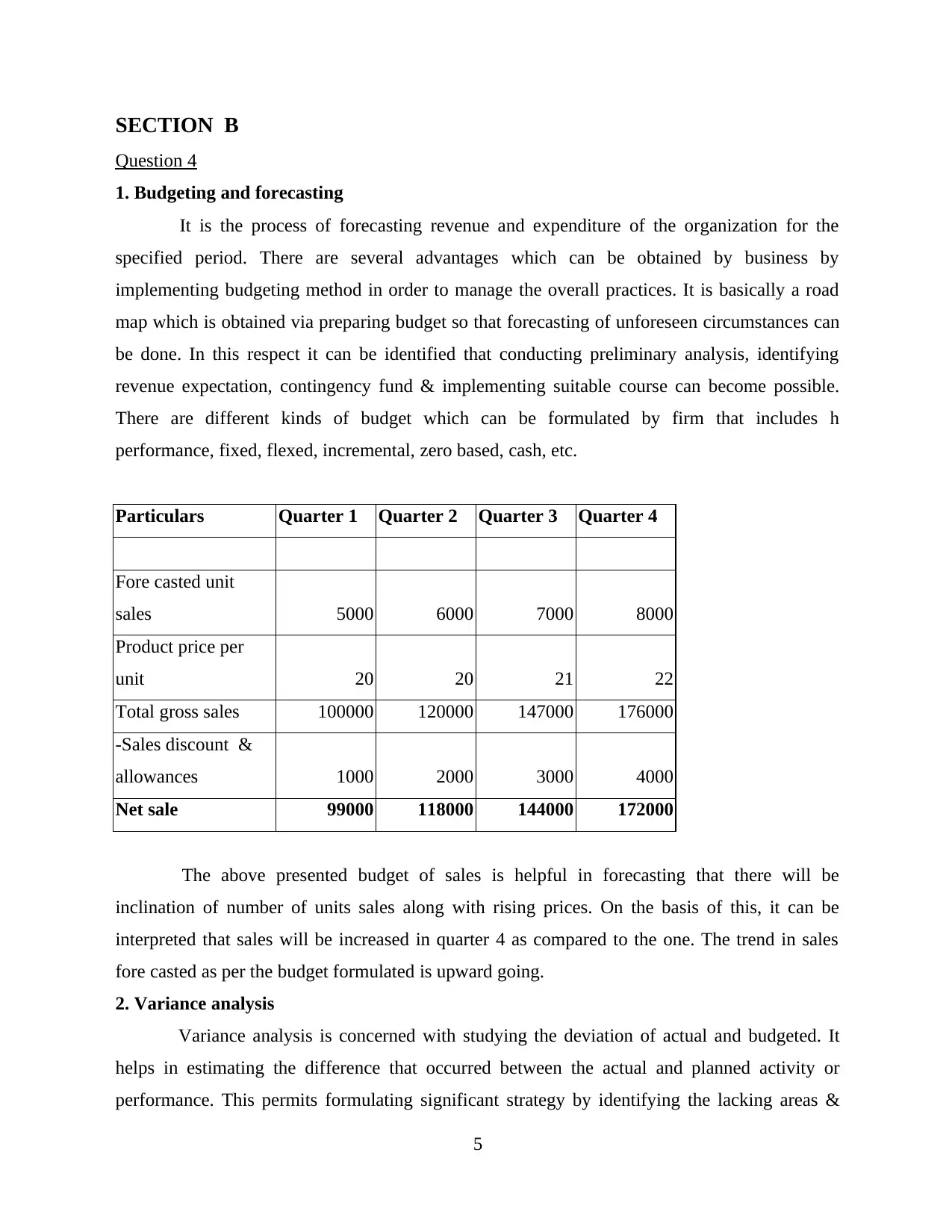

1. Budgeting and forecasting

It is the process of forecasting revenue and expenditure of the organization for the

specified period. There are several advantages which can be obtained by business by

implementing budgeting method in order to manage the overall practices. It is basically a road

map which is obtained via preparing budget so that forecasting of unforeseen circumstances can

be done. In this respect it can be identified that conducting preliminary analysis, identifying

revenue expectation, contingency fund & implementing suitable course can become possible.

There are different kinds of budget which can be formulated by firm that includes h

performance, fixed, flexed, incremental, zero based, cash, etc.

Particulars Quarter 1 Quarter 2 Quarter 3 Quarter 4

Fore casted unit

sales 5000 6000 7000 8000

Product price per

unit 20 20 21 22

Total gross sales 100000 120000 147000 176000

-Sales discount &

allowances 1000 2000 3000 4000

Net sale 99000 118000 144000 172000

The above presented budget of sales is helpful in forecasting that there will be

inclination of number of units sales along with rising prices. On the basis of this, it can be

interpreted that sales will be increased in quarter 4 as compared to the one. The trend in sales

fore casted as per the budget formulated is upward going.

2. Variance analysis

Variance analysis is concerned with studying the deviation of actual and budgeted. It

helps in estimating the difference that occurred between the actual and planned activity or

performance. This permits formulating significant strategy by identifying the lacking areas &

5

Question 4

1. Budgeting and forecasting

It is the process of forecasting revenue and expenditure of the organization for the

specified period. There are several advantages which can be obtained by business by

implementing budgeting method in order to manage the overall practices. It is basically a road

map which is obtained via preparing budget so that forecasting of unforeseen circumstances can

be done. In this respect it can be identified that conducting preliminary analysis, identifying

revenue expectation, contingency fund & implementing suitable course can become possible.

There are different kinds of budget which can be formulated by firm that includes h

performance, fixed, flexed, incremental, zero based, cash, etc.

Particulars Quarter 1 Quarter 2 Quarter 3 Quarter 4

Fore casted unit

sales 5000 6000 7000 8000

Product price per

unit 20 20 21 22

Total gross sales 100000 120000 147000 176000

-Sales discount &

allowances 1000 2000 3000 4000

Net sale 99000 118000 144000 172000

The above presented budget of sales is helpful in forecasting that there will be

inclination of number of units sales along with rising prices. On the basis of this, it can be

interpreted that sales will be increased in quarter 4 as compared to the one. The trend in sales

fore casted as per the budget formulated is upward going.

2. Variance analysis

Variance analysis is concerned with studying the deviation of actual and budgeted. It

helps in estimating the difference that occurred between the actual and planned activity or

performance. This permits formulating significant strategy by identifying the lacking areas &

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

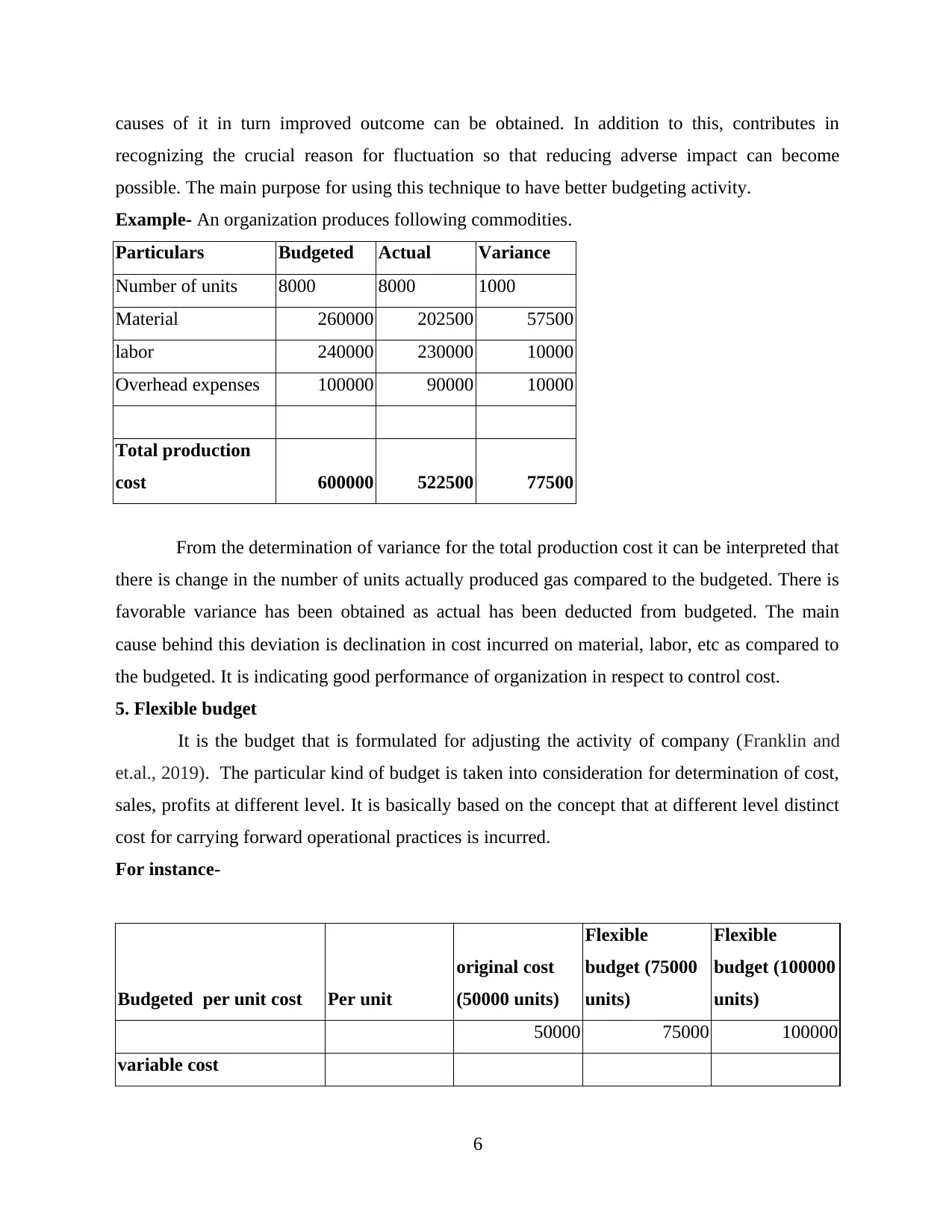

causes of it in turn improved outcome can be obtained. In addition to this, contributes in

recognizing the crucial reason for fluctuation so that reducing adverse impact can become

possible. The main purpose for using this technique to have better budgeting activity.

Example- An organization produces following commodities.

Particulars Budgeted Actual Variance

Number of units 8000 8000 1000

Material 260000 202500 57500

labor 240000 230000 10000

Overhead expenses 100000 90000 10000

Total production

cost 600000 522500 77500

From the determination of variance for the total production cost it can be interpreted that

there is change in the number of units actually produced gas compared to the budgeted. There is

favorable variance has been obtained as actual has been deducted from budgeted. The main

cause behind this deviation is declination in cost incurred on material, labor, etc as compared to

the budgeted. It is indicating good performance of organization in respect to control cost.

5. Flexible budget

It is the budget that is formulated for adjusting the activity of company (Franklin and

et.al., 2019). The particular kind of budget is taken into consideration for determination of cost,

sales, profits at different level. It is basically based on the concept that at different level distinct

cost for carrying forward operational practices is incurred.

For instance-

Budgeted per unit cost Per unit

original cost

(50000 units)

Flexible

budget (75000

units)

Flexible

budget (100000

units)

50000 75000 100000

variable cost

6

recognizing the crucial reason for fluctuation so that reducing adverse impact can become

possible. The main purpose for using this technique to have better budgeting activity.

Example- An organization produces following commodities.

Particulars Budgeted Actual Variance

Number of units 8000 8000 1000

Material 260000 202500 57500

labor 240000 230000 10000

Overhead expenses 100000 90000 10000

Total production

cost 600000 522500 77500

From the determination of variance for the total production cost it can be interpreted that

there is change in the number of units actually produced gas compared to the budgeted. There is

favorable variance has been obtained as actual has been deducted from budgeted. The main

cause behind this deviation is declination in cost incurred on material, labor, etc as compared to

the budgeted. It is indicating good performance of organization in respect to control cost.

5. Flexible budget

It is the budget that is formulated for adjusting the activity of company (Franklin and

et.al., 2019). The particular kind of budget is taken into consideration for determination of cost,

sales, profits at different level. It is basically based on the concept that at different level distinct

cost for carrying forward operational practices is incurred.

For instance-

Budgeted per unit cost Per unit

original cost

(50000 units)

Flexible

budget (75000

units)

Flexible

budget (100000

units)

50000 75000 100000

variable cost

6

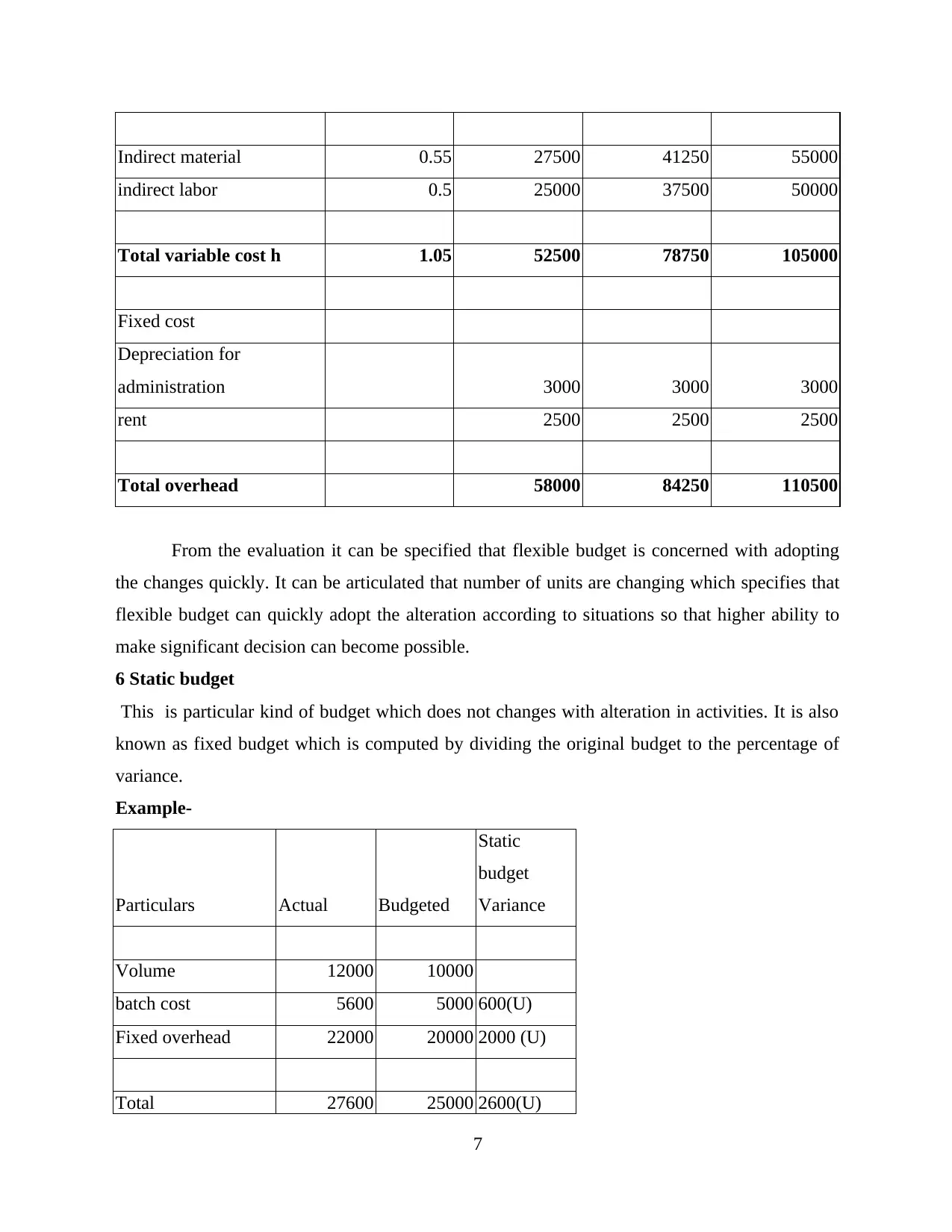

Indirect material 0.55 27500 41250 55000

indirect labor 0.5 25000 37500 50000

Total variable cost h 1.05 52500 78750 105000

Fixed cost

Depreciation for

administration 3000 3000 3000

rent 2500 2500 2500

Total overhead 58000 84250 110500

From the evaluation it can be specified that flexible budget is concerned with adopting

the changes quickly. It can be articulated that number of units are changing which specifies that

flexible budget can quickly adopt the alteration according to situations so that higher ability to

make significant decision can become possible.

6 Static budget

This is particular kind of budget which does not changes with alteration in activities. It is also

known as fixed budget which is computed by dividing the original budget to the percentage of

variance.

Example-

Particulars Actual Budgeted

Static

budget

Variance

Volume 12000 10000

batch cost 5600 5000 600(U)

Fixed overhead 22000 20000 2000 (U)

Total 27600 25000 2600(U)

7

indirect labor 0.5 25000 37500 50000

Total variable cost h 1.05 52500 78750 105000

Fixed cost

Depreciation for

administration 3000 3000 3000

rent 2500 2500 2500

Total overhead 58000 84250 110500

From the evaluation it can be specified that flexible budget is concerned with adopting

the changes quickly. It can be articulated that number of units are changing which specifies that

flexible budget can quickly adopt the alteration according to situations so that higher ability to

make significant decision can become possible.

6 Static budget

This is particular kind of budget which does not changes with alteration in activities. It is also

known as fixed budget which is computed by dividing the original budget to the percentage of

variance.

Example-

Particulars Actual Budgeted

Static

budget

Variance

Volume 12000 10000

batch cost 5600 5000 600(U)

Fixed overhead 22000 20000 2000 (U)

Total 27600 25000 2600(U)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

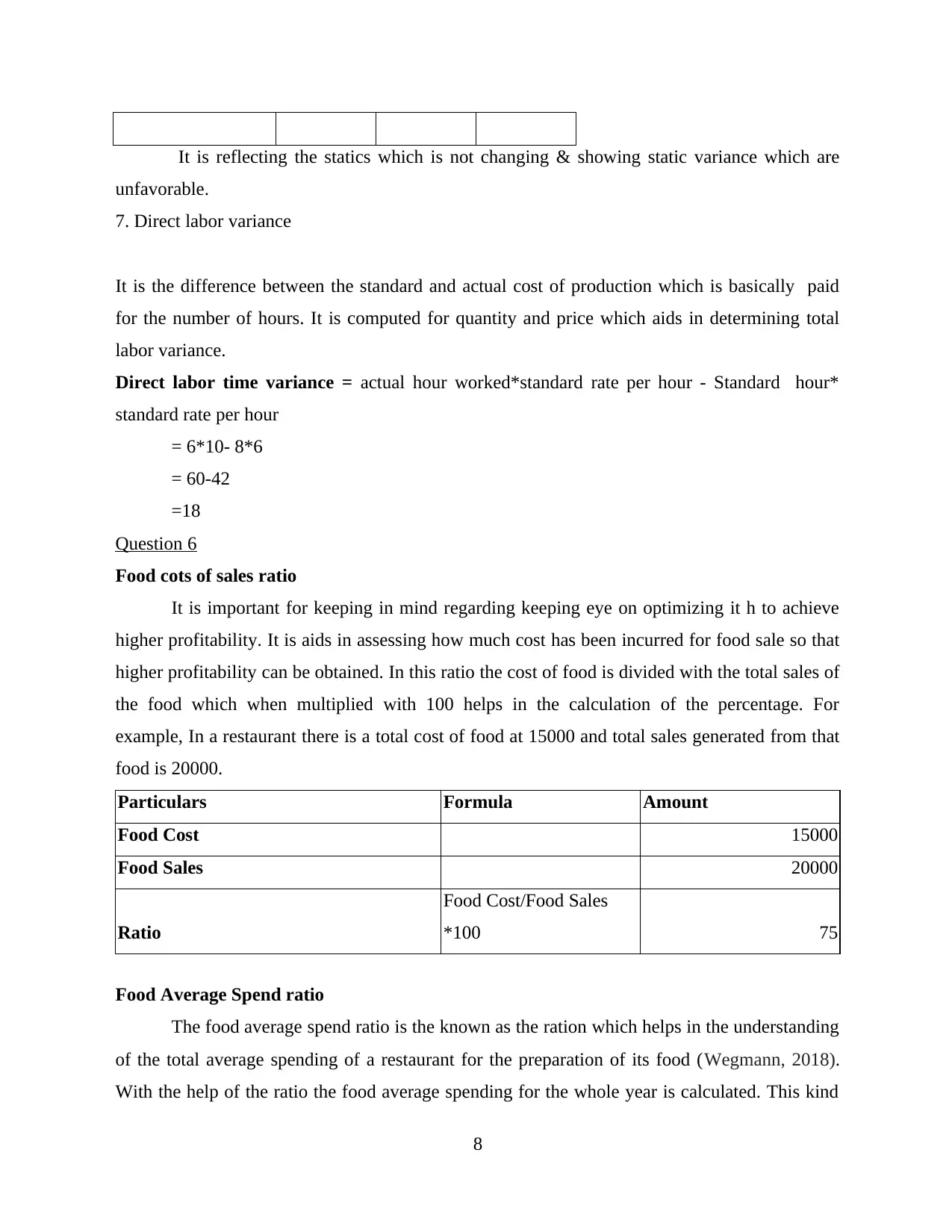

It is reflecting the statics which is not changing & showing static variance which are

unfavorable.

7. Direct labor variance

It is the difference between the standard and actual cost of production which is basically paid

for the number of hours. It is computed for quantity and price which aids in determining total

labor variance.

Direct labor time variance = actual hour worked*standard rate per hour - Standard hour*

standard rate per hour

= 6*10- 8*6

= 60-42

=18

Question 6

Food cots of sales ratio

It is important for keeping in mind regarding keeping eye on optimizing it h to achieve

higher profitability. It is aids in assessing how much cost has been incurred for food sale so that

higher profitability can be obtained. In this ratio the cost of food is divided with the total sales of

the food which when multiplied with 100 helps in the calculation of the percentage. For

example, In a restaurant there is a total cost of food at 15000 and total sales generated from that

food is 20000.

Particulars Formula Amount

Food Cost 15000

Food Sales 20000

Ratio

Food Cost/Food Sales

*100 75

Food Average Spend ratio

The food average spend ratio is the known as the ration which helps in the understanding

of the total average spending of a restaurant for the preparation of its food (Wegmann, 2018).

With the help of the ratio the food average spending for the whole year is calculated. This kind

8

unfavorable.

7. Direct labor variance

It is the difference between the standard and actual cost of production which is basically paid

for the number of hours. It is computed for quantity and price which aids in determining total

labor variance.

Direct labor time variance = actual hour worked*standard rate per hour - Standard hour*

standard rate per hour

= 6*10- 8*6

= 60-42

=18

Question 6

Food cots of sales ratio

It is important for keeping in mind regarding keeping eye on optimizing it h to achieve

higher profitability. It is aids in assessing how much cost has been incurred for food sale so that

higher profitability can be obtained. In this ratio the cost of food is divided with the total sales of

the food which when multiplied with 100 helps in the calculation of the percentage. For

example, In a restaurant there is a total cost of food at 15000 and total sales generated from that

food is 20000.

Particulars Formula Amount

Food Cost 15000

Food Sales 20000

Ratio

Food Cost/Food Sales

*100 75

Food Average Spend ratio

The food average spend ratio is the known as the ration which helps in the understanding

of the total average spending of a restaurant for the preparation of its food (Wegmann, 2018).

With the help of the ratio the food average spending for the whole year is calculated. This kind

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

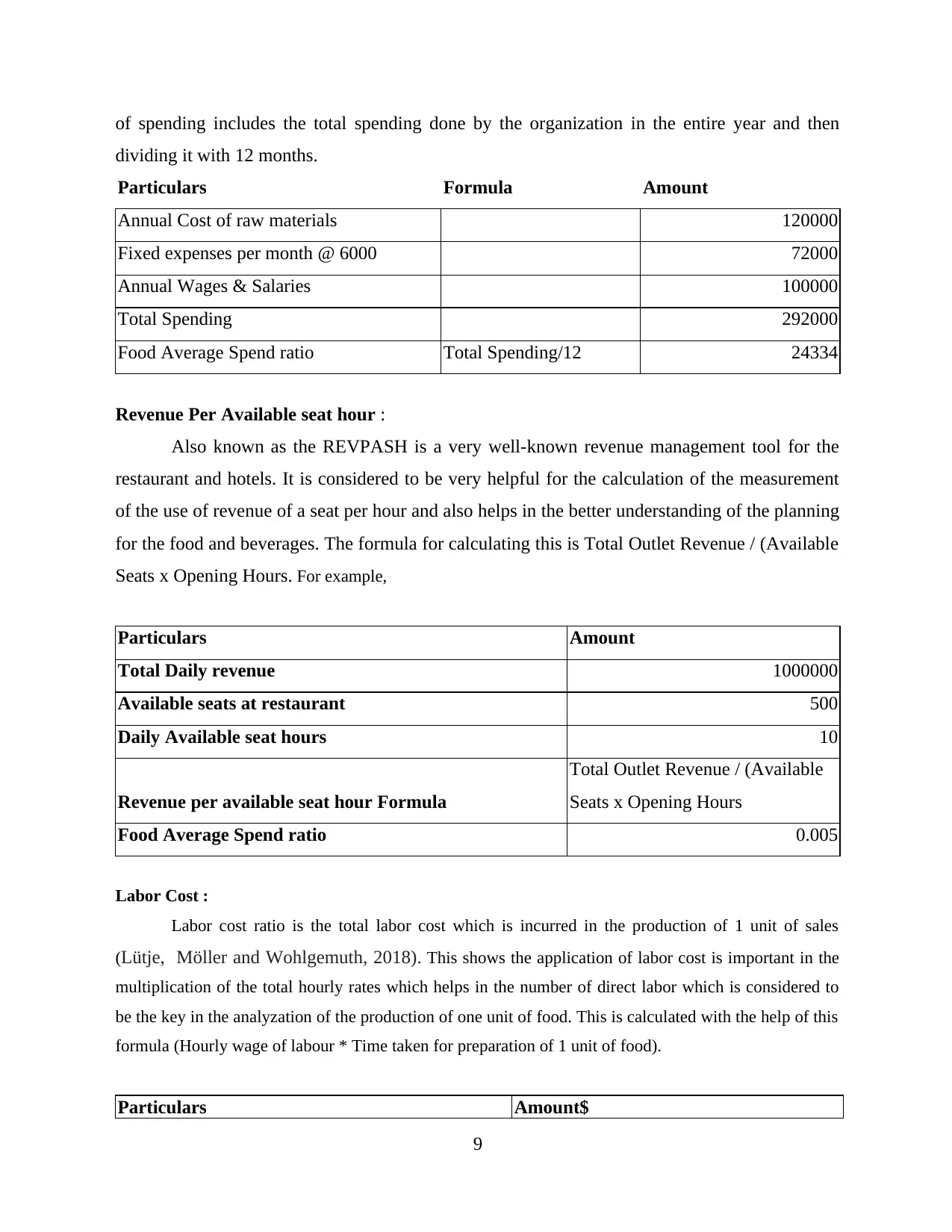

of spending includes the total spending done by the organization in the entire year and then

dividing it with 12 months.

Particulars Formula Amount

Annual Cost of raw materials 120000

Fixed expenses per month @ 6000 72000

Annual Wages & Salaries 100000

Total Spending 292000

Food Average Spend ratio Total Spending/12 24334

Revenue Per Available seat hour :

Also known as the REVPASH is a very well-known revenue management tool for the

restaurant and hotels. It is considered to be very helpful for the calculation of the measurement

of the use of revenue of a seat per hour and also helps in the better understanding of the planning

for the food and beverages. The formula for calculating this is Total Outlet Revenue / (Available

Seats x Opening Hours. For example,

Particulars Amount

Total Daily revenue 1000000

Available seats at restaurant 500

Daily Available seat hours 10

Revenue per available seat hour Formula

Total Outlet Revenue / (Available

Seats x Opening Hours

Food Average Spend ratio 0.005

Labor Cost :

Labor cost ratio is the total labor cost which is incurred in the production of 1 unit of sales

(Lütje, Möller and Wohlgemuth, 2018). This shows the application of labor cost is important in the

multiplication of the total hourly rates which helps in the number of direct labor which is considered to

be the key in the analyzation of the production of one unit of food. This is calculated with the help of this

formula (Hourly wage of labour * Time taken for preparation of 1 unit of food).

Particulars Amount$

9

dividing it with 12 months.

Particulars Formula Amount

Annual Cost of raw materials 120000

Fixed expenses per month @ 6000 72000

Annual Wages & Salaries 100000

Total Spending 292000

Food Average Spend ratio Total Spending/12 24334

Revenue Per Available seat hour :

Also known as the REVPASH is a very well-known revenue management tool for the

restaurant and hotels. It is considered to be very helpful for the calculation of the measurement

of the use of revenue of a seat per hour and also helps in the better understanding of the planning

for the food and beverages. The formula for calculating this is Total Outlet Revenue / (Available

Seats x Opening Hours. For example,

Particulars Amount

Total Daily revenue 1000000

Available seats at restaurant 500

Daily Available seat hours 10

Revenue per available seat hour Formula

Total Outlet Revenue / (Available

Seats x Opening Hours

Food Average Spend ratio 0.005

Labor Cost :

Labor cost ratio is the total labor cost which is incurred in the production of 1 unit of sales

(Lütje, Möller and Wohlgemuth, 2018). This shows the application of labor cost is important in the

multiplication of the total hourly rates which helps in the number of direct labor which is considered to

be the key in the analyzation of the production of one unit of food. This is calculated with the help of this

formula (Hourly wage of labour * Time taken for preparation of 1 unit of food).

Particulars Amount$

9

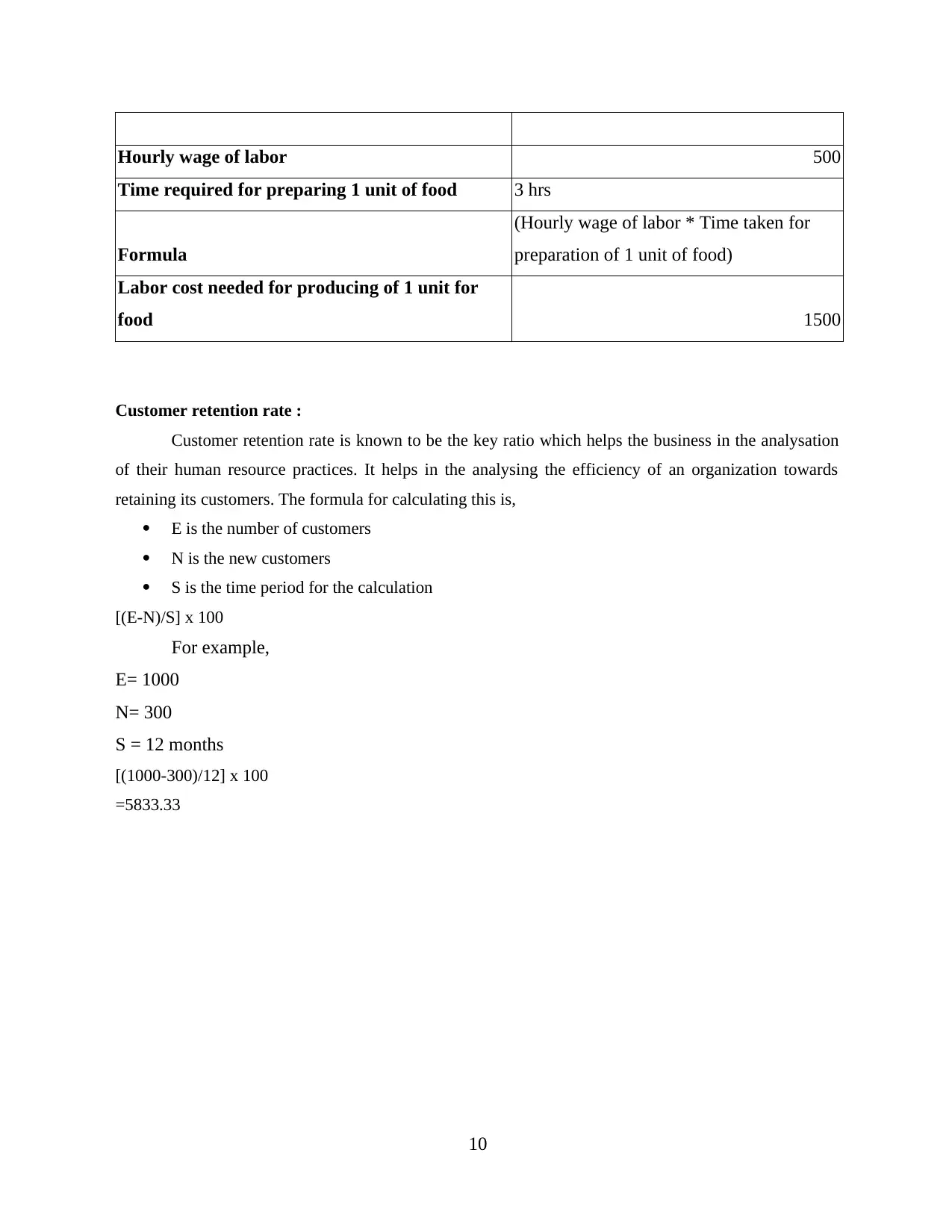

Hourly wage of labor 500

Time required for preparing 1 unit of food 3 hrs

Formula

(Hourly wage of labor * Time taken for

preparation of 1 unit of food)

Labor cost needed for producing of 1 unit for

food 1500

Customer retention rate :

Customer retention rate is known to be the key ratio which helps the business in the analysation

of their human resource practices. It helps in the analysing the efficiency of an organization towards

retaining its customers. The formula for calculating this is,

E is the number of customers

N is the new customers

S is the time period for the calculation

[(E-N)/S] x 100

For example,

E= 1000

N= 300

S = 12 months

[(1000-300)/12] x 100

=5833.33

10

Time required for preparing 1 unit of food 3 hrs

Formula

(Hourly wage of labor * Time taken for

preparation of 1 unit of food)

Labor cost needed for producing of 1 unit for

food 1500

Customer retention rate :

Customer retention rate is known to be the key ratio which helps the business in the analysation

of their human resource practices. It helps in the analysing the efficiency of an organization towards

retaining its customers. The formula for calculating this is,

E is the number of customers

N is the new customers

S is the time period for the calculation

[(E-N)/S] x 100

For example,

E= 1000

N= 300

S = 12 months

[(1000-300)/12] x 100

=5833.33

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.