Analyzing Costs, Budgeting, and Financial Resource Management

VerifiedAdded on 2023/06/15

|13

|2691

|189

Report

AI Summary

This report provides a comprehensive analysis of financial resource management, covering various costing methods, budgeting techniques, and performance metrics. It begins with a detailed breakdown of prime cost, production cost, sales and distribution cost, and administration expenses, calculating total costs for an organization. The report then delves into budgeting and forecasting, variance analysis (including adverse variance), and flexible versus static budgets. Furthermore, it explores key performance indicators (KPIs) such as Average Daily Rate (ADR), Revenue per Available Room (RevPAR), Average Rate Index (ARI), and Market Penetration Index (MPI), demonstrating their application with examples. The report emphasizes the importance of these financial tools in achieving organizational objectives, controlling costs, and improving profitability. Desklib provides students access to this and other solved assignments.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

SECTION A.....................................................................................................................................3

QUESTION 1...................................................................................................................................3

a) Prime cost ...............................................................................................................................3

b) Production cost.......................................................................................................................3

c)..................................................................................................................................................4

Sales & Distribution cost............................................................................................................4

Administration expenses.............................................................................................................4

d) Total cost.................................................................................................................................5

SECTION B.....................................................................................................................................6

QUESTION 4...................................................................................................................................6

1 Budgeting & forecasting..........................................................................................................6

2 Variance Analysis....................................................................................................................6

3 Adverse variance......................................................................................................................7

5 Flexible Budget........................................................................................................................7

6 Static budget ............................................................................................................................8

QUESTION 5...................................................................................................................................8

1 Average daily rate (ADR)........................................................................................................8

2 Revenue per available room (RevPAR)...................................................................................9

5 Average rate index (ARI).........................................................................................................9

6 Market Penetration index (MPI)............................................................................................10

7 Customer satisfaction.............................................................................................................10

REFERENCES..............................................................................................................................11

SECTION A.....................................................................................................................................3

QUESTION 1...................................................................................................................................3

a) Prime cost ...............................................................................................................................3

b) Production cost.......................................................................................................................3

c)..................................................................................................................................................4

Sales & Distribution cost............................................................................................................4

Administration expenses.............................................................................................................4

d) Total cost.................................................................................................................................5

SECTION B.....................................................................................................................................6

QUESTION 4...................................................................................................................................6

1 Budgeting & forecasting..........................................................................................................6

2 Variance Analysis....................................................................................................................6

3 Adverse variance......................................................................................................................7

5 Flexible Budget........................................................................................................................7

6 Static budget ............................................................................................................................8

QUESTION 5...................................................................................................................................8

1 Average daily rate (ADR)........................................................................................................8

2 Revenue per available room (RevPAR)...................................................................................9

5 Average rate index (ARI).........................................................................................................9

6 Market Penetration index (MPI)............................................................................................10

7 Customer satisfaction.............................................................................................................10

REFERENCES..............................................................................................................................11

SECTION A

QUESTION 1

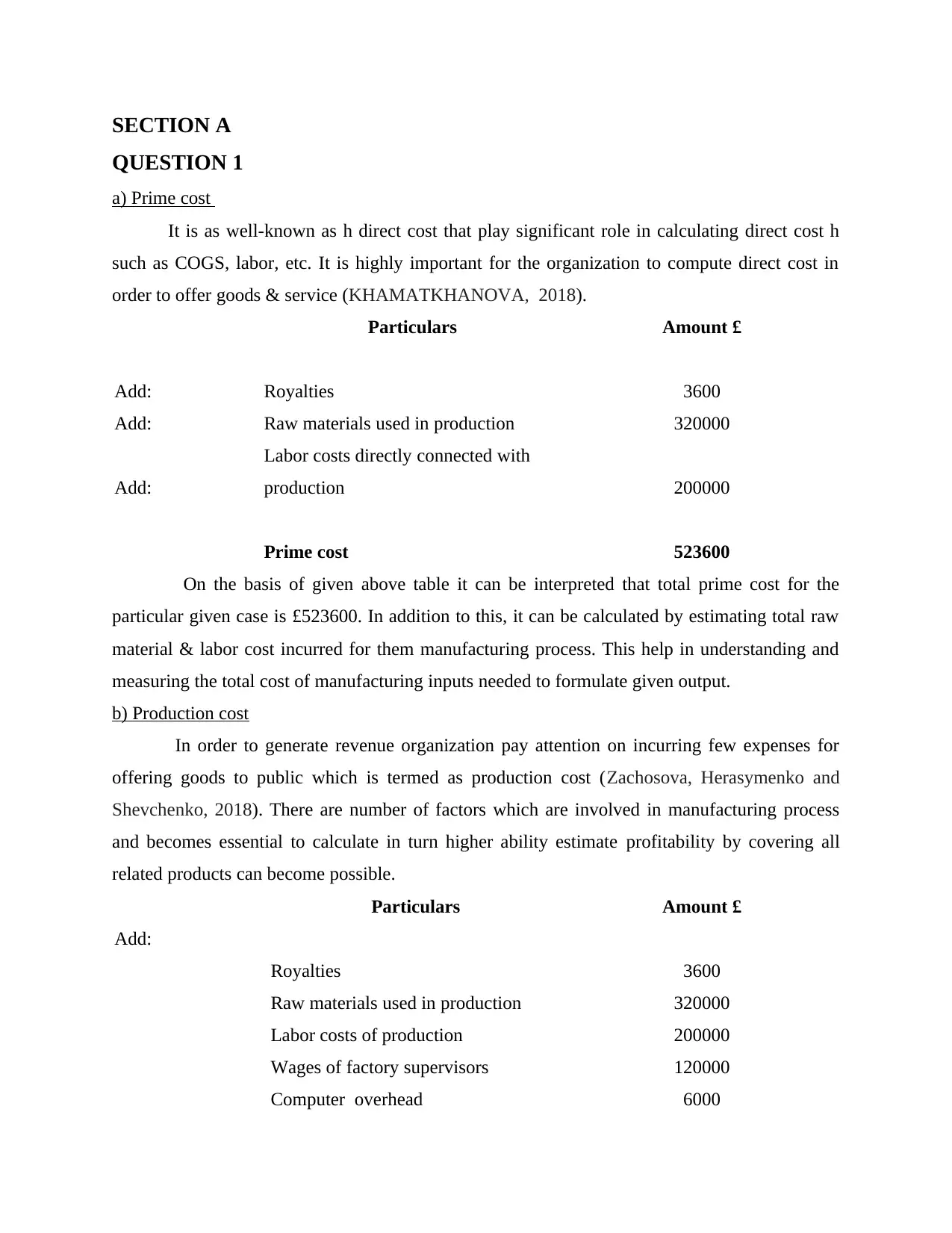

a) Prime cost

It is as well-known as h direct cost that play significant role in calculating direct cost h

such as COGS, labor, etc. It is highly important for the organization to compute direct cost in

order to offer goods & service (KHAMATKHANOVA, 2018).

Particulars Amount £

Add: Royalties 3600

Add: Raw materials used in production 320000

Add:

Labor costs directly connected with

production 200000

Prime cost 523600

On the basis of given above table it can be interpreted that total prime cost for the

particular given case is £523600. In addition to this, it can be calculated by estimating total raw

material & labor cost incurred for them manufacturing process. This help in understanding and

measuring the total cost of manufacturing inputs needed to formulate given output.

b) Production cost

In order to generate revenue organization pay attention on incurring few expenses for

offering goods to public which is termed as production cost (Zachosova, Herasymenko and

Shevchenko, 2018). There are number of factors which are involved in manufacturing process

and becomes essential to calculate in turn higher ability estimate profitability by covering all

related products can become possible.

Particulars Amount £

Add:

Royalties 3600

Raw materials used in production 320000

Labor costs of production 200000

Wages of factory supervisors 120000

Computer overhead 6000

QUESTION 1

a) Prime cost

It is as well-known as h direct cost that play significant role in calculating direct cost h

such as COGS, labor, etc. It is highly important for the organization to compute direct cost in

order to offer goods & service (KHAMATKHANOVA, 2018).

Particulars Amount £

Add: Royalties 3600

Add: Raw materials used in production 320000

Add:

Labor costs directly connected with

production 200000

Prime cost 523600

On the basis of given above table it can be interpreted that total prime cost for the

particular given case is £523600. In addition to this, it can be calculated by estimating total raw

material & labor cost incurred for them manufacturing process. This help in understanding and

measuring the total cost of manufacturing inputs needed to formulate given output.

b) Production cost

In order to generate revenue organization pay attention on incurring few expenses for

offering goods to public which is termed as production cost (Zachosova, Herasymenko and

Shevchenko, 2018). There are number of factors which are involved in manufacturing process

and becomes essential to calculate in turn higher ability estimate profitability by covering all

related products can become possible.

Particulars Amount £

Add:

Royalties 3600

Raw materials used in production 320000

Labor costs of production 200000

Wages of factory supervisors 120000

Computer overhead 6000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

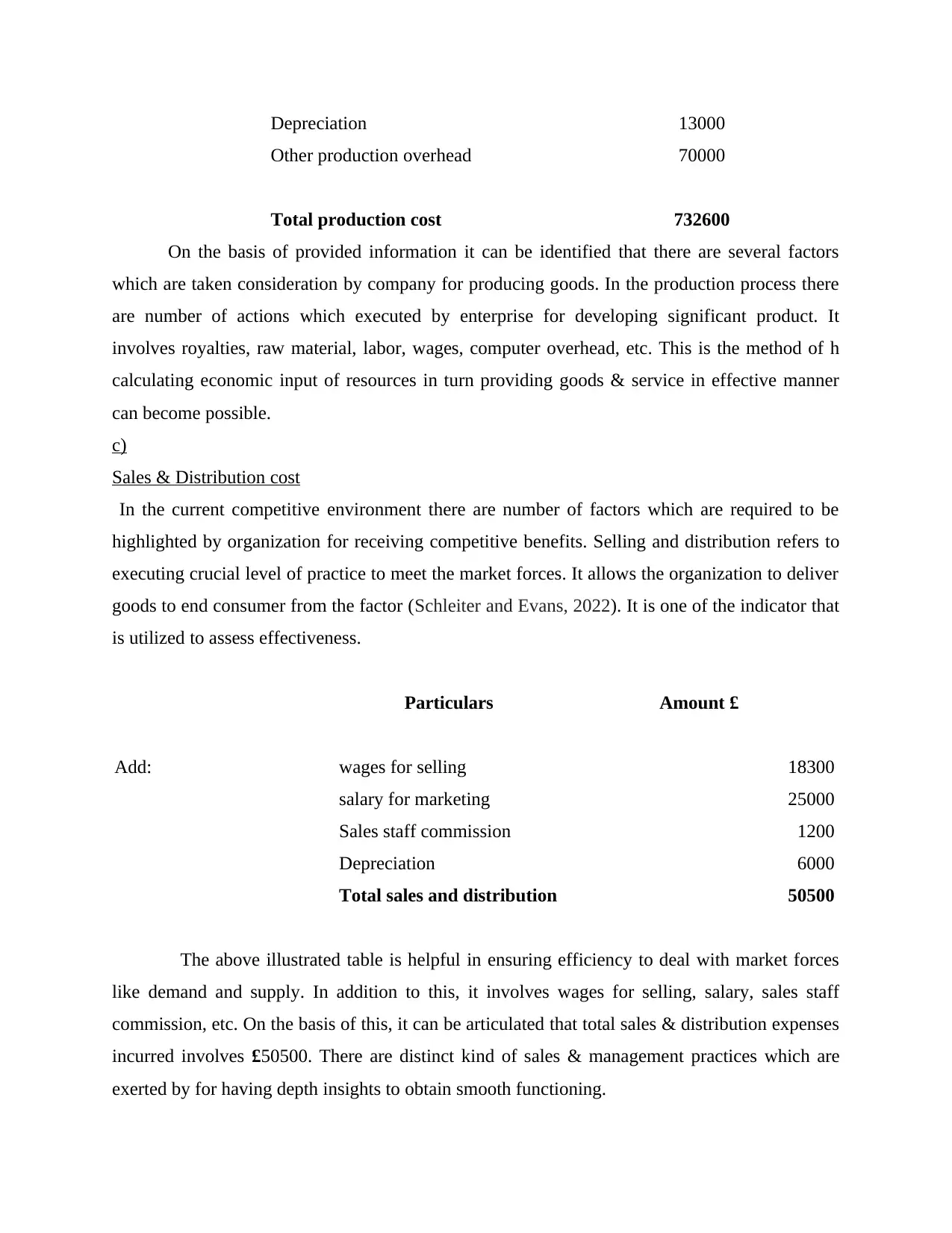

Depreciation 13000

Other production overhead 70000

Total production cost 732600

On the basis of provided information it can be identified that there are several factors

which are taken consideration by company for producing goods. In the production process there

are number of actions which executed by enterprise for developing significant product. It

involves royalties, raw material, labor, wages, computer overhead, etc. This is the method of h

calculating economic input of resources in turn providing goods & service in effective manner

can become possible.

c)

Sales & Distribution cost

In the current competitive environment there are number of factors which are required to be

highlighted by organization for receiving competitive benefits. Selling and distribution refers to

executing crucial level of practice to meet the market forces. It allows the organization to deliver

goods to end consumer from the factor (Schleiter and Evans, 2022). It is one of the indicator that

is utilized to assess effectiveness.

Particulars Amount £

Add: wages for selling 18300

salary for marketing 25000

Sales staff commission 1200

Depreciation 6000

Total sales and distribution 50500

The above illustrated table is helpful in ensuring efficiency to deal with market forces

like demand and supply. In addition to this, it involves wages for selling, salary, sales staff

commission, etc. On the basis of this, it can be articulated that total sales & distribution expenses

incurred involves £50500. There are distinct kind of sales & management practices which are

exerted by for having depth insights to obtain smooth functioning.

Other production overhead 70000

Total production cost 732600

On the basis of provided information it can be identified that there are several factors

which are taken consideration by company for producing goods. In the production process there

are number of actions which executed by enterprise for developing significant product. It

involves royalties, raw material, labor, wages, computer overhead, etc. This is the method of h

calculating economic input of resources in turn providing goods & service in effective manner

can become possible.

c)

Sales & Distribution cost

In the current competitive environment there are number of factors which are required to be

highlighted by organization for receiving competitive benefits. Selling and distribution refers to

executing crucial level of practice to meet the market forces. It allows the organization to deliver

goods to end consumer from the factor (Schleiter and Evans, 2022). It is one of the indicator that

is utilized to assess effectiveness.

Particulars Amount £

Add: wages for selling 18300

salary for marketing 25000

Sales staff commission 1200

Depreciation 6000

Total sales and distribution 50500

The above illustrated table is helpful in ensuring efficiency to deal with market forces

like demand and supply. In addition to this, it involves wages for selling, salary, sales staff

commission, etc. On the basis of this, it can be articulated that total sales & distribution expenses

incurred involves £50500. There are distinct kind of sales & management practices which are

exerted by for having depth insights to obtain smooth functioning.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

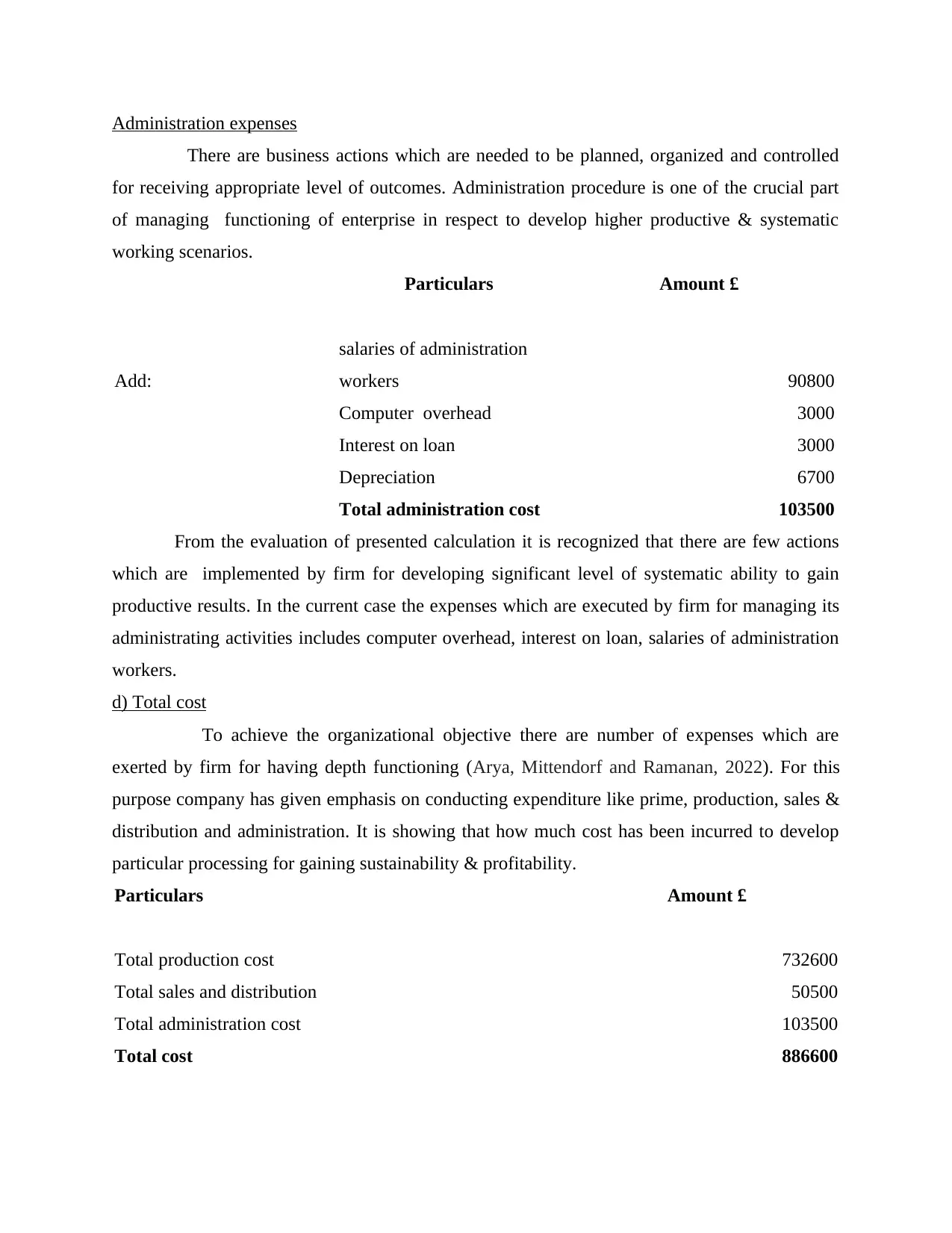

Administration expenses

There are business actions which are needed to be planned, organized and controlled

for receiving appropriate level of outcomes. Administration procedure is one of the crucial part

of managing functioning of enterprise in respect to develop higher productive & systematic

working scenarios.

Particulars Amount £

Add:

salaries of administration

workers 90800

Computer overhead 3000

Interest on loan 3000

Depreciation 6700

Total administration cost 103500

From the evaluation of presented calculation it is recognized that there are few actions

which are implemented by firm for developing significant level of systematic ability to gain

productive results. In the current case the expenses which are executed by firm for managing its

administrating activities includes computer overhead, interest on loan, salaries of administration

workers.

d) Total cost

To achieve the organizational objective there are number of expenses which are

exerted by firm for having depth functioning (Arya, Mittendorf and Ramanan, 2022). For this

purpose company has given emphasis on conducting expenditure like prime, production, sales &

distribution and administration. It is showing that how much cost has been incurred to develop

particular processing for gaining sustainability & profitability.

Particulars Amount £

Total production cost 732600

Total sales and distribution 50500

Total administration cost 103500

Total cost 886600

There are business actions which are needed to be planned, organized and controlled

for receiving appropriate level of outcomes. Administration procedure is one of the crucial part

of managing functioning of enterprise in respect to develop higher productive & systematic

working scenarios.

Particulars Amount £

Add:

salaries of administration

workers 90800

Computer overhead 3000

Interest on loan 3000

Depreciation 6700

Total administration cost 103500

From the evaluation of presented calculation it is recognized that there are few actions

which are implemented by firm for developing significant level of systematic ability to gain

productive results. In the current case the expenses which are executed by firm for managing its

administrating activities includes computer overhead, interest on loan, salaries of administration

workers.

d) Total cost

To achieve the organizational objective there are number of expenses which are

exerted by firm for having depth functioning (Arya, Mittendorf and Ramanan, 2022). For this

purpose company has given emphasis on conducting expenditure like prime, production, sales &

distribution and administration. It is showing that how much cost has been incurred to develop

particular processing for gaining sustainability & profitability.

Particulars Amount £

Total production cost 732600

Total sales and distribution 50500

Total administration cost 103500

Total cost 886600

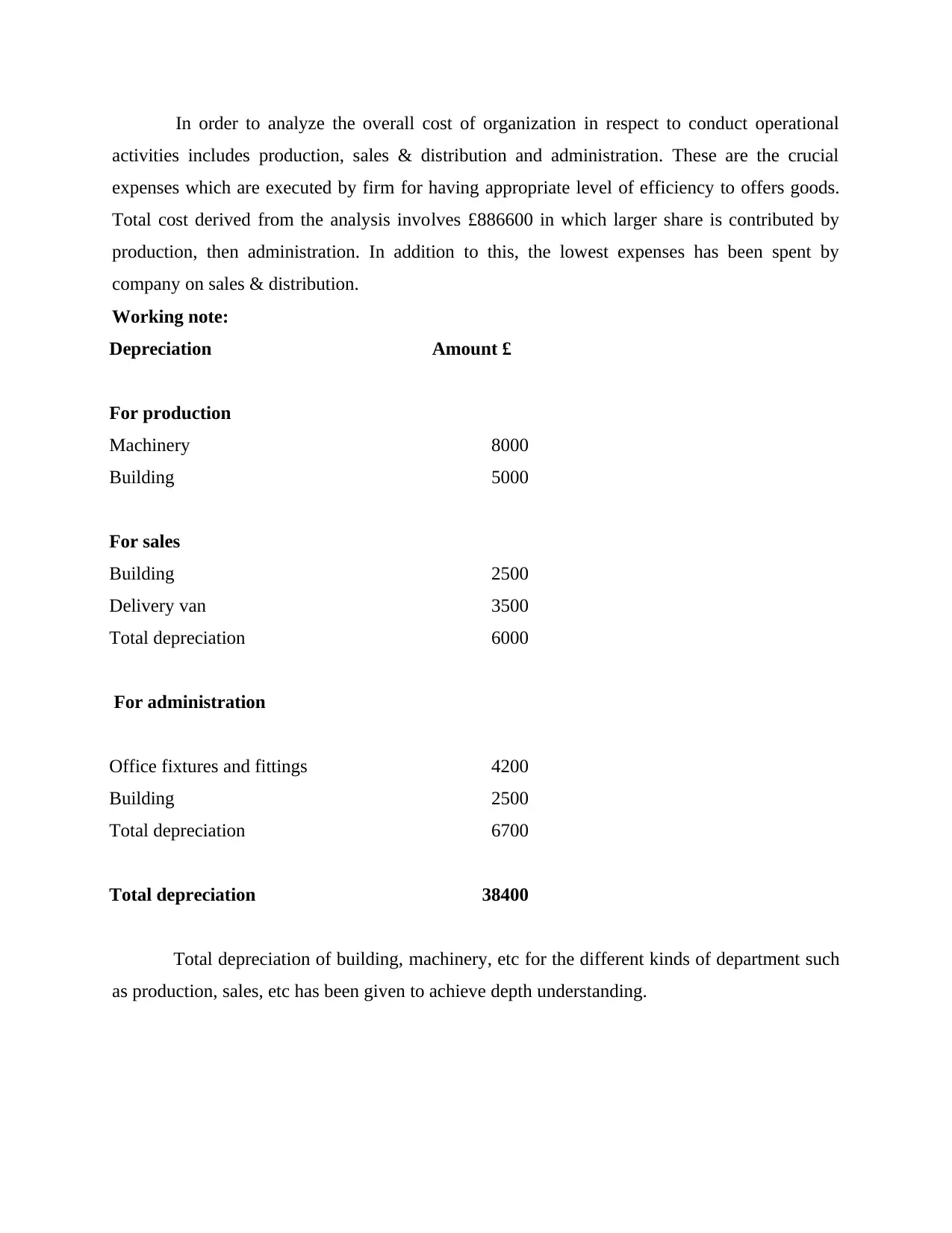

In order to analyze the overall cost of organization in respect to conduct operational

activities includes production, sales & distribution and administration. These are the crucial

expenses which are executed by firm for having appropriate level of efficiency to offers goods.

Total cost derived from the analysis involves £886600 in which larger share is contributed by

production, then administration. In addition to this, the lowest expenses has been spent by

company on sales & distribution.

Working note:

Depreciation Amount £

For production

Machinery 8000

Building 5000

For sales

Building 2500

Delivery van 3500

Total depreciation 6000

For administration

Office fixtures and fittings 4200

Building 2500

Total depreciation 6700

Total depreciation 38400

Total depreciation of building, machinery, etc for the different kinds of department such

as production, sales, etc has been given to achieve depth understanding.

activities includes production, sales & distribution and administration. These are the crucial

expenses which are executed by firm for having appropriate level of efficiency to offers goods.

Total cost derived from the analysis involves £886600 in which larger share is contributed by

production, then administration. In addition to this, the lowest expenses has been spent by

company on sales & distribution.

Working note:

Depreciation Amount £

For production

Machinery 8000

Building 5000

For sales

Building 2500

Delivery van 3500

Total depreciation 6000

For administration

Office fixtures and fittings 4200

Building 2500

Total depreciation 6700

Total depreciation 38400

Total depreciation of building, machinery, etc for the different kinds of department such

as production, sales, etc has been given to achieve depth understanding.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SECTION B

QUESTION 4

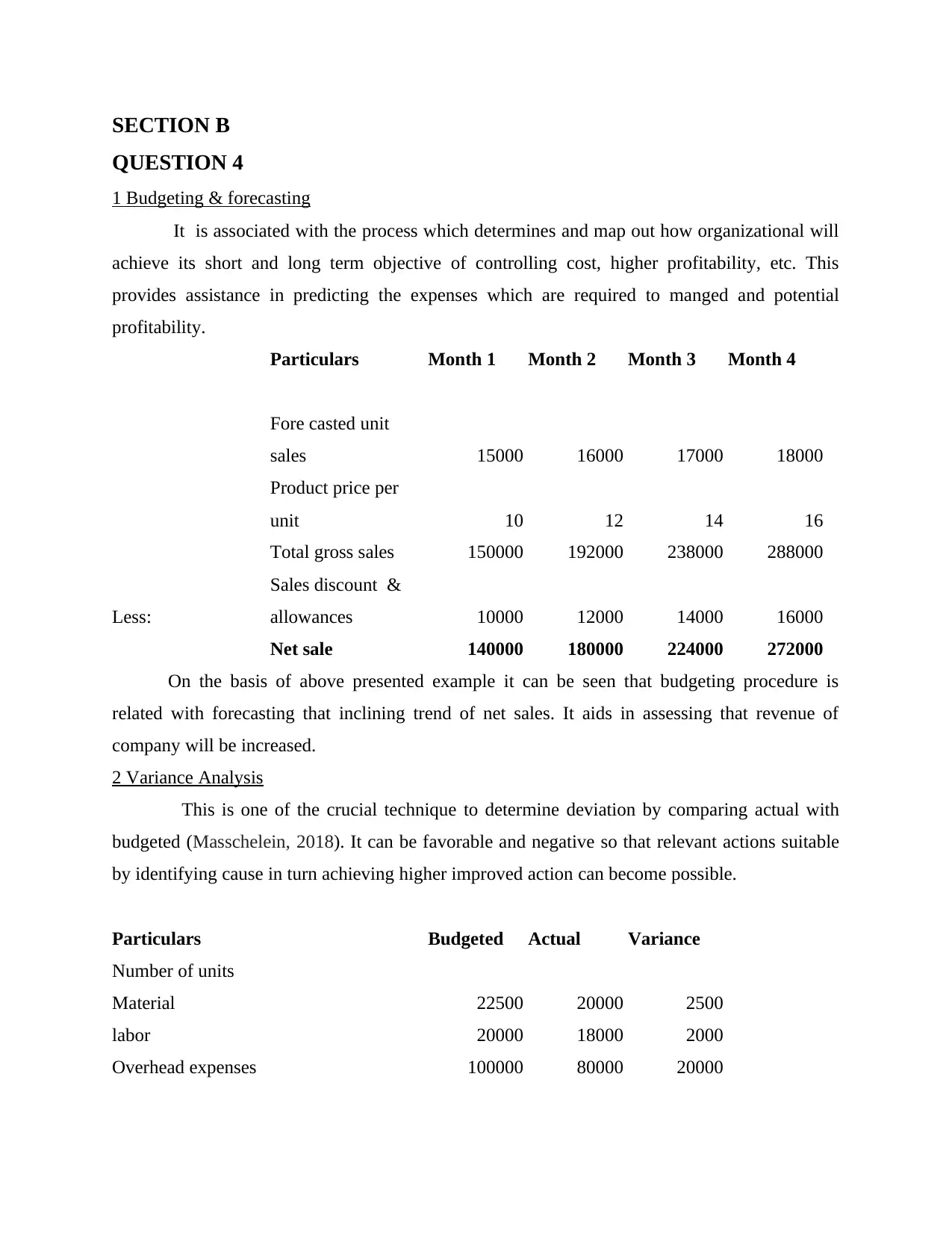

1 Budgeting & forecasting

It is associated with the process which determines and map out how organizational will

achieve its short and long term objective of controlling cost, higher profitability, etc. This

provides assistance in predicting the expenses which are required to manged and potential

profitability.

Particulars Month 1 Month 2 Month 3 Month 4

Fore casted unit

sales 15000 16000 17000 18000

Product price per

unit 10 12 14 16

Total gross sales 150000 192000 238000 288000

Less:

Sales discount &

allowances 10000 12000 14000 16000

Net sale 140000 180000 224000 272000

On the basis of above presented example it can be seen that budgeting procedure is

related with forecasting that inclining trend of net sales. It aids in assessing that revenue of

company will be increased.

2 Variance Analysis

This is one of the crucial technique to determine deviation by comparing actual with

budgeted (Masschelein, 2018). It can be favorable and negative so that relevant actions suitable

by identifying cause in turn achieving higher improved action can become possible.

Particulars Budgeted Actual Variance

Number of units

Material 22500 20000 2500

labor 20000 18000 2000

Overhead expenses 100000 80000 20000

QUESTION 4

1 Budgeting & forecasting

It is associated with the process which determines and map out how organizational will

achieve its short and long term objective of controlling cost, higher profitability, etc. This

provides assistance in predicting the expenses which are required to manged and potential

profitability.

Particulars Month 1 Month 2 Month 3 Month 4

Fore casted unit

sales 15000 16000 17000 18000

Product price per

unit 10 12 14 16

Total gross sales 150000 192000 238000 288000

Less:

Sales discount &

allowances 10000 12000 14000 16000

Net sale 140000 180000 224000 272000

On the basis of above presented example it can be seen that budgeting procedure is

related with forecasting that inclining trend of net sales. It aids in assessing that revenue of

company will be increased.

2 Variance Analysis

This is one of the crucial technique to determine deviation by comparing actual with

budgeted (Masschelein, 2018). It can be favorable and negative so that relevant actions suitable

by identifying cause in turn achieving higher improved action can become possible.

Particulars Budgeted Actual Variance

Number of units

Material 22500 20000 2500

labor 20000 18000 2000

Overhead expenses 100000 80000 20000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

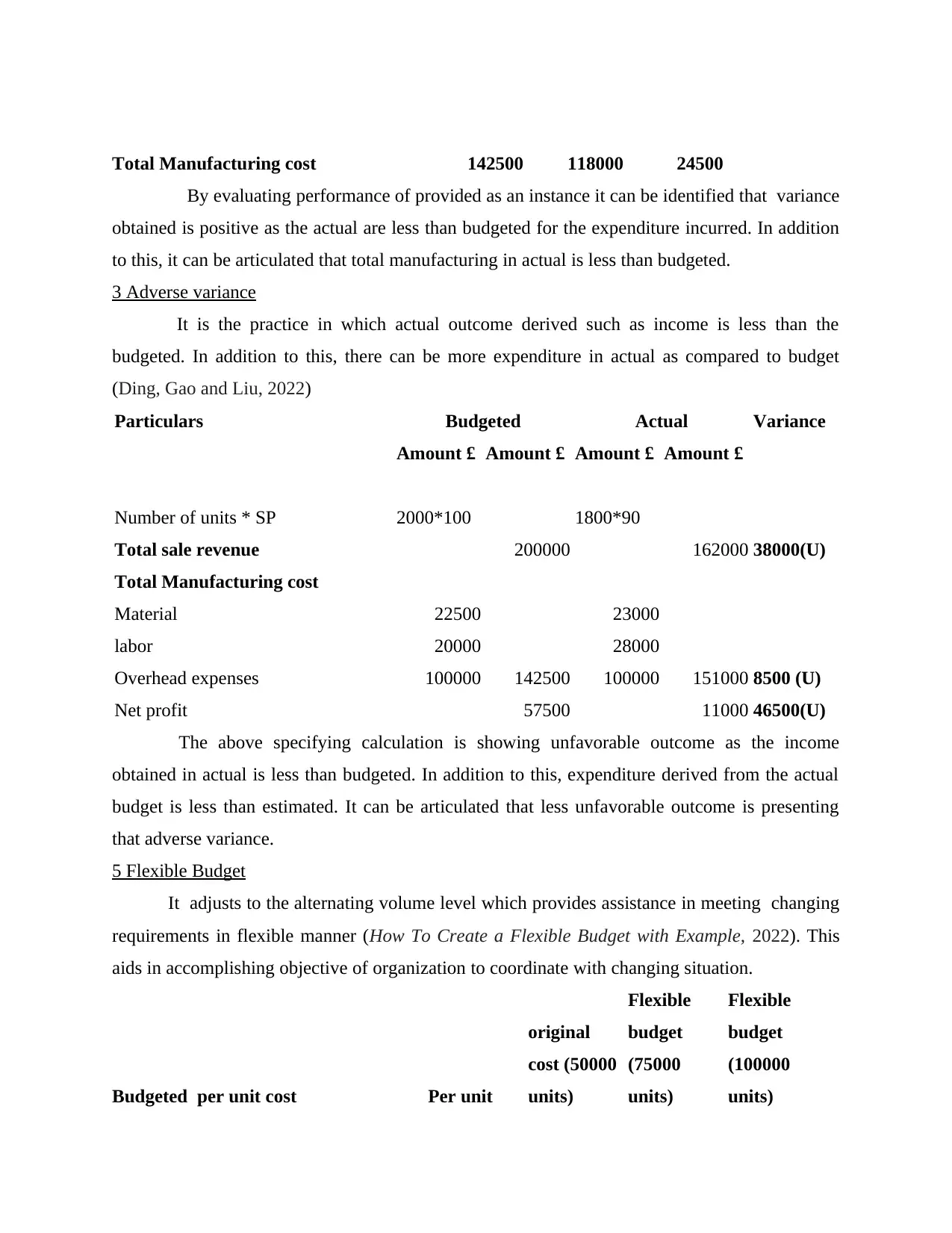

Total Manufacturing cost 142500 118000 24500

By evaluating performance of provided as an instance it can be identified that variance

obtained is positive as the actual are less than budgeted for the expenditure incurred. In addition

to this, it can be articulated that total manufacturing in actual is less than budgeted.

3 Adverse variance

It is the practice in which actual outcome derived such as income is less than the

budgeted. In addition to this, there can be more expenditure in actual as compared to budget

(Ding, Gao and Liu, 2022)

Particulars Budgeted Actual Variance

Amount £ Amount £ Amount £ Amount £

Number of units * SP 2000*100 1800*90

Total sale revenue 200000 162000 38000(U)

Total Manufacturing cost

Material 22500 23000

labor 20000 28000

Overhead expenses 100000 142500 100000 151000 8500 (U)

Net profit 57500 11000 46500(U)

The above specifying calculation is showing unfavorable outcome as the income

obtained in actual is less than budgeted. In addition to this, expenditure derived from the actual

budget is less than estimated. It can be articulated that less unfavorable outcome is presenting

that adverse variance.

5 Flexible Budget

It adjusts to the alternating volume level which provides assistance in meeting changing

requirements in flexible manner (How To Create a Flexible Budget with Example, 2022). This

aids in accomplishing objective of organization to coordinate with changing situation.

Budgeted per unit cost Per unit

original

cost (50000

units)

Flexible

budget

(75000

units)

Flexible

budget

(100000

units)

By evaluating performance of provided as an instance it can be identified that variance

obtained is positive as the actual are less than budgeted for the expenditure incurred. In addition

to this, it can be articulated that total manufacturing in actual is less than budgeted.

3 Adverse variance

It is the practice in which actual outcome derived such as income is less than the

budgeted. In addition to this, there can be more expenditure in actual as compared to budget

(Ding, Gao and Liu, 2022)

Particulars Budgeted Actual Variance

Amount £ Amount £ Amount £ Amount £

Number of units * SP 2000*100 1800*90

Total sale revenue 200000 162000 38000(U)

Total Manufacturing cost

Material 22500 23000

labor 20000 28000

Overhead expenses 100000 142500 100000 151000 8500 (U)

Net profit 57500 11000 46500(U)

The above specifying calculation is showing unfavorable outcome as the income

obtained in actual is less than budgeted. In addition to this, expenditure derived from the actual

budget is less than estimated. It can be articulated that less unfavorable outcome is presenting

that adverse variance.

5 Flexible Budget

It adjusts to the alternating volume level which provides assistance in meeting changing

requirements in flexible manner (How To Create a Flexible Budget with Example, 2022). This

aids in accomplishing objective of organization to coordinate with changing situation.

Budgeted per unit cost Per unit

original

cost (50000

units)

Flexible

budget

(75000

units)

Flexible

budget

(100000

units)

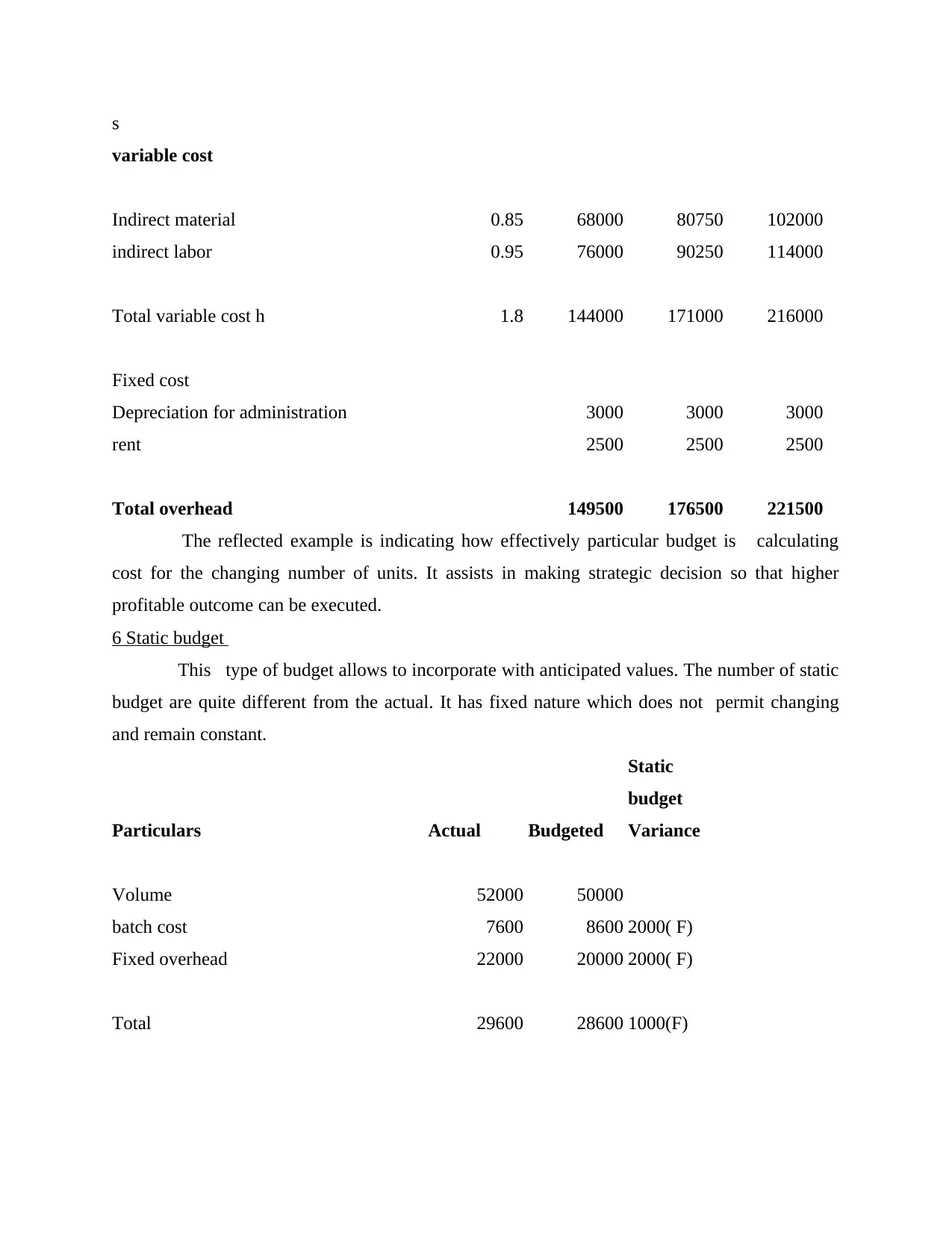

s

variable cost

Indirect material 0.85 68000 80750 102000

indirect labor 0.95 76000 90250 114000

Total variable cost h 1.8 144000 171000 216000

Fixed cost

Depreciation for administration 3000 3000 3000

rent 2500 2500 2500

Total overhead 149500 176500 221500

The reflected example is indicating how effectively particular budget is calculating

cost for the changing number of units. It assists in making strategic decision so that higher

profitable outcome can be executed.

6 Static budget

This type of budget allows to incorporate with anticipated values. The number of static

budget are quite different from the actual. It has fixed nature which does not permit changing

and remain constant.

Particulars Actual Budgeted

Static

budget

Variance

Volume 52000 50000

batch cost 7600 8600 2000( F)

Fixed overhead 22000 20000 2000( F)

Total 29600 28600 1000(F)

variable cost

Indirect material 0.85 68000 80750 102000

indirect labor 0.95 76000 90250 114000

Total variable cost h 1.8 144000 171000 216000

Fixed cost

Depreciation for administration 3000 3000 3000

rent 2500 2500 2500

Total overhead 149500 176500 221500

The reflected example is indicating how effectively particular budget is calculating

cost for the changing number of units. It assists in making strategic decision so that higher

profitable outcome can be executed.

6 Static budget

This type of budget allows to incorporate with anticipated values. The number of static

budget are quite different from the actual. It has fixed nature which does not permit changing

and remain constant.

Particulars Actual Budgeted

Static

budget

Variance

Volume 52000 50000

batch cost 7600 8600 2000( F)

Fixed overhead 22000 20000 2000( F)

Total 29600 28600 1000(F)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above presenting example is showing how well business is obtaining static budget. It aids in

resulting variance as static budget variance. On the basis of this h it can be identified that statistic

is fixed kind of budge which stick to the particular information for fixed budget.

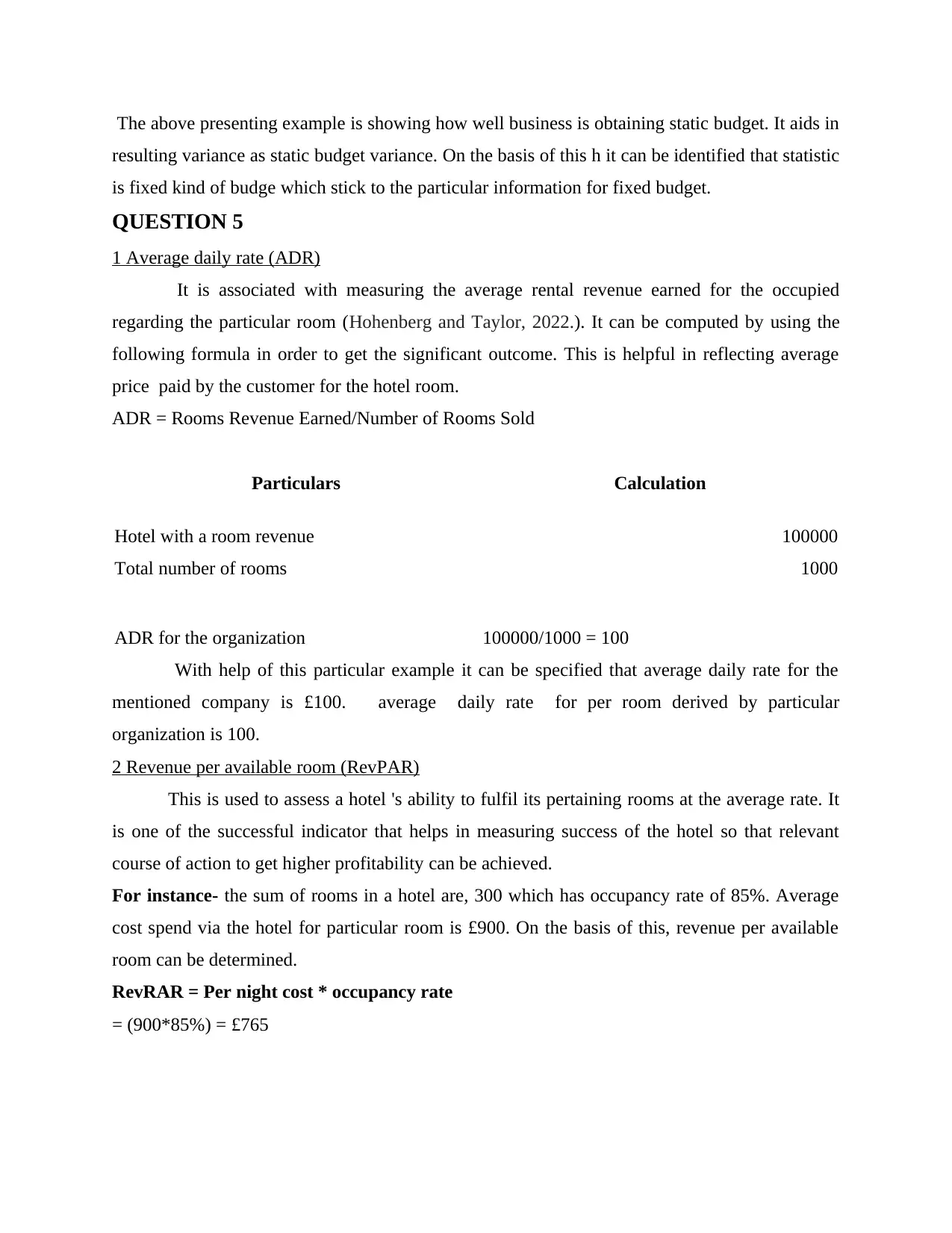

QUESTION 5

1 Average daily rate (ADR)

It is associated with measuring the average rental revenue earned for the occupied

regarding the particular room (Hohenberg and Taylor, 2022.). It can be computed by using the

following formula in order to get the significant outcome. This is helpful in reflecting average

price paid by the customer for the hotel room.

ADR = Rooms Revenue Earned/Number of Rooms Sold

Particulars Calculation

Hotel with a room revenue 100000

Total number of rooms 1000

ADR for the organization 100000/1000 = 100

With help of this particular example it can be specified that average daily rate for the

mentioned company is £100. average daily rate for per room derived by particular

organization is 100.

2 Revenue per available room (RevPAR)

This is used to assess a hotel 's ability to fulfil its pertaining rooms at the average rate. It

is one of the successful indicator that helps in measuring success of the hotel so that relevant

course of action to get higher profitability can be achieved.

For instance- the sum of rooms in a hotel are, 300 which has occupancy rate of 85%. Average

cost spend via the hotel for particular room is £900. On the basis of this, revenue per available

room can be determined.

RevRAR = Per night cost * occupancy rate

= (900*85%) = £765

resulting variance as static budget variance. On the basis of this h it can be identified that statistic

is fixed kind of budge which stick to the particular information for fixed budget.

QUESTION 5

1 Average daily rate (ADR)

It is associated with measuring the average rental revenue earned for the occupied

regarding the particular room (Hohenberg and Taylor, 2022.). It can be computed by using the

following formula in order to get the significant outcome. This is helpful in reflecting average

price paid by the customer for the hotel room.

ADR = Rooms Revenue Earned/Number of Rooms Sold

Particulars Calculation

Hotel with a room revenue 100000

Total number of rooms 1000

ADR for the organization 100000/1000 = 100

With help of this particular example it can be specified that average daily rate for the

mentioned company is £100. average daily rate for per room derived by particular

organization is 100.

2 Revenue per available room (RevPAR)

This is used to assess a hotel 's ability to fulfil its pertaining rooms at the average rate. It

is one of the successful indicator that helps in measuring success of the hotel so that relevant

course of action to get higher profitability can be achieved.

For instance- the sum of rooms in a hotel are, 300 which has occupancy rate of 85%. Average

cost spend via the hotel for particular room is £900. On the basis of this, revenue per available

room can be determined.

RevRAR = Per night cost * occupancy rate

= (900*85%) = £765

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

With help of the mentioned instance it can be interpreted that revenue obtained from the

per room available in the hospitality sector by the specified organization is £765. From

executing the operational activities of organizational in the particular hospitality sector is able to

offer it £765 revenue. Continuos inclination indicates how well business is improving in terms of

financial aspects.

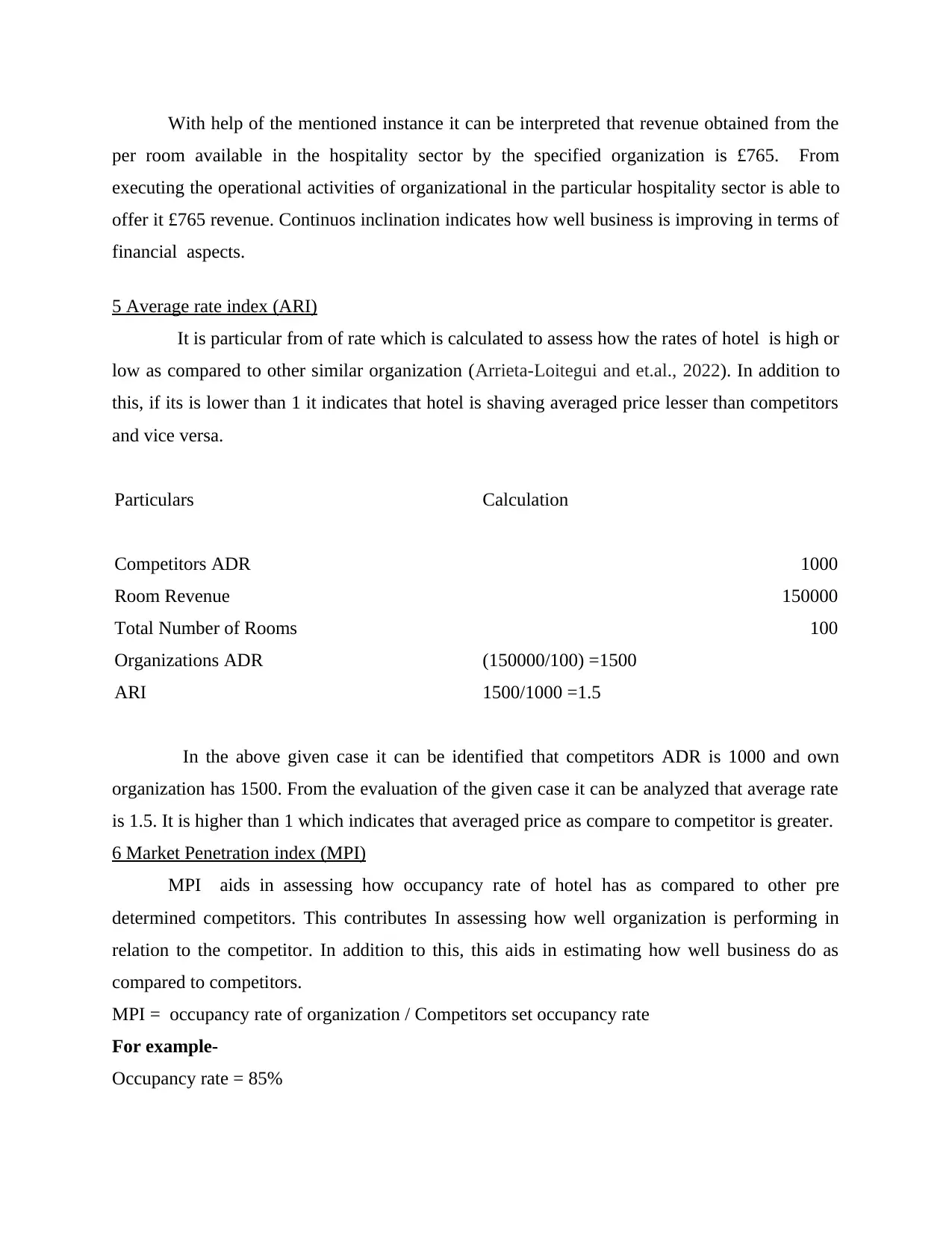

5 Average rate index (ARI)

It is particular from of rate which is calculated to assess how the rates of hotel is high or

low as compared to other similar organization (Arrieta-Loitegui and et.al., 2022). In addition to

this, if its is lower than 1 it indicates that hotel is shaving averaged price lesser than competitors

and vice versa.

Particulars Calculation

Competitors ADR 1000

Room Revenue 150000

Total Number of Rooms 100

Organizations ADR (150000/100) =1500

ARI 1500/1000 =1.5

In the above given case it can be identified that competitors ADR is 1000 and own

organization has 1500. From the evaluation of the given case it can be analyzed that average rate

is 1.5. It is higher than 1 which indicates that averaged price as compare to competitor is greater.

6 Market Penetration index (MPI)

MPI aids in assessing how occupancy rate of hotel has as compared to other pre

determined competitors. This contributes In assessing how well organization is performing in

relation to the competitor. In addition to this, this aids in estimating how well business do as

compared to competitors.

MPI = occupancy rate of organization / Competitors set occupancy rate

For example-

Occupancy rate = 85%

per room available in the hospitality sector by the specified organization is £765. From

executing the operational activities of organizational in the particular hospitality sector is able to

offer it £765 revenue. Continuos inclination indicates how well business is improving in terms of

financial aspects.

5 Average rate index (ARI)

It is particular from of rate which is calculated to assess how the rates of hotel is high or

low as compared to other similar organization (Arrieta-Loitegui and et.al., 2022). In addition to

this, if its is lower than 1 it indicates that hotel is shaving averaged price lesser than competitors

and vice versa.

Particulars Calculation

Competitors ADR 1000

Room Revenue 150000

Total Number of Rooms 100

Organizations ADR (150000/100) =1500

ARI 1500/1000 =1.5

In the above given case it can be identified that competitors ADR is 1000 and own

organization has 1500. From the evaluation of the given case it can be analyzed that average rate

is 1.5. It is higher than 1 which indicates that averaged price as compare to competitor is greater.

6 Market Penetration index (MPI)

MPI aids in assessing how occupancy rate of hotel has as compared to other pre

determined competitors. This contributes In assessing how well organization is performing in

relation to the competitor. In addition to this, this aids in estimating how well business do as

compared to competitors.

MPI = occupancy rate of organization / Competitors set occupancy rate

For example-

Occupancy rate = 85%

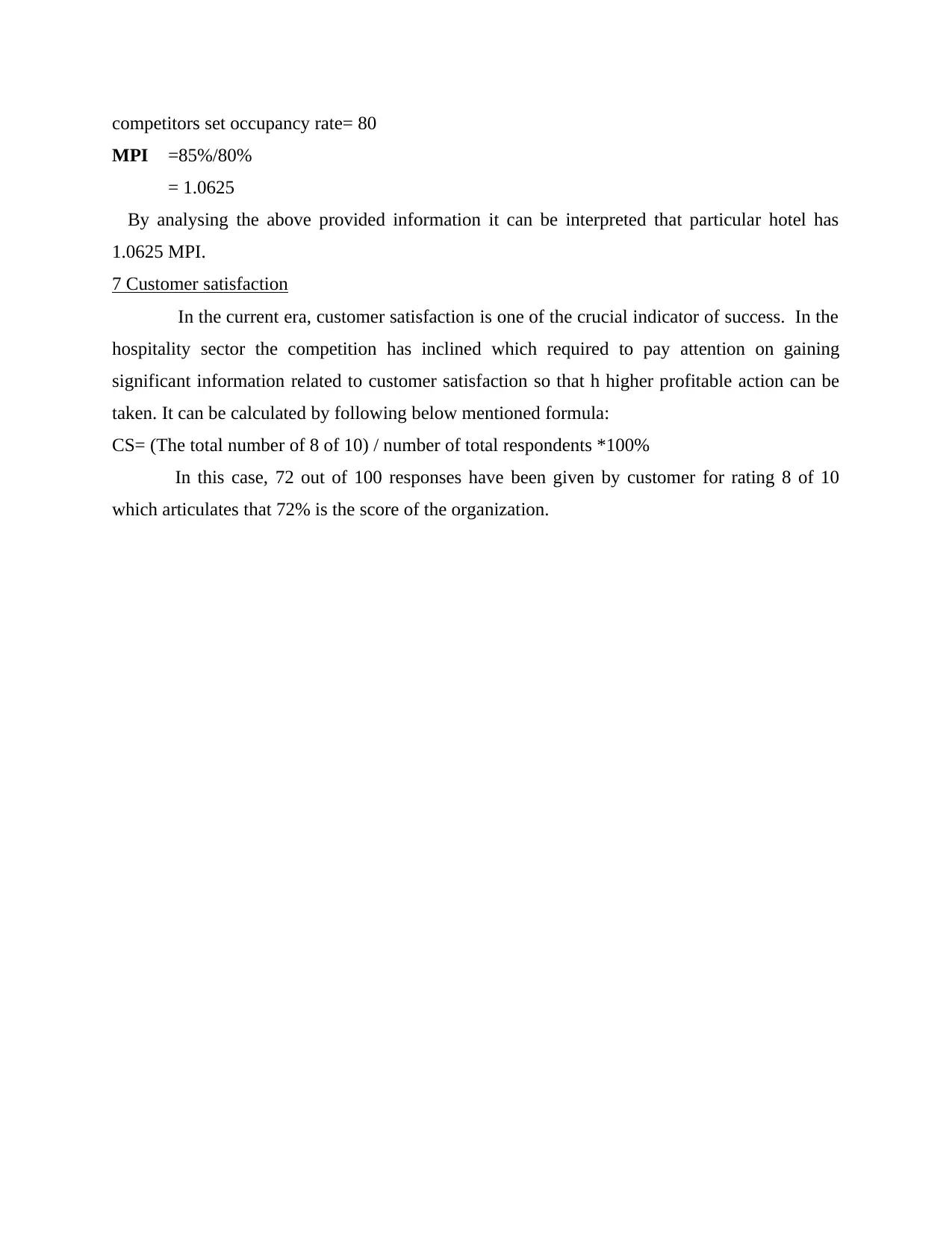

competitors set occupancy rate= 80

MPI =85%/80%

= 1.0625

By analysing the above provided information it can be interpreted that particular hotel has

1.0625 MPI.

7 Customer satisfaction

In the current era, customer satisfaction is one of the crucial indicator of success. In the

hospitality sector the competition has inclined which required to pay attention on gaining

significant information related to customer satisfaction so that h higher profitable action can be

taken. It can be calculated by following below mentioned formula:

CS= (The total number of 8 of 10) / number of total respondents *100%

In this case, 72 out of 100 responses have been given by customer for rating 8 of 10

which articulates that 72% is the score of the organization.

MPI =85%/80%

= 1.0625

By analysing the above provided information it can be interpreted that particular hotel has

1.0625 MPI.

7 Customer satisfaction

In the current era, customer satisfaction is one of the crucial indicator of success. In the

hospitality sector the competition has inclined which required to pay attention on gaining

significant information related to customer satisfaction so that h higher profitable action can be

taken. It can be calculated by following below mentioned formula:

CS= (The total number of 8 of 10) / number of total respondents *100%

In this case, 72 out of 100 responses have been given by customer for rating 8 of 10

which articulates that 72% is the score of the organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.