Management Accounting Report: Cost Analysis, Budgeting, and Variance

VerifiedAdded on 2020/01/28

|18

|5067

|40

Report

AI Summary

This report delves into management accounting principles, focusing on a case study of Jeffrey & Son's. It begins with cost classification, including direct, indirect, fixed, and variable costs, and then moves on to determining unit costs using job costing and absorption costing methods. The report covers overhead allocation using both machine hour and labor hour bases, followed by a cost report analysis that examines variances in material, labor, and overhead costs. Performance indicators, such as revenue, product quality, and profitability, are discussed to identify areas for improvement. The report also explores cost reduction strategies, product quality enhancement, and value creation. Furthermore, it examines budgeting processes, including production, material purchase, and cash budgets. Finally, it addresses variance analysis, identifies possible causes, and recommends corrective actions, concluding with a discussion of responsibility centers and their roles in financial management.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

TASK 1 .....................................................................................................................................1

AC 1.1 Cost classification on various types..........................................................................1

AC 1.2 Determining the unit cost using job costing method.................................................3

AC 1.3 Cost calculation using absorption costing method....................................................3

AC 1.4 OAR using labour hours basis..................................................................................5

TASK 2 .....................................................................................................................................5

AC 2.1 Preparation and analysing the cost report and comment on the variances................5

AC 2.2 Performance indicator to identify areas for potential improvement.........................6

AC 2.3 Ways to reduce cost, improve product quality and enhance value...........................7

TASK 3......................................................................................................................................8

AC 3.1 Nature and purpose of budgeting process.................................................................8

AC 3.2 Appropriate budgeting method and its need.............................................................8

AC 3.3 Production and Material purchase budget.................................................................9

AC 3.4 Preparing Jeffrey & Son's cash budget...................................................................10

Working note: .....................................................................................................................10

TASK 4....................................................................................................................................11

AC 4.1 Computing variances, identify possible causes and recommend corrective actions

.............................................................................................................................................11

AC 4.2 Operating statement................................................................................................12

AC 4.3 Responsibility centres.............................................................................................13

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION......................................................................................................................1

TASK 1 .....................................................................................................................................1

AC 1.1 Cost classification on various types..........................................................................1

AC 1.2 Determining the unit cost using job costing method.................................................3

AC 1.3 Cost calculation using absorption costing method....................................................3

AC 1.4 OAR using labour hours basis..................................................................................5

TASK 2 .....................................................................................................................................5

AC 2.1 Preparation and analysing the cost report and comment on the variances................5

AC 2.2 Performance indicator to identify areas for potential improvement.........................6

AC 2.3 Ways to reduce cost, improve product quality and enhance value...........................7

TASK 3......................................................................................................................................8

AC 3.1 Nature and purpose of budgeting process.................................................................8

AC 3.2 Appropriate budgeting method and its need.............................................................8

AC 3.3 Production and Material purchase budget.................................................................9

AC 3.4 Preparing Jeffrey & Son's cash budget...................................................................10

Working note: .....................................................................................................................10

TASK 4....................................................................................................................................11

AC 4.1 Computing variances, identify possible causes and recommend corrective actions

.............................................................................................................................................11

AC 4.2 Operating statement................................................................................................12

AC 4.3 Responsibility centres.............................................................................................13

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION

Managers play a crucial role in the organizations as they make policies, analyse

operational difficulties and take better decisions to remove hazards and run the business

successfully. Management accounting is a process of identifying, analysing and interpretation

of the financial information in order to take qualified decisions. In the present project report,

its importance will be discussed in accordance with a manufacturing organization named

Jeffrey & Son's. The company has a wide range of popular and branded product called

Exquisite.

In the present age, competition is rising at exponential rate. Thus, management

accounting plays a satisfactory role in the firms as it provides reliable and prominent

information’s to the managers and help to take effective decisions. In this report, numerous

managerial tools such as cost sheet, budgeting process and variance analysis have been

discussed. The report determines that how the techniques contribute to achieve organizational

targets and ensure long term survival.

TASK 1

AC 1.1 Cost classification on various types

Elements

Material Jeffrey & Sons need raw material to produce

its Exquisite product. Thus, the amount of

expenditure incurred on material purchase is

known as material cost (Paul, 2012.).

Labour Labours are the individuals who convert the

raw material into finished products through

putting their efforts (Datar and et. al., 2013).

Jeffrey & Son's make payment of wages to

the labours that are known as labour called

labour cost.

Overhead All the other incurred expenses are known as

overheads. It includes salary, printing

expenditures, rent and rates and etc.

1 | P a g e

Managers play a crucial role in the organizations as they make policies, analyse

operational difficulties and take better decisions to remove hazards and run the business

successfully. Management accounting is a process of identifying, analysing and interpretation

of the financial information in order to take qualified decisions. In the present project report,

its importance will be discussed in accordance with a manufacturing organization named

Jeffrey & Son's. The company has a wide range of popular and branded product called

Exquisite.

In the present age, competition is rising at exponential rate. Thus, management

accounting plays a satisfactory role in the firms as it provides reliable and prominent

information’s to the managers and help to take effective decisions. In this report, numerous

managerial tools such as cost sheet, budgeting process and variance analysis have been

discussed. The report determines that how the techniques contribute to achieve organizational

targets and ensure long term survival.

TASK 1

AC 1.1 Cost classification on various types

Elements

Material Jeffrey & Sons need raw material to produce

its Exquisite product. Thus, the amount of

expenditure incurred on material purchase is

known as material cost (Paul, 2012.).

Labour Labours are the individuals who convert the

raw material into finished products through

putting their efforts (Datar and et. al., 2013).

Jeffrey & Son's make payment of wages to

the labours that are known as labour called

labour cost.

Overhead All the other incurred expenses are known as

overheads. It includes salary, printing

expenditures, rent and rates and etc.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Functions

Production department cost The amount of expenses that has been

incurred for producing the goods of Jeffrey &

Son's is identified as production cost such as

factory lighting, rent and so on.

Office/Administrative cost Jeffrey & Son's administrative staff manage

the business functions thus, incurred office

expenditures such as office lighting,

stationery and photo copy charges.

Selling and distribution department cost After producing Exquisite, Jeffrey & Sons

sales and marketing manager are responsible

for selling the product in the market. It

includes all the marketing, advertisement and

free sample distributions.

Nature

Direct Chargeable business expenses directly

towards the product Exquisite is known as

direct cost such as material's purchase and

labour's wages.

Indirect A payment that cannot be directly charged to

the Exquisite product is known as indirect

cost such as insurance, depreciation and

manager's salary (VanDerbeck, 2012).

Behaviour

Fixed Expenditures that are unrelated to changing

the production volume of Jeffrey & Son's is

known as fixed cost such as depreciation and

building insurance (Blocher, Chen and Lin,

2 | P a g e

Production department cost The amount of expenses that has been

incurred for producing the goods of Jeffrey &

Son's is identified as production cost such as

factory lighting, rent and so on.

Office/Administrative cost Jeffrey & Son's administrative staff manage

the business functions thus, incurred office

expenditures such as office lighting,

stationery and photo copy charges.

Selling and distribution department cost After producing Exquisite, Jeffrey & Sons

sales and marketing manager are responsible

for selling the product in the market. It

includes all the marketing, advertisement and

free sample distributions.

Nature

Direct Chargeable business expenses directly

towards the product Exquisite is known as

direct cost such as material's purchase and

labour's wages.

Indirect A payment that cannot be directly charged to

the Exquisite product is known as indirect

cost such as insurance, depreciation and

manager's salary (VanDerbeck, 2012).

Behaviour

Fixed Expenditures that are unrelated to changing

the production volume of Jeffrey & Son's is

known as fixed cost such as depreciation and

building insurance (Blocher, Chen and Lin,

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2008).

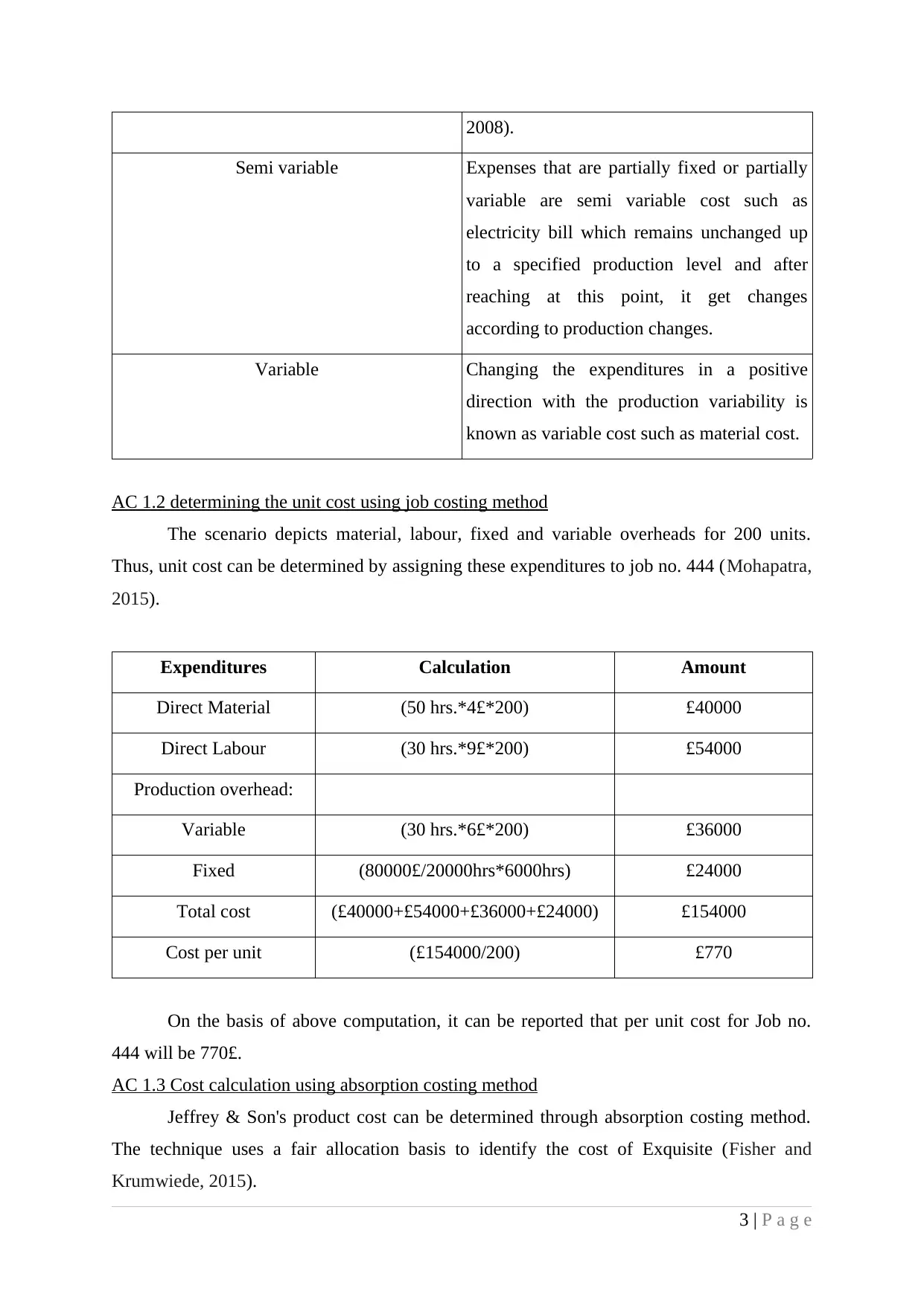

Semi variable Expenses that are partially fixed or partially

variable are semi variable cost such as

electricity bill which remains unchanged up

to a specified production level and after

reaching at this point, it get changes

according to production changes.

Variable Changing the expenditures in a positive

direction with the production variability is

known as variable cost such as material cost.

AC 1.2 determining the unit cost using job costing method

The scenario depicts material, labour, fixed and variable overheads for 200 units.

Thus, unit cost can be determined by assigning these expenditures to job no. 444 (Mohapatra,

2015).

Expenditures Calculation Amount

Direct Material (50 hrs.*4£*200) £40000

Direct Labour (30 hrs.*9£*200) £54000

Production overhead:

Variable (30 hrs.*6£*200) £36000

Fixed (80000£/20000hrs*6000hrs) £24000

Total cost (£40000+£54000+£36000+£24000) £154000

Cost per unit (£154000/200) £770

On the basis of above computation, it can be reported that per unit cost for Job no.

444 will be 770£.

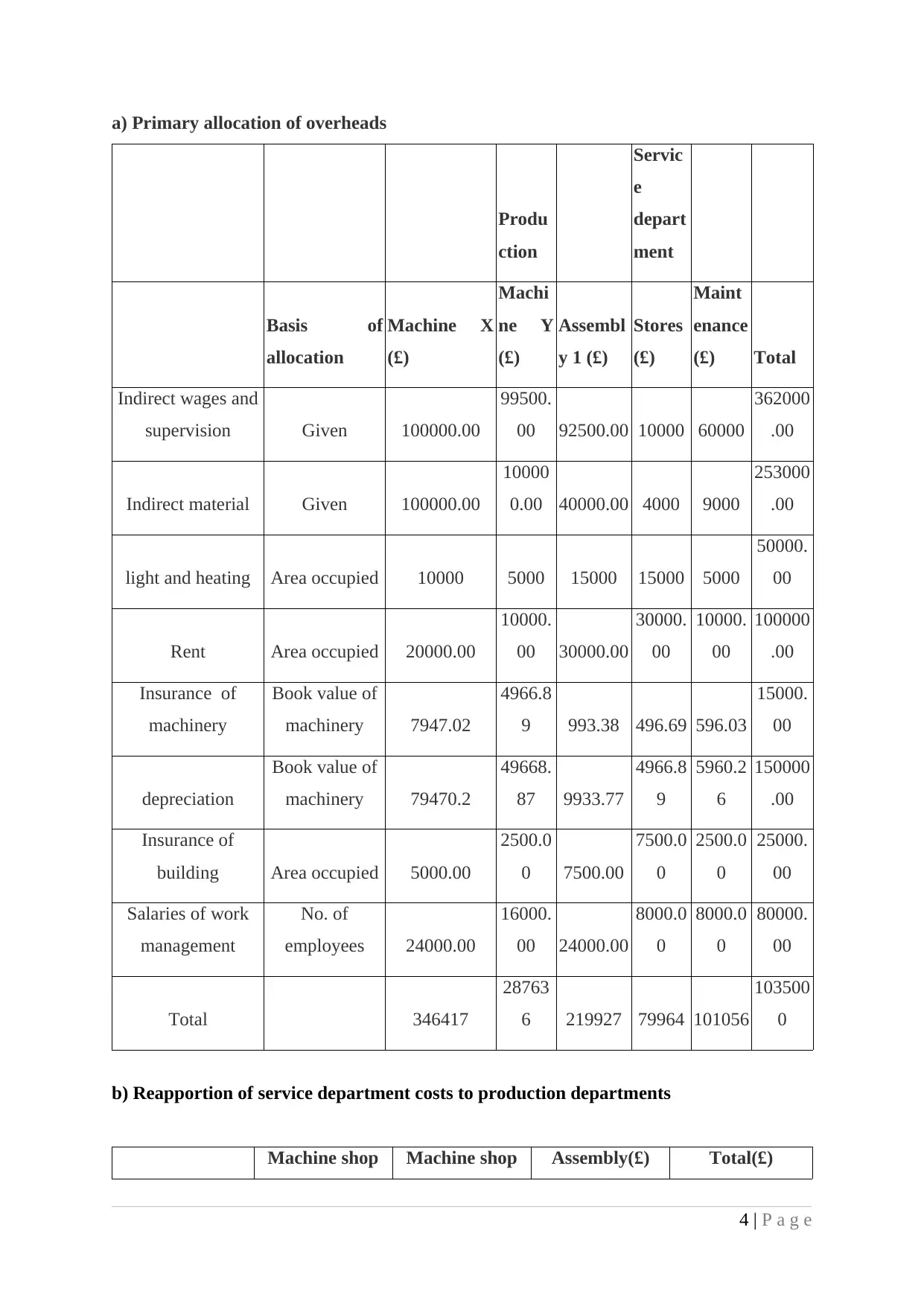

AC 1.3 Cost calculation using absorption costing method

Jeffrey & Son's product cost can be determined through absorption costing method.

The technique uses a fair allocation basis to identify the cost of Exquisite (Fisher and

Krumwiede, 2015).

3 | P a g e

Semi variable Expenses that are partially fixed or partially

variable are semi variable cost such as

electricity bill which remains unchanged up

to a specified production level and after

reaching at this point, it get changes

according to production changes.

Variable Changing the expenditures in a positive

direction with the production variability is

known as variable cost such as material cost.

AC 1.2 determining the unit cost using job costing method

The scenario depicts material, labour, fixed and variable overheads for 200 units.

Thus, unit cost can be determined by assigning these expenditures to job no. 444 (Mohapatra,

2015).

Expenditures Calculation Amount

Direct Material (50 hrs.*4£*200) £40000

Direct Labour (30 hrs.*9£*200) £54000

Production overhead:

Variable (30 hrs.*6£*200) £36000

Fixed (80000£/20000hrs*6000hrs) £24000

Total cost (£40000+£54000+£36000+£24000) £154000

Cost per unit (£154000/200) £770

On the basis of above computation, it can be reported that per unit cost for Job no.

444 will be 770£.

AC 1.3 Cost calculation using absorption costing method

Jeffrey & Son's product cost can be determined through absorption costing method.

The technique uses a fair allocation basis to identify the cost of Exquisite (Fisher and

Krumwiede, 2015).

3 | P a g e

a) Primary allocation of overheads

Produ

ction

Servic

e

depart

ment

Basis of

allocation

Machine X

(£)

Machi

ne Y

(£)

Assembl

y 1 (£)

Stores

(£)

Maint

enance

(£) Total

Indirect wages and

supervision Given 100000.00

99500.

00 92500.00 10000 60000

362000

.00

Indirect material Given 100000.00

10000

0.00 40000.00 4000 9000

253000

.00

light and heating Area occupied 10000 5000 15000 15000 5000

50000.

00

Rent Area occupied 20000.00

10000.

00 30000.00

30000.

00

10000.

00

100000

.00

Insurance of

machinery

Book value of

machinery 7947.02

4966.8

9 993.38 496.69 596.03

15000.

00

depreciation

Book value of

machinery 79470.2

49668.

87 9933.77

4966.8

9

5960.2

6

150000

.00

Insurance of

building Area occupied 5000.00

2500.0

0 7500.00

7500.0

0

2500.0

0

25000.

00

Salaries of work

management

No. of

employees 24000.00

16000.

00 24000.00

8000.0

0

8000.0

0

80000.

00

Total 346417

28763

6 219927 79964 101056

103500

0

b) Reapportion of service department costs to production departments

Machine shop Machine shop Assembly(£) Total(£)

4 | P a g e

Produ

ction

Servic

e

depart

ment

Basis of

allocation

Machine X

(£)

Machi

ne Y

(£)

Assembl

y 1 (£)

Stores

(£)

Maint

enance

(£) Total

Indirect wages and

supervision Given 100000.00

99500.

00 92500.00 10000 60000

362000

.00

Indirect material Given 100000.00

10000

0.00 40000.00 4000 9000

253000

.00

light and heating Area occupied 10000 5000 15000 15000 5000

50000.

00

Rent Area occupied 20000.00

10000.

00 30000.00

30000.

00

10000.

00

100000

.00

Insurance of

machinery

Book value of

machinery 7947.02

4966.8

9 993.38 496.69 596.03

15000.

00

depreciation

Book value of

machinery 79470.2

49668.

87 9933.77

4966.8

9

5960.2

6

150000

.00

Insurance of

building Area occupied 5000.00

2500.0

0 7500.00

7500.0

0

2500.0

0

25000.

00

Salaries of work

management

No. of

employees 24000.00

16000.

00 24000.00

8000.0

0

8000.0

0

80000.

00

Total 346417

28763

6 219927 79964 101056

103500

0

b) Reapportion of service department costs to production departments

Machine shop Machine shop Assembly(£) Total(£)

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

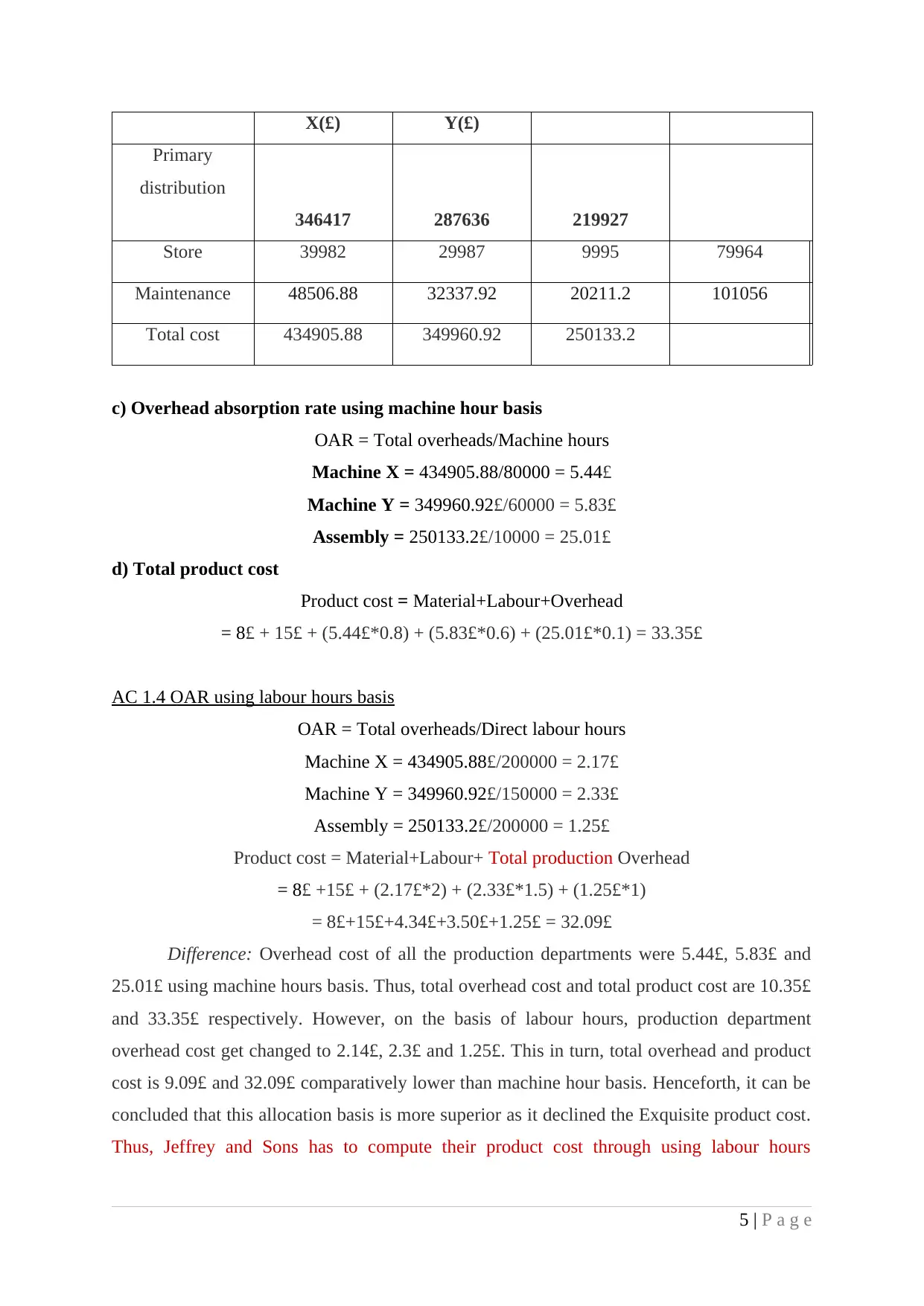

X(£) Y(£)

Primary

distribution

346417 287636 219927

Store 39982 29987 9995 79964

Maintenance 48506.88 32337.92 20211.2 101056

Total cost 434905.88 349960.92 250133.2

c) Overhead absorption rate using machine hour basis

OAR = Total overheads/Machine hours

Machine X = 434905.88/80000 = 5.44£

Machine Y = 349960.92£/60000 = 5.83£

Assembly = 250133.2£/10000 = 25.01£

d) Total product cost

Product cost = Material+Labour+Overhead

= 8£ + 15£ + (5.44£*0.8) + (5.83£*0.6) + (25.01£*0.1) = 33.35£

AC 1.4 OAR using labour hours basis

OAR = Total overheads/Direct labour hours

Machine X = 434905.88£/200000 = 2.17£

Machine Y = 349960.92£/150000 = 2.33£

Assembly = 250133.2£/200000 = 1.25£

Product cost = Material+Labour+ Total production Overhead

= 8£ +15£ + (2.17£*2) + (2.33£*1.5) + (1.25£*1)

= 8£+15£+4.34£+3.50£+1.25£ = 32.09£

Difference: Overhead cost of all the production departments were 5.44£, 5.83£ and

25.01£ using machine hours basis. Thus, total overhead cost and total product cost are 10.35£

and 33.35£ respectively. However, on the basis of labour hours, production department

overhead cost get changed to 2.14£, 2.3£ and 1.25£. This in turn, total overhead and product

cost is 9.09£ and 32.09£ comparatively lower than machine hour basis. Henceforth, it can be

concluded that this allocation basis is more superior as it declined the Exquisite product cost.

Thus, Jeffrey and Sons has to compute their product cost through using labour hours

5 | P a g e

Primary

distribution

346417 287636 219927

Store 39982 29987 9995 79964

Maintenance 48506.88 32337.92 20211.2 101056

Total cost 434905.88 349960.92 250133.2

c) Overhead absorption rate using machine hour basis

OAR = Total overheads/Machine hours

Machine X = 434905.88/80000 = 5.44£

Machine Y = 349960.92£/60000 = 5.83£

Assembly = 250133.2£/10000 = 25.01£

d) Total product cost

Product cost = Material+Labour+Overhead

= 8£ + 15£ + (5.44£*0.8) + (5.83£*0.6) + (25.01£*0.1) = 33.35£

AC 1.4 OAR using labour hours basis

OAR = Total overheads/Direct labour hours

Machine X = 434905.88£/200000 = 2.17£

Machine Y = 349960.92£/150000 = 2.33£

Assembly = 250133.2£/200000 = 1.25£

Product cost = Material+Labour+ Total production Overhead

= 8£ +15£ + (2.17£*2) + (2.33£*1.5) + (1.25£*1)

= 8£+15£+4.34£+3.50£+1.25£ = 32.09£

Difference: Overhead cost of all the production departments were 5.44£, 5.83£ and

25.01£ using machine hours basis. Thus, total overhead cost and total product cost are 10.35£

and 33.35£ respectively. However, on the basis of labour hours, production department

overhead cost get changed to 2.14£, 2.3£ and 1.25£. This in turn, total overhead and product

cost is 9.09£ and 32.09£ comparatively lower than machine hour basis. Henceforth, it can be

concluded that this allocation basis is more superior as it declined the Exquisite product cost.

Thus, Jeffrey and Sons has to compute their product cost through using labour hours

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

allocation basis. It reduces company's cost and provides greater profitability. This in turn,

organization will be able to improve its operational performance and get benefited through it.

TASK 2

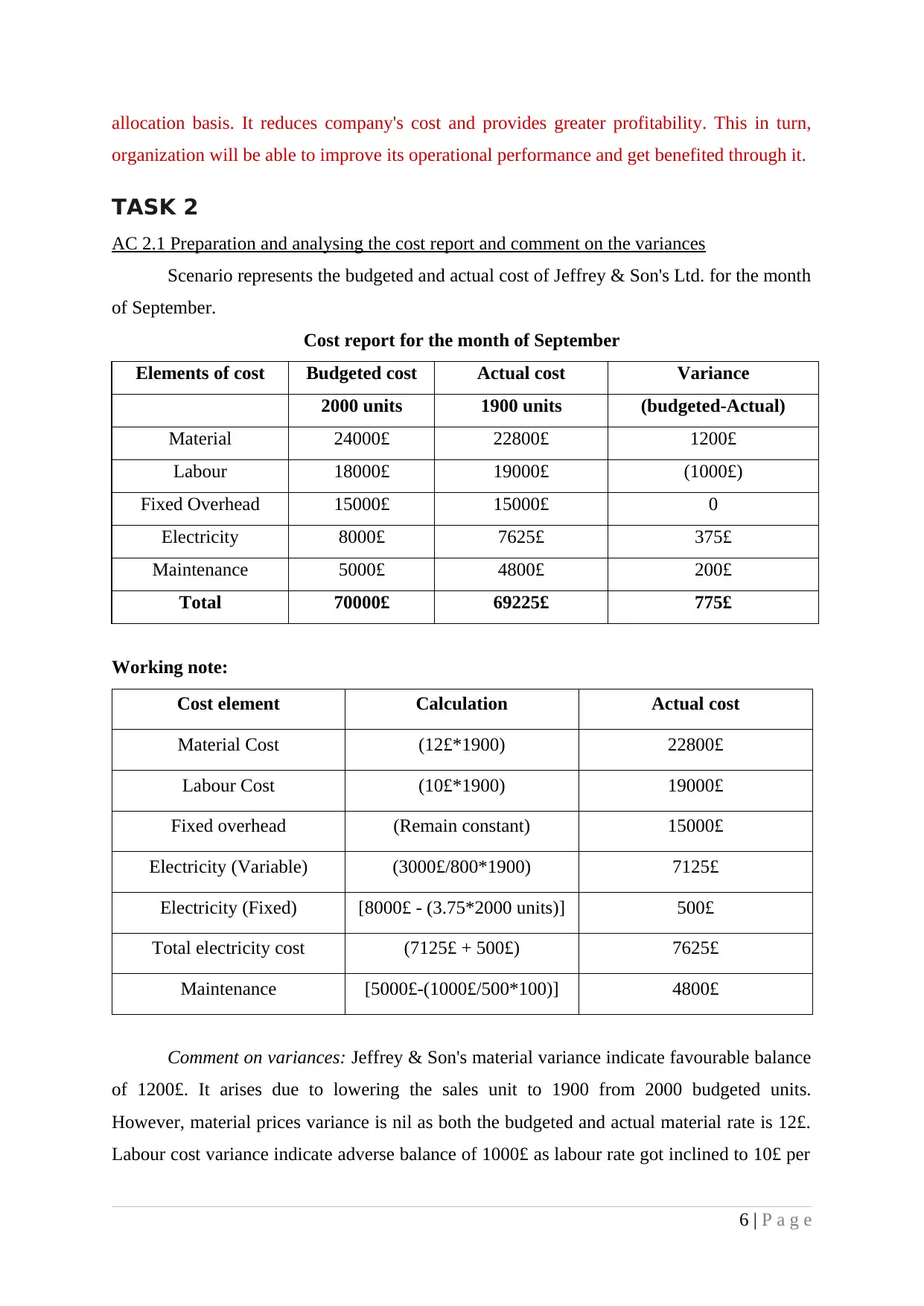

AC 2.1 Preparation and analysing the cost report and comment on the variances

Scenario represents the budgeted and actual cost of Jeffrey & Son's Ltd. for the month

of September.

Cost report for the month of September

Elements of cost Budgeted cost Actual cost Variance

2000 units 1900 units (budgeted-Actual)

Material 24000£ 22800£ 1200£

Labour 18000£ 19000£ (1000£)

Fixed Overhead 15000£ 15000£ 0

Electricity 8000£ 7625£ 375£

Maintenance 5000£ 4800£ 200£

Total 70000£ 69225£ 775£

Working note:

Cost element Calculation Actual cost

Material Cost (12£*1900) 22800£

Labour Cost (10£*1900) 19000£

Fixed overhead (Remain constant) 15000£

Electricity (Variable) (3000£/800*1900) 7125£

Electricity (Fixed) [8000£ - (3.75*2000 units)] 500£

Total electricity cost (7125£ + 500£) 7625£

Maintenance [5000£-(1000£/500*100)] 4800£

Comment on variances: Jeffrey & Son's material variance indicate favourable balance

of 1200£. It arises due to lowering the sales unit to 1900 from 2000 budgeted units.

However, material prices variance is nil as both the budgeted and actual material rate is 12£.

Labour cost variance indicate adverse balance of 1000£ as labour rate got inclined to 10£ per

6 | P a g e

organization will be able to improve its operational performance and get benefited through it.

TASK 2

AC 2.1 Preparation and analysing the cost report and comment on the variances

Scenario represents the budgeted and actual cost of Jeffrey & Son's Ltd. for the month

of September.

Cost report for the month of September

Elements of cost Budgeted cost Actual cost Variance

2000 units 1900 units (budgeted-Actual)

Material 24000£ 22800£ 1200£

Labour 18000£ 19000£ (1000£)

Fixed Overhead 15000£ 15000£ 0

Electricity 8000£ 7625£ 375£

Maintenance 5000£ 4800£ 200£

Total 70000£ 69225£ 775£

Working note:

Cost element Calculation Actual cost

Material Cost (12£*1900) 22800£

Labour Cost (10£*1900) 19000£

Fixed overhead (Remain constant) 15000£

Electricity (Variable) (3000£/800*1900) 7125£

Electricity (Fixed) [8000£ - (3.75*2000 units)] 500£

Total electricity cost (7125£ + 500£) 7625£

Maintenance [5000£-(1000£/500*100)] 4800£

Comment on variances: Jeffrey & Son's material variance indicate favourable balance

of 1200£. It arises due to lowering the sales unit to 1900 from 2000 budgeted units.

However, material prices variance is nil as both the budgeted and actual material rate is 12£.

Labour cost variance indicate adverse balance of 1000£ as labour rate got inclined to 10£ per

6 | P a g e

unit. Electricity cost get declined by 375£ due to lower the production. Further, maintenance

is a stepped cost that decreased by 200£ due to declined production volume.

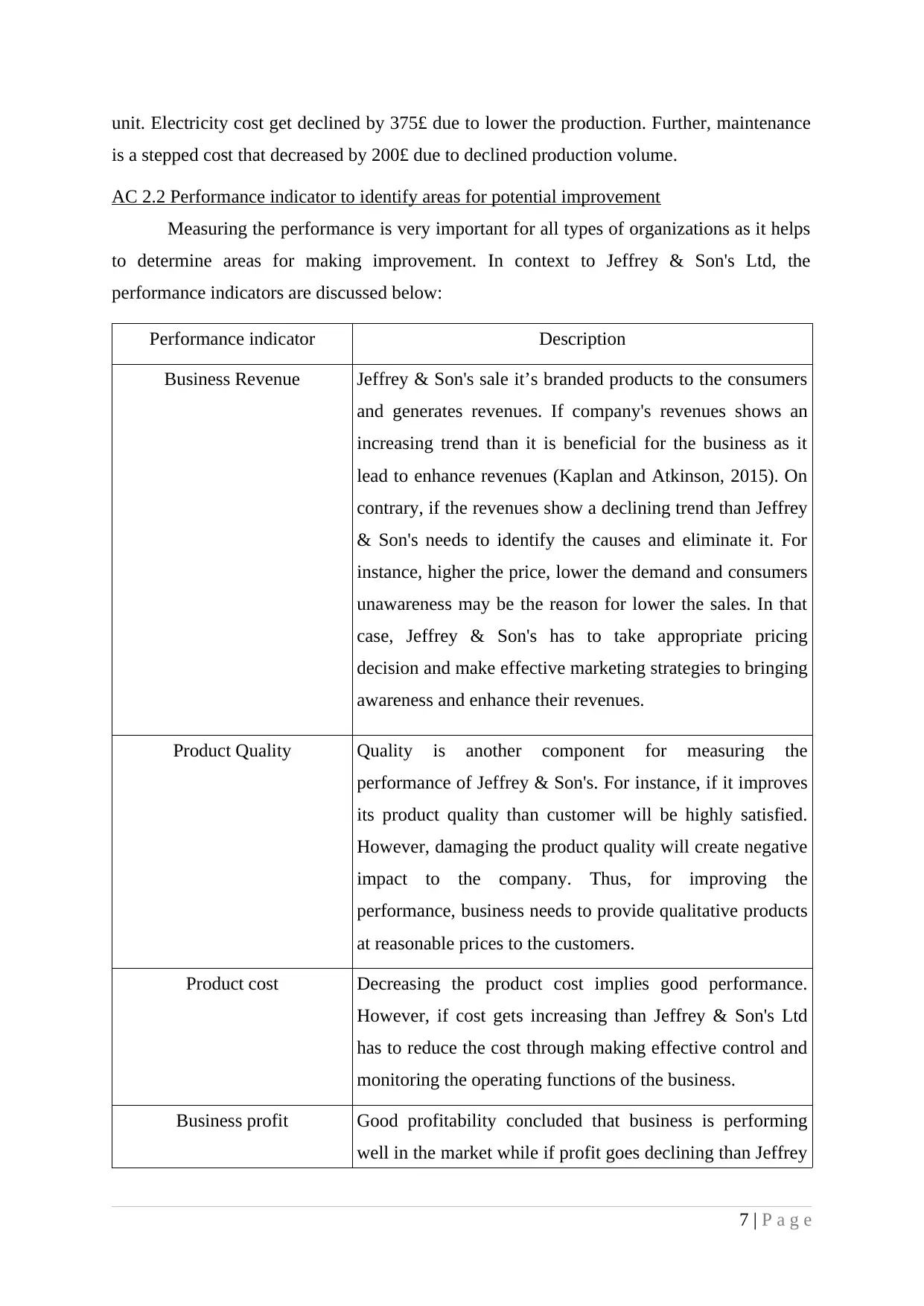

AC 2.2 Performance indicator to identify areas for potential improvement

Measuring the performance is very important for all types of organizations as it helps

to determine areas for making improvement. In context to Jeffrey & Son's Ltd, the

performance indicators are discussed below:

Performance indicator Description

Business Revenue Jeffrey & Son's sale it’s branded products to the consumers

and generates revenues. If company's revenues shows an

increasing trend than it is beneficial for the business as it

lead to enhance revenues (Kaplan and Atkinson, 2015). On

contrary, if the revenues show a declining trend than Jeffrey

& Son's needs to identify the causes and eliminate it. For

instance, higher the price, lower the demand and consumers

unawareness may be the reason for lower the sales. In that

case, Jeffrey & Son's has to take appropriate pricing

decision and make effective marketing strategies to bringing

awareness and enhance their revenues.

Product Quality Quality is another component for measuring the

performance of Jeffrey & Son's. For instance, if it improves

its product quality than customer will be highly satisfied.

However, damaging the product quality will create negative

impact to the company. Thus, for improving the

performance, business needs to provide qualitative products

at reasonable prices to the customers.

Product cost Decreasing the product cost implies good performance.

However, if cost gets increasing than Jeffrey & Son's Ltd

has to reduce the cost through making effective control and

monitoring the operating functions of the business.

Business profit Good profitability concluded that business is performing

well in the market while if profit goes declining than Jeffrey

7 | P a g e

is a stepped cost that decreased by 200£ due to declined production volume.

AC 2.2 Performance indicator to identify areas for potential improvement

Measuring the performance is very important for all types of organizations as it helps

to determine areas for making improvement. In context to Jeffrey & Son's Ltd, the

performance indicators are discussed below:

Performance indicator Description

Business Revenue Jeffrey & Son's sale it’s branded products to the consumers

and generates revenues. If company's revenues shows an

increasing trend than it is beneficial for the business as it

lead to enhance revenues (Kaplan and Atkinson, 2015). On

contrary, if the revenues show a declining trend than Jeffrey

& Son's needs to identify the causes and eliminate it. For

instance, higher the price, lower the demand and consumers

unawareness may be the reason for lower the sales. In that

case, Jeffrey & Son's has to take appropriate pricing

decision and make effective marketing strategies to bringing

awareness and enhance their revenues.

Product Quality Quality is another component for measuring the

performance of Jeffrey & Son's. For instance, if it improves

its product quality than customer will be highly satisfied.

However, damaging the product quality will create negative

impact to the company. Thus, for improving the

performance, business needs to provide qualitative products

at reasonable prices to the customers.

Product cost Decreasing the product cost implies good performance.

However, if cost gets increasing than Jeffrey & Son's Ltd

has to reduce the cost through making effective control and

monitoring the operating functions of the business.

Business profit Good profitability concluded that business is performing

well in the market while if profit goes declining than Jeffrey

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

& Son's Ltd need to enhance sales and reduce cost to

increase their profits.

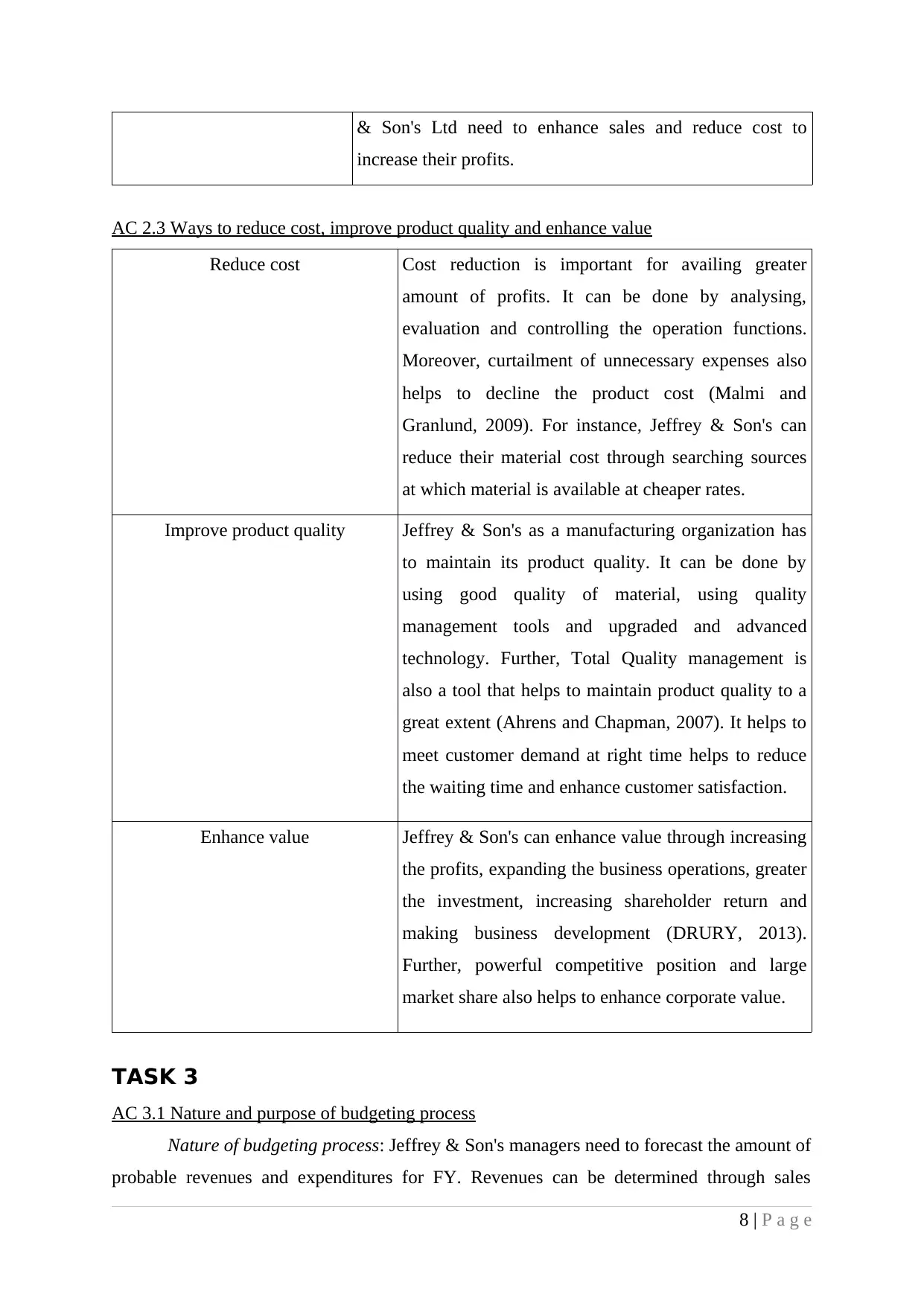

AC 2.3 Ways to reduce cost, improve product quality and enhance value

Reduce cost Cost reduction is important for availing greater

amount of profits. It can be done by analysing,

evaluation and controlling the operation functions.

Moreover, curtailment of unnecessary expenses also

helps to decline the product cost (Malmi and

Granlund, 2009). For instance, Jeffrey & Son's can

reduce their material cost through searching sources

at which material is available at cheaper rates.

Improve product quality Jeffrey & Son's as a manufacturing organization has

to maintain its product quality. It can be done by

using good quality of material, using quality

management tools and upgraded and advanced

technology. Further, Total Quality management is

also a tool that helps to maintain product quality to a

great extent (Ahrens and Chapman, 2007). It helps to

meet customer demand at right time helps to reduce

the waiting time and enhance customer satisfaction.

Enhance value Jeffrey & Son's can enhance value through increasing

the profits, expanding the business operations, greater

the investment, increasing shareholder return and

making business development (DRURY, 2013).

Further, powerful competitive position and large

market share also helps to enhance corporate value.

TASK 3

AC 3.1 Nature and purpose of budgeting process

Nature of budgeting process: Jeffrey & Son's managers need to forecast the amount of

probable revenues and expenditures for FY. Revenues can be determined through sales

8 | P a g e

increase their profits.

AC 2.3 Ways to reduce cost, improve product quality and enhance value

Reduce cost Cost reduction is important for availing greater

amount of profits. It can be done by analysing,

evaluation and controlling the operation functions.

Moreover, curtailment of unnecessary expenses also

helps to decline the product cost (Malmi and

Granlund, 2009). For instance, Jeffrey & Son's can

reduce their material cost through searching sources

at which material is available at cheaper rates.

Improve product quality Jeffrey & Son's as a manufacturing organization has

to maintain its product quality. It can be done by

using good quality of material, using quality

management tools and upgraded and advanced

technology. Further, Total Quality management is

also a tool that helps to maintain product quality to a

great extent (Ahrens and Chapman, 2007). It helps to

meet customer demand at right time helps to reduce

the waiting time and enhance customer satisfaction.

Enhance value Jeffrey & Son's can enhance value through increasing

the profits, expanding the business operations, greater

the investment, increasing shareholder return and

making business development (DRURY, 2013).

Further, powerful competitive position and large

market share also helps to enhance corporate value.

TASK 3

AC 3.1 Nature and purpose of budgeting process

Nature of budgeting process: Jeffrey & Son's managers need to forecast the amount of

probable revenues and expenditures for FY. Revenues can be determined through sales

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

estimation on the basis of probable consumer demand and previous year sales. Further,

expenditures can be forecasted through identifying the material, labour and overhead

payments to produce require number of units. Comparison between revenues and expenses

will results in deficit or surplus. For instance, higher the revenues than expenses will indicate

surplus otherwise deficit. Thereafter, Jeffrey & Son's managers have to determine the actual

operational performance for variance computation. Adverse variance need to be eliminated

through taking corrective actions as actual expenses are higher and actual incomes are lower

than set budgeted.

Purpose of budgeting process: Jeffrey & Son's Ltd construct budget for an estimating

future performance. It aims at determining operational performance of the company for future

years. The budgetary tools helps to maintain business profits through controlling cost to set

targets and maximize revenues (Zimmerman and Yahya-Zadeh, 2011). This in turn, Jeffrey &

Son's can achieve its target objectives to a great extent. Moreover, it aims at ensure optimum

allocation of business resources in various operating functions. At last, variance elimination

mainly aims at meet organizational objectives for long term success of the company.

AC 3.2 Appropriate budgeting method and its need

Budget must be prepared in an appropriate manner as it provides reliable and most

accurate estimate towards the future period. It is beneficial because it helps to take right

decisions with right cost and at right time. The present scenario depicts that sales volume is

the key component in Jeffrey & Son's budget manual. Moreover, paramount takes place in

order to establish co-ordination. Henceforth, it became clear that incremental technique has

been applied to prepare Jeffrey & Son's budget. Thus, the marketing manager as a budget

holder will face many problems. The reason behind that is this method increased all the

incomes and expenses by a fixed percentage or amount without examining their future

importance (cost and mangement accounting, n.d). Further, historical budget is the basis of

company's budgeting process hence, it do not make proper analysis of operating functions in

future context.

Zero base budgeting will be considered as most effective techniques for budget

construction. The need of adopting this technique will be arise because it identifies the

importance of all the operating activities for the FY (Glass, Stefanova and Prinzivalli, 2014).

Thus, it helps to cut off undesired expenditures and reduce business cost. Further, through

sales maximization and optimum allocation of resources, Jeffrey & Son's can improve their

profit earnings. This in turn, operational performance can be improved to a large extent.

9 | P a g e

expenditures can be forecasted through identifying the material, labour and overhead

payments to produce require number of units. Comparison between revenues and expenses

will results in deficit or surplus. For instance, higher the revenues than expenses will indicate

surplus otherwise deficit. Thereafter, Jeffrey & Son's managers have to determine the actual

operational performance for variance computation. Adverse variance need to be eliminated

through taking corrective actions as actual expenses are higher and actual incomes are lower

than set budgeted.

Purpose of budgeting process: Jeffrey & Son's Ltd construct budget for an estimating

future performance. It aims at determining operational performance of the company for future

years. The budgetary tools helps to maintain business profits through controlling cost to set

targets and maximize revenues (Zimmerman and Yahya-Zadeh, 2011). This in turn, Jeffrey &

Son's can achieve its target objectives to a great extent. Moreover, it aims at ensure optimum

allocation of business resources in various operating functions. At last, variance elimination

mainly aims at meet organizational objectives for long term success of the company.

AC 3.2 Appropriate budgeting method and its need

Budget must be prepared in an appropriate manner as it provides reliable and most

accurate estimate towards the future period. It is beneficial because it helps to take right

decisions with right cost and at right time. The present scenario depicts that sales volume is

the key component in Jeffrey & Son's budget manual. Moreover, paramount takes place in

order to establish co-ordination. Henceforth, it became clear that incremental technique has

been applied to prepare Jeffrey & Son's budget. Thus, the marketing manager as a budget

holder will face many problems. The reason behind that is this method increased all the

incomes and expenses by a fixed percentage or amount without examining their future

importance (cost and mangement accounting, n.d). Further, historical budget is the basis of

company's budgeting process hence, it do not make proper analysis of operating functions in

future context.

Zero base budgeting will be considered as most effective techniques for budget

construction. The need of adopting this technique will be arise because it identifies the

importance of all the operating activities for the FY (Glass, Stefanova and Prinzivalli, 2014).

Thus, it helps to cut off undesired expenditures and reduce business cost. Further, through

sales maximization and optimum allocation of resources, Jeffrey & Son's can improve their

profit earnings. This in turn, operational performance can be improved to a large extent.

9 | P a g e

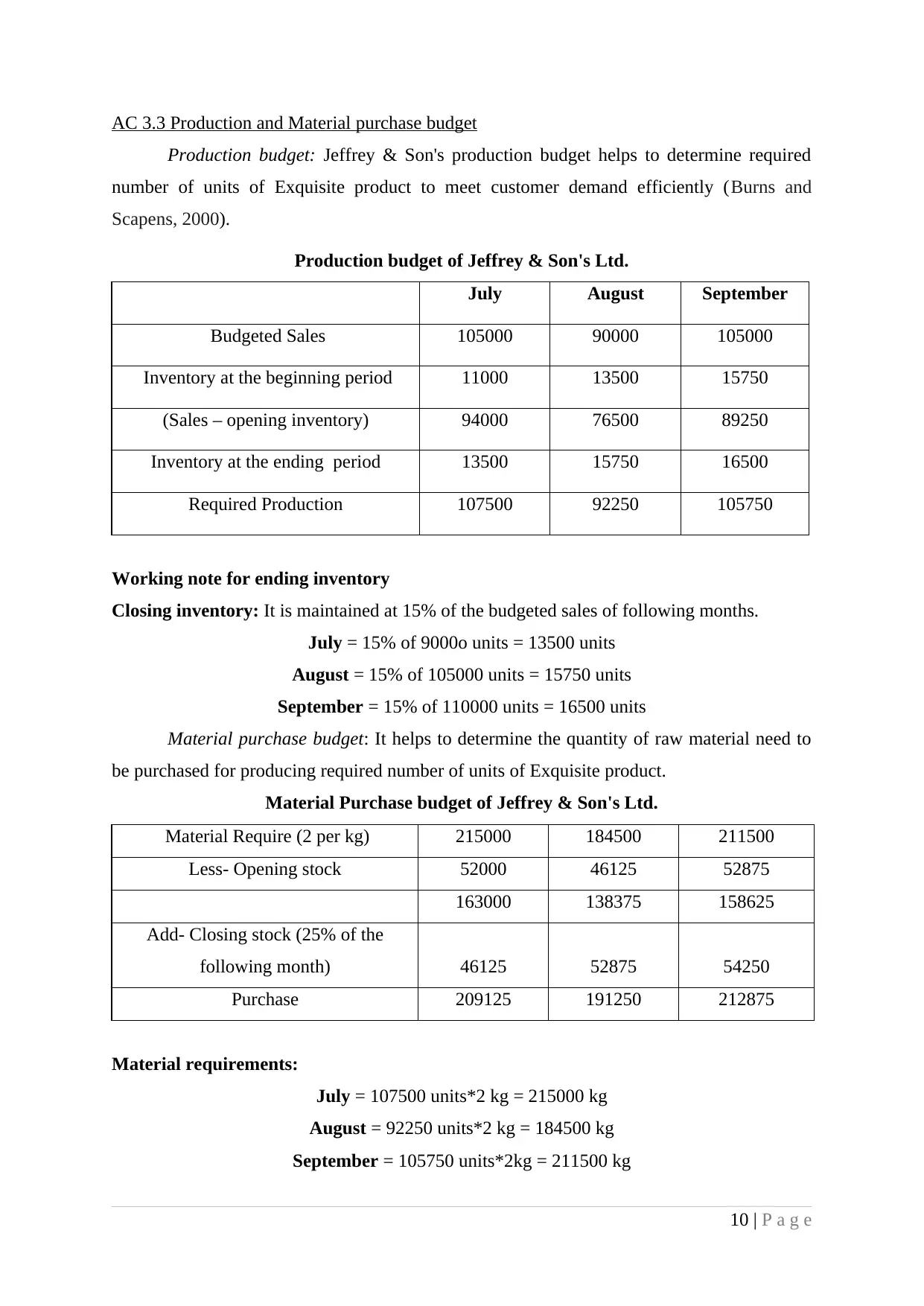

AC 3.3 Production and Material purchase budget

Production budget: Jeffrey & Son's production budget helps to determine required

number of units of Exquisite product to meet customer demand efficiently (Burns and

Scapens, 2000).

Production budget of Jeffrey & Son's Ltd.

July August September

Budgeted Sales 105000 90000 105000

Inventory at the beginning period 11000 13500 15750

(Sales – opening inventory) 94000 76500 89250

Inventory at the ending period 13500 15750 16500

Required Production 107500 92250 105750

Working note for ending inventory

Closing inventory: It is maintained at 15% of the budgeted sales of following months.

July = 15% of 9000o units = 13500 units

August = 15% of 105000 units = 15750 units

September = 15% of 110000 units = 16500 units

Material purchase budget: It helps to determine the quantity of raw material need to

be purchased for producing required number of units of Exquisite product.

Material Purchase budget of Jeffrey & Son's Ltd.

Material Require (2 per kg) 215000 184500 211500

Less- Opening stock 52000 46125 52875

163000 138375 158625

Add- Closing stock (25% of the

following month) 46125 52875 54250

Purchase 209125 191250 212875

Material requirements:

July = 107500 units*2 kg = 215000 kg

August = 92250 units*2 kg = 184500 kg

September = 105750 units*2kg = 211500 kg

10 | P a g e

Production budget: Jeffrey & Son's production budget helps to determine required

number of units of Exquisite product to meet customer demand efficiently (Burns and

Scapens, 2000).

Production budget of Jeffrey & Son's Ltd.

July August September

Budgeted Sales 105000 90000 105000

Inventory at the beginning period 11000 13500 15750

(Sales – opening inventory) 94000 76500 89250

Inventory at the ending period 13500 15750 16500

Required Production 107500 92250 105750

Working note for ending inventory

Closing inventory: It is maintained at 15% of the budgeted sales of following months.

July = 15% of 9000o units = 13500 units

August = 15% of 105000 units = 15750 units

September = 15% of 110000 units = 16500 units

Material purchase budget: It helps to determine the quantity of raw material need to

be purchased for producing required number of units of Exquisite product.

Material Purchase budget of Jeffrey & Son's Ltd.

Material Require (2 per kg) 215000 184500 211500

Less- Opening stock 52000 46125 52875

163000 138375 158625

Add- Closing stock (25% of the

following month) 46125 52875 54250

Purchase 209125 191250 212875

Material requirements:

July = 107500 units*2 kg = 215000 kg

August = 92250 units*2 kg = 184500 kg

September = 105750 units*2kg = 211500 kg

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.