A Detailed Report on Cost Calculation: Traditional and ABC Methods

VerifiedAdded on 2023/06/11

|7

|721

|109

Report

AI Summary

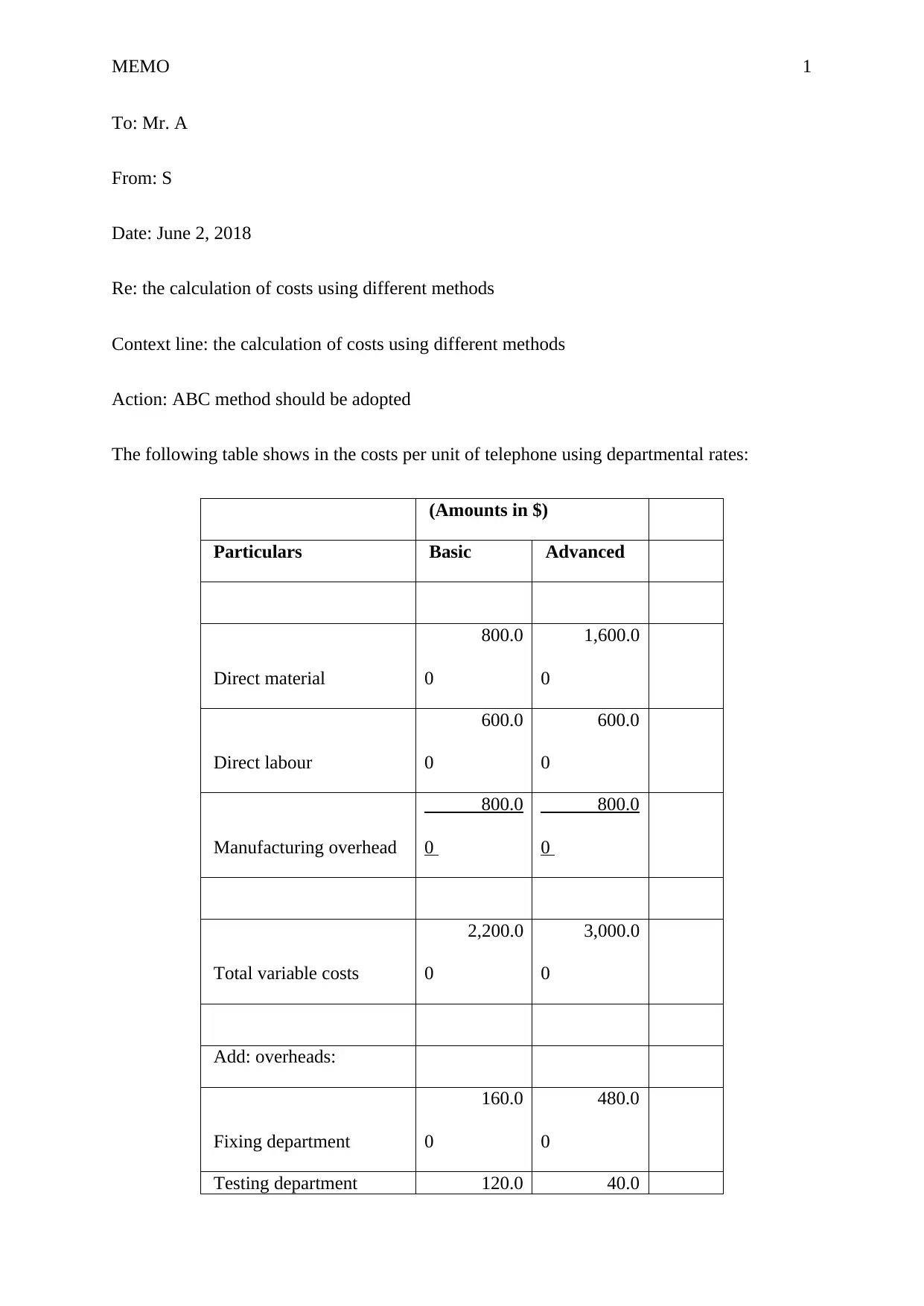

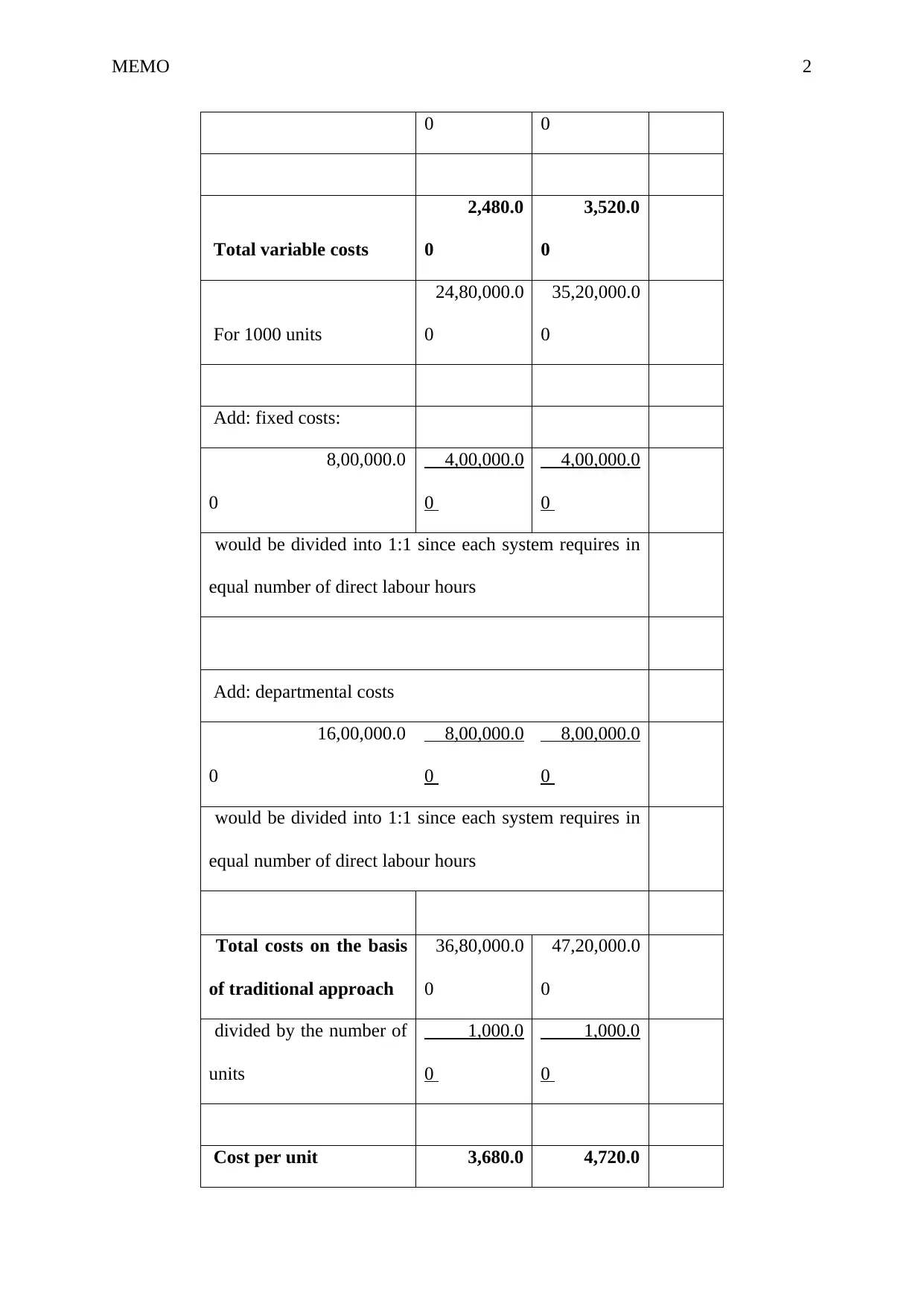

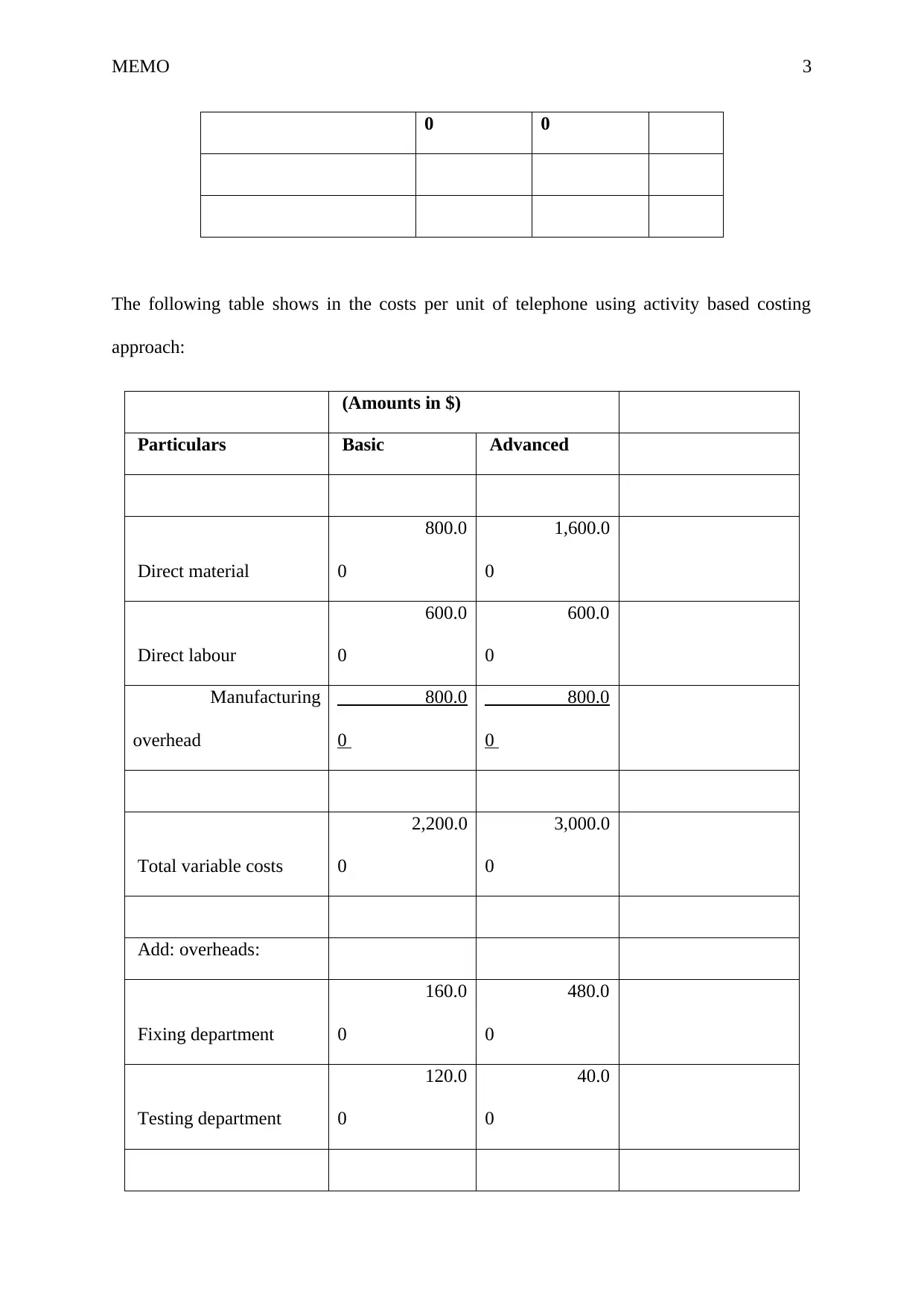

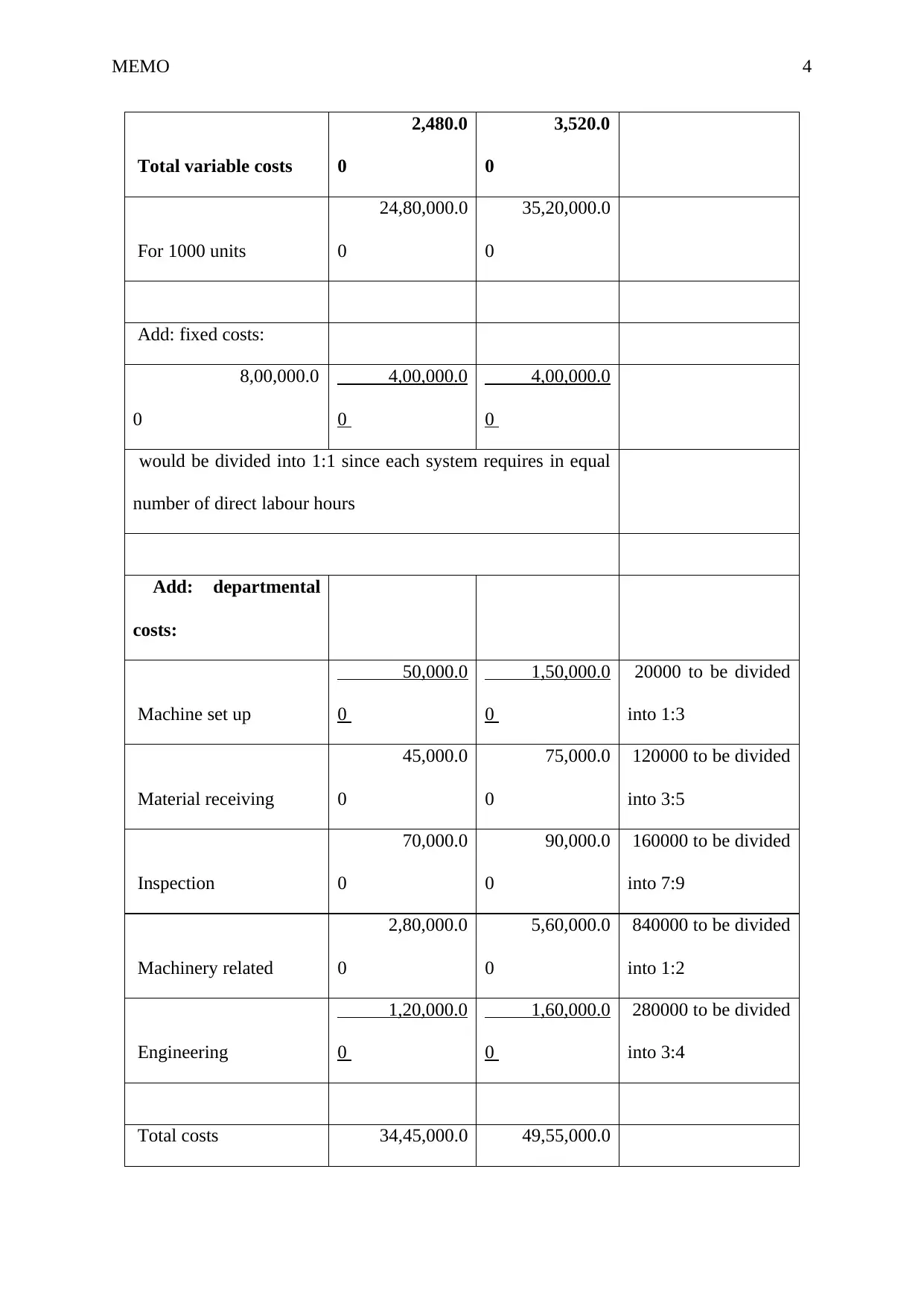

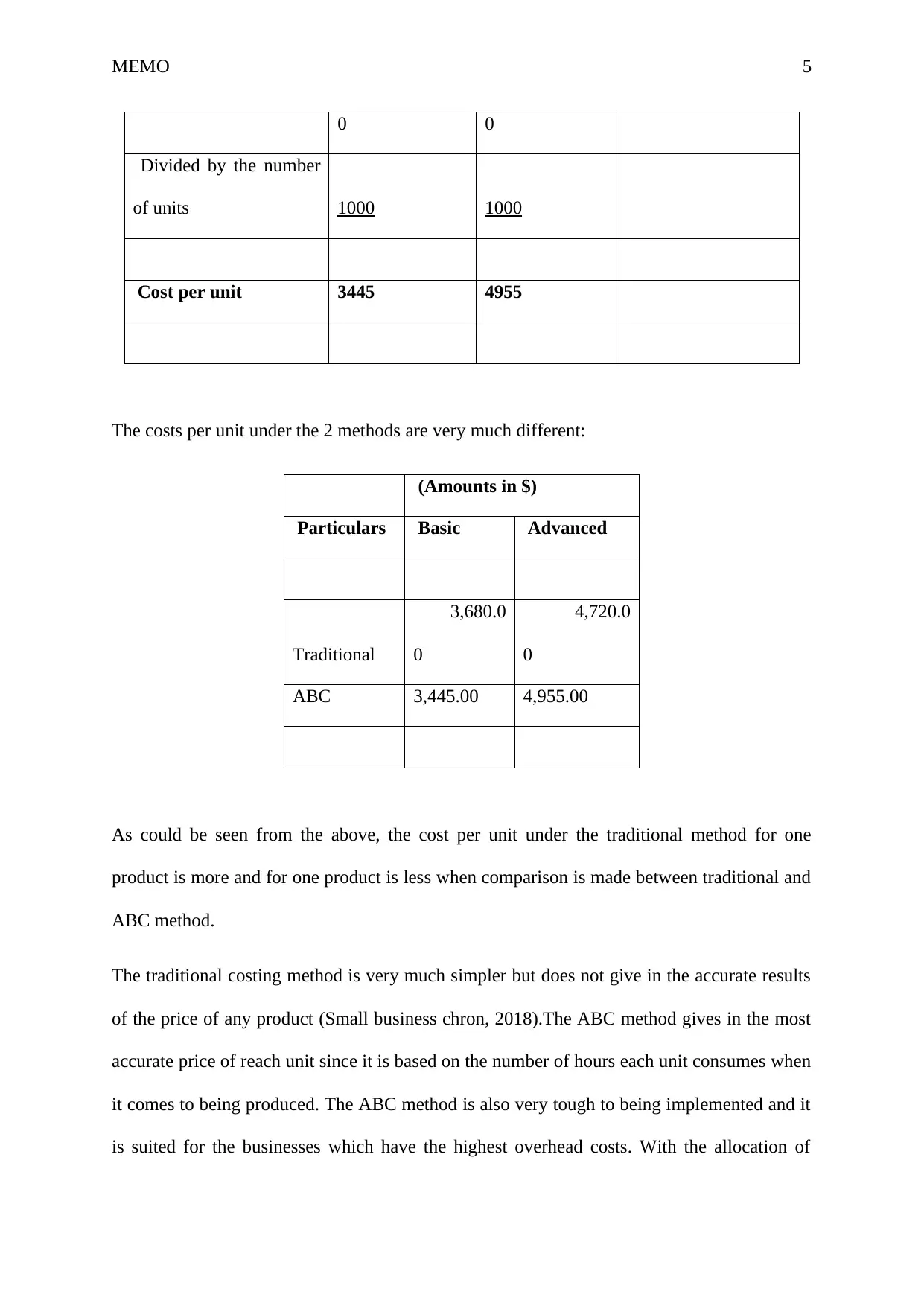

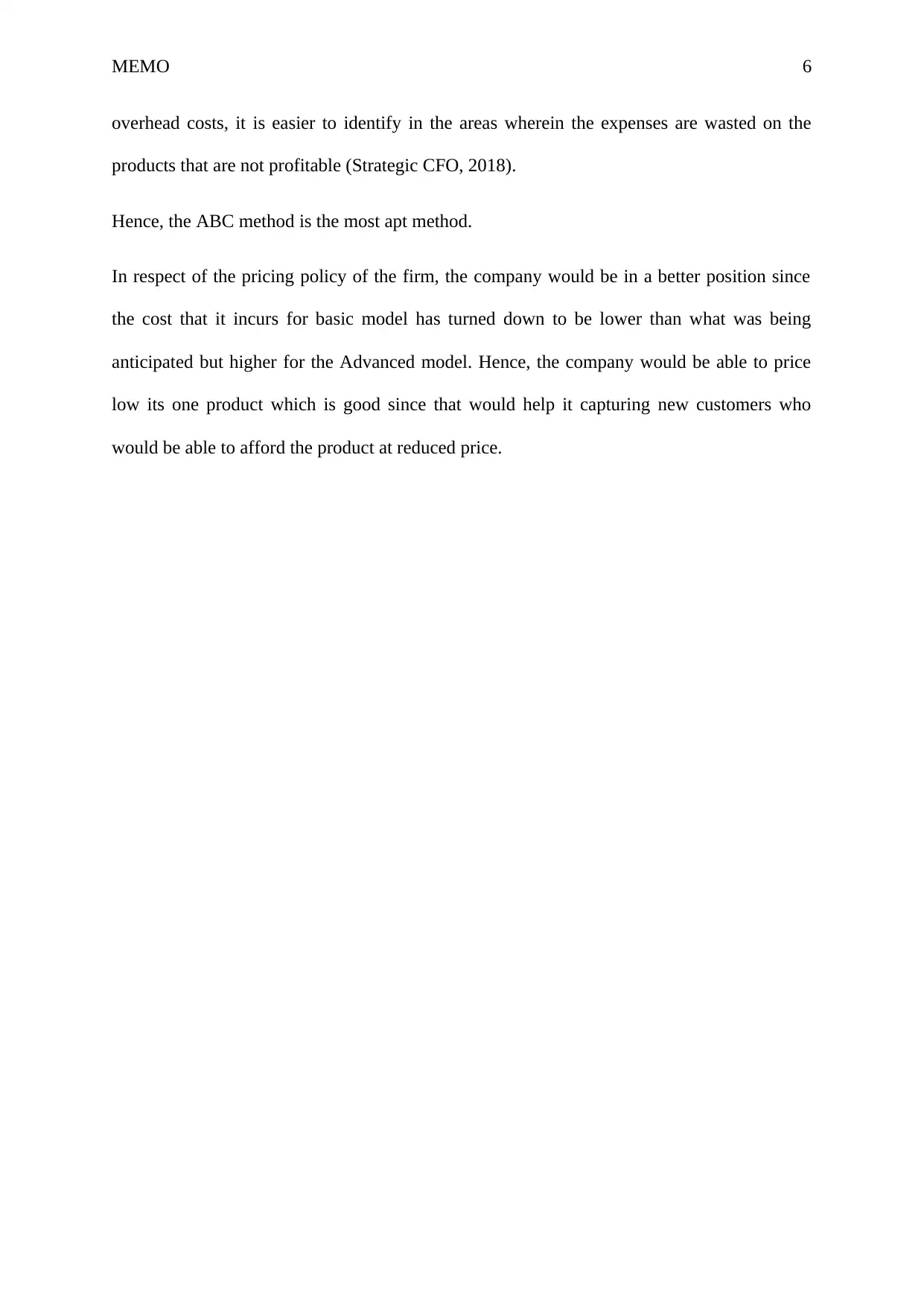

This report provides a comparative analysis of traditional costing methods and activity-based costing (ABC) methods for calculating the cost per unit of a telephone. It begins by presenting the cost per unit using departmental rates under the traditional method, highlighting direct material, direct labor, and manufacturing overhead. The report then calculates the total costs based on this traditional approach. Subsequently, the report delves into the activity-based costing approach, detailing costs associated with machine setup, material receiving, inspection, and engineering. The cost per unit is then determined using ABC. The report concludes that while traditional costing is simpler, ABC offers a more accurate price per unit by considering the number of hours each unit consumes during production, making it suitable for businesses with high overhead costs. The adoption of ABC method can help identify areas of wasted expenses on unprofitable products, ultimately improving the company's pricing policy and competitive positioning. Desklib provides access to this and many other solved assignments.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.