University Strategic Management Assignment: Cost of Capital Analysis

VerifiedAdded on 2022/10/04

|20

|3068

|20

Homework Assignment

AI Summary

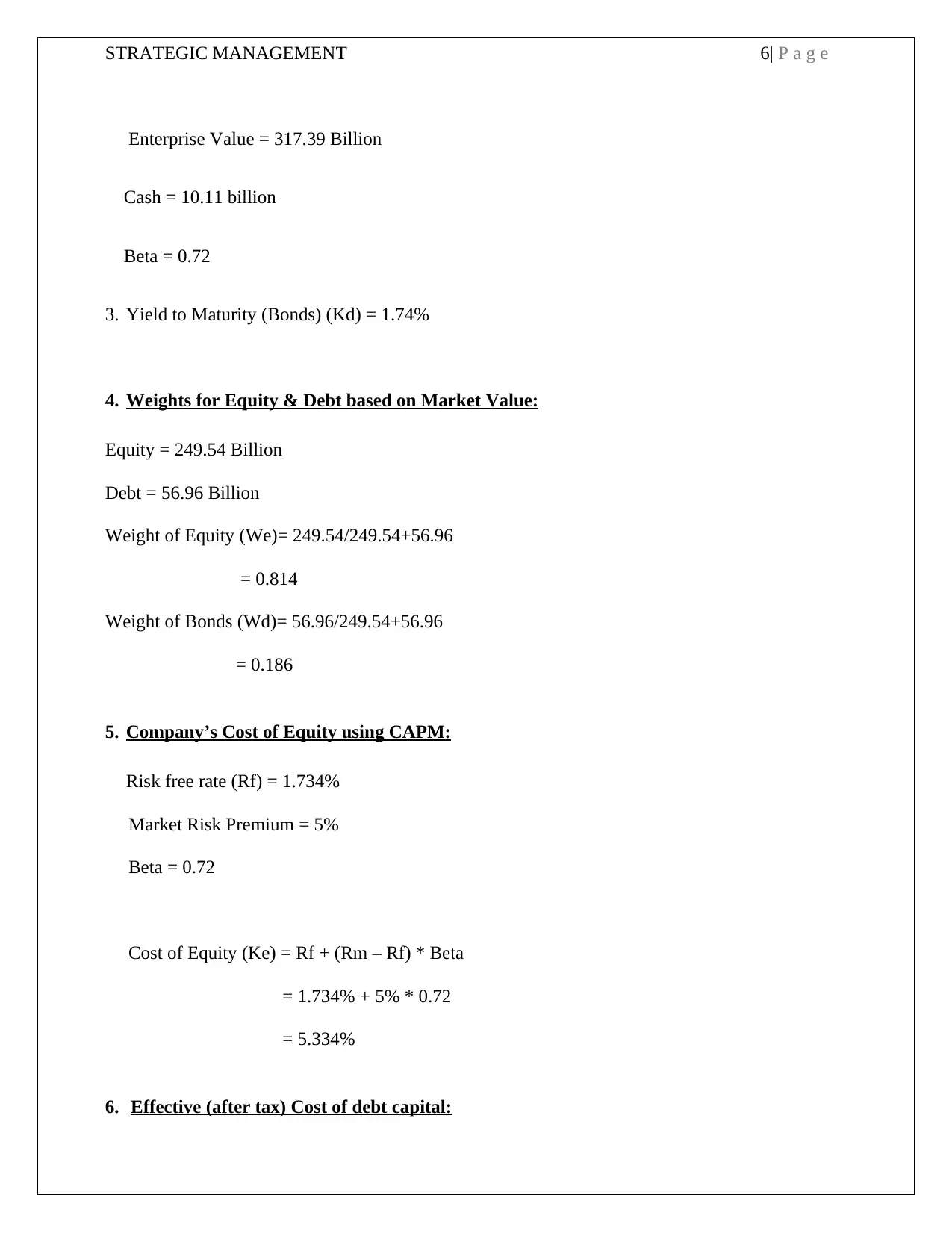

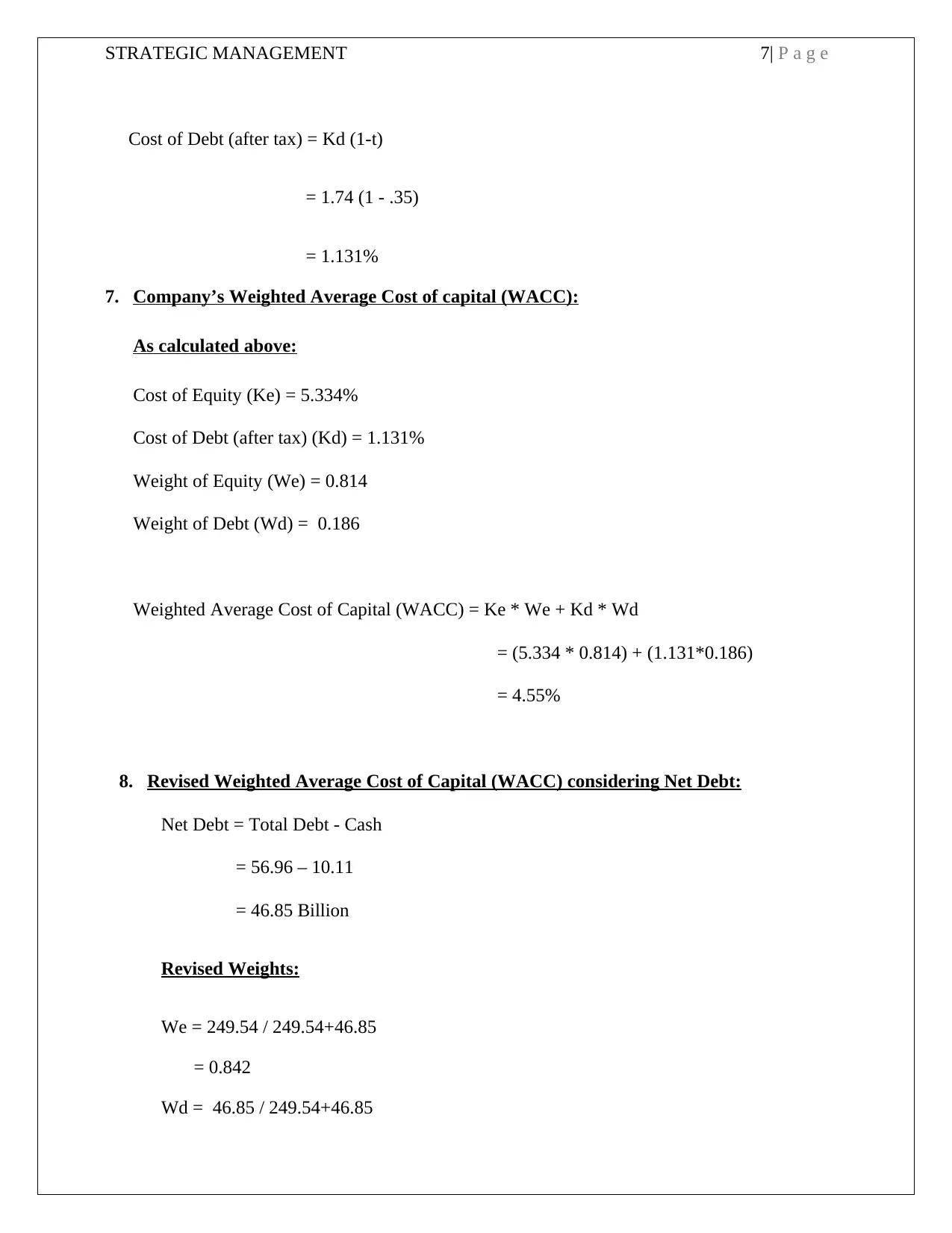

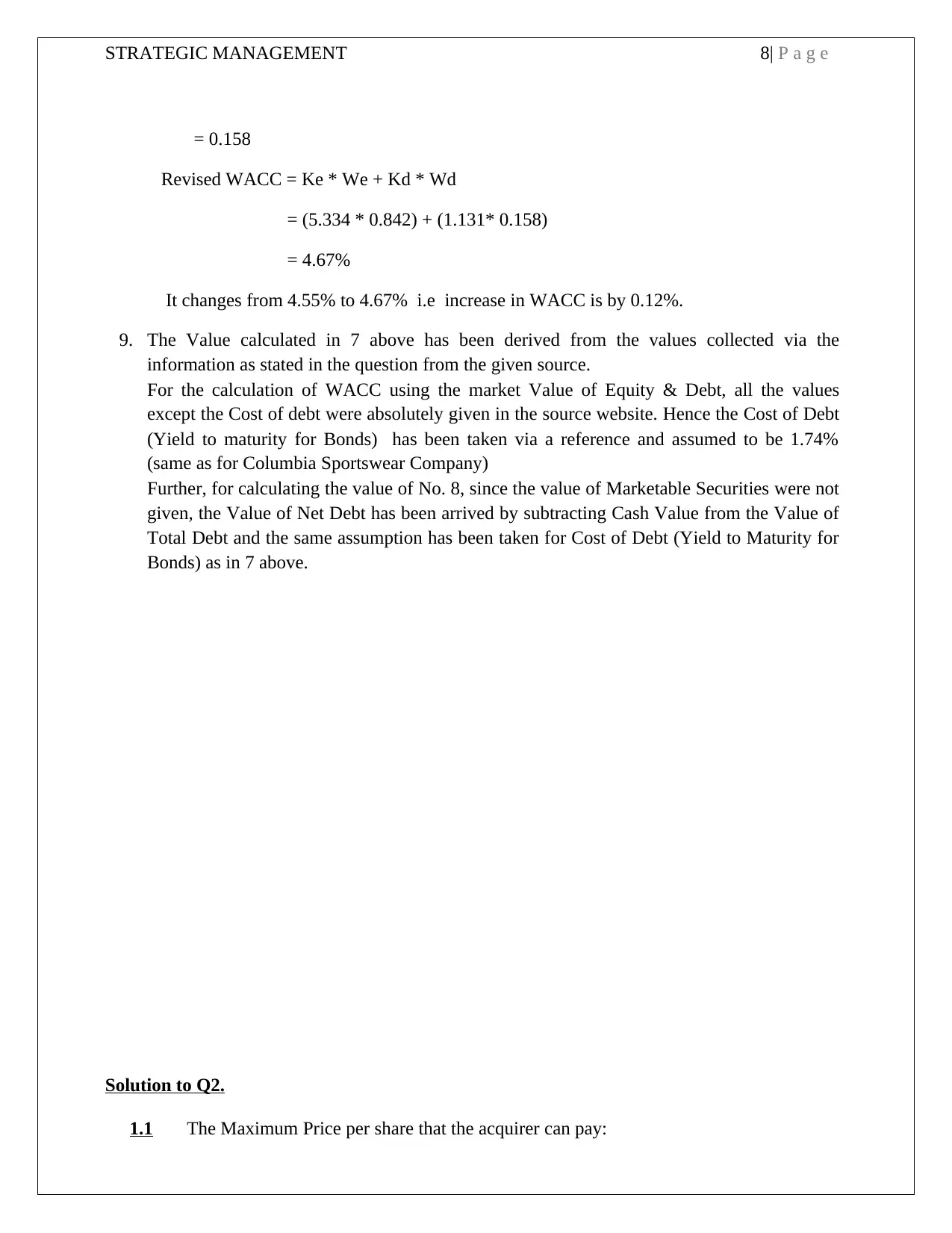

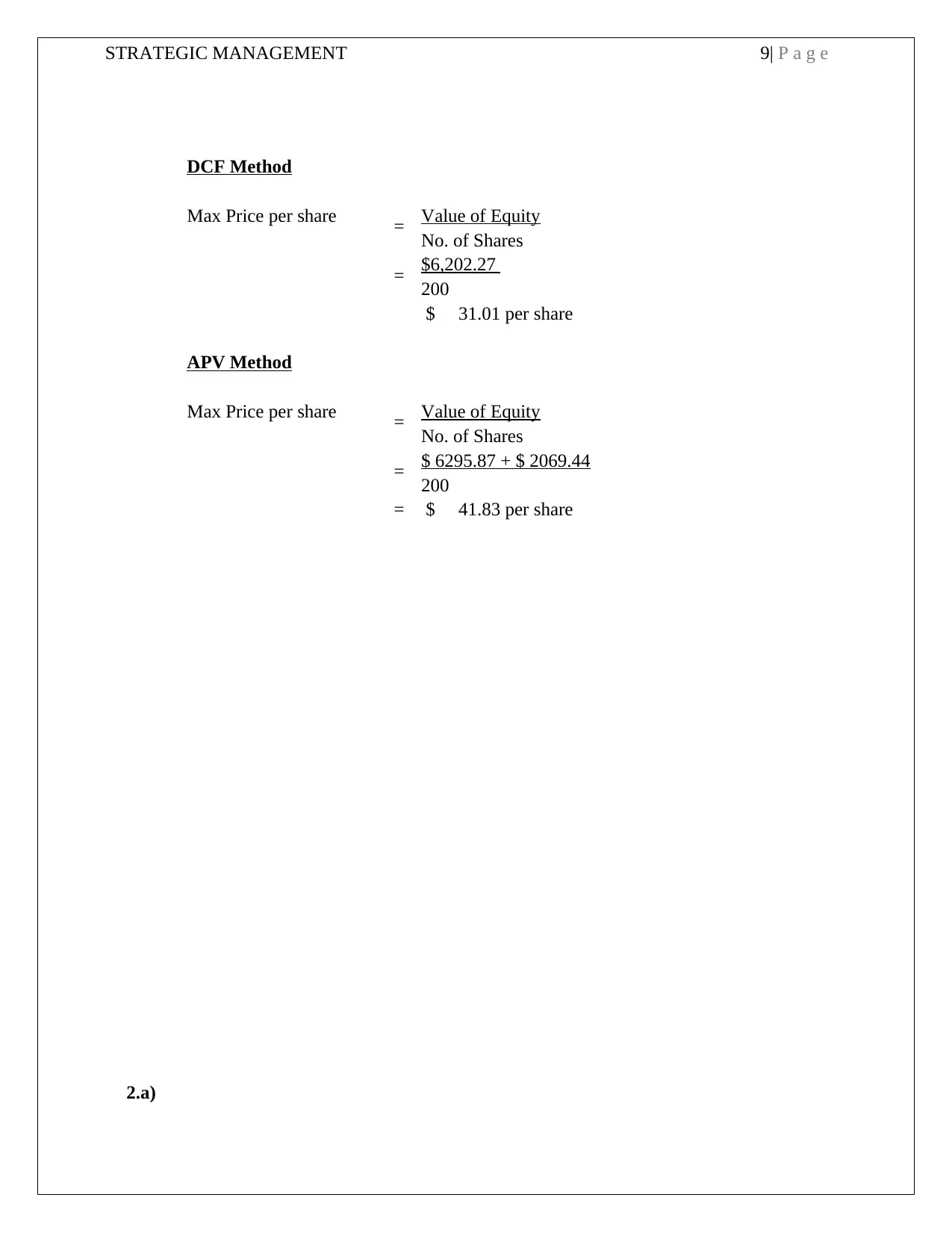

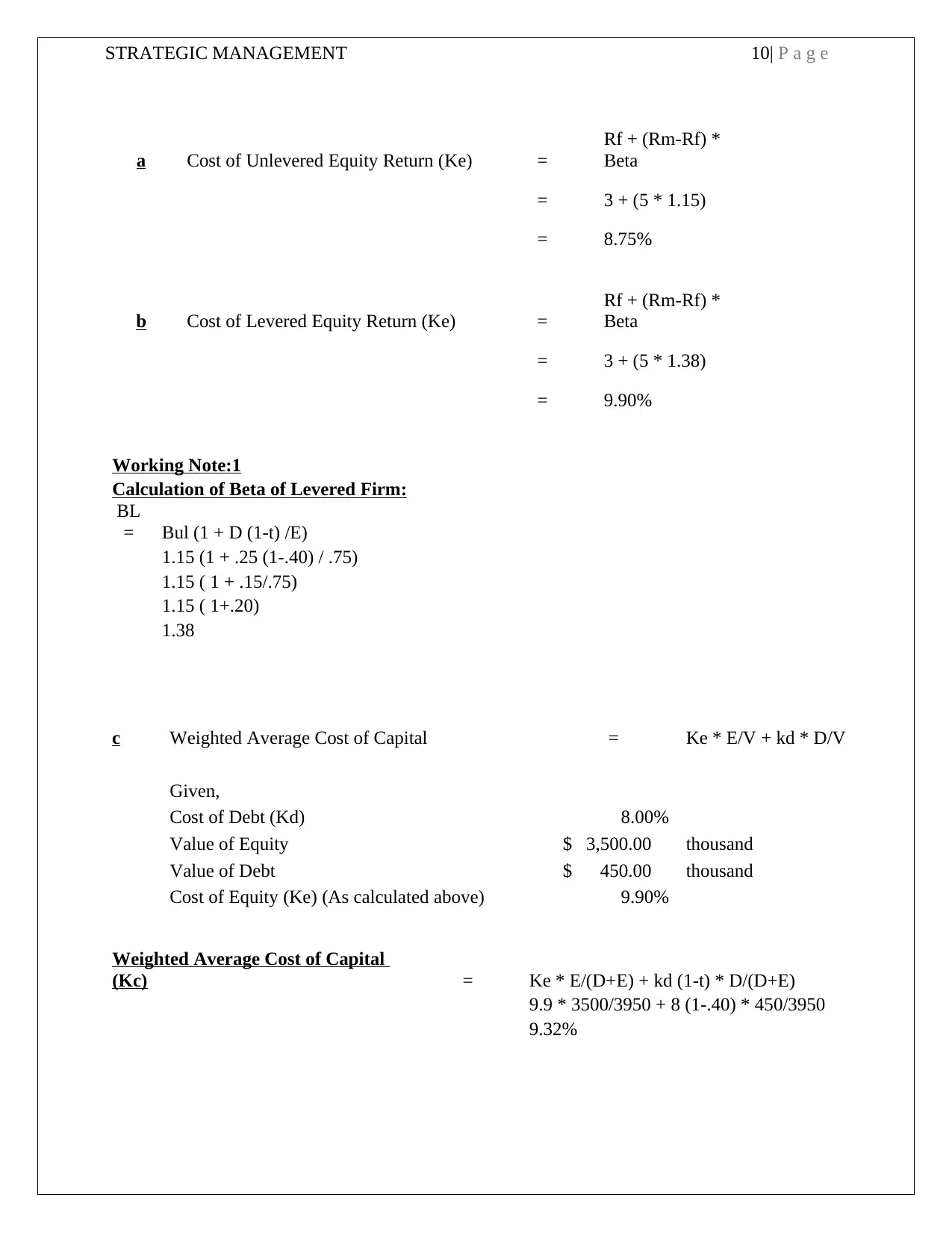

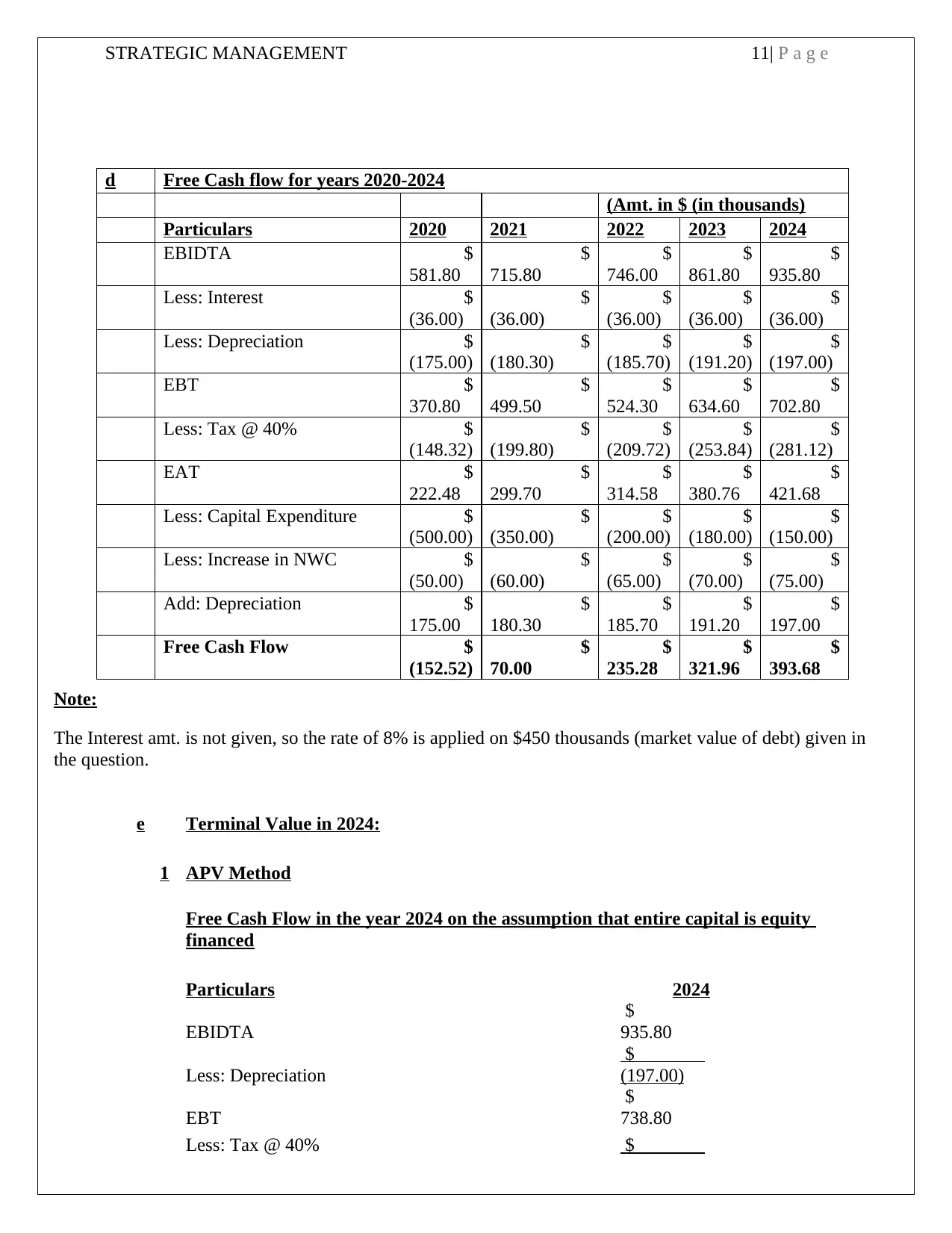

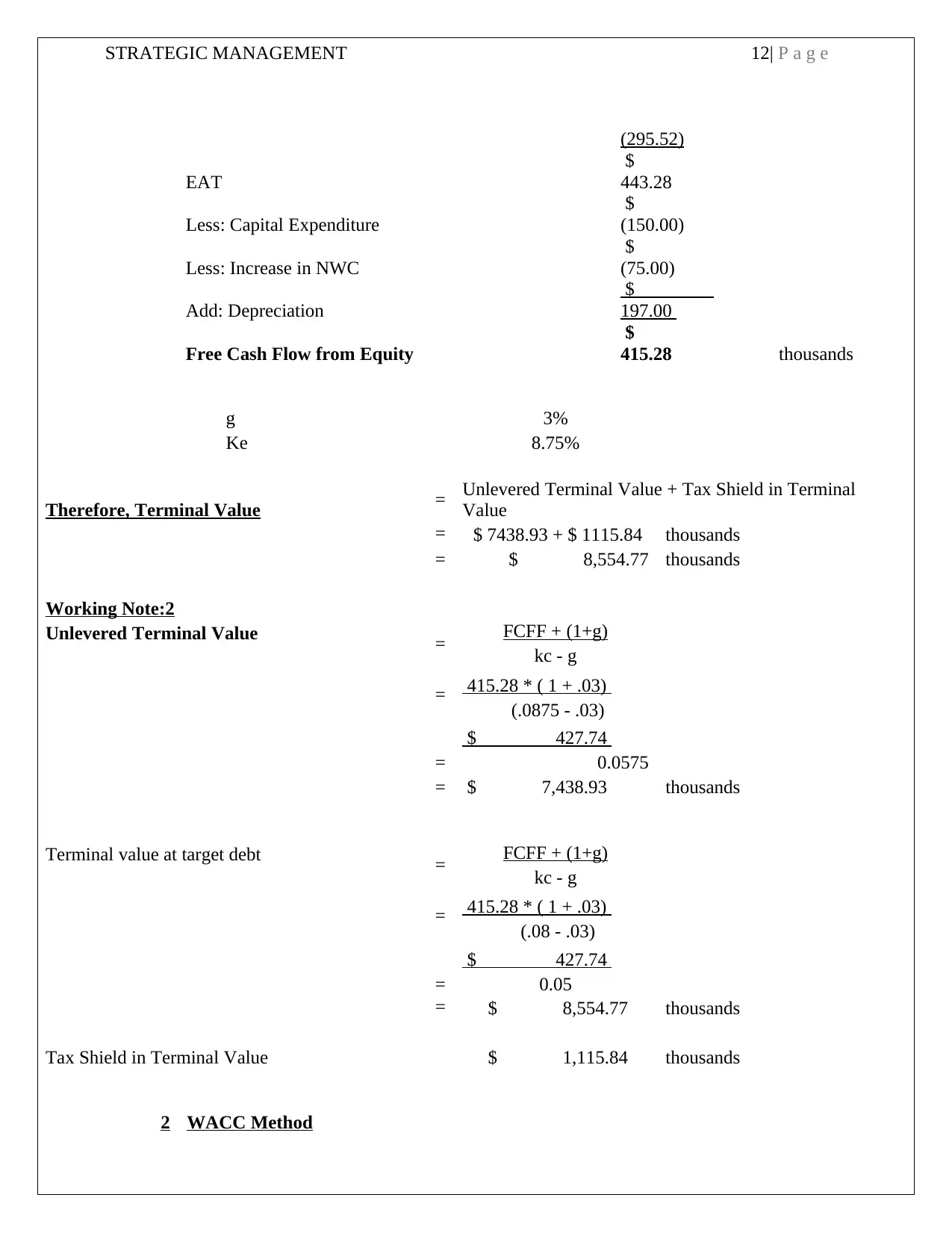

This assignment provides a detailed financial analysis of two companies, Columbia Sportswear and The Walt Disney Company, as part of a strategic management course. The solution encompasses the calculation of the Weighted Average Cost of Capital (WACC) using both market value and net debt considerations, along with the application of the Capital Asset Pricing Model (CAPM) to determine the cost of equity. The assignment also includes valuation using Discounted Cash Flow (DCF) and Adjusted Present Value (APV) methods to determine the maximum price per share in an acquisition scenario. The assignment also covers the calculation of free cash flow, terminal value using both the APV and WACC methods, and the value of a levered target firm using both APV and WACC methods. The calculations are thoroughly presented, demonstrating a strong understanding of financial modeling and valuation techniques. The assignment meets the requirements of the MGT 339 course at the university level, and addresses core concepts in strategic management and corporate finance, including the cost of capital and valuation in the context of mergers and acquisitions.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.