<University Name> THH3113: Cost Classification and Control Report

VerifiedAdded on 2022/10/02

|12

|2650

|411

Report

AI Summary

This report, prepared for THH3113 at , provides a comprehensive overview of cost classification and cost control techniques within a business context. It begins with an executive summary highlighting the importance of cost management for maximizing profits. The report then delves into various cost classifications, including variable, fixed, semi-fixed, semi-variable, direct, and indirect costs, providing detailed definitions and examples for each. Key concepts such as cost drivers and cost-based pricing are also examined. The report further explores cost control techniques, differentiating between internal and external methods, and discussing tools like budgetary control, standard control, ratio analysis, and value analysis. The analysis extends to specific examples, such as the DOSM case, where the report analyzes costs associated with event management, including venue costs, event staff, equipment, and social media expenses, and then determines the most acceptable offer for the business. This detailed examination provides a practical understanding of cost management principles and their application in real-world business scenarios.

Running head: THH3113 1

THH3113

<Name>

<University Name>

THH3113

<Name>

<University Name>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THH3113 2

Executive summary

Cost classification and cost control techniques are considered as one of the most

important and significant areas in the business to ensure that profit are maximized by

minimizing on expenses. The article gives a brief explanation on the importance of a

business management to categorize various costs based on the individual unit of an item

that would result to a change in the overall costs. These costs include variable costs,

semi-variable, semi- fixed, direct and indirect costs. During distribution of these costs the

business should ensure to use various cost control techniques such as value analysis, ratio

analysis, budget control and standard control to ensure cost incurred bring an added value

to the business. In addition to that, it shows the need of the organization to input cost

based on pricing which is the activity of setting prices based on the cost of producing a

product and providing a service. This article provided means that made it possible to

learn and study on a section of cost classification, cost drivers, cost control techniques

and its application in real business venture to identify most profitable business

opportunity.

Executive summary

Cost classification and cost control techniques are considered as one of the most

important and significant areas in the business to ensure that profit are maximized by

minimizing on expenses. The article gives a brief explanation on the importance of a

business management to categorize various costs based on the individual unit of an item

that would result to a change in the overall costs. These costs include variable costs,

semi-variable, semi- fixed, direct and indirect costs. During distribution of these costs the

business should ensure to use various cost control techniques such as value analysis, ratio

analysis, budget control and standard control to ensure cost incurred bring an added value

to the business. In addition to that, it shows the need of the organization to input cost

based on pricing which is the activity of setting prices based on the cost of producing a

product and providing a service. This article provided means that made it possible to

learn and study on a section of cost classification, cost drivers, cost control techniques

and its application in real business venture to identify most profitable business

opportunity.

THH3113 3

Table of Contents

Executive summary.........................................................................................................................2

Variable costs..................................................................................................................................4

Fixed costs.......................................................................................................................................4

Semi-fixed cost.................................................................................................................................4

Semi-variable cost...........................................................................................................................4

Direct cost........................................................................................................................................4

Direct material.................................................................................................................................5

Direct labour...................................................................................................................................5

Directed expenses............................................................................................................................5

Indirect cost.....................................................................................................................................5

Indirect material..............................................................................................................................5

Indirect labour.................................................................................................................................5

Indirect expenses.............................................................................................................................5

Cost drivers......................................................................................................................................5

Cost-based pricing...........................................................................................................................5

Cost control.....................................................................................................................................6

Cost control techniques...................................................................................................................6

Tools of cost control........................................................................................................................6

Internal............................................................................................................................................6

Budgetary control............................................................................................................................6

Standard control..............................................................................................................................6

External............................................................................................................................................7

Ratio analysis...................................................................................................................................7

Value analysis..................................................................................................................................7

Appendices.....................................................................................................................................10

References......................................................................................................................................12

Table of Contents

Executive summary.........................................................................................................................2

Variable costs..................................................................................................................................4

Fixed costs.......................................................................................................................................4

Semi-fixed cost.................................................................................................................................4

Semi-variable cost...........................................................................................................................4

Direct cost........................................................................................................................................4

Direct material.................................................................................................................................5

Direct labour...................................................................................................................................5

Directed expenses............................................................................................................................5

Indirect cost.....................................................................................................................................5

Indirect material..............................................................................................................................5

Indirect labour.................................................................................................................................5

Indirect expenses.............................................................................................................................5

Cost drivers......................................................................................................................................5

Cost-based pricing...........................................................................................................................5

Cost control.....................................................................................................................................6

Cost control techniques...................................................................................................................6

Tools of cost control........................................................................................................................6

Internal............................................................................................................................................6

Budgetary control............................................................................................................................6

Standard control..............................................................................................................................6

External............................................................................................................................................7

Ratio analysis...................................................................................................................................7

Value analysis..................................................................................................................................7

Appendices.....................................................................................................................................10

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

THH3113 4

Task 1: Categorizing costs based on the cost drivers and evaluating examples of cost

drivers in DOSM

Classification of costs according to costs drivers, (Toompuu, & Põlajeva, 2014).

Variable costs

These are type of costs that rises or falls relatively with the amount of venture that is, it is the

portion of the cost of a venture that changes with the amount of output. The cost level, for

instance, is one then production is one.

The cost rises equally with the rise in the undertaking level; thus the variable cost function is

given by a clear line starting at the origin of the graph

This cost is considered as a cost driver as a change in a unit of activity may result in a

proportionate difference in the cost of the venture or the operational costs

This activity base is an amount of effort that operates as a natural component in the incurrence of

variable costs. Therefore, in managing these costs, cost accountants should be very familiar with

the various cost drivers (operation bases) within the business

Examples of variable costs are remuneration paid to casual staff paid on an hourly basis and

number of customers served in a given event at the agreed time. With variable costs, the cost

level is one when manufacture is one.

Fixed costs

These are costs that do not vary with the amount of production. It is also known autonomous

cost, as it remains the constant regardless of the output level.

Fixed costs that cannot be avoided in the short run are called committed fixed costs. They

sometimes are also referred to as capacity costs. Such costs concern senior managers for strategic

decision making. Discretionary fixed costs are those that can entirely be avoided without having

an immediate impact on the level of activity. These costs are subject to management decision e.g.

advertisement costs.

Semi-fixed cost

These are costs that have a fixed and variable cost factors. The fixed factor is that part that does

not change with the amount of output. They are variable within a given venture level but are

constant within other venture levels

The variable part is considered as the cost that rises or falls relatively with the level of

undertaking

They are sometimes referred to as step costs.

Semi-variable cost

These are costs with both a fixed and variable cost factor. The fixed factor is that part which does

not vary regardless of the level of production. They change within particular activity quantities

but are constant within other production levels.

Direct cost

These refer to costs that can be immediately associated with and traced in the production of a

given object at a particular level of activity. Direct costs include:

Task 1: Categorizing costs based on the cost drivers and evaluating examples of cost

drivers in DOSM

Classification of costs according to costs drivers, (Toompuu, & Põlajeva, 2014).

Variable costs

These are type of costs that rises or falls relatively with the amount of venture that is, it is the

portion of the cost of a venture that changes with the amount of output. The cost level, for

instance, is one then production is one.

The cost rises equally with the rise in the undertaking level; thus the variable cost function is

given by a clear line starting at the origin of the graph

This cost is considered as a cost driver as a change in a unit of activity may result in a

proportionate difference in the cost of the venture or the operational costs

This activity base is an amount of effort that operates as a natural component in the incurrence of

variable costs. Therefore, in managing these costs, cost accountants should be very familiar with

the various cost drivers (operation bases) within the business

Examples of variable costs are remuneration paid to casual staff paid on an hourly basis and

number of customers served in a given event at the agreed time. With variable costs, the cost

level is one when manufacture is one.

Fixed costs

These are costs that do not vary with the amount of production. It is also known autonomous

cost, as it remains the constant regardless of the output level.

Fixed costs that cannot be avoided in the short run are called committed fixed costs. They

sometimes are also referred to as capacity costs. Such costs concern senior managers for strategic

decision making. Discretionary fixed costs are those that can entirely be avoided without having

an immediate impact on the level of activity. These costs are subject to management decision e.g.

advertisement costs.

Semi-fixed cost

These are costs that have a fixed and variable cost factors. The fixed factor is that part that does

not change with the amount of output. They are variable within a given venture level but are

constant within other venture levels

The variable part is considered as the cost that rises or falls relatively with the level of

undertaking

They are sometimes referred to as step costs.

Semi-variable cost

These are costs with both a fixed and variable cost factor. The fixed factor is that part which does

not vary regardless of the level of production. They change within particular activity quantities

but are constant within other production levels.

Direct cost

These refer to costs that can be immediately associated with and traced in the production of a

given object at a particular level of activity. Direct costs include:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THH3113 5

Direct material

This refers to costs incurred in the acquisition of physical inputs involved in the production

process; these materials include raw materials, work in progress and consumable materials

Direct labour

These are wages paid to employees whose efforts can be traceable to the production of a product

Directed expenses

These are costs incurred on expenses which can be directly associated with the production

process

Indirect cost

These refer to costs that cannot be immediately associated with and traced in the production of a

given object at a particular level of activity. Indirect costs include:

Indirect material

This refers to the cost incurred in the acquisition of physical inputs involved in the production

process but cannot be immediately traced to the production process, these materials include raw

materials, work in progress and consumable materials

Indirect labour

These are wages paid to employees whose efforts cannot be immediately traced to the production

of a product

Indirect expenses

These are costs incurred on expenses which cannot be directly associated with the production

processes

Cost drivers

These refer to a unit of an object or component that would result to change in the overall cost,

(Ratnatunga, Michael, & Balachandran, 2012).

In the case of DOSM the cost drove cost for instance in the first event are:

Event staff this cost incurred is a cost-driven cost since a unit change in the number of staff

needed, number of hours worked and the wage rate per hour will change the cost. The other cost

driven factors include the number of chairs needed.

In the second event include number of mats, the event staff and the display screens required, any

change in the numbers of these items will result in a corresponding change in the cost incurred

by the organization.

Task 2: Analysis of costs directly associated with pricing and the cost control techniques

Cost-based pricing

This refers to the activity of mounting or making prices in relation to the costs suffered in the

manufacture or delivery of goods and services.

Direct material

This refers to costs incurred in the acquisition of physical inputs involved in the production

process; these materials include raw materials, work in progress and consumable materials

Direct labour

These are wages paid to employees whose efforts can be traceable to the production of a product

Directed expenses

These are costs incurred on expenses which can be directly associated with the production

process

Indirect cost

These refer to costs that cannot be immediately associated with and traced in the production of a

given object at a particular level of activity. Indirect costs include:

Indirect material

This refers to the cost incurred in the acquisition of physical inputs involved in the production

process but cannot be immediately traced to the production process, these materials include raw

materials, work in progress and consumable materials

Indirect labour

These are wages paid to employees whose efforts cannot be immediately traced to the production

of a product

Indirect expenses

These are costs incurred on expenses which cannot be directly associated with the production

processes

Cost drivers

These refer to a unit of an object or component that would result to change in the overall cost,

(Ratnatunga, Michael, & Balachandran, 2012).

In the case of DOSM the cost drove cost for instance in the first event are:

Event staff this cost incurred is a cost-driven cost since a unit change in the number of staff

needed, number of hours worked and the wage rate per hour will change the cost. The other cost

driven factors include the number of chairs needed.

In the second event include number of mats, the event staff and the display screens required, any

change in the numbers of these items will result in a corresponding change in the cost incurred

by the organization.

Task 2: Analysis of costs directly associated with pricing and the cost control techniques

Cost-based pricing

This refers to the activity of mounting or making prices in relation to the costs suffered in the

manufacture or delivery of goods and services.

THH3113 6

The advantage of cost-based pricing and cost-plus prices is that the business is always

guaranteed to generating profit from this practice.

Event staff this is a cost directly associated with the general price of the service being delivered,

this cost is related to price in that the amount of time taken by each worker to provide a service

will determine the amount of profit gained on the cost on an hourly basis, therefore, time

management as a cost control techniques is important.

Secondly, the number of staff needed to ensure that services are delivered effectively and

efficiently by DOSM is another factor that will influence event staff to be cost-related as the

number of staff hired, if many will ensure more service is delivered in the shortest time possible

and the extra cost incurred on staff added to the price of the service.

Cost control

This refers to the regulation by the executive management to oversee that; there is a balance of

cost incurred in a given undertaking to ensure target of sales is attained.

Cost control techniques

This can be defined as various methods used by a business to attain maximum profit at the

lowest possible cost, (Arce, Mac, Shah, & Vega, 2012).

Tools of cost control

The techniques or tools used in controlling the costs incurred in the business attain given

standards into controlling costs these are:

Internal

The internal standards are used to regulate, control and evaluate the costs incurred within the

firm for instance cost on labor, material or other expenses

Internal cost controlling standards established include:

Budgetary control

A budget refers to a forecast financial statement showing the revenues and the expenses of a

business in a particular period of time.

Budgeting refers to the expression or articulation of a plan in an organization in numerical terms

Budgetary control, therefore, refers to a technique that uses budgets as way of planning and

controlling every detail or part of an organization’s activity.

The advantage of budgetary control is that it provides and sets a clear policy and defines the set

targets and objectives of a particular undertaking of the organization

Budgetary control also enhances adequate and proper planning and control of costs by

integrating the various activities in the organization

Standard control

This the most commonly used cost control technique as its objective is to define the set standards

of performance and set cost targets to be attained under a particular working situation.

Standard control can, therefore, be defined as the technique that aims at predetermining cost

which can be associated with a particular product or service under a certain condition.

The advantage of cost-based pricing and cost-plus prices is that the business is always

guaranteed to generating profit from this practice.

Event staff this is a cost directly associated with the general price of the service being delivered,

this cost is related to price in that the amount of time taken by each worker to provide a service

will determine the amount of profit gained on the cost on an hourly basis, therefore, time

management as a cost control techniques is important.

Secondly, the number of staff needed to ensure that services are delivered effectively and

efficiently by DOSM is another factor that will influence event staff to be cost-related as the

number of staff hired, if many will ensure more service is delivered in the shortest time possible

and the extra cost incurred on staff added to the price of the service.

Cost control

This refers to the regulation by the executive management to oversee that; there is a balance of

cost incurred in a given undertaking to ensure target of sales is attained.

Cost control techniques

This can be defined as various methods used by a business to attain maximum profit at the

lowest possible cost, (Arce, Mac, Shah, & Vega, 2012).

Tools of cost control

The techniques or tools used in controlling the costs incurred in the business attain given

standards into controlling costs these are:

Internal

The internal standards are used to regulate, control and evaluate the costs incurred within the

firm for instance cost on labor, material or other expenses

Internal cost controlling standards established include:

Budgetary control

A budget refers to a forecast financial statement showing the revenues and the expenses of a

business in a particular period of time.

Budgeting refers to the expression or articulation of a plan in an organization in numerical terms

Budgetary control, therefore, refers to a technique that uses budgets as way of planning and

controlling every detail or part of an organization’s activity.

The advantage of budgetary control is that it provides and sets a clear policy and defines the set

targets and objectives of a particular undertaking of the organization

Budgetary control also enhances adequate and proper planning and control of costs by

integrating the various activities in the organization

Standard control

This the most commonly used cost control technique as its objective is to define the set standards

of performance and set cost targets to be attained under a particular working situation.

Standard control can, therefore, be defined as the technique that aims at predetermining cost

which can be associated with a particular product or service under a certain condition.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

THH3113 7

The merit of standard control is that it provides the management with a basis of setting prices

and shift costs in order to achieve maximum use of plant capacity and enhance cost reduction to

be able to generate higher returns

External

These are set of standards used by the organization to compare its performance with other

organization in order to come up with and shape a given number of cost ratios

The external cost control techniques include:

Ratio analysis

This is the most prominently used external standard used by an organization to compare

performance with other organizations and control costs.

The ratio refers to a yardstick used to provide estimates on the relationship between two

numbers.

An acceptable ratio is therefore first formulated then used to compare the actual performance and

the anticipated performance to come up with corrective courses of action to control costs

Value analysis

This is a system involved in cost saving by first analyzing the product design

The main advantage of value analysis is that it aims at identifying costs in a product which does

not in any way add functional value, thus it helps in cost reduction without necessarily affecting

the standard of which performance was set.

Ultimately, value analysis is a system which specifies the use of a product or its units and

formulates relevant costs, come up with various alternatives and evaluates them

The merit of value analysis is that it helps in cost reduction through proper evaluation of all the

necessary costs to be incurred in the production of a given production without necessarily giving

up the anticipated standards of performance laid out.

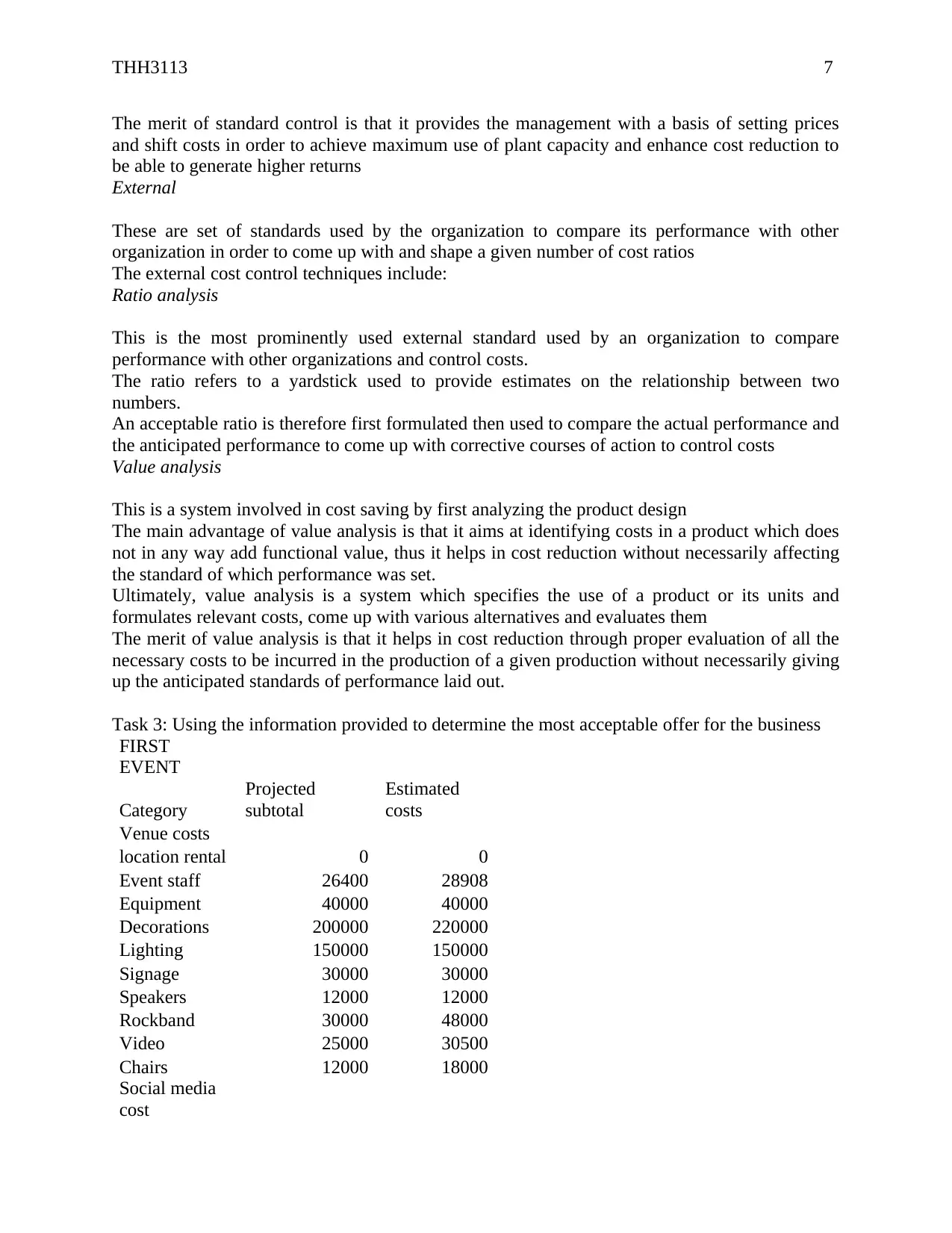

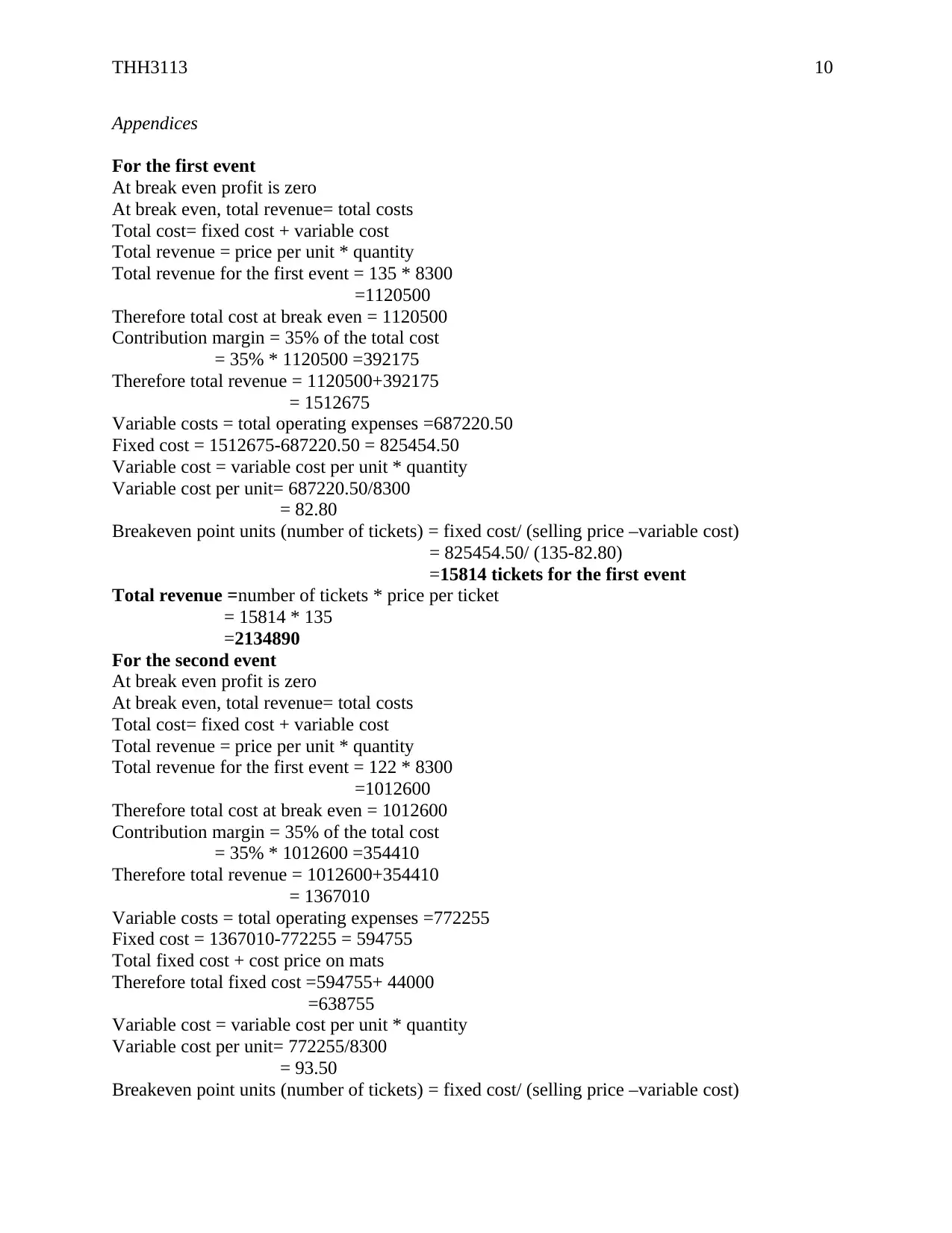

Task 3: Using the information provided to determine the most acceptable offer for the business

FIRST

EVENT

Category

Projected

subtotal

Estimated

costs

Venue costs

location rental 0 0

Event staff 26400 28908

Equipment 40000 40000

Decorations 200000 220000

Lighting 150000 150000

Signage 30000 30000

Speakers 12000 12000

Rockband 30000 48000

Video 25000 30500

Chairs 12000 18000

Social media

cost

The merit of standard control is that it provides the management with a basis of setting prices

and shift costs in order to achieve maximum use of plant capacity and enhance cost reduction to

be able to generate higher returns

External

These are set of standards used by the organization to compare its performance with other

organization in order to come up with and shape a given number of cost ratios

The external cost control techniques include:

Ratio analysis

This is the most prominently used external standard used by an organization to compare

performance with other organizations and control costs.

The ratio refers to a yardstick used to provide estimates on the relationship between two

numbers.

An acceptable ratio is therefore first formulated then used to compare the actual performance and

the anticipated performance to come up with corrective courses of action to control costs

Value analysis

This is a system involved in cost saving by first analyzing the product design

The main advantage of value analysis is that it aims at identifying costs in a product which does

not in any way add functional value, thus it helps in cost reduction without necessarily affecting

the standard of which performance was set.

Ultimately, value analysis is a system which specifies the use of a product or its units and

formulates relevant costs, come up with various alternatives and evaluates them

The merit of value analysis is that it helps in cost reduction through proper evaluation of all the

necessary costs to be incurred in the production of a given production without necessarily giving

up the anticipated standards of performance laid out.

Task 3: Using the information provided to determine the most acceptable offer for the business

FIRST

EVENT

Category

Projected

subtotal

Estimated

costs

Venue costs

location rental 0 0

Event staff 26400 28908

Equipment 40000 40000

Decorations 200000 220000

Lighting 150000 150000

Signage 30000 30000

Speakers 12000 12000

Rockband 30000 48000

Video 25000 30500

Chairs 12000 18000

Social media

cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THH3113 8

Twitter 2500 2875

Face book 3000 3450

Pinterest 1200 1380

Instagram 4000 4600

Google 2500 2875

LinkedIn 3000 3450

Snap chat 750 862.5

Advertising

Print 8000 6000

Outdoor 40000 56000

Radio 6000 18000

Television 10000 0

Drinks 4000 3600

Snacks 6000 6720

TOTAL 616350 687220.5

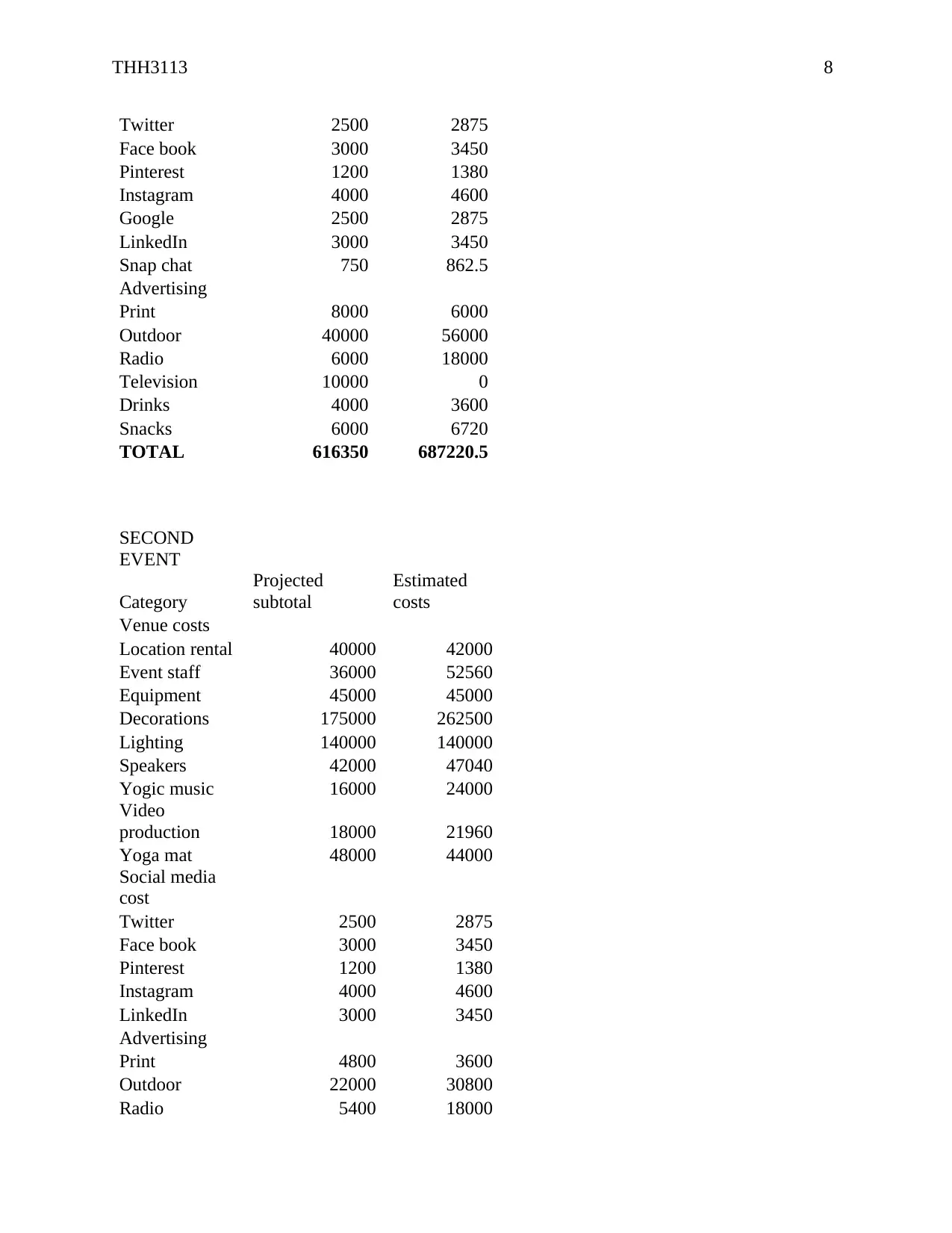

SECOND

EVENT

Category

Projected

subtotal

Estimated

costs

Venue costs

Location rental 40000 42000

Event staff 36000 52560

Equipment 45000 45000

Decorations 175000 262500

Lighting 140000 140000

Speakers 42000 47040

Yogic music 16000 24000

Video

production 18000 21960

Yoga mat 48000 44000

Social media

cost

Twitter 2500 2875

Face book 3000 3450

Pinterest 1200 1380

Instagram 4000 4600

LinkedIn 3000 3450

Advertising

Print 4800 3600

Outdoor 22000 30800

Radio 5400 18000

Twitter 2500 2875

Face book 3000 3450

Pinterest 1200 1380

Instagram 4000 4600

Google 2500 2875

LinkedIn 3000 3450

Snap chat 750 862.5

Advertising

Print 8000 6000

Outdoor 40000 56000

Radio 6000 18000

Television 10000 0

Drinks 4000 3600

Snacks 6000 6720

TOTAL 616350 687220.5

SECOND

EVENT

Category

Projected

subtotal

Estimated

costs

Venue costs

Location rental 40000 42000

Event staff 36000 52560

Equipment 45000 45000

Decorations 175000 262500

Lighting 140000 140000

Speakers 42000 47040

Yogic music 16000 24000

Video

production 18000 21960

Yoga mat 48000 44000

Social media

cost

Twitter 2500 2875

Face book 3000 3450

Pinterest 1200 1380

Instagram 4000 4600

LinkedIn 3000 3450

Advertising

Print 4800 3600

Outdoor 22000 30800

Radio 5400 18000

THH3113 9

Television 2000 10000

Drinks 8000 7200

Snacks 7000 7840

TOTAL 622900 772255

Television 2000 10000

Drinks 8000 7200

Snacks 7000 7840

TOTAL 622900 772255

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

THH3113 10

Appendices

For the first event

At break even profit is zero

At break even, total revenue= total costs

Total cost= fixed cost + variable cost

Total revenue = price per unit * quantity

Total revenue for the first event = 135 * 8300

=1120500

Therefore total cost at break even = 1120500

Contribution margin = 35% of the total cost

= 35% * 1120500 =392175

Therefore total revenue = 1120500+392175

= 1512675

Variable costs = total operating expenses =687220.50

Fixed cost = 1512675-687220.50 = 825454.50

Variable cost = variable cost per unit * quantity

Variable cost per unit= 687220.50/8300

= 82.80

Breakeven point units (number of tickets) = fixed cost/ (selling price –variable cost)

= 825454.50/ (135-82.80)

=15814 tickets for the first event

Total revenue =number of tickets * price per ticket

= 15814 * 135

=2134890

For the second event

At break even profit is zero

At break even, total revenue= total costs

Total cost= fixed cost + variable cost

Total revenue = price per unit * quantity

Total revenue for the first event = 122 * 8300

=1012600

Therefore total cost at break even = 1012600

Contribution margin = 35% of the total cost

= 35% * 1012600 =354410

Therefore total revenue = 1012600+354410

= 1367010

Variable costs = total operating expenses =772255

Fixed cost = 1367010-772255 = 594755

Total fixed cost + cost price on mats

Therefore total fixed cost =594755+ 44000

=638755

Variable cost = variable cost per unit * quantity

Variable cost per unit= 772255/8300

= 93.50

Breakeven point units (number of tickets) = fixed cost/ (selling price –variable cost)

Appendices

For the first event

At break even profit is zero

At break even, total revenue= total costs

Total cost= fixed cost + variable cost

Total revenue = price per unit * quantity

Total revenue for the first event = 135 * 8300

=1120500

Therefore total cost at break even = 1120500

Contribution margin = 35% of the total cost

= 35% * 1120500 =392175

Therefore total revenue = 1120500+392175

= 1512675

Variable costs = total operating expenses =687220.50

Fixed cost = 1512675-687220.50 = 825454.50

Variable cost = variable cost per unit * quantity

Variable cost per unit= 687220.50/8300

= 82.80

Breakeven point units (number of tickets) = fixed cost/ (selling price –variable cost)

= 825454.50/ (135-82.80)

=15814 tickets for the first event

Total revenue =number of tickets * price per ticket

= 15814 * 135

=2134890

For the second event

At break even profit is zero

At break even, total revenue= total costs

Total cost= fixed cost + variable cost

Total revenue = price per unit * quantity

Total revenue for the first event = 122 * 8300

=1012600

Therefore total cost at break even = 1012600

Contribution margin = 35% of the total cost

= 35% * 1012600 =354410

Therefore total revenue = 1012600+354410

= 1367010

Variable costs = total operating expenses =772255

Fixed cost = 1367010-772255 = 594755

Total fixed cost + cost price on mats

Therefore total fixed cost =594755+ 44000

=638755

Variable cost = variable cost per unit * quantity

Variable cost per unit= 772255/8300

= 93.50

Breakeven point units (number of tickets) = fixed cost/ (selling price –variable cost)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THH3113 11

= 638755/ (122-93.50)

=22413 tickets for the second event

Total revenue =number of tickets * price per ticket

= 22413 * 135

=2734386

The second event is the most profitable; DOSM should choose it as it generates the highest

revenue with the lowest fixed costs to be incurred

= 638755/ (122-93.50)

=22413 tickets for the second event

Total revenue =number of tickets * price per ticket

= 22413 * 135

=2734386

The second event is the most profitable; DOSM should choose it as it generates the highest

revenue with the lowest fixed costs to be incurred

THH3113 12

References

Arce, A., Mac Dowell, N., Shah, N., & Vega, L. F. (2012). Flexible operation of solvent

regeneration systems for CO2 capture processes using advanced control techniques:

Towards operational cost minimisation. International Journal of Greenhouse Gas

Control, 11, 236-250.

Ratnatunga, J., Michael, S. C., & Balachandran, K. R. (2012). Cost management in Sri Lanka: A

case study on volume, activity and time as cost drivers. The International Journal of

Accounting, 47(3), 281-301.

Toompuu, K., & Põlajeva, T. (2014). Theoretical framework and an overview of the cost drivers

that are applied in universities for allocating indirect costs. Procedia-Social and

Behavioral Sciences, 110, 1014-1022.

References

Arce, A., Mac Dowell, N., Shah, N., & Vega, L. F. (2012). Flexible operation of solvent

regeneration systems for CO2 capture processes using advanced control techniques:

Towards operational cost minimisation. International Journal of Greenhouse Gas

Control, 11, 236-250.

Ratnatunga, J., Michael, S. C., & Balachandran, K. R. (2012). Cost management in Sri Lanka: A

case study on volume, activity and time as cost drivers. The International Journal of

Accounting, 47(3), 281-301.

Toompuu, K., & Põlajeva, T. (2014). Theoretical framework and an overview of the cost drivers

that are applied in universities for allocating indirect costs. Procedia-Social and

Behavioral Sciences, 110, 1014-1022.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.