University Finance Project: Cost and Control Job Costing

VerifiedAdded on 2020/04/01

|22

|2481

|39

Project

AI Summary

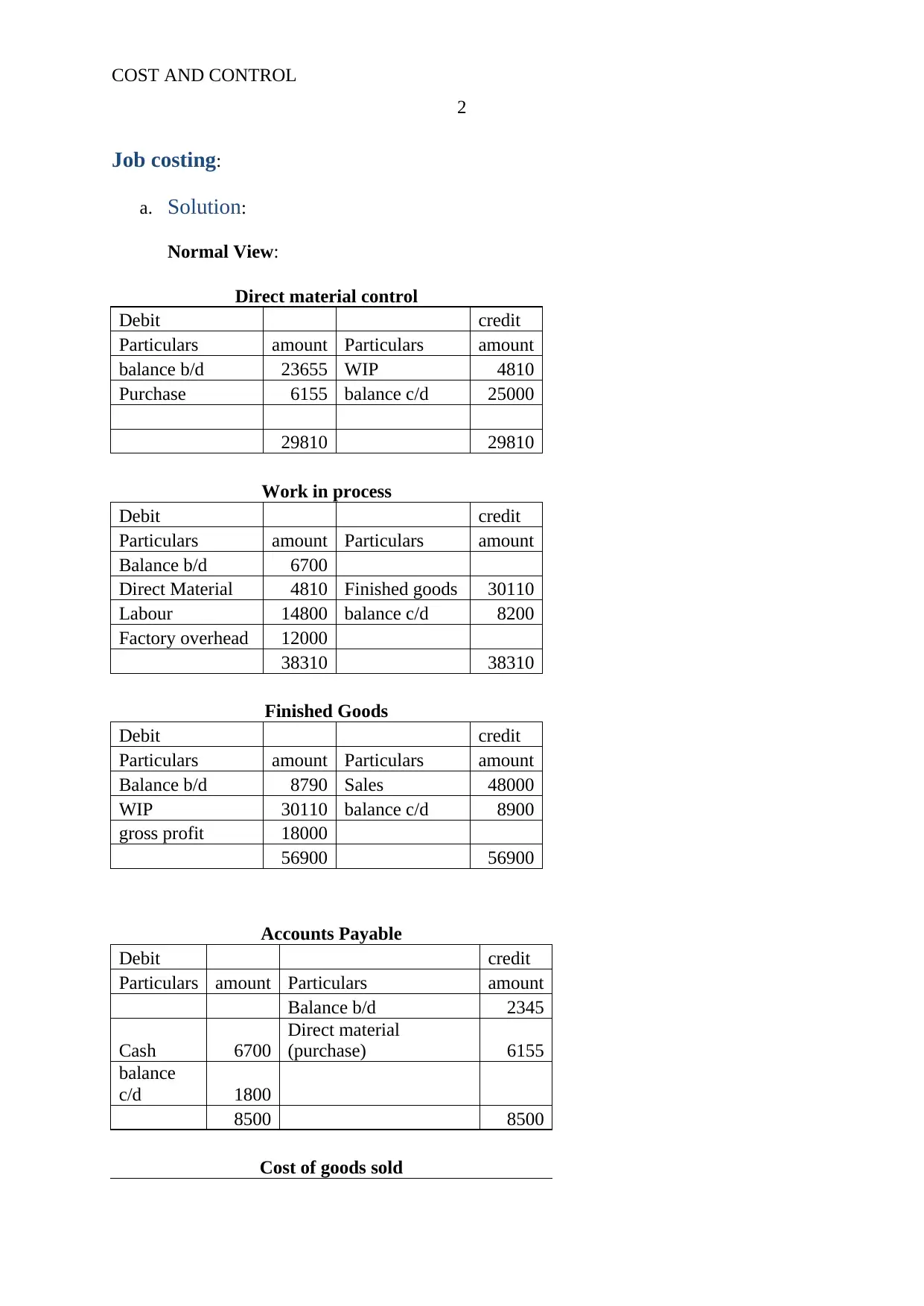

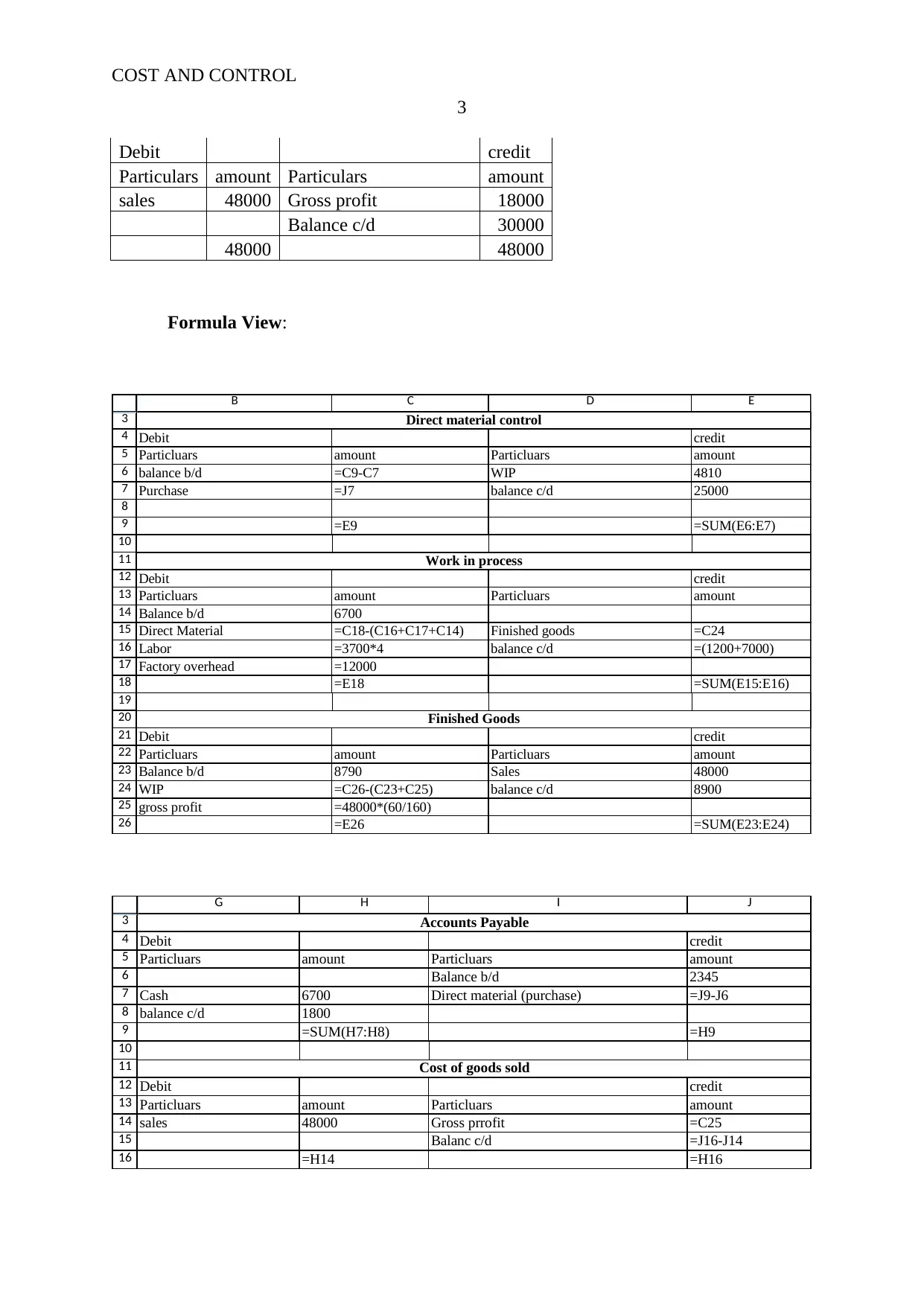

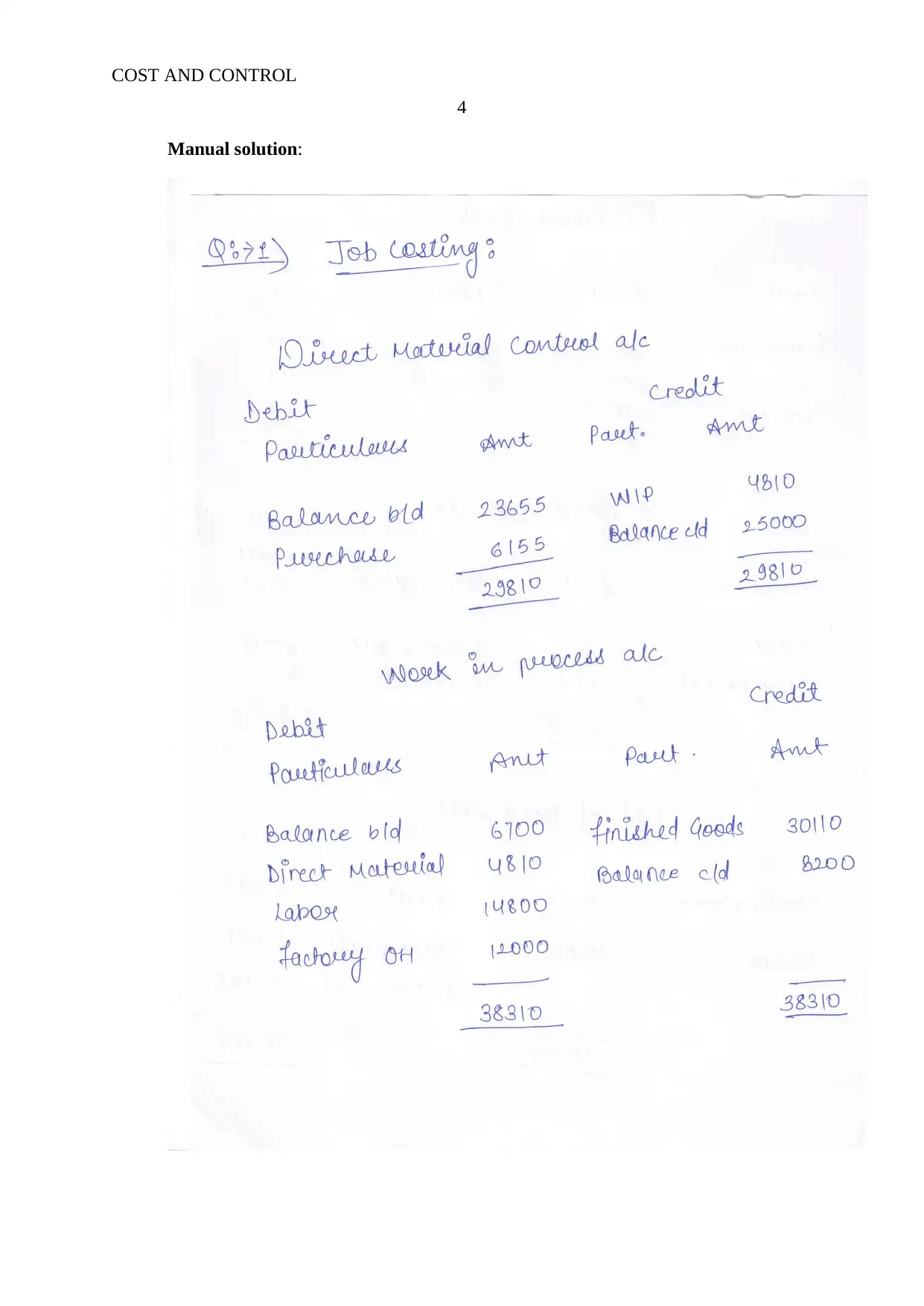

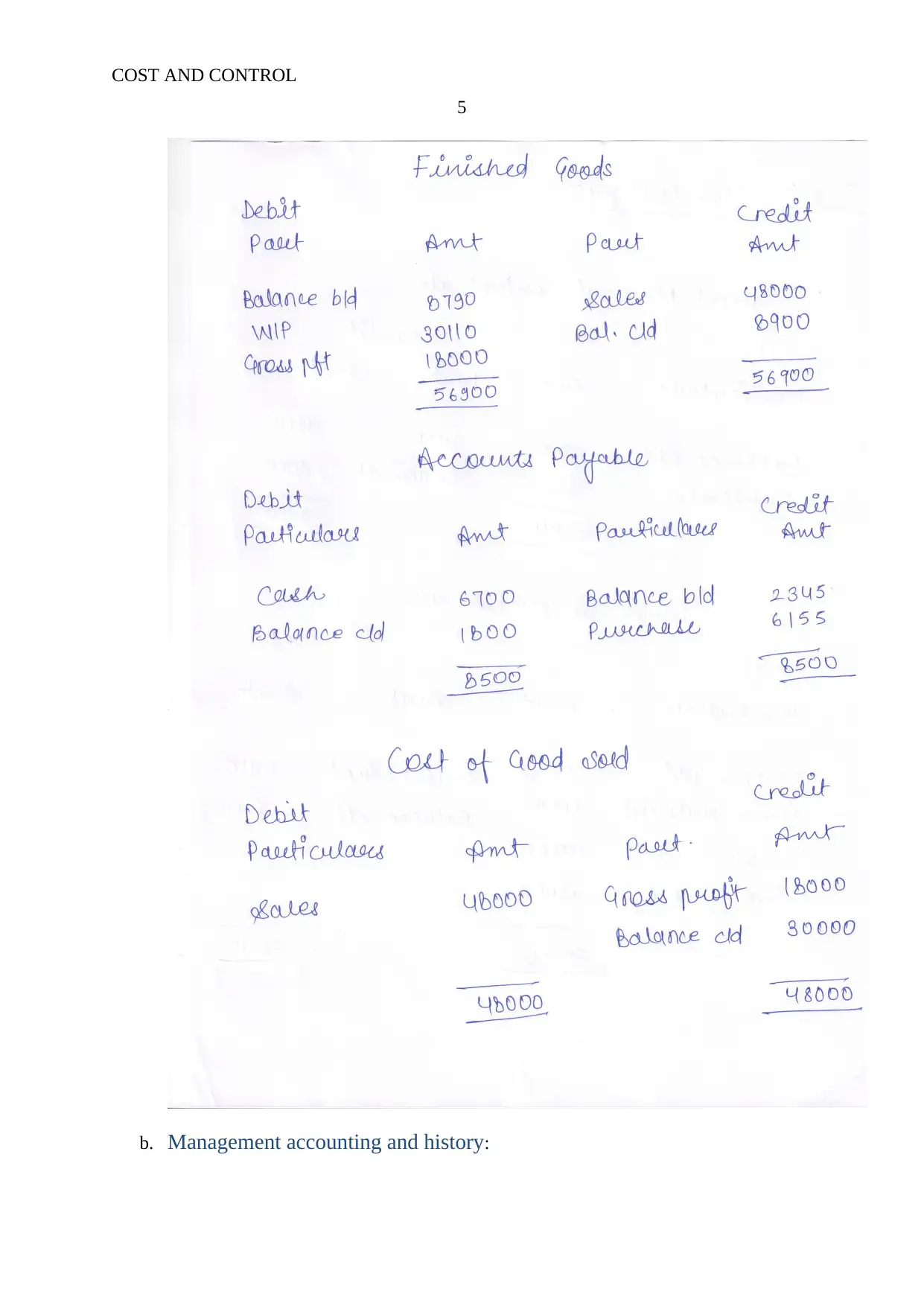

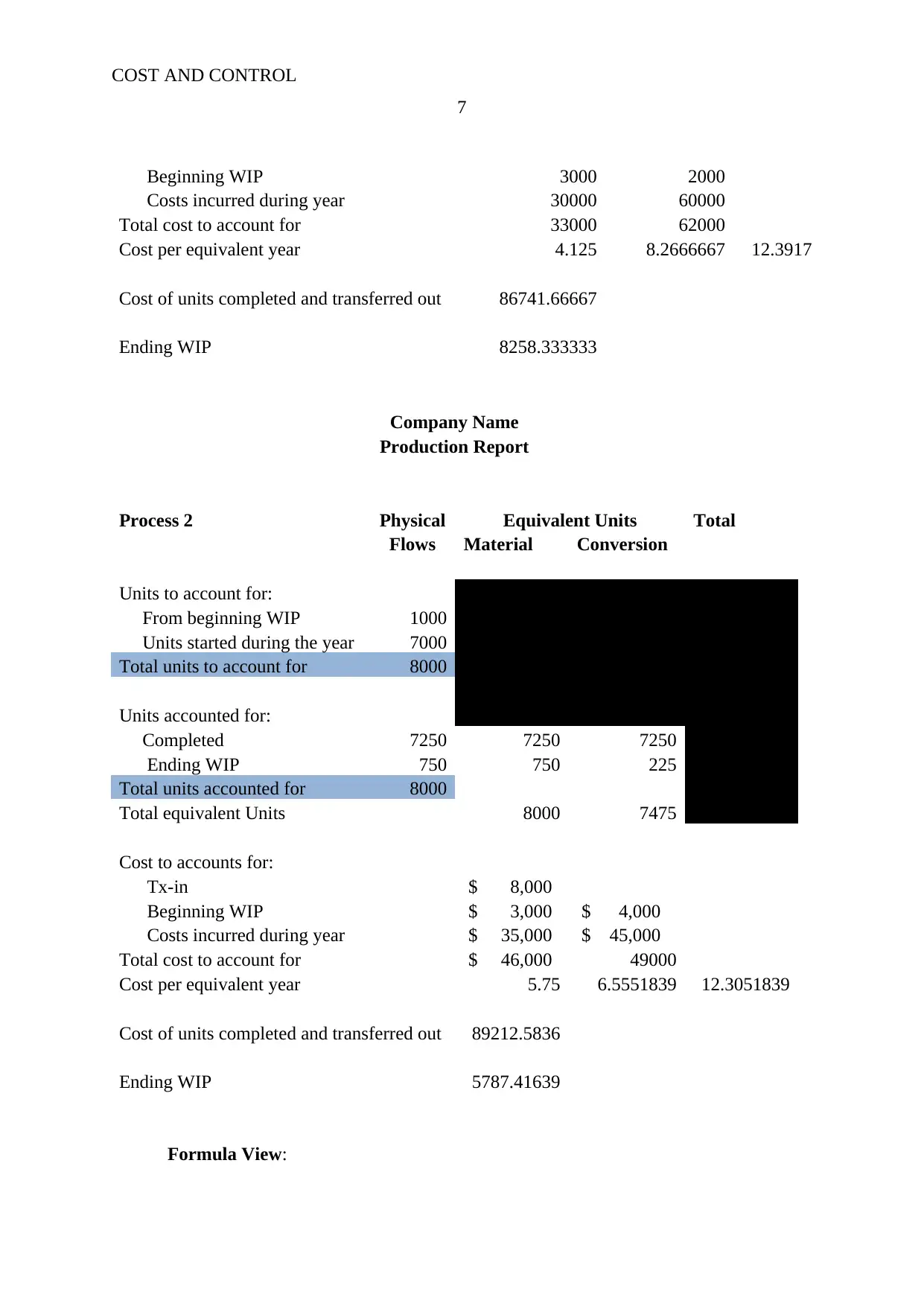

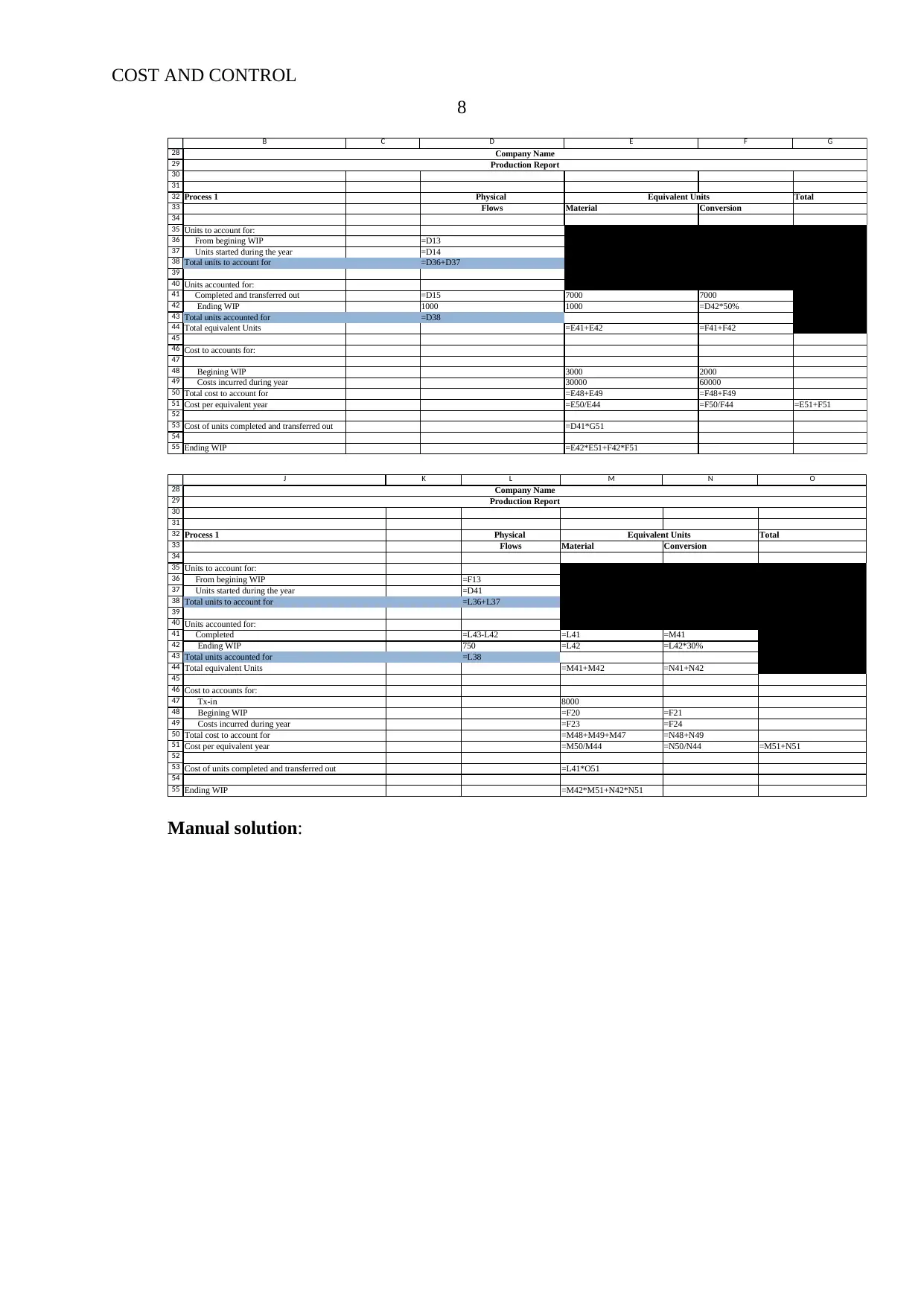

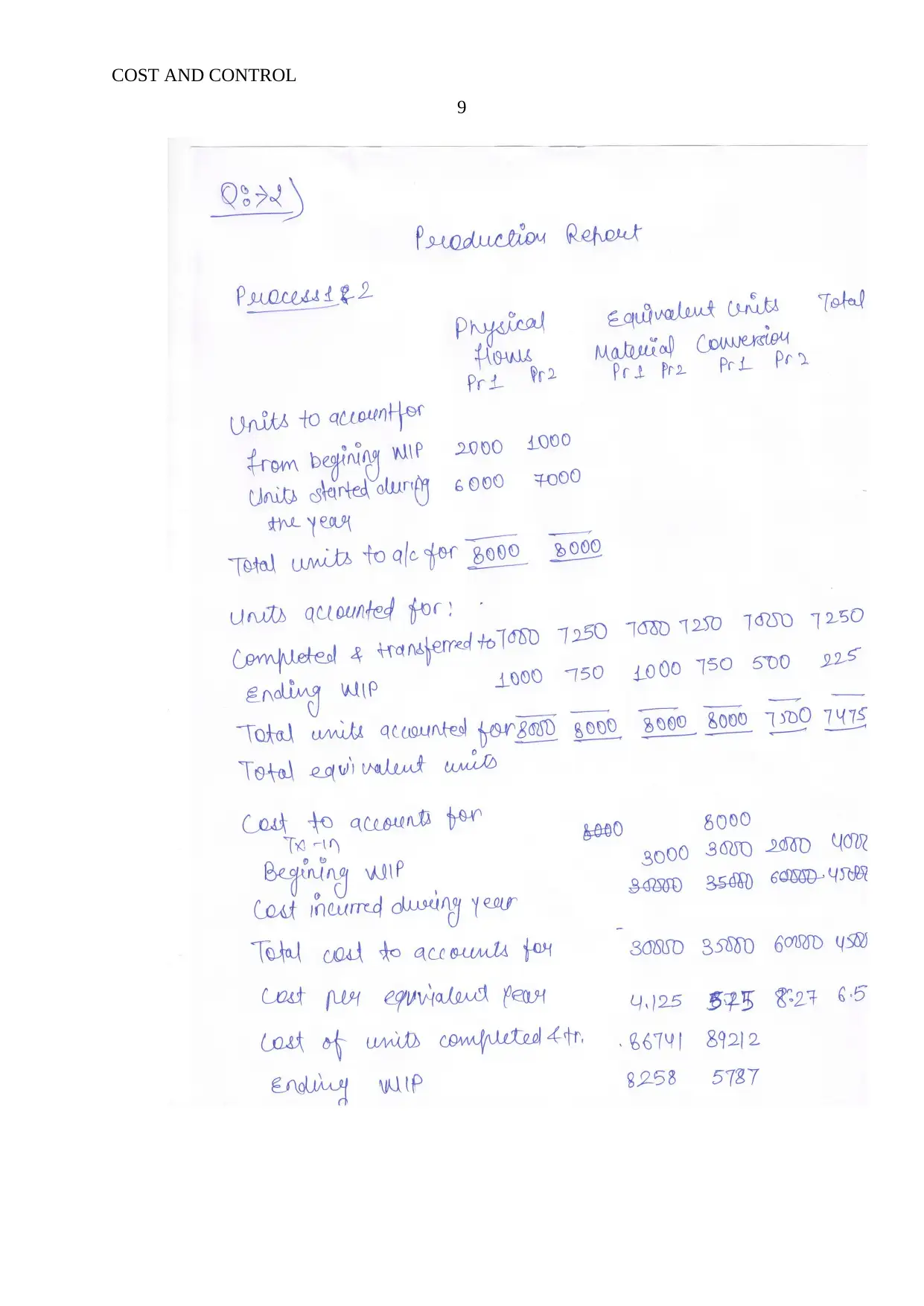

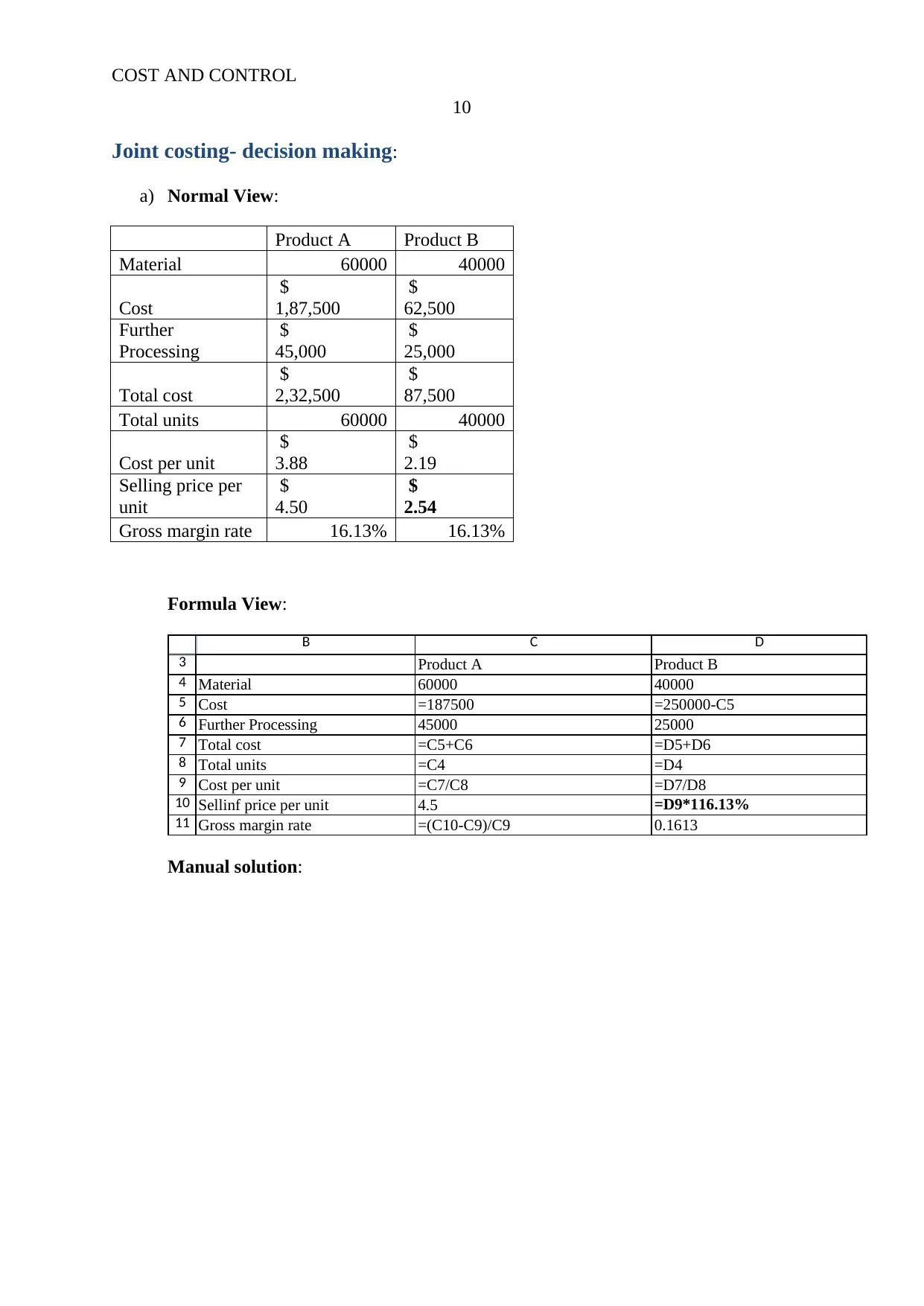

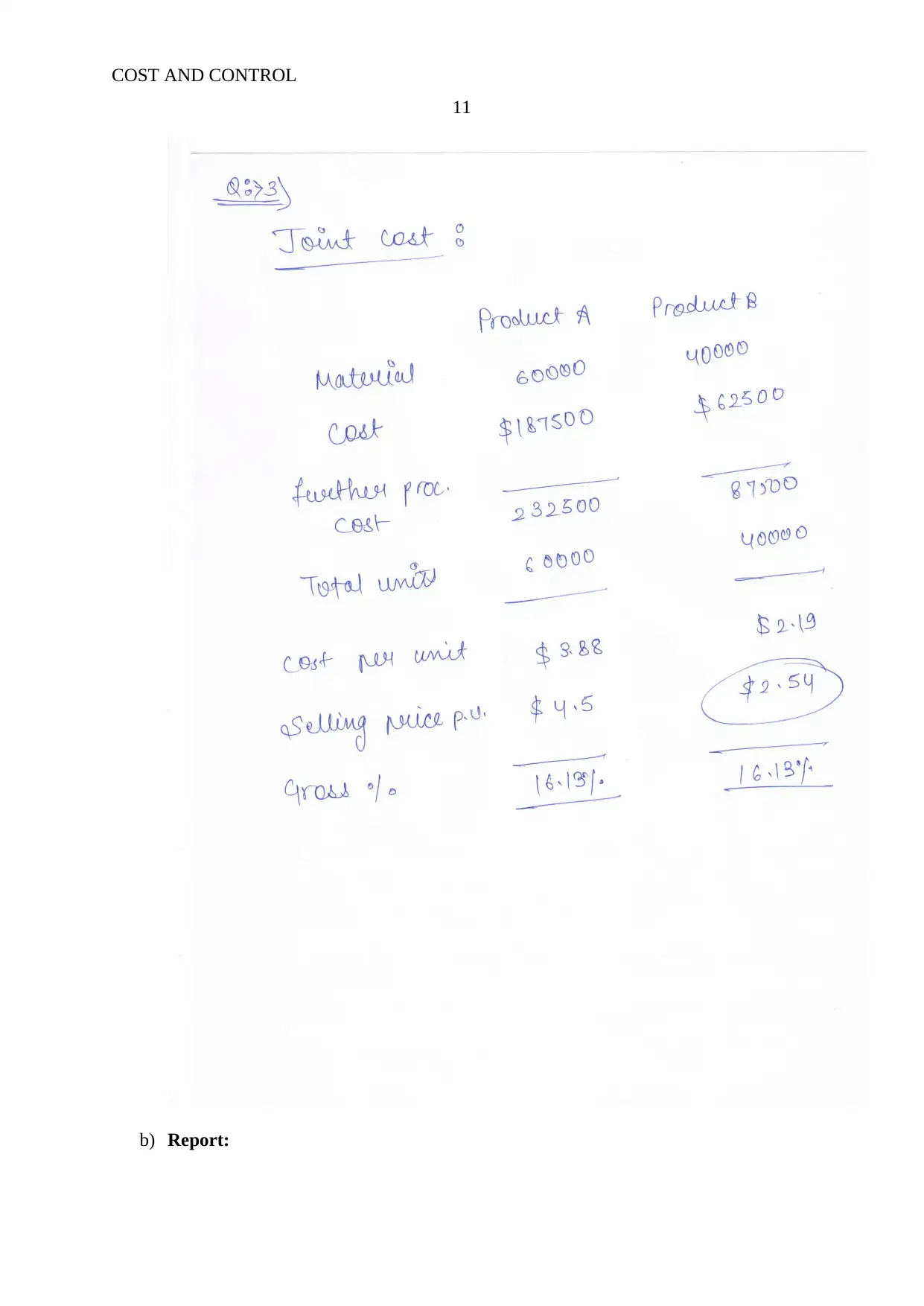

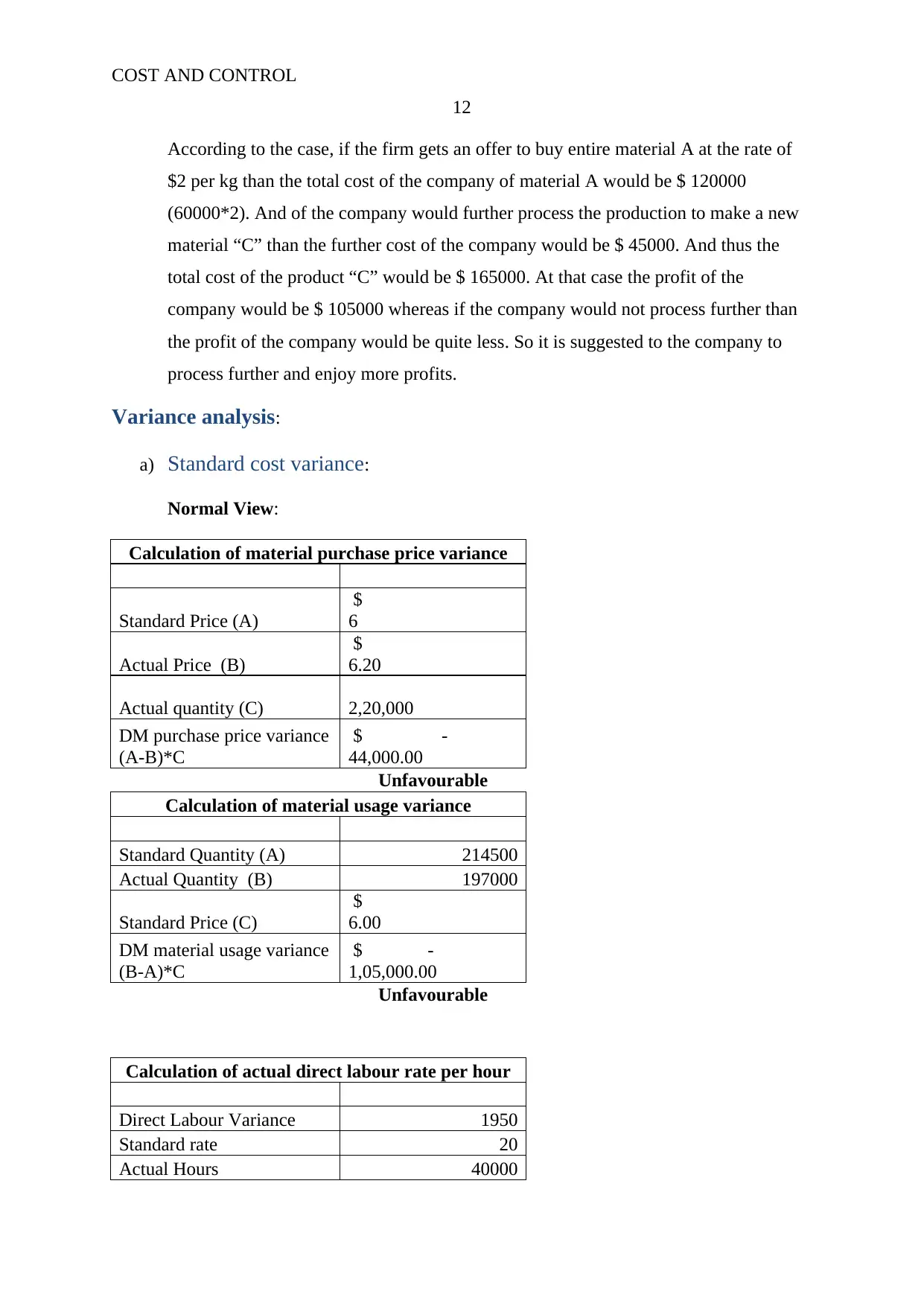

This project report provides a comprehensive analysis of cost and control principles, encompassing job costing, variance analysis, and budgeting techniques. The report begins with a detailed examination of job costing, including normal and formula views, along with manual solutions. It then delves into management accounting and its historical context, emphasizing modern cost management practices. The report further explores process costing, presenting production reports for two processes, complete with physical and equivalent units analysis, and cost calculations. Joint costing and decision-making are addressed, including normal views and formula views, along with a discussion of further processing decisions. The project also includes a thorough analysis of variance, covering material purchase price variance, material usage variance, and labor rate variance, along with journal entries. Finally, the report concludes with a financial model for forecasting income statements, providing a budgeting report for several years, including sales, cost of goods sold, and gross profit calculations.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.