Management Accounting for Cost and Control Assignment - Analysis

VerifiedAdded on 2022/09/26

|18

|2138

|19

Homework Assignment

AI Summary

This assignment analyzes the application of management accounting principles for cost and control within the context of Farm Organic Ltd, a business providing organic drenches. The solution begins with a value chain analysis, identifying opportunities for the company and discussing the importance of collaboration and market orientation. It then proceeds to prepare a cost of goods manufactured statement, calculate cost of sales and gross profit, and discuss the limitations of such statements for decision-making. The assignment further explores overhead allocation methods (direct, step-down, and reciprocal), calculates overhead allocation rates, and performs journal entries. Finally, it examines different costing methods (weighted average and FIFO) for inventory valuation, and provides journal entries for production costs, explaining the differences between the methods. The assignment uses realistic data to illustrate the application of these concepts in a practical business scenario.

Running head: MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Management Accounting for Cost and Control

Name of the Student:

Name of the University:

Authors Note:

Management Accounting for Cost and Control

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Table of Contents

Question 1:.................................................................................................................................3

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................3

Conclusion:................................................................................................................................4

Question 2:.................................................................................................................................5

1. Preparing the cost of goods manufactured statement for the month ended 31 July 2019:.....5

2. Depicting company’s cost of sales for the month ended 31 July 2019:.................................5

3. Depicting company’s gross profit for the month ended 31 July 2019:..................................6

4. Explaining David about the limitations of a cost of goods manufactured statement for

decision making:........................................................................................................................6

Question 3:.................................................................................................................................7

1. Allocating the support department costs to the operating departments using the direct

method:.......................................................................................................................................7

2. Allocating the support department costs to the operating departments using the step-down

method:.......................................................................................................................................7

3. Allocating the support department costs to the operating departments using the reciprocal

method:.......................................................................................................................................8

Question 4:.................................................................................................................................9

1. Estimated overhead allocation rate:.......................................................................................9

2. Total overhead allocated to job Gargantua:...........................................................................9

3. Unit cost for this job:..............................................................................................................9

Table of Contents

Question 1:.................................................................................................................................3

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................3

Conclusion:................................................................................................................................4

Question 2:.................................................................................................................................5

1. Preparing the cost of goods manufactured statement for the month ended 31 July 2019:.....5

2. Depicting company’s cost of sales for the month ended 31 July 2019:.................................5

3. Depicting company’s gross profit for the month ended 31 July 2019:..................................6

4. Explaining David about the limitations of a cost of goods manufactured statement for

decision making:........................................................................................................................6

Question 3:.................................................................................................................................7

1. Allocating the support department costs to the operating departments using the direct

method:.......................................................................................................................................7

2. Allocating the support department costs to the operating departments using the step-down

method:.......................................................................................................................................7

3. Allocating the support department costs to the operating departments using the reciprocal

method:.......................................................................................................................................8

Question 4:.................................................................................................................................9

1. Estimated overhead allocation rate:.......................................................................................9

2. Total overhead allocated to job Gargantua:...........................................................................9

3. Unit cost for this job:..............................................................................................................9

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

4. Actual overhead for the Gargantua job:.................................................................................9

5. Journal entries to record the allocation:...............................................................................10

6. Total profit and the profit per unit:......................................................................................10

Question 5:...............................................................................................................................10

1. Depicting the cost:................................................................................................................10

2. Journal entries to record the production costs for February:................................................14

3. Explaining the difference between the costs calculated using the weighted average cost

method and the FIFO method:.................................................................................................15

References and Bibliography:..................................................................................................16

4. Actual overhead for the Gargantua job:.................................................................................9

5. Journal entries to record the allocation:...............................................................................10

6. Total profit and the profit per unit:......................................................................................10

Question 5:...............................................................................................................................10

1. Depicting the cost:................................................................................................................10

2. Journal entries to record the production costs for February:................................................14

3. Explaining the difference between the costs calculated using the weighted average cost

method and the FIFO method:.................................................................................................15

References and Bibliography:..................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Question 1:

Introduction:

The report outlines the importance value chain analysis to Farm Organic Ltd in their

decision making process. For the opportunities that is found along the value chain, the first

response of the farmers is the production for market. Value chain is a set of connected

activities and actions that helps in adding value to the product by improving the attributes of

the product (Cognizant.com, 2019). Flow of knowledge, product, finance, social capital and

payment is encompassed in the value chain that is required to organize communities and

producers. Farm Organic Ltd can use value chain for using actions to add more value and

identifying the weak points.

Discussion:

Value chain are the interactive systems dealing with the flow of money, products and

information that is dependent upon the relationship and emphasizing on the importance of

collaboration and market orientation. The thinking of value chain would supplement the

production of smallholders and increase the income by utilizing the post harvesting skills.

Value chain is more or less of a supply chain which focuses on the value added at each step.

Organic business wants to bring organic products and Farm Organic Ltd would be dependent

upon number of players who are involved directly such as farmers, input suppliers,

transporters, store keepers, retailers and traders. The crucial role is played by the relationship

between the people buying the products and the farmers who are producing the products

(Edeling & Fischer, 2016).

Question 1:

Introduction:

The report outlines the importance value chain analysis to Farm Organic Ltd in their

decision making process. For the opportunities that is found along the value chain, the first

response of the farmers is the production for market. Value chain is a set of connected

activities and actions that helps in adding value to the product by improving the attributes of

the product (Cognizant.com, 2019). Flow of knowledge, product, finance, social capital and

payment is encompassed in the value chain that is required to organize communities and

producers. Farm Organic Ltd can use value chain for using actions to add more value and

identifying the weak points.

Discussion:

Value chain are the interactive systems dealing with the flow of money, products and

information that is dependent upon the relationship and emphasizing on the importance of

collaboration and market orientation. The thinking of value chain would supplement the

production of smallholders and increase the income by utilizing the post harvesting skills.

Value chain is more or less of a supply chain which focuses on the value added at each step.

Organic business wants to bring organic products and Farm Organic Ltd would be dependent

upon number of players who are involved directly such as farmers, input suppliers,

transporters, store keepers, retailers and traders. The crucial role is played by the relationship

between the people buying the products and the farmers who are producing the products

(Edeling & Fischer, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Farm Organic limited can capture the value with the help of value chain by buying

into the value added enterprise and integrating with such value added facts. This involve pre-

production enterprises, post-harvest processing of products and post-harvest handling of

products. A value adding possibility is represented by each of these activities and the value

added by the value chain has shown to be remarkably adaptive to the evolving demands of

customer. The increase in the popularity of organic food would require the business to

manage the complex and increasingly global environment (Hu et al., 2018). Value chain will

help retailers in collaborating with others that helps in fulfillment of needs of customers

through the joint efforts for the operation of warehouse such as fulfillment, management of

inventory, providing home delivery and operating and creating online stores. The existing

model of supply chain is restructured by involving local organic farmers in the planning of

the delivery network of value chain. In addition to all these, the value chain helps in the

integration of the end customers with the perspective of supply chain and make a contribution

to the framework of consumer behavior (Ey.com, 2019). The competitive position of the

organic farmers in the value chain can be improved through the collective organic marketing.

Conclusion:

Organic products producers are struggling to optimize the scale of their operations

and at the same time for maintaining profitability. It is so because producers such as Farm

Organic Ltd faces challenges in terms of increasing input cost, challenges pertaining to

certification and elongated conversion period. Therefore, the development of comprehensive

value chain would make organic market more profitable and scalable by bringing down cost

of cultivation.

Farm Organic limited can capture the value with the help of value chain by buying

into the value added enterprise and integrating with such value added facts. This involve pre-

production enterprises, post-harvest processing of products and post-harvest handling of

products. A value adding possibility is represented by each of these activities and the value

added by the value chain has shown to be remarkably adaptive to the evolving demands of

customer. The increase in the popularity of organic food would require the business to

manage the complex and increasingly global environment (Hu et al., 2018). Value chain will

help retailers in collaborating with others that helps in fulfillment of needs of customers

through the joint efforts for the operation of warehouse such as fulfillment, management of

inventory, providing home delivery and operating and creating online stores. The existing

model of supply chain is restructured by involving local organic farmers in the planning of

the delivery network of value chain. In addition to all these, the value chain helps in the

integration of the end customers with the perspective of supply chain and make a contribution

to the framework of consumer behavior (Ey.com, 2019). The competitive position of the

organic farmers in the value chain can be improved through the collective organic marketing.

Conclusion:

Organic products producers are struggling to optimize the scale of their operations

and at the same time for maintaining profitability. It is so because producers such as Farm

Organic Ltd faces challenges in terms of increasing input cost, challenges pertaining to

certification and elongated conversion period. Therefore, the development of comprehensive

value chain would make organic market more profitable and scalable by bringing down cost

of cultivation.

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Question 2:

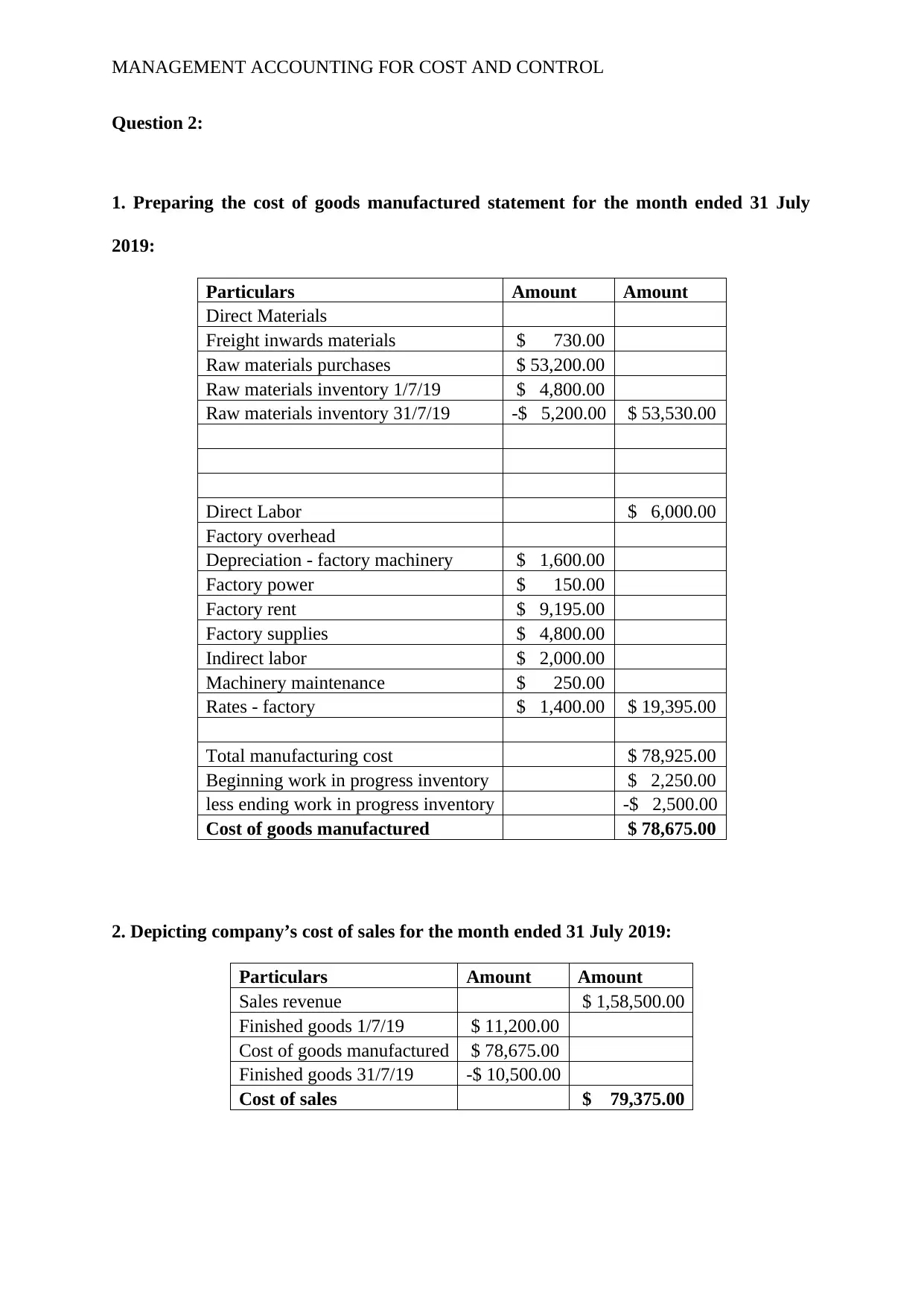

1. Preparing the cost of goods manufactured statement for the month ended 31 July

2019:

Particulars Amount Amount

Direct Materials

Freight inwards materials $ 730.00

Raw materials purchases $ 53,200.00

Raw materials inventory 1/7/19 $ 4,800.00

Raw materials inventory 31/7/19 -$ 5,200.00 $ 53,530.00

Direct Labor $ 6,000.00

Factory overhead

Depreciation - factory machinery $ 1,600.00

Factory power $ 150.00

Factory rent $ 9,195.00

Factory supplies $ 4,800.00

Indirect labor $ 2,000.00

Machinery maintenance $ 250.00

Rates - factory $ 1,400.00 $ 19,395.00

Total manufacturing cost $ 78,925.00

Beginning work in progress inventory $ 2,250.00

less ending work in progress inventory -$ 2,500.00

Cost of goods manufactured $ 78,675.00

2. Depicting company’s cost of sales for the month ended 31 July 2019:

Particulars Amount Amount

Sales revenue $ 1,58,500.00

Finished goods 1/7/19 $ 11,200.00

Cost of goods manufactured $ 78,675.00

Finished goods 31/7/19 -$ 10,500.00

Cost of sales $ 79,375.00

Question 2:

1. Preparing the cost of goods manufactured statement for the month ended 31 July

2019:

Particulars Amount Amount

Direct Materials

Freight inwards materials $ 730.00

Raw materials purchases $ 53,200.00

Raw materials inventory 1/7/19 $ 4,800.00

Raw materials inventory 31/7/19 -$ 5,200.00 $ 53,530.00

Direct Labor $ 6,000.00

Factory overhead

Depreciation - factory machinery $ 1,600.00

Factory power $ 150.00

Factory rent $ 9,195.00

Factory supplies $ 4,800.00

Indirect labor $ 2,000.00

Machinery maintenance $ 250.00

Rates - factory $ 1,400.00 $ 19,395.00

Total manufacturing cost $ 78,925.00

Beginning work in progress inventory $ 2,250.00

less ending work in progress inventory -$ 2,500.00

Cost of goods manufactured $ 78,675.00

2. Depicting company’s cost of sales for the month ended 31 July 2019:

Particulars Amount Amount

Sales revenue $ 1,58,500.00

Finished goods 1/7/19 $ 11,200.00

Cost of goods manufactured $ 78,675.00

Finished goods 31/7/19 -$ 10,500.00

Cost of sales $ 79,375.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

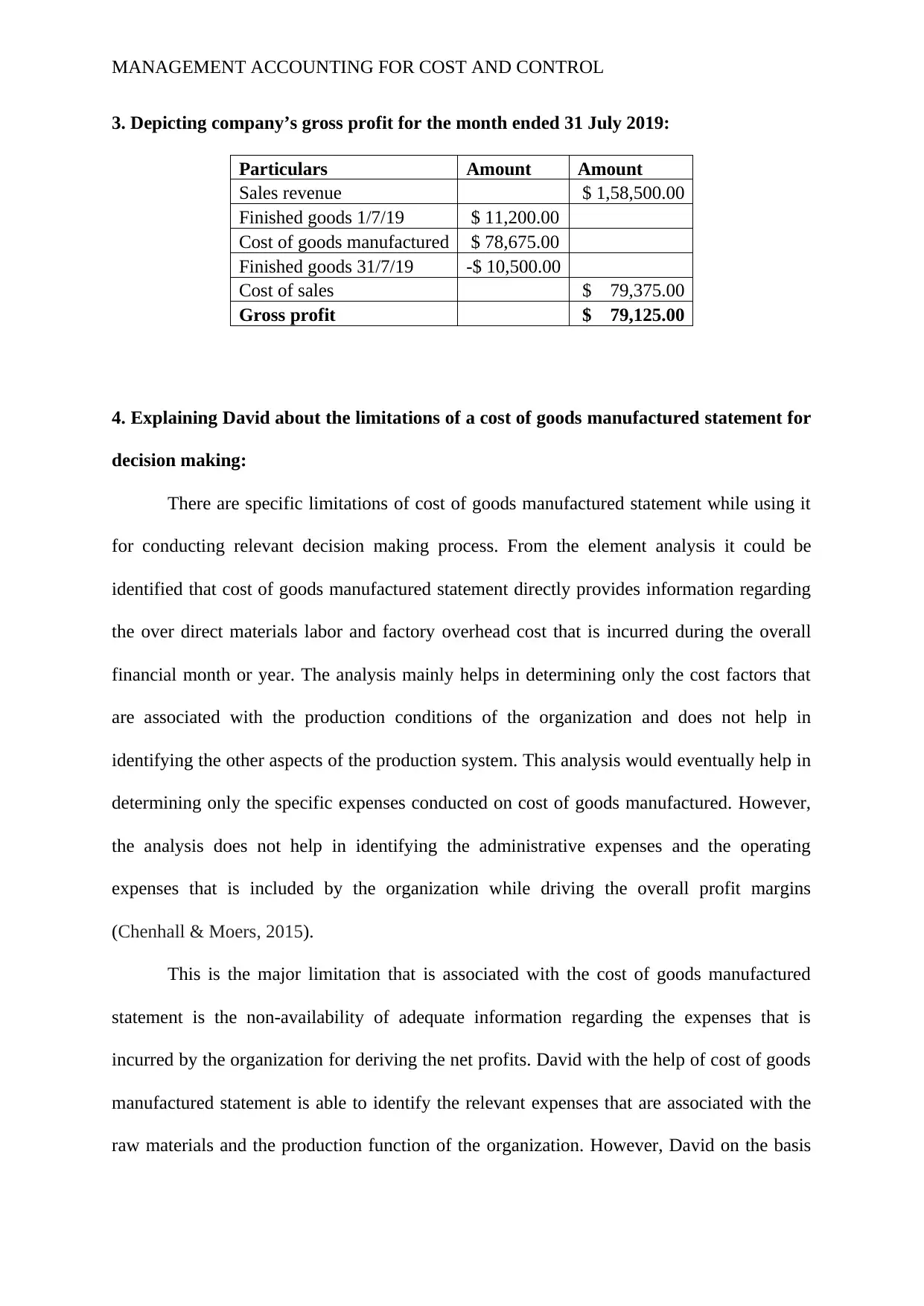

3. Depicting company’s gross profit for the month ended 31 July 2019:

Particulars Amount Amount

Sales revenue $ 1,58,500.00

Finished goods 1/7/19 $ 11,200.00

Cost of goods manufactured $ 78,675.00

Finished goods 31/7/19 -$ 10,500.00

Cost of sales $ 79,375.00

Gross profit $ 79,125.00

4. Explaining David about the limitations of a cost of goods manufactured statement for

decision making:

There are specific limitations of cost of goods manufactured statement while using it

for conducting relevant decision making process. From the element analysis it could be

identified that cost of goods manufactured statement directly provides information regarding

the over direct materials labor and factory overhead cost that is incurred during the overall

financial month or year. The analysis mainly helps in determining only the cost factors that

are associated with the production conditions of the organization and does not help in

identifying the other aspects of the production system. This analysis would eventually help in

determining only the specific expenses conducted on cost of goods manufactured. However,

the analysis does not help in identifying the administrative expenses and the operating

expenses that is included by the organization while driving the overall profit margins

(Chenhall & Moers, 2015).

This is the major limitation that is associated with the cost of goods manufactured

statement is the non-availability of adequate information regarding the expenses that is

incurred by the organization for deriving the net profits. David with the help of cost of goods

manufactured statement is able to identify the relevant expenses that are associated with the

raw materials and the production function of the organization. However, David on the basis

3. Depicting company’s gross profit for the month ended 31 July 2019:

Particulars Amount Amount

Sales revenue $ 1,58,500.00

Finished goods 1/7/19 $ 11,200.00

Cost of goods manufactured $ 78,675.00

Finished goods 31/7/19 -$ 10,500.00

Cost of sales $ 79,375.00

Gross profit $ 79,125.00

4. Explaining David about the limitations of a cost of goods manufactured statement for

decision making:

There are specific limitations of cost of goods manufactured statement while using it

for conducting relevant decision making process. From the element analysis it could be

identified that cost of goods manufactured statement directly provides information regarding

the over direct materials labor and factory overhead cost that is incurred during the overall

financial month or year. The analysis mainly helps in determining only the cost factors that

are associated with the production conditions of the organization and does not help in

identifying the other aspects of the production system. This analysis would eventually help in

determining only the specific expenses conducted on cost of goods manufactured. However,

the analysis does not help in identifying the administrative expenses and the operating

expenses that is included by the organization while driving the overall profit margins

(Chenhall & Moers, 2015).

This is the major limitation that is associated with the cost of goods manufactured

statement is the non-availability of adequate information regarding the expenses that is

incurred by the organization for deriving the net profits. David with the help of cost of goods

manufactured statement is able to identify the relevant expenses that are associated with the

raw materials and the production function of the organization. However, David on the basis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

of only cost of goods manufactured is not able to identify the relevant increment in sales in

future and make adjustments to budget for supporting future production needs. Hence, it

could be identified that with the help of cost of goods manufactured only expenses incurred

in the process can be identified, which cannot be used for the decision making process.

Furthermore, it cannot support the company to increase its profits in the long run by

addressing the continuous change in demand from customers and the price change.

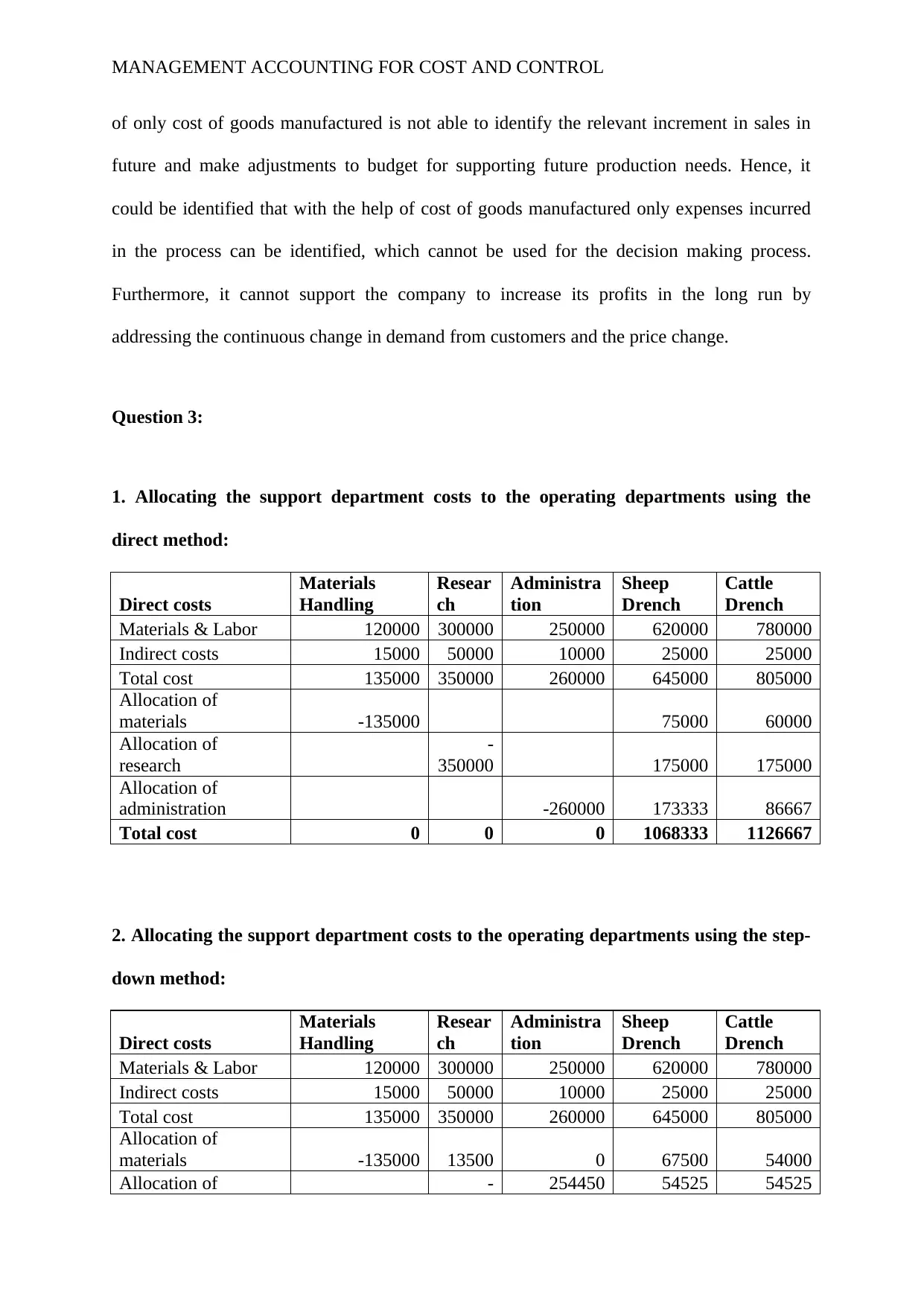

Question 3:

1. Allocating the support department costs to the operating departments using the

direct method:

Direct costs

Materials

Handling

Resear

ch

Administra

tion

Sheep

Drench

Cattle

Drench

Materials & Labor 120000 300000 250000 620000 780000

Indirect costs 15000 50000 10000 25000 25000

Total cost 135000 350000 260000 645000 805000

Allocation of

materials -135000 75000 60000

Allocation of

research

-

350000 175000 175000

Allocation of

administration -260000 173333 86667

Total cost 0 0 0 1068333 1126667

2. Allocating the support department costs to the operating departments using the step-

down method:

Direct costs

Materials

Handling

Resear

ch

Administra

tion

Sheep

Drench

Cattle

Drench

Materials & Labor 120000 300000 250000 620000 780000

Indirect costs 15000 50000 10000 25000 25000

Total cost 135000 350000 260000 645000 805000

Allocation of

materials -135000 13500 0 67500 54000

Allocation of - 254450 54525 54525

of only cost of goods manufactured is not able to identify the relevant increment in sales in

future and make adjustments to budget for supporting future production needs. Hence, it

could be identified that with the help of cost of goods manufactured only expenses incurred

in the process can be identified, which cannot be used for the decision making process.

Furthermore, it cannot support the company to increase its profits in the long run by

addressing the continuous change in demand from customers and the price change.

Question 3:

1. Allocating the support department costs to the operating departments using the

direct method:

Direct costs

Materials

Handling

Resear

ch

Administra

tion

Sheep

Drench

Cattle

Drench

Materials & Labor 120000 300000 250000 620000 780000

Indirect costs 15000 50000 10000 25000 25000

Total cost 135000 350000 260000 645000 805000

Allocation of

materials -135000 75000 60000

Allocation of

research

-

350000 175000 175000

Allocation of

administration -260000 173333 86667

Total cost 0 0 0 1068333 1126667

2. Allocating the support department costs to the operating departments using the step-

down method:

Direct costs

Materials

Handling

Resear

ch

Administra

tion

Sheep

Drench

Cattle

Drench

Materials & Labor 120000 300000 250000 620000 780000

Indirect costs 15000 50000 10000 25000 25000

Total cost 135000 350000 260000 645000 805000

Allocation of

materials -135000 13500 0 67500 54000

Allocation of - 254450 54525 54525

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

research 363500

Allocation of

administration -514450 342967 171483

Total cost 0 0 0 1109992 1085008

3. Allocating the support department costs to the operating departments using the

reciprocal method:

Direct costs

Materials

Handling

Resear

ch

Administra

tion

Sheep

Drench

Cattle

Drench

Materials & Labor 120000 300000 250000 620000 780000

Indirect costs 15000 50000 10000 25000 25000

Total cost 135000 350000 260000 645000 805000

Allocation of

materials -135000 13500 0 67500 54000

Allocation of

research

-

363500 254450 54525 54525

Allocation of

administration 146986 146986 -514450 146986 73493

Allocation of

materials -146986 14699 0 73493 58794

Allocation of

research

-

161684 113179 24253 24253

Allocation of

administration 32337 32337 -113179 32337 16168

Allocation of

materials -32337 3234 0 16168 12935

Allocation of

research -35571 24899 5336 5336

Allocation of

administration 7114 7114 -24899 7114 3557

Allocation of

materials -7114 711 0 3557 2846

Allocation of

research -7826 5478 1174 1174

Allocation of

administration 1565 1565 -5478 1565 783

Allocation of

materials -1565 626 0 626 626

Allocation of

research -2191 1096 1096

Total cost 0 0 0 1080729 1114584

research 363500

Allocation of

administration -514450 342967 171483

Total cost 0 0 0 1109992 1085008

3. Allocating the support department costs to the operating departments using the

reciprocal method:

Direct costs

Materials

Handling

Resear

ch

Administra

tion

Sheep

Drench

Cattle

Drench

Materials & Labor 120000 300000 250000 620000 780000

Indirect costs 15000 50000 10000 25000 25000

Total cost 135000 350000 260000 645000 805000

Allocation of

materials -135000 13500 0 67500 54000

Allocation of

research

-

363500 254450 54525 54525

Allocation of

administration 146986 146986 -514450 146986 73493

Allocation of

materials -146986 14699 0 73493 58794

Allocation of

research

-

161684 113179 24253 24253

Allocation of

administration 32337 32337 -113179 32337 16168

Allocation of

materials -32337 3234 0 16168 12935

Allocation of

research -35571 24899 5336 5336

Allocation of

administration 7114 7114 -24899 7114 3557

Allocation of

materials -7114 711 0 3557 2846

Allocation of

research -7826 5478 1174 1174

Allocation of

administration 1565 1565 -5478 1565 783

Allocation of

materials -1565 626 0 626 626

Allocation of

research -2191 1096 1096

Total cost 0 0 0 1080729 1114584

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

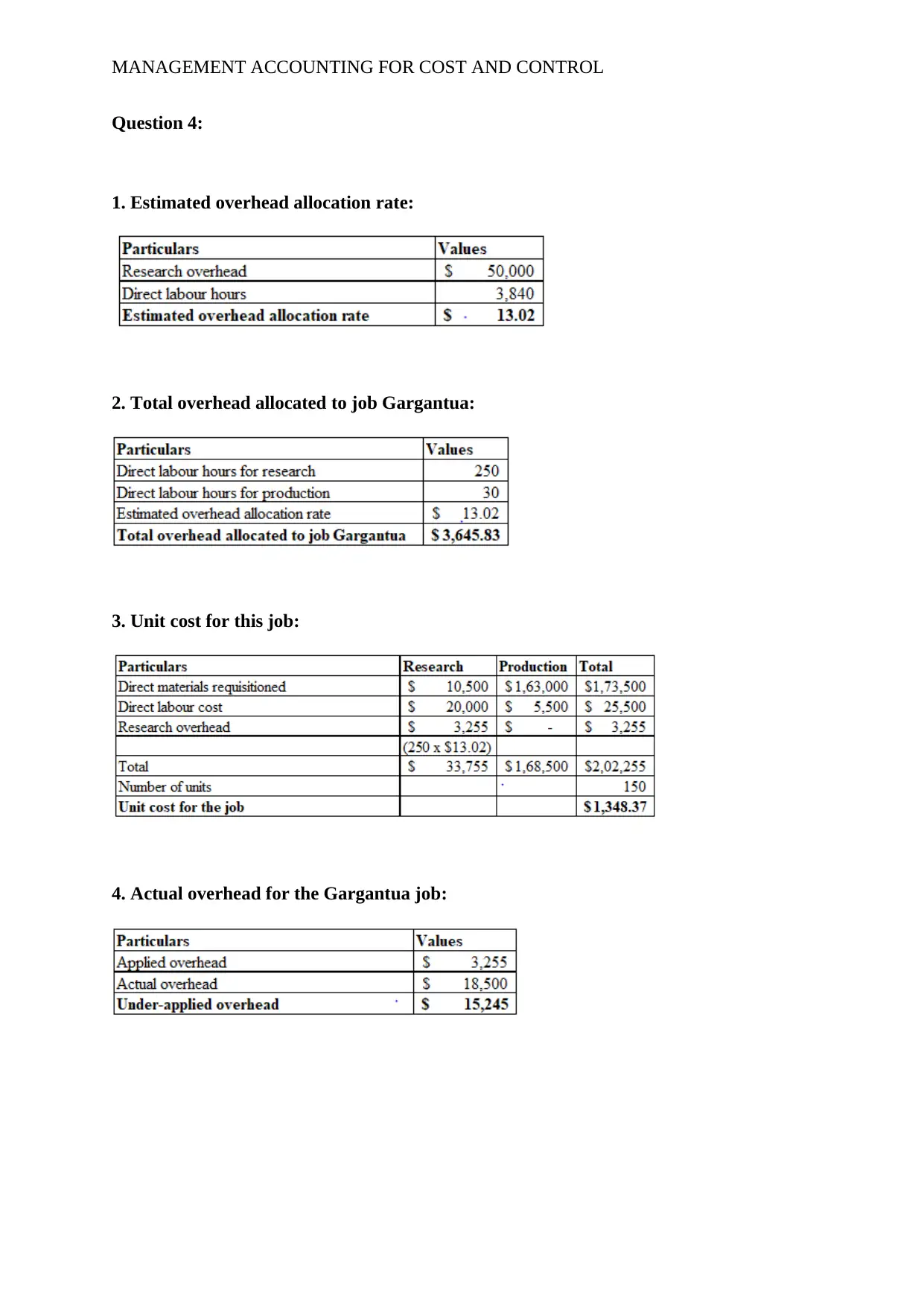

Question 4:

1. Estimated overhead allocation rate:

2. Total overhead allocated to job Gargantua:

3. Unit cost for this job:

4. Actual overhead for the Gargantua job:

Question 4:

1. Estimated overhead allocation rate:

2. Total overhead allocated to job Gargantua:

3. Unit cost for this job:

4. Actual overhead for the Gargantua job:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

5. Journal entries to record the allocation:

6. Total profit and the profit per unit:

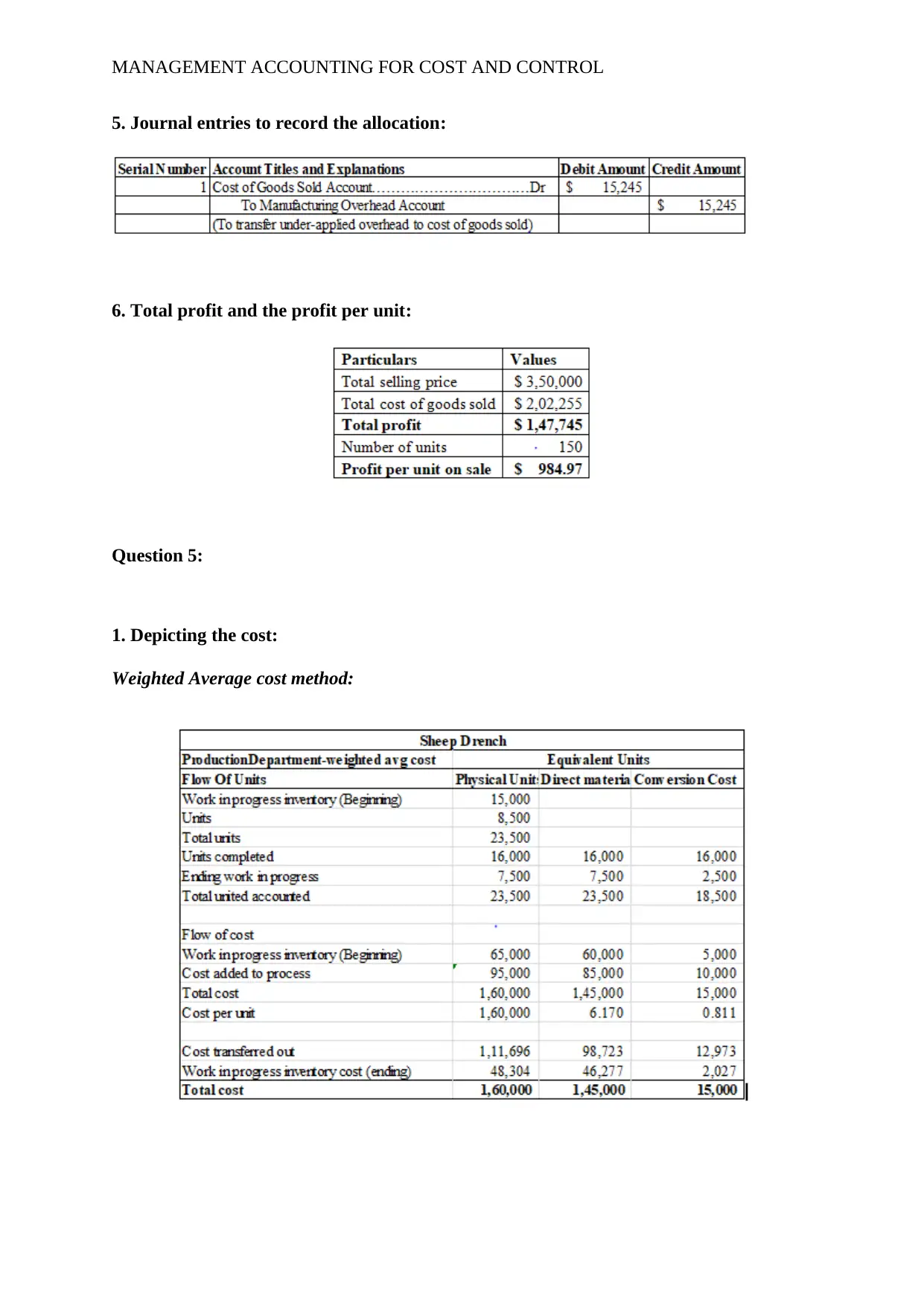

Question 5:

1. Depicting the cost:

Weighted Average cost method:

5. Journal entries to record the allocation:

6. Total profit and the profit per unit:

Question 5:

1. Depicting the cost:

Weighted Average cost method:

MANAGEMENT ACCOUNTING FOR COST AND CONTROL

ProductionDepartment-weighted avg cost

Flow Of Units Physical Units Direct material Conversion Cost

Work in progress inventory (Beginning) 15000

Units =+C16

Total units =SUM(H6:H7)

Units completed 16000 16000 16000

Ending work in progress 7500 =+H10 =+H10/3

Total united accounted =SUM(H9:H10) =SUM(I9:I10) =SUM(J9:J10)

Flow of cost

Work in progress inventory (Beginning) =+SUM(C7:C8) =+C7 =+C8

Cost added to process =SUM(C14:C15) =+C14 =+C15

Total cost =SUM(H14:H15) =SUM(I14:I15) =SUM(J14:J15)

Cost per unit =+H16 =+I16/I11 =+J16/J11

Cost transferred out =SUM(I19:J19) =+I17*I9 =+J17*J9

Work in progress inventory cost (ending) =SUM(I20:J20) =+I17*I10 =+J17*J10

Total cost =SUM(H19:H20) =SUM(I19:I20) =SUM(J19:J20)

ProductionDepartment-weighted avg cost

Flow Of Units Physical Units Direct material Conversion Cost

Work in progress inventory (Beginning) 25000

Units =+D16

Total units =SUM(H26:H27)

Units completed 30000 =+H29 =+I29

Ending work in progress 15000 =+H30 =+I30*20%

Total united accounted =SUM(H29:H30) =SUM(I29:I30) =SUM(J29:J30)

Flow of cost

Work in progress inventory (Beginning) =+SUM(D7:D8) =+D7 =+D8

Cost added to process =SUM(D14:D15) =+D14 =+D15

Total cost =SUM(H34:H35) =SUM(I34:I35) =SUM(J34:J35)

Cost per unit =+H36 =+I36/I31 =+J36/J31

Cost transferred out =SUM(I39:J39) =+I37*I29 =+J37*J29

Work in progress inventory cost (ending) =SUM(I40:J40) =+I37*I30 =+J37*J30

Total cost =SUM(H39:H40) =SUM(I39:I40) =SUM(J39:J40)

=+D4

Equivalent Units

=+C4

Equivalent Units

FIFO Method:

ProductionDepartment-weighted avg cost

Flow Of Units Physical Units Direct material Conversion Cost

Work in progress inventory (Beginning) 15000

Units =+C16

Total units =SUM(H6:H7)

Units completed 16000 16000 16000

Ending work in progress 7500 =+H10 =+H10/3

Total united accounted =SUM(H9:H10) =SUM(I9:I10) =SUM(J9:J10)

Flow of cost

Work in progress inventory (Beginning) =+SUM(C7:C8) =+C7 =+C8

Cost added to process =SUM(C14:C15) =+C14 =+C15

Total cost =SUM(H14:H15) =SUM(I14:I15) =SUM(J14:J15)

Cost per unit =+H16 =+I16/I11 =+J16/J11

Cost transferred out =SUM(I19:J19) =+I17*I9 =+J17*J9

Work in progress inventory cost (ending) =SUM(I20:J20) =+I17*I10 =+J17*J10

Total cost =SUM(H19:H20) =SUM(I19:I20) =SUM(J19:J20)

ProductionDepartment-weighted avg cost

Flow Of Units Physical Units Direct material Conversion Cost

Work in progress inventory (Beginning) 25000

Units =+D16

Total units =SUM(H26:H27)

Units completed 30000 =+H29 =+I29

Ending work in progress 15000 =+H30 =+I30*20%

Total united accounted =SUM(H29:H30) =SUM(I29:I30) =SUM(J29:J30)

Flow of cost

Work in progress inventory (Beginning) =+SUM(D7:D8) =+D7 =+D8

Cost added to process =SUM(D14:D15) =+D14 =+D15

Total cost =SUM(H34:H35) =SUM(I34:I35) =SUM(J34:J35)

Cost per unit =+H36 =+I36/I31 =+J36/J31

Cost transferred out =SUM(I39:J39) =+I37*I29 =+J37*J29

Work in progress inventory cost (ending) =SUM(I40:J40) =+I37*I30 =+J37*J30

Total cost =SUM(H39:H40) =SUM(I39:I40) =SUM(J39:J40)

=+D4

Equivalent Units

=+C4

Equivalent Units

FIFO Method:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.