Regression Analysis and Cost Estimation in Management Accounting

VerifiedAdded on 2024/05/14

|19

|3296

|218

Report

AI Summary

This report provides a comprehensive analysis of cost estimation using regression analysis within a management accounting context. It includes an overhead cost equation derived from regression results, calculations of total costs for specific projects, and explanations for discrepancies between regression-based overhead rates and preliminary estimates. The report also presents a bid calculation for a landscaping project, incorporating overtime considerations. Furthermore, it contains a literature review comparing traditional and contemporary costing systems, highlighting the importance of identifying various cost drivers for informed decision-making. The literature review also delves into the classification of costs into fixed, variable, and semi-variable categories, illustrating their impact on business operations. This student contributed report is available on Desklib, where students can find similar solved assignments and study tools.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Part I – Part I Report........................................................................................................................3

Introduction:.................................................................................................................................3

Q1. Overhead cost equation developed based on regression results........................................3

Q2. Calculate total cost for 500 square metres of landscaping using the overhead formula

that was derived from the regression analysis..........................................................................3

Q3. Explain why the overhead rate calculated from the regression analysis is different from

preliminary estimate of $ 19 per direct labour hour.................................................................3

Q4. Calculate and include a bid on a landscaping project consisting of 100 000 square

metres. Mary estimates that 20% of the direct labour hours required for the project will be

on overtime...............................................................................................................................4

Q5. Explain as to how Greenery Pty Ltd relies on the overhead formula derived from the

regression analysis as the basis for the variable overhead component of its cost estimate......4

Recommendation and Conclusion:..............................................................................................5

Part II Literature Review.................................................................................................................6

Executive summary:.....................................................................................................................6

Content:........................................................................................................................................7

Conclusion:................................................................................................................................13

References:....................................................................................................................................14

Appendices:...................................................................................................................................15

2

Part I – Part I Report........................................................................................................................3

Introduction:.................................................................................................................................3

Q1. Overhead cost equation developed based on regression results........................................3

Q2. Calculate total cost for 500 square metres of landscaping using the overhead formula

that was derived from the regression analysis..........................................................................3

Q3. Explain why the overhead rate calculated from the regression analysis is different from

preliminary estimate of $ 19 per direct labour hour.................................................................3

Q4. Calculate and include a bid on a landscaping project consisting of 100 000 square

metres. Mary estimates that 20% of the direct labour hours required for the project will be

on overtime...............................................................................................................................4

Q5. Explain as to how Greenery Pty Ltd relies on the overhead formula derived from the

regression analysis as the basis for the variable overhead component of its cost estimate......4

Recommendation and Conclusion:..............................................................................................5

Part II Literature Review.................................................................................................................6

Executive summary:.....................................................................................................................6

Content:........................................................................................................................................7

Conclusion:................................................................................................................................13

References:....................................................................................................................................14

Appendices:...................................................................................................................................15

2

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part I – Part I Report

Introduction:

The report is concerned with performing a regression analysis for a given project which is related

with management accounting concepts and costing systems. The report will present an overhead

cost equation which will help in making costing decision for the project under consideration. The

total cost associated with the given problem will be identified and analysis will be performed in

this report. The observations related with overhead cost allocation and absorption will be

discussed in this report.

Q1. Overhead cost equation developed based on regression results.

Y = total overheads = 25901.05 + 10.60 * total labour hours

It implies that for each unit decrease in total direct labour hours, total overheads increase with

10.60 units.

Q2. Calculate total cost for 500 square metres of landscaping using the overhead formula

that was derived from the regression analysis.

For 500 square metres of landscaping, 6 direct labour hours will be needed and accordingly

overhead cost, being dependent on labour hours, will be charged accordingly.

Taking the regression equation into consideration, total overhead costs will be computed.

Overhead cost for 6 direct labour hours will be 10.60*6 = 63.6.

Direct material cost and direct labour cost amounting $500 and $126 will remain same. Total

cost will be = (500+126+63.6) = $689.6.

Q3. Explain why the overhead rate calculated from the regression analysis is different from

preliminary estimate of $ 19 per direct labour hour.

This is different from the preliminary estimate because the same was based on traditional

approach of cost accounting in which consideration was given to labour hours worked only

4

Introduction:

The report is concerned with performing a regression analysis for a given project which is related

with management accounting concepts and costing systems. The report will present an overhead

cost equation which will help in making costing decision for the project under consideration. The

total cost associated with the given problem will be identified and analysis will be performed in

this report. The observations related with overhead cost allocation and absorption will be

discussed in this report.

Q1. Overhead cost equation developed based on regression results.

Y = total overheads = 25901.05 + 10.60 * total labour hours

It implies that for each unit decrease in total direct labour hours, total overheads increase with

10.60 units.

Q2. Calculate total cost for 500 square metres of landscaping using the overhead formula

that was derived from the regression analysis.

For 500 square metres of landscaping, 6 direct labour hours will be needed and accordingly

overhead cost, being dependent on labour hours, will be charged accordingly.

Taking the regression equation into consideration, total overhead costs will be computed.

Overhead cost for 6 direct labour hours will be 10.60*6 = 63.6.

Direct material cost and direct labour cost amounting $500 and $126 will remain same. Total

cost will be = (500+126+63.6) = $689.6.

Q3. Explain why the overhead rate calculated from the regression analysis is different from

preliminary estimate of $ 19 per direct labour hour.

This is different from the preliminary estimate because the same was based on traditional

approach of cost accounting in which consideration was given to labour hours worked only

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

however the regression analysis helps in considering the different factors and variables resulting

in costs occurred (Renz, et. al., 2016).

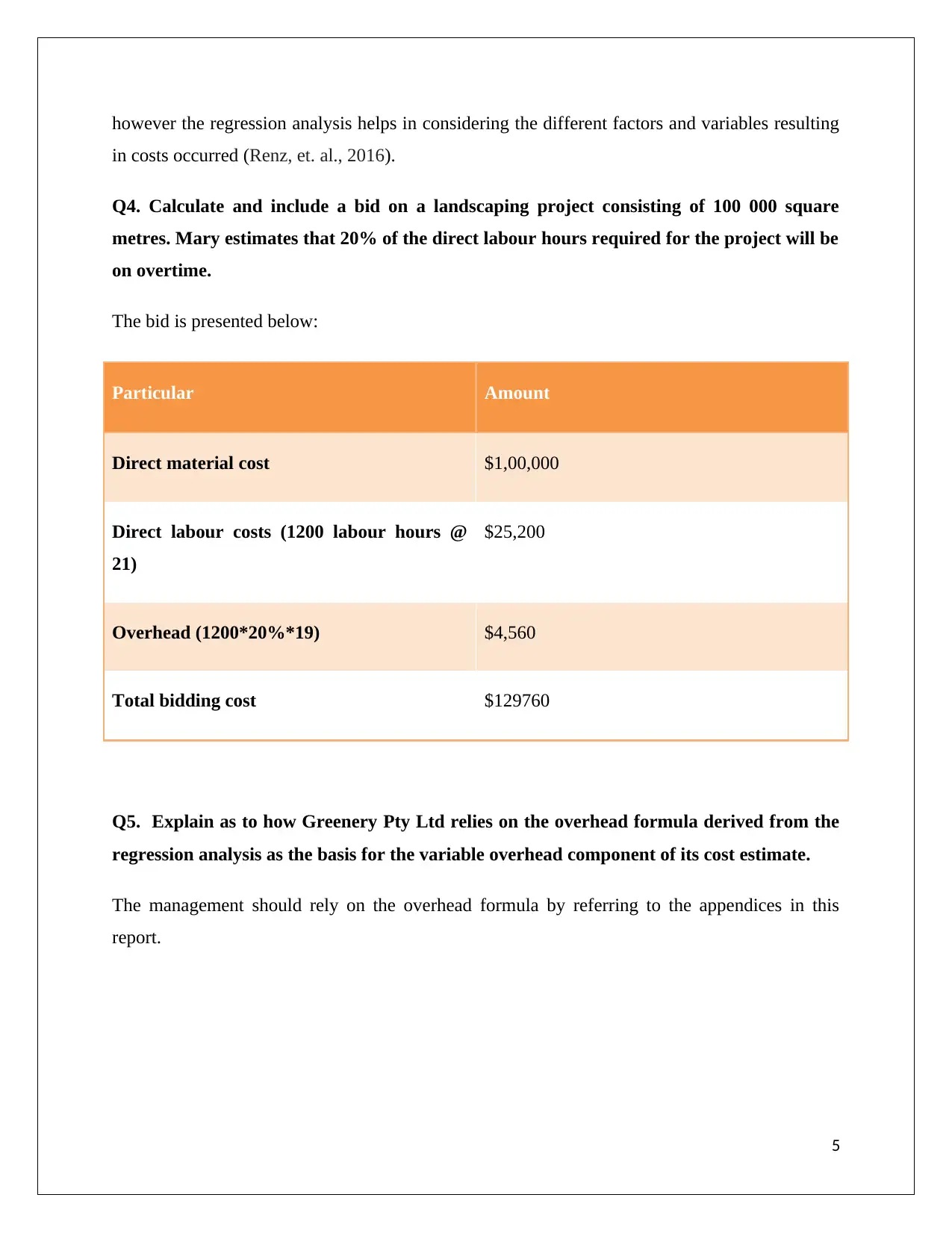

Q4. Calculate and include a bid on a landscaping project consisting of 100 000 square

metres. Mary estimates that 20% of the direct labour hours required for the project will be

on overtime.

The bid is presented below:

Particular Amount

Direct material cost $1,00,000

Direct labour costs (1200 labour hours @

21)

$25,200

Overhead (1200*20%*19) $4,560

Total bidding cost $129760

Q5. Explain as to how Greenery Pty Ltd relies on the overhead formula derived from the

regression analysis as the basis for the variable overhead component of its cost estimate.

The management should rely on the overhead formula by referring to the appendices in this

report.

5

in costs occurred (Renz, et. al., 2016).

Q4. Calculate and include a bid on a landscaping project consisting of 100 000 square

metres. Mary estimates that 20% of the direct labour hours required for the project will be

on overtime.

The bid is presented below:

Particular Amount

Direct material cost $1,00,000

Direct labour costs (1200 labour hours @

21)

$25,200

Overhead (1200*20%*19) $4,560

Total bidding cost $129760

Q5. Explain as to how Greenery Pty Ltd relies on the overhead formula derived from the

regression analysis as the basis for the variable overhead component of its cost estimate.

The management should rely on the overhead formula by referring to the appendices in this

report.

5

Recommendation and Conclusion:

It can be recommended and concluded that the modern technique of identifying cost drivers will

help in achieving better decision making. The application of management accounting techniques

such as regression analysis can help the management in taking appropriate decision and cost

estimates.

6

It can be recommended and concluded that the modern technique of identifying cost drivers will

help in achieving better decision making. The application of management accounting techniques

such as regression analysis can help the management in taking appropriate decision and cost

estimates.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part II Literature Review

Executive summary:

The modern business organisation and business managers have realized the importance of

measuring the behaviour of cost in an enterprise for vital decision making purposes.

Understanding the behaviour of costs in relation to the production activities helps the managers

in making important and critical decision in the business. The concept of fixed, variable and semi

variable cost have evolved over the last decade and the management needs to consider the same

while making decisions about the cost aspects of the company. The report will help in evaluating

the key components associated with traditional costing system and the contemporary costing

system in an enterprise. The explanation regarding the different elements of cost associated with

fixed and variable costs will be explained in this report. This will help the management in

analysing the change in identifying the cost drivers in contemporary costing system and

traditional costing system of company.

7

Executive summary:

The modern business organisation and business managers have realized the importance of

measuring the behaviour of cost in an enterprise for vital decision making purposes.

Understanding the behaviour of costs in relation to the production activities helps the managers

in making important and critical decision in the business. The concept of fixed, variable and semi

variable cost have evolved over the last decade and the management needs to consider the same

while making decisions about the cost aspects of the company. The report will help in evaluating

the key components associated with traditional costing system and the contemporary costing

system in an enterprise. The explanation regarding the different elements of cost associated with

fixed and variable costs will be explained in this report. This will help the management in

analysing the change in identifying the cost drivers in contemporary costing system and

traditional costing system of company.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Content:

As per (Renz, et. al., 2016), the traditional system of cost accounting can be referred to as the

system of accounting in which manufacturing overheads associated with the production

operation for company are allocated between the various products manufactured by the company

on the basis of volume of production. In traditional system of cost accounting the indirect

overheads related with the production operations are segregated and distributed on the basis of

volumes which includes number of units produced, based on the direct labour hours or the

production of machine hours on the company. The traditional costing system thus used only one

variable component to distribute the costs to different products of company. This may imply that

only that one variable component is the cause of factory overheads incurred in the company. On

the traditional perspective that seems to be sufficient for the company in preparing its external

financial statements. However in the modern business environment the manufacturing overheads

of the many are driven or caused by various other factors present in the manufacturing operations

(Kren, 2018). For example some of the customers may be likely to demand the additional

manufacturing operations for the diversified products of company while some wants greater

quantities of uniformed products of company. Therefore in order to acquire ad obtain the actual

or real cost of manufacturing which are specific to certain products or specific customers the

traditional costing system seems to be inadequate.

The different components associated with costing system in a company are related with:

Cost object – It represents something for which, measurement of cost is desired. In general these

represent the products or services provided by the company in ordinary course of business.

Direct costs – The direct cost represents the type of cost that can be directly attributable or traced

with the product or service of a company.

Indirect cost – Te indirect costs represents that portion of overall cost which can’t be directly

traced or attribute to a particular product or service of the company.

8

As per (Renz, et. al., 2016), the traditional system of cost accounting can be referred to as the

system of accounting in which manufacturing overheads associated with the production

operation for company are allocated between the various products manufactured by the company

on the basis of volume of production. In traditional system of cost accounting the indirect

overheads related with the production operations are segregated and distributed on the basis of

volumes which includes number of units produced, based on the direct labour hours or the

production of machine hours on the company. The traditional costing system thus used only one

variable component to distribute the costs to different products of company. This may imply that

only that one variable component is the cause of factory overheads incurred in the company. On

the traditional perspective that seems to be sufficient for the company in preparing its external

financial statements. However in the modern business environment the manufacturing overheads

of the many are driven or caused by various other factors present in the manufacturing operations

(Kren, 2018). For example some of the customers may be likely to demand the additional

manufacturing operations for the diversified products of company while some wants greater

quantities of uniformed products of company. Therefore in order to acquire ad obtain the actual

or real cost of manufacturing which are specific to certain products or specific customers the

traditional costing system seems to be inadequate.

The different components associated with costing system in a company are related with:

Cost object – It represents something for which, measurement of cost is desired. In general these

represent the products or services provided by the company in ordinary course of business.

Direct costs – The direct cost represents the type of cost that can be directly attributable or traced

with the product or service of a company.

Indirect cost – Te indirect costs represents that portion of overall cost which can’t be directly

traced or attribute to a particular product or service of the company.

8

Cost pool – The cost pool refers to the grouping associated with individual cost items in a

company. The cost pools are formed when the company uses more allocation base in allocating

the costs to different products and services.

Cost allocation base – It refers to the factor which links the systematic way for indirect cost

relating with the particular product or service.

The traditional costing system of management accounting used a single predetermined overhead

rate in order to distribute the indirect cost to products and these were as follows:

Job order costing – In this costing system the direct labour costs was assumed to be

relevant for the activity base and the costs are allocated on the basis of jobs performed.

Process costing – In the accounting system the machine hours are assumed to be relevant

activity base for the company. The processes are allocated the costs based on the machine

hours used.

The difference between contemporary management accounting system can be established with

traditional cost accounting system in the following manner:

There are limited number of cost accounting pools identified in the traditional accounting

system and the allocation is restricted to only one variable cost driver however in

contemporary cost accounting various or many cost drivers are identified and used for

reflecting different activities in the manufacturing operations (Christopher, 2016).

The allocation of overheads in this type of costing system is associated with assigning the

overhead cost first to departments and then they are distributed among different products

and services while in contemporary cost accounting system the overhead costs are

assigned to different activity pools and then they are charged to different products and

services.

The focus associated with traditional costing system is related with managing costs

aspects of different functional departments or the responsibility centres however the

focus in contemporary costing system is associated with managing processes and

activities and solving the cross functional problems associated with cost in the company.

9

company. The cost pools are formed when the company uses more allocation base in allocating

the costs to different products and services.

Cost allocation base – It refers to the factor which links the systematic way for indirect cost

relating with the particular product or service.

The traditional costing system of management accounting used a single predetermined overhead

rate in order to distribute the indirect cost to products and these were as follows:

Job order costing – In this costing system the direct labour costs was assumed to be

relevant for the activity base and the costs are allocated on the basis of jobs performed.

Process costing – In the accounting system the machine hours are assumed to be relevant

activity base for the company. The processes are allocated the costs based on the machine

hours used.

The difference between contemporary management accounting system can be established with

traditional cost accounting system in the following manner:

There are limited number of cost accounting pools identified in the traditional accounting

system and the allocation is restricted to only one variable cost driver however in

contemporary cost accounting various or many cost drivers are identified and used for

reflecting different activities in the manufacturing operations (Christopher, 2016).

The allocation of overheads in this type of costing system is associated with assigning the

overhead cost first to departments and then they are distributed among different products

and services while in contemporary cost accounting system the overhead costs are

assigned to different activity pools and then they are charged to different products and

services.

The focus associated with traditional costing system is related with managing costs

aspects of different functional departments or the responsibility centres however the

focus in contemporary costing system is associated with managing processes and

activities and solving the cross functional problems associated with cost in the company.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The use of traditional costing methods were easy but it does not involve any type of value

added function which could help in decision making function while the contemporary

cost accounting system proves to be capital intensive function, product diversified and

have higher capabilities of assisting in decision making function of managers in the

company (Kren, 2018). The reports obtained in this modernized accounting system helps

in analysing the current cost aspects of company and this will help the business managers

in taking critical decisions.

In the past researches related with cost the costs has been classified into three categories

concerning with fixed, variable and semi variable costs. The classification of these types of costs

helps the company in identifying the nature of activity performed and the decisions can be taken

effectively. The various components are explained below:

Fixed costs – The fixed cost as the name suggest represents the portion of costs that remain

constant over the given period of time and range of activities in spite of different types of

fluctuations associated with the level of production. However the per unit fixed cost of

production varies with the level of activity performed in a company but the overall fixed cost

remain constant during the period (Otley, 2016). This leads to the fact that if the production

volumes increases in the company the per unit fixed cost decreases for the company and if the

volume of production decreases the per unit fixed cost increases. In order to explain this concept

in relation to company two examples have been explained:

Star Limited which is a manufacturing company engage in production of electrical wires have a

fixed cost associated with building in the form of premises, depreciation on plant and machinery

associated with production operations. The fixed cost pattern for this company is explained

below:

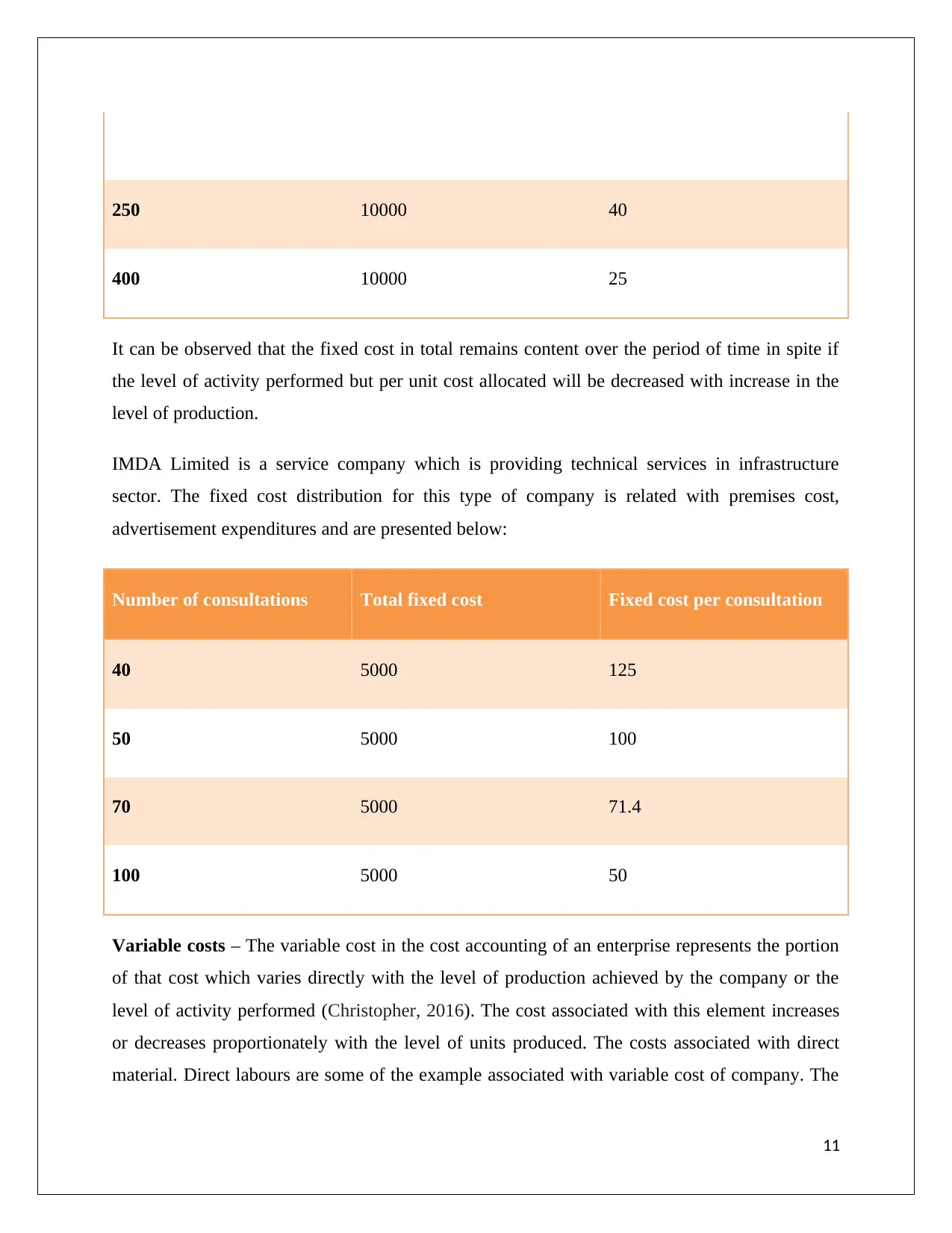

Output (Cms) Total fixed cost Fixed cost per cms

100 10000 100

200 10000 50

10

added function which could help in decision making function while the contemporary

cost accounting system proves to be capital intensive function, product diversified and

have higher capabilities of assisting in decision making function of managers in the

company (Kren, 2018). The reports obtained in this modernized accounting system helps

in analysing the current cost aspects of company and this will help the business managers

in taking critical decisions.

In the past researches related with cost the costs has been classified into three categories

concerning with fixed, variable and semi variable costs. The classification of these types of costs

helps the company in identifying the nature of activity performed and the decisions can be taken

effectively. The various components are explained below:

Fixed costs – The fixed cost as the name suggest represents the portion of costs that remain

constant over the given period of time and range of activities in spite of different types of

fluctuations associated with the level of production. However the per unit fixed cost of

production varies with the level of activity performed in a company but the overall fixed cost

remain constant during the period (Otley, 2016). This leads to the fact that if the production

volumes increases in the company the per unit fixed cost decreases for the company and if the

volume of production decreases the per unit fixed cost increases. In order to explain this concept

in relation to company two examples have been explained:

Star Limited which is a manufacturing company engage in production of electrical wires have a

fixed cost associated with building in the form of premises, depreciation on plant and machinery

associated with production operations. The fixed cost pattern for this company is explained

below:

Output (Cms) Total fixed cost Fixed cost per cms

100 10000 100

200 10000 50

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

250 10000 40

400 10000 25

It can be observed that the fixed cost in total remains content over the period of time in spite if

the level of activity performed but per unit cost allocated will be decreased with increase in the

level of production.

IMDA Limited is a service company which is providing technical services in infrastructure

sector. The fixed cost distribution for this type of company is related with premises cost,

advertisement expenditures and are presented below:

Number of consultations Total fixed cost Fixed cost per consultation

40 5000 125

50 5000 100

70 5000 71.4

100 5000 50

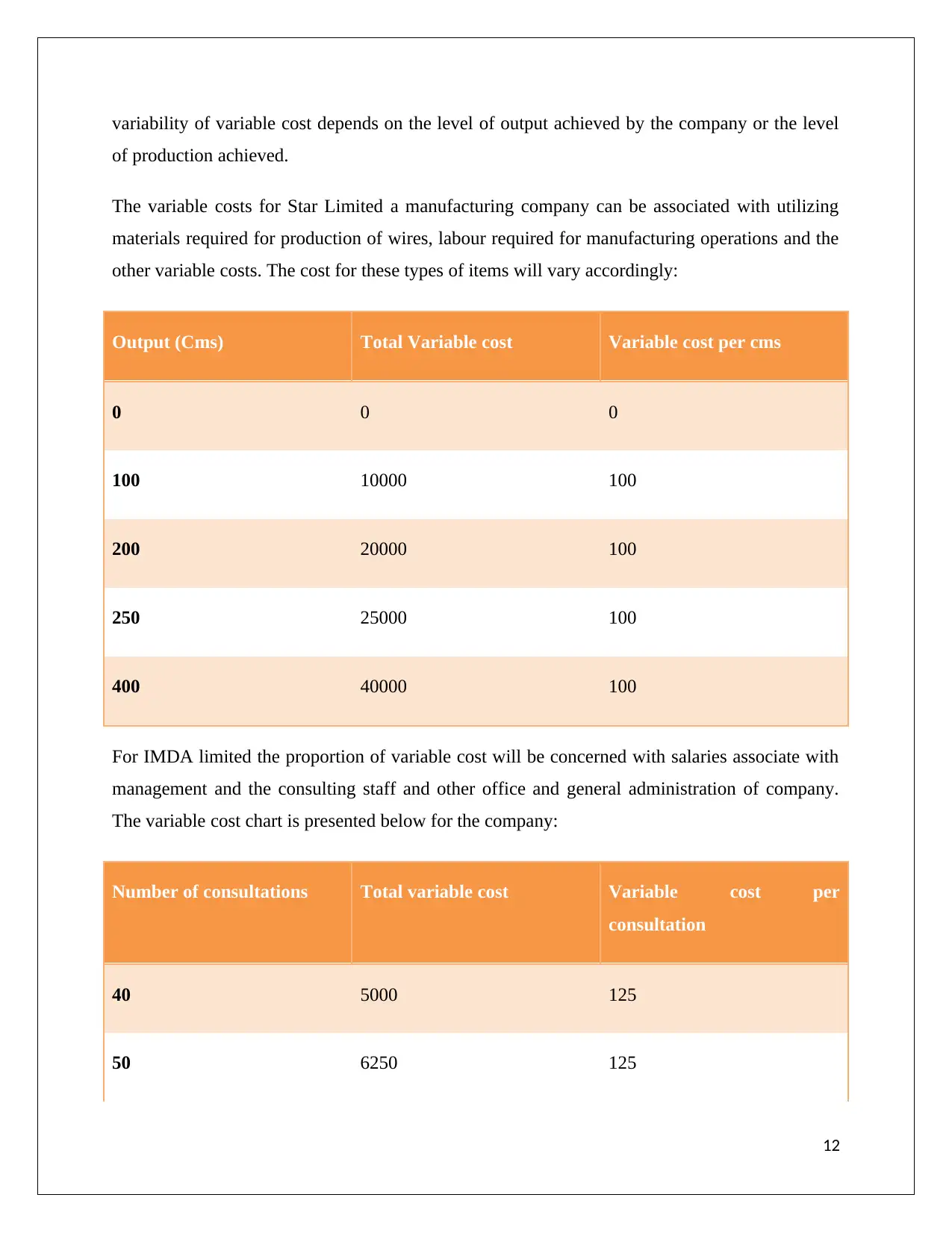

Variable costs – The variable cost in the cost accounting of an enterprise represents the portion

of that cost which varies directly with the level of production achieved by the company or the

level of activity performed (Christopher, 2016). The cost associated with this element increases

or decreases proportionately with the level of units produced. The costs associated with direct

material. Direct labours are some of the example associated with variable cost of company. The

11

400 10000 25

It can be observed that the fixed cost in total remains content over the period of time in spite if

the level of activity performed but per unit cost allocated will be decreased with increase in the

level of production.

IMDA Limited is a service company which is providing technical services in infrastructure

sector. The fixed cost distribution for this type of company is related with premises cost,

advertisement expenditures and are presented below:

Number of consultations Total fixed cost Fixed cost per consultation

40 5000 125

50 5000 100

70 5000 71.4

100 5000 50

Variable costs – The variable cost in the cost accounting of an enterprise represents the portion

of that cost which varies directly with the level of production achieved by the company or the

level of activity performed (Christopher, 2016). The cost associated with this element increases

or decreases proportionately with the level of units produced. The costs associated with direct

material. Direct labours are some of the example associated with variable cost of company. The

11

variability of variable cost depends on the level of output achieved by the company or the level

of production achieved.

The variable costs for Star Limited a manufacturing company can be associated with utilizing

materials required for production of wires, labour required for manufacturing operations and the

other variable costs. The cost for these types of items will vary accordingly:

Output (Cms) Total Variable cost Variable cost per cms

0 0 0

100 10000 100

200 20000 100

250 25000 100

400 40000 100

For IMDA limited the proportion of variable cost will be concerned with salaries associate with

management and the consulting staff and other office and general administration of company.

The variable cost chart is presented below for the company:

Number of consultations Total variable cost Variable cost per

consultation

40 5000 125

50 6250 125

12

of production achieved.

The variable costs for Star Limited a manufacturing company can be associated with utilizing

materials required for production of wires, labour required for manufacturing operations and the

other variable costs. The cost for these types of items will vary accordingly:

Output (Cms) Total Variable cost Variable cost per cms

0 0 0

100 10000 100

200 20000 100

250 25000 100

400 40000 100

For IMDA limited the proportion of variable cost will be concerned with salaries associate with

management and the consulting staff and other office and general administration of company.

The variable cost chart is presented below for the company:

Number of consultations Total variable cost Variable cost per

consultation

40 5000 125

50 6250 125

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.