Cost Accounting: Core Concepts, Methods, and Applications

VerifiedAdded on 2022/01/21

|19

|7215

|79

Homework Assignment

AI Summary

This assignment delves into the core concepts of cost accounting, starting with the fundamental reasons for its existence in business. It defines cost accounting, contrasting it with financial accounting and highlighting their complementary roles. The document outlines the differences between financial and management accounting, emphasizing the distinct objectives and information needs they serve. It then compares cost accounting with management accounting, elucidating their relationship and the activities involved in each. Furthermore, the assignment lists the advantages of a well-organized cost accounting system, such as improved decision-making and cost control. Key terms like 'cost' and 'expenditure' are defined, and the concepts of cost ascertainment and cost estimation are explained, including their differences and respective uses. The document provides a comprehensive introduction to the field, suitable for students learning the basics of cost accounting.

Joseph Anbarasu

Basics of

Cost

Accounting

Cost Accounting

Basics of

Cost

Accounting

Cost Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Joseph Anbarasu

CHAPTER 1

COST ACCOUNTING

INTRODUCTION

1. Why should there be costing in the field of business?

Costing is a branch of accounting. It helps us to classify, record, and

allocate the expenditure for the determination of costs of product.

Expenditure involved in business has to be ascertained to fix the price of a

product produced. The expenditure is to be understood in terms of

material, labour and other direct and indirect expenses. The major purpose

of such classification is to estimate the profit and to understand its

relationship with costs and price. The three elements of a transaction i.e.,

cost, profit and price are necessary components of any business activity.

Example:

A mobile phone factory introduces a new device. The factory

incurs Rs. 400 for material, Rs.400 for labour and Rs.200 for

overhead on every mobile phone produced and supplied in the

market. The total cost comes around Rs.1000. If the price of the

device is Rs. 1500, the profit per device is Rs. 500 (1500-1000).

The management requires all information as seen in the example for each

product produced. The above estimation is done for the purpose of

planning, cost control and decision-making. The existing system of

financial accounting does not provide the necessary information to do

similar estimation. Such deficiency of financial accounting has given rise to

the need of cost accounting.

2. Define cost accounting.

The word ‘Costing’ refers to the technique and process of ascertaining

costs. There have been certain rules and principles in the field of costing

developed over years by our forefathers. These rules and principles help us

to ascertain the cost of products produced. The term 'Cost Accounting’

refers to the recording of all incomes and expenditures and ends with the

preparation of periodical statements and reports for ascertaining and

controlling costs.

Definitions of Cost Accounting.

According to the Terminology used by the Institute of Cost and

Management Accountants, “Cost accounting is the part of

management accounting which establishes budgets and

standard costs and actual costs of operations, processes,

departments or products and the analysis of variances,

profitability or social use of funds.”

Cost Accounting

CHAPTER 1

COST ACCOUNTING

INTRODUCTION

1. Why should there be costing in the field of business?

Costing is a branch of accounting. It helps us to classify, record, and

allocate the expenditure for the determination of costs of product.

Expenditure involved in business has to be ascertained to fix the price of a

product produced. The expenditure is to be understood in terms of

material, labour and other direct and indirect expenses. The major purpose

of such classification is to estimate the profit and to understand its

relationship with costs and price. The three elements of a transaction i.e.,

cost, profit and price are necessary components of any business activity.

Example:

A mobile phone factory introduces a new device. The factory

incurs Rs. 400 for material, Rs.400 for labour and Rs.200 for

overhead on every mobile phone produced and supplied in the

market. The total cost comes around Rs.1000. If the price of the

device is Rs. 1500, the profit per device is Rs. 500 (1500-1000).

The management requires all information as seen in the example for each

product produced. The above estimation is done for the purpose of

planning, cost control and decision-making. The existing system of

financial accounting does not provide the necessary information to do

similar estimation. Such deficiency of financial accounting has given rise to

the need of cost accounting.

2. Define cost accounting.

The word ‘Costing’ refers to the technique and process of ascertaining

costs. There have been certain rules and principles in the field of costing

developed over years by our forefathers. These rules and principles help us

to ascertain the cost of products produced. The term 'Cost Accounting’

refers to the recording of all incomes and expenditures and ends with the

preparation of periodical statements and reports for ascertaining and

controlling costs.

Definitions of Cost Accounting.

According to the Terminology used by the Institute of Cost and

Management Accountants, “Cost accounting is the part of

management accounting which establishes budgets and

standard costs and actual costs of operations, processes,

departments or products and the analysis of variances,

profitability or social use of funds.”

Cost Accounting

Joseph Anbarasu

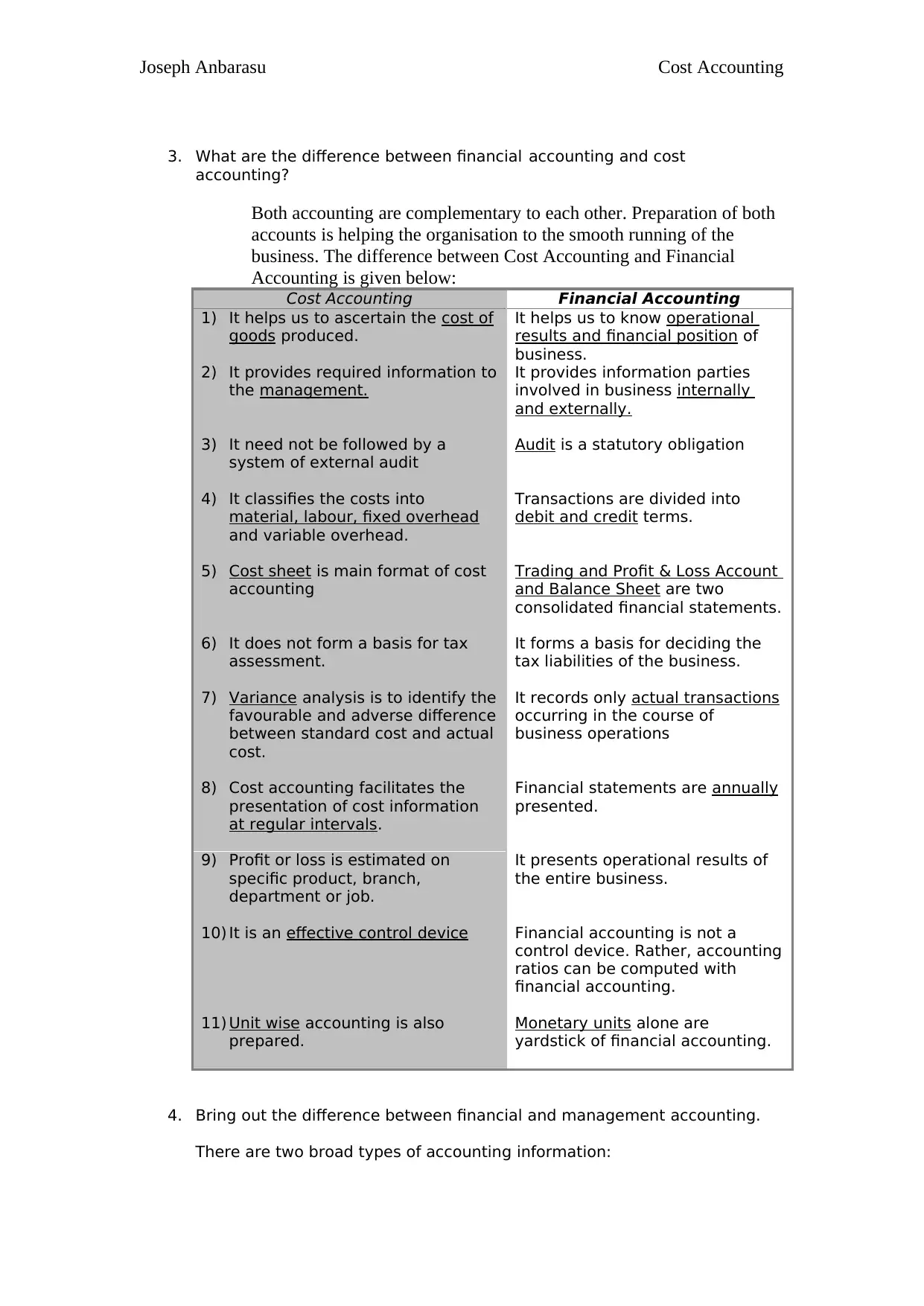

3. What are the difference between financial accounting and cost

accounting?

Both accounting are complementary to each other. Preparation of both

accounts is helping the organisation to the smooth running of the

business. The difference between Cost Accounting and Financial

Accounting is given below:

Cost Accounting Financial Accounting

1) It helps us to ascertain the cost of

goods produced.

It helps us to know operational

results and financial position of

business.

2) It provides required information to

the management.

It provides information parties

involved in business internally

and externally.

3) It need not be followed by a

system of external audit

Audit is a statutory obligation

4) It classifies the costs into

material, labour, fixed overhead

and variable overhead.

Transactions are divided into

debit and credit terms.

5) Cost sheet is main format of cost

accounting

Trading and Profit & Loss Account

and Balance Sheet are two

consolidated financial statements.

6) It does not form a basis for tax

assessment.

It forms a basis for deciding the

tax liabilities of the business.

7) Variance analysis is to identify the

favourable and adverse difference

between standard cost and actual

cost.

It records only actual transactions

occurring in the course of

business operations

8) Cost accounting facilitates the

presentation of cost information

at regular intervals.

Financial statements are annually

presented.

9) Profit or loss is estimated on

specific product, branch,

department or job.

It presents operational results of

the entire business.

10) It is an effective control device Financial accounting is not a

control device. Rather, accounting

ratios can be computed with

financial accounting.

11) Unit wise accounting is also

prepared.

Monetary units alone are

yardstick of financial accounting.

4. Bring out the difference between financial and management accounting.

There are two broad types of accounting information:

Cost Accounting

3. What are the difference between financial accounting and cost

accounting?

Both accounting are complementary to each other. Preparation of both

accounts is helping the organisation to the smooth running of the

business. The difference between Cost Accounting and Financial

Accounting is given below:

Cost Accounting Financial Accounting

1) It helps us to ascertain the cost of

goods produced.

It helps us to know operational

results and financial position of

business.

2) It provides required information to

the management.

It provides information parties

involved in business internally

and externally.

3) It need not be followed by a

system of external audit

Audit is a statutory obligation

4) It classifies the costs into

material, labour, fixed overhead

and variable overhead.

Transactions are divided into

debit and credit terms.

5) Cost sheet is main format of cost

accounting

Trading and Profit & Loss Account

and Balance Sheet are two

consolidated financial statements.

6) It does not form a basis for tax

assessment.

It forms a basis for deciding the

tax liabilities of the business.

7) Variance analysis is to identify the

favourable and adverse difference

between standard cost and actual

cost.

It records only actual transactions

occurring in the course of

business operations

8) Cost accounting facilitates the

presentation of cost information

at regular intervals.

Financial statements are annually

presented.

9) Profit or loss is estimated on

specific product, branch,

department or job.

It presents operational results of

the entire business.

10) It is an effective control device Financial accounting is not a

control device. Rather, accounting

ratios can be computed with

financial accounting.

11) Unit wise accounting is also

prepared.

Monetary units alone are

yardstick of financial accounting.

4. Bring out the difference between financial and management accounting.

There are two broad types of accounting information:

Cost Accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Joseph Anbarasu

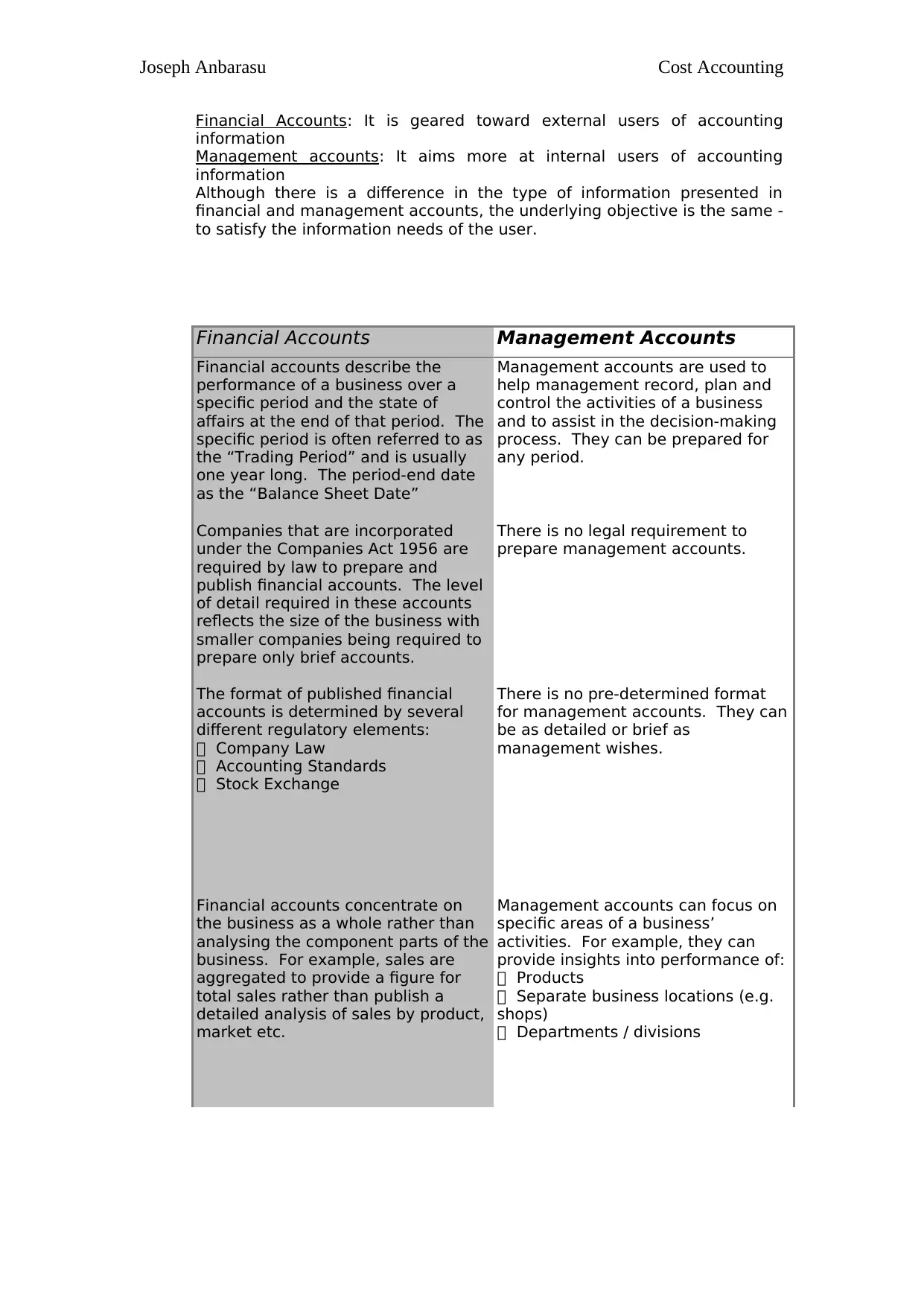

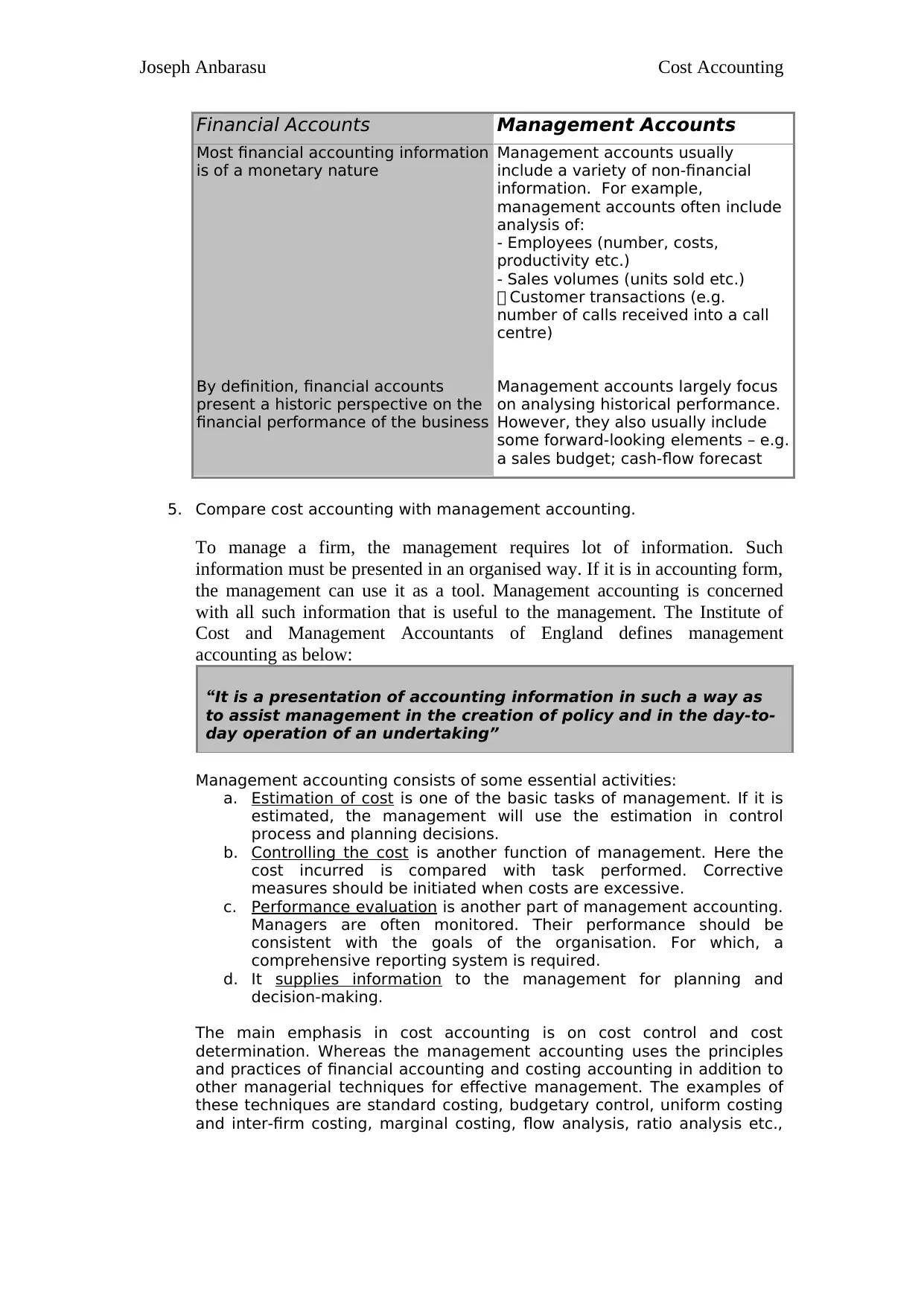

Financial Accounts: It is geared toward external users of accounting

information

Management accounts: It aims more at internal users of accounting

information

Although there is a difference in the type of information presented in

financial and management accounts, the underlying objective is the same -

to satisfy the information needs of the user.

Financial Accounts Management Accounts

Financial accounts describe the

performance of a business over a

specific period and the state of

affairs at the end of that period. The

specific period is often referred to as

the “Trading Period” and is usually

one year long. The period-end date

as the “Balance Sheet Date”

Management accounts are used to

help management record, plan and

control the activities of a business

and to assist in the decision-making

process. They can be prepared for

any period.

Companies that are incorporated

under the Companies Act 1956 are

required by law to prepare and

publish financial accounts. The level

of detail required in these accounts

reflects the size of the business with

smaller companies being required to

prepare only brief accounts.

There is no legal requirement to

prepare management accounts.

The format of published financial

accounts is determined by several

different regulatory elements:

Company Law

Accounting Standards

Stock Exchange

There is no pre-determined format

for management accounts. They can

be as detailed or brief as

management wishes.

Financial accounts concentrate on

the business as a whole rather than

analysing the component parts of the

business. For example, sales are

aggregated to provide a figure for

total sales rather than publish a

detailed analysis of sales by product,

market etc.

Management accounts can focus on

specific areas of a business’

activities. For example, they can

provide insights into performance of:

Products

Separate business locations (e.g.

shops)

Departments / divisions

Cost Accounting

Financial Accounts: It is geared toward external users of accounting

information

Management accounts: It aims more at internal users of accounting

information

Although there is a difference in the type of information presented in

financial and management accounts, the underlying objective is the same -

to satisfy the information needs of the user.

Financial Accounts Management Accounts

Financial accounts describe the

performance of a business over a

specific period and the state of

affairs at the end of that period. The

specific period is often referred to as

the “Trading Period” and is usually

one year long. The period-end date

as the “Balance Sheet Date”

Management accounts are used to

help management record, plan and

control the activities of a business

and to assist in the decision-making

process. They can be prepared for

any period.

Companies that are incorporated

under the Companies Act 1956 are

required by law to prepare and

publish financial accounts. The level

of detail required in these accounts

reflects the size of the business with

smaller companies being required to

prepare only brief accounts.

There is no legal requirement to

prepare management accounts.

The format of published financial

accounts is determined by several

different regulatory elements:

Company Law

Accounting Standards

Stock Exchange

There is no pre-determined format

for management accounts. They can

be as detailed or brief as

management wishes.

Financial accounts concentrate on

the business as a whole rather than

analysing the component parts of the

business. For example, sales are

aggregated to provide a figure for

total sales rather than publish a

detailed analysis of sales by product,

market etc.

Management accounts can focus on

specific areas of a business’

activities. For example, they can

provide insights into performance of:

Products

Separate business locations (e.g.

shops)

Departments / divisions

Cost Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Joseph Anbarasu

Financial Accounts Management Accounts

Most financial accounting information

is of a monetary nature

Management accounts usually

include a variety of non-financial

information. For example,

management accounts often include

analysis of:

- Employees (number, costs,

productivity etc.)

- Sales volumes (units sold etc.)

Customer transactions (e.g.

number of calls received into a call

centre)

By definition, financial accounts

present a historic perspective on the

financial performance of the business

Management accounts largely focus

on analysing historical performance.

However, they also usually include

some forward-looking elements – e.g.

a sales budget; cash-flow forecast

5. Compare cost accounting with management accounting.

To manage a firm, the management requires lot of information. Such

information must be presented in an organised way. If it is in accounting form,

the management can use it as a tool. Management accounting is concerned

with all such information that is useful to the management. The Institute of

Cost and Management Accountants of England defines management

accounting as below:

“It is a presentation of accounting information in such a way as

to assist management in the creation of policy and in the day-to-

day operation of an undertaking”

Management accounting consists of some essential activities:

a. Estimation of cost is one of the basic tasks of management. If it is

estimated, the management will use the estimation in control

process and planning decisions.

b. Controlling the cost is another function of management. Here the

cost incurred is compared with task performed. Corrective

measures should be initiated when costs are excessive.

c. Performance evaluation is another part of management accounting.

Managers are often monitored. Their performance should be

consistent with the goals of the organisation. For which, a

comprehensive reporting system is required.

d. It supplies information to the management for planning and

decision-making.

The main emphasis in cost accounting is on cost control and cost

determination. Whereas the management accounting uses the principles

and practices of financial accounting and costing accounting in addition to

other managerial techniques for effective management. The examples of

these techniques are standard costing, budgetary control, uniform costing

and inter-firm costing, marginal costing, flow analysis, ratio analysis etc.,

Cost Accounting

Financial Accounts Management Accounts

Most financial accounting information

is of a monetary nature

Management accounts usually

include a variety of non-financial

information. For example,

management accounts often include

analysis of:

- Employees (number, costs,

productivity etc.)

- Sales volumes (units sold etc.)

Customer transactions (e.g.

number of calls received into a call

centre)

By definition, financial accounts

present a historic perspective on the

financial performance of the business

Management accounts largely focus

on analysing historical performance.

However, they also usually include

some forward-looking elements – e.g.

a sales budget; cash-flow forecast

5. Compare cost accounting with management accounting.

To manage a firm, the management requires lot of information. Such

information must be presented in an organised way. If it is in accounting form,

the management can use it as a tool. Management accounting is concerned

with all such information that is useful to the management. The Institute of

Cost and Management Accountants of England defines management

accounting as below:

“It is a presentation of accounting information in such a way as

to assist management in the creation of policy and in the day-to-

day operation of an undertaking”

Management accounting consists of some essential activities:

a. Estimation of cost is one of the basic tasks of management. If it is

estimated, the management will use the estimation in control

process and planning decisions.

b. Controlling the cost is another function of management. Here the

cost incurred is compared with task performed. Corrective

measures should be initiated when costs are excessive.

c. Performance evaluation is another part of management accounting.

Managers are often monitored. Their performance should be

consistent with the goals of the organisation. For which, a

comprehensive reporting system is required.

d. It supplies information to the management for planning and

decision-making.

The main emphasis in cost accounting is on cost control and cost

determination. Whereas the management accounting uses the principles

and practices of financial accounting and costing accounting in addition to

other managerial techniques for effective management. The examples of

these techniques are standard costing, budgetary control, uniform costing

and inter-firm costing, marginal costing, flow analysis, ratio analysis etc.,

Cost Accounting

Joseph Anbarasu

Therefore, the management accounting is an all inclusive package. It is an

application of managerial aspect of cost accounting.

6. List the advantages of cost accounting.

An effective and organised system of costing may have the following

advantages:

a. Providing information to the insiders and outsiders with respect to

production, cost, materials, labour, stores, plant capacity etc.,

which assist out planning

b. Revealing profitable and unprofitable activities which help the

management to reduce or eliminate wasteages and inefficiencies

such as under utilization, idle time, spoilage of material etc.,

c. Systematic management of cost which will lead to effective product

pricing.

d. Maintaining perpetual inventory system, this ensures preparation of

interim profit and loss account.

e. Aiding in formulation of policies related to product, price etc.,

f. Comparison of cost between different periods, products,

departments or firms.

g. Revealing idle capacity, this would help the management to deal

bottlenecks.

h. Ascertainment of cost and profit more frequently and examination

of their causes in details.

i. Taking decisions based on facts and formulation of suitable polices

for various matters. (Level of output, make or buy decision,

replacement of old equipment, shut down or continue, introduction

of new products or elimination, acceptance of a special order and

replacement of labour with machinery.)

The use of cost accounting is no more restricted to manufacturing

organisations. It is used by other organisatios too banks, educational

institutions, hospitals, local governments so on.

7. Define the term cost.

The terms ‘Cost’ and ‘expenditure’ are used interchangeably to mention

same thing in the field of business. Cost means the amount of expenditure

incurred on, or attributable to, a given thing.

According to the committee on Cost Concepts and

Standards of the American Accounting Association, “Cost is

foregoing, measured in monetary terms, incurred or

potential to be incurred to achieve a specific objective”

It may be an actual cost or estimated expenditure. It also indicates a direct

or indirect expenditure. It is also related to job, process, product or service.

Examples of costs are material, labour, factory overhead, administrative

overheads, and selling and distribution overheads.

8. What are ascertainment costs? How does it differ from cost estimation?

Cost Ascertainment:

Cost ascertainment is related to computation of actual costs incurred. It

means the methods and process employed in ascertaining costs. Different

methods are employed for ascertaining cost in different organisations. Job

Cost Accounting

Therefore, the management accounting is an all inclusive package. It is an

application of managerial aspect of cost accounting.

6. List the advantages of cost accounting.

An effective and organised system of costing may have the following

advantages:

a. Providing information to the insiders and outsiders with respect to

production, cost, materials, labour, stores, plant capacity etc.,

which assist out planning

b. Revealing profitable and unprofitable activities which help the

management to reduce or eliminate wasteages and inefficiencies

such as under utilization, idle time, spoilage of material etc.,

c. Systematic management of cost which will lead to effective product

pricing.

d. Maintaining perpetual inventory system, this ensures preparation of

interim profit and loss account.

e. Aiding in formulation of policies related to product, price etc.,

f. Comparison of cost between different periods, products,

departments or firms.

g. Revealing idle capacity, this would help the management to deal

bottlenecks.

h. Ascertainment of cost and profit more frequently and examination

of their causes in details.

i. Taking decisions based on facts and formulation of suitable polices

for various matters. (Level of output, make or buy decision,

replacement of old equipment, shut down or continue, introduction

of new products or elimination, acceptance of a special order and

replacement of labour with machinery.)

The use of cost accounting is no more restricted to manufacturing

organisations. It is used by other organisatios too banks, educational

institutions, hospitals, local governments so on.

7. Define the term cost.

The terms ‘Cost’ and ‘expenditure’ are used interchangeably to mention

same thing in the field of business. Cost means the amount of expenditure

incurred on, or attributable to, a given thing.

According to the committee on Cost Concepts and

Standards of the American Accounting Association, “Cost is

foregoing, measured in monetary terms, incurred or

potential to be incurred to achieve a specific objective”

It may be an actual cost or estimated expenditure. It also indicates a direct

or indirect expenditure. It is also related to job, process, product or service.

Examples of costs are material, labour, factory overhead, administrative

overheads, and selling and distribution overheads.

8. What are ascertainment costs? How does it differ from cost estimation?

Cost Ascertainment:

Cost ascertainment is related to computation of actual costs incurred. It

means the methods and process employed in ascertaining costs. Different

methods are employed for ascertaining cost in different organisations. Job

Cost Accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Joseph Anbarasu

costing, contract costing, batch costing, process costing, unit costing and

multiple costing are some methods. (Refer the method of costing). Each

method is chosen according to its suitability with the organisation

concerned.

The ascertainment of actual cost has a small impact because of the

following possible reasons:

a. Actual cost cannot be used for the purpose of price quotations and

filing tenders.

b. Actual cost has practically no utility for control purposes.

c. Actual cost is ineffective as means of measuring performance

efficiency.

Ascertainment of actual costs proves to be important though there are

limitations as shown above. Ascertainment of actual costs tells us

unprofitable activities and losses and inefficiencies occurring in the form

idle time, excessive scrap etc.,

Uses of Cost Estimation:

Cost estimation is the process of predetermined costs of products or

services. The costs are prepared in advance of production and precede the

operations. Estimated costs are definitely the future costs. They are based

on the average of the past actual costs adjusted for anticipated changes in

future. The following are the uses of cost estimation:

i. Cost estimates are used in making price quotations and

bidding for contracts

ii. they are used in the preparations of budgets

iii. it helps in evaluating performance

iv. Projected financial statements are prepared with the help of

such estimations

v. It serves as targets in contoling costs

9. What is cost centre? How is it identified? List its uses.

Cost is generally ascertained by cost centres. Let us understand about cost

centre.

A cost centre is a location, person or item of equipment (or

group of these) for which costs may be ascertained and

used for the purposes of cost control. (I.C.M.A. London)

The entire organisation may be divided into specified cost centres, which

jointly contribute to the total cost. A cost centre is primarily identified in

two major ways. They are

a. Personal cost centre: It consists of a person or a group of persons.

b. Impersonal cost centre: It consists of a location or an item of

equipment or group of these.

Identification and establishments of cost centres depend on the nature and

type of industry. Cost centres may be of the following types.

i. Process cost centre (based on sequence of operation)

ii. Production cost centre(for regular production in a shop)

iii. Operation cost centre(where various operations are involved

in the production process)

iv. Service cost centre(for activities supporting the main

production)

Identification and establishment of cost centres help us in

i) ascertaining the centre-wise costs,

ii) comparing the centre-wise costs periodically,

Cost Accounting

costing, contract costing, batch costing, process costing, unit costing and

multiple costing are some methods. (Refer the method of costing). Each

method is chosen according to its suitability with the organisation

concerned.

The ascertainment of actual cost has a small impact because of the

following possible reasons:

a. Actual cost cannot be used for the purpose of price quotations and

filing tenders.

b. Actual cost has practically no utility for control purposes.

c. Actual cost is ineffective as means of measuring performance

efficiency.

Ascertainment of actual costs proves to be important though there are

limitations as shown above. Ascertainment of actual costs tells us

unprofitable activities and losses and inefficiencies occurring in the form

idle time, excessive scrap etc.,

Uses of Cost Estimation:

Cost estimation is the process of predetermined costs of products or

services. The costs are prepared in advance of production and precede the

operations. Estimated costs are definitely the future costs. They are based

on the average of the past actual costs adjusted for anticipated changes in

future. The following are the uses of cost estimation:

i. Cost estimates are used in making price quotations and

bidding for contracts

ii. they are used in the preparations of budgets

iii. it helps in evaluating performance

iv. Projected financial statements are prepared with the help of

such estimations

v. It serves as targets in contoling costs

9. What is cost centre? How is it identified? List its uses.

Cost is generally ascertained by cost centres. Let us understand about cost

centre.

A cost centre is a location, person or item of equipment (or

group of these) for which costs may be ascertained and

used for the purposes of cost control. (I.C.M.A. London)

The entire organisation may be divided into specified cost centres, which

jointly contribute to the total cost. A cost centre is primarily identified in

two major ways. They are

a. Personal cost centre: It consists of a person or a group of persons.

b. Impersonal cost centre: It consists of a location or an item of

equipment or group of these.

Identification and establishments of cost centres depend on the nature and

type of industry. Cost centres may be of the following types.

i. Process cost centre (based on sequence of operation)

ii. Production cost centre(for regular production in a shop)

iii. Operation cost centre(where various operations are involved

in the production process)

iv. Service cost centre(for activities supporting the main

production)

Identification and establishment of cost centres help us in

i) ascertaining the centre-wise costs,

ii) comparing the centre-wise costs periodically,

Cost Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Joseph Anbarasu

iii) finding out the major trends of variance,

iv) applying the techniques of control to check undue,

undesirable or unexpected movements in costs.

The concept of costing by cost centres may be applied to almost any

industry. The number of cost centres and the size of each vary from one

undertaking to another. The main purpose of identification of cost centres

is to fix responsibilities for every cost centres. A large number of cost

centres tend to be expensive but having too few cost centres defeat the

very purpose of control.

10. Describe about cost unit.

The cost centres help in ascertaining the costs by location, equipment or

person. Cost unit is an extension of identification of cost centres. Cost unit

helps in breaking up the cost into smaller sub-divisions. It also facilitates in

ascertaining the cost of saleable product or services.

According to I.C.M.A. London

A cost unit is a unit of product, service or time in relation to

which cost may be ascertained or expressed

Cost units are the ‘things’ that the business is setup to provide of which

cost is ascertained. Cost units will normally be the quantity of a product for

which price is quoted to the customers.

Cost units may be:

i. unit of product (e.g., cost per book)

ii. unit of time (e.g., cost of generating electricity per hour)

iii. unit of weight (e.g., cost per kilogram of sugar)

iv. unit of measurement (e.g., cost per square foot of

construction)

v. operating unit of service (e.g., cost of running a car per

kilometre)

Selection of a cost unit must be appropriate. Convenience is the first

criterion. Secondly, it should be easier to correlate expenses with cost

units. Thirdly, it should be according to the nature and practice of the

business.

A few more examples of cost units in various industries are given:

Industry Cost Unit

Cars Per Car

Cement Tonne

Chemicals Tonne, kilogram, litre, gallon

etc

Bricks 1,000 bricks

Shoes Pair or dozen pairs

Pencils Dozen or gross

Electricity Kilowatt hour

Transport Passenger Kilometre

Automobile Number

Printing

Press

Thousand copies

Cotton Bale

Timber Cubic foot

Mines Tonne

Cost Accounting

iii) finding out the major trends of variance,

iv) applying the techniques of control to check undue,

undesirable or unexpected movements in costs.

The concept of costing by cost centres may be applied to almost any

industry. The number of cost centres and the size of each vary from one

undertaking to another. The main purpose of identification of cost centres

is to fix responsibilities for every cost centres. A large number of cost

centres tend to be expensive but having too few cost centres defeat the

very purpose of control.

10. Describe about cost unit.

The cost centres help in ascertaining the costs by location, equipment or

person. Cost unit is an extension of identification of cost centres. Cost unit

helps in breaking up the cost into smaller sub-divisions. It also facilitates in

ascertaining the cost of saleable product or services.

According to I.C.M.A. London

A cost unit is a unit of product, service or time in relation to

which cost may be ascertained or expressed

Cost units are the ‘things’ that the business is setup to provide of which

cost is ascertained. Cost units will normally be the quantity of a product for

which price is quoted to the customers.

Cost units may be:

i. unit of product (e.g., cost per book)

ii. unit of time (e.g., cost of generating electricity per hour)

iii. unit of weight (e.g., cost per kilogram of sugar)

iv. unit of measurement (e.g., cost per square foot of

construction)

v. operating unit of service (e.g., cost of running a car per

kilometre)

Selection of a cost unit must be appropriate. Convenience is the first

criterion. Secondly, it should be easier to correlate expenses with cost

units. Thirdly, it should be according to the nature and practice of the

business.

A few more examples of cost units in various industries are given:

Industry Cost Unit

Cars Per Car

Cement Tonne

Chemicals Tonne, kilogram, litre, gallon

etc

Bricks 1,000 bricks

Shoes Pair or dozen pairs

Pencils Dozen or gross

Electricity Kilowatt hour

Transport Passenger Kilometre

Automobile Number

Printing

Press

Thousand copies

Cotton Bale

Timber Cubic foot

Mines Tonne

Cost Accounting

Joseph Anbarasu

Carpets Square yard

Hotel Room per day

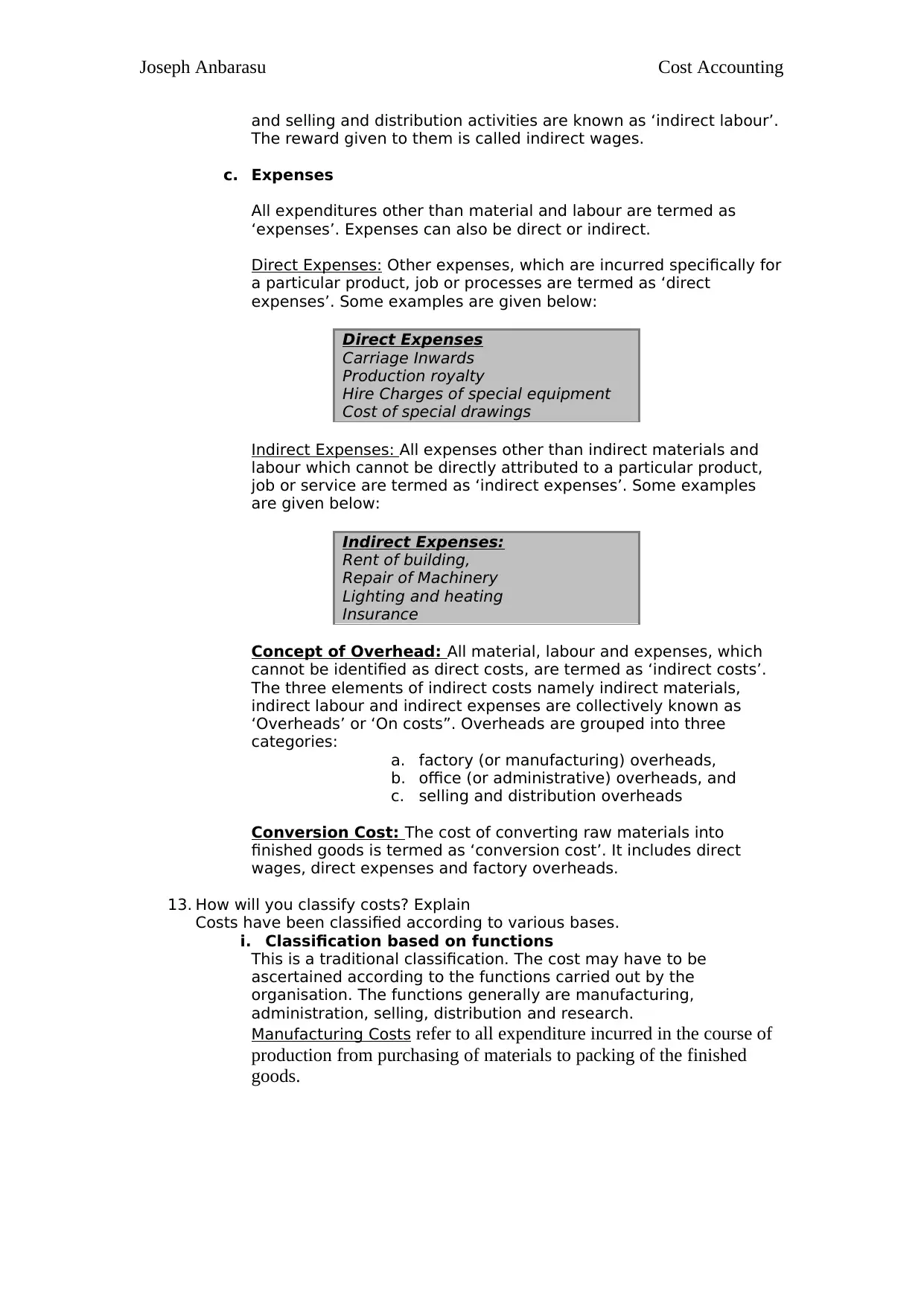

11. Explain the components of total cost?

The total cost comprises of direct costs (also known as prime cost) and

indirect costs (known as overheads). The prime cost consists of direct

materials, direct labour and other direct expenses. Overhead consists of

factory overheads, office overheads, and selling and distribution

overheads.

Mechanism of Cost Build Up

Prime Cost

=

Direct Material

+

Direct Labour

+

Direct

Expenses

Works Cost

=

Prime Cost

+

Factory Overhead

Cost of Production

=

Works Cost

+

Office And Administrative

Overhead

Total Cost

=

Cost of Production

+

Selling And Distribution

Overhead

12. What are the various elements of cost?

There are three elements of Cost

a. Materials:

The word “Materials” refers to those commodities, which are used

as raw materials, components, or consumables for manufacturing

product. Materials can be direct or indirect.

Direct materials: All materials used as raw-materials or components

for a finished product are known as ‘direct materials’. Cotton for

textiles, tyres for car are few examples of direct material. It also

includes package material.

Indirect Materials: Consumable like lubricating oil, spare parts for

machinery are called as indirect materials. Such commodities do

not form part of the finished product.

b. Labour and

The workers are involved in converting raw material into finished

goods. Such involvement of workers forms the word ‘labour’. The

reward given to them for their involvement is called ‘wages’. Wages

can be direct or indirect.

Direct Labour: The workers who are directly involved in the

production of goods are known as ‘direct labour’. The reward paid

to them is called direct wages.

Indirect Labour: The workers employed for carrying out tasks

incidental to production of goods or those engaged for office work

Cost Accounting

Carpets Square yard

Hotel Room per day

11. Explain the components of total cost?

The total cost comprises of direct costs (also known as prime cost) and

indirect costs (known as overheads). The prime cost consists of direct

materials, direct labour and other direct expenses. Overhead consists of

factory overheads, office overheads, and selling and distribution

overheads.

Mechanism of Cost Build Up

Prime Cost

=

Direct Material

+

Direct Labour

+

Direct

Expenses

Works Cost

=

Prime Cost

+

Factory Overhead

Cost of Production

=

Works Cost

+

Office And Administrative

Overhead

Total Cost

=

Cost of Production

+

Selling And Distribution

Overhead

12. What are the various elements of cost?

There are three elements of Cost

a. Materials:

The word “Materials” refers to those commodities, which are used

as raw materials, components, or consumables for manufacturing

product. Materials can be direct or indirect.

Direct materials: All materials used as raw-materials or components

for a finished product are known as ‘direct materials’. Cotton for

textiles, tyres for car are few examples of direct material. It also

includes package material.

Indirect Materials: Consumable like lubricating oil, spare parts for

machinery are called as indirect materials. Such commodities do

not form part of the finished product.

b. Labour and

The workers are involved in converting raw material into finished

goods. Such involvement of workers forms the word ‘labour’. The

reward given to them for their involvement is called ‘wages’. Wages

can be direct or indirect.

Direct Labour: The workers who are directly involved in the

production of goods are known as ‘direct labour’. The reward paid

to them is called direct wages.

Indirect Labour: The workers employed for carrying out tasks

incidental to production of goods or those engaged for office work

Cost Accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Joseph Anbarasu

and selling and distribution activities are known as ‘indirect labour’.

The reward given to them is called indirect wages.

c. Expenses

All expenditures other than material and labour are termed as

‘expenses’. Expenses can also be direct or indirect.

Direct Expenses: Other expenses, which are incurred specifically for

a particular product, job or processes are termed as ‘direct

expenses’. Some examples are given below:

Direct Expenses

Carriage Inwards

Production royalty

Hire Charges of special equipment

Cost of special drawings

Indirect Expenses: All expenses other than indirect materials and

labour which cannot be directly attributed to a particular product,

job or service are termed as ‘indirect expenses’. Some examples

are given below:

Indirect Expenses:

Rent of building,

Repair of Machinery

Lighting and heating

Insurance

Concept of Overhead: All material, labour and expenses, which

cannot be identified as direct costs, are termed as ‘indirect costs’.

The three elements of indirect costs namely indirect materials,

indirect labour and indirect expenses are collectively known as

‘Overheads’ or ‘On costs”. Overheads are grouped into three

categories:

a. factory (or manufacturing) overheads,

b. office (or administrative) overheads, and

c. selling and distribution overheads

Conversion Cost: The cost of converting raw materials into

finished goods is termed as ‘conversion cost’. It includes direct

wages, direct expenses and factory overheads.

13. How will you classify costs? Explain

Costs have been classified according to various bases.

i. Classification based on functions

This is a traditional classification. The cost may have to be

ascertained according to the functions carried out by the

organisation. The functions generally are manufacturing,

administration, selling, distribution and research.

Manufacturing Costs refer to all expenditure incurred in the course of

production from purchasing of materials to packing of the finished

goods.

Cost Accounting

and selling and distribution activities are known as ‘indirect labour’.

The reward given to them is called indirect wages.

c. Expenses

All expenditures other than material and labour are termed as

‘expenses’. Expenses can also be direct or indirect.

Direct Expenses: Other expenses, which are incurred specifically for

a particular product, job or processes are termed as ‘direct

expenses’. Some examples are given below:

Direct Expenses

Carriage Inwards

Production royalty

Hire Charges of special equipment

Cost of special drawings

Indirect Expenses: All expenses other than indirect materials and

labour which cannot be directly attributed to a particular product,

job or service are termed as ‘indirect expenses’. Some examples

are given below:

Indirect Expenses:

Rent of building,

Repair of Machinery

Lighting and heating

Insurance

Concept of Overhead: All material, labour and expenses, which

cannot be identified as direct costs, are termed as ‘indirect costs’.

The three elements of indirect costs namely indirect materials,

indirect labour and indirect expenses are collectively known as

‘Overheads’ or ‘On costs”. Overheads are grouped into three

categories:

a. factory (or manufacturing) overheads,

b. office (or administrative) overheads, and

c. selling and distribution overheads

Conversion Cost: The cost of converting raw materials into

finished goods is termed as ‘conversion cost’. It includes direct

wages, direct expenses and factory overheads.

13. How will you classify costs? Explain

Costs have been classified according to various bases.

i. Classification based on functions

This is a traditional classification. The cost may have to be

ascertained according to the functions carried out by the

organisation. The functions generally are manufacturing,

administration, selling, distribution and research.

Manufacturing Costs refer to all expenditure incurred in the course of

production from purchasing of materials to packing of the finished

goods.

Cost Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Joseph Anbarasu

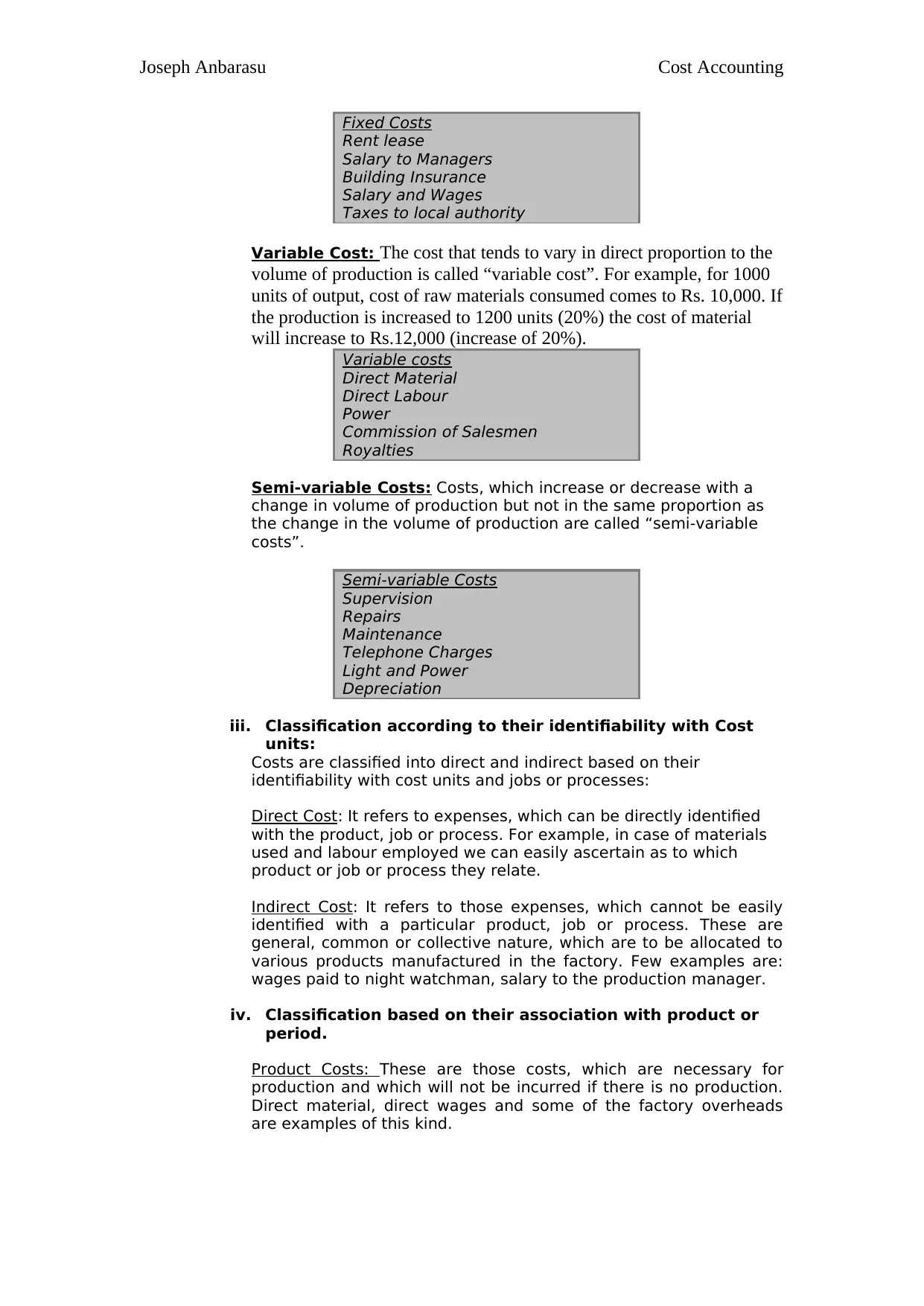

Manufacturing Costs

Material

Labour

Factory Rent

Depreciation

Power & Lighting

Insurance

Store Keeping

Administration Costs are incurred for general administration of the

organisation and for the operational control.

Administration Costs

Accounts office expenses

Legal charges

Audit charges

Office Rent

Remuneration to Director

Postage Expenses

Selling Costs are incurred to create and stimulate the demand and

to secure the demand

Selling Costs

Salaries

Commission to Salesmen

Advertising and promotion Expenses

Samples

Travelling Expenses

Distribution Costs are incurred on dispatch of the finished goods to

customer including transportation.

Distribution Costs

Packaging costs

Warehousing Costs

Carriage outwards

Insurance

Upkeep of Vans

ii. Classification based on Variability or behaviour

Costs have a definite relationship with the volume of production.

They behave differently when volume of production rises or falls.

On this basis, costs are classified into fixed cost, variable costs and

semi-variable (semi-fixed) costs.

Fixed Cost: Costs, which remain unaffected by changes in volume

of production, are called as “fixed Costs”. For example, the rent and

manager’s salary will not change when you increase the units of

production from 1000 to 1200.

Cost Accounting

Manufacturing Costs

Material

Labour

Factory Rent

Depreciation

Power & Lighting

Insurance

Store Keeping

Administration Costs are incurred for general administration of the

organisation and for the operational control.

Administration Costs

Accounts office expenses

Legal charges

Audit charges

Office Rent

Remuneration to Director

Postage Expenses

Selling Costs are incurred to create and stimulate the demand and

to secure the demand

Selling Costs

Salaries

Commission to Salesmen

Advertising and promotion Expenses

Samples

Travelling Expenses

Distribution Costs are incurred on dispatch of the finished goods to

customer including transportation.

Distribution Costs

Packaging costs

Warehousing Costs

Carriage outwards

Insurance

Upkeep of Vans

ii. Classification based on Variability or behaviour

Costs have a definite relationship with the volume of production.

They behave differently when volume of production rises or falls.

On this basis, costs are classified into fixed cost, variable costs and

semi-variable (semi-fixed) costs.

Fixed Cost: Costs, which remain unaffected by changes in volume

of production, are called as “fixed Costs”. For example, the rent and

manager’s salary will not change when you increase the units of

production from 1000 to 1200.

Cost Accounting

Joseph Anbarasu

Fixed Costs

Rent lease

Salary to Managers

Building Insurance

Salary and Wages

Taxes to local authority

Variable Cost: The cost that tends to vary in direct proportion to the

volume of production is called “variable cost”. For example, for 1000

units of output, cost of raw materials consumed comes to Rs. 10,000. If

the production is increased to 1200 units (20%) the cost of material

will increase to Rs.12,000 (increase of 20%).

Variable costs

Direct Material

Direct Labour

Power

Commission of Salesmen

Royalties

Semi-variable Costs: Costs, which increase or decrease with a

change in volume of production but not in the same proportion as

the change in the volume of production are called “semi-variable

costs”.

Semi-variable Costs

Supervision

Repairs

Maintenance

Telephone Charges

Light and Power

Depreciation

iii. Classification according to their identifiability with Cost

units:

Costs are classified into direct and indirect based on their

identifiability with cost units and jobs or processes:

Direct Cost: It refers to expenses, which can be directly identified

with the product, job or process. For example, in case of materials

used and labour employed we can easily ascertain as to which

product or job or process they relate.

Indirect Cost: It refers to those expenses, which cannot be easily

identified with a particular product, job or process. These are

general, common or collective nature, which are to be allocated to

various products manufactured in the factory. Few examples are:

wages paid to night watchman, salary to the production manager.

iv. Classification based on their association with product or

period.

Product Costs: These are those costs, which are necessary for

production and which will not be incurred if there is no production.

Direct material, direct wages and some of the factory overheads

are examples of this kind.

Cost Accounting

Fixed Costs

Rent lease

Salary to Managers

Building Insurance

Salary and Wages

Taxes to local authority

Variable Cost: The cost that tends to vary in direct proportion to the

volume of production is called “variable cost”. For example, for 1000

units of output, cost of raw materials consumed comes to Rs. 10,000. If

the production is increased to 1200 units (20%) the cost of material

will increase to Rs.12,000 (increase of 20%).

Variable costs

Direct Material

Direct Labour

Power

Commission of Salesmen

Royalties

Semi-variable Costs: Costs, which increase or decrease with a

change in volume of production but not in the same proportion as

the change in the volume of production are called “semi-variable

costs”.

Semi-variable Costs

Supervision

Repairs

Maintenance

Telephone Charges

Light and Power

Depreciation

iii. Classification according to their identifiability with Cost

units:

Costs are classified into direct and indirect based on their

identifiability with cost units and jobs or processes:

Direct Cost: It refers to expenses, which can be directly identified

with the product, job or process. For example, in case of materials

used and labour employed we can easily ascertain as to which

product or job or process they relate.

Indirect Cost: It refers to those expenses, which cannot be easily

identified with a particular product, job or process. These are

general, common or collective nature, which are to be allocated to

various products manufactured in the factory. Few examples are:

wages paid to night watchman, salary to the production manager.

iv. Classification based on their association with product or

period.

Product Costs: These are those costs, which are necessary for

production and which will not be incurred if there is no production.

Direct material, direct wages and some of the factory overheads

are examples of this kind.

Cost Accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.