Comprehensive Cost Management, Budgeting, and Variance Analysis

VerifiedAdded on 2022/02/28

|21

|5338

|123

Report

AI Summary

This report delves into the critical aspects of cost management, essential for organizational decision-making and profit maximization. It begins with a thorough classification of costs, distinguishing between direct and indirect costs, and explores various costing methods such as job order, process, batch, contract, and service costing, including hybrid approaches. The report then delves into the calculation of costs using FIFO, LIFO, and weighted average methods. A significant portion is dedicated to preparing and analyzing cost reports, identifying variances, and commenting on performance, including the use of performance indicators. Furthermore, the report examines the purpose and nature of budgeting, appropriate budgeting methods like incremental and zero-based budgeting, and the preparation of production, purchase, and cash budgets. It concludes with variance calculations, identifying potential causes for variances, and recommendations for corrective actions, along with a reconciliation of budgeted and actual results, culminating in reports to management.

Contents

INTRODUCTION:......................................................................................................................................2

1.1 Classification of Costs:..........................................................................................................................3

1.2 Costing Methods:...................................................................................................................................4

1.2.1 Job Order Costing:..........................................................................................................................4

1.2.2 Process Costing:..............................................................................................................................5

1.2.3 Batch Costing:...............................................................................................................................5

1.2.4 Contract costing:.............................................................................................................................6

1.2.5 Service costing:...............................................................................................................................6

1.2.6 Hybrid or Mixed Methods:..............................................................................................................6

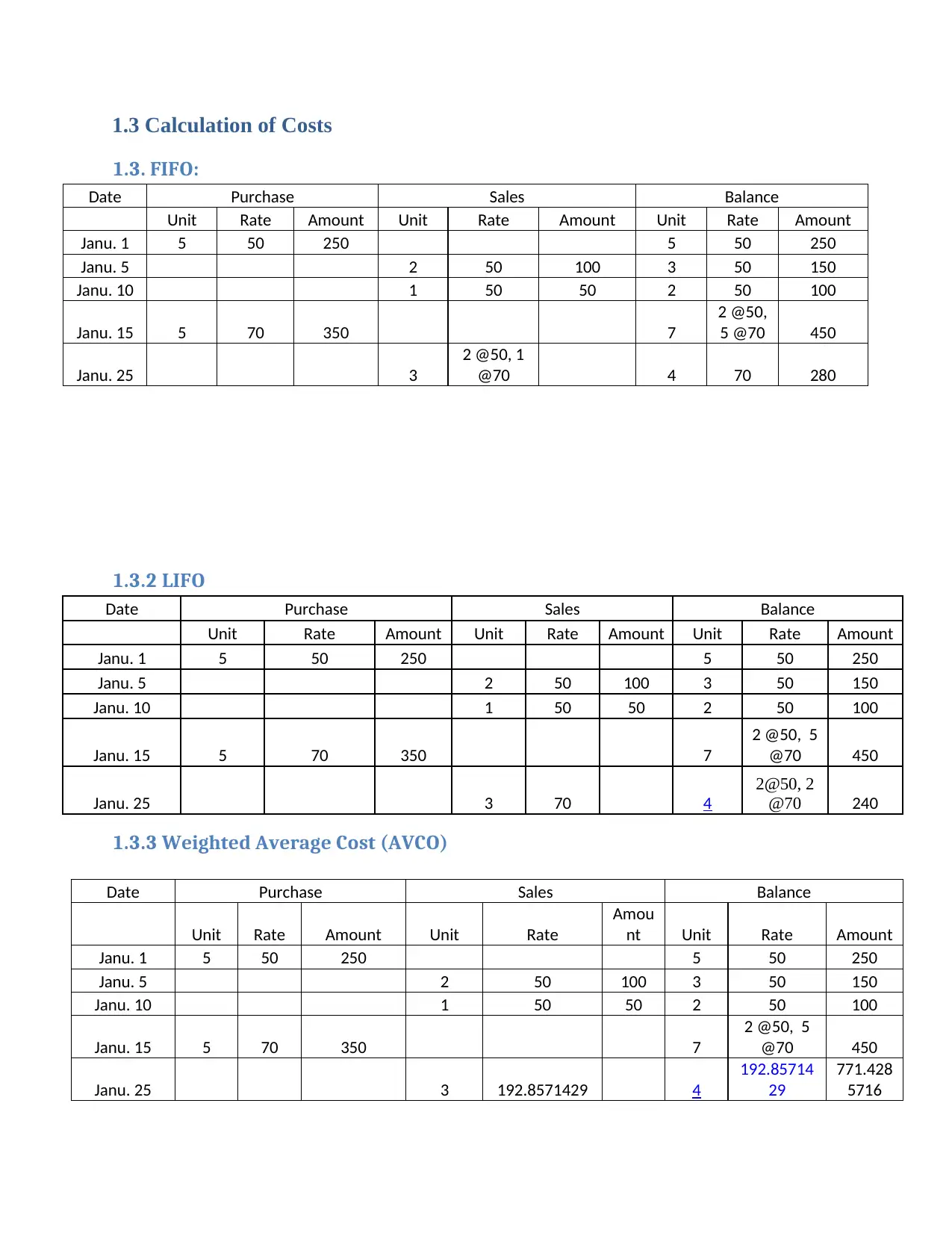

1.3 Calculation of Costs..............................................................................................................................7

1.3. FIFO:.................................................................................................................................................7

1.3.2 LIFO.................................................................................................................................................7

1.3.3 Weighted Average Cost (AVCO)......................................................................................................7

Analysis of Cost Data Using Appropriate Method....................................................................................8

2.1 Preparation and Analysis of Cost Report.............................................................................................8

Comments on Performance:....................................................................................................................9

2.2 Use of Performance Indicators:.............................................................................................................9

2.3 Suggest improvements to reduce costs, enhance value and quality:..................................................10

3.1 Purpose and Nature of Budgeting Process:..........................................................................................11

3.1.1 Purposes of Budgeting:.................................................................................................................11

3.1.2: Nature of the Budgeting Process:................................................................................................11

3.2: Appropriate Budgeting Methods and Their needs in the Organization:.............................................11

3.2.1 Incremental Budgeting:................................................................................................................12

3.2.2 Zero Based Budgets:.....................................................................................................................12

3.2.3 Top- down Budgeting:..................................................................................................................12

3.2.4 Bottom-up Budgeting:..................................................................................................................12

3.3 PREPERATION OF BUDGET.........................................................................................................12

3.3.1 Preparation of Production Budget:................................................................................................12

3.3.2 Preparation of Purchase Budget:..................................................................................................13

INTRODUCTION:......................................................................................................................................2

1.1 Classification of Costs:..........................................................................................................................3

1.2 Costing Methods:...................................................................................................................................4

1.2.1 Job Order Costing:..........................................................................................................................4

1.2.2 Process Costing:..............................................................................................................................5

1.2.3 Batch Costing:...............................................................................................................................5

1.2.4 Contract costing:.............................................................................................................................6

1.2.5 Service costing:...............................................................................................................................6

1.2.6 Hybrid or Mixed Methods:..............................................................................................................6

1.3 Calculation of Costs..............................................................................................................................7

1.3. FIFO:.................................................................................................................................................7

1.3.2 LIFO.................................................................................................................................................7

1.3.3 Weighted Average Cost (AVCO)......................................................................................................7

Analysis of Cost Data Using Appropriate Method....................................................................................8

2.1 Preparation and Analysis of Cost Report.............................................................................................8

Comments on Performance:....................................................................................................................9

2.2 Use of Performance Indicators:.............................................................................................................9

2.3 Suggest improvements to reduce costs, enhance value and quality:..................................................10

3.1 Purpose and Nature of Budgeting Process:..........................................................................................11

3.1.1 Purposes of Budgeting:.................................................................................................................11

3.1.2: Nature of the Budgeting Process:................................................................................................11

3.2: Appropriate Budgeting Methods and Their needs in the Organization:.............................................11

3.2.1 Incremental Budgeting:................................................................................................................12

3.2.2 Zero Based Budgets:.....................................................................................................................12

3.2.3 Top- down Budgeting:..................................................................................................................12

3.2.4 Bottom-up Budgeting:..................................................................................................................12

3.3 PREPERATION OF BUDGET.........................................................................................................12

3.3.1 Preparation of Production Budget:................................................................................................12

3.3.2 Preparation of Purchase Budget:..................................................................................................13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.3.3 Preparation of Cash Budget:.........................................................................................................13

Variance Calculation, Possible Causes and Recommendation of Corrective:............................................15

4.1 Calculation of Variance and Possible Causes......................................................................................15

4.2 Causes and Corrective Actions:...........................................................................................................17

4.3 Reconciliation of Budget and Actual Result:.......................................................................................17

4.4 Reports to Management about the Findings:........................................................................................18

CONCLUSION:............................................................................................................................................18

INTRODUCTION:

Cost management is a very important part of management for decision making in any

organization that are reduction or manufacturing based. Identification of cost, allocation of cost,

analyzing cost and controlling cost are most important aspects of cost management. Without

proper cost management, an organization cannot survive for long to achieve its goals and

Variance Calculation, Possible Causes and Recommendation of Corrective:............................................15

4.1 Calculation of Variance and Possible Causes......................................................................................15

4.2 Causes and Corrective Actions:...........................................................................................................17

4.3 Reconciliation of Budget and Actual Result:.......................................................................................17

4.4 Reports to Management about the Findings:........................................................................................18

CONCLUSION:............................................................................................................................................18

INTRODUCTION:

Cost management is a very important part of management for decision making in any

organization that are reduction or manufacturing based. Identification of cost, allocation of cost,

analyzing cost and controlling cost are most important aspects of cost management. Without

proper cost management, an organization cannot survive for long to achieve its goals and

maximization of profit. On the other hand, for proper cost management knowing the nature and

behavior of different costs is vital.AS cost is directly related to the financial bottom line target

achievement of an organization, it indispensable for management to minimize cost by proper

allocation and controlling of cost. Preparation of budget, maintaining proper records of actual

outcome achieved, comparing the actual outcome with the targeted one( calculation of variance)

are some major tools of controlling cost and optimization of benefit.

Task 1:

1.1 Classification of Costs:

The following table contains the classification of the costs mentioned in the requirement 1.1.

Before detailed classification it is pertinent to mention that direct cost or indirect cost of

producing a goods or performing a service are determined based on whether those costs are

inextricable or directly influential on the quality and quantity of the goods or services.

S.L

No.

Name of the Cost Description of the Cost Classification of

the Cost

1. Wage of the Electrician Wage of electrician is directly

related to the ob and completion of

the job is highly dependent on the

performance of the electrician.

That is why, it is the direct labor

cost of the job.

Direct Cost

2. Depreciation of the tools used

by ht electricians

Depreciation of the tools used by

the electrician are incurred

whenever it is used for the job

purpose It is directly related to the

performance of the job.

Direct Cost

3. Salary of the Sparky Ltd’s

Accountant

Sparky has to give salary to its

accountants on the basis of the

terms of the employment. Whether

any job is performed or not( in the

short run), the salary of the

accountants shall have to be paid.

Salary of the accountants doesn’t

affect the performance of any job.

Rather it is an administrative cost.

Indirect cost.

4. Cost of cable and other

material used on the job

Cost of cable and other materials

used on the job are in inextricable

part of the performance of an

Direct cost

behavior of different costs is vital.AS cost is directly related to the financial bottom line target

achievement of an organization, it indispensable for management to minimize cost by proper

allocation and controlling of cost. Preparation of budget, maintaining proper records of actual

outcome achieved, comparing the actual outcome with the targeted one( calculation of variance)

are some major tools of controlling cost and optimization of benefit.

Task 1:

1.1 Classification of Costs:

The following table contains the classification of the costs mentioned in the requirement 1.1.

Before detailed classification it is pertinent to mention that direct cost or indirect cost of

producing a goods or performing a service are determined based on whether those costs are

inextricable or directly influential on the quality and quantity of the goods or services.

S.L

No.

Name of the Cost Description of the Cost Classification of

the Cost

1. Wage of the Electrician Wage of electrician is directly

related to the ob and completion of

the job is highly dependent on the

performance of the electrician.

That is why, it is the direct labor

cost of the job.

Direct Cost

2. Depreciation of the tools used

by ht electricians

Depreciation of the tools used by

the electrician are incurred

whenever it is used for the job

purpose It is directly related to the

performance of the job.

Direct Cost

3. Salary of the Sparky Ltd’s

Accountant

Sparky has to give salary to its

accountants on the basis of the

terms of the employment. Whether

any job is performed or not( in the

short run), the salary of the

accountants shall have to be paid.

Salary of the accountants doesn’t

affect the performance of any job.

Rather it is an administrative cost.

Indirect cost.

4. Cost of cable and other

material used on the job

Cost of cable and other materials

used on the job are in inextricable

part of the performance of an

Direct cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

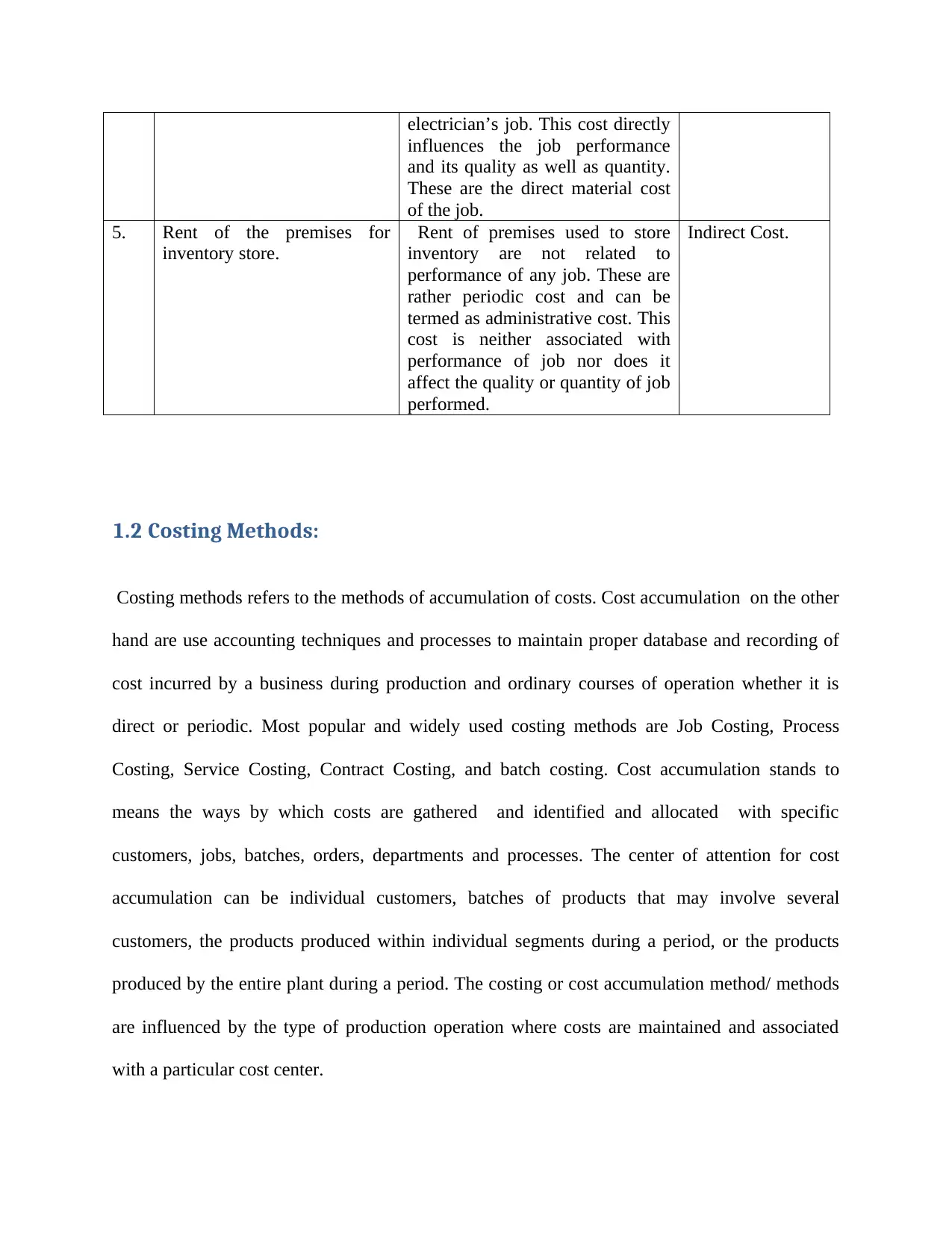

electrician’s job. This cost directly

influences the job performance

and its quality as well as quantity.

These are the direct material cost

of the job.

5. Rent of the premises for

inventory store.

Rent of premises used to store

inventory are not related to

performance of any job. These are

rather periodic cost and can be

termed as administrative cost. This

cost is neither associated with

performance of job nor does it

affect the quality or quantity of job

performed.

Indirect Cost.

1.2 Costing Methods:

Costing methods refers to the methods of accumulation of costs. Cost accumulation on the other

hand are use accounting techniques and processes to maintain proper database and recording of

cost incurred by a business during production and ordinary courses of operation whether it is

direct or periodic. Most popular and widely used costing methods are Job Costing, Process

Costing, Service Costing, Contract Costing, and batch costing. Cost accumulation stands to

means the ways by which costs are gathered and identified and allocated with specific

customers, jobs, batches, orders, departments and processes. The center of attention for cost

accumulation can be individual customers, batches of products that may involve several

customers, the products produced within individual segments during a period, or the products

produced by the entire plant during a period. The costing or cost accumulation method/ methods

are influenced by the type of production operation where costs are maintained and associated

with a particular cost center.

influences the job performance

and its quality as well as quantity.

These are the direct material cost

of the job.

5. Rent of the premises for

inventory store.

Rent of premises used to store

inventory are not related to

performance of any job. These are

rather periodic cost and can be

termed as administrative cost. This

cost is neither associated with

performance of job nor does it

affect the quality or quantity of job

performed.

Indirect Cost.

1.2 Costing Methods:

Costing methods refers to the methods of accumulation of costs. Cost accumulation on the other

hand are use accounting techniques and processes to maintain proper database and recording of

cost incurred by a business during production and ordinary courses of operation whether it is

direct or periodic. Most popular and widely used costing methods are Job Costing, Process

Costing, Service Costing, Contract Costing, and batch costing. Cost accumulation stands to

means the ways by which costs are gathered and identified and allocated with specific

customers, jobs, batches, orders, departments and processes. The center of attention for cost

accumulation can be individual customers, batches of products that may involve several

customers, the products produced within individual segments during a period, or the products

produced by the entire plant during a period. The costing or cost accumulation method/ methods

are influenced by the type of production operation where costs are maintained and associated

with a particular cost center.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2.1 Job Order Costing:

In job order costing, costs are accumulated by jobs, orders, contracts, or lots. The key is that the

work is done to the customer's specifications. As a result, each job tends to be different. For

example, job order costing is used for construction projects, government contracts, shipbuilding,

automobile repair, job printing, textbooks, toys, wood furniture, office machines, caskets,

machine tools, and luggage. Accumulation of the costs of professional services (e.g., lawyers,

doctors and CPA's) also fall into this category.

1.2.2 Process Costing:

In process costing, costs are accumulated by departments, operations, or processes. The work

performed on each unit is standardized or uniform where a continuous mass production or

assembly operation is involved. For example, process costing is used by companies that produce

appliances, alcoholic beverages, tires, sugar, breakfast cereals, leather, paint, coal, textiles,

lumber, candy, coke, plastics, rubber, cigarettes, shoes, typewriters, cement, gasoline, steel, baby

foods, flour, glass, men's suits, pharmaceuticals and automobiles. Process costing is also used in

meat packing and for public utility services such as water, gas and electricity.

1.2.3 Batch Costing:

In Batch Costing products are produces in batches in large quantity. Each batch is assigned a

batch number so that the batches can be identified and traced easily for the purpose of cost

accumulation. Later on, the batch cost can be averaged by the number of product produced.

Batch cost includes both periodic and product cost or fixed and variable cost. Anytime, per unit

cost of production can be determined by dividing the total cost of a batch by the number of units

produced in that batch.

In job order costing, costs are accumulated by jobs, orders, contracts, or lots. The key is that the

work is done to the customer's specifications. As a result, each job tends to be different. For

example, job order costing is used for construction projects, government contracts, shipbuilding,

automobile repair, job printing, textbooks, toys, wood furniture, office machines, caskets,

machine tools, and luggage. Accumulation of the costs of professional services (e.g., lawyers,

doctors and CPA's) also fall into this category.

1.2.2 Process Costing:

In process costing, costs are accumulated by departments, operations, or processes. The work

performed on each unit is standardized or uniform where a continuous mass production or

assembly operation is involved. For example, process costing is used by companies that produce

appliances, alcoholic beverages, tires, sugar, breakfast cereals, leather, paint, coal, textiles,

lumber, candy, coke, plastics, rubber, cigarettes, shoes, typewriters, cement, gasoline, steel, baby

foods, flour, glass, men's suits, pharmaceuticals and automobiles. Process costing is also used in

meat packing and for public utility services such as water, gas and electricity.

1.2.3 Batch Costing:

In Batch Costing products are produces in batches in large quantity. Each batch is assigned a

batch number so that the batches can be identified and traced easily for the purpose of cost

accumulation. Later on, the batch cost can be averaged by the number of product produced.

Batch cost includes both periodic and product cost or fixed and variable cost. Anytime, per unit

cost of production can be determined by dividing the total cost of a batch by the number of units

produced in that batch.

1.2.4 Contract costing:

A contract refers to a big job usually. In contract costing methods, cost are identified and

allocated to a specific contract or a customer for whom a contract is performed. It helps the

organization to assess the potential customers especially in big jobs. For, example, a company

may bid to sale an Air Craft. There may have several customers willing to by its product. In this

case, contract costing allows the company to determine the cost of performing the contract for

the each customer and profitability analysis of each may help the company to make a proper

decision.

1.2.5 Service costing:

Service costing, from the name it can be easily traced that, is the accumulation of service cost. It

is applicable for only service providing organizations rather than business of goods. The another

name of service costing is operation costing that maintains that cost providing service for a

particular time or period or operation a particular service oriented business. Examples are

Transportation, Hotels, Mobile phone companies, etc.

1.2.6 Hybrid or Mixed Methods:

Hybrid or mixed systems are used in situations where more than one cost accumulation method

is required. For example, in some cases process costing is used for direct materials and job order

costing is used for conversion costs, (i.e., direct labor and factory overhead). In other cases, job

order costing might be used for direct materials, and process costing for conversion costs. The

different departments or operations within a company might require different cost accumulation

methods. For this reason, hybrid or mixed cost accumulation methods are sometime referred to

as operational costing methods.

A contract refers to a big job usually. In contract costing methods, cost are identified and

allocated to a specific contract or a customer for whom a contract is performed. It helps the

organization to assess the potential customers especially in big jobs. For, example, a company

may bid to sale an Air Craft. There may have several customers willing to by its product. In this

case, contract costing allows the company to determine the cost of performing the contract for

the each customer and profitability analysis of each may help the company to make a proper

decision.

1.2.5 Service costing:

Service costing, from the name it can be easily traced that, is the accumulation of service cost. It

is applicable for only service providing organizations rather than business of goods. The another

name of service costing is operation costing that maintains that cost providing service for a

particular time or period or operation a particular service oriented business. Examples are

Transportation, Hotels, Mobile phone companies, etc.

1.2.6 Hybrid or Mixed Methods:

Hybrid or mixed systems are used in situations where more than one cost accumulation method

is required. For example, in some cases process costing is used for direct materials and job order

costing is used for conversion costs, (i.e., direct labor and factory overhead). In other cases, job

order costing might be used for direct materials, and process costing for conversion costs. The

different departments or operations within a company might require different cost accumulation

methods. For this reason, hybrid or mixed cost accumulation methods are sometime referred to

as operational costing methods.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.3 Calculation of Costs

1.3. FIFO:

Date Purchase Sales Balance

Unit Rate Amount Unit Rate Amount Unit Rate Amount

Janu. 1 5 50 250 5 50 250

Janu. 5 2 50 100 3 50 150

Janu. 10 1 50 50 2 50 100

Janu. 15 5 70 350 7

2 @50,

5 @70 450

Janu. 25 3

2 @50, 1

@70 4 70 280

1.3.2 LIFO

Date Purchase Sales Balance

Unit Rate Amount Unit Rate Amount Unit Rate Amount

Janu. 1 5 50 250 5 50 250

Janu. 5 2 50 100 3 50 150

Janu. 10 1 50 50 2 50 100

Janu. 15 5 70 350 7

2 @50, 5

@70 450

Janu. 25 3 70 4

2@50, 2

@70 240

1.3.3 Weighted Average Cost (AVCO)

Date Purchase Sales Balance

Unit Rate Amount Unit Rate

Amou

nt Unit Rate Amount

Janu. 1 5 50 250 5 50 250

Janu. 5 2 50 100 3 50 150

Janu. 10 1 50 50 2 50 100

Janu. 15 5 70 350 7

2 @50, 5

@70 450

Janu. 25 3 192.8571429 4

192.85714

29

771.428

5716

1.3. FIFO:

Date Purchase Sales Balance

Unit Rate Amount Unit Rate Amount Unit Rate Amount

Janu. 1 5 50 250 5 50 250

Janu. 5 2 50 100 3 50 150

Janu. 10 1 50 50 2 50 100

Janu. 15 5 70 350 7

2 @50,

5 @70 450

Janu. 25 3

2 @50, 1

@70 4 70 280

1.3.2 LIFO

Date Purchase Sales Balance

Unit Rate Amount Unit Rate Amount Unit Rate Amount

Janu. 1 5 50 250 5 50 250

Janu. 5 2 50 100 3 50 150

Janu. 10 1 50 50 2 50 100

Janu. 15 5 70 350 7

2 @50, 5

@70 450

Janu. 25 3 70 4

2@50, 2

@70 240

1.3.3 Weighted Average Cost (AVCO)

Date Purchase Sales Balance

Unit Rate Amount Unit Rate

Amou

nt Unit Rate Amount

Janu. 1 5 50 250 5 50 250

Janu. 5 2 50 100 3 50 150

Janu. 10 1 50 50 2 50 100

Janu. 15 5 70 350 7

2 @50, 5

@70 450

Janu. 25 3 192.8571429 4

192.85714

29

771.428

5716

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis of Cost Data Using Appropriate Method

Using any of the above mentioned techniques, the company can maintain its costing records.

FIFO and Weighted Average costing method are nowadays accepted by accounting standards.

LIFO can also be used for internal purposes. The use of each of the cost flow technique has

several implication for companies cost, profitability, and taxation during a particular period that

is geared by the changes in price level of the products.

TASK 2

2.1 Preparation and Analysis of Cost Report

2.1 Preparation and Analysis of the Cost Report('000)

Particulars

Tentative/

Budgeted

amount

Out Come

Achieved/Act

ual

Varianc

e in

Numbe

r

Variance

Type

Unit 3 2.8 0.2

Unfavorab

le

Direct Material 30 28 2 favorable

Direct Labor 24 26 -2

Unfavorab

le

Factory

Overhead 18 18 0 0

Operating

Overhead 9 10.5 -1.5

Unfavorab

le

Marketing

overhead 3 2.5 0.5

Unfavorab

le

Total Cost 84 85 -1

Unfavorab

le

Comments on Performance:

From the table above, depicted variances and their comments, it is observed that total variance of

cost performance is Unfavorable. This Unfavorable to performance is achieved because among

Using any of the above mentioned techniques, the company can maintain its costing records.

FIFO and Weighted Average costing method are nowadays accepted by accounting standards.

LIFO can also be used for internal purposes. The use of each of the cost flow technique has

several implication for companies cost, profitability, and taxation during a particular period that

is geared by the changes in price level of the products.

TASK 2

2.1 Preparation and Analysis of Cost Report

2.1 Preparation and Analysis of the Cost Report('000)

Particulars

Tentative/

Budgeted

amount

Out Come

Achieved/Act

ual

Varianc

e in

Numbe

r

Variance

Type

Unit 3 2.8 0.2

Unfavorab

le

Direct Material 30 28 2 favorable

Direct Labor 24 26 -2

Unfavorab

le

Factory

Overhead 18 18 0 0

Operating

Overhead 9 10.5 -1.5

Unfavorab

le

Marketing

overhead 3 2.5 0.5

Unfavorab

le

Total Cost 84 85 -1

Unfavorab

le

Comments on Performance:

From the table above, depicted variances and their comments, it is observed that total variance of

cost performance is Unfavorable. This Unfavorable to performance is achieved because among

the five categories of cost, the company has achieved favorable variance only in direct materials;

other four cost categories have unfavorable outcomes. The company has achieved a favorable

outcome in direct material cost that means it has achieved cost efficiency in using or purchasing

it required raw materials. But, in other cost category it has negative variance due to either

inefficiency of management or unavoidable circumstances. This huge unfavorable variance may

cause a great financial loss for the company. Management should focus highly with in depth

analysis of budget and actual market to acquire a positive outcome and sustain the healthy

performance of the company.

2.2 Use of Performance Indicators:

Performance indicators are variables used to measure and assess the performance of a company.

A performance e is simply the outcome achieved. It can be expressed both in absolute value or

percentage form. Use of performance indicators helps the organization to identify the factors that

are differently affecting the performance of the organization and to control those factors to

achieve a better outcome. Performance indicator highly aids the achievement of targets and goals

along with control over and efficiency in cost and circumstances surrounding them. Some of the

major performance indicators used by business entities nowadays are given below:

a) Bottom Line:

Bottom line or net profit of company is the widely used performance indicators to

measure and assess the performance of a company. It is affected by the cost and

revenue figures of a firm directly. Operating profit, profit before tax, gross profit is

something that should be individually developed and controlled to acquire a healthy

bottom line of the organization.

b) Sales Increase:

Increase in sales is another vital performance indicator for a business. It is easy to

conclude that, the higher the sales revenue, the higher will be the profit of a business,.

But caution should be there that, mare increase in sales with considering how much it

is contributing to the margin of business may become very dangerous for an

organization to sustain. For example, a business may try to increase sales volume at a

very competitive price to retain customers at very competitive price. This may lead to

huge financial loss for the company.

c) Customer Satisfaction:

Customer satisfaction is a relatively quantitative measurement of performance and

much more important than any other factor in present very competitive business

environment for the survival of a company. A satisfied customer is a resource for a

company who himself contributes to the business by not only purchasing the product

but also promoting the product in the market.

d) Cost Reduction:

Today’s business environment is very competitive and volatile. Businesses have to

perform in a very unpredictable environment. To sustain in this competitive

environment and survive in the face of unpredictable rapidly changing environment,

cutting cost is very important. Reducing the process tie of production, delay in supply

other four cost categories have unfavorable outcomes. The company has achieved a favorable

outcome in direct material cost that means it has achieved cost efficiency in using or purchasing

it required raw materials. But, in other cost category it has negative variance due to either

inefficiency of management or unavoidable circumstances. This huge unfavorable variance may

cause a great financial loss for the company. Management should focus highly with in depth

analysis of budget and actual market to acquire a positive outcome and sustain the healthy

performance of the company.

2.2 Use of Performance Indicators:

Performance indicators are variables used to measure and assess the performance of a company.

A performance e is simply the outcome achieved. It can be expressed both in absolute value or

percentage form. Use of performance indicators helps the organization to identify the factors that

are differently affecting the performance of the organization and to control those factors to

achieve a better outcome. Performance indicator highly aids the achievement of targets and goals

along with control over and efficiency in cost and circumstances surrounding them. Some of the

major performance indicators used by business entities nowadays are given below:

a) Bottom Line:

Bottom line or net profit of company is the widely used performance indicators to

measure and assess the performance of a company. It is affected by the cost and

revenue figures of a firm directly. Operating profit, profit before tax, gross profit is

something that should be individually developed and controlled to acquire a healthy

bottom line of the organization.

b) Sales Increase:

Increase in sales is another vital performance indicator for a business. It is easy to

conclude that, the higher the sales revenue, the higher will be the profit of a business,.

But caution should be there that, mare increase in sales with considering how much it

is contributing to the margin of business may become very dangerous for an

organization to sustain. For example, a business may try to increase sales volume at a

very competitive price to retain customers at very competitive price. This may lead to

huge financial loss for the company.

c) Customer Satisfaction:

Customer satisfaction is a relatively quantitative measurement of performance and

much more important than any other factor in present very competitive business

environment for the survival of a company. A satisfied customer is a resource for a

company who himself contributes to the business by not only purchasing the product

but also promoting the product in the market.

d) Cost Reduction:

Today’s business environment is very competitive and volatile. Businesses have to

perform in a very unpredictable environment. To sustain in this competitive

environment and survive in the face of unpredictable rapidly changing environment,

cutting cost is very important. Reducing the process tie of production, delay in supply

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and procurement, increasing efficiency of the workers and employees, closer source

of raw materials with improves quality are some major ways of cost reduction.

2.3 Suggest improvements to reduce costs, enhance value and quality:

Here are the some ways the company can follow to reduce the cost, increase profit and

enhancing value of the firm:

1. Procure raw material with improved quality and from more convenient sources.

2. Ensure more variable that fixed type operating expenses.

3. Increase efficiency of operating and management people.

4. Employ more efficient workers.

5. Use of improved technology in the production process.

6. Scrutinizing cost, identifying controllable cost and minimizing those as far as

possible.

7. Identify unwanted costs and eliminate those.

8. Fasten the production and operating processes.

9. Fasten the business cycle.

10. Ensure more loyal employees and commitment to the firm who can also contribute to

the promotion of the firm.

11. Ensure more customer satisfaction and internal marketing.

TASK #3:

3.1 Purpose and Nature of Budgeting Process:

3.1.1 Purposes of Budgeting:

If we want define budget in a very simple way, it is just the estimation of probable inflows and outflow in

the form of revenue and expenses. The main purpose of budgeting is to know the tentative cost prior and

take corrective action after the actual situation is incurred. It helps the assessment of management

performance. Some important purposes of budget are as follows:

a) Identify the sources of revenue and inflows.

b) Identify the uses and outflows of resources.

c) To run the business properly with effectiveness and efficiency.

d) To

e) To identify the sources and uses that required more attention.

f) To identify those activities that are not contributing to the business to a desired level

and take corrective actions

g) To eliminate unwanted expenses.

h) To compare what is achieved with what is desired to evaluate performance.

of raw materials with improves quality are some major ways of cost reduction.

2.3 Suggest improvements to reduce costs, enhance value and quality:

Here are the some ways the company can follow to reduce the cost, increase profit and

enhancing value of the firm:

1. Procure raw material with improved quality and from more convenient sources.

2. Ensure more variable that fixed type operating expenses.

3. Increase efficiency of operating and management people.

4. Employ more efficient workers.

5. Use of improved technology in the production process.

6. Scrutinizing cost, identifying controllable cost and minimizing those as far as

possible.

7. Identify unwanted costs and eliminate those.

8. Fasten the production and operating processes.

9. Fasten the business cycle.

10. Ensure more loyal employees and commitment to the firm who can also contribute to

the promotion of the firm.

11. Ensure more customer satisfaction and internal marketing.

TASK #3:

3.1 Purpose and Nature of Budgeting Process:

3.1.1 Purposes of Budgeting:

If we want define budget in a very simple way, it is just the estimation of probable inflows and outflow in

the form of revenue and expenses. The main purpose of budgeting is to know the tentative cost prior and

take corrective action after the actual situation is incurred. It helps the assessment of management

performance. Some important purposes of budget are as follows:

a) Identify the sources of revenue and inflows.

b) Identify the uses and outflows of resources.

c) To run the business properly with effectiveness and efficiency.

d) To

e) To identify the sources and uses that required more attention.

f) To identify those activities that are not contributing to the business to a desired level

and take corrective actions

g) To eliminate unwanted expenses.

h) To compare what is achieved with what is desired to evaluate performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

i) To set organization goals and targets.

j) To perform the activities in a timely manner.

k) To reduce cost without compromising the quality and earning a higher profit margin.

l) To assess the clients/ customers, suppliers, lender, investors, borrower and statutory

levies.

3.1.2: Nature of the Budgeting Process:

Preparation of a budget always depends on the target and goals of an organization. It is always based on

the past performance of the business. Specific increments or decrement are assumed and some fixed ratios

are used to reach the budgeted amount based on the past performance. For example, if the companies

target is to maintain an Asset turnover ratio at 2 and its current level of asset is 2 million, then its

budgeted sales will b e 4 million( Asset*Asset Turnover ratio). Therefore, making a budget is a simple

process. But precaution should be taken to avoid overambitious expectation in making budget and

probable future business environment should also be taken into consideration.

3.2: Appropriate Budgeting Methods and Their needs in the Organization:

There are different types of budgeting methods that an organization can use based on its goals,

objectives, targets and nature of business. Different organization may require different budgeting methods

as their activities are different. Even in a very single organization, different budgeting may be used based

on the needs of management. Here we describe some commonly used budget methods and their needs in

the organization.

3.2.1 Incremental Budgeting:

Incremental budgets are made solely based on the current period budgets where some additions are made.

These additions are made based on the expectation regarding the inflation or increase in sales. So,

incremental budget also considers the macro-economic features also.

3.2.2 Zero Based Budgets:

Zero based budgeting eliminates the problems of incremental budgeting. IT starts with a zero base. To

clarify more, there remains no balance from the previous year and all the earning are expensed with

remaining zero balance.

3.2.3 Top- down Budgeting:

This type of budgeting gives more attention to the higher level tasks. Lower level tasks get relatively poor

attention. At first the budget for the higher level task is produced and after that the lower level task’s

budget is prepared. This is also called imposed budgeting.

3.2.4 Bottom-up Budgeting:

This is an opposite method of top-down budgeting methods. It at first prepares the budget for the

activities required for the implementation of a planning. As it focuses more on the fictional level of the

activities, it is more goal achievement oriented in nature.

j) To perform the activities in a timely manner.

k) To reduce cost without compromising the quality and earning a higher profit margin.

l) To assess the clients/ customers, suppliers, lender, investors, borrower and statutory

levies.

3.1.2: Nature of the Budgeting Process:

Preparation of a budget always depends on the target and goals of an organization. It is always based on

the past performance of the business. Specific increments or decrement are assumed and some fixed ratios

are used to reach the budgeted amount based on the past performance. For example, if the companies

target is to maintain an Asset turnover ratio at 2 and its current level of asset is 2 million, then its

budgeted sales will b e 4 million( Asset*Asset Turnover ratio). Therefore, making a budget is a simple

process. But precaution should be taken to avoid overambitious expectation in making budget and

probable future business environment should also be taken into consideration.

3.2: Appropriate Budgeting Methods and Their needs in the Organization:

There are different types of budgeting methods that an organization can use based on its goals,

objectives, targets and nature of business. Different organization may require different budgeting methods

as their activities are different. Even in a very single organization, different budgeting may be used based

on the needs of management. Here we describe some commonly used budget methods and their needs in

the organization.

3.2.1 Incremental Budgeting:

Incremental budgets are made solely based on the current period budgets where some additions are made.

These additions are made based on the expectation regarding the inflation or increase in sales. So,

incremental budget also considers the macro-economic features also.

3.2.2 Zero Based Budgets:

Zero based budgeting eliminates the problems of incremental budgeting. IT starts with a zero base. To

clarify more, there remains no balance from the previous year and all the earning are expensed with

remaining zero balance.

3.2.3 Top- down Budgeting:

This type of budgeting gives more attention to the higher level tasks. Lower level tasks get relatively poor

attention. At first the budget for the higher level task is produced and after that the lower level task’s

budget is prepared. This is also called imposed budgeting.

3.2.4 Bottom-up Budgeting:

This is an opposite method of top-down budgeting methods. It at first prepares the budget for the

activities required for the implementation of a planning. As it focuses more on the fictional level of the

activities, it is more goal achievement oriented in nature.

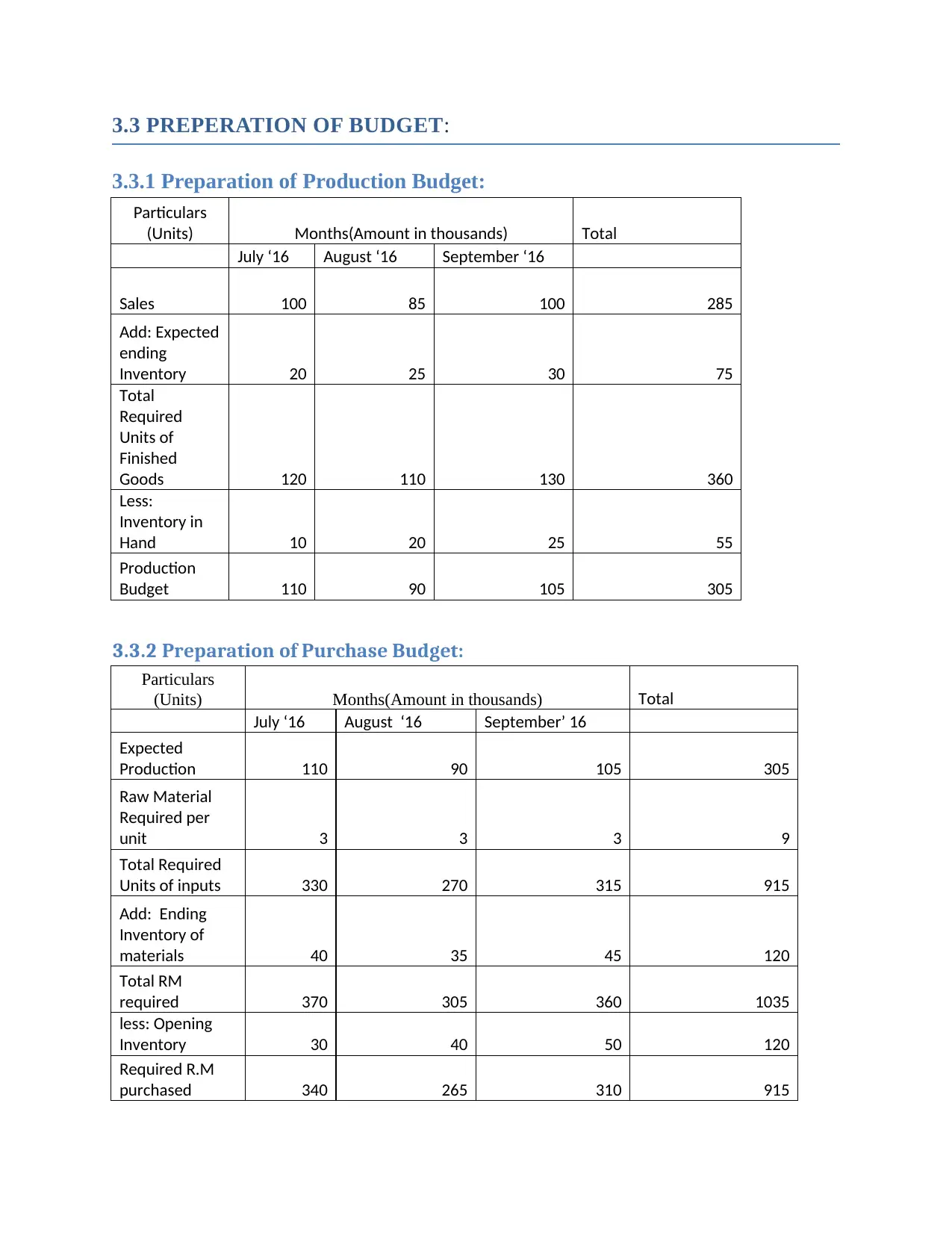

3.3 PREPERATION OF BUDGET:

3.3.1 Preparation of Production Budget:

Particulars

(Units) Months(Amount in thousands) Total

July ‘16 August ‘16 September ‘16

Sales 100 85 100 285

Add: Expected

ending

Inventory 20 25 30 75

Total

Required

Units of

Finished

Goods 120 110 130 360

Less:

Inventory in

Hand 10 20 25 55

Production

Budget 110 90 105 305

3.3.2 Preparation of Purchase Budget:

Particulars

(Units) Months(Amount in thousands) Total

July ‘16 August ‘16 September’ 16

Expected

Production 110 90 105 305

Raw Material

Required per

unit 3 3 3 9

Total Required

Units of inputs 330 270 315 915

Add: Ending

Inventory of

materials 40 35 45 120

Total RM

required 370 305 360 1035

less: Opening

Inventory 30 40 50 120

Required R.M

purchased 340 265 310 915

3.3.1 Preparation of Production Budget:

Particulars

(Units) Months(Amount in thousands) Total

July ‘16 August ‘16 September ‘16

Sales 100 85 100 285

Add: Expected

ending

Inventory 20 25 30 75

Total

Required

Units of

Finished

Goods 120 110 130 360

Less:

Inventory in

Hand 10 20 25 55

Production

Budget 110 90 105 305

3.3.2 Preparation of Purchase Budget:

Particulars

(Units) Months(Amount in thousands) Total

July ‘16 August ‘16 September’ 16

Expected

Production 110 90 105 305

Raw Material

Required per

unit 3 3 3 9

Total Required

Units of inputs 330 270 315 915

Add: Ending

Inventory of

materials 40 35 45 120

Total RM

required 370 305 360 1035

less: Opening

Inventory 30 40 50 120

Required R.M

purchased 340 265 310 915

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.