Radisson Blu Hotel: Cost Management, Break-Even and Target Profit

VerifiedAdded on 2023/06/07

|8

|1726

|153

Report

AI Summary

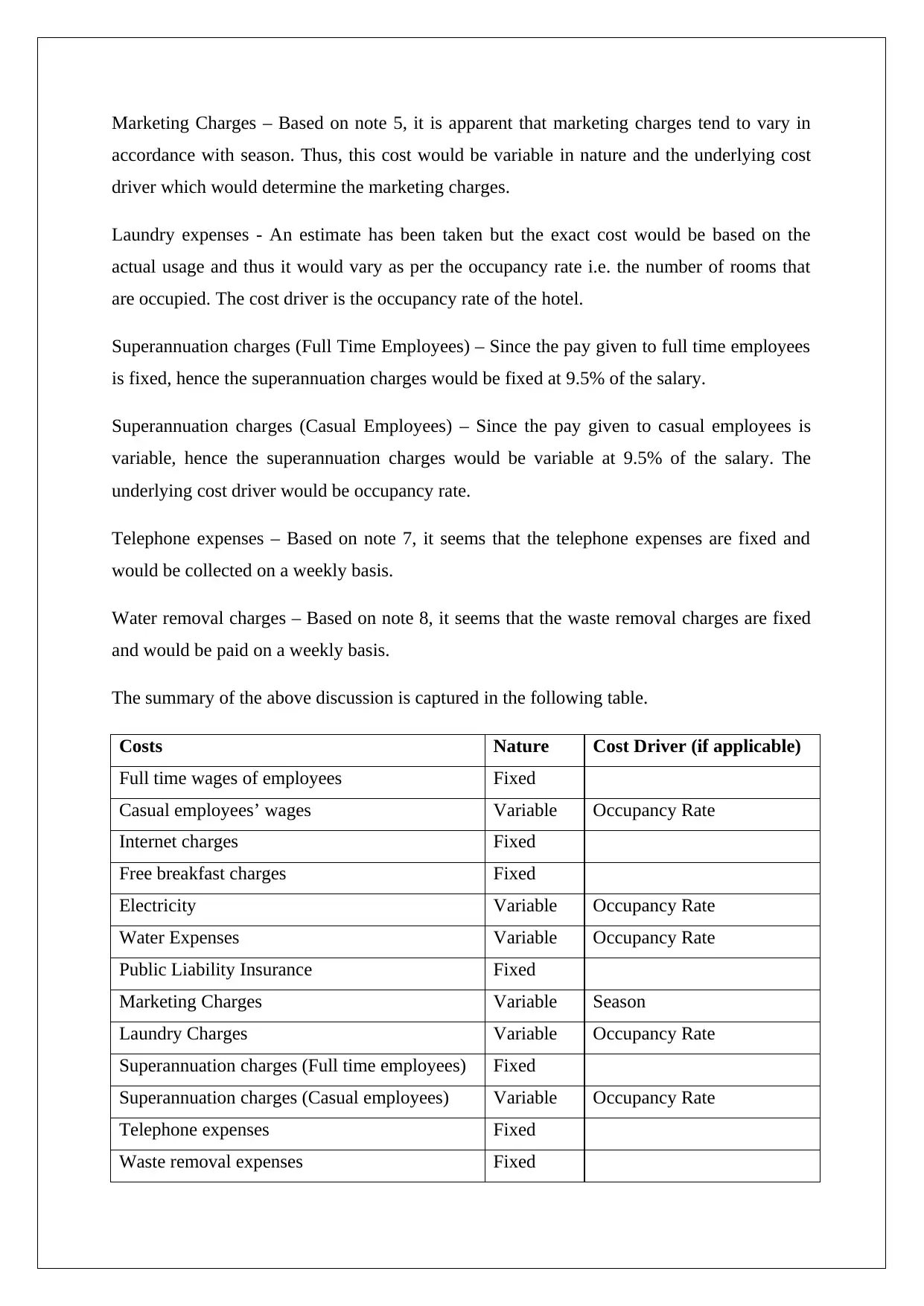

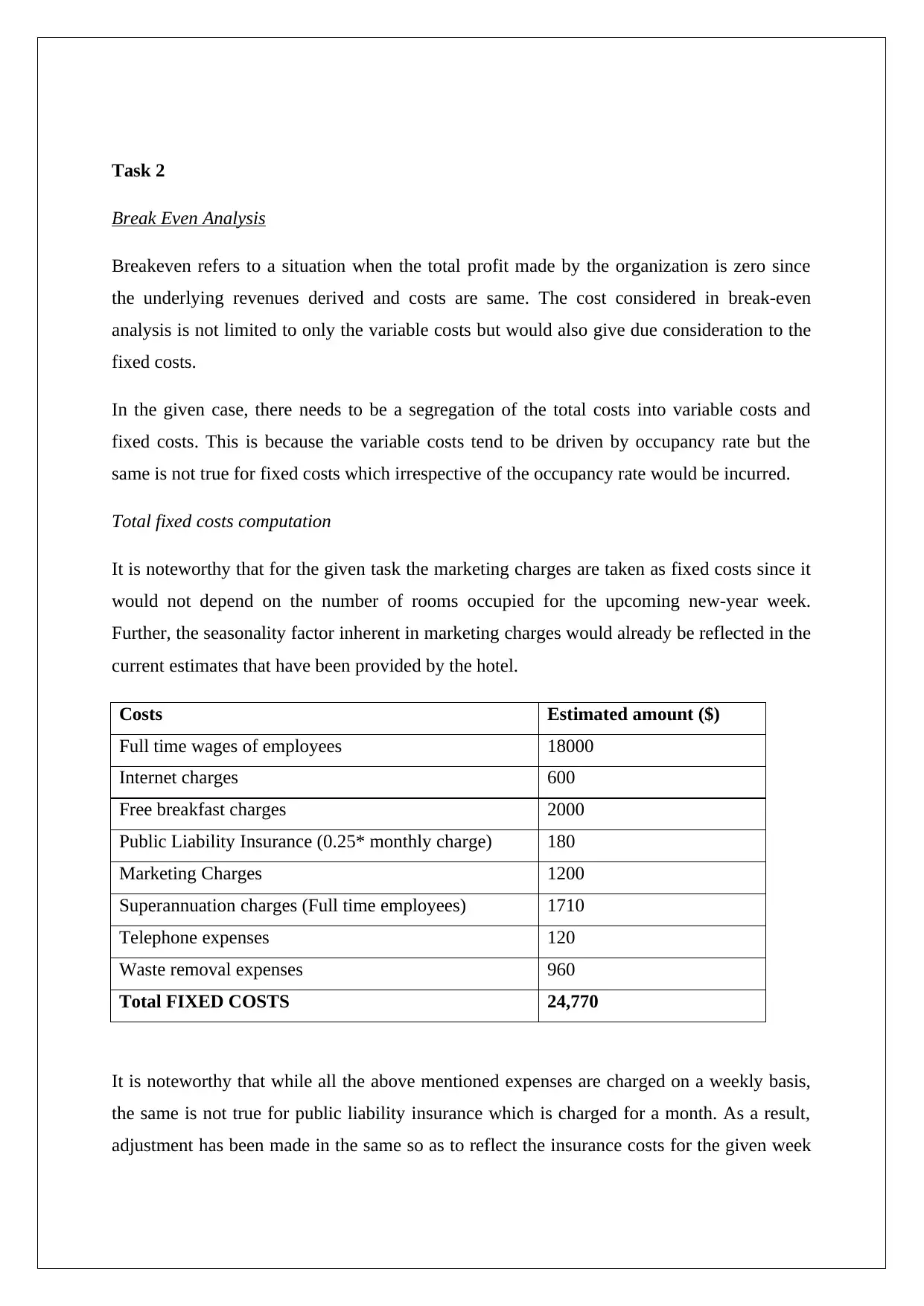

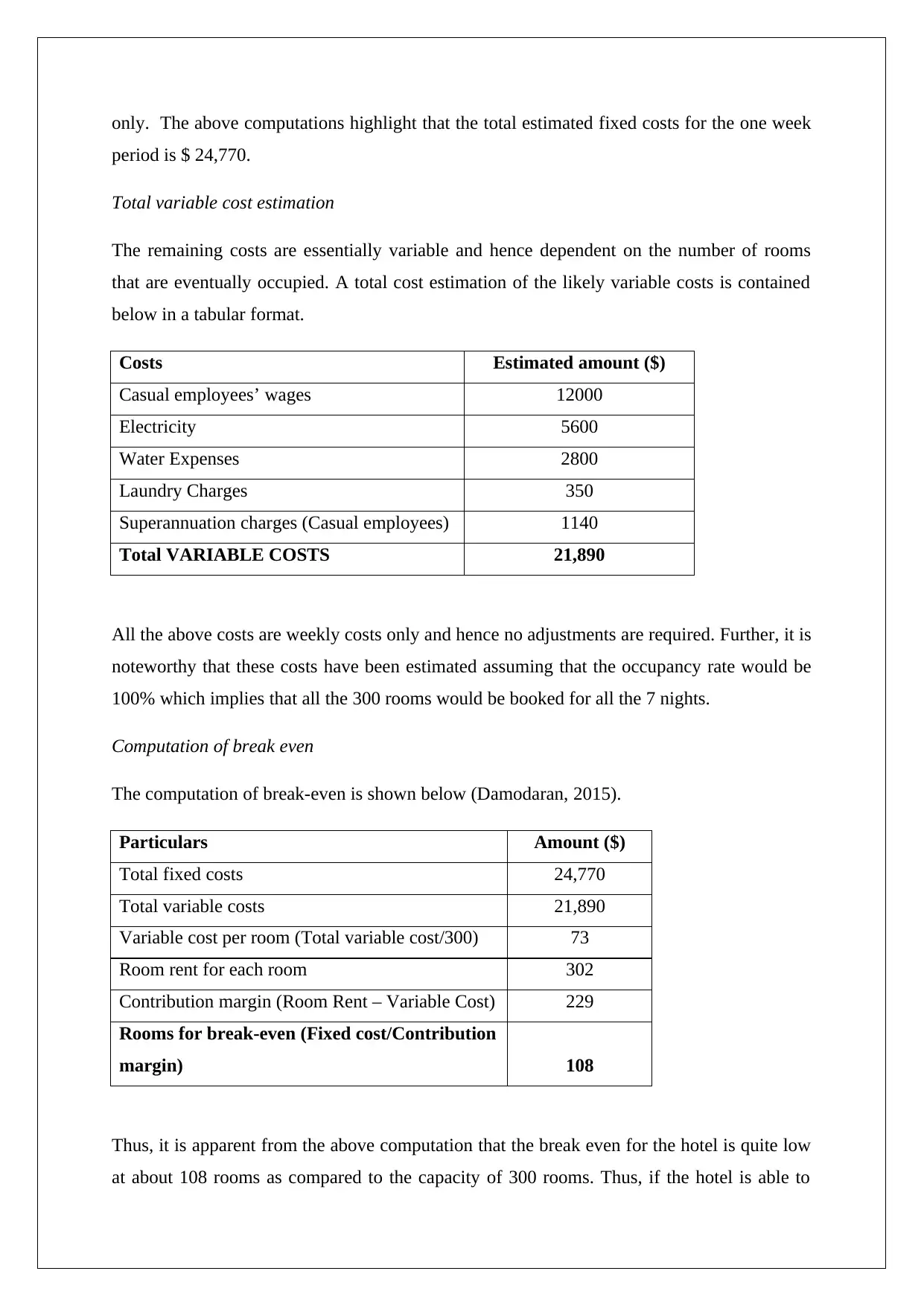

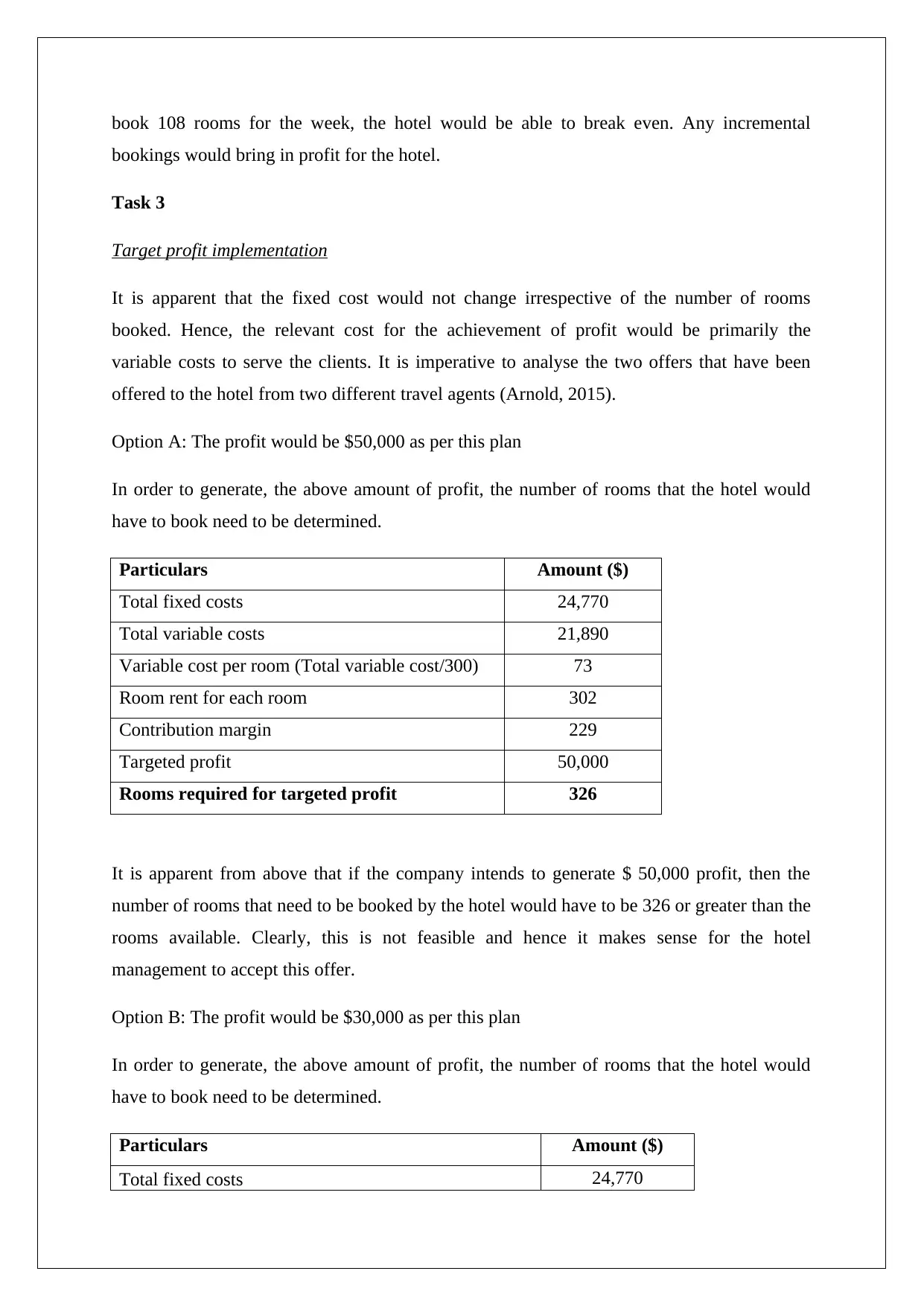

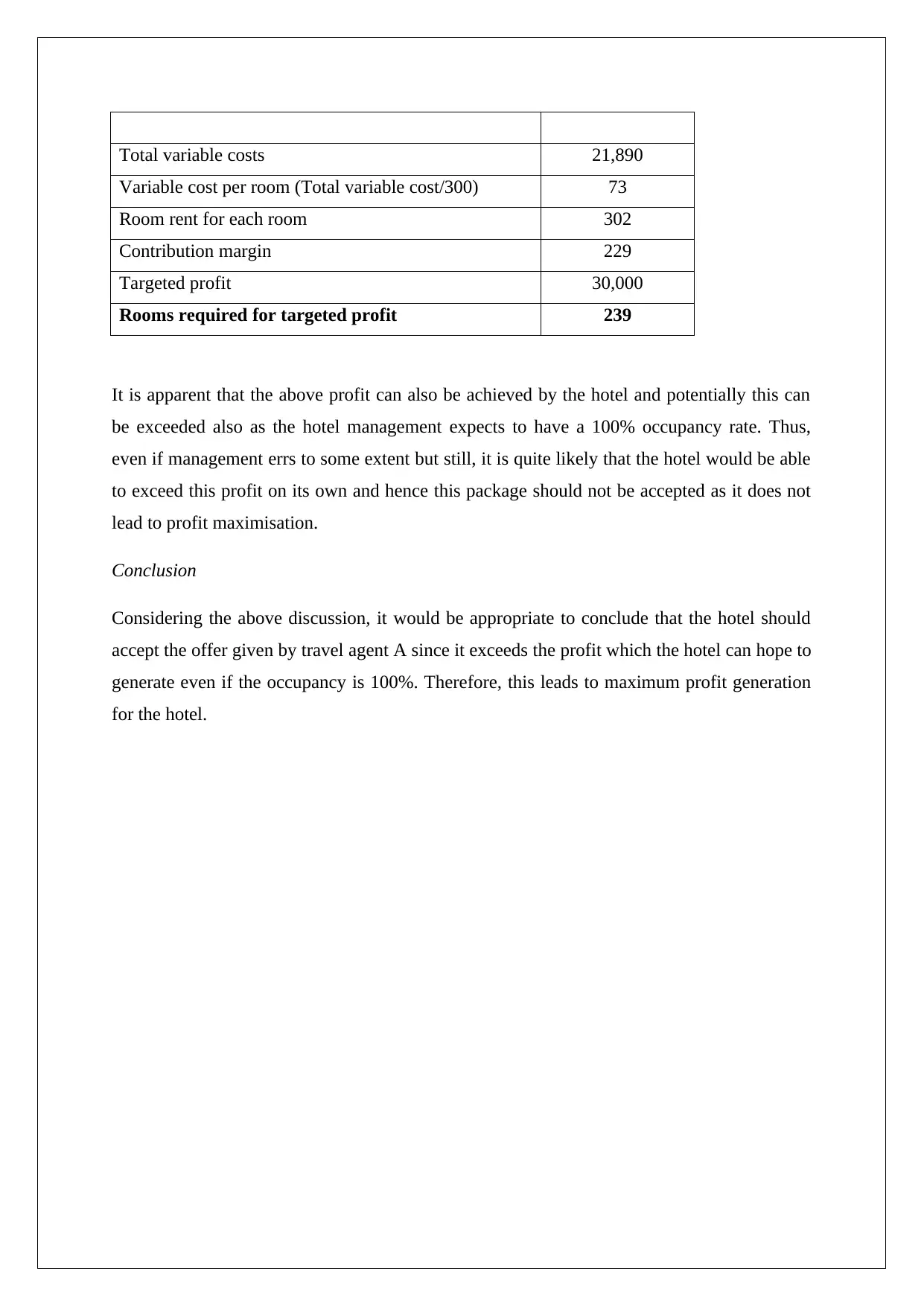

This report provides a comprehensive cost management analysis for Radisson Blu, focusing on cost drivers, cost behavior, and break-even analysis. It categorizes various costs, such as full-time wages, casual employee wages, internet charges, and electricity, as either fixed or variable, identifying occupancy rate and season as key cost drivers. The break-even analysis calculates that the hotel needs to book 108 rooms to cover its costs, considering fixed costs of $24,770 and variable costs of $21,890. Furthermore, the report evaluates two profit-generating options from travel agents, determining that accepting the offer from travel agent A, with a targeted profit of $50,000, is the more financially sound decision due to its potential for maximizing profits, even though it exceeds the hotel's capacity, whereas the second offer is not recommended as it will not lead to profit maximization. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.